Asia-Pacific Semiconductor Materials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

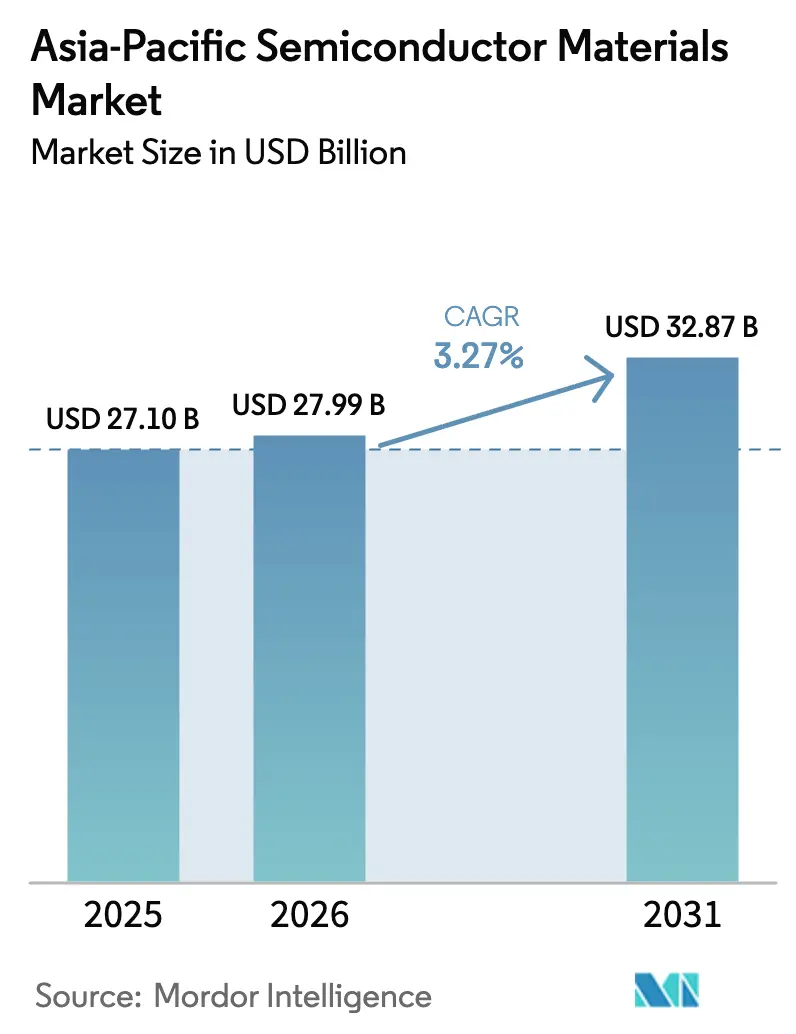

| Base Year Market Size (2025) | USD 27.10 Billion |

| Market Size (2026) | USD 27.99 Billion |

| Market Size (2031) | USD 32.87 Billion |

| Growth Rate (2026 - 2031) | 3.27% CAGR |

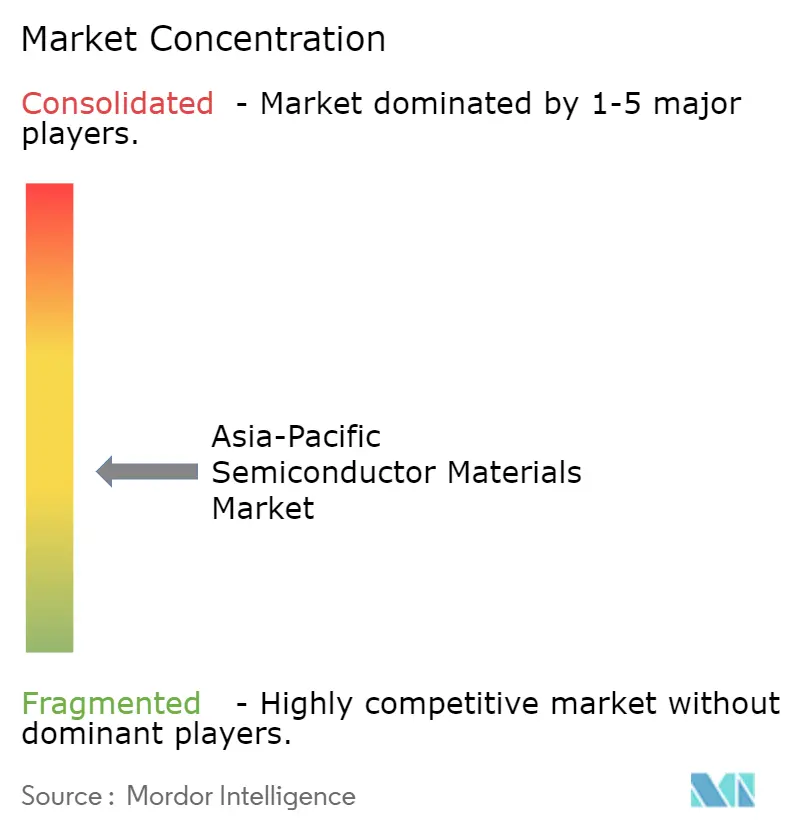

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Semiconductor Materials Market Analysis by Mordor Intelligence

The Asia-Pacific semiconductor materials market size is expected to grow from USD 27.10 billion in 2025 to USD 27.99 billion in 2026 and is forecast to reach USD 32.87 billion by 2031 at 3.27% CAGR over 2026-2031. Momentum comes from sovereign technology programs in China, Japan and Korea that prioritize local sourcing of specialty chemistries, while tighter design rules at sub-10 nm nodes are lifting per-wafer material content. Electric-vehicle electrification, mini/micro-LED investments and heterogeneous integration are enlarging demand for wide-bandgap substrates, advanced gases and novel under-fill compounds. At the same time, export-control compliance and water-scarcity mitigation are reshaping site-selection strategies, creating both risk and opportunity for regional suppliers. Competitive intensity is growing as new Chinese entrants target commodity segments, compelling incumbents to accelerate process innovation and expand local production footprints.

Key Report Takeaways

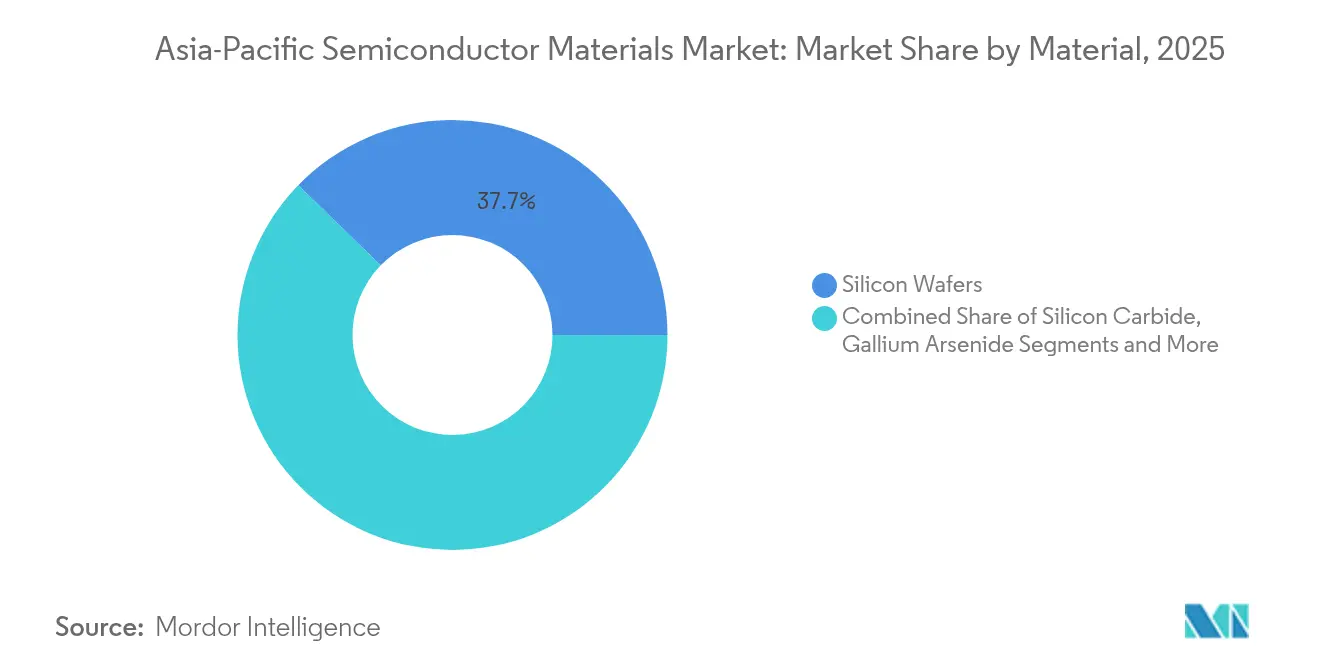

- By material, Silicon Wafers held the largest 37.74% share of the Asia-Pacific semiconductor materials market in 2025, while Silicon Carbide is forecast to grow fastest at 9.08% CAGR to 2031.

- By application, the Fabrication segment commanded 65.12% of the Asia-Pacific semiconductor materials market share in 2025; Advanced Packaging is expected to expand at a 6.84% CAGR to 2031.

- By end-user, Consumer Electronics accounted for 41.02% of the Asia-Pacific semiconductor materials market in 2025, but Automotive and Mobility is advancing at the highest 8.29% CAGR to 2031.

- By geography, Taiwan led with a 34.75% revenue share of the Asia-Pacific semiconductor materials market in 2025, whereas China is projected to post the quickest 3.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Semiconductor Materials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed chip sovereignty funds | +0.80% | China, Japan, Korea | Medium term (2-4 years) |

| Surge in SiC and GaN adoption for EV powertrains | +0.60% | China, Japan | Short term (≤ 2 years) |

| Mini/Micro-LED ramp-up elevating metal-organic demand | +0.40% | Korea, Taiwan | Medium term (2-4 years) |

| ASEAN re-shoring initiatives for backend materials | +0.30% | ASEAN | Long term (≥ 4 years) |

| Low-GWP fluorinated-gas mandates | +0.20% | Global | Short term (≤ 2 years) |

| Heterogeneous-integration materials for 2.5D/3D IC | +0.50% | Taiwan, Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-backed Chip Sovereignty Funds Accelerating New Material Fabs in China, Japan and Korea

Several Northeast-Asian governments are using dedicated chip funds to subsidize local material plants, shortening qualification cycles and lifting regional content in leading-edge fabs. In Korea, a USD 471 billion cluster in Gyeonggi Province targets 50% self-sufficiency in critical chemistries by 2030. [1]Ministry of Trade, Industry and Energy, “Korea’s Semiconductor Cluster Roadmap,” koreatimes.co.kr Japan is tying TSMC’s Kumamoto expansion to joint R&D programs with domestic photoresist and wafer suppliers, while China is channeling capital toward indigenous CMP slurries, electronic gases and fluorochemicals. These coordinated investments underpin steady demand even during cyclical downturns, giving the Asia-Pacific semiconductor materials market a structural growth floor.

Surge in SiC and GaN Adoption for EV Powertrains Across China and Japan

Electric-vehicle makers are shifting from silicon MOSFETs to SiC and GaN power devices to cut conduction losses and boost driving range. Chinese vertically integrated substrate pioneers have begun supplying 200 mm SiC wafers that meet automotive-grade defect density thresholds, helping local OEMs lock-in long-term contracts. Japanese material houses are parallel-tracking crystalline-quality improvements for GaN-on-Si epitaxy to serve on-board chargers. This transition is tilting material demand toward wide-bandgap substrates, epitaxial gases and high-temperature encapsulants, broadening the Asia-Pacific semiconductor materials market beyond its silicon core.

Mini/Micro-LED Ramp-up Driving Demand for High-Purity Metal-Organics in Korea and Taiwan

Commercial readiness of micro-LED displays with pixel densities above 500 PPI is pulling in unprecedented volumes of ultra-high-purity trimethyl-gallium, trimethyl-indium and precursors for quantum-dot color-conversion layers. Korean panel makers and Taiwanese OSATs are collaborating to co-optimize epitaxial growth and bump-bonding flows, raising the bar for impurity controls to parts-per-trillion. Suppliers capable of delivering such contamination thresholds at scale are capturing premium margins, reinforcing the value-add shift within the Asia-Pacific semiconductor materials market.

ASEAN Re-shoring Initiatives Creating Green-field Chemical Plants for Backend Materials

Malaysia, Vietnam and Thailand are stepping up incentives for local production of molding compounds, substrates and lead-frame alloys. Penang’s backend cluster alone tripled its factory space to 3.4 million ft² in 2025. Green-field plants in these markets shorten logistics loops for regional OSATs, diversify geo-political exposure and unlock lower-carbon utility footprints. As capacity migrates south, chemical vendors are adding localized mixing, purification and drum-recycling operations, widening the geographic spread of the Asia-Pacific semiconductor materials market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile silicon and rare-metal prices | -0.40% | Global | Short term (≤ 2 years) |

| US/EU export controls delaying qualification in China | -0.60% | China | Medium term (2-4 years) |

| Ultrapure-water scarcity | -0.30% | Taiwan, Singapore | Long term (≥ 4 years) |

| Lengthy EHS permitting for chemical plants | -0.20% | Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Silicon and Rare-Metal Prices Squeezing Fab Margins

Spot silicon-wafers and crucible-grade quartz have exhibited double-digit price swings amid tight supply chains concentrated in a handful of mines. Parallel spikes in gallium and germanium prices, following export-license restrictions, are forcing fabs to re-negotiate long-term contracts and hedge commodity exposure. Because material outlays can represent 25-30% of wafer-fabrication cash costs, these fluctuations compress profitability and temper expansion plans, keeping the Asia-Pacific semiconductor materials market on a cautious capital-expenditure footing.

US/EU Export Controls Delaying Material Qualification in Mainland China

Expanded Foreign Direct Product rules issued in December 2024 now require special licenses for a wider set of photoresists, lithography gases and deposition precursors destined for advanced Chinese fabs. [2]Federal Register, “Advanced-Computing and Semiconductor Manufacturing Export Controls,” federalregister.gov As compliance audits lengthen, local foundries are forced to dual-source or initiate in-house development, stretching qualification timelines by 6-12 months. The lag slows node migrations and curbs near-term material volumes, subtracting 0.6 percentage points from the Asia-Pacific semiconductor materials market CAGR during the forecast window.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Wide-Bandgap Semiconductors Drive Innovation

Silicon Wafers retained the largest 37.74% share of the Asia-Pacific semiconductor materials market in 2025, supported by capacity additions at 5 nm and 3 nm nodes. Yet Silicon Carbide is the clear growth engine, expanding at 9.08% CAGR as vehicle electrification and renewable grids demand high-voltage efficiency. This shift is enlarging the Asia-Pacific semiconductor materials market size for wide-bandgap substrates, gases and polishing slurries that meet stringent surface-defect criteria. GaN and GaAs materials are also gaining traction for 5G base-stations and RF front-ends, even though substrate costs remain a cap on volume adoption.

Process innovation is bringing 200 mm SiC wafers to pilot scale, with defect densities below 0.1 cm⁻² setting new automotive benchmarks. At the same time, the Korea Research Institute of Chemical Technology’s breakthrough in hydrofluoroether synthesis improves local supply security for advanced etch chemistries. As these technical milestones reduce unit costs and raise reliability, they reinforce a performance-over-price paradigm that re-shapes procurement decisions within the Asia-Pacific semiconductor materials market.

By Application: Advanced Packaging Reshapes Material Demands

Fabrication consumed 65.12% of total material revenues in 2025, anchored by lithography-heavy logic and memory expansions. Electronic specialty gases represent the fastest-growing fabrication sub-segment, climbing at 8.11% CAGR as patterning complexity increases. However, Advanced Packaging is the headline growth story, rising 6.84% annually as chiplet and 3D-stack architectures move into high-volume manufacturing. The Asia-Pacific semiconductor materials market size tied to organic and ceramic substrates is projected to reach USD 10.06 billion by 2031, with under-fill and dielectric films advancing in tandem.

TOPPAN’s coreless organic interposer allows fine-pitch interconnects below 10 µm, eliminating build-up layers and reducing package Z-height. Copper-to-copper hybrid bonding is simultaneously displacing traditional solder bumps, pushing demand for oxide-removal cleaners and low-temperature diffusion barriers. Together, these advances expand material-count per package and diversify the bill-of-materials, adding resilience to the Asia-Pacific semiconductor materials market.

By End-user: Automotive Transformation Accelerates

Consumer Electronics still represented 41.02% of the Asia-Pacific semiconductor materials market in 2025, but unit growth is plateauing. In contrast, Automotive and Mobility is escalating at 8.29% CAGR, propelled by battery-electric drivetrain volumes and the proliferation of advanced driver-assistance systems. A premium electric vehicle can now carry USD 1,600-1,900 worth of semiconductors, double that of an entry-level smartphone, creating a lucrative pull for AEC-Q101-qualified wafers, encapsulants and power modules. These dynamics are redistributing the Asia-Pacific semiconductor materials market share toward suppliers with automotive-grade certification capabilities.

Parallel tailwinds exist in data-center processors and high-performance computing accelerators, where packaging materials with superior thermal conductivity and low-loss dielectrics are mission-critical. Telecom infrastructure, industrial automation and medical electronics round out the demand profile, each segment adding specialized requirements that raise the overall technical ceiling-and barriers to entry-within the Asia-Pacific semiconductor materials market.

Geography Analysis

Taiwan captured 34.75% of the Asia-Pacific semiconductor materials market in 2025, thanks to its dense ecosystem linking logic foundries, memory fabs and advanced packaging houses. Close physical proximity between fabs and material suppliers reduces cycle time for slurry, resist and specialty-gas qualifications, reinforcing Taiwan’s leadership. Yet water-stress projections show semiconductor plants could raise local water demand 236% between 2021 and 2030, prompting accelerated adoption of closed-loop reclamation systems. Energy-price volatility adds further cost pressure, encouraging fabs to shift incremental capacity for mature nodes to alternate hubs.

China is the fastest-growing market, forecast at a 3.92% CAGR through 2031 as industrial-policy incentives, tax rebates and land grants underwrite domestic sourcing programs. While export-control headwinds persist, tier-1 Chinese foundries are qualifying indigenous slurries, photoresists and CMP pads for 28 nm nodes and below. Regional material parks in Anhui, Hubei and Guangdong bundle gas farms, chemical mixing and waste-treatment facilities, reducing inbound logistics costs by up to 15%. As localization takes hold, the Asia-Pacific semiconductor materials market gains a second gravitational center beyond Taiwan.

South Korea’s USD 471 billion mega-cluster will add new demand for lithography chemicals, ALD precursors and high-bandwidth-memory substrates, with SK Hynix alone budgeting USD 75 billion to 2028. Japan, already a top exporter of fluorinated gases and photo-initiators, is bolstering resilience by constructing its first domestic 300 mm wafer plant in over five decades. Meanwhile, ASEAN countries-led by Malaysia and Vietnam-are scaling backend assembly and selectively moving into front-end pilot lines. This geographic diversification diffuses single-country risk while enlarging the overall addressable base of the Asia-Pacific semiconductor materials market.

Competitive Landscape

The Asia-Pacific semiconductor materials market shows moderate fragmentation. In value-added niches such as EUV photoresists, less than five suppliers meet stochastic-defect targets, whereas bulk chemicals face intense price competition from new Chinese producers. Incumbent Japanese and European firms are responding by deepening local manufacturing: Shin-Etsu is expanding wafer capacity in Japan after a 56-year hiatus, and BASF is constructing a semiconductor-grade sulfuric-acid plant to tighten control over upstream supply. [3]BASF, “Investment in Semiconductor-Grade Sulfuric Acid,” basf.com

Technology co-development is emerging as a key differentiator. The US-JOINT consortium, which includes 3M, is pooling resources to accelerate non-PFAS surface-modifier research, seeking drop-in replacements ahead of regulatory bans. In packaging, Applied Materials’ 9% stake in BE Semiconductor is aimed at hybrid-bonding line-integration, ensuring equipment-to-material process compatibility. Such alliances underscore a strategic pivot from scale-based competition toward ecosystem orchestration within the Asia-Pacific semiconductor materials market.

Chinese challengers are gaining traction in commodity segments such as sputter targets and wet chemicals by leveraging cost-advantaged energy tariffs and state-backed financing. Qualification barriers remain steep for safety-critical chemistries, yet once approved, domestic suppliers can rapidly scale, pressuring incumbents on margin. Taken together, these dynamics point toward a landscape where intellectual-property depth, regional manufacturing breadth and ESG compliance ultimately determine share capture in the Asia-Pacific semiconductor materials market.

Asia-Pacific Semiconductor Materials Industry Leaders

Shin-Etsu Chemical Co., Ltd.

Sumitomo Chemical Co., Ltd.

Merck KGaA (incl. Versum Materials)

Air Liquide S.A.

BASF SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Ampoc partnered with South Korea’s DCT Material to expand advanced-process material offerings in Taiwan, reinforcing regional coverage.

- April 2025: Applied Materials acquired a 9% stake in BE Semiconductor Industries to strengthen hybrid-bonding collaboration.

- April 2025: BASF committed to a new semiconductor-grade sulfuric-acid unit in Ludwigshafen, slated for 2027 on-stream.

- April 2025: Toppan’s Tekscend unit filed for an IPO to fund advanced-material expansion.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Asia-Pacific semiconductor materials market as the annual demand for front-end fabrication and back-end packaging consumables, silicon and compound wafers, photoresists and ancillaries, ultra-high-purity gases, CMP slurries and pads, substrates, bonding wires, die-attach materials, and encapsulation resins used inside foundries and assembly plants located in China, Taiwan, South Korea, Japan, and the remainder of Southeast Asia. This coverage tracks only virgin material shipments sold to device makers or OSATs and values them at manufacturer transfer price.

Exclusion: Capital equipment, refurbished consumables, and recycled scrap are outside the scope.

Segmentation Overview

- By Material

- Silicon Wafers

- Silicon Carbide (SiC)

- Gallium Arsenide (GaAs)

- Gallium Nitride (GaN)

- Silicon Germanium (SiGe)

- Indium Phosphide (InP)

- Copper Indium Gallium Selenide (CIGS)

- Molybdenum Disulfide (MoS?)

- Bismuth Telluride (Bi?Te?)

- Other Materials

- By Application

- Fabrication

- Process Chemicals

- Photomasks

- Electronic Gases

- Photoresist Ancillaries

- Sputtering Targets

- Silicon Wafers

- CMP Slurries and Pads

- Other Fabrication Materials

- Packaging

- Substrates

- Lead Frames

- Ceramic Packages

- Bonding Wire

- Encapsulation Resins

- Die-Attach Materials

- Other Packaging Materials

- Fabrication

- By End-user Industry

- Consumer Electronics

- Telecommunication and 5G Infrastructure

- Industrial and Manufacturing Automation

- Automotive and Mobility (EV, ADAS)

- Energy and Utility (Solar, Power Conversion)

- Data Centers and HPC

- Healthcare Devices

- Others

- By Geography

- Taiwan

- South Korea

- China

- Japan

- Rest of Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Multiple in-depth interviews and structured surveys with wafer makers, specialty chemical suppliers, OSAT engineers, and regional trade associations bridge data gaps, validate pricing corridors, and align our adoption timelines for SiC, GaN, and heterogeneous integration substrates across China, Taiwan, Korea, Japan, India, and ASEAN. Respondents also stress test our mid-term demand drivers with perspectives from consumer electronics, EV, and 5G infrastructure clients.

Desk Research

Mordor analysts first gather publicly available statistics from tier-one bodies such as WSTS, JEITA, SEMI's Material Market Data Subscription, and customs trade panels, which reveal quarterly volume flows and ASP shifts for key inputs. We enrich these with national science agency datasets, patent filings harvested through Questel, and regulatory releases on environment and export controls that shape material substitution cycles. Company 10-Ks, investor decks, and relevant peer-reviewed journals then help us confirm technology road maps and cost inflection points. Additional signals from D&B Hoovers and Dow Jones Factiva allow cross-checking of plant capacities and outage news. The sources listed here are illustrative; many other open datasets and specialist feeds inform the desk study.

Market-Sizing & Forecasting

A top-down model begins with WSTS device revenue for Asia-Pacific; we back-calculate material demand through production-stage bill of materials ratios that differ for logic, memory, and power devices, and then layer country-level wafer start data to refine volumes. Select bottom-up checks, supplier shipment roll-ups, sampled ASP × wafer area maths, and channel feedback anchor the totals. Key variables include 300 mm wafer starts, advanced packaging penetration, wide bandgap device share, silicon price indices, and fab utilization rates. Multivariate regression combined with scenario analysis projects these drivers through 2030, while missing bottom-up data points are bridged with triangulated ranges agreed during expert calls.

Data Validation & Update Cycle

Outputs pass three-step peer review; variance dashboards flag anomalies against historical ratios, and any ±5% deviation triggers a re-interview loop. Reports refresh once a year; material plant closures, new subsidy programs, or export control shifts prompt interim updates before client delivery.

Why Mordor's Asia-Pacific Semiconductor Materials Baseline Earns Trust

Published values often diverge because each firm chooses different scope limits, price bases, and refresh cadences. Our disciplined inclusion of both fab and packaging consumables, coupled with yearly primary data resets, delivers a balanced baseline.

Key gap drivers include rival reports that fold electronic chemicals or advanced substrates from other regions into Asia totals, omit packaging resins, or rely on unstated markup factors when silicon prices spike. Others publish conservative scenarios without checking live ASP movements that our quarterly expert loops capture.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 27.1 B (2025) | Mordor Intelligence | - |

| USD 41.7 B (2024) | Regional Consultancy A | Combines electronic chemicals and advanced materials from global plants into APAC scope, inflating base value |

| USD 16.3 B (2024) | Trade Journal B | Excludes packaging substrates and bonding materials, leading to understated market pool |

Taken together, the comparison shows that when scope alignment and live pricing validation are applied consistently, Mordor Intelligence offers decision-makers the most dependable, transparent starting point for strategy and investment planning in Asia-Pacific semiconductor materials.

Key Questions Answered in the Report

What is the current value of the Asia-Pacific semiconductor materials market?

The market stands at USD 27.99 billion in 2026 and is projected to reach USD 32.87 billion by 2031 at a 3.27% CAGR.

Which country holds the largest share of the Asia-Pacific semiconductor materials market?

Taiwan leads with a 34.75% revenue share in 2025, driven by its concentration of advanced logic and packaging facilities.

Which material category is growing the fastest?

Silicon Carbide is expanding at 9.08% CAGR between 2026 and 2031 owing to electric-vehicle power-electronics adoption.

Why is advanced packaging important for material suppliers?

Chiplet and 3D-stack designs boost demand for innovative under-fill, substrate and bonding materials, lifting Advanced Packaging revenues at a 6.84% CAGR.

How are export controls affecting the Asia-Pacific semiconductor materials market?

New US/EU rules lengthen material qualification for Chinese fabs by up to 12 months, subtracting 0.6 percentage points from the regional CAGR.

What environmental issues influence investment decisions?

Water scarcity in Taiwan and Singapore, along with forthcoming PFAS regulations, are prompting fabs and suppliers to adopt reclamation systems and develop non-fluorinated chemistries.

Page last updated on: