Medical Computer Workstation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

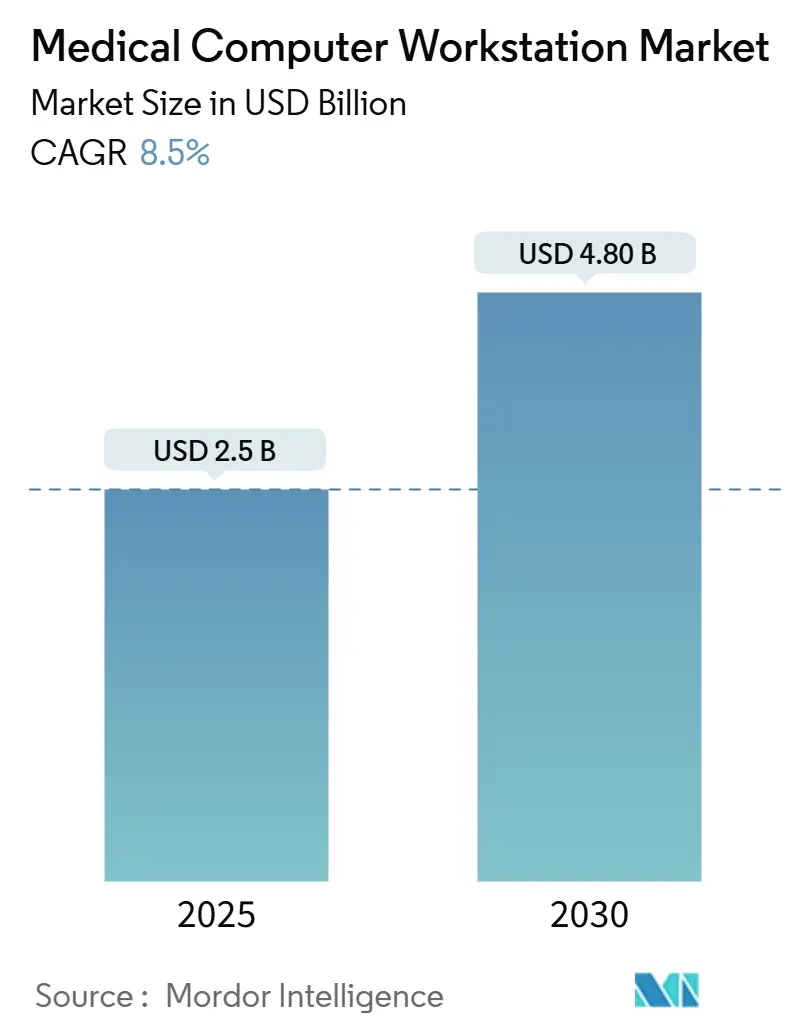

| Market Size (2025) | USD 2.5 Billion |

| Market Size (2030) | USD 4.80 Billion |

| Growth Rate (2025 - 2030) | 8.50% CAGR |

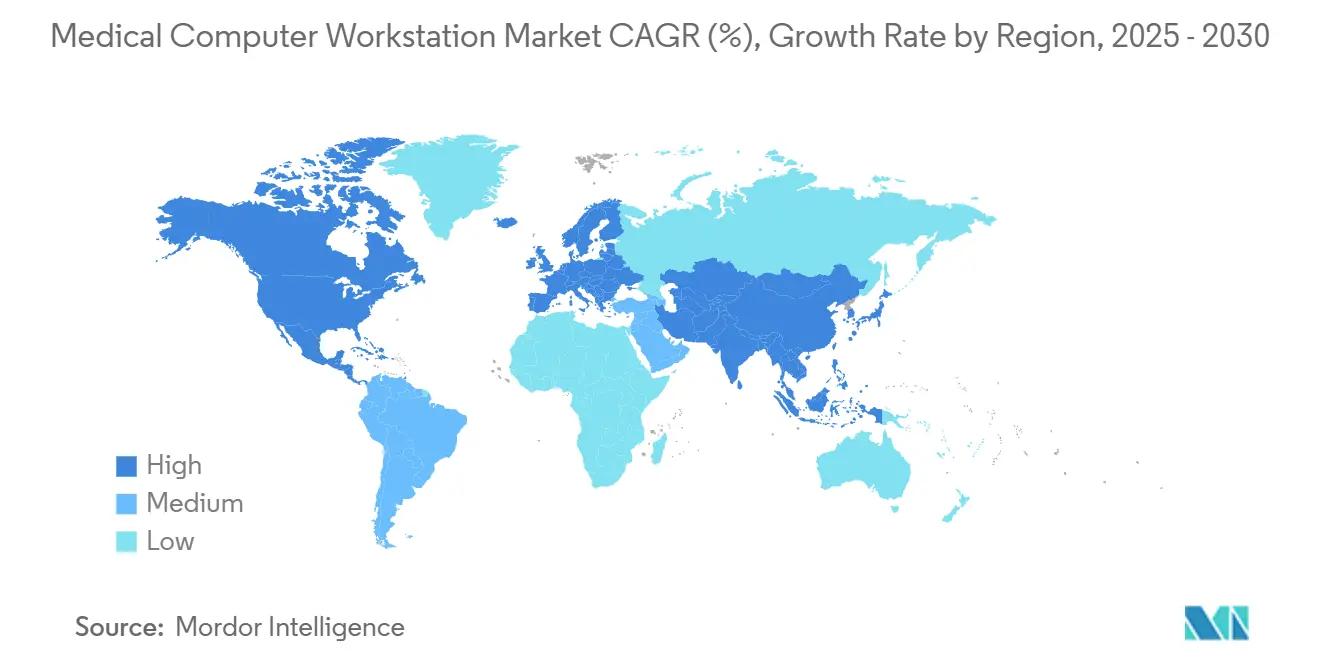

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Computer Workstation Market Analysis by Mordor Intelligence

The medical computer workstations market size stands at USD 2.50 billion in 2025 and is forecast to reach USD 4.80 billion by 2030, advancing at an 8.50% CAGR. Demand climbs as hospitals, clinics, and field-care units digitize point-of-care workflows, guided by electronic health record mandates, telehealth expansion, and strict infection-control rules. Mobile carts with hot-swap power systems now anchor mobility-first strategies that let caregivers document, consult, and dispense medications without interrupting care. Hardware remains the most significant component, but software-defined features such as fleet analytics and secure video deepen value and lift replacement cycles. Vendors also face rising cybersecurity and ergonomic standards that favor integrated designs and recurring service contracts—growth opportunities cluster in Asia Pacific, where government funding accelerates digital infrastructure across public and private facilities.

Key Report Takeaways

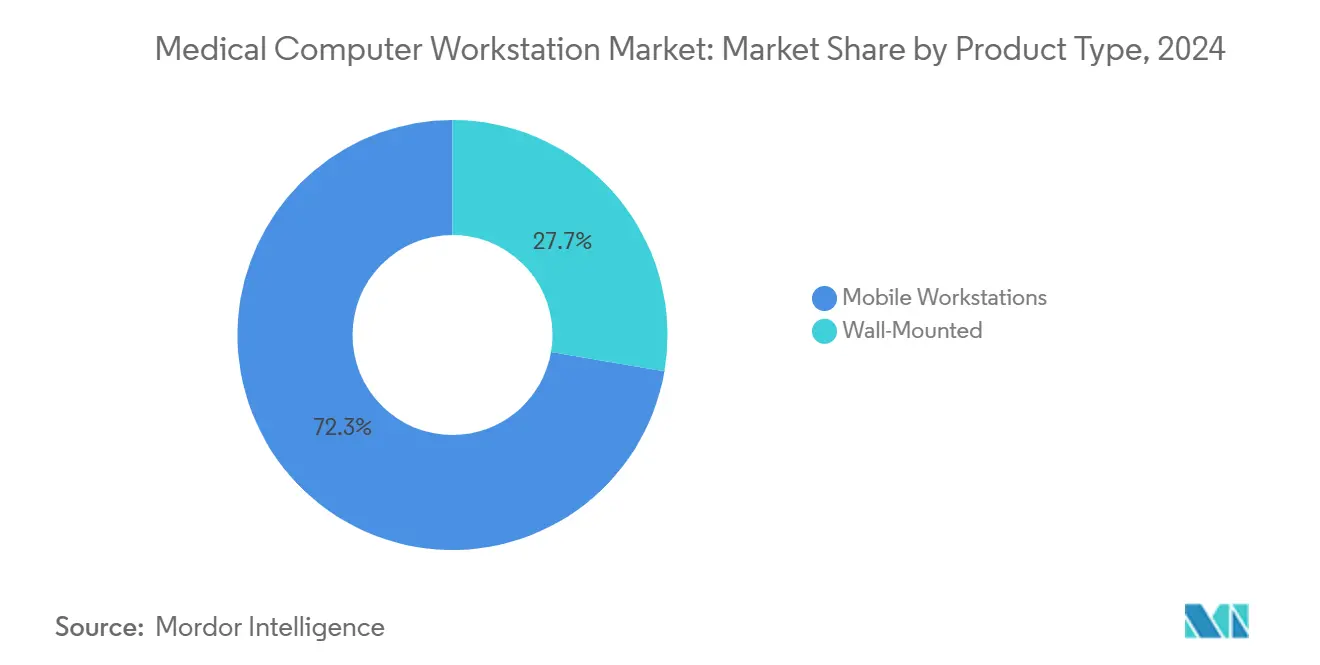

- By product type, mobile workstations led with 72.3% revenue share in 2024; the same segment is projected to expand at a 14.9% CAGR through 2030.

- By power source, non-powered models accounted for 54.7% of the medical computer workstations market share in 2024, while Li-ion hot-swap systems are set to grow at 17.8% CAGR to 2030.

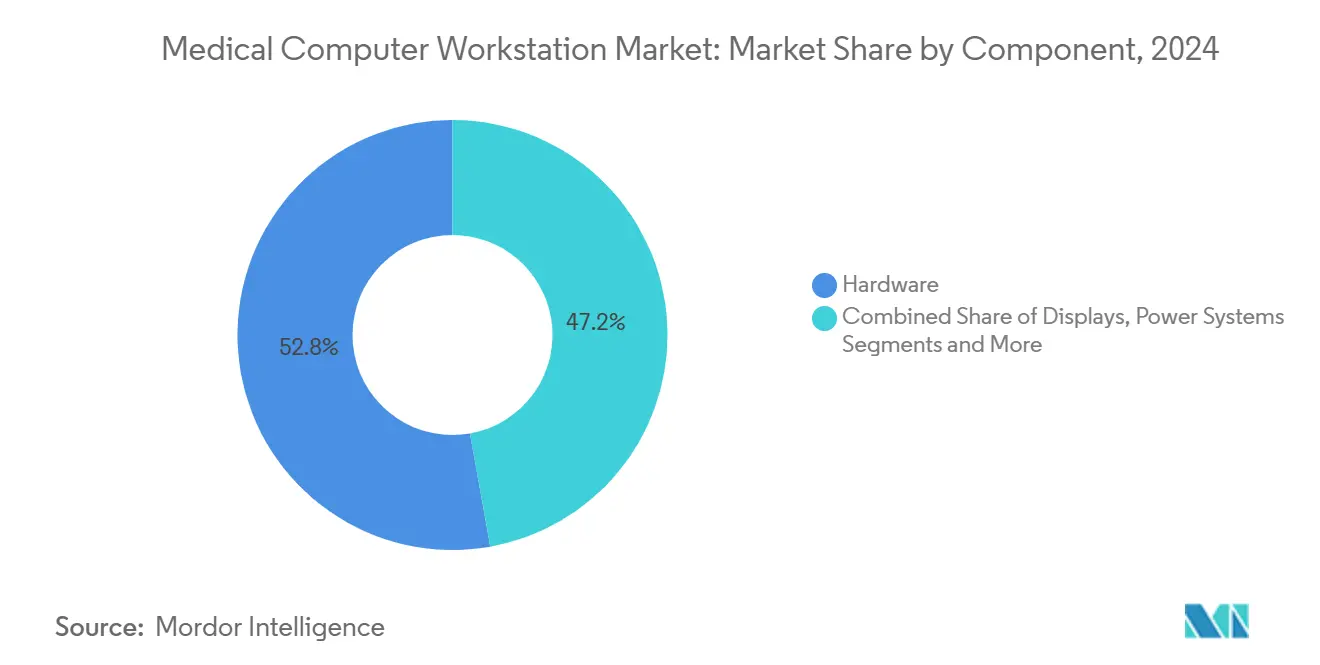

- By component, computing hardware held a 52.8% share of the medical computer workstations market size in 2024, and software-connectivity layers are advancing at a 16.4% CAGR through 2030.

- By end user, hospitals captured a 61.2% revenue share in 2024; ambulatory surgical centers recorded the fastest projected CAGR, at 14.1% through 2030.

- By application, electronic medical records documentation represented a 45.9% share in 2024, and teleconsultation is forecast to expand at an 18.1% CAGR to 2030.

- By geography, North America commanded a 34.8% share in 2024, while Asia Pacific is projected to rise at a 13.7% CAGR through 2030.

Global Medical Computer Workstation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EHR-Mandated Point-Of-Care Documentation Needs | +2.10% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Expansion Of Mobile Telemedicine Programs | +1.80% | Global, accelerated in APAC and rural markets | Short term (≤ 2 years) |

| Nursing Staff Shortage Driving Workflow-Efficiency Tools | +1.60% | North America & EU core, spill-over to APAC | Long term (≥ 4 years) |

| Infection-Control Regulations For Shared Equipment | +1.20% | Global, with stringent compliance in developed markets | Medium term (2-4 years) |

| Surge In Military Field-Hospital Digitalization | +0.90% | North America, EU, and defense-allied nations | Long term (≥ 4 years) |

| Battery-As-A-Service (BaaS) Subscription Models | +0.70% | North America & EU early adopters, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EHR-Mandated Point-of-Care Documentation Needs

Federal rules now require at least a 180-day electronic health record reporting period and higher interoperability scores, pushing facilities to capture data bedside rather than at nursing stations.[1]Centers for Medicare & Medicaid Services, “Calendar Year 2024 Program Requirements,” cms.govContinuous uptime is essential, making powered carts with hot-swap batteries a preferred choice. Hospitals that adopted these carts report smoother medication reconciliation and fewer documentation backlogs. South Eastern Health and Social Care Trust in Belfast deployed mobile carts to support its new enterprise record system and noted faster chart completion and improved ergonomics. As compliance audits tighten, investments in fleet-wide analytics and automatic patching rise.

Expansion of Mobile Telemedicine Programs

Telemedicine adoption among U.S. hospitals jumped from 46% in 2017 to 72% in 2021, and many of those encounters now occur on carts equipped with cameras, directional microphones, and antimicrobial keyboards.[2]Journal of General Internal Medicine, “Unveiling the Adoption and Barriers of Telemedicine in US Hospitals,” springer.com Demand extends to rural markets where carts link community clinics to urban specialists, reducing travel delays and broadening care access. Hungary’s nationwide mobile health service centers consulted nearly 1,900 rural patients in six months using telemedicine-ready carts that improved satisfaction and continuity of care. Vendors respond with lighter frames, height-adjustable screens, and modular mounts that adapt to language-interpretation or remote-monitoring kits.

Nursing Staff Shortage Driving Workflow-Efficiency Tools

The American Hospital Association warns that the U.S. could face 100,000 critical workforce vacancies by 2028, with nursing assistants most affected.[3]American Hospital Association, “5 Health Care Workforce Shortage Takeaways for 2028,” aha.org Streamlined documentation and automated charge capture allow nurses to reclaim clinical time. An Ergotron survey shows 95% of caregivers believe upgraded ergonomic equipment would ease workloads. Carts integrating AI-powered dictation and barcode scanning shorten medication rounds and reduce click fatigue. Flexible leasing models help budget-strapped hospitals accelerate deployment without large upfront costs.

Infection-Control Regulations for Shared Equipment

Updated Centers for Disease Control and Prevention guidelines emphasize rigorous disinfection of high-touch surfaces. Manufacturers answer with smooth, sealed enclosures, copper-infused plastics, and tool-free accessory removal that cuts cleaning cycles. TouchPoint Medical’s current generation ships with antimicrobial coatings validated to endure harsh wipes while maintaining screen clarity. These features appeal to intensive care, oncology, and long-term-care units where immunocompromised patients heighten infection risks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cap-Ex Of Powered Carts | -1.40% | Global, particularly acute in cost-sensitive markets | Short term (≤ 2 years) |

| Cyber-Security Compliance Costs (HIPAA, MDR) | -1.10% | Global, with stringent requirements in North America & EU | Medium term (2-4 years) |

| Limited Floor-Space In Legacy Facilities | -0.80% | North America & EU core, with aging infrastructure | Medium term (2-4 years) |

| Growing Use Of Handheld Tablets As Substitutes | -0.60% | Global, accelerated in cost-conscious emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Powered Carts

Powered models cost 40-60% more than non-powered units, testing budgets for ambulatory centers and rural hospitals. Though subscription batteries convert capital to operating expenses, executives remain cautious about long-term fees and vendor lock-in. Price-sensitive buyers often choose manual carts for non-critical tasks and reserve powered models for medication rounds or emergency departments. Volume rebates and grant funding help offset sticker shock, but pay-back cases hinge on demonstrated time savings and lower overtime expenses.

Cybersecurity Compliance Costs (HIPAA, PATCH Act, MDR)

Since October 2023, the U.S. Food and Drug Administration has required a software bill of materials and ongoing security maintenance for connected devices. Upcoming HIPAA updates add multifactor authentication for protected health information. In the EU, the Medical Device Regulation extends post-market surveillance to cyber threats. Smaller cart makers must hire specialists and certify processes, raising overhead and lengthening release cycles. Healthcare providers also budget for regular penetration testing and fleet-wide patch orchestration, redirecting funds from hardware refreshes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mobile Solutions Lead Next-Generation Care

Mobile carts captured 72.3% of 2024 revenues and will expand at a 14.9% CAGR to 2030, reflecting the medical computer workstation market's transition from fixed to point-of-care mobility. They support bedside charting, medication verification, and virtual consults, limiting caregiver travel across units and increasing patient satisfaction. Wall-mounted stations remain vital in operating rooms and imaging suites, where stable placement and cable routing outweigh mobility.

The mobile segment benefits from lighter lithium-ion batteries, embedded asset tracking, and fleet dashboards that allow clinical engineering teams to view charge levels and utilization in real time. Altus added a secure remote lock and 250 W power capacity to its IoT-connected carts so that nurses could move uninterrupted throughout the shifts. In contrast, wall-mount vendors improve articulation ranges and infection-control coatings to guard against infection in intensive care. Both formats integrate 24-inch touch displays and antimicrobial keyboards as standard.

By Power Source: Battery Innovation Accelerates Workflow

Non-powered configurations held 54.7% revenue in 2024, but powered carts are set for a 17.8% CAGR through 2030. Hot-swap packs now deliver 12-14 hour run time and charge to 80% within 90 minutes, eliminating mid-shift downtime. Hospitals cite fewer cart “dead zones” and shorter medication rounds after upgrading to powered fleets. Battery management software triggers replacement alerts and balances load, extending pack life and lowering total cost of ownership.

Plug-in carts still appeal in outpatient clinics with ample wall outlets and eight-hour service windows. They require minimal maintenance and carry lower acquisition prices that suit budget-constrained buyers. Yet infection-control teams favor wireless designs that remove floor cords and ease room turnover. Military field hospitals, where generators power mission-critical equipment, pick hybrid solutions that can charge on-board batteries from AC when available and switch to autonomous mode during transport.

By Component: Software Connectivity Unlocks New Value

Computing hardware continued to dominate, with a 52.8% share in 2024, but the fastest growth lies in software-connectivity stacks, which expanded at a 16.4% CAGR. Fleet analytics suites provide heat maps of cart location, helping clinics reallocate underused assets and cut shrinkage. Single sign-on and privacy screen filters guard patient data while reducing log-in times. API-driven designs link carts to drug cabinets, nurse call systems, and smart pumps, creating a unified workflow surface.

Display panels shift to higher brightness for operating rooms, and camera modules jump to 4K with noise-cancelling arrays to support tele-ICU rounding. Accessory and mount makers focus on quick-release couplings and standardized rail systems to simplify disassembly for disinfecting. Component commoditization pushes vendors to bundle warranties and live-chat technical support that shorten downtime.

By End User: Ambulatory Surgery Centers Gain Momentum

Hospitals generated 61.2% of the 2024 demand, using a broad mix of carts for emergency, intensive care, and general wards. However, ambulatory surgery centers will grow at a 14.1% CAGR as payers steer higher-acuity orthopedic and cardiovascular cases to cost-efficient outpatient venues. These facilities value slim footprints and integrated anesthesia charting, allowing rapid room turnover.

Long-term-care and nursing homes adopt carts to meet infection-control goals and comply with electronic medication administration record mandates. Specialty clinics such as endoscopy suites prefer wall units near procedure tables, but add mobile carts for recovery bays. Laboratories integrate compact models with barcode scanners to streamline specimen labeling and chain-of-custody tracking.

By Application: Teleconsultation Redefines Care Delivery

Electronic medical records documentation retained 45.9% share in 2024, yet teleconsultation will climb at an 18.1% CAGR to 2030. Carts equipped with autofocus cameras and secure messaging enable clinicians to examine and counsel patients remotely, sustaining virtual-care volumes that surged during the pandemic. Airports, corporations, and universities experiment with telehealth pods that rely on adaptable workstation cores.

Medication dispensing modules integrate lockable drawers and software that syncs with pharmacy systems, cutting handoff errors. Clinical imaging review grows as high-resolution displays allow on-ward assessment of CT or ultrasound, trimming diagnostic delays. In operating rooms, self-driving imaging systems link to carts for real-time surgical navigation.

Geography Analysis

North America accounted for 34.8% of 2024 revenue thanks to well-funded health systems and federal incentives that reimburse digital infrastructure upgrades. The United States also modernizes field hospitals with USD 9 million modular medical kits including ruggedized carts that endure harsh transport and climate conditions. Canada expands interoperable health exchanges through nation-wide digital standards that favor mobile point-of-care documentation.

Europe advances through aggressive targets such as Germany’s plan to reach 80% electronic patient record uptake by 2025. The European Health Data Space sets cross-border data-sharing rules that push workstation makers to certify encryption and identity management across jurisdictions. Hospital digital-readiness surveys reveal budget allocations for hardware upgrades still sit near 2.4% of operating spend, leaving ample room for market penetration.

Asia Pacific is the fastest-growing region at 13.7% CAGR. India’s Ayushman Bharat Digital Mission onboards more than 800 provider partners that need reliable carts in both urban and rural clinics. Singapore’s national HealthTech program invests in workforce skills and centralized procurement that accelerates adoption across public hospitals. China and Japan combine aging demographics with smart hospital blueprints, driving demand for battery-powered carts that integrate AI triage and infection-tracking features.

Competitive Landscape

The medical computer workstations market shows moderate fragmentation. Recent acquisitions, including GCX’s purchase of JACO in December 2024 and Auxo Investment Partners’ takeover of Altus Industries in January 2024, illustrate a roll-up strategy aimed at product breadth and manufacturing scale. Larger groups leverage global distribution and shared R&D, while niche players differentiate with specialty mounts or cybersecurity certifications.

Innovation centers on AI-enabled voice capture, ambient documentation, and predictive battery analytics. Vendors collaborate with semiconductor and cloud firms to embed secure GPUs that run bedside inference for decision support. Strategic partnerships with electronic health record providers tighten integration and create switching costs that fortify installed bases. Military and disaster-response contracts reward ruggedized designs and may open exports to allied nations.

White-space opportunities include airport clinics, cruise-ship infirmaries, and remote mining sites that require flexible, network-independent solutions. Companies that deliver modular, standards-based systems and remote firmware updates stand to attract enterprise-wide purchasing agreements. Cybersecurity competence and transparent software bills of materials now influence tender scores alongside ergonomics and battery life.

Medical Computer Workstation Industry Leaders

Ergotron Inc.

Capsa Healthcare

Enovate Medical

JACO Inc.

Advantech Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: OnMed opened the first airport-based CareStation, delivering virtual consults and drug dispensing.

- March 2025: AvaSure, Oracle, and NVIDIA unveiled an AI virtual care assistant that automates observation and triage tasks.

- March 2025: GE HealthCare and NVIDIA deepened their collaboration on autonomous X-ray and ultrasound workflow automation.

- December 2024: GCX acquired JACO, broadening its mounting solutions portfolio.

Global Medical Computer Workstation Market Report Scope

| Wall-Mounted Workstations |

| Mobile Workstations |

| Non-Powered (Plug-in/Manual) |

| Powered |

| Computing Hardware |

| Display Panels |

| Power-Management Systems |

| Accessories & Mounts |

| Software & Connectivity Layer |

| Hospitals |

| Ambulatory Surgical Centers |

| Long-Term Care & Nursing Homes |

| Specialty Clinics & Labs |

| Electronic Medical Records (EMR) Documentation |

| Medication Dispensing & Management |

| Clinical Imaging Review & PACS Access |

| Teleconsultation & Remote Rounding |

| Operating Room & Surgical Support |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Wall-Mounted Workstations | |

| Mobile Workstations | ||

| By Power Source | Non-Powered (Plug-in/Manual) | |

| Powered | ||

| By Component | Computing Hardware | |

| Display Panels | ||

| Power-Management Systems | ||

| Accessories & Mounts | ||

| Software & Connectivity Layer | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Long-Term Care & Nursing Homes | ||

| Specialty Clinics & Labs | ||

| By Application | Electronic Medical Records (EMR) Documentation | |

| Medication Dispensing & Management | ||

| Clinical Imaging Review & PACS Access | ||

| Teleconsultation & Remote Rounding | ||

| Operating Room & Surgical Support | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the medical computer workstations market?

The market is valued at USD 2.50 billion in 2025 and is projected to reach USD 4.80 billion by 2030.

Which product category leads sales?

Mobile workstations dominate with 72.3% revenue share, supported by fast 14.9% CAGR growth through 2030.

Why are powered carts gaining popularity?

Hot-swap lithium batteries remove downtime, improve infection-control by eliminating cords, and support continuous bedside documentation.

Which region shows the fastest growth?

Asia Pacific is forecast to grow at a 13.7% CAGR due to extensive government-funded digitization programs.

How are cybersecurity regulations affecting vendors?

FDA PATCH Act rules and upcoming HIPAA updates require a software bill of materials and ongoing security maintenance, raising development and compliance costs.

Page last updated on: