Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

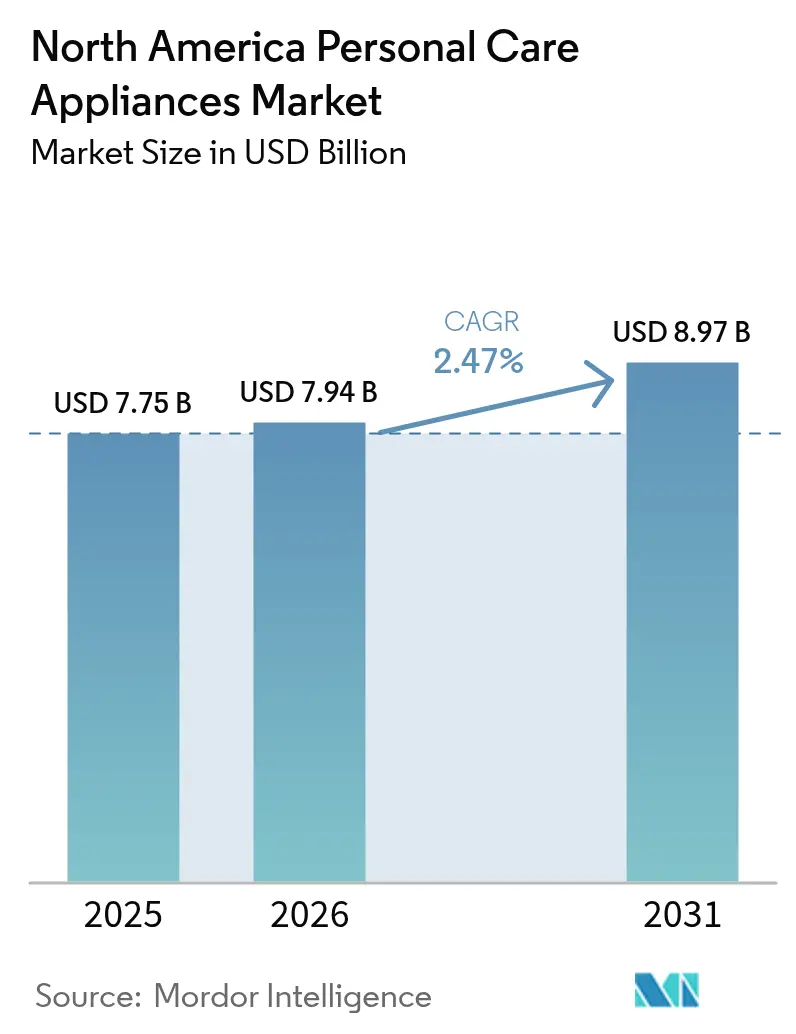

| Base Year Market Size (2025) | USD 7.75 Billion |

| Market Size (2026) | USD 7.94 Billion |

| Market Size (2031) | USD 8.97 Billion |

| Growth Rate (2026 - 2031) | 2.47% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Personal Care Appliances Market Analysis by Mordor Intelligence

The North American personal care appliances market size in 2026 is estimated at USD 7.94 billion, growing from 2025 value of USD 7.75 billion with 2031 projections showing USD 8.97 billion, growing at 2.47% CAGR over 2026-2031. This growth trajectory suggests a maturing market where innovation cycles and consumer behavior shifts drive value creation more than volume expansion. The relatively modest growth rate indicates that market leaders must compete on technological differentiation and operational efficiency rather than riding demographic tailwinds. The personal care appliances market is maturing, so value creation now depends more on technology upgrades, premium positioning, and razor-thin operational efficiency than on basic unit expansion. Competitive intensity has therefore shifted toward cordless power performance, IoT-enabled functionality, and gender-neutral design that can justify premium price points in an environment where consumers already own core devices. E-commerce’s rise reshapes discovery and purchasing habits, forcing brands to build direct relationships while managing margin pressure from online price transparency. Manufacturers that master battery innovation, data-driven personalization, and omnichannel fulfillment are best positioned to capture the next wave of replacement-driven demand.

Key Report Takeaways

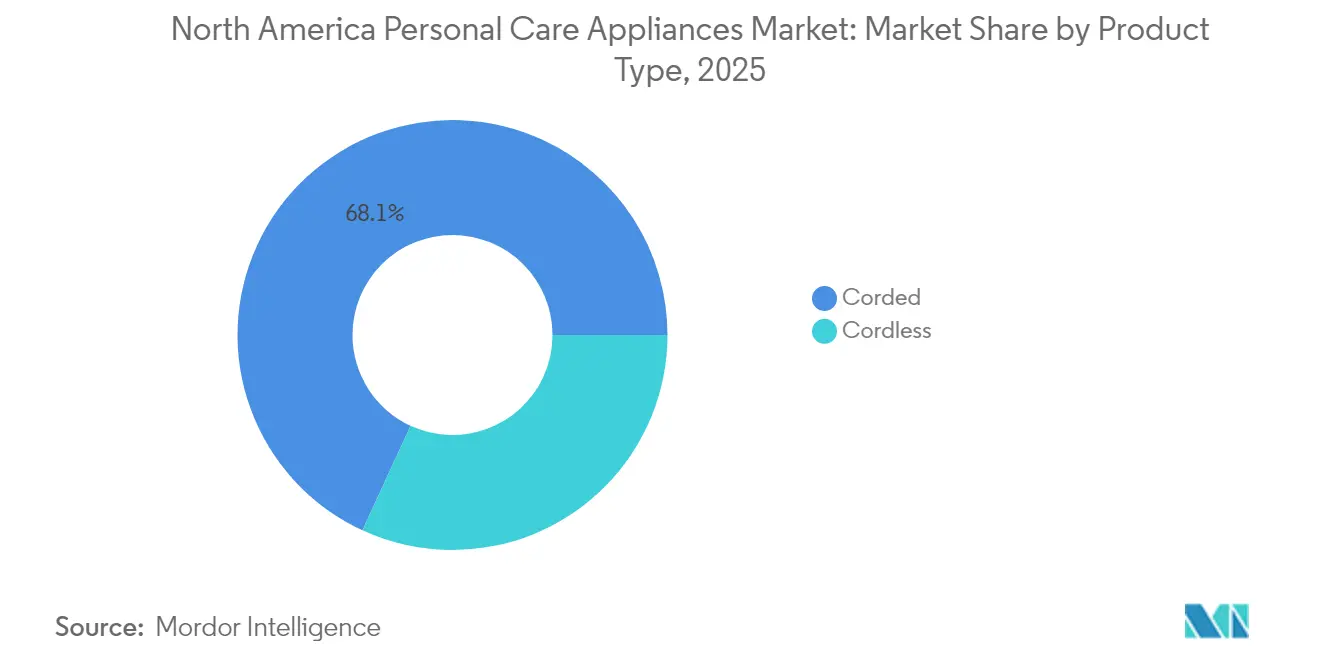

- By product type, corded devices retained 68.12% of the personal care appliances market in 2025, while cordless devices are forecast to expand at 2.78% CAGR through 2031.

- By product category, hair-styling appliances led with 32.86% of personal care appliances market share in 2025; oral care is projected to post the fastest 3.14% CAGR through 2031.

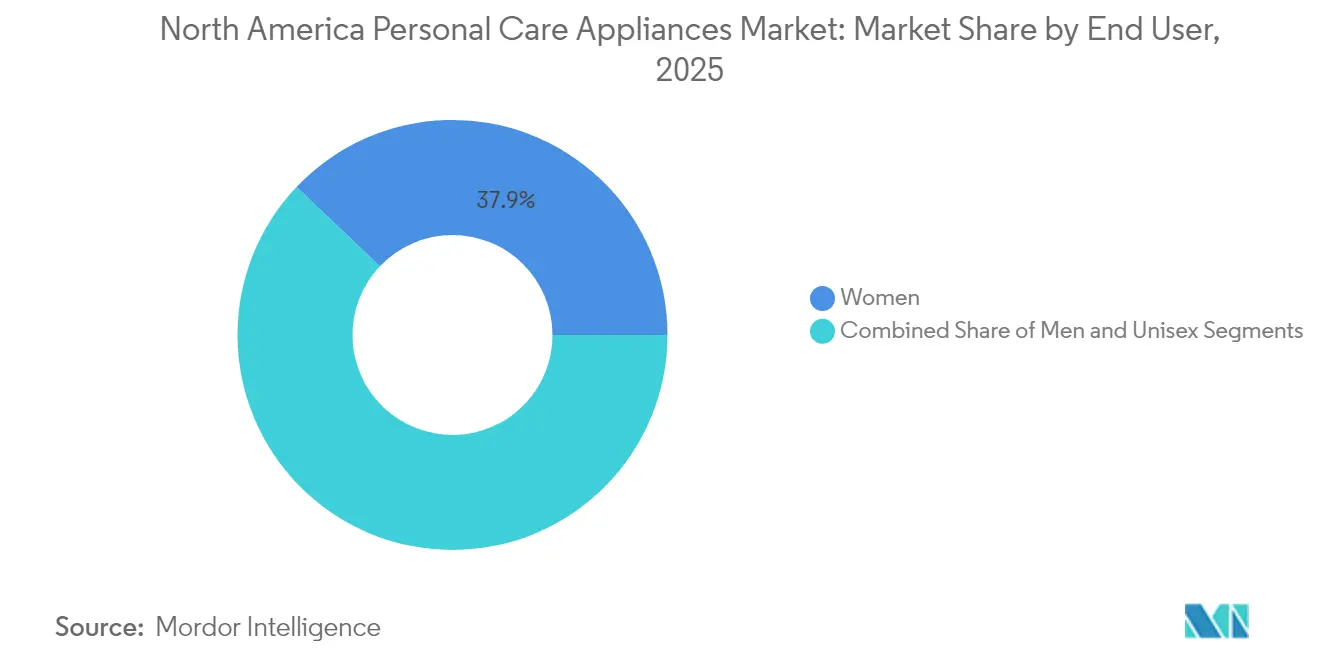

- By end user, women accounted for 37.92% revenue in 2025; men are expected to record the highest 3.47% CAGR to 2031.

- By distribution channel, online retail captured 47.65% of the personal care appliances market size in 2025 and is advancing at a 3.78% CAGR through 2031.

- By geography, the United States held 84.12% of regional revenue in 2025, whereas Mexico is poised to post the quickest 4.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Personal Care Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong emphasis on self-grooming drives the market | +0.8% | Strongest in United States urban centers | Medium term (2-4 years) |

| Technological advancement supports the market | +0.6% | North America and other developed markets | Long term (≥ 4 years) |

| Influence of social media platform and celebrity endorsement | +0.4% | United States and Canada; spillover to Mexico | Short term (≤ 2 years) |

| Rising popularity of cordless rechargeable styling tools among travelers | +0.3% | Concentrated in business-travel hubs | Medium term (2-4 years) |

| Deterring oral health drives the market | +0.2% | North America; aging demographics | Long term (≥ 4 years) |

| Growth of smart personal care appliances | +0.2% | United States and Canada early adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strong emphasis on self-grooming drives the market

Post-pandemic workplace dynamics have transformed grooming investment trends. The adoption of hybrid work models has created dual grooming requirements for virtual meetings and in-person engagements. Professional appearance expectations now extend beyond traditional office settings to include home-based video conferencing, driving demand for efficient styling appliances that ensure consistent results throughout the day. Metropolitan regions, particularly Toronto, Ontario, which recorded 3,674.2 thousand employed individuals in February 2024, according to Statistics Canada, exhibit a heightened emphasis on grooming[1]Source: Statistics Canada, "Labour force characteristics, three-month moving average, seasonally adjusted, inactive", www.statcan.gc.ca. The shift toward "camera-ready" grooming has significantly boosted the demand for compact, high-performance devices capable of delivering salon-quality results in minimal time. Consumer spending patterns demonstrate a preference for premium appliances that optimize daily grooming routines while maintaining professional standards. This trend aligns with the broader wellness movement, where personal grooming is perceived as both a self-care practice and a professional investment, supporting higher price points for technologically advanced appliances.

Technological advancement supports the market

Smart connectivity integration represents the next competitive battleground, with manufacturers embedding IoT capabilities to create ecosystem lock-in effects and recurring revenue streams through app-based services. Advanced battery technologies, particularly lithium-ion improvements, have enabled cordless devices to match corded performance while offering superior portability and safety features. Heat management innovations, including ceramic and tourmaline coatings, address long-standing consumer concerns about hair damage while enabling faster styling times. The integration of artificial intelligence for personalized styling recommendations and usage optimization creates differentiation opportunities that extend beyond hardware specifications. Regulatory frameworks, including FDA device classification standards, continue to evolve to accommodate smart features while maintaining safety protocols according to U.S. Food and Drug Administration.

Influence of social media platform and celebrity endorsement

Social media platforms have redefined product discovery and purchasing behavior. Influencer-led demonstrations, supported by integrated e-commerce functionalities, are now driving immediate sales conversions. Additionally, celebrity endorsements have transitioned from traditional advertising to include product co-development collaborations, fostering authentic narratives that align with target audience preferences. The rise of micro-influencers has decentralized product promotion while enabling precise demographic targeting, particularly effective for niche segments like personal care appliances. Moreover, user-generated content and tutorial videos have emerged as key consumer research tools, prompting brands to shift marketing budgets toward content creation and influencer partnerships instead of conventional advertising. However, changes in platform algorithms can significantly affect brand visibility, presenting both opportunities and challenges for businesses heavily reliant on social media marketing strategies.

Rising popularity of cordless rechargeable styling tools among travelers

With the resurgence of business travel and the expansion of leisure travel, there is an increased focus on portable grooming solutions designed to perform reliably across varied electrical infrastructures. Enhanced battery technology has bridged the performance gap between corded and cordless devices, driving greater adoption of cordless options among professional users. Travel-oriented features, such as dual voltage compatibility and compact charging cases, have evolved into standard offerings, reflecting manufacturers' strategic prioritization of mobility. The number of inbound Canadian visitors to the United States was 20.24 million in 2024, according to the International Trade Administration[2]Source: International Trade Administration, “Survey of International Air Travelers Results 2024”, www.trade.gov. Interestingly, the rise of remote work has led to more frequent travel for in-person meetings, boosting demand for appliances that deliver consistent performance regardless of location. Additionally, the complexities of international travel, including differing electrical standards and voltage requirements, continue to drive advancements in universal compatibility features.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced appliances | -0.3% | Mexico; especially price-sensitive segments | Short term (≤ 2 years) |

| Concerns over heat damage and safety | -0.2% | North America; reinforced by regulatory scrutiny | Medium term (2-4 years) |

| Increasing preference for long-term styling treatments | -0.2% | United States and Canada urban markets | Long term (≥ 4 years) |

| Proliferation of counterfeit products | -0.1% | Cross-border e-commerce channels | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High cost of advanced appliances

Premium pricing strategies for technologically advanced appliances create distinct market segmentation, restricting the addressable customer base, particularly during periods of economic uncertainty when discretionary spending is under pressure. The price disparity between basic and smart-enabled devices is often evident, resulting in a value perception gap that many consumers find difficult to justify based on functional advantages alone. Financing options and subscription models are emerging approaches to mitigate price sensitivity; however, their adoption remains limited compared to other consumer electronics categories. Economic challenges and inflationary pressures have shifted consumer preferences toward value-oriented purchases, potentially extending the adoption cycles for premium appliances. Manufacturers face margin pressures as they strive to balance the integration of advanced features with the need for competitive pricing in an increasingly price-sensitive market.

Concerns over heat damage and safety

Consumer awareness regarding heat-related hair damage has grown substantially, driven by social media campaigns and professional stylists promoting heat protection practices. Negative publicity stemming from safety incidents and product recalls continues to impact the perception of high-temperature styling devices. Regulatory oversight, particularly from the Consumer Product Safety Commission, has intensified, imposing stricter testing standards and increasing liability risks for manufacturers. Advancements in temperature control and heat distribution technologies present opportunities to address safety concerns but also introduce higher production costs. Despite the significant investment required, initiatives focused on consumer education and enhanced safety features are critical for sustaining market credibility and driving long-term growth. As consumers become more discerning, brands are compelled to prioritize transparency and safety in their offerings. This shift not only underscores the evolving landscape of the heat styling market but also highlights the delicate balance between innovation and consumer trust.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cordless Innovation Accelerates Despite Corded Dominance

Corded appliances maintain market leadership with 68.12% share in 2025, reflecting established consumer preferences for consistent power delivery and unlimited usage duration. However, cordless devices represent the future growth engine at 2.78% CAGR through 2031, driven by battery technology improvements and changing lifestyle patterns that prioritize mobility and convenience. The performance gap between corded and cordless devices has narrowed significantly, with lithium-ion battery advances enabling cordless tools to deliver comparable power output and styling effectiveness.

Professional users and frequent travelers increasingly prefer cordless options despite higher initial costs, recognizing the operational flexibility and safety benefits of eliminating cord entanglement risks. Charging infrastructure improvements, including fast-charging capabilities and wireless charging integration, address traditional cordless limitations while creating opportunities for ecosystem development. The transition toward cordless dominance appears inevitable, though the timeline depends on continued battery technology advancement and cost reduction initiatives that make cordless options accessible to price-sensitive consumer segments.

By Product Category : Oral Care Disrupts Hair-Styling Leadership

Hair-styling accounted for 32.86% revenue in 2025, underscoring its historical centrality to the personal care appliances market. The segment’s maturity, however, pushes incumbents to differentiate through smart sensors that adjust heat to hair moisture and texture. AI-driven apps now capture user profiles and recommend exact temperature curves, reinforcing brand loyalty and building data moats. As competition intensifies, brands are also exploring collaborations with beauty influencers to amplify their market reach. Moreover, sustainability is becoming a focal point, with brands investing in eco-friendly materials and energy-efficient technologies.

In contrast, oral-care devices, smart toothbrushes, irrigators, and UV sanitizers,are expanding at a 3.14% CAGR, the fastest within the personal care appliances market. Accelerants include aging demographics grappling with gum disease, insurer emphasis on preventive dentistry, and dentists endorsing connected brushing routines that track coverage zones. Subscription brush-head replacements stabilize the manufacturer's cash flow, enabling lower upfront prices. Education campaigns describe unobtrusive links between oral health and systemic conditions such as cardiovascular disease, further legitimizing regular device use. Furthermore, tech giants are eyeing the oral-care segment, hinting at potential collaborations or acquisitions. As a result, traditional players are ramping up R&D to fend off these tech-driven entrants.

By End User: Men’s Grooming Momentum Challenges Women’s Market Leadership

Women purchased 37.92% of devices in 2025, retaining the largest slice of the personal care appliances market demand thanks to established beauty regimens encompassing hair tools, epilators, and facial devices. Marketing historically emphasized feminine aesthetics, color palettes, and salon-grade results. However, men are recording the quickest 3.47% CAGR, fueled by workplace shifts that regard neat appearance as part of professional etiquette. Beard-care culture, shaped by social media, promotes regular trimming, edging, and fade maintenance with precision clippers. As grooming becomes a focal point for many, the demand for high-quality devices is surging. This shift indicates a broader societal acceptance of personal grooming across genders.

Manufacturers answer with charcoal-hued, angular-lined devices packaged with multipurpose guards. Feature sets mirror women’s lines, cordless torque, and waterproof construction, but emphasize rugged design. Simultaneously, the unisex space grows as neutral palettes simplify shelf SKUs and resonate with Gen Z’s rejection of binary branding. Cross-over marketing positions devices as household assets rather than gender-specific items, helping firms squeeze more volume from each core technology platform. As brands innovate, they're not just catering to traditional markets but are also tapping into emerging trends. This adaptability showcases the industry's keen awareness of shifting consumer dynamics.

By Distribution Channel: Online Retail Achieves Dual Leadership

In 2025, digital storefronts accounted for 47.65% of total sales, and with a projected CAGR of 3.78%, they're set to eclipse more revenue by 2031. E-commerce platforms boast advantages like a vast product assortment, peer reviews, price-matching algorithms, and swift one-day shipping. Moreover, they provide brands with invaluable first-party demand data, facilitating ongoing product enhancements. Features like livestream tutorials, augmented-reality try-ons, and chat-based consultations effectively mimic in-store demonstrations on a larger scale. For pricier devices, online platforms offer integrated financing options, broadening their appeal to budget-conscious shoppers. As internet penetration rises in various regions, e-commerce continues to flourish. In 2023, the International Telecommunication Union reported that 94% of Canadians were internet users.

In response, physical retail chains are enhancing the shopping experience: from live styling bars and dental-care kiosks to instant device engraving, they're personalizing purchases in ways online platforms haven't matched. Some manufacturers are employing hybrid strategies, offering exclusive colorways or accessory bundles to brick-and-mortar partners, ensuring they remain visible on shelves. Yet, the inherent advantages of online shopping—like 24/7 availability and seamless checkout—are steering more manufacturer investments towards digital channels.

Geography Analysis

The United States represented 84.12% of regional revenue in 2025, making it the anchor of the personal care appliances market. Saturation means growth chiefly comes from premium upgrades and smart add-ons rather than first-time purchases. Consumers prioritize performance and durability over price, allowing brands to deploy subscription consumables and extended warranty upsells. The FDA and CPSC regulate safety and connected-device claims, raising compliance costs but ensuring consumer trust.

Mexico delivers the highest 4.05% CAGR through 2031. Disposable income growth, urban migration, and influencer culture expose consumers to US grooming trends. Retail infrastructure modernizes via mall openings and cross-border shipping hubs; yet smartphone-driven online shopping accelerates fastest, given high social-media usage. Currency stability and free-trade frameworks keep import duties manageable, though retailers still face logistical hurdles to reach rural areas. Major brands often test value-engineered SKUs priced below premium US lines to seed adoption, then up-sell features as wages climb.

Canada is steady, with consumers valuing eco-labels and energy efficiency. Seasonal extremes spur demand for anti-static hair tools in winter and frizz-control irons in humid summers. Regulations mirror US standards, giving manufacturers scale leverage across both markets. Meanwhile, the Rest of North America, including Caribbean territories, presents niche potential via tourism-driven duty-free outlets and hospitality supply chains.

Competitive Landscape

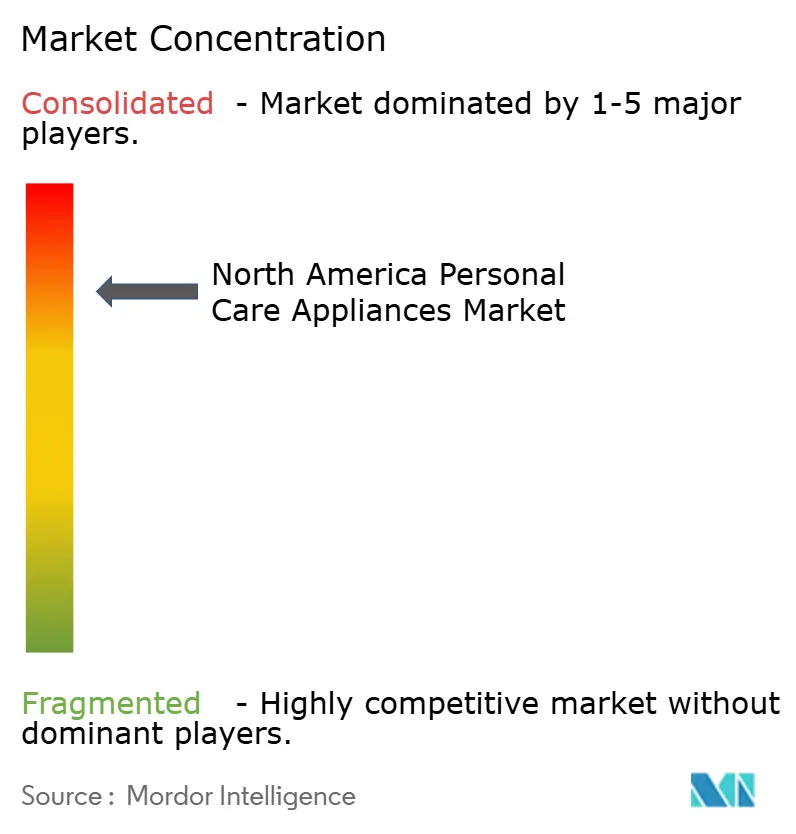

The North American personal care appliances market features a consolidated structure. The key players in the market include Procter & Gamble Company, Panasonic Corporation, Koninklijke Philips N.V., Spectrum Brands, Inc., among others. The leading players in the North American personal care appliances market enjoy a dominant presence across the region. These companies leverage their extensive distribution networks and brand recognition to capture a significant market share. As consumer preferences evolve, these key players are also adapting their product offerings to stay relevant.

Brand loyalty is a high-impact factor, with the features being a prime parameter. Companies need to have a strong focus on quality, and this attribute plays a pivotal role in brand positioning. Companies are increasing their investments in research and development facilities and marketing and expanding their distribution channels to maintain their position in the market and to offer innovative offerings across the region. With the rise of e-commerce, brands are also enhancing their online presence to reach a broader audience. Furthermore, collaborations with influencers and beauty experts are becoming a common strategy to boost brand visibility and trust.

Product launches now bundle cloud dashboards for habit tracking or AI-derived styling feedback. Subscription head-replacement plans mimic printer-ink models, yielding recurring revenue. Brands also explore circular-economy pilots, trade-in credits for old tools, and recycled-plastic housings to satisfy escalating ESG scrutiny. Standards bodies like GS1 refine barcode and packaging norms that support traceability across e-commerce supply chains. Overall, sustaining edge requires harmonizing multiple disciplines: hardware engineering, mobile software, brand storytelling, and agile logistics.

North America Personal Care Appliances Industry Leaders

-

Koninklijke Philips N.V.

-

Wahl Clipper Corporation

-

Panasonic Corporation

-

Spectrum Brands, Inc.

-

Procter & Gamble Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Harry's, the men's grooming brand, unveiled Harry's Plus, its new, next-generation razor system, marking the most significant launch in the brand's history. Culminating a decade of research, development, and engineering, Harry's Plus set a new standard for delivering a premium shaving experience at an exceptional value.

- October 2024: Andis Company has introduced its Explorer Series Trimmers, designed to deliver exceptional comfort and confidence in personal grooming. Engineered specifically for body and groin grooming, the trimmer efficiently addresses challenging and hard-to-reach areas, ensuring safe and comfortable trimming.

- July 2024: MANSCAPED has introduced its latest product, The Dome Shaver Pro Electric Head Shaver. This advanced device incorporates FlexAdjust Technology, designed to adapt to the unique contours of the head. It also includes ultra-thin foils for precise shaving and a five-blade configuration, delivering efficient cutting performance in a single pass.

North America Personal Care Appliances Market Report Scope

The North America personal care appliances market is segmented by gender, type, distribution channel, and country. The market by type is segmented into shaving and grooming, styling, beauty appliances, and oral care. Further the market by gender is segmented into men, women, and unisex. By distribution channel the market is segmented into supermarkets/hypermarkets, specialty stores, online retail stores, and other distribution channels. The market by geography is segmented into United States, Mexico, Canada, and Rest of North America.

By Product Type

| Corded |

| Cordless |

By Product Category

| Shaving and Grooming | Shavers |

| Trimmers | |

| Epilator | |

| Hair Styling | Hair Straightener |

| Hair Dryer | |

| Hair Curler | |

| Others | |

| Beauty Appliances | |

| Oral Care |

By End User

| Men |

| Women |

| Unisex |

By Distribution Channel

| Specialist Stores |

| Supermarkets/Hypermarkets |

| Online Retaile Stores |

| Other Distribution Channels |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Product Type | Corded | |

| Cordless | ||

| By Product Category | Shaving and Grooming | Shavers |

| Trimmers | ||

| Epilator | ||

| Hair Styling | Hair Straightener | |

| Hair Dryer | ||

| Hair Curler | ||

| Others | ||

| Beauty Appliances | ||

| Oral Care | ||

| By End User | Men | |

| Women | ||

| Unisex | ||

| By Distribution Channel | Specialist Stores | |

| Supermarkets/Hypermarkets | ||

| Online Retaile Stores | ||

| Other Distribution Channels | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Key Questions Answered in the Report

What is the current value of the North American personal care appliances market?

The personal care appliances market stands at USD 7.94 billion in 2026 and is projected to hit USD 8.97 billion by 2031.

Which product category dominates sales?

Hair-styling appliances hold the largest 32.86% share of regional revenue, though oral-care devices are expanding fastest.

How important is e-commerce to future growth?

Online retail already accounts for 47.65% of revenue and is growing at 3.78% CAGR, making it the most influential distribution channel.

Which country offers the quickest growth opportunity?

Mexico leads with a 4.05% CAGR through 2031, driven by rising middle-class incomes, social-media influence, and improving retail infrastructure.

Page last updated on: