Marine Gensets Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 6.86 Billion |

| Market Size (2031) | USD 8.25 Billion |

| Growth Rate (2026 - 2031) | 3.75% CAGR |

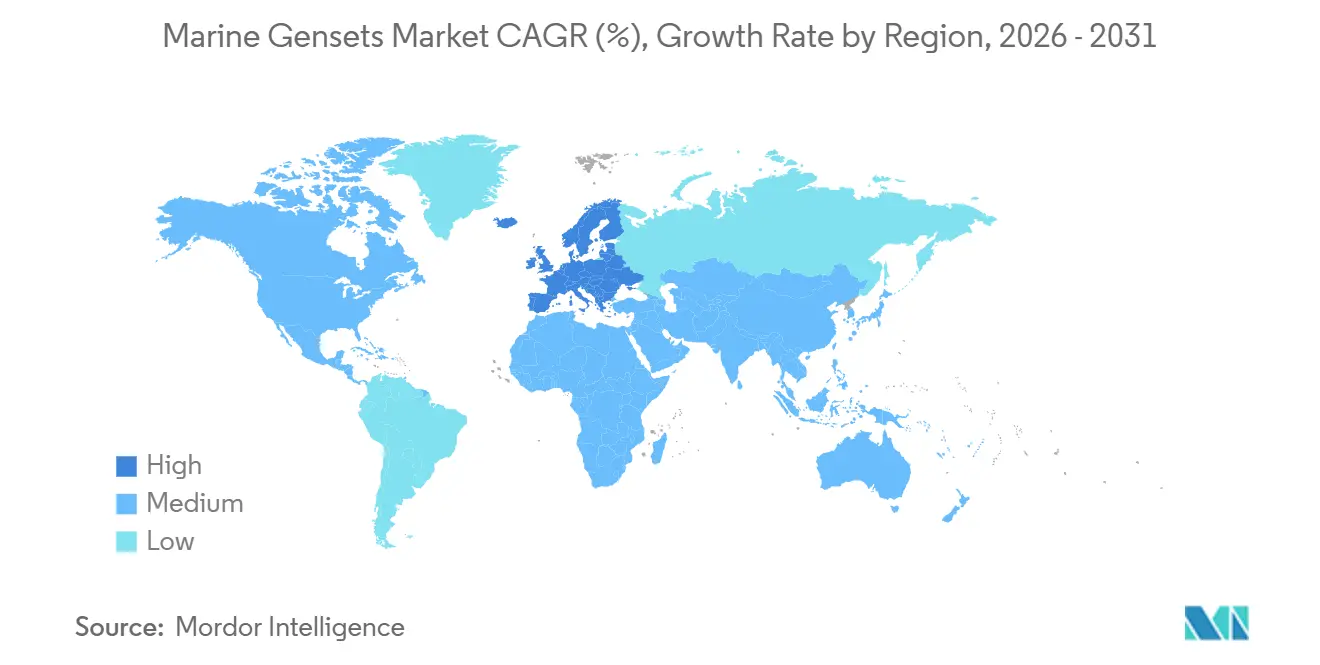

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Marine Gensets Market Analysis by Mordor Intelligence

The Marine Gensets Market size is expected to grow from USD 6.58 billion in 2025 to USD 6.86 billion in 2026 and is forecast to reach USD 8.25 billion by 2031 at 3.75% CAGR over 2026-2031. Regulatory pressure from the International Maritime Organization’s tightened Carbon Intensity Indicator and the European Union’s FuelEU Maritime rule is steering shipowners toward hybrid diesel-electric packages, battery buffering, and shore-power interfaces. Diesel units still dominate, but hybrid configurations are climbing swiftly as battery prices fall below USD 150 per kilowatt-hour and cold-ironing mandates proliferate. Demand is strongest in Asia-Pacific, where China’s and South Korea’s yards command a combined 84% share of newbuild orders, while Europe is the fastest-growing region as ferry and cruise operators retrofit for greenhouse-gas compliance. North American naval programs and Middle Eastern offshore projects create smaller, high-specification niches. Top suppliers - Caterpillar, MAN Energy Solutions, Wärtsilä, Rolls-Royce, and Cummins - control roughly 55% to 60% of revenue, yet regional specialists such as Yanmar and Daihatsu retain footholds in fishing and workboat segments that prefer compact, air-cooled designs.[1]International Maritime Organization, “Marine Environment Protection Committee 83rd Session,” imo.org

Key Report Takeaways

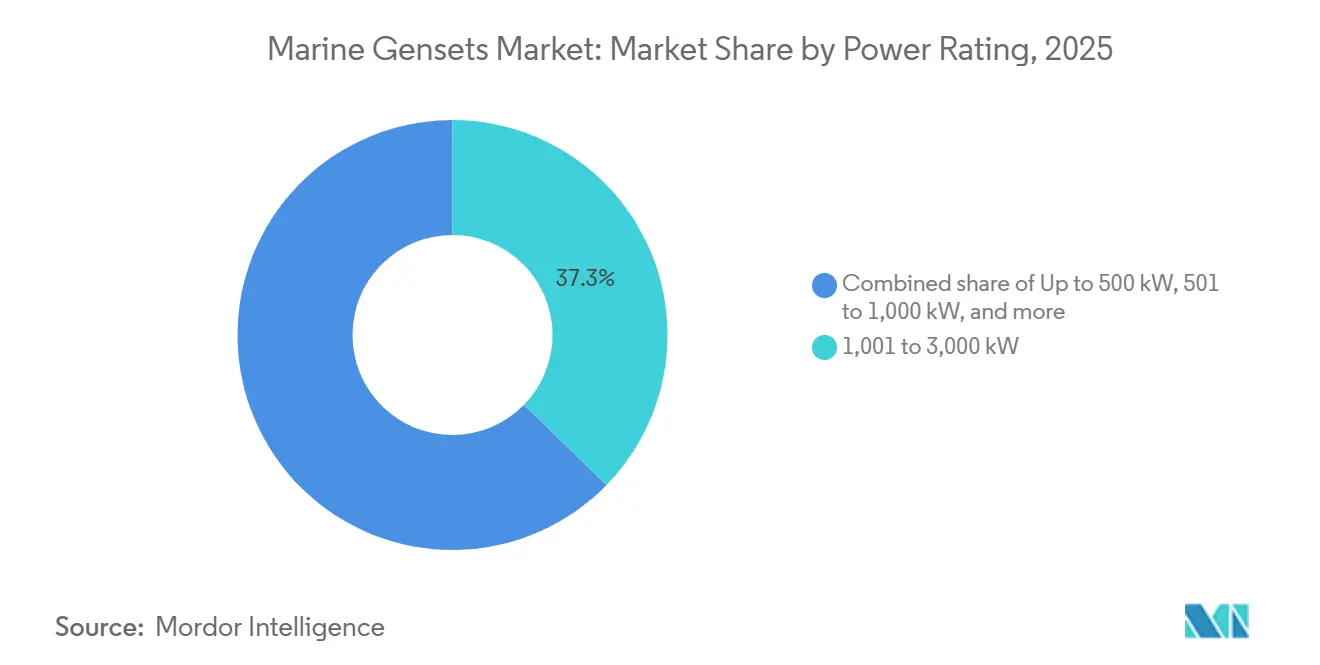

- By power rating, the 1,001–3,000 kilowatt bracket led with 37.3% of marine gensets market share in 2025, while sub-500 kilowatt units are projected to expand at a 5.9% CAGR through 2031.

- By fuel type, diesel accounted for 70.1% of the marine gensets market size in 2025; hybrid diesel-electric systems are expected to advance at a 6.3% CAGR over 2026–2031.

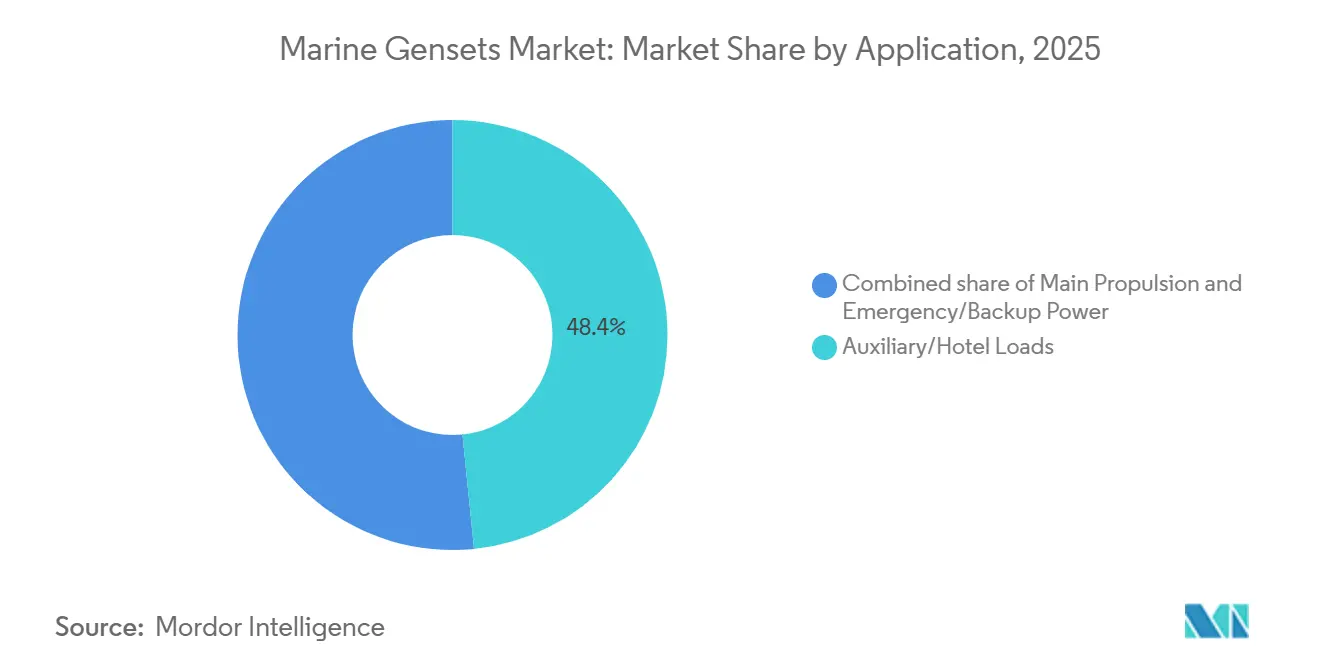

- By application, auxiliary and hotel loads captured 48.4% share of the marine gensets market size in 2025, while emergency power is set to grow at a 5.0% CAGR to 2031.

- By vessel type, commercial cargo vessels held 23.6% of marine gensets market share in 2025; defense and naval platforms are projected to record the highest CAGR, at 5.5%, through 2031

- By geography, Asia-Pacific held 45.2% of marine gensets market share in 2025; Europe is expected to grow CAGR at 4.6% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Marine Gensets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Marine Trade Activities | +0.6% | Asia-Pacific, Europe | Medium term (2-4 years) |

| Technological Advancements in Genset Design & Hybridization | +0.8% | Europe, North America, select Asia-Pacific yards | Long term (≥ 4 years) |

| Stringent IMO Tier III & CII Emission Regulations | +1.2% | Global | Short term (≤ 2 years) |

| Rising Demand for Offshore Support Vessels (OSVs) | +0.4% | Middle East, West Africa, North Sea, Southeast Asia | Medium term (2-4 years) |

| Adoption of On-Board Microgrids / DC Power Architectures | +0.3% | Nordic countries, Japan, North America pilots | Long term (≥ 4 years) |

| Cold-Ironing Retrofits Driving Load-Following LNG-Ready Gensets | +0.5% | EU ports, California, China coastal hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Marine Trade Activities

Global seaborne trade reached 12,720 million tons in 2024, and route diversions around the Red Sea are lengthening voyages and increasing auxiliary-power demand.[2]United Nations Conference on Trade and Development, “Review of Maritime Transport 2024,” unctad.org A 10 million TEU container-ship orderbook, equal to roughly one-third of the active fleet, embeds the newest auxiliary technologies yet risks oversupply if ton-mile growth lags. Older gensets remain in service as scrapping slows, sustaining a retrofit aftermarket for emission-control modules. Operators hedge geopolitical uncertainty by favoring modular genset banks that can be re-sorted as route economics shift, rewarding suppliers of plug-and-play auxiliary packages.

Technological Advancements in Genset Design & Hybridization

Wärtsilä recorded 31 hybrid-propulsion and 46 hybrid-auxiliary installations in 2024, confirming the pivot to battery-buffered architectures that let gensets run near peak efficiency.[3]Wärtsilä Corporation, “Marine Power Solutions—Hybrid and Battery Systems,” wartsila.com Corvus Energy has delivered over 3,000 MWh of maritime batteries, enabling ferries to shut down engines during port stays.[4]Corvus Energy, “Maritime Battery Systems Delivered Capacity,” corvusenergy.com Ballard’s FCwave fuel-cell module entered sea trials on a Norwegian OSV, hinting at hydrogen’s auxiliary potential. DC microgrids from ABB and Siemens eliminate frequency-sync constraints, reduce harmonic distortion, and simplify battery integration on cruise ships whose hotel loads swing drastically.

Stringent IMO Tier III & CII Emission Regulations

The IMO will tighten the Carbon Intensity Indicator by 11% in 2026 versus the 2019 baseline, pushing under-performing vessels into D or E ratings that trigger inspections and charter penalties. The EU Emissions Trading System prices full life-cycle emissions from 2026, including methane and nitrous oxide, eroding LNG’s cost edge unless methane slip is controlled. California’s expanded at-berth rule forces tankers and ro-ro vessels to install load-following gensets able to ramp to 10% within minutes of shore-power connection. Divergent flag-state protocols raise certification costs for manufacturers validating equipment across multiple classification societies.

Rising Demand for Offshore Support Vessels (OSVs)

OSV utilization hit 76% in 2025 and is projected to surpass 79% by 2027 as offshore EPC spending climbs from USD 54 billion in 2025 to USD 71 billion in 2026 on Saudi Aramco and Mozambique LNG activity. Offshore wind drives service-operation-vessel orders needing 500-1,500 kilowatt gensets for dynamic positioning in emission-control areas. Selective catalytic-reduction retrofits add 8%-12% to genset capital cost but are favored over complex dual-fuel systems in remote fields.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital expenditure | -0.7% | Global, with acute pressure in emerging markets (SEA, MEA) | Short term (≤2 years) |

| Volatile marine diesel & LNG prices | -0.5% | Global, with highest exposure in spot-charter markets | Short term (≤2 years) |

| Certification & compliance complexity across flag states | -0.3% | Global, with delays in dual-fuel and alternative-fuel approvals | Medium term (2–4 years) |

| Supply-chain bottlenecks for high-pressure fuel-injection components | -0.4% | Global, with OEMs lacking captive foundry capacity most exposed | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure

A 2-megawatt dual-fuel genset with selective catalytic reduction costs 35%-45% more than a diesel-only unit, while battery-hybrid packages can lift auxiliary-power spend on a mid-size ferry to USD 8 million. Finance hurdles persist: interest rates on ship mortgages exceeded 6% in 2025, and lenders often exclude hybrid retrofits from collateral value estimates. Operating-hour leasing from Caterpillar and Siemens converts capex to opex but covers less than 15% of placements, restricted to top-tier credits.

Volatile Marine Diesel & LNG Prices

Very-low-sulfur fuel oil fell 16% between January 2024 and February 2026, while LNG slid 32%, compressing the differential that justifies dual-fuel genset premiums. Geopolitical rerouting added up to 20% bunker consumption and USD 40 per-ton price spreads between Singapore and Rotterdam in 2025. LNG supply remains concentrated in fewer than 200 ports, forcing dual-fuel vessels to carry diesel reserve and eroding perceived flexibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Rating: Distributed Architectures Outpace Monolithic Sets

The 1,001 to 3,000 kilowatt band held 37.3% marine gensets market share in 2025, matching the auxiliary needs of Panamax container ships and Aframax tankers. Up to 500 kilowatt systems, though smaller in value, are forecast to grow at 5.9% annually as battery-electric ferries and patrol vessels adopt modular range-extender gensets. Rolls-Royce’s 2025 contract for eight 2,840-kilowatt MTU units on Baleària electric ferries highlights the shift toward smaller safety-critical sets. The marine gensets market size for units above 5 megawatts remains niche, focused on ultra-large container ships and FPSOs where single gensets can exceed 10 megawatts. Operators increasingly specify four 2.5 megawatt machines instead of two 5 megawatt ones, adding 5%-8% upfront yet cutting unscheduled downtime by 20% over a 15-year life.

By Fuel Type: Hybrid Configurations Challenge Diesel Dominance

Diesel retained 70.1% of 2025 revenue, but hybrid diesel-electric systems are expanding at 6.3% annually to 2031. Battery costs have plunged, and shore-power mandates reward gensets that run at 70%-85% load while batteries manage peaks. Dual-fuel LNG-diesel units held a significant share, centered on LNG carriers and cruise ships where gas is already onboard. Fuel-cell or battery-assisted gensets show double-digit gains as Ballard FCwave and Corvus battery packs reach serial production. Skill gaps limit adoption; hybrid systems need engineers with battery and gas-handling expertise who command 15%-25% wage premiums in Northern Europe and the U.S. Gulf.

By Application: Emergency Power Gains Regulatory Tailwind

Auxiliary and hotel loads captured 48.4% of 2025 revenue, underpinned by cruise ships whose hotel demands can equal propulsion loads. Emergency and backup sets grow at 5.0% thanks to SOLAS rules requiring separate gensets that auto-start within 45 seconds and run 18 hours at full load on passenger ships. Classification society requirements for independent fuel tanks and location above the bulkhead deck favor modular, type-approved packages. Battery-hybrid ferries reclassify gensets as range extenders, altering maintenance and insurance regimes, yet still counted under auxiliary roles in most taxonomies.

By Vessel Type: Defense Orders Accelerate

Commercial cargo vessels held 23.6% share in 2025 owing to fleet scale, but defense platforms post the highest CAGR at 5.5% as India targets 230 new hulls by 2037 and the U.S. Navy funds 19 vessels in fiscal 2026 with ruggedized gensets. LNG carriers and cruise ships demand 3,000-5,000 kilowatt sets for refrigeration and hotel loads, while OSVs require dynamic-positioning-ready units maintaining station within 1 meter under 25-knot winds. Fishing and workboats still opt for sub-500-kilowatt air-cooled designs, prioritizing parts availability over emission sophistication.

Geography Analysis

Asia-Pacific generated 45.2% of 2025 revenue, underpinned by China’s 63%-70% share of global shipbuilding volume and South Korea’s 70% share of LNG-carrier orders. Korean engine exports to China topped USD 1.29 billion in 2024, reflecting tight regional integration. Japan’s consolidation, including Tsuneishi’s acquisition of Mitsui E&S shipbuilding assets, aims to secure larger genset contracts. India’s Maritime Vision 2030 seeks 5% global share yet relies on imported auxiliary systems.

Europe is the fastest-growing region at a 4.6% CAGR through 2031, propelled by FuelEU Maritime penalties that drive hybrid retrofits and shore-power adoption. Norway’s NOx Fund subsidizes hybrid ferries, and Sweden’s fee discounts spur cold-ironing upgrades. Naval projects-Germany’s EUR 5.3 billion F126 frigate build and the UK Type 26 program-support demand for shock-qualified gensets near Kiel, Hamburg, and Glasgow yards.

North America and the Middle East form smaller yet high-specification pockets. The U.S. Navy’s USD 47.4 billion FY 2026 build plan fuels emergency-genset orders, though schedule slippage pushes the Pentagon to explore sustainment tie-ups with Korean, Japanese, and Indian yards. Canada’s CAD 40 billion National Shipbuilding Strategy sources Caterpillar and Cummins sets for Arctic patrol and support ships. Offshore expansion in Saudi Arabia and Mozambique lifts OSV orders needing 3,000 kilowatt-plus gensets, while Brazil’s pre-salt projects and South Africa’s patrol-vessel buys offer selective wins for European suppliers.

Competitive Landscape

The marine gensets market is moderately concentrated. Wärtsilä leverages battery integration and lifecycle-service contracts that can equal 40%-50% of customer lifetime value. MAN Energy Solutions dominates LNG-carrier gensets with ME-GI and ME-LGI dual-fuel lines, bundling proprietary fuel-gas supply systems. ABB’s Onboard DC Grid positions the company as a power-management orchestrator rather than engine maker. Disruptors such as Corvus Energy and Ballard enter via control software and fuel-cell modules, respectively, while regional specialists like Yanmar and Anglo Belgian Corporation serve price-sensitive sub-500-kilowatt niches. Predictive-maintenance analytics embedded in Rolls-Royce MTU units detect anomalies 500-1,000 hours in advance, justifying a 10%-15% price premium.

Marine Gensets Industry Leaders

Caterpillar Inc.

Wärtsilä Corporation

MAN Energy Solutions

Cummins Inc.

Rolls-Royce plc (Bergen/MTU)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The Indian Navy commissioned INS Taragiri with four indigenous Cummins-Kirloskar gensets totaling 4 MW.

- March 2026: ABB and Sembcorp Marine agreed to retrofit 12 OSVs with 60 MWh of batteries and DC grids.

- December 2025: Caterpillar expanded its Lafayette, Indiana, plant, boosting marine genset capacity by 30%.

- March 2025: Cummins secured DNV type approval for its QSK60 2,700 kW genset.

Global Marine Gensets Market Report Scope

A marine genset is a power generation unit specifically designed to supply electrical energy for boats, ships, and other maritime vessels. It comprises two main components: an internal combustion engine (the driver) and an alternator (the electrical generator).

The Marine Gensets Market is segmented into power rating, fuel type, application, vessel type, and geography. By power rating, the market is segmented into up to 500 kW, 501 to 1,000 kW, 1,001 to 3,000 kW, 3,001 to 5,000 kW, and above 5,000 kW. By fuel type, the market is segmented into diesel, gas, hybrid diesel-electric, dual-fuel, and fuel-cell/battery-assisted systems. By application, the market is segmented into main propulsion, auxiliary/hotel loads, and emergency/backup power. By vessel type, the market is segmented into commercial cargo, tankers and bulk carriers, container ships, OSVs, defense/naval vessels, leisure and passenger vessels, and fishing and workboats. The report also covers the market size and forecasts for the marine gensets market across major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Up to 500 kW |

| 501 to 1,000 kW |

| 1,001 to 3,000 kW |

| 3,001 to 5,000 kW |

| Above 5,000 kW |

| Diesel |

| Gas (NG/LPG) |

| Hybrid Diesel-Electric |

| Dual-Fuel (LNG + Diesel) |

| Fuel-Cell/Battery-Assisted |

| Main Propulsion |

| Auxiliary/Hotel Loads |

| Emergency/Backup Power |

| Commercial Cargo Vessels |

| Tankers and Bulk Carriers |

| Container Ships |

| Offshore Support Vessels |

| Defense/Naval Vessels |

| Leisure and Passenger (Cruise/Ferry/Yacht) |

| Fishing and Workboats |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Power Rating | Up to 500 kW | |

| 501 to 1,000 kW | ||

| 1,001 to 3,000 kW | ||

| 3,001 to 5,000 kW | ||

| Above 5,000 kW | ||

| By Fuel Type | Diesel | |

| Gas (NG/LPG) | ||

| Hybrid Diesel-Electric | ||

| Dual-Fuel (LNG + Diesel) | ||

| Fuel-Cell/Battery-Assisted | ||

| By Application | Main Propulsion | |

| Auxiliary/Hotel Loads | ||

| Emergency/Backup Power | ||

| By Vessel Type | Commercial Cargo Vessels | |

| Tankers and Bulk Carriers | ||

| Container Ships | ||

| Offshore Support Vessels | ||

| Defense/Naval Vessels | ||

| Leisure and Passenger (Cruise/Ferry/Yacht) | ||

| Fishing and Workboats | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the size of the marine gensets market?

The marine gensets market stands at USD 6.86 billion in 2026 and is expected to reach USD 8.25 billion by 2031, expanding at a 3.75% CAGR over 2026-2031.

How fast is demand for hybrid diesel-electric gensets growing?

Hybrid diesel-electric units are advancing at a 6.3% CAGR over 2026-2031 as battery costs fall and cold-ironing rules tighten.

Which power-rating segment is expanding the quickest?

Sub-500 kilowatt gensets are projected to grow at 5.9% annually, driven by battery-electric ferries and offshore patrol vessels.

Why is Europe the fastest-growing regional market?

The EU's FuelEU Maritime rule, NOx Fund incentives, and shore-power mandates push ferry and cruise operators to retrofit faster than other regions.

How concentrated is supplier competition?

Five vendors Caterpillar, MAN Energy Solutions, Wärtsilä, Rolls-Royce, and Cummins' control about major share of revenue, indicating moderate concentration.

What regulatory change will most affect genset choices in the near term?

The IMO's 11% tightening of the Carbon Intensity Indicator in 2026 will compel shipowners to upgrade or replace older auxiliary gensets.

Page last updated on: