Europe Wearable Medical Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 11.86 Billion |

| Market Size (2030) | USD 24.19 Billion |

| Growth Rate (2025 - 2030) | 15.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Wearable Medical Devices Market Analysis by Mordor Intelligence

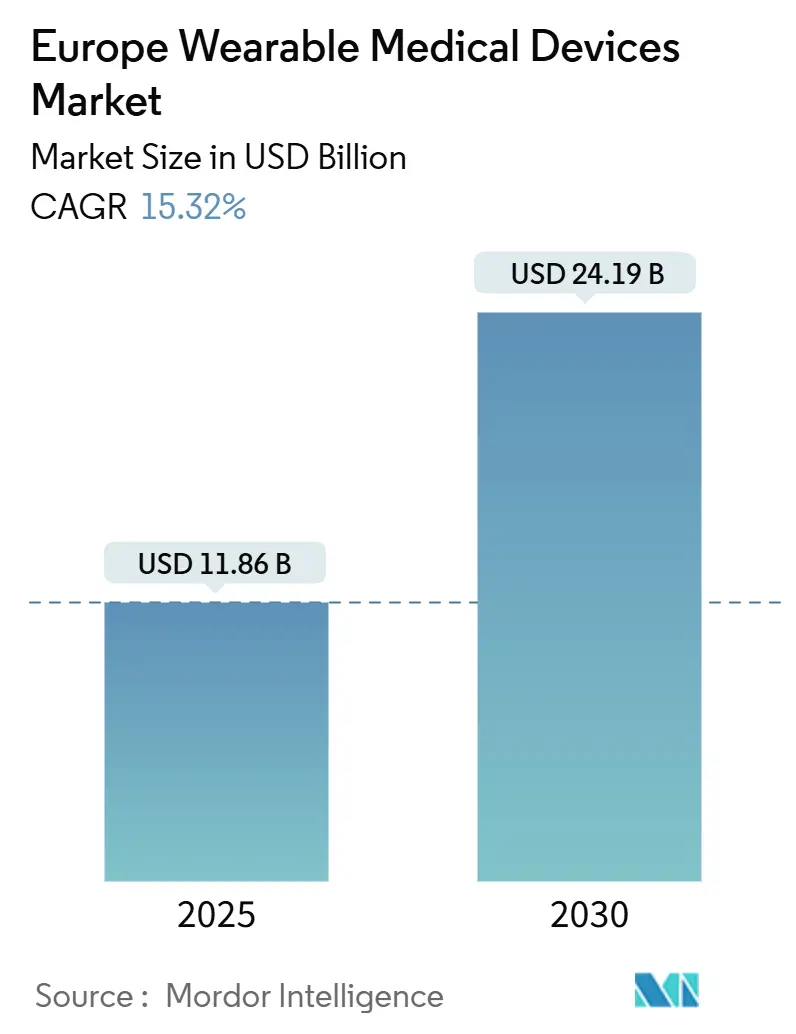

The Europe Wearable Medical Devices Market size is estimated at USD 11.86 billion in 2025, and is expected to reach USD 24.19 billion by 2030, at a CAGR of 15.32% during the forecast period (2025-2030).

Ongoing regulatory harmonization under the Medical Device Regulation (MDR), the increasing prevalence of chronic diseases, and workforce shortages are driving the adoption of continuous monitoring across both clinical and consumer settings. National reimbursement frameworks—most notably Germany’s Digital Care Act—are recasting clinically validated wearables as prescribable therapies rather than wellness accessories, while EUR 403 million in fresh EU innovation funding is accelerating product pipelines for next-generation devices. Supply-chain diversification, energy-harvesting breakthroughs, and multimodal sensor stacks are lowering form-factor barriers and enabling longer device lifespans. At the same time, fragmented post-GDPR data-sharing rules and concerns about physician accuracy temper near-term momentum, keeping clinical validation central to market expansion strategies.

Key Report Takeaways

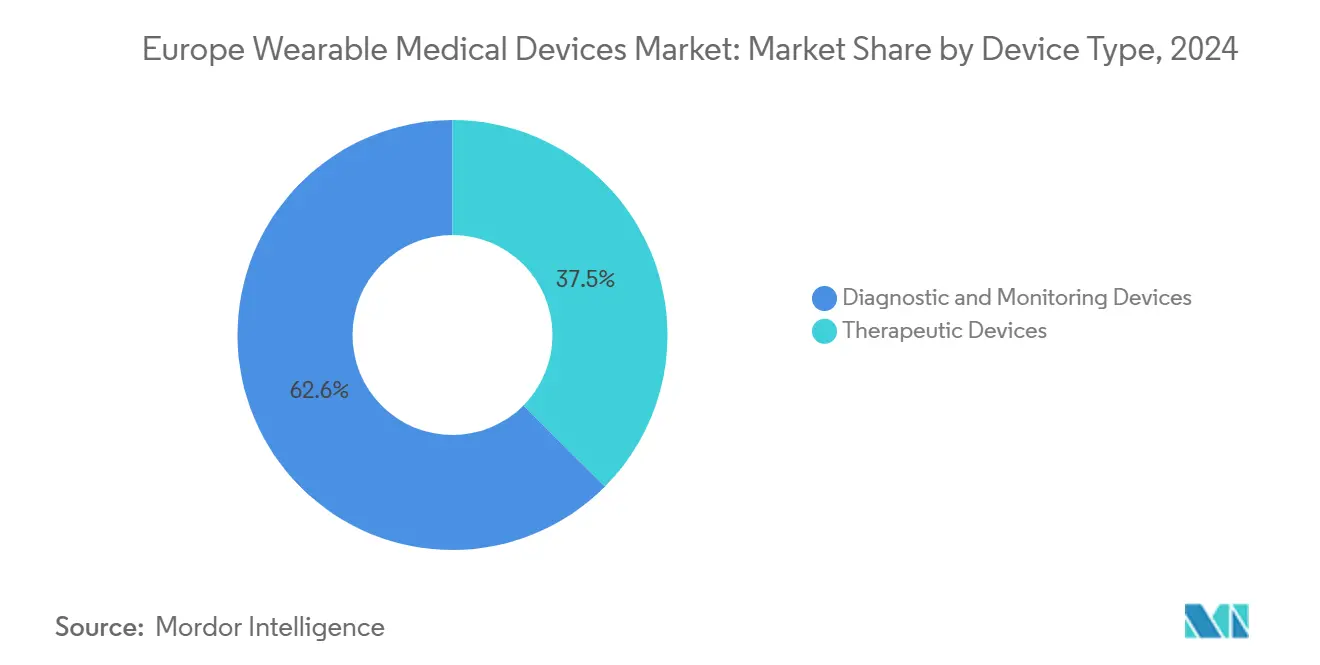

- By device type, diagnostic and monitoring wearables accounted for 62.55% of the European wearable medical device market share in 2024; therapeutic wearables are forecasted to expand at a 15.73% CAGR through 2030.

- By age group, the under-18 segment was the fastest-growing cohort at a 16.29% CAGR between 2025 and 2030; the 18-60 group retained 60.22% of the European wearable medical device market size in 2024.

- By distribution channel, offline vendors accounted for 53.39% of revenue in 2024, while online channels are expected to expand at a 15.50% CAGR during the forecast horizon.

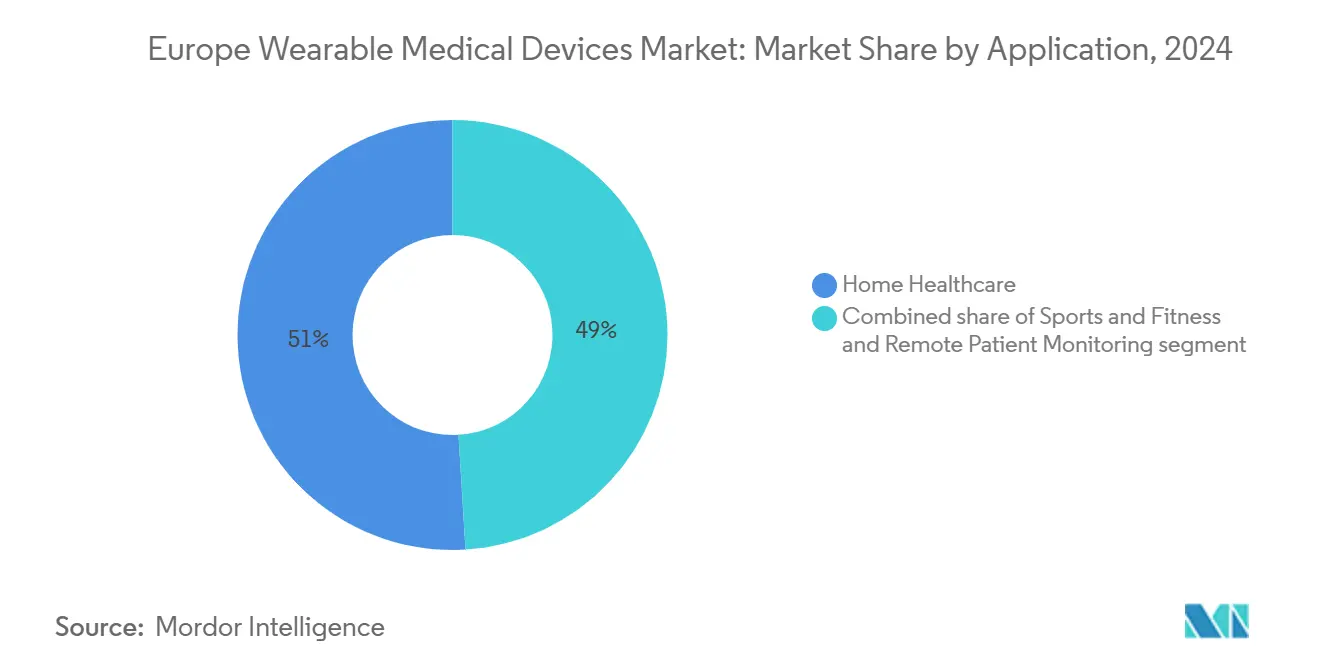

- By application, home healthcare accounted for 50.96% of the European wearable medical device market share in 2024, while sports and fitness applications are projected to advance at a 15.84% CAGR through 2030.

- By end-user, consumers held 63.07% of the European wearable medical device market share in 2024 and are forecast to grow at a 15.61% CAGR to 2030; hospitals and clinics remain the second-largest buyers.

- By geography, Germany led with 28.37% revenue share in 2024, whereas the United Kingdom is expected to post the highest 15.94% CAGR through 2030.

Europe Wearable Medical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory push for MDR-approved medical wearables | 2.80% | EU-wide (strongest in Germany, France) | Medium term (2-4 years) |

| Rapid sensor miniaturization & multimodal chips | 2.10% | Global, EU manufacturing hubs | Long term (≥ 4 years) |

| Employer-funded corporate wellness programs | 1.90% | Germany, UK, Netherlands | Short term (≤ 2 years) |

| Healthcare payer shift to outcomes-based models | 1.60% | Nordic countries, Germany, UK | Medium term (2-4 years) |

| Micro-energy harvesting to remove charging friction | 1.20% | Global, EU R&D leadership | Long term (≥ 4 years) |

| EU digital therapeutics reimbursement pilots | 0.90% | Germany, France, Netherlands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Push for MDR-Approved Medical Wearables

MDR enforcement since 2021 has made Europe wearable medical device market entrants prove clinical performance, transforming wearables from lifestyle gadgets into regulated medical tools. Heightened post-market clinical follow-up requirements[1]Medical Device Coordination Group, “MDCG 2023-7 Practical application of Article 61,” HEALTH.EC.EUROPA.EUDriverscreate continuous data loops that improve algorithmic accuracy, but longer certification timelines favor capital-rich incumbents. Material-safety clauses are prompting shifts toward biocompatible polymers, spurring sustainable design innovations. Collectively, these factors enhance physician confidence and raise entry barriers for small, non-specialist startups.

Rapid Sensor Miniaturization & Multimodal Chips

Micro-fabrication has enabled single chips to track multiple vitals, reducing device bulk and broadening use cases. Trinity Biotech’s CGM+ integrates continuous glucose, temperature, and hydration sensing into a coin-sized patch, illustrating this shift. Power draw has fallen to microwatt levels, extending battery life and paving the way for energy-harvesting modules. The design freedom encourages diverse form factors—from adhesive patches to implantable—expanding the European wearable medical device market adoption among pediatric and geriatric cohorts.

Healthcare Payer Shift to Outcomes-Based Models

National payers are linking reimbursements to clinical endpoints, incentivizing device makers to supply outcome data rather than raw metrics. Germany’s DiGA pathway[2]Lasse Cirkel, “Adoption and perception of prescribable digital health applications (DiGA) and the advancing digitalization among German internal medicine physicians: a cross-sectional survey study,” Lasse Cirke, bmchealthservres.biomedcentral.com , for example, reimburses apps and devices only after proven patient benefit, fostering stronger algorithm development and long-term patient engagement. By monetizing event avoidance—such as reduced emergency admissions—the model ensures sustained device usage and underpins the European wearable medical device market’s double-digit trajectory.

EU Digital Therapeutics Reimbursement Pilots

Germany’s “Fast-Track” DiGA approvals[3]Robby Bräuniger, “The Digital Health Market in Germany,” Germany Trade & Invest, gtai.de have sparked copycat pilots across France and the Netherlands, creating progressive reimbursement blueprints. More than 50 apps and wearables now qualify for statutory coverage, signaling future harmonization of digital-therapy funding. Integrating continuous sensor data with behavioral interventions elevates wearables from monitoring tools to first-line therapies, widening the Europe wearable medical device market reach.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented EU data-sharing rules post-GDPR | -1.8% | EU-wide (most complex in Germany) | Short term (≤ 2 years) |

| Supply-chain risk from China-centric battery vendors | -1.3% | Global, EU vulnerability | Medium term (2-4 years) |

| Plateauing early-adopter replacement cycles | -0.9% | Germany, UK, Netherlands | Short term (≤ 2 years) |

| Clinical-grade accuracy skepticism among physicians | -0.7% | Conservative EU health systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented EU Data-Sharing Rules Post-GDPR

National differences in GDPR interpretations oblige manufacturers to redesign consent flows for each market, delaying pan-EU launches. Providers remain wary of integrating continuous data into electronic records due to liability exposure and privacy litigation risk. These siloes impede predictive analytics models that rely on transnational data sets, curbing Europe's wearable medical device market scalability until harmonized guidance emerges.

Clinical-Grade Accuracy Skepticism Among Physicians

A 2024 systematic review[4]Melanie Rabe, “Use of Patient-Generated Health Data From Consumer-Grade Devices by Health Care Professionals,” Journal of Medical Internet Research, jmir.org found that physicians have limited reliance on consumer-derived vitals due to their inconsistent accuracy, especially in uncontrolled environments. Training gaps and liability concerns hinder data-driven care pathways, underscoring the need for robust validation studies and standardized accuracy metrics before the widespread clinical integration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Diagnostics Drive Clinical Integration

Diagnostic and monitoring wearables accounted for 62.55% of the European wearable medical device market share in 2024, confirming hospital and payer priorities for continuous surveillance over on-device therapy. The subsegment is projected to grow at 15.73% through 2030, driven by the prevalence of chronic diseases and post-discharge monitoring mandates. Continuous glucose monitors spearhead growth, benefiting from improved catalytic enzymes and wireless calibration. Vital-sign patches now bundle ECG, SpO₂, and respiratory-rate sensing, lowering equipment budgets for tele-ICU programs. Therapeutic wearables remain a niche market but show promise in neuromodulation and closed-loop insulin delivery. Energy-autonomous stimulators and patch pumps are reducing patient burden and encouraging broader adoption in endocrinology. These trends cement the European wearable medical device market as a cornerstone of predictive, outpatient-centric care.

Therapeutic devices own the remainder of the segment share and are pivoting toward condition-specific algorithms that titrate therapy in real time. Pain-management platforms combine electrical stimulation with biometric feedback, addressing opioid-reduction mandates. Respiratory wearables equipped with AI cough classifiers have found post-COVID-19 utility, while rehabilitation exosleeves transmit range-of-motion telemetry to physiotherapists. Segment differentiation now revolves around clinical evidence, algorithm transparency, and MDR compliance—factors that define winning positions within the European wearable medical device market.

By Age Group: Youth Adoption Accelerates

Users aged 18-60 accounted for 60.22% of the European wearable medical device market size in 2024, driven by employer wellness subsidies and digital-first insurance products. However, under-18 adoption is expanding at a 16.29% CAGR, aided by parental demand for pediatric diabetes sensors and school-based wellness programs. Designs featuring gamified dashboards and child-sized wear bands improve engagement, lowering attrition rates. For seniors, interface simplicity and energy harvesting are paramount. Night-time fall-detection pendants and low-dexterity charging cradles target common geriatric pain points. As EU demographics skew older, long-term adoption hinges on caregiver integration and reimbursement-backed remote monitoring—both of which are pivotal to the European wearable medical device market.

Clinicians report higher adherence among digital-native minors compared to seniors, creating longitudinal data sets that bolster preventive-care algorithms. Policy makers view early-life monitoring as a lifetime cost-saving lever, reinforcing government funding for pediatric trials. Across all groups, personalized coaching rooted in behavioral science is lifting sustained device engagement, a critical KPI for recurring-revenue business models in the European wearable medical device industry.

By Distribution Channel: Clinical Validation Drives Offline Preference

Offline channels held 53.39% of the European wearable medical device market share in 2024 as prescribers, pharmacies, and specialist retailers provide fitting, calibration, and MDR-required paperwork—all essential to clinical acceptance. Hospitals frequently bundle devices into discharge kits, boosting offline sales while reducing readmission penalties. Meanwhile, online channels are advancing at a 15.50% CAGR, supported by telehealth expansion and e-prescription integrations. Direct-to-consumer portals feature symptom checkers, virtual onboarding, and AI-powered chat support, providing scalable educational resources. Cross-border e-commerce faces regulatory frictions; however, streamlined VAT processes and CE-mark equivalence with UKCA may widen its reach, sustaining online gains within the European wearable medical device market.

As AI chatbots handle first-line support, online platforms are reducing operating costs, allowing manufacturers to price-match brick-and-mortar outlets. However, a lack of physical fitting can hinder sensor accuracy, prompting hybrid models where users collect devices in pharmacies after making an online purchase. The channel mix is expected to converge toward equilibrium, optimizing convenience and clinical credentialing for Europe wearable medical device market buyers.

By Application: Home Healthcare Dominance Reflects Care Model Evolution

Home healthcare captured 50.96% of the European wearable medical device market size in 2024 as health systems shift care to lower-cost settings. Hospital-at-home pilots pair vital signs patches with nurse dashboards, slashing inpatient costs and freeing up bed capacity. Chronic-care bundles for heart failure and COPD include escalation triage protocols, demonstrating payer savings that reinforce Europe's penetration of the wearable medical device market. The sports and fitness segment, although smaller, is growing at the fastest rate of 15.84% CAGR as clinical-grade sensors migrate into wellness wearables. Partnerships between sports apparel brands and sensor OEMs are trailblazing the use of evidence-backed performance analytics, blurring the boundaries between consumer and medical applications.

Remote patient monitoring (RPM) straddles the realms of medicine and wellness, serving as a proving ground for reimbursement models tied to event reduction. Device makers must navigate dual compliance lanes—medical device directives and consumer data regulations—while delivering actionable insights. The ability to plug into tele-rehab and virtual care ecosystems will determine the long-term relevance of each application cluster within the European wearable medical device market.

By End-User: Consumer Empowerment Drives Market Growth

Consumers accounted for 63.07% of 2024 revenue as MDR-cleared devices became ready for self-care on the shelf. Companion apps translate clinical vitals into user-friendly dashboards, fueling habit-forming daily engagement. Subscription analytics and cloud services are expanding average revenue per user, underpinning profitability across the European wearable medical device market. Hospitals and clinics, the second-largest cohort, deploy wearables for post-operative surveillance, enabling earlier discharge and cost avoidance. Long-term care facilities leverage continuous vital signs tracking to mitigate staff shortages, while ambulatory surgical centers adopt single-use sensor patches for same-day recovery oversight.

Enterprise-grade platforms offering multi-patient views, EMR hooks, and audit trails meet institutional governance needs. Consumer OEMs entering the clinical domain must elevate cybersecurity and traceability to the same levels as those required by MDR. Conversely, traditional med-tech players are enhancing user experience guises borrowed from consumer electronics, signaling convergence that will shape competitive intensity inside the European wearable medical device market.

Geography Analysis

Germany held 28.37% of 2024 revenue, anchored by the Digital Care Act's reimbursement engine that positions digitally prescribed wearables as mainstream therapeutic tools. Over EUR 4 billion in hospital digitalization grants have laid the infrastructure for seamless sensor-to-EMR connectivity, fostering systematic adoption. Strict regional GDPR interpretations, however, impose multi-layer consent processes, complicating multinational rollouts. Germany's ageing population and high per-capita health outlays continue to create fertile ground for remote monitoring solutions, sustaining its leadership in the European wearable medical device market.

The United Kingdom, freed from MDR timelines, is shaping a nimble regulatory regime through the MHRA that pledges 12-month approval cycles, undercutting the EU's average. NHS Long Term Plan funding and virtual ward targets are driving the procurement of vital patches and AI arrhythmia detectors, propelling a 15.94% CAGR through 2030. Cloud-native data architectures and centralized procurement frameworks accelerate scale, offsetting Brexit-related supply-chain friction.

France, Italy, and Spain exhibit cautious progress, balancing stringent HTA evidence demands with the mounting burdens of chronicFrance'srance’s reimbursement dossier now includes digital biomarkers, suggesting broader coverage for wearables once their cost-effectivenesItaly'soven. Italy’s mature electronic health record footprint aids regional pilots, albeit with funding disparities across provinces. Spain prioritizes ageing-in-place programs; however, constrained healthcare budgets slow national scale-up. Nordic states, though smaller, serve as living labs for AI-first monitoring models, while Eastern Europe offers greenfield opportunities where mobile-first strategies may leapfrog legacy infrastructures.

Competitive Landscape

Competition is moderate, tilting toward incumbents with robust clinical portfolios and regulatory expertise. Medtronic, Abbott, and Philips hold strong cardiometabolic franchises, leveraging years of post-market data to refine algorithms. Consumer giants Apple and Samsung are progressively gaining CE marks for ECG and blood oxygen functions, eroding traditional medical technology's share. Strategic alliances typify market maneuvering: Dexcom’s USD 75 million equity in ŌURA merges continuous glucose telemetry with lifestyle analytics to deepen patient insights.

Investment is flowing into AI diagnostic layers that transform raw biosignals into actionable predictions. Start-ups specializing in solid-state batteries and energy harvesting are becoming acquisition targets for device majors seeking to eliminate charging as a friction point. Supply-chain reshoring to Europe is emerging as a differentiator as firms respond to battery sourcing risks and increased scrutiny of their carbon footprint. Over the next five years, value capture will hinge on clinical-grade accuracy, evidence-linked reimbursement, and interoperable data ecosystems—elements that define leadership in the European wearable medical device market.

Europe Wearable Medical Devices Industry Leaders

Abbott Laboratories

Apple Inc.

Koninklijke Philips N.V.

Medtronic plc

Samsung Electronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The EU allocated EUR 403 million to medical-device innovators, fast-tracking clinical trials and regulatory filings for next-generation wearables.

- June 2025: PharmaSens and SiBionics partnered to develop a wearable insulin patch pump targeting closed-loop diabetes management.

- November 2024: Dexcom invested USD 75 million in ŌURA to fuse continuous glucose monitoring with holistic health-tracking rings.

- June 2024: B-Secur and Galen Data collaborated on cloud-linked ECG analytics aimed at reducing false arrhythmia alerts in wearable cardiac monitors.

Europe Wearable Medical Devices Market Report Scope

According to the report's scope, wearable medical devices are autonomous devices that can diagnose or monitor medical conditions, often combined with digital health information, and are typically worn on the body. These devices possess features, such as noninvasive physiological sensors, data processing modules, medical feedback, and wireless data transmission capabilities. The European wearable Medical Devices Market is segmented by Device Type (Monitoring Devices and Therapeutic Devices), Application (Sports and Fitness, Remote Patient Monitoring, and Home Healthcare), Product Type (Watch, Wristband, Ear Wear, and Other Product Types), and Geography. The report offers the value (in USD million) for the above segments.

| Diagnostic & Monitoring Devices | Vital-sign Monitoring Devices |

| Sleep-monitoring Devices | |

| Continuous-Glucose Monitors | |

| Blood-pressure Monitors | |

| Other Diagnostic & Monitoring Devices | |

| Therapeutic Devices | Pain-management Devices |

| Rehabilitation Devices | |

| Respiratory-therapy Devices | |

| Insulin-delivery Devices | |

| Other Therapeutic Devices |

| Under 18 |

| 18 - 60 |

| Above 60 |

| Online |

| Offline |

| Sports & Fitness |

| Remote Patient Monitoring |

| Home Healthcare |

| Consumers |

| Hospitals & Clinics |

| Long-term Care Centres |

| Ambulatory Surgical Centres |

| Others |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Device Type | Diagnostic & Monitoring Devices | Vital-sign Monitoring Devices |

| Sleep-monitoring Devices | ||

| Continuous-Glucose Monitors | ||

| Blood-pressure Monitors | ||

| Other Diagnostic & Monitoring Devices | ||

| Therapeutic Devices | Pain-management Devices | |

| Rehabilitation Devices | ||

| Respiratory-therapy Devices | ||

| Insulin-delivery Devices | ||

| Other Therapeutic Devices | ||

| By Age Group | Under 18 | |

| 18 - 60 | ||

| Above 60 | ||

| By Distribution Channel | Online | |

| Offline | ||

| By Application | Sports & Fitness | |

| Remote Patient Monitoring | ||

| Home Healthcare | ||

| By End-User | Consumers | |

| Hospitals & Clinics | ||

| Long-term Care Centres | ||

| Ambulatory Surgical Centres | ||

| Others | ||

| By Geography | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

Key Questions Answered in the Report

Which regulatory factor most strongly boosts adoption of wearable medical devices across Europe?

Full enforcement of the Medical Device Regulation (MDR) positions wearables as clinically validated tools, giving physicians confidence to prescribe devices that meet hospital-grade safety and performance requirements.

How are European employers influencing uptake of medical-grade wearables?

Corporate wellness programs now subsidize devices capable of continuous glucose or cardiac monitoring, linking usage to reduced absenteeism and lower insurance costs

What technological advance is expected to extend device usage without user intervention?

On-board energy-harvesting modules—such as kinetic, thermal, and photovoltaic components—are eliminating the need for routine charging, an especially valuable feature for elderly and chronic-care patients.

Why do clinicians remain cautious about integrating consumer-grade wearables into care pathways?

Concerns persist over variable measurement accuracy and liability exposure; physicians prefer devices backed by peer-reviewed validation studies and standardized accuracy metrics.

How are online sales platforms changing support models for medical wearables?

E-commerce channels increasingly bundle virtual onboarding and AI-driven customer support, allowing users to receive remote fitting guidance and troubleshooting without in-person visits.

Which supply-chain risk has become a focal point for European manufacturers?

Heavy reliance on Chinese lithium-ion battery suppliers poses disruption threats, prompting reshoring initiatives and exploration of alternative cell chemistries within the EU.

Page last updated on: