E-commerce Personal Care Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

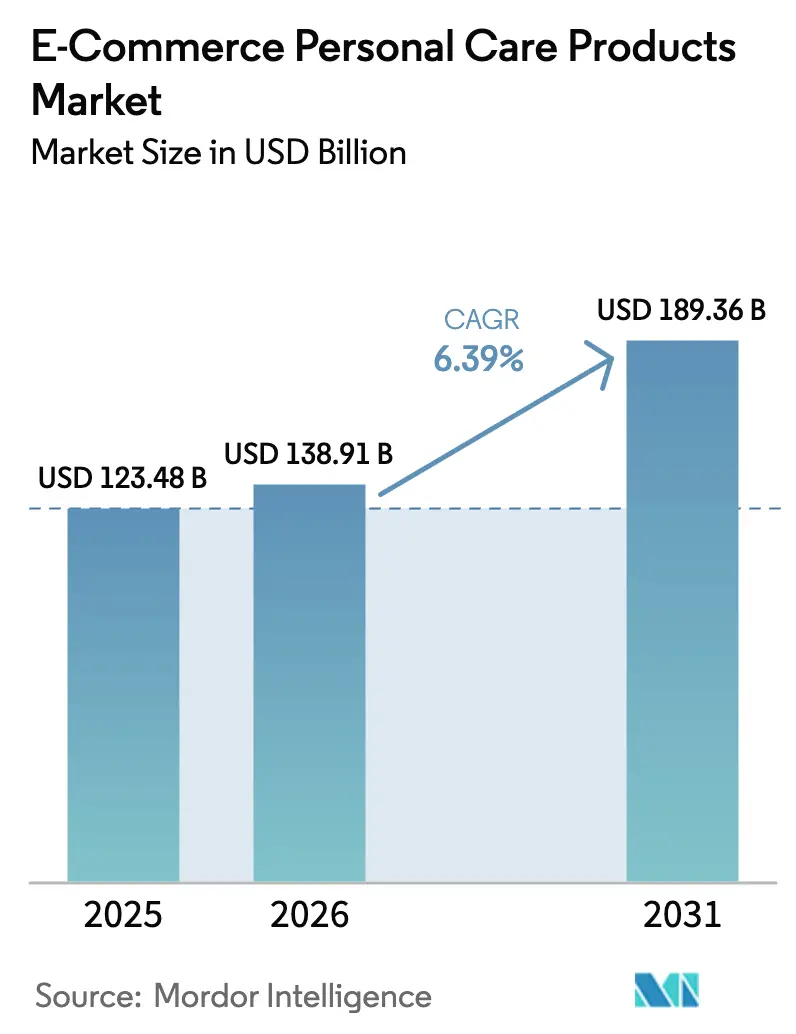

| Market Size (2026) | USD 138.91 Billion |

| Market Size (2031) | USD 189.36 Billion |

| Growth Rate (2026 - 2031) | 6.39% CAGR |

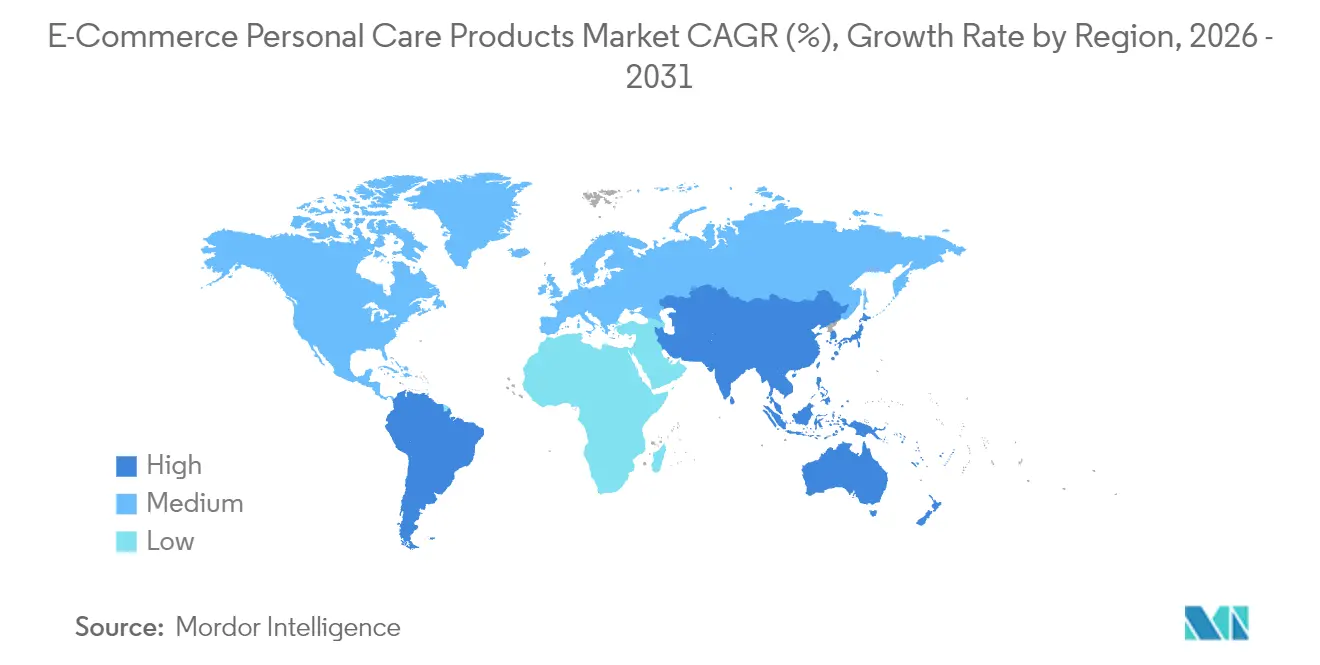

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

E-commerce Personal Care Products Market Analysis by Mordor Intelligence

The global E-commerce Personal Care Products Market size in 2026 is estimated at USD 138.91 billion, growing from 2025 value of USD 123.48 billion with 2031 projections showing USD 189.36 billion, growing at 6.39% CAGR over 2026-2031. This trajectory reflects the evolving consumer preferences for convenience, personalization, and digital engagement. E-commerce, mobile shopping, AI-driven recommendations, and the influence of social media have transformed how consumers discover and purchase beauty and grooming products. This transition is expanding the market by enabling brands to reach a broader audience through innovative channels like live streaming and social commerce. Consumers are increasingly drawn to platforms that offer seamless purchasing experiences, flexible payment options, and personalized product suggestions tailored to their unique needs. The growing demand for clean, sustainable, and ethical products further fuels this shift, as shoppers prioritize transparency and authenticity in their choices. Additionally, advancements in augmented reality and secure payment systems enhance the online shopping experience, bridging the gap between mass-market affordability and premium offerings.

Key Report Takeaways

- By product type, skin care led with 41.52% revenue share in 2025, while hair care is projected to expand at a 7.10% CAGR to 2031.

- By ingredient, conventional formulations captured 70.78% of the E-commerce Personal Care Products Market share in 2025; natural/organic formats are forecast to grow at an 8.95% CAGR through 2031.

- By category, mass items commanded 71.36% of the E-commerce Personal Care Products Market size in 2025, and premium items are advancing at a 7.52% CAGR to 2031.

- By platform type, third-party marketplaces captured 87.60% share in 2025, while company-owned sites are growing faster at a 9.21% CAGR to 2031.

- By geography, Asia-Pacific held 42.10% of global value in 2025 and is set to record a 9.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global E-commerce Personal Care Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Influence of social media and influencer marketing | +1.2% | Global, with concentration in North America, Asia-Pacific | Medium term (2-4 years) |

| Availability of flexible payment methods | +0.9% | Global, strongest in Europe, South America, Asia-Pacific | Short term (≤ 2 years) |

| Attractive promotion and discounts driving purchases | +0.8% | Global, particularly intense in third-party marketplaces across all regions | Short term (≤ 2 years) |

| Growing preference for clean, sustainable, and ethical options | +1.1% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Surge in online shopping habits | +1.3% | Global, accelerated adoption in Asia-Pacific, persistent in North America and Europe | Medium term (2-4 years) |

| AI-led personalization and product recommendations | +1.0% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Influence of social media and influencer marketing

The E-commerce Personal Care Products Market has transformed its promotional strategies, with social commerce emerging as a key growth driver. This shift is primarily due to the increasing reliance on digital platforms for product discovery and reviews. Creator-driven sales streamline the path from awareness to purchase by leveraging compelling short-form videos that trigger immediate purchases. Platforms such as LTK and Collabstr formalize affiliate partnerships, enabling micro-influencers to monetize niche audiences while brands access granular attribution data. Seamless integration of digital payments has further sped up this transformation. In July 2025, Press Information Bureau reported that Unified Payments Interface (UPI) processed INR 18.39 billion financial transactions in a single month, demonstrating its importance in India's e-commerce digital transformation [1]Source: Press Information Bureau (PIB), "India’s UPI Revolution", pib.gov.in. Influencers, particularly micro and nano influencers, build authentic trust with their followers, amplifying the influence of their endorsements. Brands leverage social media platforms like Instagram, TikTok, and YouTube for dynamic, visual engagement with audiences. This momentum broadens market access, boosts brand awareness, and drives direct consumer sales.

Availability of flexible payment methods

Flexible payment choices propel expansion in the E-commerce Personal Care Products Market by reshaping how consumers shop and boosting checkout completions. Buyers demand safe, tailored payment flows, from credit cards to digital wallets. These wallets now handle a large share of worldwide online transactions, enabling one-tap buys and stronger security to cut drop-offs and abandoned carts. In January 2025, PayPal reported 26.3 billion global payment transactions processed in 2024 [2]Source: PayPal, "Enterprise Payments Processing Solutions", paypal.com. The integration of diverse payment solutions remains essential for e-commerce platforms to maintain market competitiveness and meet evolving consumer preferences in the personal care products segment. As digital payment technologies continue to advance, companies embracing these advancing digital payment innovations secure sustained growth in the online personal care arena.

AI-led personalization and product recommendations

Personalization and product recommendation technologies exert significant influence on consumer purchasing behavior in the E-commerce Personal Care Products Market, serving as critical tools to elevate customer engagement and drive sales growth. Generative AI and computer vision elevate product matching beyond keyword search. Consumers derive substantial advantages from sophisticated AI-driven solutions, encompassing computer-vision shade matching, chat-based routine builders, and dynamic bundling engines, which deliver customized product recommendations aligned with individual preferences and requirements. Brands that embed AI into mobile apps and owned platforms capture first-party data, reducing reliance on third-party cookies as privacy regulations tighten. These technologies streamline the decision-making process, affording enhanced convenience and a bespoke shopping experience. By incorporating these tools into their platforms, brands deliver seamless shopping experiences, reduce cart abandonment rates, and nurture enduring customer loyalty.

Growing preference for clean, sustainable, and ethical options

The E-commerce Personal Care Products Market is undergoing a profound shift, fueled by surging consumer demand for clean, sustainable, and ethical products. Certified clean labels have transitioned from niche appeal to mainstream expectation. Heightened consumer awareness of ingredient profiles, sustainability practices, and ethical standards continues to shape buying decisions, prompting manufacturers to realign their product offerings. According to the National Science Foundation, certification frameworks such as NATRUE, COSMOS, and USDA Organic provide verifiable claims that resonate with 74% of consumers who consider organic ingredients important when purchasing beauty products [3]Source: National Science Foundation (NSF), "74% of Consumers Consider Organic Ingredients Important in Personal Care Products", nsf.org. Refillable packaging resonates strongly with eco-conscious consumers, especially Gen Z, who rank sustainability as a top purchase driver. Subscription-based refill models merge environmental benefits with everyday convenience, fostering steady engagement and reliable replenishment. Market leaders are embedding ingredient transparency, sustainable sourcing, and cruelty-free certifications to meet these rising expectations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise of counterfeit and substandard products | -0.7% | Global, with highest impact in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Logistics hurdles in fulfillment and delivery | -0.5% | Global, particularly affecting rural and remote areas | Long term (≥ 4 years) |

| Intense price competition reduces profit margins | -0.6% | Global, particularly severe in third-party marketplaces | Short term (≤ 2 years) |

| Data privacy issues restricting personalization | -0.4% | Europe and North America leading regulatory restrictions, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise of counterfeit and substandard products

The growth of the global E-commerce Personal Care Products Market faces major hurdles from rampant counterfeit goods, which threaten consumer safety and undermine brand trust. This critical issue manifests predominantly within third-party e-commerce platforms, where product authentication mechanisms remain insufficient. U.S. Customs and Border Protection reported the seizure of personal care products worth USD 8 million and USD 57 million in perfumes in 2023 [4]Source: U.S. Customs and Border Protection, "FY 2024 IPR Seizure Statistics", cbp.gov. E-commerce platforms are subject to increased regulatory accountability under revised frameworks, including the elimination of the de minimis exemption for low-value shipments, which has strengthened customs surveillance and necessitated the implementation of more rigorous seller verification protocols. Despite these challenges, the E-commerce Personal Care Products Market continues to grow via stronger compliance measures, advanced authentication tools, and fortified supply chains, safeguarding consumers and supporting ongoing expansion.

Logistics hurdles in fulfillment and delivery

The E-commerce Personal Care Products Market faces key operational hurdles, particularly in fulfillment and delivery logistics. Handling varied product formulas, packaging needs, and regulatory standards across borders poses steep challenges for firms pursuing international scale. Companies must tackle intricate customs processes alongside region-specific rules on packaging and ingredients. Non-compliance with these requirements can lead to operational delays, increased costs, and restricted market access. Additionally, peak seasons such as festivals, holidays, New Year, Valentine's week, and back-to-school periods place immense pressure on logistics networks, resulting in inventory management issues and delivery delays. These issues highlight the critical need for resilient supply chain systems and thorough compliance frameworks to enable steady growth and competitive strength in the global e-commerce personal care products arena.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Skin Care Dominates Digital Beauty Landscape

The skin care segment leads the market with a 41.52% share in 2025, surpassing the overall personal care market. This dominance is driven by facial products enhanced with AR diagnostic tools and ingredient transparency, which clean-beauty advocates prioritize for routines targeting hydration, acne, and anti-aging concerns. The hair care segment exhibits the highest growth rate, achieving a 7.10% CAGR through 2031. This growth is fueled by customization platforms offering AI-driven formulas tailored to individual porosity, texture, and scalp needs. Consumers increasingly adopt personalized shampoos and treatments that deliver visible results, while demand for clean, bond-repair, and scalp-focused innovations rises across both mass and premium channels. Technological advancements, such as L'Oréal Groupe's AirLight Pro, a professional-grade hair drying instrument launched in January 2024, exemplify this trend.

The lip care segment is experiencing a significant recovery, driven by the resurgence of social activities post-pandemic, which has boosted demand for products offering both hydration and aesthetic benefits. The oral care and bath-and-shower segments continue to expand steadily, supported by subscription models that simplify replenishment. Meanwhile, the men's grooming category benefits from direct-to-consumer brands like Harry's and Dollar Shave Club, which normalize male self-care through razors and skincare products. Perfumes address counterfeit challenges by adopting blockchain-authenticated luxury solutions, such as Coty's Aura partnership. Additionally, sun care products leverage dermatologist endorsements, while deodorants gain traction with premium, natural aluminum-free options available on owned platforms.

By Ingredients: Natural/Organic Outpace Conventional Lines

Conventional ingredients dominate the global E-commerce Personal Care Products Market with a 70.78% market share, benefiting from established supply chains and lower price points that appeal to mass-market buyers. This dominance is attributed to well-established supply chains that ensure consistent product availability and cost advantages for manufacturers and retailers. Conventional formulations continue to appeal due to their proven efficacy, stability, and scalability, particularly among price-sensitive consumers in mass market segments where affordability and reliability are key. E-commerce sharpens the split, with price-sensitive shoppers chasing discounts on marketplaces and values-driven buyers favoring brand sites for certified, filterable options, erasing legacy retail's information edge through instant ingredient scans and badges.

Natural/organic formulations lead growth at 8.95% CAGR through 2031, outpacing the market average as consumers demand NATRUE, COSMOS, and USDA Organic certifications to cut through greenwashing and verify clean claims. These ingredients power shampoos, serums, and creams tailored for sensitive skin and scalps, with premium pricing justified by transparency and sustainability sourcing. Manufacturers are innovating with new formulations, adopting sustainable packaging, and obtaining certifications to align with consumer preferences. The combination of premium natural and organic products with digital marketing strategies is accelerating adoption across both developed and emerging markets.

By Category: Premium Segment Drives Value Growth in Online Beauty

Mass products continue to dominate the global E-commerce Personal Care Products Market, holding a 71.36% market share in 2025. Economic conditions have amplified consumer price sensitivity, driving a shift toward value-focused purchasing behaviors. fueled by aggressive pricing on third-party marketplaces and promotions that prioritize volume over margins in drugstores and hypermarkets. Estée Lauder's shift to owned platforms captures first-party data for tailored bundles, shielding premium-like experiences from commoditized discounting. Well-established supply chains, strategic promotional efforts, and a strong presence in online marketplaces further reinforce the dominance of mass-market products globally.

The premium segment is projected to grow significantly, with a compound annual growth rate of 7.52% through 2031, seamless omnichannel delivery, and exclusive online drops that elevate the experiential shopping experience. These high-end offerings thrive on virtual consultations and AI shade matching, fostering exclusivity that supports elevated pricing amid e-commerce's rise. This growth is fueled by rising disposable incomes, increasing demand for advanced formulations, and a growing preference for personalized luxury experiences. Premium brands are enhancing their market presence through technological innovations, strategic influencer partnerships, and targeted online product launches.

By Platform Type: Growth and Strategic Importance of Company-Owned Platforms

Third-party marketplaces are projected to dominate the global E-commerce Personal Care Products Market in 2025, accounting for 87.60% of platform share, driven by unmatched traffic, payments, and logistics that fuel volume for mass brands. Glossier's hybrid play, expanding to Amazon and Sephora, balances acquisition scale with owned-channel equity, though commoditization risks persist. Consumers favor these platforms for their convenience in comparing products, finding competitive prices, and consolidating purchases. Leading marketplaces such as Amazon, Tmall, Flipkart, and Shopee allow customers to buy multiple brands and categories in a single transaction. These platforms attract users through customer reviews, frequent promotions, and reliable shipping services.

Company-owned platforms, while holding a smaller market share, are anticipated to grow at a CAGR of 9.21% through 2031, outpacing all rivals as brands seize first-party data, margin control, and direct relationships that marketplaces can't match. Mobile apps with AI skin diagnostics and virtual try-ons build loyalty, turning one-time buyers into subscribers while shielding differentiation from price wars. This growth is driven by the increasing adoption of direct-to-consumer (DTC) strategies, which enhance customer engagement and personalization.

Geography Analysis

The Asia-Pacific region is expected to dominate the market with a 42.10% share by 2025, growing at a robust CAGR of 9.88% through 2031. This growth is fueled by the rapid evolution of China's digital retail landscape and India's Unified Payments Interface (UPI), which processed over 100 billion transactions in 2025, enabling platforms like Nykaa to expand into tier-2 and tier-3 cities. Mobile-first super-apps and data localization regulations further strengthen the region's leadership. Southeast Asia is emerging as a critical beauty e-commerce market, driven by a growing middle class and advancements in internet infrastructure. The region's dominance is underpinned by mobile-first consumer behavior and super-app ecosystems that integrate beauty with related services. Platforms such as Alibaba and Shopee play a pivotal role in providing market access to developing areas.

North America remains a leader in the E-commerce Personal Care Products Market, demonstrating steady growth despite political and market challenges, reflecting its maturity and saturation in urban centers. The region benefits from well-established logistics networks, high credit card penetration, and increasing competition from direct-to-consumer brands that bypass traditional retail channels. Growth is further supported by high disposable incomes, established personal care routines, same-day delivery options, loyalty programs, and a rising focus on dermatological and hair care needs among consumers.

European markets continue to hold a significant position in online beauty commerce, driven by heightened environmental awareness. According to IfD Allensbach data, 21.91 million German-speaking consumers expressed a willingness to increase spending on environmentally sustainable products in 2024. While GDPR compliance requirements impose higher operational costs, they also create a competitive advantage for brands investing in privacy-preserving personalization technologies. Meanwhile, the Middle East and Africa remain smaller markets, constrained by fragmented logistics and lower e-commerce adoption. However, Gulf Cooperation Council countries are experiencing rapid growth, supported by high smartphone penetration and government-led digital transformation initiatives.

Competitive Landscape

The market is moderately consolidated, with key players such as L'Oréal S.A., Procter & Gamble Company, Unilever PLC, Colgate-Palmolive Company, and Natura & Co Holding SA holding significant market shares. These companies utilize global supply chains, omnichannel distribution, and diverse brand portfolios spanning mass to premium segments. Meanwhile, direct-to-consumer entrants leverage niche positioning, influencer networks, and first-party data to attract younger demographics with lower customer acquisition costs. These companies continue to strengthen their positions through innovation and strategic acquisitions.

Technology adoption increasingly defines competitive advantage, with leading companies investing in mobile-first experiences, privacy-preserving personalization, and supply-chain visibility to enable rapid replenishment and minimize out-of-stock incidents. For instance, L'Oréal has introduced the Light Straight + Multi-styler and an LED face mask equipped with patented infrared light technology. Brands that fail to integrate these capabilities risk commoditization on third-party marketplaces, where price competition erodes margins and customer loyalty. These developments highlight how traditional companies are forming strategic partnerships to enhance digital capabilities.

The competitive landscape is evolving as new entrants adopt digital business models, utilize social media sales channels, and collaborate with content creators. These companies disrupt conventional distribution networks by developing direct-to-consumer channels and leveraging customer data analytics to strengthen their market presence. Opportunities are emerging in underserved segments such as men's grooming, where subscription models remain underpenetrated compared to women's beauty, and in natural-formulation oral care, where certification frameworks lag behind those in skin and hair care. Emerging disruptors include customization platforms like Prose and Function of Beauty, which use algorithmic formulation to bypass traditional product development cycles, and blockchain-authenticated luxury brands addressing counterfeit concerns through serialized digital certificates.

E-commerce Personal Care Products Industry Leaders

-

L'Oréal S.A.

-

Procter & Gamble Company

-

Unilever PLC

-

Estée Lauder Companies Inc.

-

Natura & Co Holding SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: L’Oréal S.A. introduced Light Straight + Multi-styler and LED Face Mask at the CES 2026, with patented Infrared Technology & Light Module to augment hair and skin results.

- December 2025: The Estée Lauder Companies and Jo Malone London introduce AI-powered scent advisor, built with Google Cloud’s AI. It leverages advanced artificial intelligence to digitally recreate the in-store consultation experience. This scent advisor is available on JoMalone.com.

- May 2025: CHANEL introduced its fragrance and beauty products on Nykaa, making them available through Nykaa's app, website, and select Nykaa Luxe stores across India. The brand maintains a dedicated space on Nykaa's platform where customers can explore and purchase its product range.

- February 2025: Suave Brands Company expanded its beauty product line by introducing 34 new items. The company maintains its focus on providing high-quality products at affordable prices, offering premium performance in everyday personal care items. Suave products are distributed through a network of over 60,000 retail locations across the United States and through Amazon.

Global E-commerce Personal Care Products Market Report Scope

The E-commerce Personal Care Products Market encompasses the online sale of beauty and personal care items. It provides consumers with the convenience of online purchasing from their homes.

The E-commerce Personal Care Products Market is segmented based on product type, ingredients, category, platform type, and geography. By product type, the market is segmented into skin care, hair care, bath and shower, deodorants and antiperspirants, oral care, men's grooming products, sun care products, perfumes & fragrances. Based on ingredients, the market is segmented into conventional and natural/organic. Based on category, the market is segmented into mass and premium. Based on platform type, the market is segmented into third-party marketplaces and the company-owned platform. By geography, the market is segmented into North America, Europe, Asia Pacific, South America, the Middle East, and Africa. The market sizing has been done in value terms in USD for all the above mentioned segments.

| Hair Care | Shampoo |

| Conditioner | |

| Hair Colorant | |

| Hair Styling Products | |

| Others | |

| Skin Care | Facial Care Products |

| Body Care Products | |

| Lip and Nail Care Products | |

| Bath and Shower | Shower Gels |

| Soaps | |

| Others | |

| Oral Care | Toothbrush |

| Toothpaste | |

| Mouthwash and Rinses | |

| Others | |

| Men's Grooming Products | |

| Sun Care Products | |

| Deodorants and Antiperspirants | |

| Perfumes and Fragrance |

| Conventional |

| Natural/Organic |

| Mass |

| Premium |

| Third-Party Marketplace |

| Company-owned Platform |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Hair Care | Shampoo |

| Conditioner | ||

| Hair Colorant | ||

| Hair Styling Products | ||

| Others | ||

| Skin Care | Facial Care Products | |

| Body Care Products | ||

| Lip and Nail Care Products | ||

| Bath and Shower | Shower Gels | |

| Soaps | ||

| Others | ||

| Oral Care | Toothbrush | |

| Toothpaste | ||

| Mouthwash and Rinses | ||

| Others | ||

| Men's Grooming Products | ||

| Sun Care Products | ||

| Deodorants and Antiperspirants | ||

| Perfumes and Fragrance | ||

| By Ingredients | Conventional | |

| Natural/Organic | ||

| By Category | Mass | |

| Premium | ||

| By Platform Type | Third-Party Marketplace | |

| Company-owned Platform | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the E-commerce Personal Care Products Market?

The market was valued at USD 138.91 billion in 2026 and is projected to reach USD 189.36 billion by 2031.

Which product category leads online beauty sales?

Skin care holds the top position with 41.52% revenue share, driven by preventive wellness trends.

Which region currently contributes the biggest share of global digital beauty revenue?

Asia-Pacific supplied 42.10% of worldwide sales in 2025, boosted by live-streaming commerce and instant payment systems.

How important are third-party marketplaces?

Marketplaces account for 87.60% of total value, but brand-owned sites are expanding faster as firms seek data control.

Page last updated on: