Latex Medical Gloves Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.91 Billion |

| Market Size (2031) | USD 4.07 Billion |

| Growth Rate (2026 - 2031) | 6.94% CAGR |

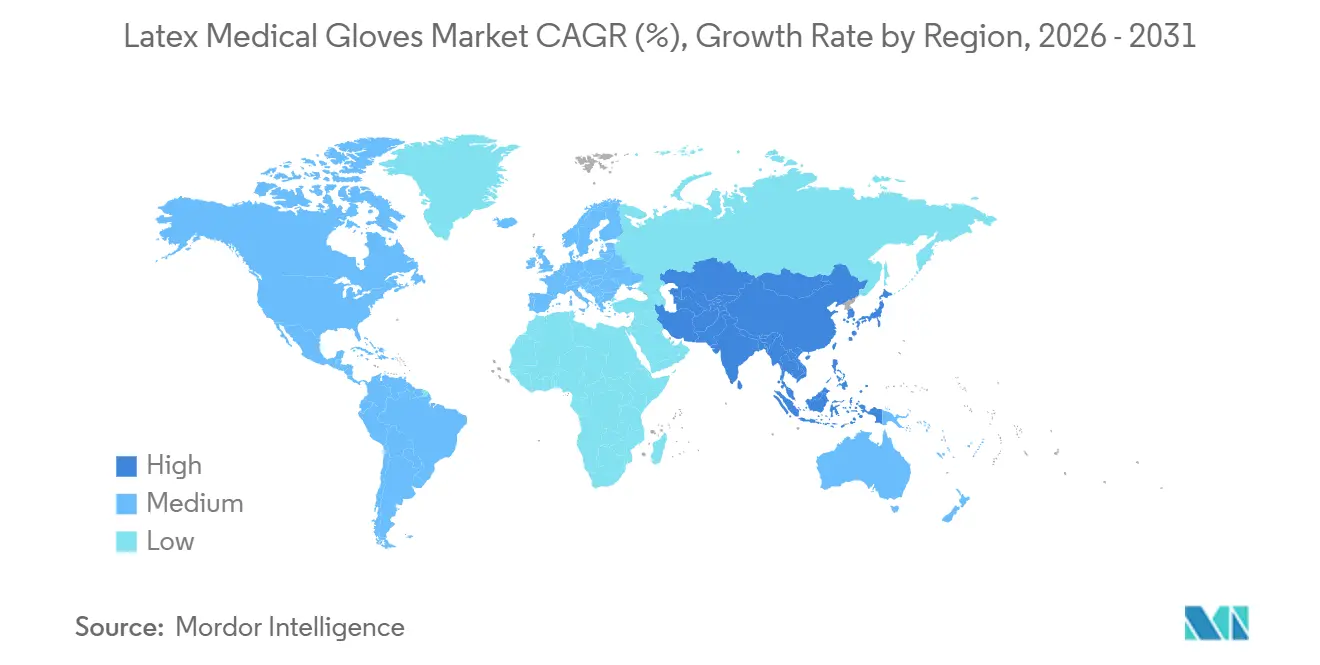

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

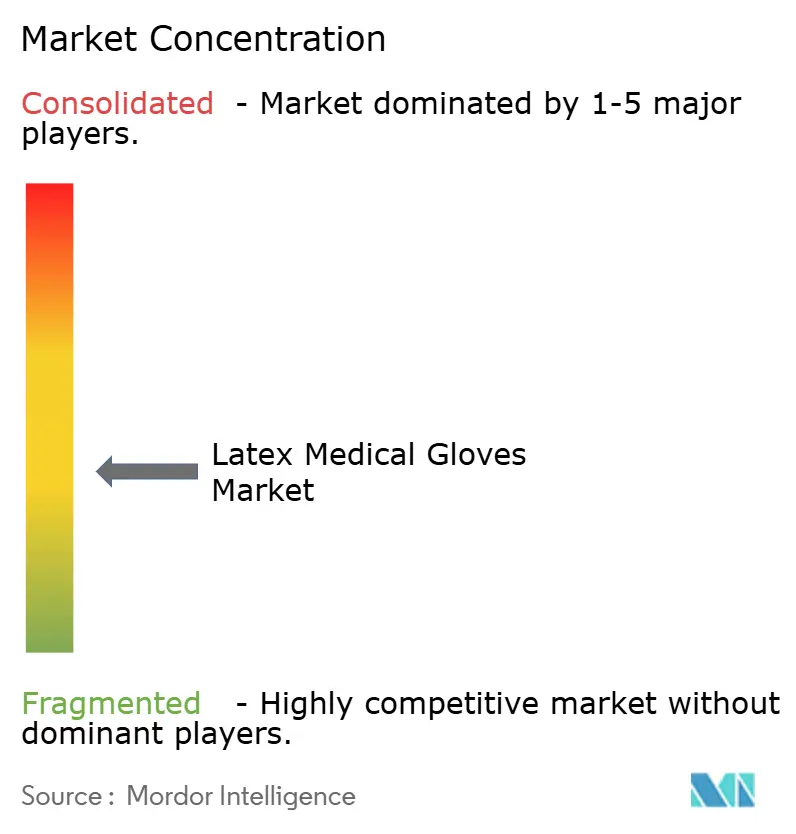

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Latex Medical Gloves Market Analysis by Mordor Intelligence

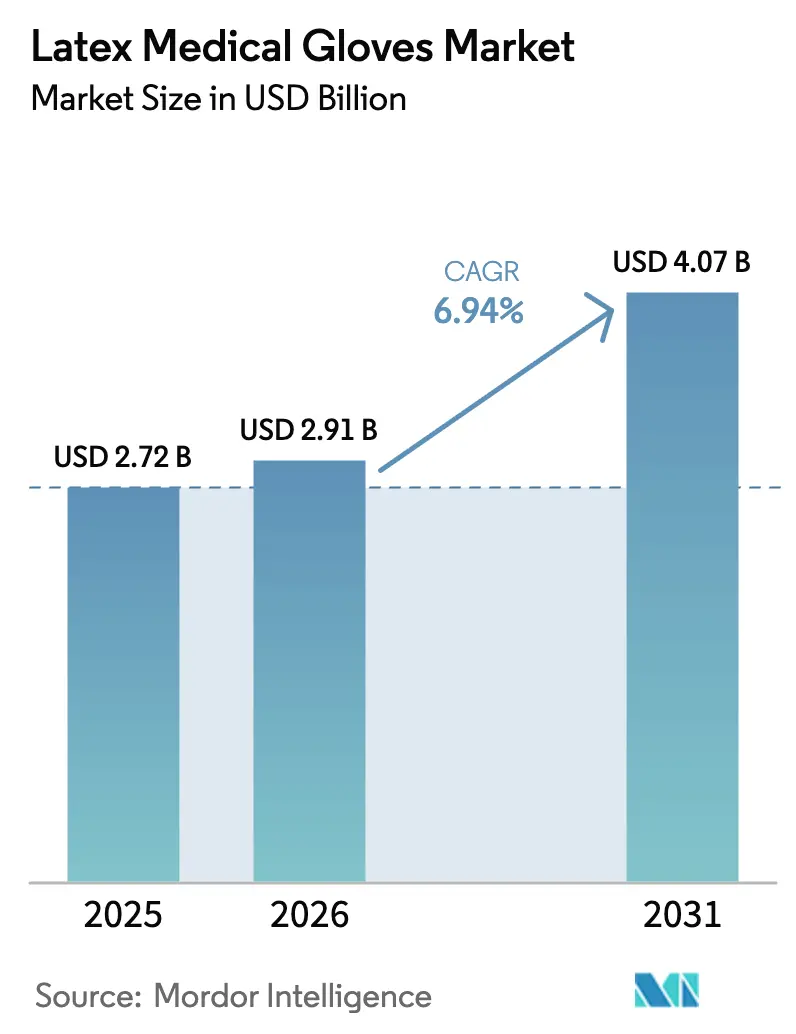

The latex medical gloves market size is expected to grow from USD 2.72 billion in 2025 to USD 2.91 billion in 2026 and is forecast to reach USD 4.07 billion by 2031 at 6.94% CAGR over 2026-2031. Accelerated adoption of powder-free, accelerator-free formulations, widening use of double-gloving in high-risk surgeries, and the rapid build-out of ambulatory surgery centers across emerging Asia are the dominant demand catalysts. On the supply side, Malaysia’s Big Four remain volume leaders, yet Chinese entrants building plants in Vietnam and Indonesia keep average selling prices muted, compelling incumbents to focus on production efficiency and sustainable sourcing. Tariff escalations in the United States, EUDR traceability requirements in Europe, and OSHA guidance favoring nitrile alternatives shape a regulatory landscape that alternately supports and restrains latex consumption. Investment in biodegradable low-protein lines and AI-enabled distribution platforms illustrates how manufacturers and distributors alike respond to cost pressure, sustainability scoring, and hospital demands for continuity.

Key Report Takeaways

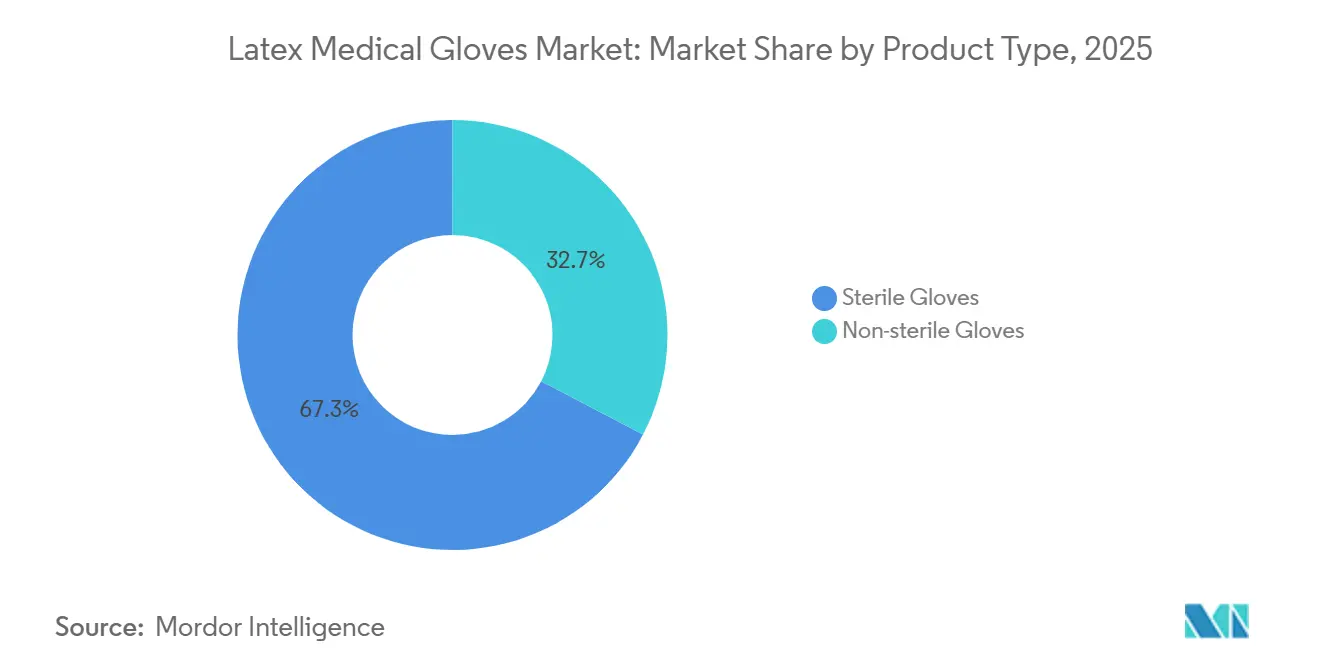

- By product type, sterile gloves captured 67.34% of the latex medical gloves market share in 2025; non-sterile gloves are forecast to rise at a 7.87% CAGR through 2031.

- By form, powder-free gloves held 70.12% of revenue in 2025, while powdered variants will shrink as powder-free products advance at a 7.91% CAGR through 2031.

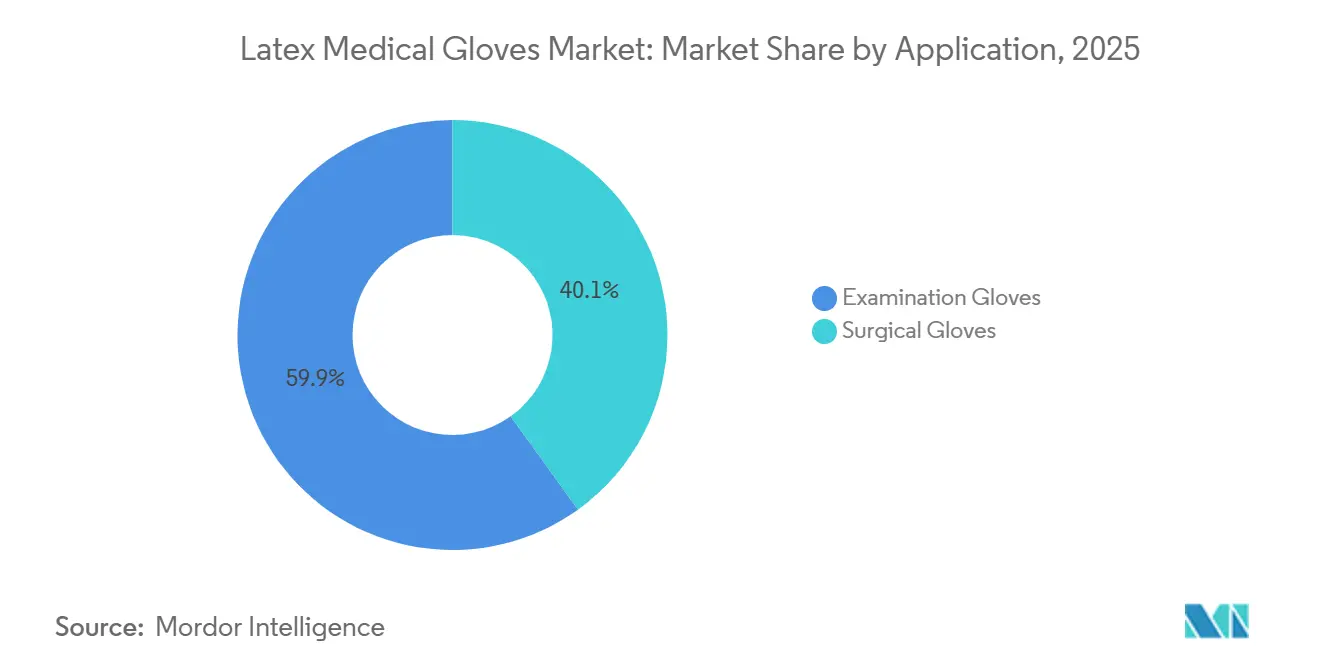

- By application, examination gloves accounted for a 59.91% share of the latex medical gloves market size in 2025, yet surgical gloves are expanding at a 7.98% CAGR through 2031.

- By end user, hospitals dominated with 56.66% of demand in 2025; clinics are set to record the fastest growth at 7.83% CAGR on the back of ambulatory surgery center expansion.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Latex Medical Gloves Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising post-pandemic institutional demand for single-use PPE | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Mandatory double-gloving protocols in high-risk surgeries | +1.2% | North America, Europe, and advanced APAC markets (Japan, South Korea, Australia) | Long term (≥ 4 years) |

| Fast-growing ambulatory surgery network in emerging APAC | +1.5% | APAC core (India, Indonesia, Vietnam, Philippines), spill-over to MEA | Medium term (2-4 years) |

| Top-5 OEMs scaling biodegradable low-protein latex lines | +0.9% | Global, with early adoption in EU and North America | Long term (≥ 4 years) |

| Hospital VMI contracts lengthening to 3–5 years | +0.7% | North America, Europe, and select APAC markets | Short term (≤ 2 years) |

| Carbon-credit incentives for natural-rubber plantations | +0.5% | Southeast Asia (Thailand, Malaysia, Indonesia) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Post-Pandemic Institutional Demand for Single-Use PPE

Global glove consumption normalized to 357 billion pieces in 2024, only 6% below the 2021 peak, yet excess capacity from Chinese plants in Vietnam and Indonesia holds down average selling prices. Hospital groups now emphasize supply resilience, exemplified by Medline’s USD 6.26 billion IPO proceeds earmarked for domestic manufacturing and predictive logistics. The U.S. Department of Justice’s Project Airbridge precedent supports distributor-led coordination that continues to guide procurement rules. Cardinal Health disclosed USD 491 million latex exposure in 2024, confirming raw-material volatility as a margin risk. Front-loading by U.S. buyers ahead of tariff hikes boosted Hartalega’s late-2024 revenue but created a volume trough in early-2025, illustrating how policy uncertainty distorts quarterly demand.[1]U.S. Department of Justice, “Response to McKesson Corporation … Business Review Letter,” justice.gov

Mandatory Double-Gloving Protocols in High-Risk Surgeries

Surgical puncture incidence exceeds 30% under single-layer use, and although WHO guidelines stop short of mandating double-gloving, leading teaching hospitals enforce it, driving higher per-case glove consumption. Surgical-grade gloves featuring puncture-indicator systems are replacing standard white gloves and carry a 10-15% premium. Sri Trang’s 2024 patent for low-zinc-oxide latex reduces metal migration below 5 mg/kg, targeting extended-wear surgical scenarios. CMS proposals that reimburse U.S.-made nitrile but not latex gloves add policy headwinds, yet tactile sensitivity keeps latex favored among surgeons. As hospitals refine infection-control metrics, color-coded indicator gloves are emerging as a de-facto standard in orthopedics and trauma theaters.

Fast-Growing Ambulatory Surgery Network in Emerging APAC

Healthcare spend in Southeast Asia reached USD 156.3 billion in 2021 and will grow 6-10% annually, with ASCs gaining momentum because they require USD 2-5 million in capital versus USD 50-100 million for full hospitals. Single-use glove consumption per ASC procedure remains 40-50% below OECD norms, indicating upside as operating protocols converge. Ansell’s acquisitions of Primus and Kimberly-Clark PPE assets secure branded portfolios and distribution breadth crucial for ASC penetration. ASEAN medical tourism, projected to top USD 100 billion by 2029, will further lift procedure volumes and associated glove demand. Production-linked incentives in India that cut import dependence from 80% to 60% between FY 2022 and FY 2024 testify to policy alignment supporting local glove uptake.

Top-5 OEMs Scaling Biodegradable Low-Protein Latex Lines

Top Glove’s BIOGREEN line achieved 36.7% biodegradation in 513 days, proving that ecological design can coexist with barrier integrity. FSC certification differentiates suppliers in public tenders where sustainability weights reach 20% of scores. SHOWA’s FDA-cleared accelerator-free glove set a benchmark for “Low Dermatitis Potential” claims, widening the premium tier. Clinical data from Thai hospitals show symptomatic reactions dropping from 9.8% to 1.2% when low-protein powder-free gloves replace traditional latex, validating the pricing premium. ISO/TS 5462:2024 now harmonizes test methods, lowering compliance costs for exporters and accelerating roll-outs of new eco-friendly formulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Natural-rubber price volatility & smallholder supply shocks | -1.1% | Global, with acute impact in Southeast Asia (Thailand, Malaysia, Indonesia) | Short term (≤ 2 years) |

| OSHA-driven switch to nitrile in U.S. outpatient clinics | -0.8% | North America, particularly U.S. outpatient and ambulatory settings | Medium term (2-4 years) |

| EU traceability rules raising compliance costs for latex importers | -0.6% | Europe, with spill-over to suppliers in Southeast Asia | Medium term (2-4 years) |

| Surging counterfeit certifications on e-commerce channels | -0.4% | Global, with concentration in unregulated online marketplaces | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Natural-Rubber Price Volatility & Smallholder Supply Shocks

Hartalega’s H1 2024 margins shrank even as revenue climbed 39% because a stronger Malaysian ringgit muted ASP gains and raw-material costs spiked during the wintering season. Smallholders supplying 85% of global latex suffer labor shortages, cutting tapping frequency, while aging tree stock heightens structural under-supply risk. Spot prices surged 15-20% during the May–July 2024 wintering phase, only easing after seasonal recovery. Although Maybank forecasts easing costs, replanting deficits signal recurrent volatility through 2027. Plant consolidations such as Hartalega’s exit from Bestari Jaya underscore a sector-wide pivot toward fewer, more efficient sites to absorb price shocks.[2]European Rubber Journal, “Hartalega ramping up rubber glove production amid signs of demand recovery,” european-rubber-journal.com

OSHA-Driven Switch to Nitrile in U.S. Outpatient Clinics

Latex allergy prevalence among healthcare workers stands at 8-12%, prompting OSHA guidance that favors nitrile gloves for sensitized staff. CMS plans to reimburse a USD 0.13 per-piece premium on U.S.-made nitrile starting January 2026, tilting procurement away from latex. Supermax’s North Carolina nitrile plant will reach 19.2 billion-piece capacity by 2Q 2026, capturing redirected demand. Domestic nitrile output still covers only 0.05% of U.S. needs, but policy incentives shift the growth trajectory. Malaysian suppliers may still fill gaps, yet OSHA guidance means the latex medical gloves market may lose share in U.S. outpatient niches over the forecast horizon.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sterile Gloves Sustain Hospital Revenue Streams

Sterile gloves accounted for 67.34% of 2025 revenue, anchoring high-value contracts across surgical suites. This dominance in the latex medical gloves market reflects regulatory mandates that demand aseptic barriers and justifies ASPs that run USD 0.02-0.05 above non-sterile equivalents. Non-sterile gloves will nonetheless post a 7.87% CAGR as outpatient clinics and diagnostic labs expand, especially in emerging Asia. Shorter 4-6-week lead times give non-sterile producers agility that proved critical during pandemic disruptions.

Sterile production requires gamma irradiation or ethylene oxide cycles, adding capital intensity that favors scale players. Sri Trang’s 2024 launch of a surgical line indicates the strategic pivot toward the 7.98% CAGR surgical segment. ISO 10282 and ISO 11193 distinctions prevent easy cross-over, preserving moats around specialist capacity. Examination of past shortages shows hospitals reluctant to trial off-brand sterile gloves because malpractice liabilities exceed USD 1 million per incident, reinforcing incumbents’ grip on the latex medical gloves market.

By Form: Powder-Free Gloves Dominate on Allergy Mitigation

Powder-free variants captured 70.12% share in 2025 and will grow at a 7.91% CAGR through 2031 as institutions phase out cornstarch-dusted alternatives banned by the FDA for surgical use in 2016. Production relies on chlorination or polymer coatings that raise costs 8-12%, yet these gloves meet low-dermatitis criteria prized by European tenders. Powdered gloves linger in veterinary and food service but will gradually cede ground.

Top Glove’s ElastiCore accelerator-free line and SHOWA’s FDA-cleared low-dermatitis glove demonstrate how product innovation supports premiums. A Thai clinical study showed symptomatic reactions falling from 9.8% to 1.2% after switching to low-protein powder-free gloves, validating hospital purchasing preferences. As procurement teams rationalize SKUs, inventory simplicity further tilts volume toward powder-free in the latex medical gloves market.

By Application: Surgical Gloves Gain Ground Through Protocol Mandates

Examination gloves represented 59.91% of sales in 2025, yet surgical gloves are forecast to outpace them at 7.98% CAGR as double-gloving proliferates. Indicator-color systems boost per-pair pricing by 10-15% but slash puncture detection time, contributing to infection-control scores that purchasing committees monitor closely. ISO performance thresholds—tensile strength ≥24 MPa and elongation ≥650%—raise manufacturing requirements, but higher ASPs of USD 0.20-0.40 make the segment attractive.

Examination gloves, with unit costs under USD 0.05 in mega-volume contracts, remain essential in basic patient contact across acute and outpatient settings. Yet OSHA-driven nitrile substitution threatens latex share in U.S. clinics, even as global preference for tactile sensitivity keeps latex dominant elsewhere. Manufacturers hedge by maintaining balanced portfolios that meet diverging regional standards within the latex medical gloves market.

By End User: Clinics Lead Growth While Hospitals Anchor Volume

Hospitals consumed 56.66% of gloves in 2025, averaging 2,000-3,000 pairs per bed annually and engaging in 3-5-year vendor-managed inventory deals that secure continuity. Clinics, including ASCs, will post a 7.83% CAGR to 2031 as emerging-market networks multiply due to lower capital barriers. Diagnostic labs supply a steady but smaller demand base, while home healthcare climbs with aging demographics.

Medline’s 98% retention rate and 2,000-truck MedTrans fleet illustrate how distribution depth cements supplier choice, raising switching costs for hospitals. ASCs focus on per-procedure cost, favoring examination-grade gloves unless surgical protocols dictate otherwise. Specialty segments such as veterinary and cleanroom applications remain niche at <5% volume but deliver 20-30% price premiums in the latex medical gloves market.

Geography Analysis

North America retained 40.01% share in 2025 as U.S. tariffs on Chinese gloves rose from 7.5% to 50% and will reach 100% in 2027, diverting orders to Malaysian and Thai producers. Hartalega captured roughly 13% of U.S. demand in FY 2026, and its sales now comprise 53% of group revenue. CMS incentives for U.S.-made nitrile cast uncertainty over latex imports, yet near-term supply gaps ensure continued inflows.

Asia-Pacific is the fastest-growing region at 8.01% CAGR, fueled by ASEAN’s 685.4 million population and medical tourism revenue that could exceed USD 100 billion by 2029. Malaysia still supplies 45% of global output, but Chinese “+1” strategies in Vietnam and Indonesia face new U.S. tariffs of 46% and 32%, respectively, announced April 2025. India’s production-linked incentives, reducing import reliance to 60% by FY 2024, signal growing domestic capacity.

Europe accounts for roughly one-fifth of demand; the EUDR adds USD 0.005-0.010 per glove for traceability, favoring vertically integrated suppliers. Middle East and Africa will expand 7.2-7.5% CAGR on over USD 50 billion GCC healthcare investment, yet fragmented logistics temper premium uptake. South America, led by Brazil, consumes 5-6% of global volume, with public tenders prioritizing low cost.

Competitive Landscape

Top Glove, Hartalega, Kossan, and Supermax held significant share in 2023, signaling moderate concentration as pandemic-era capacity swells depressed their combined dominance. Top Glove still commands about 26% of global volume but battles lower ASPs amid Chinese overcapacity. Hartalega’s decommissioning of Bestari Jaya in 2023 and land acquisition for NGC 1.5 in 2025 reflect an industry shift toward efficient mega-complexes.

Ansell’s USD 640 million purchase of Kimberly-Clark’s PPE lines adds Kimtech and KleenGuard, bolstering cleanroom penetration where margins exceed commodity gloves by up to 25 points. Medline leverages Microsoft’s AI to refine demand forecasting, embedding itself deeper in hospital workflows and squeezing smaller distributors. Intellectual-property strategies, such as Sri Trang’s low-zinc patent, illustrate how niche technical upgrades create pricing power in a price-pressured latex medical gloves market.

White-space growth resides in home healthcare and veterinary niches, where consumption per visit trails hospital norms by 30-40%, offering volume upside. Automation, predictive analytics, and sustainability certifications serve as differentiators as price competition intensifies.

Latex Medical Gloves Industry Leaders

Cardinal Health

McKesson Medical-Surgical Inc.

Valutek Inc

SHIELD Scientific

Ansell Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Medline Industries finalized its IPO, raising USD 6.26 billion to fund vertical integration and AI logistics.

- September 2025: Hartalega guided for flat FY 2026 revenue despite 357 billion global glove demand, citing suppressed ASPs.

- May 2025: Hartalega purchased 60.57 acres in Sepang for NGC 1.5, adding 19 billion-piece capacity.

- April 2025: USTR unveiled reciprocal tariffs of up to 154% on Chinese medical gloves, while Malaysia faces 24%.

Global Latex Medical Gloves Market Report Scope

As per the scope of the report, latex is a natural material extracted from flowering plants. It can also be artificially manufactured by polymerizing a monomer, such as styrene emulsified by surfactants. It is utilized to manufacture latex gloves for surgical and physical examination purposes. Latex gloves are widely used in healthcare practices and are popular among medical professionals. Latex gloves are biodegradable and provide a high level of touch sensitivity and high elasticity. The latex medical gloves market is segmented by product type (sterile gloves and non-sterile gloves), applications (examination gloves and surgical gloves), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (USD) for the above segments.

| Sterile Gloves |

| Non-sterile Gloves |

| Powder-free Gloves |

| Powdered Gloves |

| Examination Gloves |

| Surgical Gloves |

| Hospitals |

| Clinics |

| Ambulatory Surgery Centers |

| Diagnostic Laboratories |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Sterile Gloves | |

| Non-sterile Gloves | ||

| By Form | Powder-free Gloves | |

| Powdered Gloves | ||

| By Application | Examination Gloves | |

| Surgical Gloves | ||

| By End User | Hospitals | |

| Clinics | ||

| Ambulatory Surgery Centers | ||

| Diagnostic Laboratories | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the latex medical gloves market?

The market stands at USD 2.91 billion in 2026 and is projected to reach USD 4.07 billion by 2031.

How fast is global demand expected to grow?

Demand is forecast to rise at a 6.94% CAGR through 2031 driven by hospital contracts, ASC expansion, and sustainability innovation.

Which region offers the fastest growth opportunity?

Asia-Pacific leads with an 8.01% CAGR thanks to medical tourism and rapid ASC expansion across ASEAN economies.

Why are powder-free gloves gaining market share?

Institutional buyers prefer powder-free, accelerator-free latex because they minimize hypersensitivity reactions and comply with FDA bans on powdered surgical gloves.

How do U.S. tariff policies affect sourcing strategies?

Tariffs up to 100% on Chinese gloves and 24-36% on some Southeast Asian suppliers steer procurement toward Malaysian and Thai producers in the near term.

What role does sustainability play in purchasing decisions?

FSC certification, biodegradability, and EUDR compliance now influence up to 20% of tender scoring in European public procurement, favoring suppliers with robust traceability programs.

Page last updated on: