Metal Anodizing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.16 Billion |

| Market Size (2031) | USD 2.75 Billion |

| Growth Rate (2026 - 2031) | 4.95% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

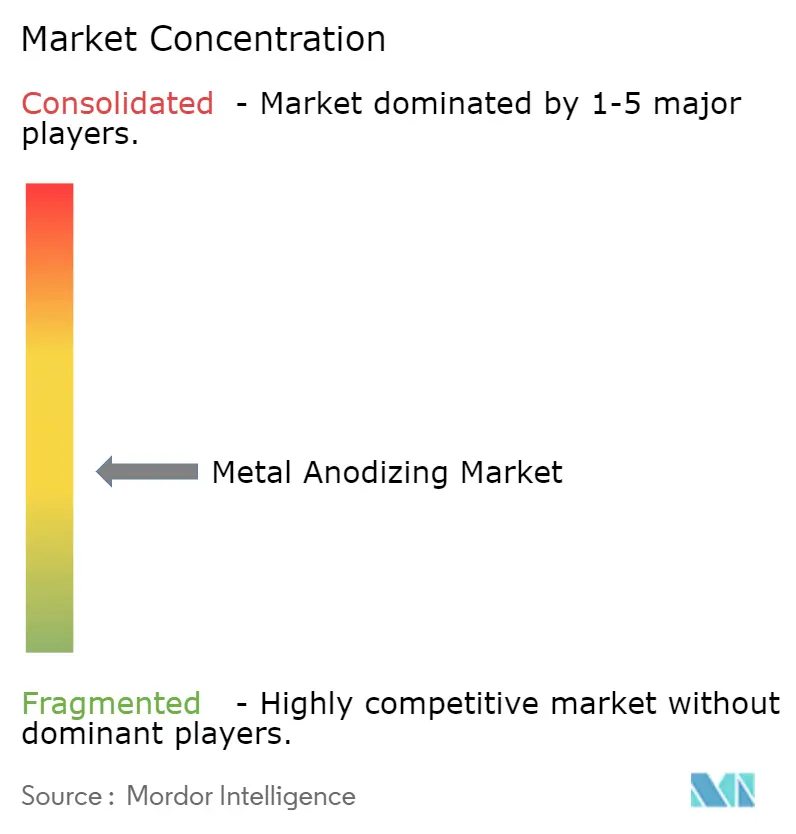

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metal Anodizing Market Analysis by Mordor Intelligence

The metal anodizing market size is expected to grow from USD 2.06 billion in 2025 to USD 2.16 billion in 2026 and is forecast to reach USD 2.75 billion by 2031 at 4.95% CAGR over 2026-2031. Demand gains stem from stricter rules that replace hexavalent chromium with safer chemistries, accelerating adoption in high-performance sectors such as electric vehicles, aerospace and data-center cooling. Weight reduction targets in battery packs, the heat-dissipation needs of 5G base stations, and the corrosion challenges of offshore wind turbines collectively sustain forward momentum. Rising biocompatibility standards for medical implants and the growing prevalence of modular edge-computing sites add further pull for specialized hard-coat treatments. Supply-side headwinds include PFAS withdrawal from surfactant blends, volatile aluminum billet premiums and European energy price spikes, yet market players benefit from process innovations that trim energy use by up to 40% and shorten line changeovers.

Key Report Takeaways

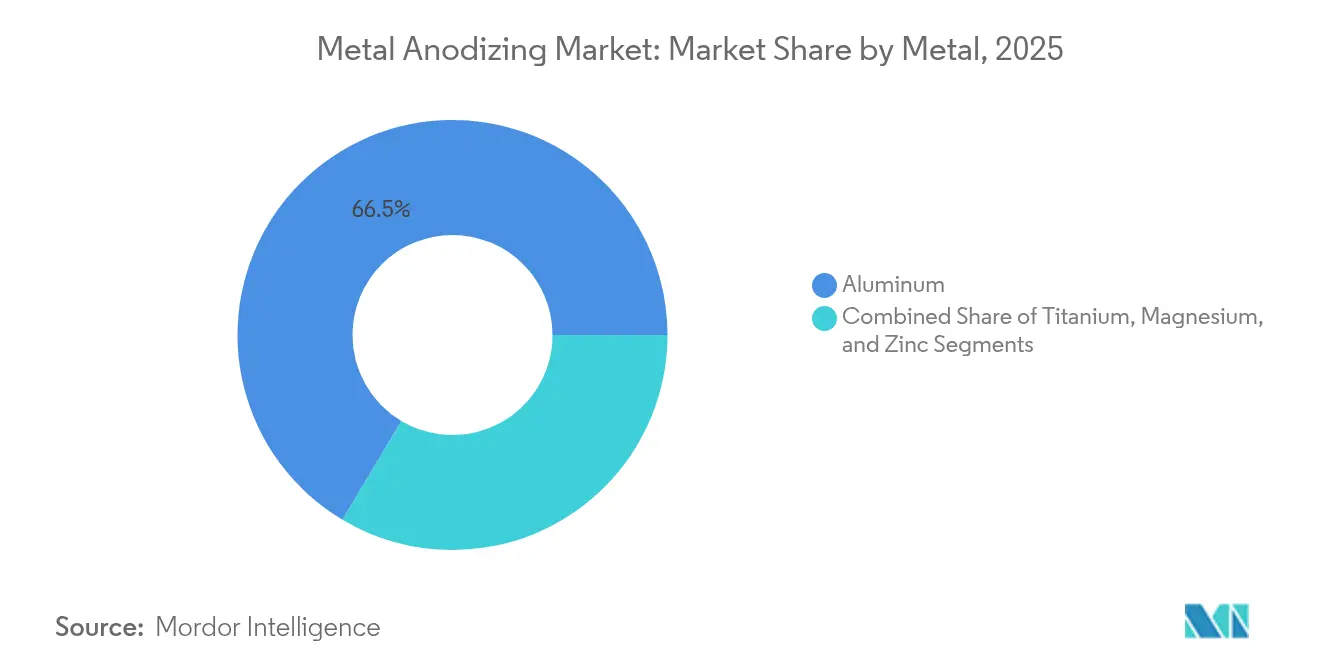

- By metal, aluminum held 66.45% of the metal anodizing market share in 2025; titanium is projected to advance at a 5.92% CAGR through 2031.

- By anodizing type, sulfuric acid processes accounted for 54.15% share of the metal anodizing market size in 2025; hard-coat variants are tracking a 6.05% CAGR during 2026-2031.

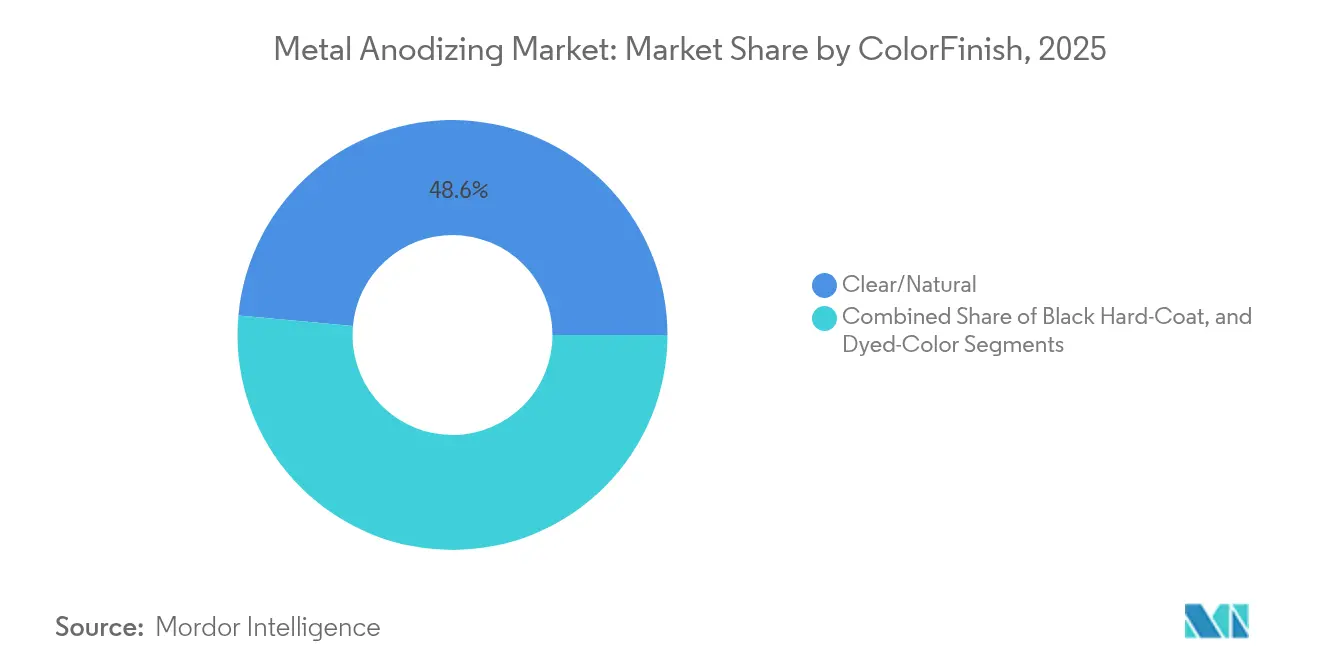

- By color/finish, clear (natural) coatings held 48.55% of revenue in 2025; black hard-coat finishes are forecast to expand at a 6.25% CAGR to 2031.

- By end-use industry, automotive led with 34.65% revenue share in 2025, while aerospace and defense records the fastest 6.72% CAGR through 2031.

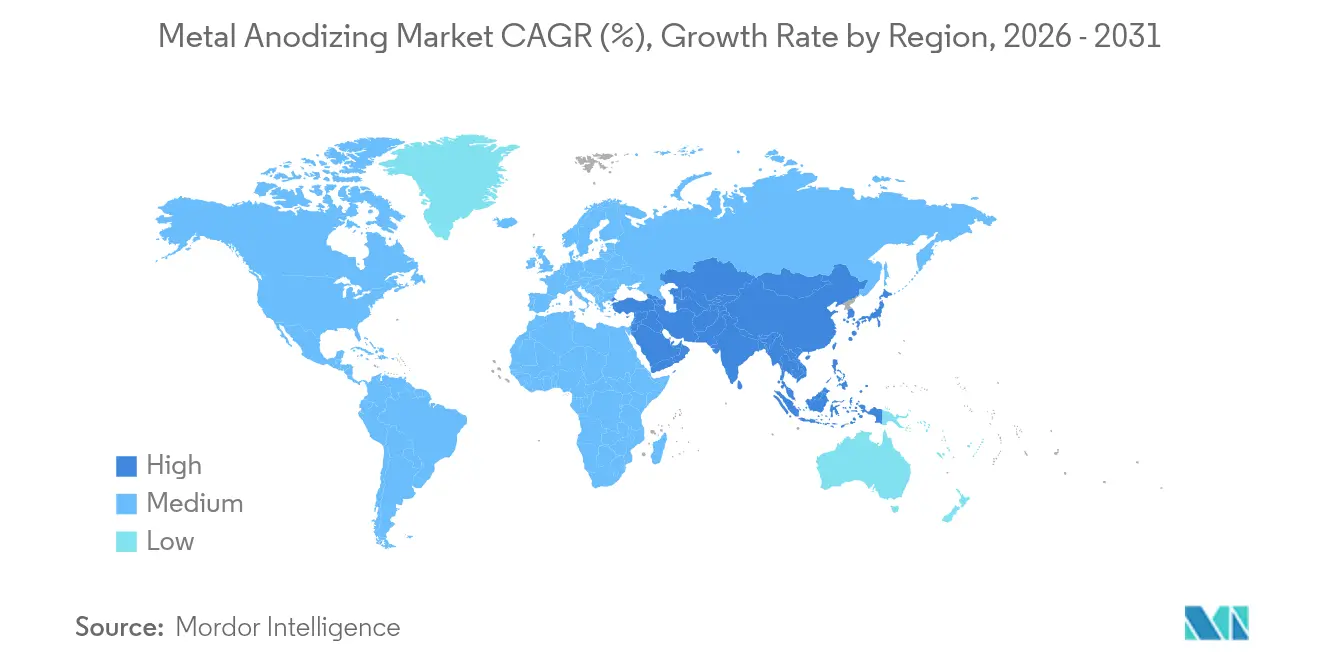

- By geography, Asia-Pacific commanded 47.05% of the metal anodizing market in 2025, whereas the Middle East and Africa is forecast to grow at a 5.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Metal Anodizing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV battery-pack lightweighting | +1.20% | Asia-Pacific, spill-over to North America | Medium term (2-4 years) |

| 5G heat-sink installations | +0.80% | Global, early gains in North America and EU | Short term (≤ 2 years) |

| Offshore wind turbine corrosion protection | +0.60% | Europe and North America coasts, expanding to APAC | Long term (≥ 4 years) |

| EU MDR-compliant titanium implants | +0.40% | Europe and North America | Medium term (2-4 years) |

| Chrome-plating substitution in US transport | +0.70% | North America, regulatory precedent worldwide | Long term (≥ 4 years) |

| Modular edge-data-center racks | +0.50% | Global, data-center hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EV battery-pack lightweighting driving Asia demand

Automakers incorporate anodized aluminum housings that cut battery-pack mass while maintaining heat dissipation, directly improving vehicle range. Honda’s USD 15 billion Canadian facility and BMW’s EUR 800 million expansion in Mexico exemplify capacity additions built around in-house anodizing that removes outsourcing delays.[1]Modern Metals, “Take it Higher,” modernmetals.com Southeast Asian lines now monitor current density in real time, lowering specific energy use by 40%.[2]Fraunhofer IPA, “Leichtmetalloberflächen für die Zukunft,” ipa.fraunhofer.de Process control ensures oxide growth suited to dry-electrode battery production, where solvent removal raises thermal stress on enclosures. Localized lines also shield producers from aluminum transport surcharges and cut lead times, cementing Asia-Pacific leadership.

5G heat-sink installations requiring high-conductivity anodized aluminum

Hard-coat anodized fins improve heat transfer coefficients and maintain dielectric isolation needed at millimeter-wave frequencies. Patented coaxial-flow exchangers for radio units specify anodized aluminum to withstand outdoor exposure.[3]Google Patents, “Electromagnetic Signal Transmission…,” patents.google.com Base-station makers adopt complex lattice geometries enabled by additive manufacturing, then seal pores to avoid corrosion creep.[4]MDPI Energies, “Recent Development of Heat Sink…,” mdpi.com As telecom operators densify small-cell grids, compact heat sinks become critical, pushing coating providers to guarantee uniform film thickness across intricate shapes. Edge-computing modules extend this requirement into enterprise campuses, broadening demand outside telecom operators.

Offshore wind turbine components seeking hard-coat corrosion protection

Marine conditions accelerate pitting, so turbine OEMs specify anodized aluminum internals and nacelle parts. Studies show pairing galvanic anodes with anodized surfaces can cut cathodic-protection costs by 70% while preserving structural life. Densified oxide layers endure salt spray and cyclic stress, while weight savings ease tower erection logistics. Environmental reviews report low acute toxicity from aluminum anodes though long-term accumulation remains under study. Growing round-three wind farms in the North Sea and accelerated permitting in the United States reinforce long-horizon demand.

Revised medical-device regulation in 2025 raises surface roughness and Ca/P ratio requirements. Anodizing forms calcium titanate layers that mimic bone chemistry and speed osseointegrationn. Pioneer Metal Finishing earned ISO 13485 status, underscoring the need for validated lines that withstand repeated sterilization cycles. Citrus-electrolyte processes reduce acid waste and enhance bioactivity, giving certified suppliers an edge in orthopedic tenders. Regulatory barriers deter new entrants, concentrating revenue among proven processors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PFAS phase-out in hard-anodizing baths | -0.90% | Global, early in North America and EU | Short term (≤ 2 years) |

| Aluminum billet premium volatility | -0.60% | Global, acute in Asia-Pacific | Short term (≤ 2 years) |

| PVD nano-ceramic coatings gaining share | -0.40% | North America and EU, expanding in APAC | Medium term (2-4 years) |

| EU electricity-price spike | -0.30% | Europe, ripple to energy-intensive hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

PFAS phase-out in surfactants for hard-anodizing baths

Mist-suppression agents based on PFOS were banned in 2015, yet residues appear in plating wastewater, prompting global regulators to tighten limits. Facilities scramble to validate fluorine-free surfactants that keep surface tension low without compromising coating quality. Some plants retrofit mechanical enclosures or fume scrubbers, raising capital outlays. Transition risk is highest for hard-coat lines that operate at elevated temperatures where splash is severe. Suppliers who qualify compliant chemistries early mitigate production downtime.

EU electricity-price spike inflating cooling costs

Anodizing is electricity-intensive; European spot power prices tripled in late 2024, lifting operating costs and pushing some capacity offshore. Process innovations such as pulse-modulated current and closed-loop chillers cut energy use by 40% but demand capex. Government green-equipment grants partially offset expenses, yet payback periods widen with market volatility. Manufacturers in Spain and Italy evaluate night-shift production to exploit cheaper tariff bands, balancing labor availability against energy savings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Metal: Aluminum Dominance Faces Titanium Disruption

Aluminum secured 66.45% of 2025 volume as its affordability, machinability and established process windows align with large-scale finishing lines. This dominance translates into the largest metal anodizing market revenue stream, with aerospace skins, automotive panels and electronics housings absorbing most capacity. The metal anodizing market size for aluminum components is set to expand steadily with EV platform rollouts that favor lightweight castings. Titanium, while holding a smaller base, accelerates at 5.92% CAGR riding regulatory demand for biocompatible orthopedic fixtures and space-constrained defense hardware that values high strength-to-weight ratios.

Titanium anodizing delivers porous oxide layers whose thickness controls color, creating non-pigmented identification coding for surgical tools. Early adopters in Europe have proven field performance, inspiring North American device approvals for spinal cages and dental abutments. Magnesium and zinc remain minority substrates, constrained by process complexity and cost. Innovations such as citrate-based electrolytes that tame pitting on magnesium show promise yet await scale-up. Zinc retains footholds in decorative hardware but competes with powder coatings. Advanced solid-state metallurgy may introduce high-strength aluminum alloys that demand modified anodizing recipes, opening fresh revenue lanes for specialists.

By Anodizing Type: Hard-Coat Gains on Sulfuric Acid Leadership

Sulfuric acid continues to headline with 54.15% share thanks to its versatility and low reagent cost. Thin-film variants replace legacy chromic acid on flight-critical aircraft parts in line with chromium bans, sustaining volume. Hard-coat treatments outpace overall growth at 6.05% CAGR, reflecting end-market shifts toward severe-duty wear zones in robotics, semiconductor carriers and energy-storage trays. The metal anodizing market size for hard-coat lines is forecast to widen as OEMs demand 25-100 µm layers that double service life in abrasive settings.

Boric-sulfuric and tartaric-sulfuric blends attract aerospace certifications by combining high fatigue life with compliance advantages. Phosphoric acid remains vital for adhesive-bonding prep in composite assemblies, while organic acid routes service color-critical consumer products. Chromic acid usage contracts toward zero beyond 2039 under US rules, driving retrofits. Across all chemistries, sealing research targets chromium-free formulations that retain low porosity and UV stability.

By Color/Finish: Black Hard-Coat Outpaces Clear Dominance

Clear anodizing still accounts for 48.55% of tonnage, safeguarding façade panels, rail interiors and general industrial parts where natural metal aesthetics matter. However black hard-coat finishes grow at 6.25% CAGR as electronics and data-center racks prioritize both heat emissivity and uniform visual branding. Dye impregnation coupled with zinc modification extends lightfastness, enabling outdoor telecom enclosures without fade. Bronze, gold and blue tints cater to architectural accents, while emerging antique-copper processes simulate patina without copper plating.

White anodized oxide, once niche, finds traction in e-mobility charging housings where glare control is critical. Sustainability concerns steer brands toward substrates containing 94% post-consumer recycled content such as trademarked evercycle, aligning finish choices with circular-economy messaging. Consistency across multi-plant networks pushes investment in automated dye make-up and on-line spectrophotometry.

By End-Use Industry: Aerospace Accelerates Past Automotive Leadership

Automotive commanded 34.65% revenue in 2025, anchored in trim, roof rails and battery enclosures. Growth moderates as global production plateaus, yet platform electrification sustains anodizing penetration in lightweight parts. The metal anodizing industry increasingly tailors oxide layers to meet battery thermal-runaway standards. Aerospace and defense, expanding at 6.72% CAGR, benefit from chrome-free mandates and fleet renewal programs that adopt aluminum-lithium and titanium alloys.

Electronics and semiconductor players specify hard-coat heat sinks compatible with high-power 5G radios. Construction outfits continue to select anodized curtain walls for durability and low maintenance. Medical devices remain a high-margin niche where validated ISO 13485 lines leverage proprietary oxide chemistries for implants that resist biofilm formation. Offshore energy and marine craft uptake grow as operators push for weight savings and longer service intervals in corrosive waters.

Geography Analysis

Asia-Pacific retained 47.05% of global demand in 2025 as China’s smelting and extrusion ecosystem feeds domestic and export-oriented finishing shops. Regional governments support in-line anodizing at EV gigafactories, slashing logistics time between battery pack machining and oxide growth. The metal anodizing market size in Asia-Pacific is projected to rise steadily through 2031 since localized capacity cushions billet volatility and energy costs. Tier-one Japanese and Korean electronics suppliers also qualify regional coating vendors, broadening end-market reach.

North America leverages chrome-substitution deadlines to expand domestic finishing capability. California’s rule spurs mid-western job shops to modernize lines with trivalent chemistry compatibility and automated emission controls. Aerospace hubs in Washington and Alabama contribute predictable throughput given strict airframe overhaul schedules. Data-center expansion across Virginia, Texas and Quebec fuels orders for black hard-coat racks, with customers demanding just-in-time shipments to narrow construction windows.

Europe faces power-price uncertainty yet benefits from stringent medical and environmental laws that favor high-value coatings. German and French facilities deploy energy-efficient pulse systems to offset tariffs, while Nordic operators exploit renewable electricity for low-carbon credentials. Offshore wind rollout in the North Sea anchors demand for marine-grade anodizing, often paired with galvanic protection to meet 25-year service life targets.

Middle East and Africa records the fastest 5.56% CAGR as Saudi and UAE industrial zones invest in downstream aluminum value chains. Offshore wind in Morocco and Egypt plus Red Sea desalination plants require corrosion-proof internals, tilting contracts toward hard-coat anodizers. South American growth remains tied to infrastructure stimulus and mining equipment orders, though macro volatility dampens capital flows. Overall, geographic diversification cushions global suppliers from single-region risk while creating specification complexity that rewards vertically integrated networks.

Competitive Landscape

The market remains moderately fragmented. Large multi-plant groups pursue vertical integration by adding chemistries, machining and assembly services to lock in customers. Pioneer Metal Finishing runs eight sites that deliver certified coatings to 3,500 account locations, illustrating a scale model that spreads quality systems cost. Recent M&A underscores consolidation momentum: Aalberts paid USD 105 million for Paulo Products to broaden heat-treatment reach in North America. Quaker Houghton committed USD 153 million for Dipsol Chemicals, securing cleaning and plating additives in Asia-Pacific portfolios.

Technology upgrades dominate capital budgets. Chicago Anodizing doubled capacity through a four-hoist line with automated dosing and recipe tracking, expanding dye options for OEM color libraries. Patent filings concentrate on dye-stabilization, eco-friendly electrolytes and process analytics. Justia lists inventions for zinc-incorporated dyes and antique copper effects, highlighting incremental yet valuable performance gains. Suppliers differentiate with ISO 13485 or AS9100 certifications that shorten customer audits.

New entrants attack niches. Precision Coating’s Registered MICRALOX process delivers pore-sealed layers that withstand 100 autoclave cycles, attracting reusable surgical instrument OEMs. Solid-state metallurgy start-ups promise alloy families needing customized anodizing, potentially reshaping substrate mixes by decade’s end. Despite innovation, switching costs and qualification hurdles reinforce incumbent positions, while regional environmental compliance pushes small shops to partner or sell.

Metal Anodizing Industry Leaders

Huber Engineered Materials

Pioneer Metal Finishing

K & L Anodizing Corporation

Advanced Plating Technologies

Anoplate Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Quaker Houghton agreed to acquire Dipsol Chemicals for USD 153 million to bolster Asia-Pacific presence.

- January 2025: Pioneer Metal Finishing was acquired by Aterian Investment Partners, strengthening North American footprint.

- January 2025: Integer Holdings bought Precision Coating, adding MICRALOX® medical-grade anodizing to its portfolio.

- January 2025: Chicago Anodizing completed a capacity-doubling retrofit, installing four-hoist automation and seven new dye tanks.

- December 2025: Aalberts announced the USD 105 million acquisition of Paulo Products, expanding heat-treatment services in the United States.

Global Metal Anodizing Market Report Scope

The metal anodizing market encompasses the process of electrolytic oxidation to enhance the surface properties of metals, primarily aluminum, by creating a durable and corrosion-resistant oxide layer. This technique is widely used in industries such as aerospace, automotive, electronics, and construction for improving material performance and aesthetics. The market is driven by the demand for lightweight, durable, and environmentally sustainable metal components.

The Metal Anodizing Market is segmented by metal (aluminum, titanium, magnesium and other metals), type (sulfuric acid anodizing, hard anodizing, chromic acid anodizing, and organic acid anodizing), end-use industry (automotive, aerospace, electronics, construction, marine, medical and others), and geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Aluminum |

| Titanium |

| Magnesium |

| Zinc |

| Sulfuric Acid Anodizing (Type II and IIB) |

| Hard-Coat Anodizing (Type III) |

| Chromic Acid Anodizing (Type I) |

| Organic/Boric-Sulfuric/Phosphoric Acid Anodizing |

| Clear/Natural |

| Black Hard-Coat |

| Dyed-Color (Broze, Gold, Blue, and More) |

| Automotive |

| Aerospace and Defense |

| Electronics and Semiconductors |

| Construction and Architecture |

| Marine and Offshore |

| Medical Devices and Implants |

| Consumer Goods and Appliances |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Metal | Aluminum | ||

| Titanium | |||

| Magnesium | |||

| Zinc | |||

| By Anodizing Type | Sulfuric Acid Anodizing (Type II and IIB) | ||

| Hard-Coat Anodizing (Type III) | |||

| Chromic Acid Anodizing (Type I) | |||

| Organic/Boric-Sulfuric/Phosphoric Acid Anodizing | |||

| By Color/Finish | Clear/Natural | ||

| Black Hard-Coat | |||

| Dyed-Color (Broze, Gold, Blue, and More) | |||

| By End-Use Industry | Automotive | ||

| Aerospace and Defense | |||

| Electronics and Semiconductors | |||

| Construction and Architecture | |||

| Marine and Offshore | |||

| Medical Devices and Implants | |||

| Consumer Goods and Appliances | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving growth in the metal anodizing market through 2031?

Weight reduction in electric vehicles, 5G thermal-management needs, offshore wind corrosion challenges and regulatory moves away from hexavalent chromium are the primary catalysts, collectively supporting a 4.95% CAGR.

Which region leads global demand?

Asia-Pacific accounts for 47.05% of 2025 volume due to its integrated aluminum supply chain and large-scale EV production capacity.

Why is titanium anodizing gaining attention?

EU medical-device rules require biocompatible surfaces, and anodized titanium offers calcium titanate layers that enhance osseointegration, driving a 5.92% CAGR in this segment.

How are PFAS regulations affecting anodizers?

Global phase-outs of PFAS mist suppressants force plants to validate fluorine-free chemistries and invest in mechanical emission controls, which can temporarily raise operating costs and slow throughput.

What advantages do hard-coat anodized finishes provide over conventional sulfuric acid films?

Hard-coat layers reach 25-100 µm thickness, delivering superior wear resistance and thermal conductivity, making them ideal for semiconductor, data-center and heavy-duty mechanical parts.

How is consolidation reshaping competition?

Strategic acquisitions such as Aalberts–Paulo and Quaker Houghton–Dipsol expand chemical portfolios and geographic reach, signaling a trend toward integrated service offerings and larger global footprints.

Page last updated on: