Market Overview

| Study Period | 2020 - 2031 |

|---|---|

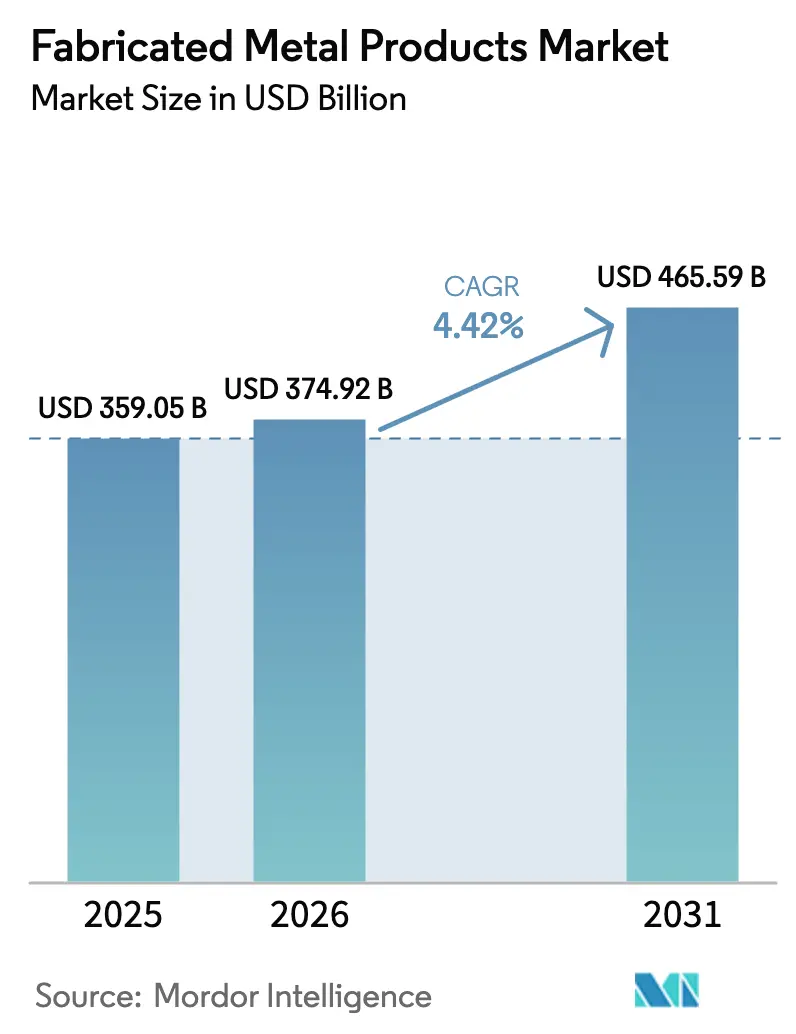

| Market Size (2026) | USD 374.92 Billion |

| Market Size (2031) | USD 465.59 Billion |

| Growth Rate (2026 - 2031) | 4.42% CAGR |

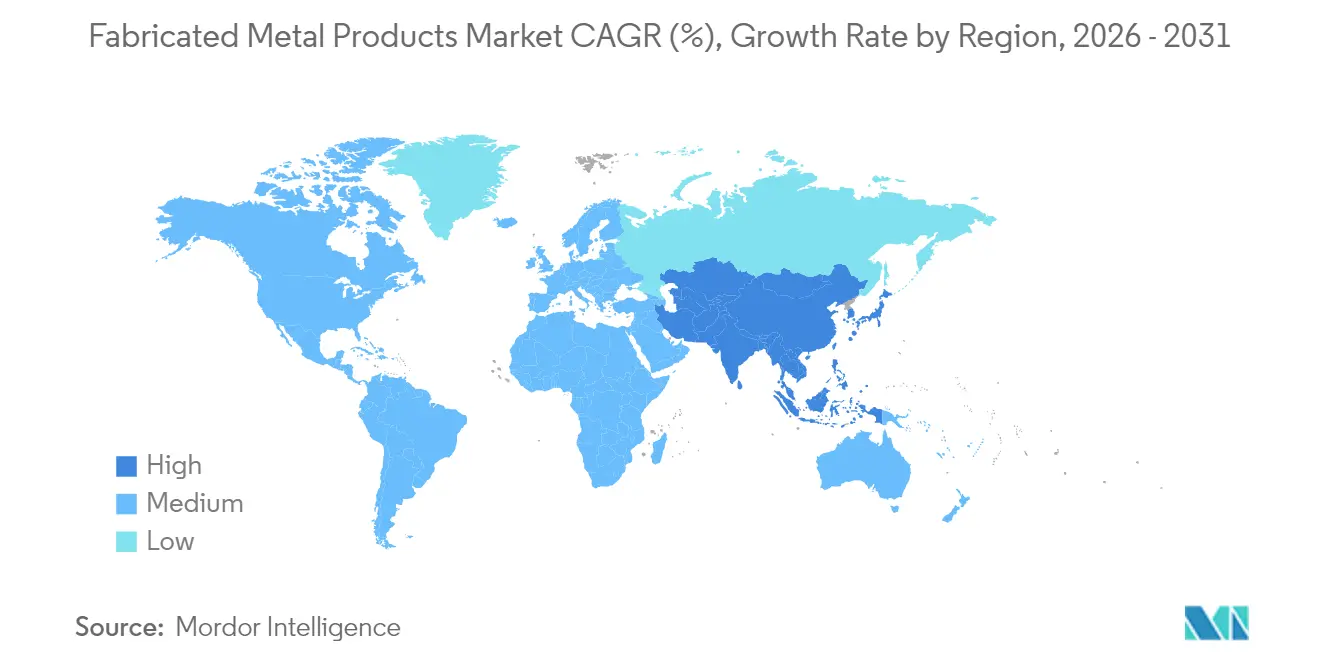

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fabricated Metal Products Market Analysis by Mordor Intelligence

The Fabricated Metal Products Market size was valued at USD 359.05 billion in 2025 and estimated to grow from USD 374.92 billion in 2026 to reach USD 465.59 billion by 2031, at a CAGR of 4.42% during the forecast period (2026-2031). Reshoring of manufacturing to high-cost economies, incentives tied to the U.S. Inflation Reduction Act, and China’s ultra-high-voltage grid build-out are the principal forces sustaining this expansion. Corporate buyers are prioritizing lead-time certainty over pure labor arbitrage, which redirects capital expenditure toward domestic or near-shore fabrication capacity. Lightweighting trends in transportation, paired with an intensified pipeline of renewable-energy projects, are widening the application base for precision-engineered components, allowing the fabricated metal products market to monetize value-added design, machining, and finishing expertise. Competitive behavior remains shaped by a mix of regional customer-proximity requirements and step-change technology investments in automation, digital twins, and additive manufacturing, all of which elevate the productivity ceiling and compress delivery cycles for custom parts.

Key Report Takeaways

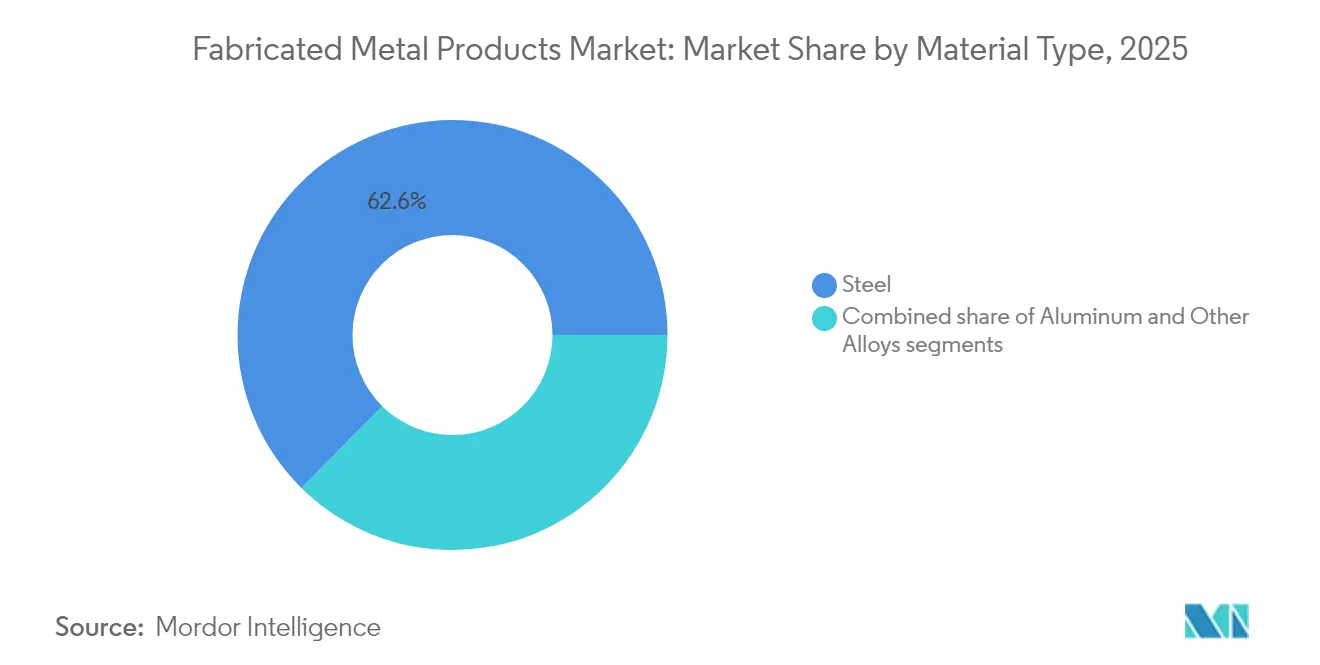

- By material type, steel dominated with 62.60% of fabricated metal products market share in 2025, whereas aluminum is projected to expand at a 5.66% CAGR through 2031.

- By fabrication process, machining commanded a 41.85% share of the fabricated metal products market size in 2025, while additive manufacturing and stamping are advancing at a 6.62% CAGR to 2031.

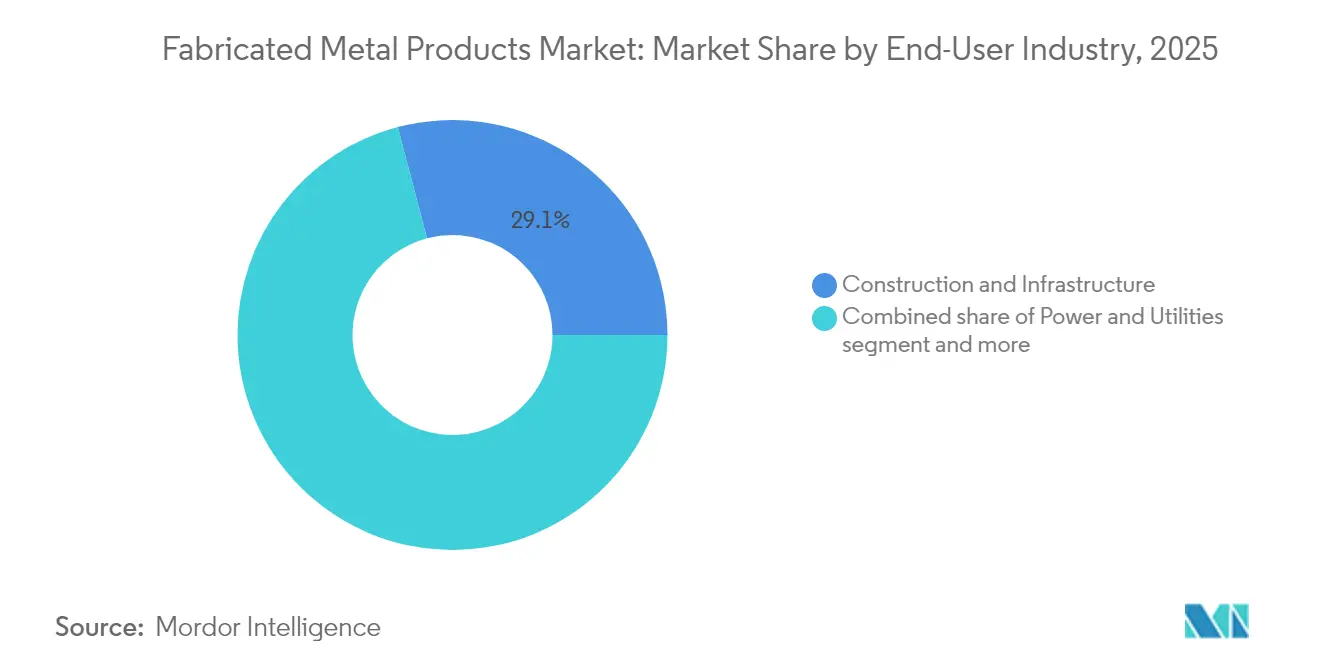

- By end-user industry, construction and infrastructure led with 29.10% revenue share in 2025; the power and utilities segment is forecast to grow at 6.12% CAGR through 2031.

- By geography, Asia-Pacific captured 48.35% of the fabricated metal products market share in 2025 and is poised to post the fastest 4.71% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fabricated Metal Products Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in demand from construction sector for structural components | +1.2% | Global, with strongest impact in Asia-Pacific and North America | Medium term (2-4 years) |

| Growth in renewable-energy installations requiring fabricated metal parts | +0.9% | Global, concentrated in APAC, North America, Europe | Long term (≥ 4 years) |

| Resurgence of manufacturing activity & reshoring initiatives | +0.8% | North America & EU, spillover to Mexico | Short term (≤ 2 years) |

| Technological advances in CNC & additive manufacturing | +0.6% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Adoption of digital twins enabling design-to-fab integration in SMEs | +0.4% | North America & EU, gradual APAC adoption | Long term (≥ 4 years) |

| Rising use of modular prefabricated data-center skids | +0.3% | Global, concentrated in North America and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Demand from the Construction Sector for Structural Components

Precision-engineered structural steel, architectural metalwork, and modular building elements keep the construction sector the single largest off-take channel for the fabricated metal products market. Infrastructure stimulus in the United States, India, and Indonesia is synchronizing with urbanization in Southeast Asia, lifting order backlogs for beams, trusses, and cold-formed sections. Contractors are shortening project cycles, prompting higher reliance on prefabricated assemblies that arrive ready for bolt-up, thereby raising fabrication complexity and margins. Strict seismic and energy-efficiency codes mandate tighter tolerances and certified weld procedures, which play to the strengths of technologically sophisticated shops able to validate quality with non-destructive testing. Although construction spending can be cyclical, demographic pressures for housing and transport renewal underpin a multi-year demand runway that offsets intermittent slowdowns.

Growth in Renewable-Energy Installations Requiring Fabricated Metal Parts

Wind, solar, and grid-reinforcement projects accelerate the need for precision tower sections, racking systems, and copper-intensive electrical hardware. The International Energy Agency expects solar additions to top 60% of new global renewable capacity in 2025, and each megawatt of photovoltaic capacity anchors roughly 5.5 tons of copper conductors. China’s State Grid tender for 1.757 million tons of steel lattice towers in 2025 dwarfs the previous year’s 460,000 tons, translating into continuous throughput for heavy-section beam and angle-line fabrication shops. Offshore wind construction depends on XL monopiles and nacelle housings that must absorb extreme dynamic loads, rewarding fabricators proficient at multi-pass submerged-arc welding. Battery-energy-storage sites further widen the scope, calling for thermally managed enclosures built from aluminum sheet and stainless structural members[1]Fatih Birol, “Renewables 2025: Analysis and Forecast to 2030,” International Energy Agency, iea.org.

Resurgence of Manufacturing Activity & Reshoring Initiatives

Reshoring is structurally lifting domestic order books as original-equipment manufacturers calculate the total cost of ownership, inclusive of logistics risk, tariff exposure, and working capital tied up in maritime transit. Between 2010 and 2023, 1.898 million cumulative jobs were announced for U.S. returns, accompanied by USD 234 billion annual manufacturing construction outlays as of May 2024. Equipment-heavy projects, such as Sumitomo Drive Technologies’ USD 22 million robotic welding line, showcase how automation neutralizes local wage differentials while trimming lead times. Federal legislation like the CHIPS and Science Act offers tax credits on capital goods, catalyzing incremental demand for fabricated semiconductor-tool frames, clean-room enclosures, and utility skids. Spillover effects reach Mexican border states, where maquiladoras absorb logistics-sensitive sub-assemblies for next-day delivery to U.S. integrators[2]Robert Ivie, “Value of Construction Put in Place: Manufacturing,” U.S. Census Bureau, census.gov.

Technological Advances in CNC & Additive Manufacturing

Advances in conversational CNC controls, tool-path automation, and real-time spindle monitoring are compressing setup times and reducing scrap, thereby improving capacity utilization. Plasma gas atomization now produces titanium powders at up to 1,500 kg/h, cutting additive raw-material costs and clearing a path for aerospace-grade 3D-printed brackets and manifolds. Alloy Enterprises’ Stack Forging shortens prototype-to-production cycles to four weeks for aluminum heat-sinks, illuminating how new build-process paradigms democratize complex geometry creation. Metal printers integrated with in-situ inspection close the feedback loop, ensuring dimensional accuracy before parts leave the chamber. Mid-tier shops increasingly access these capabilities via service-bureau partnerships or equipment leasing, bypassing the high capital hurdle while testing market appetite for printed parts.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in steel & aluminum prices | -0.7% | Global, most severe in import-dependent regions | Short term (≤ 2 years) |

| Skilled-welder shortage amid retirement cliff | -0.6% | North America & EU, emerging in developed APAC | Long term (≥ 4 years) |

| High CAPEX for advanced fabrication equipment | -0.5% | Global, particularly challenging for SMEs | Medium term (2-4 years) |

| Scope-3 emissions reporting pressure on fabricators | -0.3% | EU and North America, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Steel & Aluminum Prices

Hot-rolled coil hovered in the USD 700s per ton through late 2024, propped up by Chinese stimulus yet capped by slack Western demand and bloated service-center inventories. The U.S. antidumping duty on aluminum extrusions from 14 jurisdictions removed 400,000 tons of imports, amplifying domestic price swings and squeezing job-shop margins. While larger fabricators employ futures hedges or cost-plus contracts to mute volatility, small and medium enterprises struggle to pass surcharges through, delaying acceptance of long-term purchase orders. Project owners, wary of budget overruns, sometimes postpone steel-intensive builds, producing uneven utilization rates across the fabricated metal products market. Digital procurement platforms and transparent indexation mechanisms ease, not erase, input uncertainty, leaving price gyrations as a persistent constraint.

Skilled-Welder Shortage Amid Retirement Cliff

Roughly 21.4% of the current welder workforce in the United States is at least 55 years old, and the American Welding Society foresees an annual shortage of 90,000 hands through 2027. Miller Fabrication Solutions revived its four-week internal academy in 2024, graduating 11 workers after a COVID-era pause, but aggregate throughput lags demographic attrition. Vocational pipelines cannot scale fast enough, fueling wage inflation as small shops sweeten benefit packages to keep headcount. Robotic welding cells, once the domain of Tier-1 automotive suppliers, have migrated to medium-volume structural shops; however, integration demands capital and programming expertise that many operators lack. The labor imbalance nudges the fabricated metal products market toward platform technologies that simplify teach-pendant tasks and enable a single technician to oversee multiple cobot stations[3]John Douglass, “Welder Shortage: 2025 Workforce Report,” American Welding Society, aws.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Lightweight Metals Re-shape the Mix

Steel held 62.60% of the fabricated metal products market share in 2025, underpinned by its low cost-to-strength ratio for automotive frames, I-beams, and heavy machinery housings. Yet aluminum revenues are climbing at a 5.66% CAGR, positioning the lighter metal as the quickest-expanding contributor to the fabricated metal products market size over the outlook. Demand stems from electric-vehicle chassis, aerospace fuselage panels, and photovoltaic racking, where weight savings translate into fuel economy or easier field installation. Plasma-based powder atomization lowered titanium input prices, opening turbine and medical-implant niches, while copper volumes surge alongside high-ampere renewable circuits. Environmental scorecards guide buyers toward stainless alloys boasting 95% recycled content and 1.52 kg CO2e per kg footprints, tightening the link between material choice and Scope-3 pledges.

Downstream, alloy substitution strategies respond to commodity price gyrations and seismic code revisions. Steel producers ramp electric-arc-furnace capacity to widen scrap recycling loops, whereas extruders court solar OEMs with corrosion-resistant 6000-series profiles. Separate from cost calculus, titanium’s biocompatibility and high specific strength unlock orthopedic implant and space-qualified applications that command premium margins. Copper’s conductive superiority keeps it indispensable for EV busbars and inverter heat-sinks despite price spikes, pushing fabricators to optimize yield through nesting algorithms and remelt partnerships. Life-cycle assessment tools embedded in digital twins let engineers simulate carbon intensity at the quotation stage, helping the fabricated metal products market transform sustainability compliance into a sales lever.

By Fabrication Process: Automation Elevates Legacy Techniques

Machining represented 41.85% of the fabricated metal products market size in 2025, buoyed by multi-axis CNC mills and lathes that hit micron-level tolerances for aerospace fixtures and semiconductor tooling. Additive manufacturing combined with progressive stamping, grouped under “Others,” is racing ahead at 6.62% CAGR, proving the agility of near-net-shape printing for intricate ducts and topology-optimized brackets. High-speed machining centers integrated with tool-condition monitoring slash cycle times and extend insert life, enabling a single operator to supervise multiple spindles. Servo presses in stamping lines fine-tune stroke profiles, lessening spring-back in advanced high-strength steel parts and cutting rework.

Casting and forging remain vital for heavy-section engine blocks and gear blanks, but cede prototype work to binder-jet and directed-energy-deposition platforms that iterate designs without tooling cost. Robotic welding bridges the skills gap by automating multi-pass joints, especially in subsea and pressure-vessel fabrication. Meanwhile, laser tube-cutting cells pair with bending robots to produce modular frame kits in one continuous flow, shrinking work-in-progress inventory. Consolidators such as Nano Dimension’s USD 115 million swoop on Markforged and subsequent Desktop Metal tie-up illustrate how capital marshaled through mergers acquires intellectual property, broadens powder portfolios, and cross-sells hybrid print-and-machine workflows.

By End-user Industry: Energy Transition Re-orders Priorities

Construction and infrastructure retained the heaviest weighting at 29.10% of the fabricated metal products market size in 2025 on the back of road, rail, and public-building programs. Yet the power and utilities domain is set to post a 6.12% CAGR, propelled by wind-tower flanges, solar trackers, and grid-stiffening hardware. High-temperature hydrogen pipelines, battery-energy-storage cabinets, and substation bus frameworks all lean on code-compliant welds and corrosion-resistant alloys. Manufacturing, automotive, and aerospace sustain baseline demand through capacity expansions; electric-vehicle platforms shift bill-of-materials toward aluminum extrusions and battery enclosures, tightening collaboration with multi-process job shops.

Oil and gas still commission wellhead skids, pressure vessels, and LNG modules, though long-term share inches downward under decarbonization agendas. Data-center developers procure prefab power-distribution skids and hot-aisle containment, rewarding fabricators versed in tight-tolerance stainless panel bending and powder-coating. Across segments, digitized order portals and real-time shop-floor dashboards let buyers track cut-list progress and material certifications, improving transparency and trust between OEMs and the fabricated metal products market.

Geography Analysis

Asia-Pacific’s 48.35% stake in the fabricated metal products market share during 2025 aligns with its role as both a manufacturing powerhouse and an infrastructure build-site. China’s 1.757 million tons UHV tower tender anchors mill output, while India’s Smart Cities Mission funds multi-modal terminals, metro rails, and flyovers that demand high tonnage of rolled and welded sections. Southeast Asian countries like Vietnam capture re-shored electronics assemblies, catalyzing demand for precision sheet-metal chassis, server racks, and heat-sinks. Japan and South Korea, though mature, feed exports of high-precision semiconductor equipment frames and robotic sub-assemblies, capitalizing on lean production systems that blend machining, grinding, and metrology under one roof. Intra-Asia trade corridors shorten transit loops, allowing mill-direct deliveries of coil and bar to regional fabricators, fortifying competitiveness within the fabricated metal products market.

North America’s outlook is reinforced by more than USD 2 trillion federal stimulus earmarked for clean energy, advanced chips, and transport corridors. U.S. manufacturing construction hit USD 234 billion annualized in May 2024, a 217% surge versus 2019, indicating multi-year backlogs for mezzanines, HVAC plenums, and structural frames. Canada’s Critical Minerals Strategy funnels capital into battery-materials processing plants, inflating orders for stainless reactors and alloy-steel conveyance systems. Mexico gains from near-shoring of white-goods assembly and Tier-2 automotive sub-assemblies, spurring investments in tube-laser lines and robotic MIG cells. Cross-border supply chains leverage USMCA duty-free rules while retaining geographic proximity that minimizes logistics risk for fabricated sub-components. Europe grapples with energy-price volatility yet compensates via high-value niches in offshore wind monopiles, hydrogen electrolyzers, and medical-device housings. Germany’s Mittelstand excels at thin-gauge stainless forming, whereas Italy pivots toward boutique machining for luxury automotive. The EU’s carbon-border adjustment mechanism privileges mills employing electric-arc furnaces and high scrap ratios, influencing procurement toward low-carbon steel. Nordic producers exploit hydropower to smelt greener aluminum billets destined for offshore solar-farm structures. Middle East and Africa ride public-works megaprojects, Riyadh Metro and Egypt’s New Administrative Capital, requiring bridge girders and architectural façades. South America’s mining conveyor upgrades and floating LNG hubs sustain demand for heavy-duty plate and tubular fabrications despite macro-volatility, underscoring the geographic breadth of the fabricated metal products market.

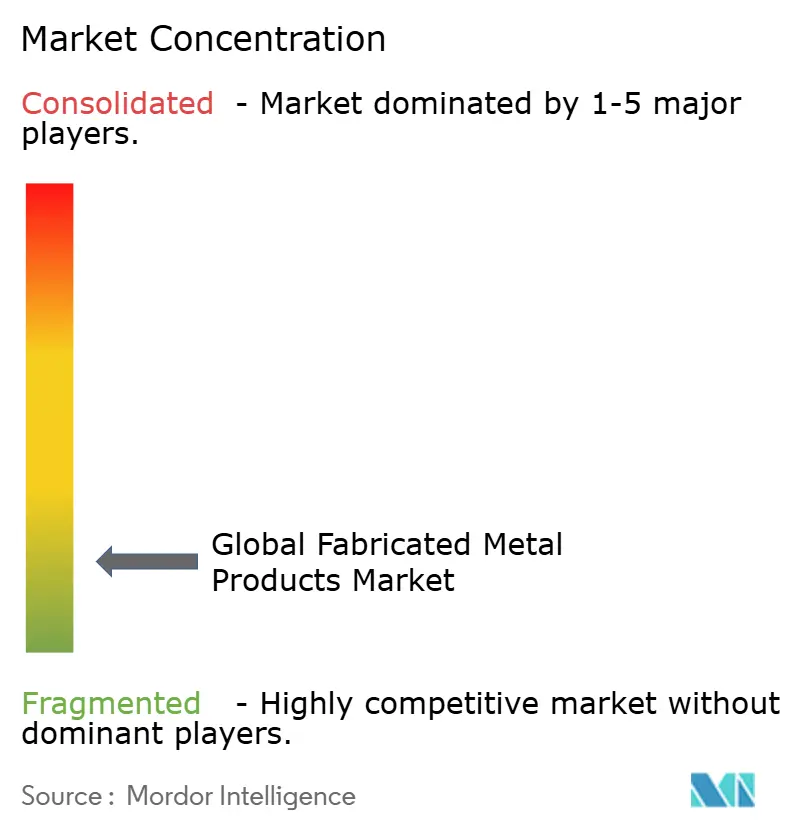

Competitive Landscape

The competitive fabric remains fragmented: thousands of regionally anchored specialists cater to proximity-sensitive customers, while a handful of roll-up platforms pursue scale through acquisition. Mayville Engineering Company topped The Fabricator’s 2024 leaderboard at USD 588.4 million revenue, but that figure equates to less than 0.2% of the worldwide fabricated metal products market size, illustrating how unconcentrated the arena is. Cadrex at USD 485 million and BTD at USD 360 million round out the top tier, yet neither has the geographic span to serve all global OEM footprints. Private-equity involvement is heating up: Arlington Capital Partners formed Keel Holdings by fusing Pegasus Steel, Metal Trades LLC, and Merrill Technologies Group into a nine-plant, 1 million sq ft defense-focused network. Deal rationales center on cross-selling, procurement leverage, and shared automation best practices.

Technology is a decisive wedge. Shops deploying industrial IoT for machine-health monitoring reduce downtime by up to 20% and feed predictive analytics that derisk tight-deadline contracts. Additive manufacturing capability bolsters bid competitiveness on low-volume, complex-geometry parts, scaring off rivals tied to hard-tooling economics. The U.S. Bureau of Industry and Security’s export-license framework for additive systems can hinder overseas competitors, effectively granting U.S. operators a home-market technology moat. Mid-cap acquirers also chase niche process know-how, explosion-welding of clad plate, friction-stir-welding of aluminum railcar bodies, or electropolishing of biomedical devices, to differentiate on quality rather than price. End-market specialization, from modular data-center skids to cryogenic fuel tanks, enables value-based rather than tonnage-based pricing within the fabricated metal products market.

Sustainability credentials are gaining weight in RFQ scoring. Fabricators integrating renewable electricity, high-recycled-content feedstock, and verifiable Scope-3 data satisfy OEM decarbonization roadmaps, potentially commanding preferred-supplier status. Equipment makers pitch energy-efficient laser cutters able to reduce kWh per linear foot cut by double-digit percentages, while powder-bed printers reclaim almost all unused metal, slashing material waste. Advancement in virtual weld simulation trims physical prototypes, saving cost and embodied carbon. Together, these shifts alter the basis of competition from purely capacity to a triad of agility, technology, and sustainability, reshaping the hierarchy inside the fabricated metal products market.

Fabricated Metal Products Industry Leaders

ArcelorMittal

Nucor Corporation

China Steel Corporation

Howmet Aerospace

Parker-Hannifin Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Olympic Steel opened a 105,000 sq ft Action Stainless facility in Houston, adding 73,000 sq ft to its local footprint and expanding specialty-metal fabrication throughput.

- January 2025: State Grid Corporation of China issued tenders for 1.757 million tons of steel towers for UHV projects, nearly quadrupling its 2024 buy volume.

- August 2024: Russel Metals acquired seven service centers from Samuel, Son & Co. across western Canada and the U.S. Northeast, reinforcing its distribution and fabrication platform.

- July 2024: Solar Atmospheres bought Certified Metal Craft, El Cajon, California, establishing its sixth U.S. site for heat-treating and brazing services.

Global Fabricated Metal Products Market Report Scope

The process of creating machinery and buildings out of raw metal resources is known as metal fabrication. To make the finished product, many processes including as cutting, burning, welding, machining, forming, and assembling are used. From hand railings to large machinery and equipment, metal fabrication tasks range widely. The manufacturing of hardware, spring and wire, screws, nuts, and bolts, as well as forging and stamping, are some examples of specific subsectors. Other subsectors include cutlery and hand tools, architectural and structural metals, and hardware manufacturing.

The Global Fabricated Metal Products market is segmented By Material Type (Steel, Aluminum, and Others), By End-User Industry (Manufacturing, Power and Utilities, Construction, Oil and Gas, and Other End-user Industries), and By Service (Casting, Forging, Machining, Welding & Tubing, and Other Services). The report offers market size and forecasts for the Fabricated Metal Products Market in value (USD Billion) for all the above segments. Furthermore, this report covers market insights, such as market dynamics, drivers, restraints, opportunities, technological innovation, its impact, and porter's five forces analysis. In addition, the report also provides company profiles to understand the competitive landscape of the market.

By Material Type

| Steel |

| Aluminum |

| Other Alloys (Titanium, Copper, etc.) |

By Fabrication Process

| Casting |

| Forging |

| Machining |

| Welding & Tubing |

| Others (Stamping, Additive Manufacturing) |

By End-user Industry

| Manufacturing |

| Power & Utilities |

| Construction & Infrastructure |

| Oil & Gas |

| Automotive |

| Aerospace & Defense |

| Other Industries |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Material Type | Steel | |

| Aluminum | ||

| Other Alloys (Titanium, Copper, etc.) | ||

| By Fabrication Process | Casting | |

| Forging | ||

| Machining | ||

| Welding & Tubing | ||

| Others (Stamping, Additive Manufacturing) | ||

| By End-user Industry | Manufacturing | |

| Power & Utilities | ||

| Construction & Infrastructure | ||

| Oil & Gas | ||

| Automotive | ||

| Aerospace & Defense | ||

| Other Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 value of the fabricated metal products market?

The fabricated metal products market size is USD 374.92 billion in 2026.

How fast is demand for aluminum fabrications expected to grow?

Aluminum components are forecast to post a 5.66% CAGR through 2031, the fastest among material segments.

Which region leads both in share and growth?

Asia-Pacific holds 48.35% of fabricated metal products market share in 2025 and is projected to advance at a 4.71% CAGR.

What role does renewable energy play in future demand?

Wind, solar, and grid-modernization investments add roughly 0.9 percentage points to overall CAGR by driving tower, racking, and conductor demand.

Page last updated on: