Medical Beds Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.06 Billion |

| Market Size (2031) | USD 5.36 Billion |

| Growth Rate (2026 - 2031) | 5.73% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

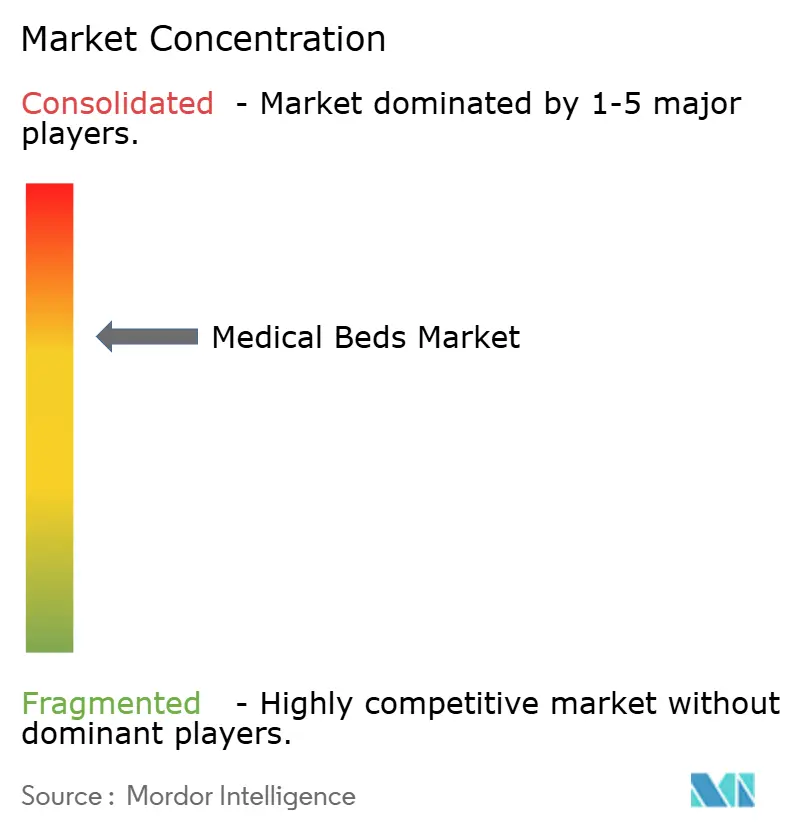

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Beds Market Analysis by Mordor Intelligence

The medical beds market size was valued at USD 3.84 billion in 2025 and estimated to grow from USD 4.06 billion in 2026 to reach USD 5.36 billion by 2031, at a CAGR of 5.73% during the forecast period (2026-2031). Demand is shaped by population aging in developed regions and the broadening of hospital-at-home models that shift part of acute care into residential settings, which elevates the importance of flexible bed fleets in both institutional and home channels. Value-based purchasing frameworks and penalties tied to hospital-acquired conditions have made pressure injury and fall prevention core to capital decisions, which pushes adoption of advanced safety and positioning features. The growing burden of chronic diseases such as diabetes, cardiovascular conditions, and respiratory disorders sustains bed-day utilization and places continuous emphasis on comfort, mobility support, and monitoring readiness. Interoperability of bed-embedded sensors and cybersecurity obligations influence buying criteria in large health systems, since premarket and postmarket expectations for connected medical devices now include robust software bills of materials and vulnerability handling.

Key Report Takeaways

- By product type, general medical beds led with a 28.02% revenue share in 2025, while Intensive Care Beds are projected to expand at a 7.22% CAGR through 2031.

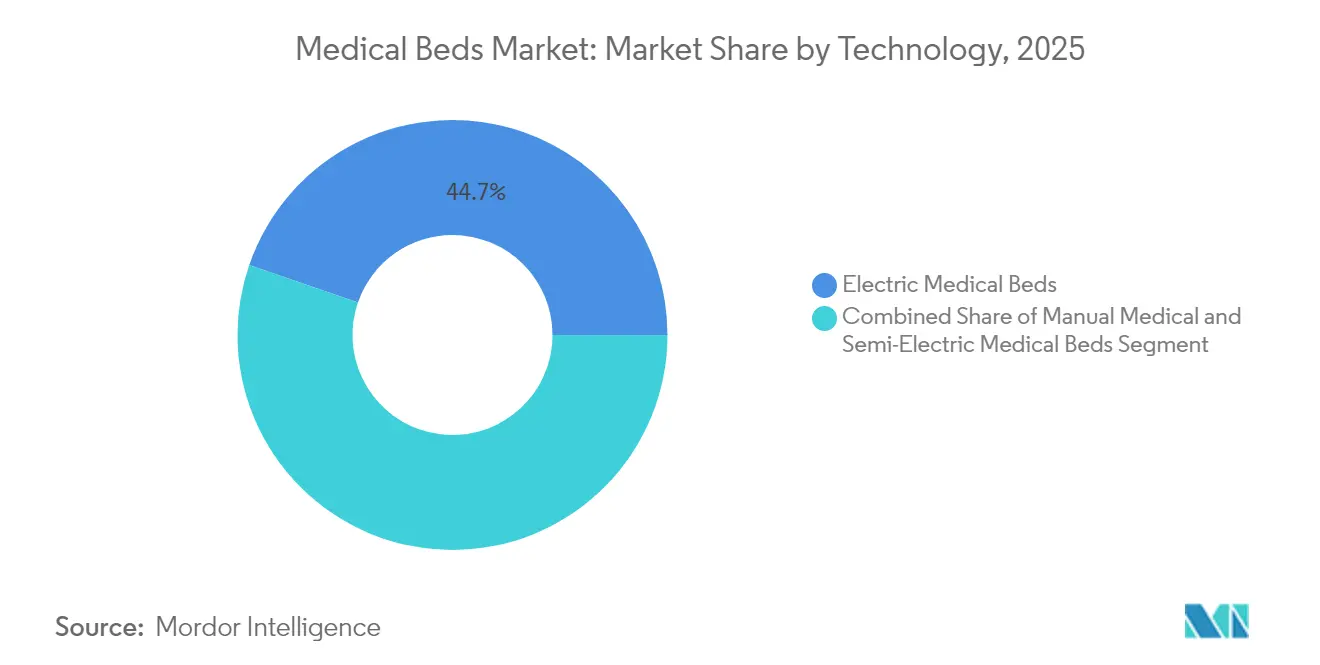

- By technology, electric medical beds held 44.72% share in 2025, while Semi-Electric Medical Beds are forecast to grow at a 7.05% CAGR through 2031.

- By end-user, hospitals and healthcare facilities accounted for 51.84% of the medical beds market share in 2025, while Long-term Care Facilities are projected to record an 8.12% CAGR from 2025 to 2031.

- By geography, North America retained a 41.93% share in 2025, while Asia-Pacific is anticipated to grow at a 6.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Medical Beds Market*

| Drivers Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Aging Population | +1.5% | Global, concentrated in North America, Europe, Japan | Long term (≥ 4 years) |

| Rising Prevalence of Chronic Diseases | +1.3% | Global, with acute pressure in North America, China, India | Medium term (2-4 years) |

| Technological Advancements in Smart Bed Features | +1.2% | North America, Europe, Asia-Pacific urban clusters | Medium term (2-4 years) |

| Rising Demand for Home Healthcare and Hospital-at-Home | +1.0% | North America lead, Europe following, pilot expansion in APAC | Short term (≤ 2 years) |

| Value-Based Harm Penalties Accelerating Safety Tech Adoption | +0.8% | United States, early adoption in UK and Germany | Short term (≤ 2 years) |

| Safe Patient Handling Mandates and Labor Shortages | +0.6% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Aging Population

The share of people aged 65 and older is on track to reach 16% of the global population by 2030, with Japan, Italy, and Germany already above 23% based on 2024 tallies. This aging dynamic raises bed-day intensity due to higher fall risk, reduced mobility, and multiple co-morbidities that require longer inpatient and post-acute stays. In the United States the Medicare-eligible cohort is expanding quickly, which sustains pressure on hospital capacity and skilled nursing bed availability as older patients represent a growing share of admissions. Electric and geriatric beds with low-height profiles, integrated scales, and caregiver-assist features have moved into the mainstream for facilities that concentrate on senior care. Payers and providers see bed technology as part of a strategy to shorten length of stay and to reduce harm events that drive penalties and reputational risk under quality programs[1]International Trade Administration, “Morocco – Healthcare,” trade.gov.

Rising Prevalence of Chronic Diseases

Noncommunicable diseases account for a growing portion of admissions and long-term placements, which anchors steady demand for general medical beds and raises the need for ICU beds that support continuous monitoring. Acute exacerbations of diabetes, COPD, heart failure, and cancer often involve prolonged bed rest followed by staged rehabilitation that benefits from beds designed for frequent repositioning. In emerging economies where the disease burden is moving toward chronic conditions, procurement cycles favor scaled purchases of electric and semi-electric beds to equip new public hospitals. This trend is most visible where government programs are building capacity rapidly with a balance of cost control and functionality. The clinical workflow emphasis on preventing complications aligns with features that mitigate pressure injuries and enhance safer mobilization during recovery[2]Indiana Business Journal, “Made in Indiana: Hospital Beds by Hill-Rom Holdings Inc.,” ibj.com.

Technological Advancements in Smart Bed Features

Modern hospital beds function as data nodes within clinical and operational systems, with sensors for load, pressure, tilt, and bed-exit behavior that can inform both care and staffing decisions. Bed-exit prediction and mobility reminders help reduce the need for continuous observation, which assists teams facing nurse shortages and rising patient acuity. Interfacing with electronic records supports automatic documentation of repositioning intervals, which strengthens compliance posture during audits and claims review. Stryker and Hillrom have expanded deployments of connected bed fleets that enable dashboards with unit-level mobility and turnover metrics, though customers still face integration work because device messaging standards continue to mature[3]Stryker Corporation, “ProCuity ZMX,” stryker.com. Early adopters report improvements in pressure injury incidence and fewer overtime hours in nursing units where bed-connected alerts and documentation are integrated into daily workflows.

Rising Demand for Home Healthcare and Hospital-at-Home

Hospital-at-home models gained traction during the pandemic and remain available under recognized reimbursement pathways in the United States and parts of Europe. Programs require beds that deliver clinical functionality in a smaller footprint with easy-to-use controls for patients and family caregivers. In the United States participation in the Acute Hospital Care at Home program expanded through 2024, and hospital systems continue to manage conditions at home that were traditionally handled inside inpatient wards. Durable medical equipment providers face coordination and margin pressures due to rapid delivery and setup requirements, which increases the value of simplified semi-electric designs for the home setting. Over time the institutional channel is expected to concentrate advanced beds with extensive monitoring while the home channel scales volumes with hybrid feature sets that meet coverage thresholds[4]Oregon Association of Hospitals and Health Systems, “Oregon Hospitals on the Brink,” oregonhospitals.org.

Restraints Impact Analysis of Medical Beds Market*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced Medical Beds (TCO Burden) | -0.9% | Global, acute in price-sensitive markets in LATAM, MEA, South Asia | Medium term (2-4 years) |

| Strict Regulatory Approvals and Safety Standards | -0.5% | Global, higher compliance overhead in United States (FDA) and European Union (MDR) | Long term (≥ 4 years) |

| Limited Reimbursement for Home and Long-term Care Beds | -0.7% | United States and Europe, payer variability in APAC | Medium term (2-4 years) |

| IoMT Interoperability and Cybersecurity Requirements | -0.6% | United States (FDA), European Union (MDR), global for networked devices | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Medical Beds

Advanced ICU and electric beds with integrated rotation therapy and network connectivity come with higher capital outlays than manual or basic semi-electric models. In health systems with limited budgets, these purchases compete with other priorities such as imaging, surgical equipment, and medications, which slows upgrade cycles outside of flagship facilities. Total cost of ownership spans maintenance, parts, software licensing, and staff training, and gaps in onsite biomedical engineering capabilities can extend downtime when vendor service is required. Leasing and rentals can mitigate capital spikes while introducing recurring costs that accumulate over contract periods. The result is a split in adoption patterns, as premium beds concentrate in tertiary and private institutions while mid-tier facilities focus on durable and cost-effective options to expand capacity.

Limited Reimbursement for Home and Long-term Care Beds

Coverage in acute care is well defined, while reimbursement for home and long-term care beds varies by payer and jurisdiction. Medicare Part B reimburses hospital beds for home use when medically necessary, but co-insurance, caps, and documentation rules shape patient affordability and provider workflows. Private coverage often mirrors Medicare criteria, and state-level variability leads to differing access for similar clinical needs. In Europe the range spans comprehensive support in some countries and means testing or waiting lists in others, which complicates supplier forecasting and inventory planning. Manufacturers respond with product tiers that meet medical-necessity thresholds at lower price points while reserving advanced features for institutional buyers where integration justifies the investment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Medical Beds Market Segment Analysis

By Product Type:

General and ICU Segments Drive Divergent Growth PathsGeneral Medical Beds held 28.02% share of the medical beds market size in 2025, reflecting their broad deployment in medical-surgical wards, step-down units, and rehabilitation environments where moderate acuity dominates. These beds emphasize durability, cleanability, and essential features such as height adjustment, Trendelenburg positioning, and standardized side rails that align with fall prevention policies. Procurement in this category concentrates on batch replacement or expansion cycles, where buyers weigh volume discounts, warranty terms, and swap guarantees alongside upfront price. Hospitals running multi-year refresh plans often standardize on a few models to optimize parts inventories and staff training. Pediatric and geriatric models adapt the general form factor to age-specific needs, while birthing beds anchor obstetrics suites with positioning that supports clinical protocols.

Intensive Care Beds are projected to grow at a 7.22% CAGR through 2031 as systems keep critical care capacity above pre-pandemic levels and embed capabilities that support complex monitoring. ICU beds integrate advanced positioning, imaging compatibility, and pass-throughs for cardiac and respiratory devices, which command price premiums tied to their role in high-acuity care. Critical care expansion budgets in Europe, Asia-Pacific, and parts of the Middle East have prioritized ICU additions, which favors suppliers with demonstrated reliability and service coverage. Birthing beds continue to track local birth trends with stable demand in maternity centers, while pediatric and geriatric units serve specialist facilities with design features that reduce anxiety and falls. Surgical or operating room tables and transport stretchers round out the category, with growth aligned to procedural volumes and throughput optimization in perioperative and emergency departments, which continues to shape the medical beds market.

By Technology:

Semi-Electric Beds Gain Ground on Cost-Efficiency AppealElectric Medical Beds accounted for 44.72% share of the market in 2025, driven by automation that reduces caregiver strain and supports precise patient positioning for interventions. These platforms interface with nurse call and EMR systems, and a single button can adjust backrest, knee section, and overall height to suit clinical tasks and patient comfort. Hospitals capture operational gains when automated positioning shortens routine tasks for nursing teams across large wards. Semi-Electric Medical Beds are forecast to grow at a 7.05% CAGR through 2031 as facilities choose hybrid configurations that deliver key ergonomics at a lower purchase price. This balance is attractive to long-term care providers and community hospitals that must scale capacity while controlling capital budgets in the medical beds market.

Manual Medical Beds remain relevant in surge inventories and settings with limited technical support because mechanical simplicity enables long service life and minimal maintenance. Technology selection also mirrors workforce regulations, since safe patient handling rules increase the value of height adjustment and powered movement for injury prevention. Jurisdictions with defined safe patient handling requirements show faster adoption of electric platforms as part of occupational health strategies to lower musculoskeletal injuries among nursing staff. Regions with less prescriptive rules often move toward semi-electric options as a step-up path that balances ergonomics, training needs, and total cost over the useful life of the bed in the medical beds market.

By End-User:

Long-term Care Facilities Emerge as Fastest-Growth ChannelHospitals and Healthcare Facilities accounted for 51.84% share of the medical beds market size in 2025, reflecting higher acuity and strong capital budgets that support premium configurations. Procurement scale via group purchasing organizations and direct contracts supports standardized fleets and predictable replacement cycles, which help large systems manage maintenance and spares. The hospital channel values integration readiness for monitoring and clinical documentation to capture quality metrics and avoid harm-related penalties. Long-term Care Facilities are projected to grow at an 8.12% CAGR through 2031 as aging-in-place policies expand demand for skilled nursing and assisted living beds. Facilities upgrade from manual to semi-electric or electric beds to support caregiver retention and resident safety, which is central to quality ratings and reimbursement in the medical beds market.

Home Healthcare Providers coordinate rentals and purchases for patients transitioning from inpatient stays to home recovery, which drives preference for compact, easy-to-assemble frames with simple control interfaces. The channel is highly fragmented and operates under varied payer rules, which reinforces price sensitivity and emphasis on reliability for transport and setup. Emergency medical services represent a smaller slice of demand, focused on stretchers and transport beds where features center on weight, maneuverability, and compatibility with vehicle restraints. Investments in these categories follow fleet replacement schedules and the integration of lighter materials that support a single-operator lift. Across end-users, facilities that invest in equipment to reduce manual handling report improved staff retention, which underscores the human factors dimension of capital decisions in the medical beds market.

Geography Analysis

North America Medical Beds Market

North America held a 41.93% share of the medical beds market size in 2025, supported by high per-bed technology spend and regulations that link financial penalties to harm events. The Hospital-Acquired Condition Reduction Program in the United States docks reimbursement for pressure ulcers and falls in hospitals with rates above the national median, which strengthens the case for features that reduce injuries and support safe mobilization. Canada and Mexico add growth through public system expansions and private hospital investments, with the region leaning toward replacement and technology refresh rather than net new bed additions. Labor shortages, particularly among nurses and certified nursing assistants, increase demand for automation and monitoring that frees staff time for higher acuity care. Health systems in multiple states have reported persistent vacancy rates, which further integrates bed design into workforce strategies in the medical beds market.

Europe Medical Beds Market

Europe contributed a significant share of 2024 revenue, with Germany, the United Kingdom, France, and Italy as anchors. The European Medical Device Regulation has raised clinical evaluation and postmarket surveillance obligations, which favors companies with the resources to meet documentation and audit requirements. Germany’s DRG framework continues to reward efficiency improvements that shorten turnover times and reduce complications, which supports investment in mobility and prevention features. The United Kingdom’s capital budgets remain tight, which tempers ICU bed replacement outside specialized centers, while southern European countries prioritize adding basic bed counts to improve access. Occupational health rules on safe patient handling vary across countries, which influences the speed of migration from manual to powered platforms in the medical beds market.

APAC, MEA and South America Medical Beds Market

Asia-Pacific is projected to grow at a 6.18% CAGR through 2031, led by infrastructure investment in China, India, and Southeast Asia. China’s Healthy China 2030 blueprint emphasizes expansion of tier-two and tier-three city hospitals, which has led to large tenders that favor suppliers with local assembly or domestic partnerships. India’s Ayushman Bharat program is upgrading health and wellness centers and district hospitals, which pushes demand for semi-electric beds with dependable ergonomics at accessible price points. Japan remains a mature market with replacement demand and advanced monitoring integration driven by its aging demographics, while Australia’s private hospital segment continues to invest in premium configurations. The Middle East and Africa and South America collectively represented less than one fifth of 2024 revenue but show steady expansion as governments fund hospital construction and private operators develop specialty centers that procure ICU and surgical beds to international specifications in the medical beds market.

Competitive Landscape

The medical beds market remains moderately concentrated as the top five manufacturers hold an estimated 45% to 50% global share. Large incumbents leverage scale in R&D, regulatory affairs, multi-country service, and compliance with standards that govern safety and cybersecurity for networked devices. Compliance with home-use design expectations such as IEC 60601-1-11 is increasingly relevant as hospital-at-home models expand, and established players can absorb the associated testing and documentation costs. Competitive strategies often emphasize ecosystems that bundle beds with patient handling equipment, nurse call systems, and analytics, which raise switching costs at the health system level.

Regional specialists such as Japanese and European manufacturers defend share through customization agility and responsive service, which wins public tenders that favor local content and short lead times. Partnerships and local assembly are common for navigating tariffs and currency risk in emerging markets, where scale and delivery reliability shape awards. Product roadmaps show a shift from mechanical innovation to sensor integration and software features, including fall detection and pressure mapping that suggest repositioning intervals. Suppliers that demonstrate secure device connectivity and clear vulnerability management workflows align with tighter regulator expectations for connected devices. These demands shape procurement criteria in the medical beds market as buyer IT teams evaluate device security posture alongside clinical benefits.

Data privacy and health information security considerations increase the importance of standards and frameworks across jurisdictions. In the United States HIPAA requirements govern handling of protected health information, which influences how bed-generated data is stored and share. In Europe GDPR establishes obligations for personal data processing, and vendors document anonymization or pseudonymization approaches to support compliance during analytics and user behavior monitoring. As beds become more deeply embedded in clinical systems, procurement teams assess interoperability alignment with evolving standards for device messaging, along with cybersecurity and data governance for fleet-wide deployments. These themes run across the medical beds market as buyers weigh safety, integration, privacy, and total cost in platform decisions.

Medical Beds Industry Leaders

Baxter International (Hillrom)

Stryker Corporation

LINET Group SE

Paramount Bed Co. Ltd.

Arjo AB

- *Disclaimer: Major Players sorted in no particular order

Medical Beds Market Companies Covered in this Report

- Amico Group of Companies

- Antano Group

- Arjo AB

- Baxter

- Besco Medical Ltd.

- Betten Malsch GmbH

- Drive DeVilbiss Healthcare

- Famed Żywiec Sp. z o.o.

- Favero Health Projects S.p.A.

- Gendron

- Getinge

- GF Health Products, Inc. (Basic American)

- Haelvoet NV

- Howard Wright Ltd.

- Invacare

- Joerns Healthcare

- Stiegelmeyer

- LINET Group

- Lojer Group

- Malvestio S.p.A.

- Medline Industries

- Narang Medical Ltd.

- Paramount Bed Co., Ltd.

- Pardo (Grupo Industrias Pardo)

- Savion Industries

- Stryker

- Völker GmbH

Recent Industry Developments in Medical Beds Market

- July 2025: SonderCare launched certified home hospital beds to support 16 million middle-income seniors facing long-term care crisis.

- February 2025: Agiliti, a manufacturer and provider of medical device solutions to the United States healthcare industry launched Essentia, a versatile, multi-acuity bed frame designed to support a wide range of patients across different hospital settings.

Medical Beds Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the medical beds market as all newly manufactured, patient-care beds sold to hospitals, long-term care centers, ambulatory surgical facilities, and approved home-health distributors. These beds include manual, semi-electric, and fully electric frames fitted with standard side rails, head-and-foot adjustability, and mattress platforms engineered for clinical use.

Furniture such as stretchers, examination couches, rental refurbishments, and non-clinical smart mattresses are not counted, so we stay focused on purpose-built patient beds only.

Segments Covered in This Report

- By Product Type

- General Medical Beds

- Intensive Care Beds

- Birthing Beds

- Pediatric Beds

- Geriatric Beds

- Surgical/Operating Room Beds

- Transport/Stretchers

- By Technology

- Manual Medical Beds

- Electric Medical Beds

- Semi-Electric Medical Beds

- By End-User

- Hospitals & Healthcare Facilities

- Home Healthcare Providers

- Long-term Care Facilities

- Emergency Medical Services

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

We spoke with hospital procurement heads in the United States, Germany, India, and Brazil, senior biomedical engineers at regional distributor networks, and product managers from the top five manufacturers. Their insights on average selling prices, feature adoption curves, and refurbishment cycles helped us reconcile desk findings and stress-test key assumptions.

Desk Research

We first gathered structural inputs from unrestricted tier-1 sources such as WHO hospital-bed density tables, OECD Health Statistics, United Nations demographic yearbooks, and U.S. Centers for Medicare & Medicaid Services capital-spend dashboards, which let us profile installed stock and replacement triggers across regions. Trade association briefs, peer-reviewed journals on pressure-injury prevention, and UN Comtrade shipment codes enriched trend signals on cross-border flows.

Mordor analysts then mined D&B Hoovers for supplier revenues, Dow Jones Factiva for contract awards, and voluntary recall notices to understand pricing and regulatory pivots. This list is illustrative; many additional sources fed into data checks, concept validation, and clarifications.

Market-Sizing & Forecasting

A top-down model converts bed-density norms (beds per 1,000 inhabitants), projected admissions, and average replacement intervals into annual demand, which is then aligned with bottom-up supplier roll-ups and sampled ASP × volume checks. Variables guiding the model include aging population growth, healthcare expenditure per capita, average length of stay, smart-bed penetration rates, regulatory funding for critical-care expansion, and public-private hospital build programs. Multivariate regression with scenario analysis captures how each driver shifts demand, while gap areas in bottom-up tallies are bridged through conservative interpolation of missing country data.

Data Validation & Update Cycle

Outputs run through variance and anomaly screens and a multi-step peer review before sign-off. Reports refresh every twelve months, with interim flashes if material events, such as major reimbursement changes, occur; an analyst re-checks all numbers just before client delivery.

How Mordor Intelligence's Medical Beds Market Size Compares to Other Published Estimates

Published figures often diverge because firms juggle different bed categories, pricing logics, and refresh cadences.

Our team flags these factors up front so users can see where totals might split.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.81 B (2025) | Mordor Intelligence | |

| USD 4.38 B (2025) | Global Consultancy A | Excludes home-health beds and ignores replacement demand |

| USD 5.23 B (2025) | Industry Association B | Adds accessories and rental fleets, uses single-source supplier poll |

| USD 5.29 B (2025) | Trade Journal C | Applies flat ASP growth and updates only every three years |

Taken together, the comparison shows that Mordor's disciplined scope selection, annually refreshed inputs, and dual-track modeling yield a balanced, transparent baseline that decision-makers can retrace with ease.

Key Questions Answered in the Report

What is the current size and expected growth of the medical beds market through 2031 ?

The medical beds market size is USD 4.06 billion in 2026 and is projected to reach USD 5.36 billion by 2031, reflecting a 5.73% CAGR.

Which product categories are leading and growing fastest within the medical beds market ?

General Medical Beds led with 28.02% revenue share in 2025 while Intensive Care Beds are projected to grow at a 7.22% CAGR through 2031.

Which technologies are most adopted by buyers in the medical beds market ?

Electric Medical Beds held 44.72% share in 2025 and Semi-Electric Medical Beds are forecast to expand at a 7.05% CAGR, reflecting the balance between automation and cost.

Which end-user segment is expanding fastest in the medical beds market ?

Long-term Care Facilities are projected to grow at an 8.12% CAGR through 2031, while Hospitals and Healthcare Facilities remain the largest customer group with 51.84% share in 2025.

Which regions show the strongest momentum in the medical beds market ?

North America held a 41.93% share in 2025, while Asia-Pacific is forecast to grow at a 6.18% CAGR through 2031 on the back of sustained infrastructure investment.

What regulations most influence purchasing decisions in the medical beds market ?

Hospitals weigh compliance with harm reduction and safe patient handling policies, as well as device cybersecurity and medical device regulations, which shape feature requirements and integration readiness.

Page last updated on: