Medical Imaging Workstations Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

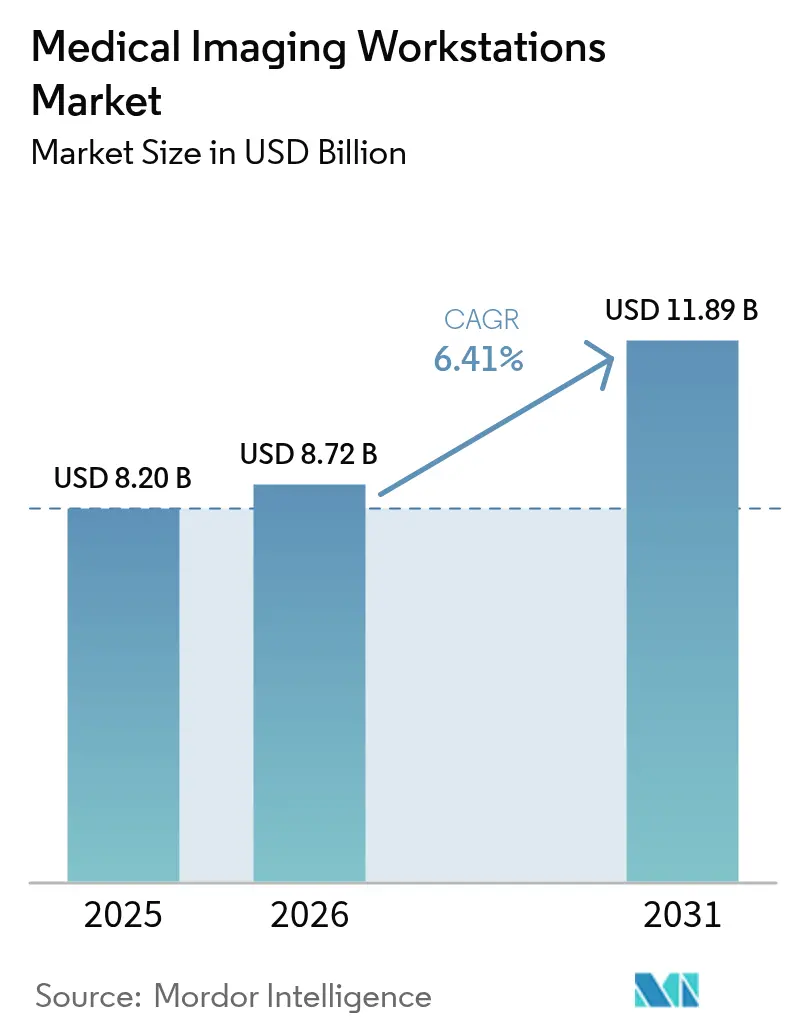

| Market Size (2026) | USD 8.72 Billion |

| Market Size (2031) | USD 11.89 Billion |

| Growth Rate (2026 - 2031) | 6.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Imaging Workstations Market Analysis by Mordor Intelligence

The Medical Imaging Workstations Market size was valued at USD 8.20 billion in 2025 and estimated to grow from USD 8.72 billion in 2026 to reach USD 11.89 billion by 2031, at a CAGR of 6.41% during the forecast period (2026-2031). Faster replacement cycles, enterprise picture-archiving migrations, and rising multi-modality procedure complexity collectively lift demand for advanced visualization platforms. Regulatory clarity, such as the FDA’s re-classification of computer-assisted detection software into Class II, has shortened innovation lead times and lowered entry barriers.[1]Source: U.S. Food and Drug Administration, “Medical Devices; Radiology Devices; Classification of the Radiological Computer-Assisted Detection and Diagnosis Software,” Federal Register, federalregister.gov Vendors now prioritize AI-ready designs and cloud-hosted delivery models that cut on-premises hardware costs, an approach that also helps hospitals cope with workforce shortages. North America keeps a performance edge through early AI adoption and mature reimbursement pathways, yet Asia Pacific records the fastest usage expansion on the back of large-scale digitization projects. Meanwhile, semiconductor supply constraints continue to throttle GPU availability, stretching lead times for high-end configurations and forcing some buyers toward thin-client alternatives.

Key Report Takeaways

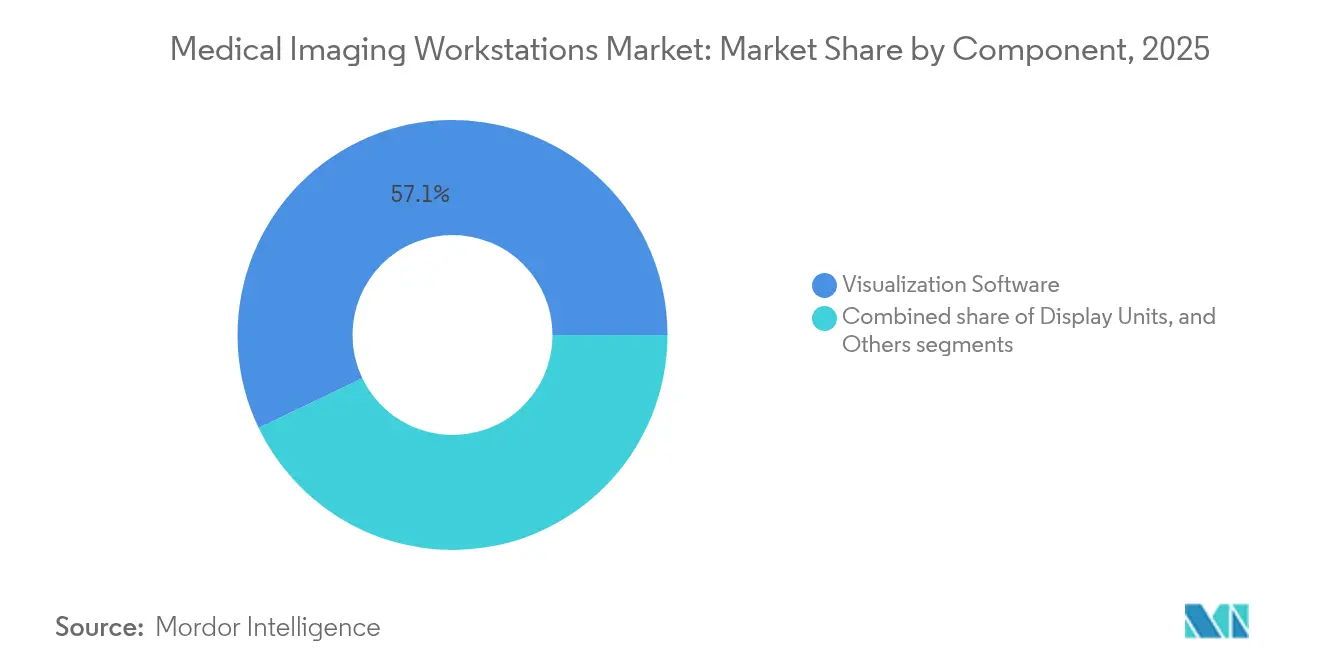

- By component, visualization software led with 57.12% revenue share in 2025, while display units are projected to advance at a 7.54% CAGR through 2031.

- By modality, Computed Tomography (CT) held 30.28% of the medical imaging workstations market share in 2025; mammography is positioned to grow at an 7.82% CAGR to 2031.

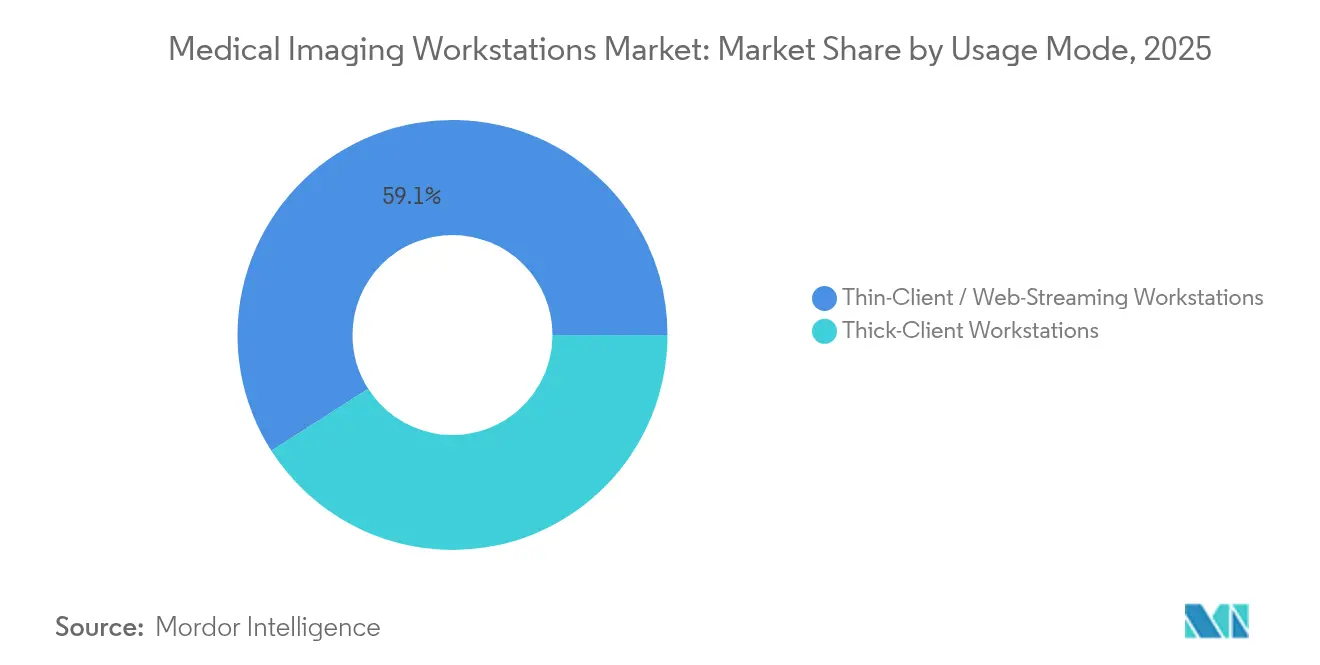

- By usage mode, thin-client/web-streaming platforms captured 59.05% of the medical imaging workstations market size in 2025; thick-client systems show a 6.93% CAGR outlook.

- By end-user, hospitals accounted for 61.40% of 2025 revenue, whereas diagnostic imaging centers are set to expand at an 7.62% CAGR over the forecast period.

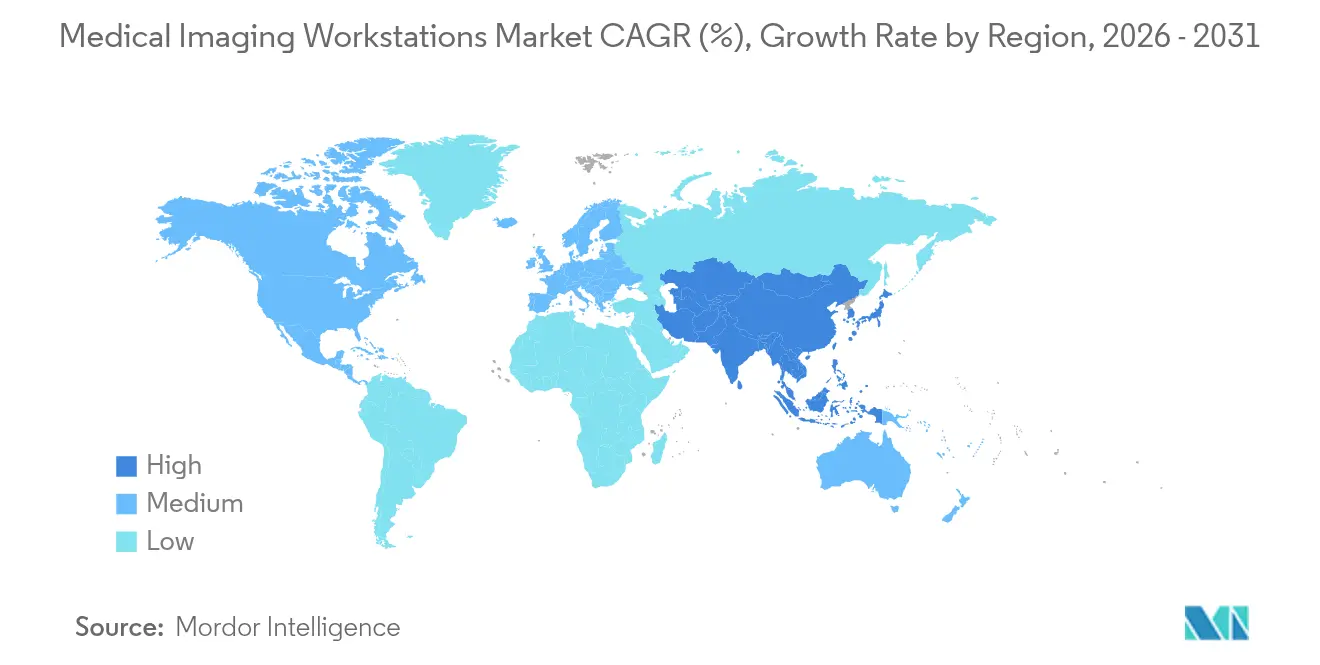

- By geography, North America commanded 37.32% of 2025 revenue; Asia Pacific exhibits the fastest regional CAGR at 8.02% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Imaging Workstations Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid technological evolution in imaging modalities | +1.8% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Growing imaging procedure volumes in emerging markets | +1.5% | APAC core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Rising healthcare expenditure coupled with rising disease burden | +1.2% | Global, particularly pronounced in aging populations | Long term (≥ 4 years) |

| Accelerated healthcare digitization—enterprise PACS/VNA migrations | +1.0% | North America & EU leading, APAC following | Medium term (2-4 years) |

| Ongoing innovations in hospital and diagnostic center infrastructure in emerging economies | +0.8% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Vendor-neutral API ecosystems enabling SaaS visualization plug-ins | +0.6% | Global, with technology leaders in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid technological evolution in imaging modalities

Photon-counting CT, whole-body MRI screening, cone-beam breast CT, and autonomous ultrasound together raise the computational ceiling for every workstation refresh cycle. Photon-counting scanners cut radiation exposure by as much as 80% while quadrupling raw data volume, demanding GPUs that support real-time 3-D reconstructions. GE HealthCare and NVIDIA’s collaboration shows how vendors are embedding AI inference at the image-acquisition layer, which in turn obliges workstation software to orchestrate automated segmentation, triage, and quality control. Prenuvo’s AI-enabled whole-body MRI platform reinforces the shift toward multi-organ analysis, compelling vendors to design workstations with higher throughput, larger cache, and multi-monitor ergonomics.[2]Source: Prenuvo, “Prenuvo Launches FDA-Cleared AI-Powered Whole Body MRI Screening Products,” itnonline.com

Growing imaging procedure volumes in emerging markets

Continual CT and MRI installation programs across Asia Pacific generate follow-on demand for visualization upgrades. Demographic aging lifts per-capita scan rates, particularly for oncology and cardiac imaging, which rely on sophisticated post-processing. Canon Medical’s India strategy signals manufacturers’ broader pivot to mid-income countries whose health ministries are funding picture-archiving rollouts alongside hardware refresh cycles. Ethiopia’s 71% reduction in patient waiting time after teleradiology deployment underscores how thin-client workstations connect remote hospitals to scarce radiologists.[3]Source: Araya Mesfin Nigatu, “Effect of Teleradiology on Patient Waiting Time and Service Satisfaction in Public Hospitals, Northwest Ethiopia,” BMC Health Services Research, biomedcentral.com Scalable cloud access therefore becomes a core purchasing criterion for facilities that lack on-site IT teams.

Rising healthcare expenditure coupled with disease burden

Cardiovascular disease prevalence propels adoption of cardiac-focused CT workstations such as GE HealthCare’s Revolution Vibe that performs one-beat coronary scans and auto-extracts functional data. Expanding breast and lung cancer screening programs require platforms tuned for 3-D mammography and low-dose CT navigation. Precision-medicine initiatives integrate genomic dossiers with radiology findings, prompting vendors to embed multimodal viewers capable of fusing omics and imaging. Point-of-care ultrasound adoption in emergency care raises the need for compact carts that offer diagnostic-grade displays and AI-driven annotation. Every dollar that health systems allocate to outcome-based reimbursement incentivizes investments in software that trims repeat exams.

Accelerated healthcare digitization—enterprise PACS/VNA migrations

Hospitals increasingly migrate from siloed PACS toward cloud-native, vendor-neutral archives that consolidate imaging across radiology, cardiology, and pathology. Recent FDA guidance exempting certain imaging-management functions from clearance has simplified upgrades to modular software stacks. Cloud PACS providers remove the need for on-premises servers and enable zero-footprint viewers, letting radiologists read from any web browser while maintaining diagnostic fidelity. AI-powered work-list orchestration plugs directly into these archives, automatically flagging critical cases and routing studies to subspecialists, which lifts throughput without adding headcount.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront & lifecycle costs of premium workstations | -1.4% | Global, particularly acute in price-sensitive emerging markets | Medium term (2-4 years) |

| Shortage of radiologists / advanced visualization specialists | -1.1% | Global, most severe in North America and EU | Long term (≥ 4 years) |

| Escalating zero-trust cybersecurity & HIPAA compliance expenses | -0.8% | North America & EU primarily, expanding globally | Short term (≤ 2 years) |

| GPU foundry capacity constraints & supply-chain shocks | -0.7% | Global, with particular impact on high-performance workstations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High upfront and lifecycle costs of premium workstations

Capital budgets still favor direct patient-care devices over support infrastructure. Total cost of ownership often doubles initial price once multiyear service contracts and software renewals are included. Smaller facilities look at certified refurbished hardware, yet those bargains often lack modern GPUs, throttling AI performance. Subscription software can smooth out capital spikes; however, cumulative fees sometimes exceed perpetual licenses over a seven-year horizon. Reimbursement erosion in radiology magnifies financial scrutiny, stretching procurement cycles.

Shortage of radiologists / advanced visualization specialists

More than 1,400 U.S. radiology positions remained vacant in 2024, a gap that technology alone cannot close. Advanced workstations ship with AI modules that promise efficiency; however, they still need trained users who understand nuanced parameters. Burnout accelerates early retirements, shrinking effective workforce capacity. Subspecialty shortages in cardiac and interventional imaging highlight how skill gaps directly limit workstation utilization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Drives Innovation

Visualization software generated 57.12% of 2025 revenue, illustrating how functionality now sits in code rather than bespoke hardware. That dominance will widen as vendors decouple algorithm licenses from display purchases, allowing rapid over-the-air updates. Subscription AI-segmentation plug-ins create recurring revenue streams and shorten feature lead times. Display units, in contrast, post the fastest 7.54% CAGR because 4 K and 8 K resolutions reduce diagnostic uncertainty in microcalcification and lung-nodule review. EIZO’s RadiForce RX670 with six-megapixel resolution and USB-C docking typifies ergonomic gains that minimize cable clutter.

Component convergence also guides procurement: thin-client setups shift value from local GPUs into centralized processing nodes, while auto-calibration and comfort-lighting features lift display ASPs. As more facilities aim for remote reading, zero-footprint viewers embedded in the hospital information system remove the last dependency on proprietary graphics cards. Consequently, software’s proportion of the medical imaging workstations market will continue to grow more rapidly than any hardware line item.

By Modality: CT Leadership Faces Mammography Disruption

Computed tomography workstations controlled 30.28% of 2025 revenue on the back of multi-organ utility and photon-counting upgrades. The segment benefits from enterprise standardization, as a single CT viewer can serve trauma, oncology, and cardiac cases. Mammography platforms, however, register the fastest 7.82% CAGR as national screening programs expand and 3-D tomosynthesis becomes common. Cone-beam breast CT’s elimination of breast compression will further raise data loads and justify workstation refresh investments.

MRI workstations gain momentum from helium-free magnet launches that ease siting constraints. Ultrasound, historically attached to hardware consoles, now leverages cloud-based post-processing that extracts automated measurements from raw cine loops. Nuclear-medicine workstation innovation hinges on digital detectors, which reduce recon time and cut dose while enabling total-body PET acquisitions.

By Usage Mode: Thin-Client Architecture Transforms Deployment

Thin-client and web-streaming configurations captured 59.05% of the medical imaging workstations market size in 2025. Hospitals accelerated remote-reading setups during the pandemic, realizing lasting productivity gains when radiologists could log in from home with the same credentials used on-site. Centralized compute pools simplify maintenance because GPU updates roll out once to a data center rather than to dozens of desks. Thick-client rigs remain essential for niche tasks such as cinematic-rendering and large-volume AI model training, which justifies their 6.93% CAGR.

Hybrid edge strategies now blend local SSD cache with cloud object storage, balancing latency and resiliency. Zero-footprint viewers embedded in EHR portals remove all installation barriers and open new possibilities for mobile reading. Encryption standards like TLS 1.3 ensure that web-streamed studies remain HIPAA-compliant without VPN overhead, an increasingly important point as ransomware risks climb.

By End-User: Hospital Consolidation Drives Procurement Patterns

Hospitals accounted for 61.40% of 2025 revenue due to multi-department imaging demand and sizable capital budgets. Consolidation among U.S. hospital groups creates bulk purchasing leverage, encouraging single-vendor framework agreements that bundle workstation, PACS, and service contracts. Meanwhile, diagnostic imaging centers demonstrate a 7.62% CAGR because payers steer non-urgent CT and MRI out of inpatient facilities to lower costs. These centers value fast image upload, one-click reporting, and pay-per-use AI that sidesteps upfront licenses.

Specialty clinics seek role-specific platforms, such as cardiovascular visualization suites that fuse CT angiography with intravascular ultrasound. Research institutions require open-API access for algorithm prototyping, whereas veterinary facilities prioritize ruggedized hardware that tolerates dust and variable temperature. Teleradiology service providers opt for cloud-native workstations, sharing compute across global reading teams while maintaining regional data-sovereignty compliance.

Geography Analysis

North America contributed 37.32% of 2025 revenue as U.S. and Canadian providers remained early adopters of AI triage tools and autonomous image acquisition. The region benefits from well-defined CPT codes that reimburse advanced procedures, allowing hospitals to recoup workstation investments quickly. A mature vendor ecosystem accelerates innovation cycles, with 300+ FDA-cleared AI algorithms already available for integration.

Asia Pacific recorded an 8.02% CAGR outlook driven by ongoing hospital build-outs, government cloud-health programs, and rapidly aging populations. China continues to scale provincial teleradiology hubs that connect county hospitals to tertiary centers, while India’s Ayushman Bharat scheme boosts diagnostic volumes in secondary cities. Many new facilities bypass legacy PACS and deploy cloud-native archives from day one, favoring thin-client architectures that minimize local IT staffing.

Europe shows steady expansion as the European Health Data Space initiative encourages cross-border image exchange, nudging hospitals toward interoperable viewers. National breast-screening extensions in Germany and France stimulate adoption of 3-D mammography workstations, while UK NHS modernization funds support AI-assisted CT lung-screening pilots.

In the Middle East and Africa, public-private partnerships fund flagship imaging centers, yet political volatility and exchange-rate swings can delay procurement.

Latin America gains traction through regional trade agreements that cut import duties on diagnostic hardware, though inconsistent broadband coverage limits thin-client rollouts in rural sites.

Competitive Landscape

The medical imaging workstations market remains moderately consolidated. GE HealthCare’s USD 51 million purchase of Intelligent Ultrasound and its agreement to take over MIM Software illustrate the race to fold specialty AI into mainstream platforms. Siemens Healthineers counters by embedding OpenRecon AI across its syngo.via viewers, while Philips deepens Spectral CT post-processing inside IntelliSpace. Hardware-display specialists such as EIZO partner with PACS vendors to certify color calibration for remote reading.

GPU shortages elevate supply-chain agility into a competitive differentiator because vendors that lock early allocations can ship premium thick-client rigs on schedule. FDA re-classification of CAD software into Class II decreased time-to-market for AI features, rewarding firms with agile R&D pipelines.

Interoperability remains a purchase-deciding factor: hospitals prefer vendors that embrace DICOMweb and FHIR to future-proof integrations. Overall, the competitive frontier is shifting toward platform breadth—hardware, cloud services, and native AI—rather than isolated point solutions.

Medical Imaging Workstations Industry Leaders

Koninklijke Philips N.V.

GE HealthCare

Siemens Healthineers AG

Canon Medical Systems Corporation

PaxeraHealth

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: A study discussed at the SIIM annual meeting suggested that mainstream consumer monitors can handle remote diagnostic reading reasonably well, though their true long-term cost advantage over purpose-built medical displays remains uncertain

- October 2024: Qure.ai began working with Roche Diagnostics’ APAC Startup Creasphere program to co-develop artificial-intelligence tools that enhance medical-imaging workflows across the region.

- October 2024: RamSoft teamed up with Mirada Medical to embed Mirada’s multimodality registration software into the cloud-native OmegaAI platform, bringing advanced oncology imaging tools to a wider global user base.

- July 2024: The FDA cleared CARPL.ai’s enterprise imaging platform, giving radiology departments one interface that can tap into more than 110 AI applications supplied by over 50 different vendors.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the medical imaging workstation market as the collection of dedicated hardware-software terminals that acquire, process, visualize, and archive diagnostic images from modalities such as CT, MRI, ultrasound, mammography, X-ray, and hybrid systems, whether installed on-premise or accessed through thin-client web streaming.

Scope Exclusions: Generic office PCs, PACS archive servers, and service-only contracts fall outside our sizing.

Segmentation Overview

- By Component

- Visualization Software

- Display Units

- Others

- By Modality

- Computed Tomography (CT)

- Magnetic Resonance Imaging (MRI)

- Ultrasound

- Mammography

- Others

- By Usage Mode

- Thick-Client Workstations

- Thin-Client / Web-Streaming Workstations

- By End-User

- Hospitals

- Diagnostic Imaging Centers

- Specialty Clinics

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Radiologists, modality OEM product managers, hospital CIOs, and regional distributors across North America, Europe, Asia-Pacific, and the Middle East were interviewed or surveyed. Their input helped us validate installed-base refresh rates, average selling prices, cloud-migration timelines, and AI-feature adoption, sharpening the desk findings before final triangulation.

Desk Research

Our analysts started with open data from authorities and professional bodies, including World Health Organization procedure volumes, OECD Health Statistics, U.S. FDA device listings, European Coordination Committee of the Radiological and Electromedical Industries, and annual RSNA abstracts, to size imaging equipment installed bases and throughput. Company 10-Ks, investor decks, and procurement tenders complemented these insights, while D&B Hoovers and Dow Jones Factiva supplied financials and news flow that flagged price shifts and unit launches. Numerous other public and subscription sources were reviewed; the list above is illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down model converts modality procedure counts and scanner shipments into workstation demand pools, adjusted for multi-viewer ratios and replacement cycles, and then cross-checked through sampled ASP × volume roll-ups. Key variables include annual CT/MRI scan growth, thin-client penetration, GPU cost trends, regional healthcare capital spending, and regulatory AI approvals. Five-year forecasts employ multivariate regression with scenario analysis, letting us stress-test uptake of cloud viewing and AI analytics. Bottom-up gaps, especially in smaller emerging markets, are filled using calibrated analogs from neighboring countries.

Data Validation & Update Cycle

Outputs run through variance checks versus import data, hospital IT budgets, and vendor revenue guidance; anomalies trigger a second analyst review. Reports refresh annually, and interim updates are issued when material events, such as major recalls, reimbursement changes, and macro shocks, move the baseline.

Why Our Medical Imaging Workstation Baseline Commands Reliability

Published values often differ because firms pick dissimilar modality baskets, count service revenue differently, or update figures on uneven schedules. We state these factors up front so readers see why numbers diverge before they reach conclusions.

Key gap drivers include some publishers bundling PACS servers or cardiology-only workstations, others assuming uniform ASP erosion, and several projecting AI adoption curves that our interviews found overly aggressive. Mordor's cadence, a yearly model rebuild anchored to verifiable imaging procedure data, keeps our baseline current yet measured.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.20 B (2025) | Mordor Intelligence | - |

| USD 9.40 B (2024) | Global Consultancy A | Includes PACS servers and cloud storage fees |

| USD 5.38 B (2024) | Trade Journal B | Uses hardware-only definition and excludes software upgrades |

These comparisons show that once scope inflation or omission is stripped away, Mordor's disciplined variable selection, timely refreshes, and transparent model steps offer decision-makers a balanced, reproducible baseline they can trust.

Key Questions Answered in the Report

What is the current value of the medical imaging workstations market?

The medical imaging workstations market size stands at USD 8.72 billion in 2026 and is projected to climb to USD 11.89 billion by 2031.

Which component segment leads the market in revenue?

Visualization software dominates with 57.12% of 2025 revenue, underscoring the shift to software-defined imaging platforms.

Why are thin-client workstations gaining popularity?

Thin-client architectures centralize processing, support remote reading, and cut on-site IT costs, which helped them secure 59.05% of 2025 revenue.

Which region shows the fastest growth?

Asia Pacific is forecast to expand at an 8.02% CAGR through 2031 due to extensive hospital build-outs and national digitization programs.

How are AI integrations influencing workstation purchases?

FDA re-classification of CAD software and vendor acquisitions of AI firms are accelerating embedded analytics, making AI-ready platforms a top buying criterion.

What key restraint could slow market expansion?

High upfront and lifecycle costs, especially in price-sensitive markets, reduce procurement momentum despite evident clinical benefits.

Page last updated on: