Market Overview

| Study Period | 2021 - 2031 |

|---|---|

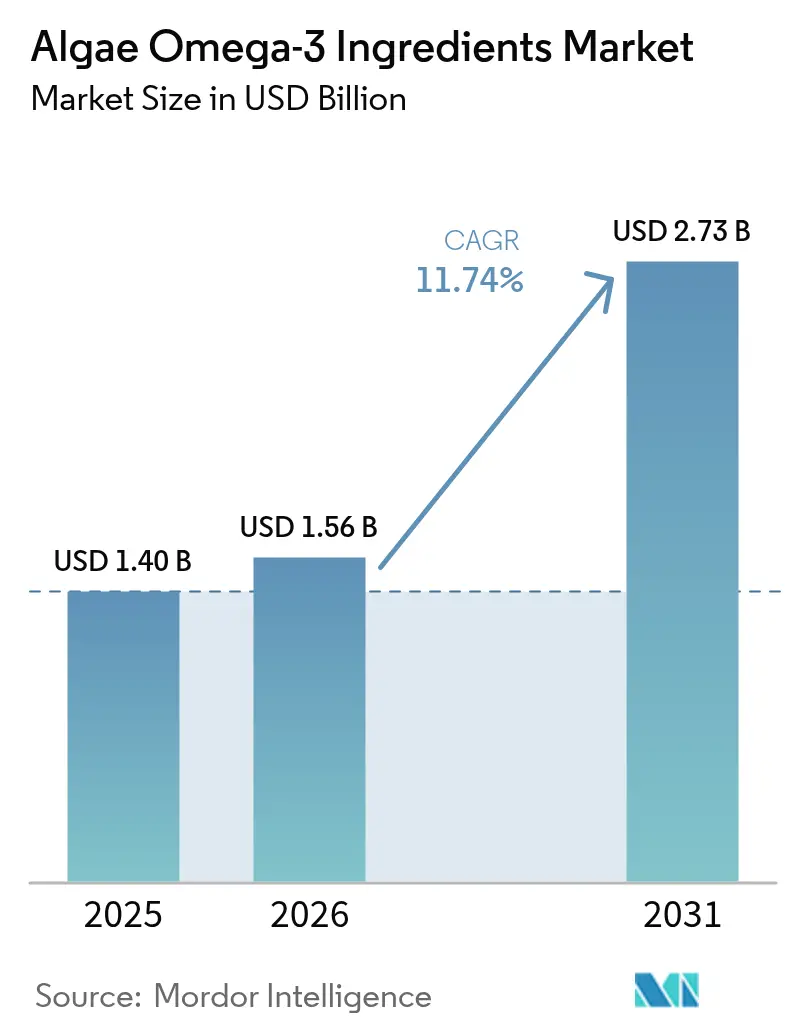

| Market Size (2026) | USD 1.56 Billion |

| Market Size (2031) | USD 2.73 Billion |

| Growth Rate (2026 - 2031) | 11.74% CAGR |

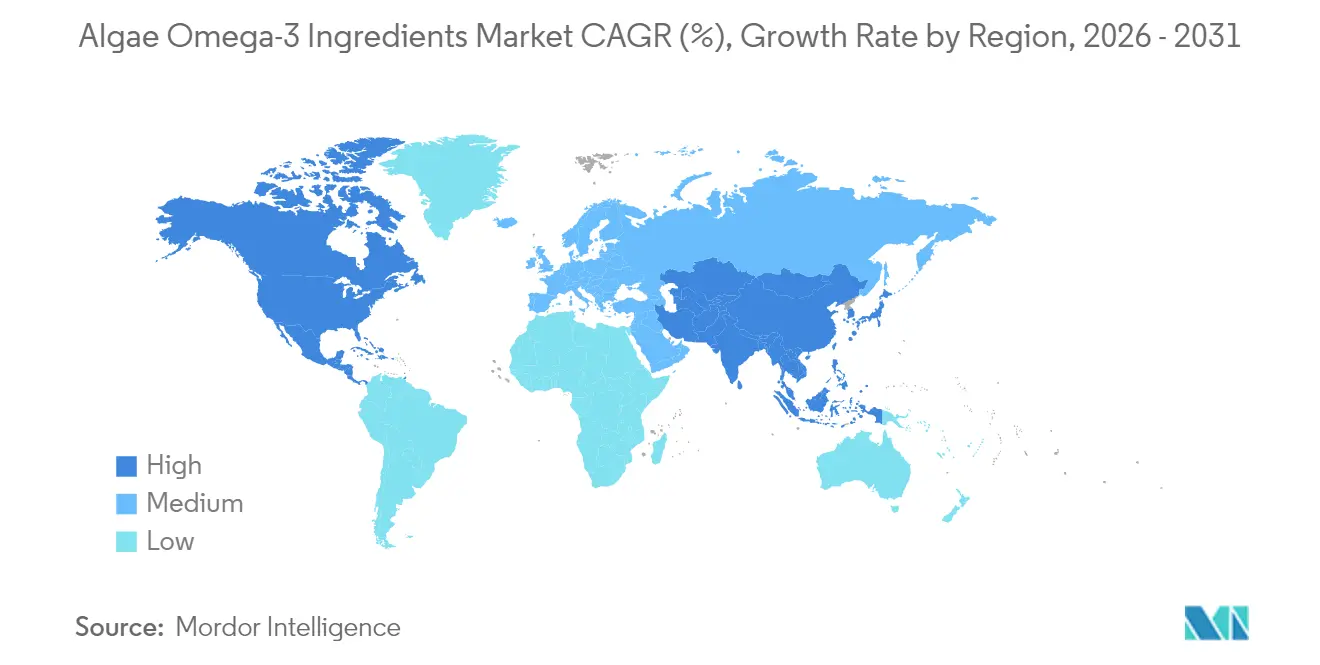

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Algae Omega-3 Ingredients Market Analysis by Mordor Intelligence

Algae omega-3 ingredients market size in 2026 is estimated at USD 1.56 billion, growing from 2025 value of USD 1.40 billion with 2031 projections showing USD 2.73 billion, growing at 11.74% CAGR over 2026-2031. This robust growth trajectory reflects accelerating consumer demand for sustainable, plant-based alternatives to traditional fish oil sources, driven by mounting concerns over marine ecosystem depletion and contamination risks associated with wild-caught fish derivatives. Regulatory momentum has emerged as a critical growth catalyst, with the FDA issuing multiple GRAS (Generally Recognized as Safe) notices for algae-derived omega-3 compounds and the European Union mandating DHA inclusion in infant formula since February 2022 [1]Source: European Food Safety Authority, "DHA inclusion in infant formula" efsa.europa.eu. These approvals have unlocked significant market opportunities across pharmaceutical, clinical nutrition, and functional food applications, where algal omega-3s offer superior purity profiles compared to marine-sourced alternatives. Competitive intensity is moderate, and technology differentiation, particularly high-DHA yielding strains, has emerged as a key success factor in the algae omega-3 ingredients market.

Key Report Takeaways

- By type, DHA commanded 63.58% of the algae omega-3 ingredients market share in 2025, and EPA/DHA blends are positioned to record a 14.30% CAGR through 2031.

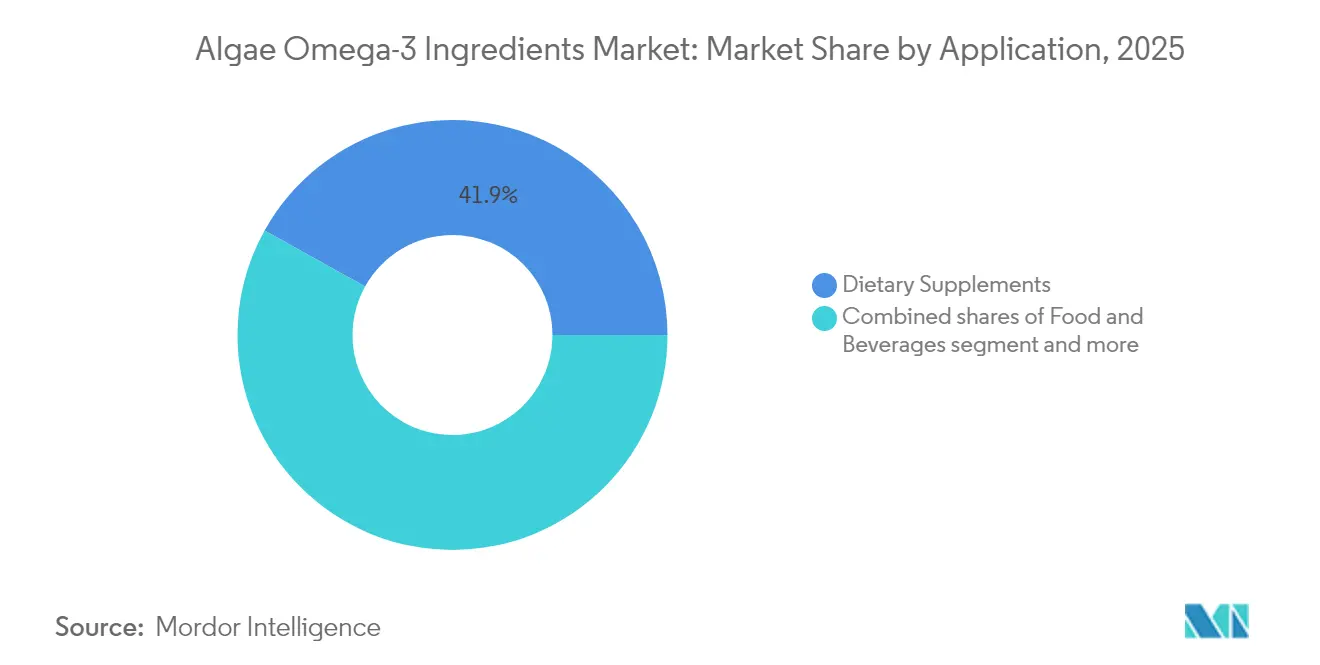

- By application, dietary supplements captured 41.92% revenue share in 2025; food and beverages are projected to expand at a 14.19% CAGR through 2031.

- By geography, North America led with 37.61% revenue share in 2025, whereas Asia-Pacific is set to post a 13.06% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Algae Omega-3 Ingredients Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Sustainable Plant-Based Omega-3 Ingredients | + 2.8% | Global, with early gains in North America and Europe | Medium term (2-4 years) |

| Growing Regulatory Approvals for Algae-Derived Omega-3 Compounds | + 2.1% | Global, spill-over from FDA (Food and Drug Administration) and European Union to Asia-Pacific | Short term (≤ 2 years) |

| Expanding Research and Development Investments in Algae Farming | + 1.9% | North America and European Union core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Increasing Use in Functional Foods and Nutraceutical Industries | + 2.3% | Global, with accelerated adoption in Asia-Pacific | Medium term (2-4 years) |

| Technological Advances Enhancing Algae Omega-3 Production Efficiency | + 1.7% | Global, concentrated in biotech hubs | Long term (≥ 4 years) |

| Growing Interest from Pharmaceutical Companies for Omega-3 Therapeutics | + 1.4% | North America & European Union, expanding to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Sustainable Plant-Based Omega-3 Ingredients

Consumer awareness of marine ecosystem degradation has catalyzed a fundamental shift toward algae-derived omega-3 sources, with algal oils offering identical EPA and DHA compositions to fish oil without environmental concerns. Life cycle assessments demonstrate that algae cultivation requires 25 days versus 24 months for fish oil production, while potentially sparing up to 22 million tons of fish annually if widely adopted. The sustainability imperative has gained regulatory support, with the Good Food Institute positioning animal-free omega-3 ingredients as critical for alternative seafood applications. Studies indicate 62% of omega-3 users prefer plant-based options, yet awareness of algal alternatives remains limited, presenting significant growth opportunities for education-focused marketing strategies. Regulatory compliance frameworks, including ISO 14001 environmental management standards, increasingly influence procurement decisions across food manufacturers seeking sustainable ingredient sourcing[2]Source: U.S. Environmental Protection Agency, "Frequent Questions About Environmental Management Systems", epa.gov .

Growing Regulatory Approvals for Algae-Derived Omega-3 Compounds

Regulatory momentum has accelerated dramatically, with multiple FDA GRAS notices issued for algae-derived omega-3 compounds and successful New Dietary Ingredient notifications clearing market access barriers[3]Source: FDA (Food and Drug Administration, "Docosahexaenoic Acid (DHA)-Rich Oil as a Food Ingredient for Use in Infant Formula and General Foods", fda.gov. Qualitas Health's AlmegaPL completed FDA NDI notification and received clearance as a medicine by Australia's Therapeutic Goods Administration, demonstrating the regulatory pathway's viability. The European Union's mandate requiring DHA in infant formula since February 2022 has created mandatory demand, with specifications ranging from 0.33-1.14% of total fat content. Clinical research supporting algal omega-3 efficacy continues expanding, with University of Toronto conducting dose-response investigations to inform Recommended Dietary Intake guidelines. Compliance with FSSC 22000, GMP+, and Kosher/Halal certifications has become standard practice among leading suppliers, facilitating global market penetration.

Expanding Research and Development Investments in Algae Farming

Venture capital and corporate R&D investments have surged, with companies like Provectus Algae raising USD 14.6 million across multiple funding rounds, including backing from Hitachi Ventures and CJ CheilJedang BIO. Advanced cultivation technologies are emerging, including MiAlgae's innovative approach utilizing whisky distillery waste streams to produce omega-3 rich microalgae while treating industrial effluent. Chinese manufacturers have made substantial commitments, with Xi'an Healthful Biotechnology investing approximately 110 million since 2022 to build thousand-ton fermentation production lines. Strain development has achieved breakthrough yields, with some Schizochytrium strains reaching up to 70% DHA content and thraustochytrids achieving oil content of 50-77% dry weight. Government support through grants and tax incentives, exemplified by Australia's government investment in Provectus Algae, indicates policy alignment with sustainable biotechnology development.

Increasing Use in Functional Foods and Nutraceutical Industries

Functional food applications have expanded beyond traditional supplement formats, with algae-derived omega-3s increasingly incorporated into plant-based dairy alternatives, nutrition bars, and fortified beverages. Bioriginal Food & Science Corp., a Cooke Inc. subsidiary, launched a comprehensive sustainable omega-3 line featuring algal oils alongside fish and plant-based options, targeting both human and pet nutrition markets. The infant formula sector represents a particularly dynamic growth area, with EU regulations mandating DHA inclusion creating substantial market opportunities for algal suppliers meeting stringent purity requirements. Clinical nutrition applications have gained traction, with algal omega-3s demonstrating comparable bioavailability to fish-derived sources while offering enhanced stability and neutral organoleptic properties. Major consumer brands including Nature's Bounty have rolled out algae-based omega-3 supplements across US retail channels, indicating mainstream market acceptance. Regulatory influence from FDA dietary supplement guidelines and EFSA health claim regulations continues shaping product development and marketing strategies.

Restraints Impact Analysis of Algae Omega-3 Ingredients Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense Competition from Established Fish Oil-Based Ingredients | -1.8% | Global, particularly in price-sensitive markets | Short term (≤ 2 years) |

| Price Sensitivity Due to Higher Production Costs Compared to Alternatives | -2.1% | Global, with higher impact in emerging markets | Medium term (2-4 years) |

| Dependence on Specific Algae Strains with Variable Yields | -1.3% | Global, concentrated in production hubs | Long term (≥ 4 years) |

| Risk of Contaminants and Quality Control Challenges | -0.9% | Global, with regulatory influence from FDA and EFSA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intense Competition from Established Fish Oil-Based Ingredients

The marine omega-3 market's established infrastructure and cost advantages present formidable competitive challenges for algae-derived alternatives. KD Pharma's acquisition of DSM-firmenich's MEG-3 fish oil business, including production facilities in Peru and Canada, demonstrates continued investment in traditional omega-3 sources despite sustainability concerns. Fish oil suppliers benefit from decades of supply chain optimization, established customer relationships, and significantly lower production costs, with Peru's anchoveta fishery alone supplying substantial volumes to global markets. Consumer familiarity with fish oil products creates marketing advantages, while established clinical research databases support health claims more extensively than newer algal alternatives. The competitive intensity has prompted strategic responses, including DSM-firmenich's strategic shift toward algae-based omega-3s while retaining fish oil operations for early life nutrition applications.

Price Sensitivity Due to Higher Production Costs Compared to Alternatives

Production cost disparities remain a significant market barrier, with algae cultivation requiring specialized bioreactor systems, controlled environmental conditions, and complex downstream processing compared to fish oil extraction. Fermentation-based production involves substantial capital investments in sterile cultivation facilities, precise nutrient management, and sophisticated purification technologies to achieve pharmaceutical-grade purity standards. Energy costs for maintaining optimal growth conditions, including temperature, pH, and oxygenation control, contribute to higher operational expenses compared to traditional fishing operations. However, technological advances are gradually reducing cost gaps, with companies like CABIO Biotech operating integrated manufacturing plants combining bio-fermentation, non-solvent extraction, and microencapsulation capabilities. Scale economies are emerging as production volumes increase, with Chinese manufacturers achieving cost reductions through thousand-ton fermentation capacity investments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Algae Omega-3 Ingredients Market Segment Analysis

By Type:

DHA Dominance Drives Specialized ApplicationsDHA (Docosahexaenoic acid) commanded 63.58% market share in 2025, reflecting its critical importance in brain development, cognitive function, and infant nutrition applications, where regulatory mandates create consistent demand. The segment's dominance stems from extensive clinical research demonstrating DHA's role in neural development and maintenance, particularly during pregnancy and early childhood development phases. EPA/DHA blends represent the fastest-growing segment with 14.30% CAGR through 2031, driven by formulator preferences for balanced omega-3 profiles that address both cardiovascular and neurological health benefits simultaneously.

Pure EPA (eicosapentaenoic acid) applications remain specialized, primarily targeting pharmaceutical and clinical nutrition markets where specific anti-inflammatory effects are desired. The University of Cincinnati's ongoing clinical trial comparing different omega-3 forms for dementia risk reduction exemplifies the continued research focus on optimizing DHA delivery mechanisms. Technological advances in strain optimization have enabled producers to achieve DHA concentrations up to 70% in certain Schizochytrium varieties, supporting premium positioning strategies. Regulatory compliance with FDA GRAS notices and EU (European Union) Novel Food regulations has streamlined market access for high-purity DHA ingredients across global markets.

By Application:

Supplements Dominate While Food Innovation AcceleratesDietary supplements captured 41.92% market share in 2025, benefiting from established consumer awareness of omega-3 health benefits and straightforward regulatory pathways for supplement manufacturers. The segment's maturity provides stable demand foundations while enabling premium positioning for algae-derived alternatives targeting environmentally conscious consumers. Food and beverages represent the fastest-growing application segment with 14.19% CAGR, indicating mainstream adoption beyond traditional supplement channels as manufacturers incorporate algal omega-3s into everyday food products.

Infant formula applications benefit from regulatory mandates, with EU requirements creating consistent demand for high-purity DHA meeting stringent contamination limits and nutritional specifications. Pharmaceutical applications show promising growth potential, supported by clinical trials investigating omega-3 therapeutics for conditions including retinitis pigmentosa and age-related macular degeneration. Clinical nutrition markets increasingly recognize algal omega-3s' advantages in medical food formulations where purity and allergen considerations are paramount. Animal nutrition applications, particularly aquaculture feeds, present emerging opportunities as fish farming operations seek sustainable alternatives to fish meal and fish oil inputs, with peer-reviewed research demonstrating comparable growth and feed conversion rates.

Geography Analysis

North America Algae Omega-3 Ingredients Market

North America maintained market leadership with a 37.61% share in 2025, supported by robust regulatory frameworks, including FDA (Food and Drug Administration) GRAS (Generally Recognized as Safe) approvals and established consumer awareness of omega-3 health benefits across dietary supplement and functional food categories. The region's dominance reflects mature market infrastructure, extensive clinical research capabilities, and strong venture capital support for biotechnology innovation, exemplified by companies like Qualitas Health securing FDA NDI notifications and TGA clearances for global market expansion. Major consumer brands, including Nature's Bounty, have successfully launched algae-based omega-3 products across US retail channels, demonstrating mainstream market acceptance and distribution capabilities. Canada's regulatory environment provides additional growth opportunities, particularly following KD Pharma's acquisition of DSM-Firmenich's marine lipids business, which included Canadian production facilities that could potentially pivot toward algae-based production.

APAC Algae Omega-3 Ingredients Market

Asia-Pacific emerges as the fastest-growing region with 13.06% CAGR through 2031, driven by rising disposable incomes, aging populations, and increasing health consciousness across China, Japan, and India. China's market development is particularly notable, with companies like CABIO Biotech operating world-scale LCPUFA manufacturing facilities and Lyxia developing proprietary downstream processing technologies for EPA production from Nannochloropsis salina strains. Japan's substantial DHA market, valued at approximately JPY 35 billion with 4-5% annual growth, has attracted strategic partnerships including Sumitomo Corporation's exclusive distributorship agreement with Huvepharma for algae-derived DHA. The region's regulatory landscape is evolving favorably, with Australia's TGA providing medicine clearances for algal omega-3 ingredients and China's GB standards establishing quality specifications for DHA products.

Europe Algae Omega-3 Ingredients Market

Europe represents a significant growth market supported by stringent regulatory requirements that favor high-purity algae-derived ingredients over potentially contaminated marine sources. Companies like Aliga Microalgae have established European production capabilities with FSSC (Food Safety System Certification) 22000 and GMP+ certifications, targeting dietary supplement brands and food manufacturers seeking locally-sourced sustainable ingredients. Ocean Rainforest's acquisition of Mexico's Alamarsa demonstrates cross-regional expansion strategies, combining Faroese seaweed farming expertise with Mexican processing capabilities to serve North American and European markets. Regulatory compliance with Novel Food regulations and EFSA (European Food Safety Authority) health claim requirements continues shaping product development and market access strategies across the region.

Regulatory Landscape

Regulation for algae omega-3 ingredients is anchored by pre-market safety pathways for novel microalgae oils and by product-category rules for foods, infant formula, and dietary supplements. In the United States, algae-derived DHA/EPA oils commonly enter as food ingredients through the FDA GRAS notice process, where dossiers emphasize strain identification, manufacturing controls, and exposure estimates. Recent activity includes Shaanxi Healthful Bioengineering Co., Ltd. filing GRAS Notice GRN 001236 (filed by FDA in February 2025 after an October 2024 submission, with amendments submitted in May 2025). In the European Union, the Novel Food framework requires an EFSA safety assessment prior to authorization, and DHA inclusion in infant formula (mandated since February 2022) creates a compliance-driven demand base for qualifying algal oils.

Standards development is also shaping cross-border commercialization. FAO/WHO Codex Alimentarius work in 2025/2026 to revise a proposed draft standard for microbial omega-3 oils (including algae-derived oils) supports harmonized definitions, quality expectations, and labeling approaches across importing markets. In parallel, jurisdiction-specific gatekeepers such as the General Administration of Customs of the People’s Republic of China (GACC) and Australia’s Therapeutic Goods Administration (TGA) influence market access and positioning for human nutrition and medicine-adjacent products, increasing the value of globally portable specifications and food safety certifications (for example, FSSC 22000 and related GMP schemes) among ingredient suppliers.

Value Chain Analysis

The value chain for algae omega-3 ingredients typically runs from strain/IP development and cultivation (fermentation or photobioreactor) through harvesting, extraction, and refining or concentration, then formulation (oil, powder, or encapsulated formats) for use in dietary supplements, functional foods, infant formula, and animal nutrition. Fermentation systems frequently rely on agricultural carbohydrate feedstocks such as sugarcane or corn-derived glucose, so upstream feedstock sourcing and utility costs matter to economics. Large producers often address this through facility siting and integrated operations, including Corbion’s algae ingredients platform and Brazil-linked integration approaches referenced in industry supply-chain materials. Downstream, formulators and brand owners translate refined DHA/EPA oils into finished products, while distributors and contract manufacturers help extend reach across supplements, food, and feed channels.

Quality, sustainability, and traceability requirements are increasingly embedded at multiple points in the chain, which affects supplier qualification and procurement. Certifications and standards referenced by market participants include ASC-MSC Seaweed/Algae-related standards, ISCC guidance for algae cultivation, and food safety and identity schemes (Non-GMO, Kosher, Halal) used to support multinational launches. In April 2026, GOED published a harmonized life cycle assessment guideline for omega-3 supply chains, reinforcing a shift toward comparable, cradle-to-gate sustainability reporting across algal, marine, and oilseed pathways, and adding documentation requirements that can influence ingredient selection and long-term supply agreements.

Competitive Landscape

The algae omega-3 ingredients market exhibits moderate concentration with established players leveraging technological advantages while emerging companies pursue niche opportunities through innovative production methods and strategic partnerships. Market leaders including dsm-firmenich, Corbion, and BASF maintain competitive positions through extensive R&D capabilities, global distribution networks, and regulatory expertise accumulated over decades of omega-3 ingredient development. These incumbents increasingly emphasize algae-derived alternatives, with DSM-firmenich positioning its life's®OMEGA platform as offering 2× potency compared to fish oil while enabling 25-day production cycles versus 24-month fish oil timelines.

Strategic consolidation continues reshaping competitive dynamics, exemplified by KD Pharma's acquisition of DSM-firmenich's MEG-3 fish oil business while DSM-firmenich simultaneously pivots toward algae-based omega-3 production. Emerging disruptors like MiAlgae pursue circular economy approaches, utilizing whisky distillery waste streams to produce omega-3 rich microalgae while providing waste treatment services to industrial partners. Technology differentiation has become increasingly critical, with companies like Qualitas Health developing proprietary polar-lipid structures claiming 1.7× superior bioavailability compared to conventional triglyceride forms.

Vertical integration strategies are emerging, with CABIO Biotech operating integrated facilities combining bio-fermentation, extraction, refining, and microencapsulation capabilities to capture value across the production chain. Opportunities exist in specialized applications including pharmaceutical therapeutics, where clinical trials investigating omega-3 treatments for retinitis pigmentosa and cognitive decline could unlock premium market segments. Regulatory compliance with FDA GRAS notices, EU Novel Food regulations, and ISO quality standards has become a competitive differentiator, particularly for suppliers targeting pharmaceutical and infant nutrition applications.

Algae Omega-3 Ingredients Industry Leaders

-

dsm-firmenich

-

Corbion N.V.

-

BASF

-

ADM

-

Neptune Wellness Solutions Inc.

- *Disclaimer: Major Players sorted in no particular order

Algae Omega-3 Ingredients Market Companies Covered in this Report

- Dsm-Firmenich

- Corbion N.V.

- BASF

- ADM

- Polaris Nutritional Lipids

- Neptune Wellness Solutions Inc.

- Algatechnologies Ltd.

- Solutex GC S.L.

- Cellana Inc.

- AlgaeCytes Ltd.

- Fermentalg SA

- Qualitas Health

- Veramaris V.O.F.

- Mara Renewables Corporation

- Cargill Incorporated

- Nordic Naturals

- Natures Way

- Novotech Nutraceuticals Inc.

- Source Omega LLC

- Algaecytes Limited

Market Opportunities and Future Outlook

Commercial whitespace is emerging where formulators need high-purity, non-fish omega-3 inputs that fit both performance and sustainability requirements across food, supplements, and animal nutrition. Product innovation is broadening beyond DHA-heavy oils into differentiated EPA:DHA profiles and higher-EPA offerings that align with use cases such as sports nutrition, healthy aging formulations, and functional formats (powders, gummies, beverage-compatible ingredients). For example, Fermentalg introduced Omega Origins in May 2026, positioned as a microalgae-derived oil with 40% EPA and 20% DHA. Portfolio expansion like this supports substitution of fish-oil inputs in finished products where sensory neutrality, contaminant control, and vegetarian positioning influence purchase decisions.

Scale-up and cost normalization opportunities are linked to new capacity and process models designed to improve yield and resource efficiency. MiAlgae’s December 2025 milestone for a large-scale facility in Grangemouth, Scotland, built around a circular feedstock concept using whisky by-products, illustrates how new plants are being designed to address both input cost structure and sustainability narratives. At the same time, regulatory clarity and market access progress (for example, GRAS pathways in the United States and Novel Food authorization in the European Union) support broader commercialization of new strains and processing technologies, while rising requirements for evidence-based sustainability claims raise the value of standardized reporting (such as GOED’s April 2026 LCA guideline) in competitive tendering with multinational food, supplement, pet food, and aquaculture customers.

Recent Industry Developments in Algae Omega-3 Ingredients Market

- June 2026: Corbion published an updated life cycle assessment for its algae-derived omega-3 DHA, reporting an 18% to 23% lower climate change impact versus its 2021 assessment. The update supports carbon-accounting claims used in procurement decisions across aquaculture, pet food, and human nutrition customers comparing algal oils with marine alternatives.

- July 2025: Corbion secured Chinese regulatory approvals from the General Administration of Customs (GACC) for its algae-derived omega-3 DHA products for human and animal nutrition, supporting commercialization of AlgaPrime DHA and AlgaVia DHA in China. The approvals broaden access to a large end-market and reinforce regulatory readiness as a differentiator for global algal ingredient suppliers.

- October 2024: dsm-firmenich expanded its life’s omega-3 nutraceutical portfolio with the launch of life’s DHA B54-0100, positioned as its most potent DHA oil at launch. The higher concentration enables smaller-dose formats and more flexible formulation options for supplement brands targeting premium omega-3 positioning with algal sourcing.

Algae Omega-3 Ingredients Market Report Scope and Research Methodology

Market Definition and Coverage

This market tracks the sales value of omega-3 ingredients that are derived from algae and then sold for use in downstream formulations such as supplements, food fortification, infant nutrition, pharmaceuticals, and animal nutrition.

Scope exclusions: finished consumer products (for example, branded capsules or ready-to-drink products) and omega-3 sources that are not algae-derived are excluded from this sizing.

Segments Covered in This Report

-

By Type

- Eicosapentaenoic Acid (EPA)

- Docosahexaenoic Acid (DHA)

- EPA / DHA Blends

-

By Application

- Food and Beverages

- Dietary Supplements

- Infant Formula

- Pharmaceuticals

- Clinical Nutrition

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean map of what is being sold, where it is used, and how value is typically reported across regions. Public and official sources help anchor assumptions, such as US FDA GRAS notices, European Commission and EFSA updates on novel foods and infant nutrition requirements, FAO fisheries and aquaculture statistics (as a demand signal for feed use), and trade and customs statistics for fats, oils, and specialty ingredients.

We also review company annual reports, investor presentations, press releases, and association websites to understand capacity additions, product launches, and application mix shifts. A paid subscription covering company financials and a separate patent database are used selectively to confirm corporate activity, technology pathways (for example, strain and extraction themes), and to avoid missing new entrants. These desk sources are not exhaustive, and additional public references are used for cross-checking, data collection, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test the demand pool and pricing logic, especially where public data does not directly break out algae-derived omega-3 ingredient value. We speak with ingredient suppliers, formulators, distributors, and downstream buyers across supplements, infant nutrition, food fortification, and animal nutrition, with coverage balanced across major consuming and producing regions so assumptions can be confirmed and then adjusted where needed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 17% | APAC: 40% |

| Mid tier: 51% | Functional/Unit leaders: 28% | EMEA: 33% |

| Smaller Players: 18% | Managers: 55% | Americas: 27% |

Market-Sizing & Forecasting

Sizing is built using a top-down and bottom-up combination, with the main structure coming from a top-down demand pool that is reconstructed from application consumption and adoption rates. For example, we estimate the addressable intake by application (supplements, infant nutrition, food fortification, animal nutrition, and pharma use), apply algae omega-3 penetration ranges, and then translate that into value using price bands that reflect concentration and grade.

To keep totals realistic, the model is corroborated using selective bottom-up checks, such as a roll-up of supplier revenues where disclosures exist, sampled volume and average selling price (ASP) builds for key application routes, and channel checks on typical contract pricing movements. Inputs that matter in this market include DHA versus EPA share, inclusion rates in infant formula, growth in plant-based nutrition adoption, relative pricing versus fish oil, and capacity utilization signals from announced expansions and commercialization timelines. For forecasting, scenario analysis is used because adoption and pricing can shift with regulation, supply expansions, and formulation trends, and those scenarios are validated through expert consensus gathered in interviews. Where bottom-up detail is missing, gaps are handled by applying conservative ranges and then narrowing them only after re-checking with multiple respondent types.

Data Validation & Update Cycle

Validation is done by triangulating model outputs against independent signals, followed by a structured variance check by analysts before numbers are finalized. Large swings are investigated by tracing them back to specific drivers like ASP changes, application mix, or adoption assumptions, and then re-confirmed through follow-up outreach when the variance cannot be explained by public facts.

The report is refreshed annually, and interim adjustments are made when material events occur, such as regulatory changes, new production capacity coming online, or major shifts in ingredient pricing. Before delivery, we do a final refresh pass so the figures reflect the latest available information and the most current set of assumptions.

Mordor Intelligence's Algae Omega 3 Ingredient Market Estimate Compared With Other Published Estimates

Different publications can show different values for the same market because they do not always count the same revenue layers, and they also vary on which applications and grades get included in the total. Differences in base year selection, currency conversion timing, and whether pricing is modeled as spot-driven or contract-driven can widen the spread further.

Finished consumer supplement products sit outside Mordor Intelligence's scope here, which is why estimates that bundle retail nutrition sales with ingredient revenues usually land at a higher 2024 value even when they use similar growth narratives.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.56 B (2026) | |

| Global Consultancy A | USD 1.20 B (2024) | Uses an earlier base year and appears to apply broader price averages without consistently separating concentration grades, which can compress value when higher-DHA ingredients are a larger share. |

| Industry Publisher B | USD 1.28 B (2024) | Likely mixes ingredient and finished-product revenue signals in parts of the narrative and applies a fixed CAGR window, which can shift the starting-year value when adoption accelerates unevenly by application. |

Across the three figures, most of the gap is explained by what is counted as ingredient revenue versus downstream product revenue, plus differences in base year and how ASP changes are handled. By tying value to clear application demand signals and price bands by grade, the market total stays traceable and can be re-checked in a repeatable way when new capacity or regulations shift the demand mix.

Key Questions Answered in the Report

What is the projected value of the algae omega-3 ingredients market by 2031?

The market is forecast to reach USD 2.73 billion by 2031, reflecting a 11.74% CAGR.

Which omega-3 type currently dominates commercial demand?

DHA leads with 63.58% revenue share due to its critical role in infant nutrition and cognitive health.

Which region is expected to grow fastest through 2031?

Asia-Pacific is projected to register a 13.06% CAGR, driven by rising incomes and health awareness in China, Japan, and India.

Why are algae sources preferred over fish oil for new product launches?

Algae oils offer sustainability, heavy-metal-free purity, and vegetarian suitability, meeting rising ESG and dietary requirements.

Page last updated on: