Medical Imaging Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

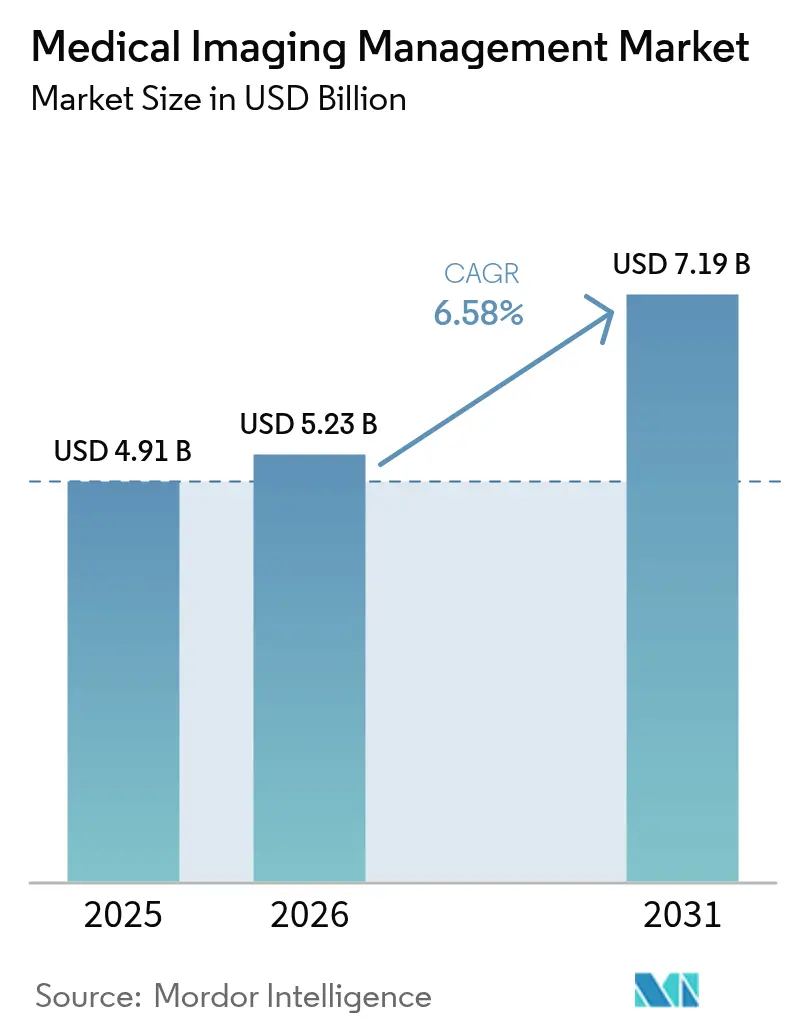

| Market Size (2026) | USD 5.23 Billion |

| Market Size (2031) | USD 7.19 Billion |

| Growth Rate (2026 - 2031) | 6.58% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Imaging Management Market Analysis by Mordor Intelligence

Medical Imaging Management market size in 2026 is estimated at USD 5.23 billion, growing from 2025 value of USD 4.91 billion with 2031 projections showing USD 7.19 billion, growing at 6.58% CAGR over 2026-2031. Demand rises because hospitals, imaging centers and outpatient facilities are moving from siloed, on-premise image archives to cloud-ready enterprise platforms that support artificial-intelligence-driven diagnostics, workflow automation and value-based care reimbursement. Cloud-native architectures, vendor-neutral archives and application-independent clinical archives together transform the storage and exchange of multi-modal imaging data, yet cybersecurity concerns and proprietary data models remain friction points for many buyers. Generative AI systems already deliver measurable productivity gains; Northwestern Medicine cut radiology report time by 15.5% and mitigates an expected shortfall of 19,500 radiologists. [1]Source: Yuta Desai et al., “Efficiency and Quality of Generative AI–Assisted Radiograph Reporting,” JAMA Network Open, jamanetwork.com

Key Report Takeaways

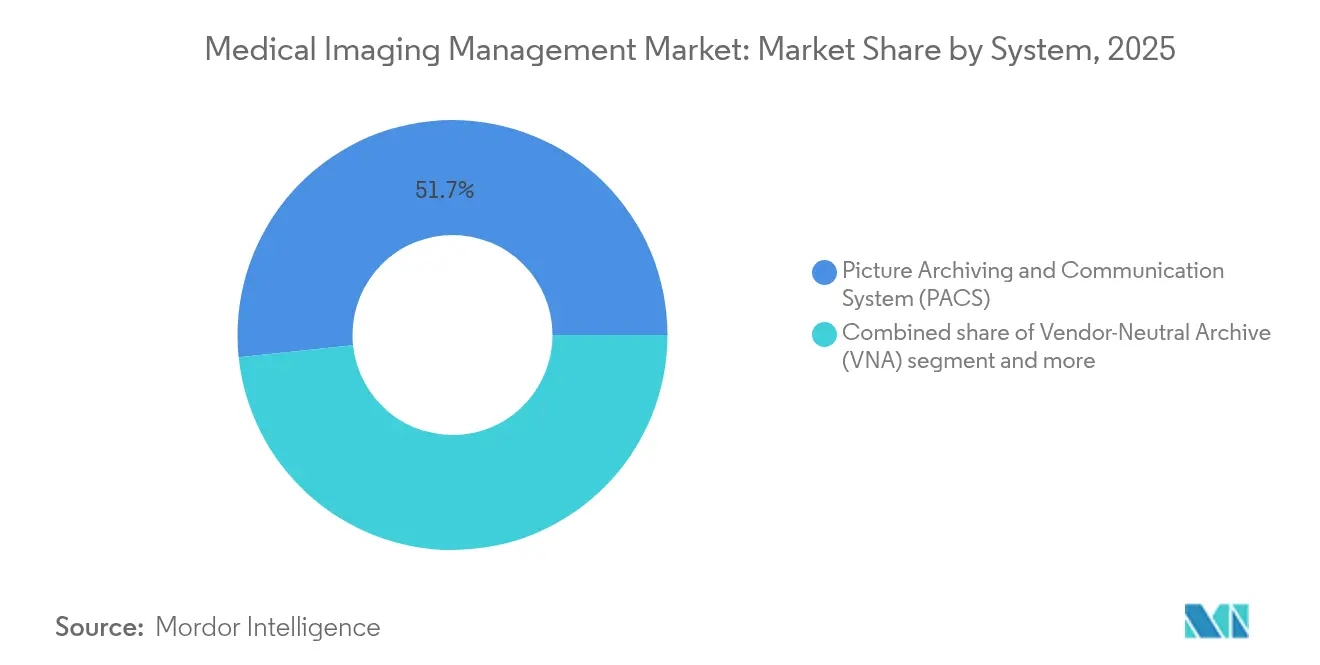

- By system, Picture Archiving & Communication Systems led with 51.65% revenue share in 2025; Vendor-Neutral Archives are projected to grow at an 7.86% CAGR through 2031.

- By deployment mode, on-premise installations accounted for 70.35% of the medical imaging management market share in 2025, while cloud-based platforms are advancing at a 7.42% CAGR to 2031.

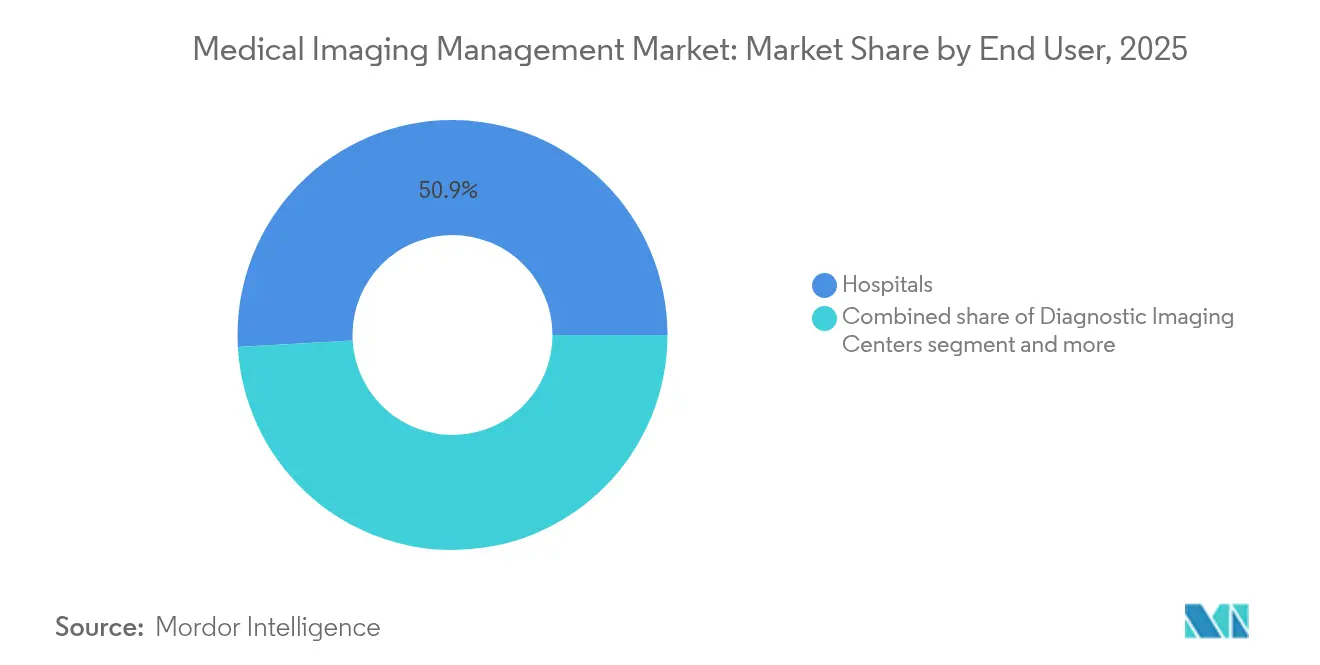

- By end user, hospitals held 50.88% share of the medical imaging management market size in 2025 and diagnostic imaging centers are expanding at an 8.11% CAGR through 2031.

- By region, North America captured 38.95% of 2025 revenue; Asia Pacific is forecast to expand at a 8.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Imaging Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological innovations in diagnostic imaging & image IT | +1.8% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Rising prevalence of chronic diseases | +1.2% | Global, with higher impact in aging populations of developed markets | Long term (≥ 4 years) |

| Big-data & AI integration into imaging workflows | +1.5% | North America & EU leading, APAC catching up rapidly | Short term (≤ 2 years) |

| Government incentives for healthcare IT adoption | +0.9% | North America, EU, and select APAC markets with national health programs | Medium term (2-4 years) |

| Rapid shift toward cloud-native enterprise imaging platforms | +1.3% | Global, with faster adoption in developed markets | Short term (≤ 2 years) |

| Value-based-care push for longitudinal imaging archives | +0.7% | North America primarily, expanding to EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Technological Innovations in Diagnostic Imaging & Image IT

Advanced photon-counting CT, whole-body MRI and AI-powered workflow tools are redefining how the medical imaging management market handles large image sets. The FDA cleared Ezra Flash AI for MRI noise reduction, proving that algorithmic post-processing can raise throughput without harming diagnostic integrity.[2]Source: Michael Walter, “FDA Clears Updated Ezra Flash AI Software for MRI Scans,” Diagnostic Imaging, diagnosticimaging.com Northwestern Medicine’s generative AI pilot cut average report time from 573 seconds to 435 seconds with no accuracy loss. Vendors now bundle AI deployment frameworks directly inside enterprise archives, enabling real-time inference while radiologists read studies. As a result, platforms must ingest multi-modal data streams, orchestrate AI models and archive results in longitudinal patient records. These capabilities strengthen the competitive edge of cloud-native firms that promise elastic compute and rapid algorithm updates, accelerating growth across the medical image management market.

Rising Prevalence of Chronic Diseases

Imaging utilization is climbing 3-4% yearly, whereas radiologist supply grows only 2.5%, tightening capacity constraints. Chronic cardiovascular, oncologic and neurologic conditions require repeat imaging to track disease progression. Hospitals now seek archives that collate multi-year image histories and integrate with population-health analytics. Vendor-neutral designs reduce data silos and let clinicians collaborate across organizations, a necessity for accountable-care models. Consequently, chronic-care pressures stimulate sustained adoption momentum across the medical imaging management market.

Big-Data & AI Integration into Imaging Workflows

Hospitals are pairing imaging archives with data lakes and AI orchestration layers that deliver predictive analytics at scale. Intelligent worklist balancing improved study distribution by 34% and generative AI boosted lung-nodule tracking efficiency 23% in controlled pilots. LILAC, a Weill Cornell model, now orders longitudinal CT slices with 99% accuracy, automating change detection over time. Such results convince C-suites to prioritize systems that embed algorithm marketplaces, GPU resources and audit trails. This data-centric mindset keeps the medical image management market on a rapid innovation curve.

Government Incentives for Healthcare IT Adoption

Policy drives technology upgrades. U.S. Promoting Interoperability Programs require hospitals to earn at least 60 points across e-prescribing, health information exchange and public-health reporting metrics. ONC allocated USD 86 million in 2024 for Leading-Edge Acceleration Projects focused on AI data quality and behavioral-health IT. President Biden’s FY25 budget requests USD 1.3 billion to reward hospitals that harden cybersecurity. Similar incentives in Europe and APAC reinforce spending on interoperable, secure platforms, broadening the addressable base of the medical image management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation & integration costs | -1.1% | Global, with higher impact on smaller healthcare providers | Short term (≤ 2 years) |

| Shortage of radioisotopes curbing SPECT / PET upgrades | -0.8% | Global, with acute impact in Europe and North America | Medium term (2-4 years) |

| Escalating cyber-attacks on imaging archives | -0.9% | Global, with higher vulnerability in under-resourced institutions | Short term (≤ 2 years) |

| Proprietary data models causing vendor lock-in | -0.6% | Global, affecting multi-vendor healthcare environments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Implementation & Integration Costs

Enterprise-grade PACS or VNA rollouts often exceed forecast budgets. One incremental-cost analysis showed that a department-wide PACS deployment struggled to deliver positive savings for high-volume specialties. Children’s Hospital of Philadelphia did save nearly USD 3 million over five years after migrating to a VNA, yet smaller providers lack the scale to absorb up-front conversion fees. Subscription cloud models reduce capital expenditure but introduce new line items such as egress charges and long-term archive fees. Cost pressure may postpone procurement among rural hospitals and independent practices, tempering short-run expansion of the medical image management market.

Escalating Cyber-Attacks on Imaging Archives

In 2024, 90% of healthcare organizations reported a data breach, with average daily ransomware losses of USD 2 million targeting diagnostic systems.[3]Source: College of Healthcare Information Management Executives, “CHIME Cheat Sheet on President’s FY25 Budget Request,” chimecentral.org The Change Healthcare incident forced payers and providers offline for weeks, spotlighting systemic risk inside centralized image exchanges. Legacy archives lack zero-trust defenses or immutable backups, making them attractive entry points. A Pennsylvania system paid USD 65 million after an attack leaked cancer-patient scans. To mitigate risk, buyers are adding multi-factor authentication, segmentation and real-time threat monitoring, steps that raise implementation cost and lengthen sales cycles for the medical image management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System: PACS Dominance Faces Cloud-Native Disruption

Picture Archiving & Communication Systems held 51.65% of the medical image management market share in 2025, confirming the installed base advantage of traditional radiology workstations and DICOM routers. The medical image management market size tied to PACS is forecast to grow more slowly than the overall market as vendor-neutral archives accelerate at an 7.86% CAGR. Vendor-neutral designs decouple the archive from the viewer, letting organizations cut licensing costs and integrate AI algorithms without modifying core storage.

Cloud-first providers are rewriting the competitive script. Application-independent clinical archives add a governance layer that surfaces imaging to cardiology, pathology and surgical planning apps on equal terms. Together these trends reshape the medical image management market as health systems reevaluate data-sovereignty, AI integration and disaster-recovery priorities.

By Deployment Mode: Cloud Migration Accelerates Despite Security Concerns

On-premise installations retained 70.35% of 2025 revenue, buoyed by sunk server investments and local-control preferences of large teaching hospitals. Yet cloud platforms are advancing at a 7.42% CAGR, reflecting mounting confidence in HIPAA-compliant infrastructure offered by hyperscalers. The medical image management market size for cloud deployments is projected to double by 2030 as organizations seek opex models, instant scalability and built-in analytics.

Hybrid strategies dominate transitional phases. Ambra Health relies on Google Cloud to facilitate encrypted study routing, enabling radiologists to read from anywhere while sensitive identifiers stay on-site. COVID-19 remote-reading mandates proved cloud viability, and executive teams now cite disaster-recovery strength as a leading reason to migrate archives. Even so, board-level anxiety over breach liability sustains demand for local fail-safe copies, moderating the near-term pace of full migration across the medical image management market.

By End User: Imaging Centers Drive Growth Through Outpatient Trends

Hospitals generated 50.88% of 2025 demand thanks to comprehensive modality fleets and enterprise-wide imaging initiatives. Diagnostic imaging centers, however, are tracking the fastest-growing 8.11% CAGR as payers steer non-acute scans toward lower-cost outpatient venues. The medical image management industry experiences heightened deal activity: RadNet invested more than USD 54 million on acquisitions in 2024 and continued to pick up AI startups in 2025.

Regulatory relaxations amplify that growth. States easing certificate-of-need rules now welcome new outpatient imaging builds in suburban and rural zip codes. Ambulatory surgery centers invest in lightweight VNA solutions that integrate intra-operative ultrasound, endoscopy and fluoroscopy images into same-day discharge workflows. These patterns sustain robust expansion within the medical image management market.

Geography Analysis

North America leads with 38.95% of global revenue, underpinned by mature reimbursement, robust broadband and aggressive AI pilots. Federal grants such as the USD 86 million LEAP program catalyze hospital spending on interoperable platforms that embed algorithm assurance features. Canadian provinces deploy province-wide VNAs to enable cross-site oncology consults, reinforcing regional leadership in the medical image management market.

Asia Pacific delivers the steepest growth at 8.74% CAGR to 2031. China’s regulator approved 59 AI imaging devices by mid-2023 versus nine in 2020, opening commercialization channels for cloud PACS and AI reporting add-ons. India’s insurance expansion fuels electronic-record mandates that bundle imaging libraries with revenue-cycle systems. Thailand rolled out telemedicine kiosks linking rural clinics to central radiologists, boosting demand for lightweight web viewers. Collectively, these policy shifts and capacity investments accelerate the medical image management market across APAC.

Europe posts steady uptake. GDPR pushes encryption, audit trails and consent management inside archives, while the EU AI Act labels most imaging-AI tools “high-risk,” forcing vendors to build compliance modules by February 2025. Germany, France and the UK channel national-digitization budgets into enterprise imaging backbones that federate regional hospitals. GCC countries in the Middle East modernize diagnostics for medical-tourism goals, and Latin American providers adopt cloud VNAs to sidestep capex barriers. These diverse drivers and constraints sustain mid-single-digit growth for the medical image management market across EMEA and the Americas outside North America.

Regulatory Landscape

Medical imaging management platforms operate under intersecting requirements for medical device software, privacy, and interoperability. In the United States, the FDA has been formalizing expectations for AI-enabled device software functions through guidance on lifecycle management and marketing submissions (January 2025), and it has also used the Federal Register to codify Class II pathways for radiology software functions (for example, the June 2025 classification order for radiological acquisition and/or optimization guidance systems). These actions translate into more explicit validation, documentation, and change-management obligations for vendors that embed AI workflow features inside PACS, VNA, viewers, and allied modules.

In Europe, compliance is shaped by the Medical Device Regulation (MDR) and In Vitro Diagnostic Regulation (IVDR) implementation framework, with ongoing updates to harmonised standards and conformity assessment processes (including European Commission actions during 2026). Alongside regional rules, global convergence is being pushed through the International Medical Device Regulators Forum (IMDRF): its software-as-a-medical-device risk and characterization work and the 2026 public consultation on an AI lifecycle management technical framework emphasize traceability, auditability, and risk controls, which directly shape procurement criteria for enterprise archives handling longitudinal imaging data.

Competitive Landscape

The field is moderately consolidated yet intensifying. GE Healthcare, Philips and Siemens Healthineers still dominate modality-attached PACS but face competition from cloud-native firms. GE HealthCare agreed in 2024 to buy MIM Software, adding adaptive-therapy planning and deep-learning segmentation to its Edison platform.

Start-ups exploit white spaces. Core Sound Imaging raised USD 80 million to scale Studycast, a cloud archive optimized for cardiology and point-of-care ultrasound. AIATELLA secured EUR 2 million to commercialize multi-modal vascular AI, betting on niche depth over broad modality coverage. ONRAD acquired Direct Radiology from Philips in January 2025, forming the largest independent teleradiology network in the United States.

Competitive strategy concentrates on three axes: full-stack enterprise imaging, AI workflow orchestration and cybersecurity differentiation. Vendors combining all three—plus flexible deployment—gain traction as health systems retire legacy PACS. This alignment positions them to capture incremental share in the medical image management market over the forecast horizon.

Medical Imaging Management Industry Leaders

Fujifilm Holdings Corporation

IBM Corporation

Siemens Healthineers

GE Healthcare

Koninklijke Philips N.V

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Enterprise imaging consolidation and operational AI adoption are converging around a need for platforms that can store multi-modal imaging, expose it through APIs, and govern AI outputs as part of the patient record, particularly as providers move beyond department-specific PACS toward centralized VNAs and application-independent clinical archives. Regulatory action also supports product roadmaps that package AI more tightly with imaging management, as reflected in the FDA signaling around predetermined change control plans for radiological ML-based quantitative imaging software (June 2026). That focus encourages vendors to build safer, faster software update mechanisms into managed viewers, archives, and workflow modules.

Cloud and hybrid modernization is another opportunity area, especially where buyers want to reduce technical debt while adding scalable compute for AI orchestration and remote reading. Product and platform moves reinforce this direction, including Merative releasing Merge Imaging Suite VNA v26.0 on Microsoft Azure (April 2026), as well as provider-side incentives for interoperable, secure IT investments that raise expectations for zero-trust access controls, immutable backup strategies, and audit trails in imaging archives. As outpatient imaging and multi-site networks expand, demand concentrates on deployments that standardize cross-facility image exchange while limiting lock-in through vendor-neutral data models and enterprise viewers.

Recent Industry Developments

- June 2026: Philips partnered with Bajaj Integrated Health System (BIHS) to deploy IntelliBridge Enterprise (IBE) 3.0 Enterprise Cloud in India, focusing on integration across medical devices and hospital systems. The deployment strengthens the data connectivity foundations that enterprise imaging programs depend on, improving the ability to route imaging and related clinical data across sites. It also highlights how imaging management value is increasingly driven by interoperability layers above departmental archives.

- May 2026: Fujifilm announced a partnership with Ardent Health to implement Synapse enterprise imaging, including Synapse Diagnostic PACS and Synapse VNA, across Ardent facilities spanning six US states. Rolling out a standardized PACS and VNA stack across a multi-state footprint supports cross-facility collaboration and centralized governance of imaging data. The agreement points to continued replacement and consolidation cycles as health systems move from siloed archives to enterprise platforms.

- March 2026: GE HealthCare received US FDA 510(k) clearance for View, a diagnostic viewer within the Genesis Radiology Workspace designed for cloud-native, zero-footprint access. Clearance supports broader deployment of remote-access viewing models aligned with cloud and hybrid archive strategies. It also increases competitive pressure for imaging management vendors to pair enterprise archives with secure, device-agnostic clinical viewing.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the medical imaging management market covers software used by healthcare providers to store, index, route, retrieve, and view diagnostic images and related files across departments and sites, so clinicians can access studies as part of care and reporting.

Scope exclusions: Imaging hardware, and stand-alone AI tools sold without an imaging storage or enterprise viewing layer, are excluded from the revenue counted here.

Segmentation Overview

- By System

- Picture Archiving & Communication System (PACS)

- Vendor-Neutral Archive (VNA)

- Application-Independent Clinical Archive (AICA)

- Other Systems

- By Deployment Mode

- On-premise

- Cloud-based

- Hybrid

- By End User

- Hospitals

- Diagnostic Imaging Centers

- Ambulatory Surgery Centers

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public baselines that explain how imaging volumes and healthcare IT spending move year to year. We referenced sources such as the World Health Organization for system-level health indicators, the US FDA for device and software regulatory context, the US Centers for Medicare and Medicaid Services for reimbursement and provider activity signals, and the OECD for cross-country health expenditure series.

To anchor the business side, we also reviewed materials like annual reports, investor presentations, press releases, and procurement notices from hospitals and public buyers, followed by peer-reviewed journal articles on enterprise imaging adoption patterns. A few paid subscriptions were used only for company financials and corporate news tracking, plus patent databases to spot product direction changes. These desk sources are illustrative, and many other public documents were checked for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming what revenue is truly attributable to imaging management software, and how pricing and deployment choices are changing. We spoke with a mix of software providers, hospital imaging IT teams, and channel or implementation partners across APAC, EMEA, and the Americas. Input from these interviews helped tighten assumptions on enterprise viewer rollouts, VNA migrations, and renewal timing.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 15% | APAC: 43% |

| Mid tier: 54% | Functional/Unit leaders: 42% | EMEA: 35% |

| Smaller Players: 19% | Managers: 43% | Americas: 22% |

Market-Sizing & Forecasting

Sizing followed a top-down approach where provider imaging activity and enterprise imaging adoption were used to reconstruct the addressable software demand pool, and then translated into revenue using typical price and contract structures. Since the model can overstate totals when adjacent IT spend leaks in, the numbers were cross-checked with selective bottom-up approximations such as sampled average selling price ranges times estimated site counts, and vendor revenue splits discussed in interviews.

Inputs were kept practical, including diagnostic imaging procedure volumes, installed base replacement cycles for PACS and VNA, enterprise viewer seat expansion in health systems, mix shifts between on-premises and cloud deployments, and average contract duration plus renewal rates. When gaps showed up for smaller geographies, proxy indicators like hospital count, imaging center density, and health expenditure were used first, and then adjusted using regional interview feedback.

Forecasts were built using scenario analysis supported by expert consensus on a few key drivers, mainly cloud migration pace, interoperability mandates, hospital capital budget trends, and imaging volume growth. Sensitivity ranges were applied so the final trajectory stayed consistent with how procurement cycles behave in real buyer budgets.

Data Validation & Update Cycle

Outputs were validated through multiple checks so the totals stay tied to real-world demand signals. We compared model results against independent indicators like provider IT spend direction, imaging procedure growth, and stated enterprise imaging priorities, then reviewed any large variances at region and component level.

Before sign-off, the file is reviewed in steps so assumptions, math, and scope logic are consistent, and follow-up outreach is triggered when an input moves beyond expected ranges. Reports are refreshed annually, and interim updates are made when material events occur such as major policy changes, pricing shifts, or large vendor acquisitions. Right before delivery, a fresh review pass is completed so clients receive the most current view available.

Mordor Intelligence's Medical Imaging Management Market Size Compared With Other Published Estimates

Published market values for imaging management often look different because each publisher draws the lines around software scope in its own way, and then uses different base years, currency timing, and assumptions on cloud subscription recognition. Differences also show up when adjacent categories get combined, or when a forecast is reported as an optimistic or conservative case without clearly labeling it.

The benchmark table shows a noticeable spread across the same general topic. In Mordor Intelligence's model, the counted revenue is limited to imaging management software layers like PACS, VNA, application-independent clinical archives, enterprise viewers, and related workflow modules, while imaging hardware and stand-alone AI tools without storage or viewing are not included. Some external estimates also start from different base years or use broader specialty and distribution channel framing, which can shift the total even before growth is applied.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.23 B (2026) | |

| Industry Research Publisher A | USD 5.97 B (2024) | Uses an earlier base year and a wider segmentation lens that can pull in adjacent workflow and specialty-specific imaging IT spend, which makes the total less comparable on a like-for-like software scope. |

| Market Tracker B | USD 3.97 B (2024) | Applies a narrower type list that emphasizes core PACS and VNA, which can undercount enterprise viewer and archive layers that are increasingly budgeted as part of enterprise imaging programs. |

Taken together, the table differences mostly trace back to what is counted as imaging management versus nearby IT categories, and how revenues are timed by year and deployment model. By keeping the scope rules explicit and then checking totals against adoption and renewal signals, we end up with a balanced value that can be replicated and updated as inputs change.

Key Questions Answered in the Report

What is the current size of the medical imaging management market?

The market is valued at USD 5.23 billion in 2026 and is projected to reach USD 7.19 billion by 2031.

Which system type holds the largest share?

Picture Archiving & Communication Systems account for 51.65% of 2025 revenue.

Why are diagnostic imaging centers growing faster than hospitals?

Outpatient cost advantages, payer steering and relaxed certificate-of-need regulations are driving an 8.11% CAGR for imaging centers.

Which region is expanding most rapidly?

Asia Pacific is expected to grow at a 8.74% CAGR through 2031 on accelerating digitization and supportive government policies.

What role does artificial intelligence play in this market?

AI improves workflow efficiency, supports predictive diagnostics and drives demand for cloud-ready archives that can deploy and monitor algorithms at scale.

Page last updated on: