Market Overview

| Study Period | 2021 - 2031 |

|---|---|

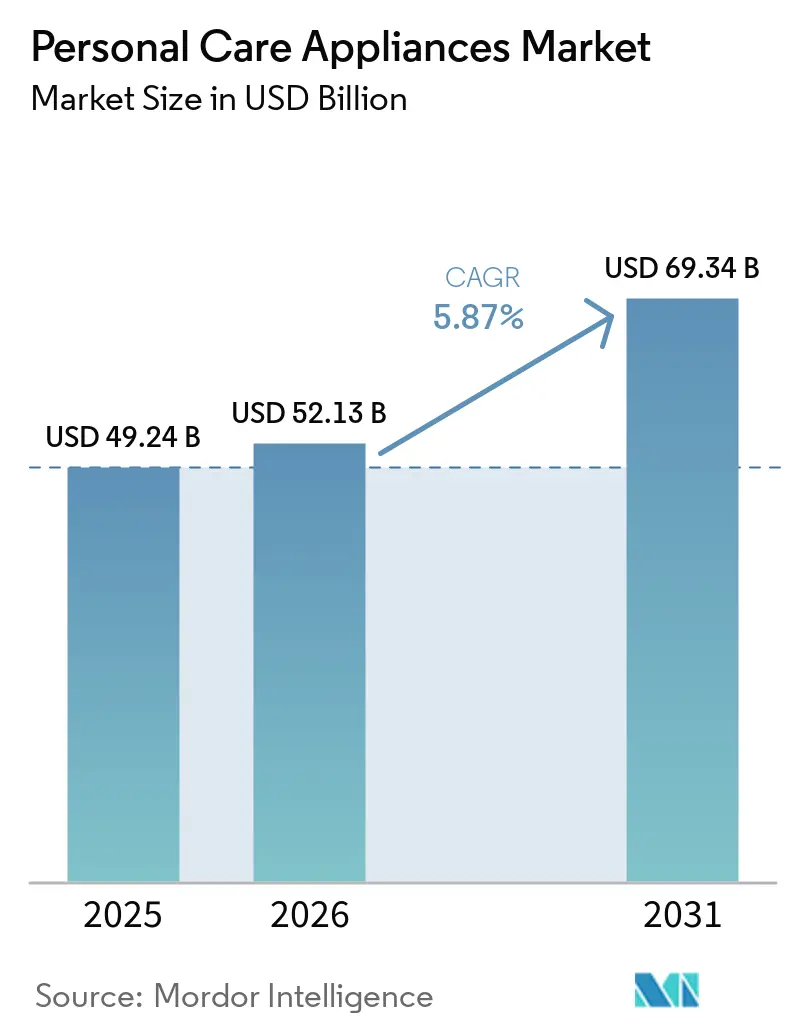

| Market Size (2026) | USD 52.13 Billion |

| Market Size (2031) | USD 69.34 Billion |

| Growth Rate (2026 - 2031) | 5.87% CAGR |

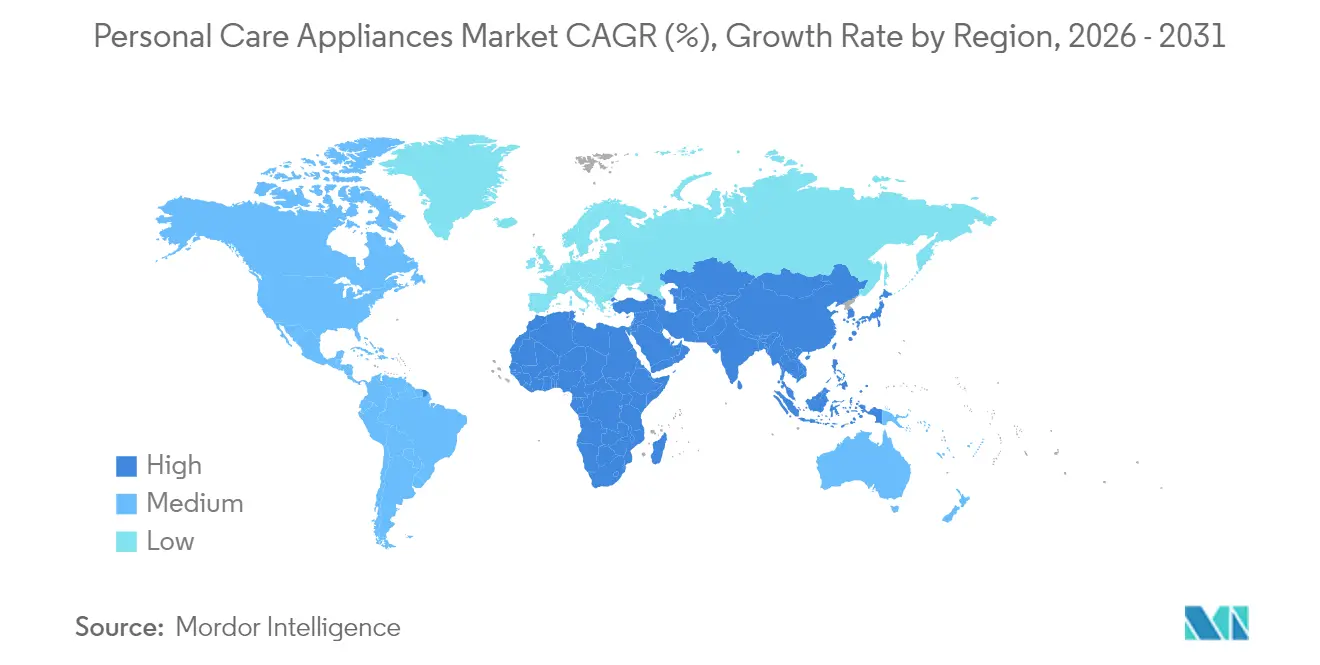

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

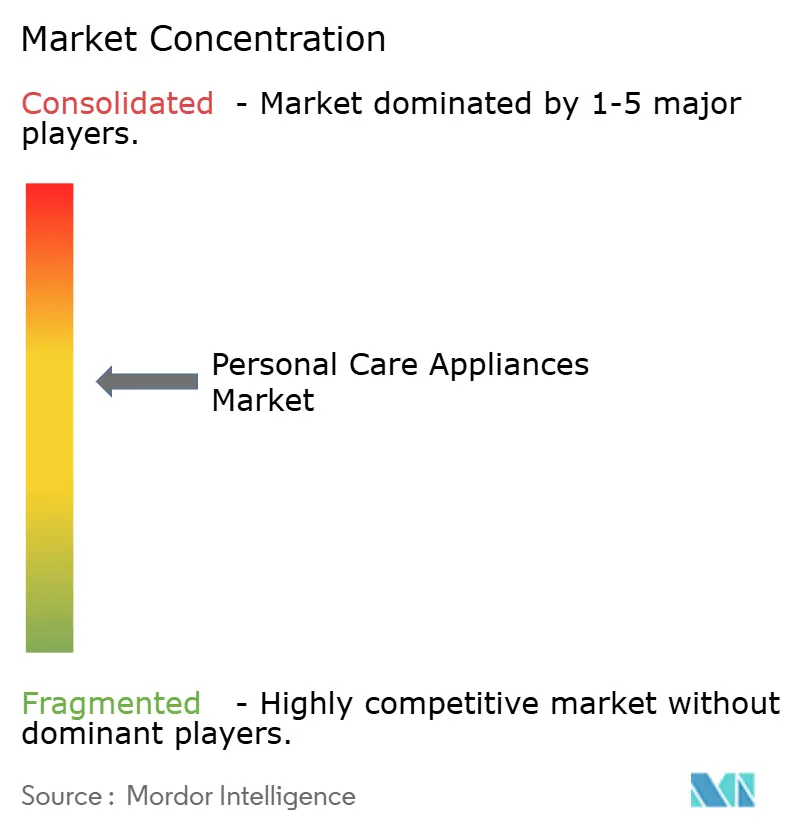

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Personal Care Appliances Market Analysis by Mordor Intelligence

The personal care appliances market size was valued at USD 49.24 billion in 2025 and estimated to grow from USD 52.13 billion in 2026 to reach USD 69.34 billion by 2031, at a CAGR of 5.87% during the forecast period (2026-2031). This growth is being fueled by consumers increasingly prioritizing wellness, rapid urbanization, and the adoption of AI-enabled devices. Leading companies are actively shifting from standalone grooming tools to comprehensive connected ecosystems that provide advanced features such as biometric feedback, subscription-based refills, and cloud-enabled software updates. Aging populations are driving demand for ergonomic designs with easy-grip features, while Gen Z consumers are favoring unisex aesthetics that challenge traditional gender distinctions. Despite the trend toward hardware premiumization, the market faces challenges from counterfeit products and semiconductor supply shortages. These issues are prompting companies to implement dual-sourcing strategies and explore near-shoring options to mitigate risks and ensure supply chain stability.

Key Report Takeaways

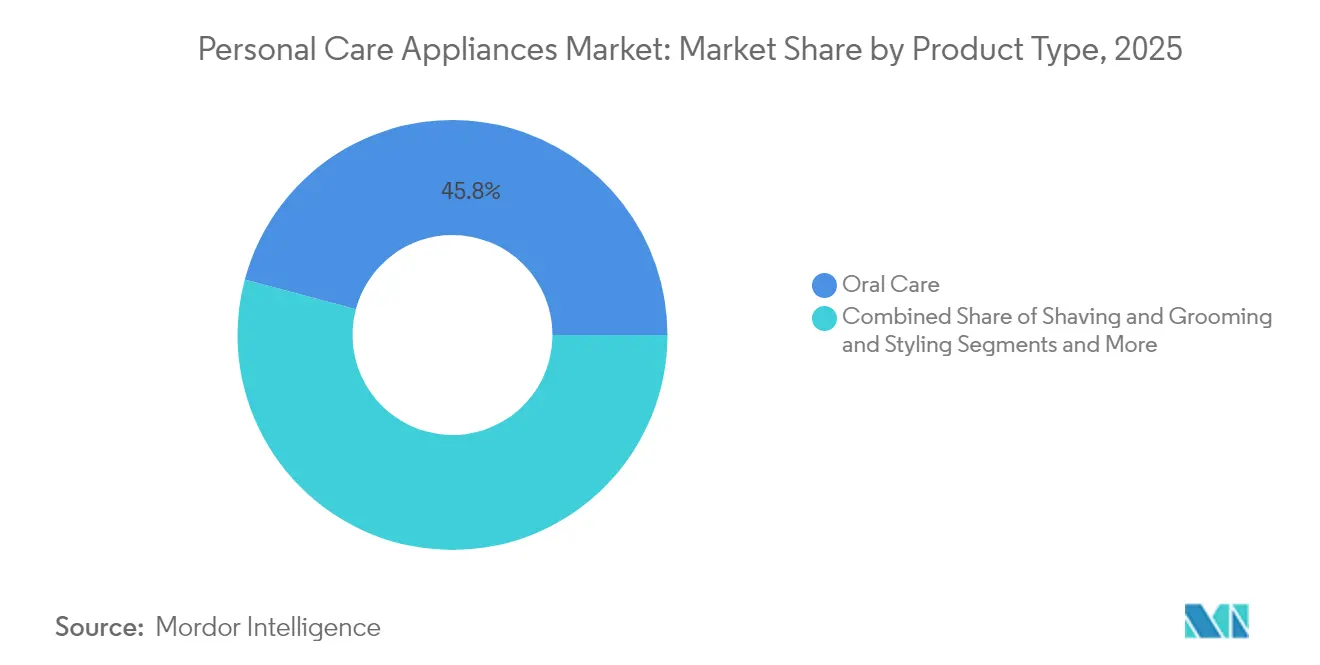

- By product type, oral care led with 45.84% of the personal care appliances market share in 2025; shaving and grooming is forecast to expand at a 6.22% CAGR through 2031.

- By gender, unisex products captured 55.05% revenue in 2025, whereas the men’s segment is advancing at a 6.68% CAGR to 2031.

- By operation, corded devices retained 56.75% of the personal care appliances market size in 2025, while cordless alternatives are projected to grow at 6.55% CAGR.

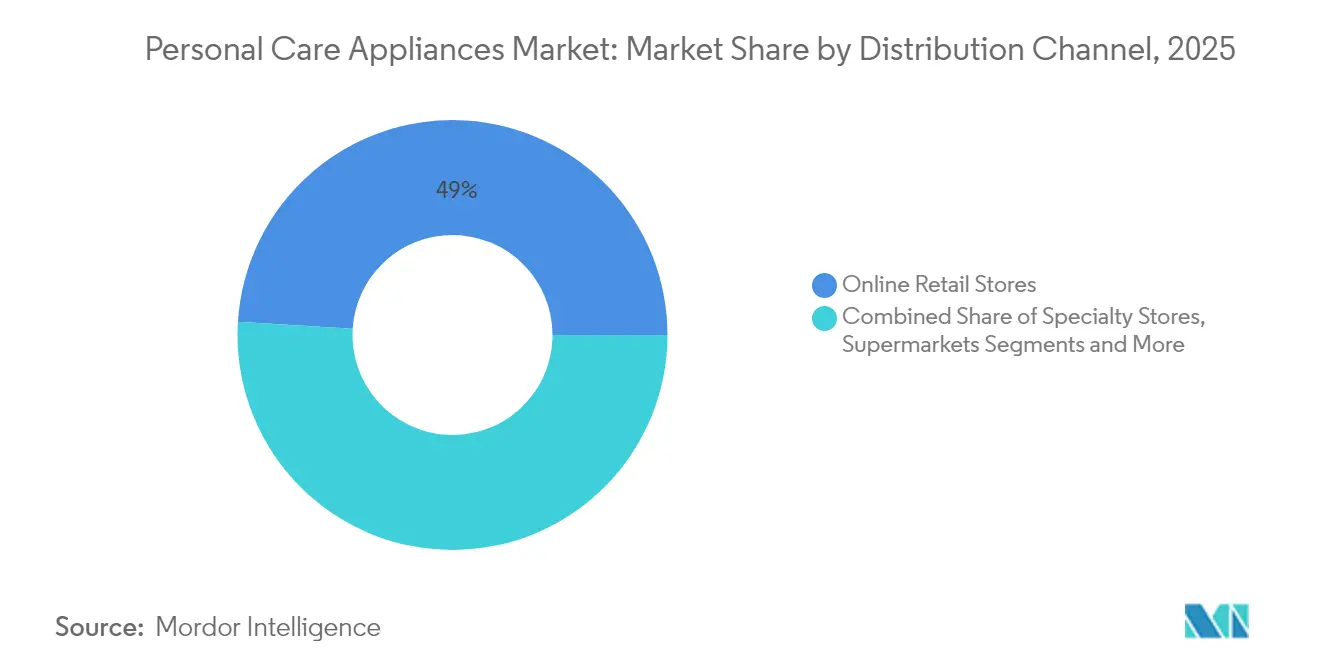

- By distribution channel, online retail accounted for 49.02% of 2025 sales and is set to rise at a 6.9% CAGR over the forecast period.

- By geography, North America controlled 37.95% revenue in 2025, whereas Asia-Pacific is on track for the fastest 6.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Personal Care Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer awareness about grooming, personal hygiene, and wellness | +1.2% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Premiumisation via connected / AI-enabled tools | +1.8% | North America, Europe, Asia-Pacific urban centers | Long term (≥ 4 years) |

| Preference for At-home grooming and DIY solutions | +1.1% | Global, accelerated by pandemic behavioral shifts | Short term (≤ 2 years) |

| Influence of social media and celebrity trends | +0.9% | Global, particularly strong in Asia-Pacific and North America | Short term (≤ 2 years) |

| Demand for eco-friendly and sustainable devices | +0.7% | Europe, North America, with growing Asia-Pacific adoption | Long term (≥ 4 years) |

| Aging population driving demand for ergonomic devices | +0.8% | North America, Europe, Japan with spillover to developed Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising consumer awareness about grooming, personal hygiene, and wellness

Consumers are increasingly prioritizing grooming, personal hygiene, and wellness, which is driving the growth of the personal care appliances market. The rising awareness about maintaining a well-groomed appearance and adhering to hygiene standards has led to a surge in demand for products such as electric shavers, trimmers, hair dryers, and other grooming tools. Additionally, the growing emphasis on wellness and self-care routines has encouraged consumers to invest in advanced personal care appliances that offer convenience and efficiency. This trend is further supported by the influence of social media, where grooming and wellness are frequently highlighted, motivating individuals to adopt these practices. Furthermore, the increasing disposable income levels, particularly in emerging economies, have enabled consumers to spend more on premium and technologically advanced personal care appliances. The availability of innovative products with features such as cordless operation, rechargeable batteries, and ergonomic designs has further fueled market growth. Moreover, the rising penetration of e-commerce platforms has made these appliances more accessible to a broader consumer base, contributing to the market's expansion. The growing awareness of sustainable and eco-friendly products is also influencing consumer preferences, with many opting for energy-efficient and environmentally friendly personal care appliances.

Preference for At-home grooming and DIY solutions

The pandemic reshaped behaviors, driving consumers to embrace at-home grooming and boosting demand for professional-grade appliances that deliver salon-quality results. SharkNinja exemplifies this trend with its CryoGlow device. Priced at USD 349.99, it combines iQLED technology with under-eye cooling to offer FDA-cleared anti-aging treatments for home use. This trend highlights a broader movement where consumers take control of their wellness routines and avoid traditional service dependencies. L'Oréal responds with its AirLight Pro hair dryer, which uses infrared-light technology to reduce drying time and energy consumption by 31%. Such innovations show how manufacturers integrate professional-grade technology into consumer devices. As consumers recognize the long-term savings of investing in premium appliances over recurring professional services, this trend accelerates. Device makers capitalize on this shift by creating holistic ecosystems that include educational content, personalized recommendations, and community features, replicating professional consultation experiences.

Influence of social media and celebrity trends

Social media platforms and celebrity endorsements significantly drive the growth of the Personal Care Appliances Market. The widespread use of social media has transformed how consumers discover and engage with personal care products. According to the University of Maine, in 2023, social media users worldwide reached 4.8 billion, accounting for 59.9% of the global population and 92.7% of all internet users [1]Source: University of Maine, "Social Media Statistics Details", umaine.edu. This massive user base highlights the extensive reach and influence of social media in shaping consumer preferences and purchasing decisions. Influencers and celebrities often showcase their preferred personal care appliances, creating aspirational trends that resonate with their followers. This trend has led to increased consumer awareness and demand for innovative and premium personal care appliances. Additionally, brands leverage social media campaigns and collaborations with celebrities to enhance their visibility and credibility, further fueling market growth. The impact of these platforms and celebrity trends is expected to remain a key driver for the market during the forecast period.

Aging population driving demand for ergonomic devices

As the population ages, the demand for ergonomic devices within the Personal Care Appliances Market is surging. This demographic shift is driving the need for appliances designed to cater to the specific requirements of older individuals, such as ease of use, enhanced comfort, and safety features. The number of people aged 60 and older worldwide is projected to increase from 1.1 billion in 2023 to 1.4 billion by 2030 [2]Source: World Health Organization, "Ageing: Global population", who.int, reflecting a significant rise in the aging population. This trend is particularly pronounced in developing regions, where the aging demographic is growing at an accelerated pace due to improved healthcare infrastructure and rising life expectancy. The rapid growth in this age group is creating a substantial demand for personal care appliances that are specifically designed to address the unique challenges faced by older individuals. Ergonomic devices, including electric shavers, hair dryers, and other personal care tools, are being increasingly tailored to meet the needs of this demographic, such as reduced dexterity, limited mobility, and the need for user-friendly designs. Manufacturers are focusing on integrating advanced features like lightweight designs, easy-grip handles, and automated functionalities to enhance usability for this demographic.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong competition from substitute products | -0.8% | Global, particularly intense in price-sensitive markets | Short term (≤ 2 years) |

| Counterfeit products hampering market growth | -0.6% | Global, with highest impact in Asia-Pacific and online channels | Medium term (2-4 years) |

| Limited awareness in rural and low-income segments | -0.4% | Emerging markets, rural areas in developing countries | Long term (≥ 4 years) |

| Regulatory and safety standards | -0.3% | Global, with varying compliance costs across regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong competition from substitute products

Traditional beauty services adapt to technological advancements while maintaining cost efficiency, outpacing premium appliances. Professional salons leverage their scale and expertise to deliver holistic treatments that specialized devices cannot match, particularly in intricate procedures requiring specialized knowledge and tools. Subscription-based beauty services and mobile professionals offer convenient solutions, eliminating concerns about device upkeep and storage while providing social interactions that surpass the solitary use of at-home appliances. Devices from related fields, like smartphones with advanced skin-analysis cameras, increasingly encroach on specialized territories by delivering "adequate" functionality at a slight premium. Generic and private-label products flood the market with basic features at steeply discounted rates, appealing to budget-conscious consumers. These products particularly attract consumers in emerging markets, where constrained disposable income drives a focus on value over advanced features.

Counterfeit products hampering the market growth

Counterfeit product proliferation creates substantial market distortions, with the EU cosmetics sector alone losing EUR 3 billion annually and 32,000 jobs due to intellectual property violations that undermine legitimate innovation investments [3]Source: European Union Intellectual Property Office, "Economic impact of counterfeiting in the clothing, cosmetics, and toy sectors in the EU", www.euipo.europa.eu. Social media platforms inadvertently facilitate counterfeit distribution, with 24% of males aged 16-60 influenced by complicit influencers to purchase fake products, creating consumer safety risks and brand reputation damage. Counterfeit devices often lack proper safety certifications and quality controls, leading to potential user injuries that create negative associations with entire product categories, particularly affecting consumer confidence in emerging technologies like AI-enabled devices. The sophistication of counterfeit operations has improved significantly, making detection increasingly difficult for consumers and requiring substantial investment from legitimate manufacturers in anti-counterfeiting technologies and legal enforcement. E-commerce platforms struggle to implement effective screening mechanisms, allowing counterfeit products to achieve significant market penetration before detection and removal, creating ongoing revenue losses for authentic manufacturers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Oral Care Dominance Faces Grooming Innovation

The oral care segment holds the largest market share of 45.84% in 2025, reflecting deeply established consumer habits and significant regulatory backing from dental health initiatives worldwide. This prominence is largely driven by growing awareness of oral hygiene and sustained government programs promoting dental health. Consumers across various demographics continue prioritizing oral care appliances such as electric toothbrushes and water flossers due to their proven benefits in enhancing dental wellness. In addition, oral care products benefit from strong brand loyalty and extensive distribution networks, ensuring wide accessibility and consistent demand. This segment also enjoys continuous innovation through advanced technology features like sonic cleaning and smart app integration, further solidifying its leadership in the market.

Conversely, the shaving and grooming segment is the fastest growing category, accelerating at a CAGR of 6.22% through 2031, propelled primarily by an expanding male demographic and innovation in premium product offerings. Increasing male grooming awareness and social acceptability have driven a surge in demand for advanced shaving devices, trimmers, and grooming kits. Premiumization trends are strong here, with consumers seeking high-performance, stylish, and multipurpose grooming appliances with smart features. Furthermore, marketing campaigns target younger generations by associating grooming habits with lifestyle and confidence. Technological innovations such as cordless, waterproof, and skin-sensitive appliances are also enhancing the appeal of this segment. This continued growth signals dynamic market shifts where shaving and grooming are emerging as key contributors to the overall personal care appliance industry expansion.

By Gender: Unisex Products Lead While Men's Segment Surges

Unisex products dominate the personal care appliances market in 2025 with a commanding 55.05% market share, reflecting a significant shift in consumer behavior and industry strategy. This substantial share highlights the growing industry recognition that traditional gender boundaries are increasingly restrictive and less relevant to consumer needs. Modern consumers prefer products that offer functional versatility and appeal to a wide audience rather than being confined to specific gender categories. Companies are expanding their product lines and marketing efforts to encompass this inclusive approach, which not only broadens their customer bases but also addresses diverse grooming and personal care needs. Unisex appliances frequently combine features that cater to a broad spectrum of users, providing convenience and efficiency.

On the other hand, the men’s segment is the fastest-growing category, expected to achieve a 6.68% CAGR through 2031, driven largely by social media influence and evolving male grooming habits. The modern male consumer is increasingly engaging in grooming routines that extend beyond traditional shaving to include skincare, hair care, and wellness products—areas historically dominated by female consumers. Social media platforms play a critical role in driving awareness and acceptance of male personal care, showcasing diverse grooming styles and routines. This has matured into a mainstream trend where men seek sophisticated, multipurpose, and premium grooming appliances. Product innovation specifically tailored to men’s needs—such as precision trimmers, beard care devices, and skin-friendly solutions—fuels this accelerated growth. Marketing campaigns now emphasize self-care and confidence-building, making grooming a vital part of many men’s daily rituals.

By Operation: Corded Reliability Versus Cordless Convenience

Corded devices continue to hold a dominant position in the personal care appliances market, commanding a substantial 56.75% market share in 2025. This robust share reflects enduring consumer preferences for products that offer reliable power and consistent performance, attributes especially valued in professional-grade applications. Corded appliances are favored because they provide uninterrupted usage without the worry of battery life, which is critical in environments requiring sustained and powerful operation. Many consumers also trust corded devices for their longer lifespan and perceived durability compared to cordless alternatives. The established infrastructure around corded appliances, including widespread availability and familiarity, further strengthens their market hold.

In contrast, cordless devices represent the fastest growing segment, expanding at a CAGR of 6.55% through 2031, driven by evolving consumer lifestyles that prioritize convenience and mobility. Advances in battery technology, such as lithium-ion improvements and longer battery life, have significantly narrowed the performance gap with corded products. Cordless appliances appeal to users who value the flexibility of use without being tethered by cords, particularly in travel, on-the-go grooming, or in households seeking greater ease of use. The safety benefits of cordless devices, such as reduced risk of cord entanglement, further enhance their desirability. Innovations like fast charging and wireless charging solutions are also increasing adoption by addressing traditional limitations.

By Distribution Channel: Online Retail Transforms Market Access

In 2025, online retail channels dominate the market with a 49.02% share and are projected to grow at a 6.9% CAGR through 2031. This growth demonstrates a significant shift in consumer behavior, as the pandemic accelerated the adoption of digital platforms. Consumers increasingly choose online channels for their convenience, ability to compare products, and direct engagement with brands, which eliminates traditional retail markups. Manufacturers actively use these channels to take control of their brand narratives, collect valuable consumer data, and implement dynamic pricing strategies. By leveraging these advantages, they reduce their reliance on physical retail partnerships, which often restrict market access and limit profit margins. This shift also allows manufacturers to expand their reach and improve profitability by directly connecting with their target audience.

Supermarkets and hypermarkets actively sustain their relevance by offering hands-on product demonstrations and fulfilling the demand for instant gratification. These channels provide consumers with the opportunity to physically evaluate products before purchase, which remains a key advantage over online platforms. Specialty stores attract consumers by delivering expert consultations and positioning themselves as premium outlets. This approach enables them to justify higher price points for complex devices that require professional guidance and personalized service. Additionally, other distribution channels, such as pharmacy and department store networks, continue to cater to specific demographic groups and geographic regions. These channels highlight the enduring strength of traditional retail relationships in serving niche markets, maintaining customer loyalty, and addressing localized consumer needs.

Geography Analysis

In 2025, North America holds a dominant 37.95% market share in the Personal Care Appliances Market, driven by its well-established infrastructure and premium positioning strategies. Consumers in the region exhibit a strong willingness to invest in advanced personal care technologies, often justifying higher price points with superior performance and brand heritage. The region benefits from mature distribution networks and regulatory frameworks that foster innovation, enabling manufacturers to introduce cutting-edge products. Additionally, demographic trends, such as an aging population, are fueling demand for ergonomic and assistive grooming devices. As the market matures, North America's growth trajectory is transitioning from volume expansion to value enhancement, emphasizing technological sophistication and personalized user experiences to cater to evolving consumer preferences.

Asia-Pacific is emerging as the fastest-growing region in the Personal Care Appliances Market, with a projected CAGR of 6.6% through 2031. This growth is underpinned by rapid urbanization, increasing disposable incomes, and the swift adoption of connected devices among tech-savvy consumers. The region's consumers are particularly drawn to AI-enabled personal care solutions, which offer convenience and advanced functionality. Global players, including Chinese small appliance manufacturers, are making significant investments in the region, with many expanding operations to countries like Japan. These investments highlight regional integration trends that optimize supply chains while addressing local consumer preferences, further accelerating market growth in Asia-Pacific.

Europe maintains steady growth in the market, supported by sustainability mandates and regulatory frameworks such as the EU GPSR, which establish stringent quality benchmarks. These regulations favor established manufacturers with robust compliance capabilities, enabling them to maintain a competitive edge. In contrast, South America and the Middle East and Africa represent emerging opportunities, albeit constrained by infrastructure limitations and income disparities. These challenges necessitate value-engineered product strategies that prioritize affordability and basic functionality. Manufacturers operating in these diverse geographic regions must balance global economies of scale with local market adaptation. This dynamic creates opportunities for tiered product strategies, allowing brands to cater to varying economic segments while maintaining consistent brand identity across international markets.

Competitive Landscape

The Personal Care Appliances Market demonstrates a moderate concentration, with a score of 6 indicating a balanced competitive environment. Established players such as Procter and Gamble, Philips, and Panasonic hold a significant share of the market but are increasingly facing competition from emerging technology-driven disruptors and regional specialists. These new entrants are leveraging advanced technologies, particularly AI integration, to develop innovative products and services that cater to evolving consumer demands. By adopting direct-to-consumer strategies, these players are bypassing traditional distribution channels, enabling them to offer competitive pricing and personalized experiences. This shift has intensified competition, compelling established players to innovate and adapt rapidly to maintain their market position.

The market is undergoing a significant transformation, with a growing emphasis on premiumization driven by the rising demand for connected device ecosystems. Manufacturers are making substantial investments in AI capabilities to enhance product functionality and deliver highly personalized user experiences. These advancements are enabling companies to differentiate their offerings and address the increasing consumer preference for smart, efficient, and user-friendly appliances. The integration of smart technologies, such as IoT-enabled devices, is fostering greater consumer engagement by providing features like real-time monitoring, customization, and seamless connectivity. This trend highlights the critical role of technological innovation in shaping the competitive dynamics of the market and meeting the expectations of tech-savvy consumers.

Another prominent trend reshaping the competitive landscape is the adoption of subscription-based service models, which are revolutionizing the revenue streams of manufacturers. By moving beyond traditional hardware sales, companies are creating recurring revenue opportunities through value-added services such as maintenance plans, software updates, and exclusive content. These models not only ensure long-term customer retention but also provide a steady and predictable income stream, making them an attractive strategy for market players. As competition continues to intensify, the ability to combine cutting-edge technology with innovative business models will be a decisive factor in determining success. Companies that can effectively integrate these strategies are likely to gain a competitive edge in the evolving market.

Personal Care Appliances Industry Leaders

-

Koninklijke Philips N.V.

-

Conair Corporation

-

Dyson Limited

-

Panasonic Holdings Corporation

-

Procter and Gamble Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Philips launched the i9000 Shaver Series globally, featuring AI-driven SenseIQ Pro technology for real-time feedback on shaving techniques, representing the company's most intelligent shaver line with models ranging from USD 329.99 to USD 499.99.

- February 2025: SharkNinja unveiled its Shark CryoGlow, an advanced at-home skincare device, priced at USD 349.99. This innovative device integrates iQLED technology with under-eye cooling to enhance skin rejuvenation and features FDA-cleared anti-aging capabilities, offering a comprehensive solution for skincare needs.

- October 2024: Cloud Nine launched its limited-edition Starlight collection of hair styling tools engineered to minimize hair damage during the festive season. The collection incorporated The Original Iron, The Wide Iron, The Curling Wand, The Airshot Hairdryer, The Airshot Pro Hairdryer, The Original Iron Gift Set, and The Wide Iron Luxe Gift Set.

- October 2024: SharkNinja, Inc., a product design and technology company, introduced two new hair styling systems through its Shark Beauty division - the Shark FlexFusion and Shark FlexFusion Straight. These systems enable styling functionality for both wet and dry hair applications.

Global Personal Care Appliances Market Report Scope

Personal care appliances are used to enhance the appearance and maintain the hygiene of an individual. The global personal care appliances market is segmented by gender, type, distribution channel, and geography. By gender, the market is segmented into men, women, and unisex. By type, the market is segmented into shaving and grooming, styling, beauty appliances, and oral care appliances. The shaving and grooming segment is further sub-segmented into shavers, trimmers, and epilators. The styling appliances are also further sub-segmented into hair straighteners, hair dryers, hair curlers, and others. By distribution channel, the market is segmented into, supermarkets/hypermarkets, specialty stores, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, Middle East, and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

By Gender

| Men |

| Women |

| Unisex |

By Operation

| Corded |

| Cordless |

By Product Type

| Shaving and Grooming | Shavers |

| Trimmers | |

| Epilator | |

| Styling | Hair Straightener |

| Hair Dryer | |

| Hair Curler | |

| Others | |

| Beauty Appliances | |

| Oral Care |

By Distribution Channel

| Supermarkets / Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Columbia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Gender | Men | |

| Women | ||

| Unisex | ||

| By Operation | Corded | |

| Cordless | ||

| By Product Type | Shaving and Grooming | Shavers |

| Trimmers | ||

| Epilator | ||

| Styling | Hair Straightener | |

| Hair Dryer | ||

| Hair Curler | ||

| Others | ||

| Beauty Appliances | ||

| Oral Care | ||

| By Distribution Channel | Supermarkets / Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Columbia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the personal care appliances market?

The market stands at USD 52.13 billion in 2026 and is forecast to reach USD 69.34 billion by 2031.

How fast is the personal care appliances market growing?

It is expanding at a 5.87% CAGR over the 2026-2031 period.

Which product category leads sales in personal care devices?

Oral-care appliances hold 45.84% of 2025 revenue, supported by dentist recommendations and insurance incentives

Which region is advancing the fastest in personal care devices?

Asia-Pacific is projected to grow at a 6.6% CAGR through 2031, driven by rising disposable incomes and e-commerce penetration.

Page last updated on: