Algae Supplements Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

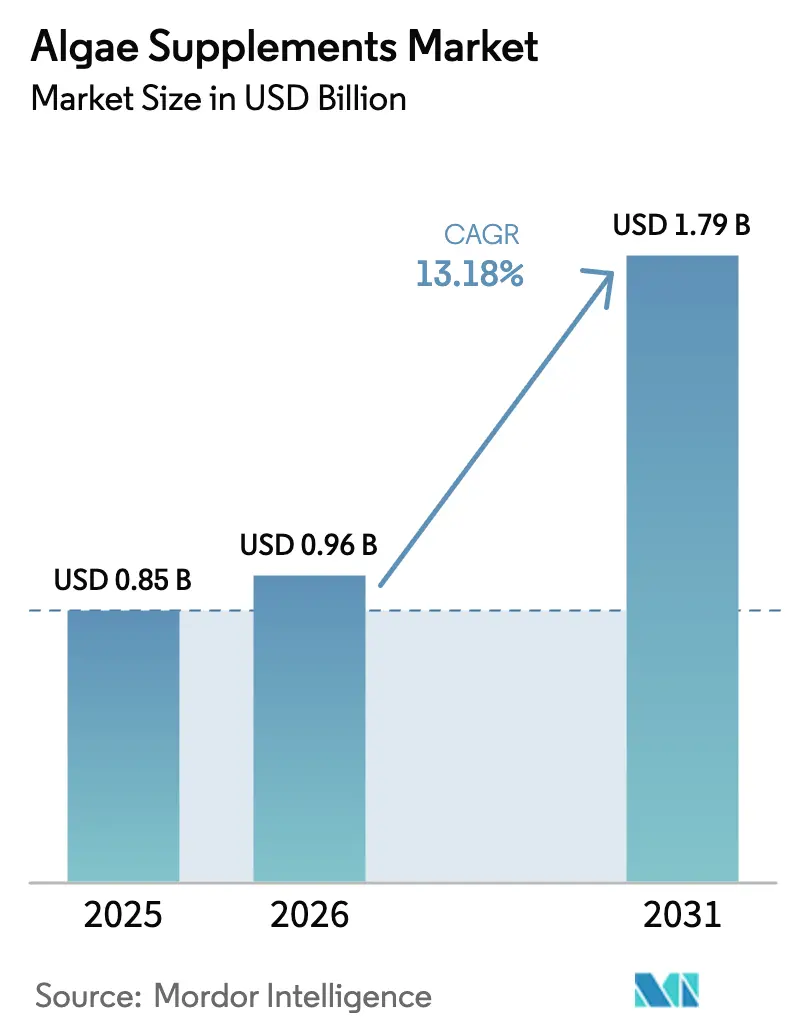

| Market Size (2026) | USD 0.96 Billion |

| Market Size (2031) | USD 1.79 Billion |

| Growth Rate (2026 - 2031) | 13.18% CAGR |

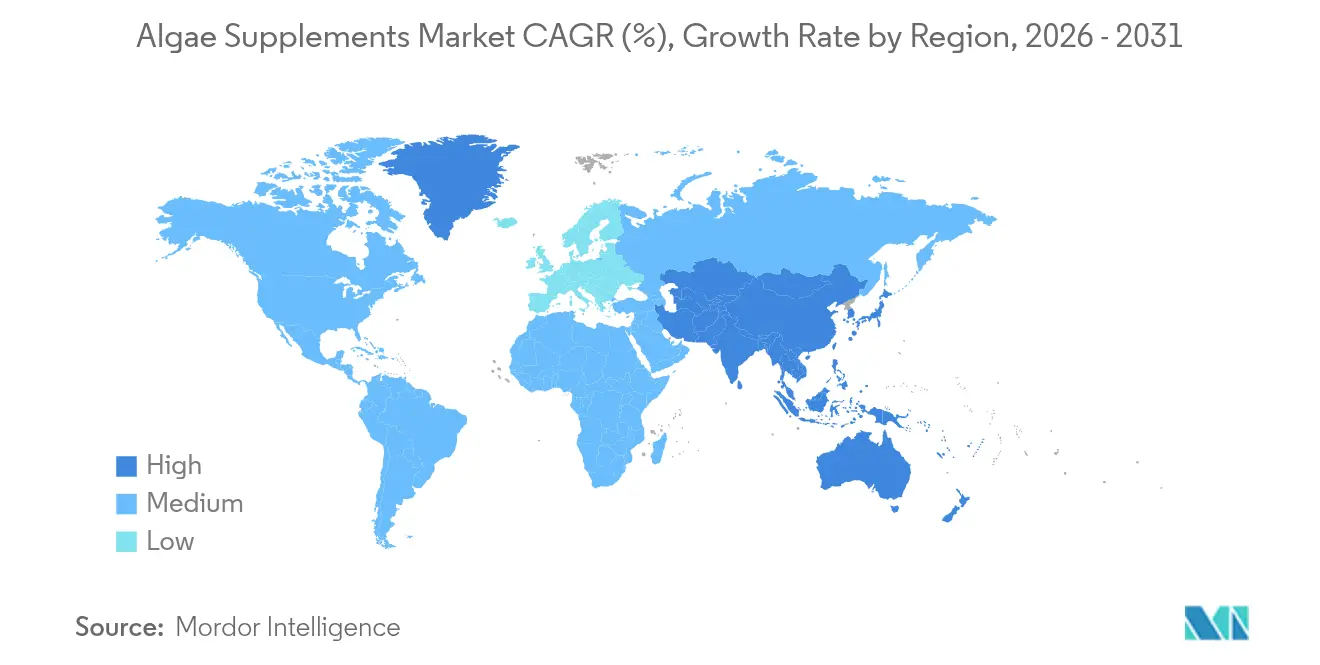

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

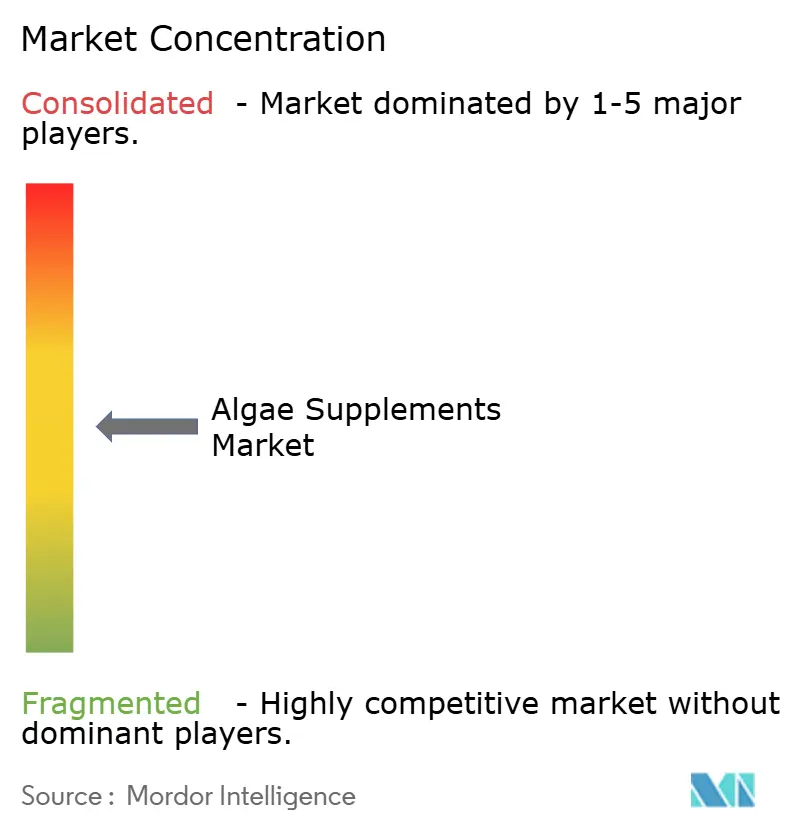

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Algae Supplements Market Analysis by Mordor Intelligence

The algae supplements market size in 2026 is estimated at USD 0.96 billion, growing from 2025 value of USD 0.85 billion with 2031 projections showing USD 1.79 billion, growing at 13.18% CAGR over 2026-2031. This double-digit trajectory reflects mounting consumer interest in sustainable plant-based nutrition, rapid regulatory clearances for novel algae species, and steady gains in extraction efficiency that compress cost curves while preserving nutrient density. Spirulina continues to anchor category sales, yet chlorella’s faster uptick signals a broadening product mix shaped by detoxification and immune-support claims. Asia-Pacific’s sizeable middle class, Europe’s rulemaking momentum, and North America’s preference for clean-label formulations converge to keep the algae supplements market on a steep growth slope. Advances such as hydrodynamic cavitation that raise yields and cut energy use strengthen the economic case for algae cultivation even as consumer education gaps in several emerging economies remain a near-term drag on uptake.

Key Report Takeaways

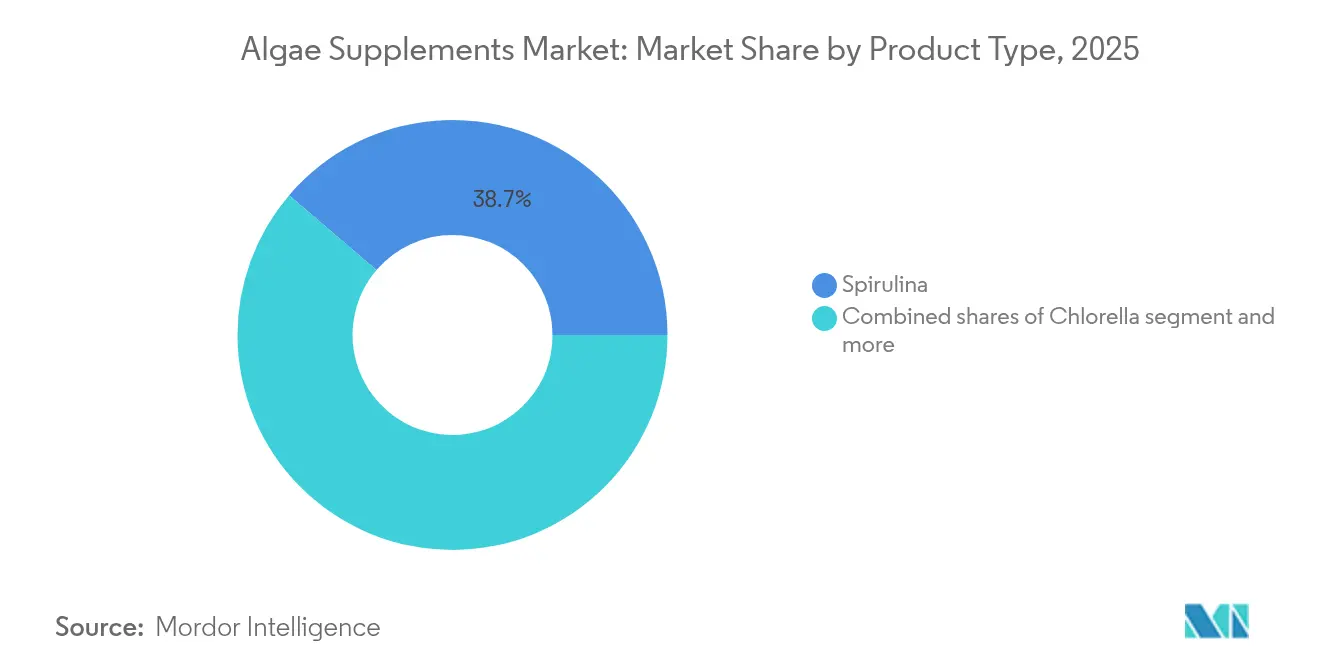

- By product type, spirulina held 38.74% of the algae supplements market share in 2025, while chlorella is set to expand at a 15.27% CAGR between 2026-2031.

- By form, powder led with 38.92% revenue share in 2025, while capsules are projected to register a 14.32% CAGR through 2031.

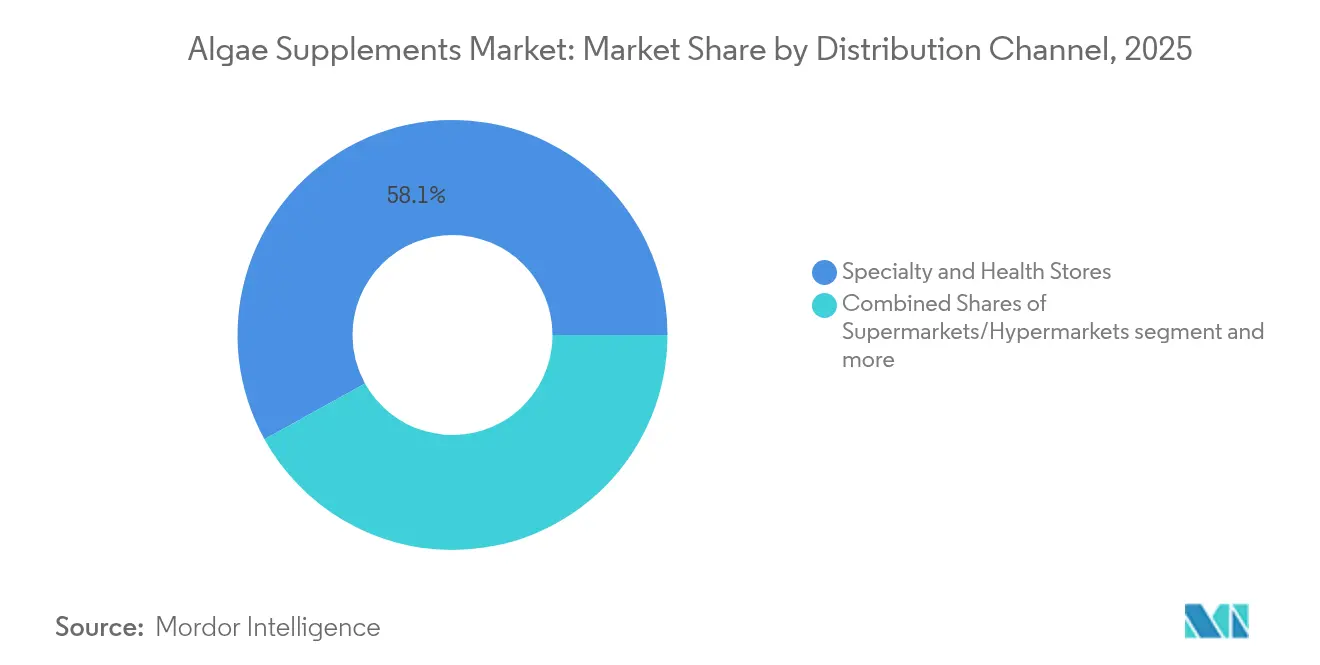

- By distribution channel, specialty and health stores captured 58.05% of the 2025 share, whereas online retailers are predicted to deliver the fastest growth at 14.58% CAGR to 2031.

- By geography, Asia-Pacific commanded 37.95% of the 2025 share and is forecast to climb at a 15.12% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Algae Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Consumer Preference for Clean-Label, Allergen-Free Supplements | +2.8% | Global, with strongest adoption in North America and Europe | Medium term (2-4 years) |

| Rising Demand for Plant-Based Omega-3 Alternatives | +3.2% | Global, particularly Asia-Pacific and North America | Long term (≥ 4 years) |

| Increasing Awareness of Spirulina and Chlorella Health Benefits | +2.1% | Asia-Pacific core, expanding to Middle East and Africa and Latin America | Medium term (2-4 years) |

| Higher Consumption of Nutrient-Dense Supplements Among Aging Populations | +1.9% | North America and Europe, emerging in Asia-Pacific urban centers | Long term (≥ 4 years) |

| Environmental Sustainability of Algae Production | +1.7% | Europe and North America leading, global spillover | Long term (≥ 4 years) |

| Rising Prevalence of Lifestyle-Related Diseases | +2.4% | Global, with accelerated impact in urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Preference for Clean-Label, Allergen-Free Supplements

The clean-label movement is changing supplement formulation strategies, as algae-based products meet consumer demands for transparent, minimally processed ingredients. According to a study by the International Food Information Council [1]International Food Information Council, "2023 Food and Health Survey", www.ific.org, 29% of consumers in the United States preferred purchasing products with clean ingredients, highlighting a significant market opportunity for algae supplements. Algae-based alternatives provide cleaner profiles and traceable cultivation methods compared to traditional fish-derived omega-3 supplements, which may contain heavy metals or require extensive purification. The United States Food and Drug Administration's GRAS approval for Euglena gracilis biomass in 2024, allowing maximum use levels of 500 mg per serving across multiple food categories, demonstrates regulatory acceptance of algae's safety profile and enables broader food fortification applications. This regulatory status benefits algae producers by allowing faster product development cycles through established safety profiles. The allergen-free nature of algae products offers advantages as food sensitivity awareness grows, avoiding common allergens such as shellfish, dairy, and gluten that limit traditional supplement formulations.

Rising Demand for Plant-Based Omega-3 Alternatives

As consumer demand for sustainable and reliable nutrition sources grows, plant-based omega-3 alternatives are emerging as a compelling solution to traditional marine-derived options. According to the DSM-Firmenich report from 2024, 64% of consumers indicate a willingness to switch from fish oil to plant-based omega-3 alternatives due to sustainability concerns and supply chain reliability. Algal omega-3 production demonstrates enhanced efficiency with 25-day production cycles, compared to 24-month cycles for fish oil, while providing comparable EPA and DHA concentrations without contamination risks. Microalgae fermentation technology enables consistent year-round production, independent of fishing seasons or marine ecosystem disruptions. The focus on concentration levels benefits algae producers who achieve higher omega-3 densities through optimized cultivation and extraction methods. The plant-based nature of algal omega-3 also allows manufacturers to target vegetarian and vegan consumer segments that traditionally avoid marine-derived supplements.

Increasing Awareness of Spirulina and Chlorella Health Benefits

Research validating the health benefits of microalgae supports wider market acceptance. Studies show that spirulina's phycocyanin compounds protect mitochondrial function and regulate oxidative stress, contributing to anti-aging effects. The compounds work by neutralizing free radicals and supporting cellular repair mechanisms, which help maintain optimal cell function. Chlorella demonstrates detoxification capabilities by binding heavy metals and supporting immune function, making it relevant for consumers concerned about environmental toxins. The algae's unique cell wall structure enables efficient toxin removal while preserving essential nutrients. Clinical evidence supporting these benefits enables product differentiation and increases consumer trust in algae-based products. The studies specifically highlight improved biomarkers for oxidative stress, immune function, and heavy metal reduction. Supplements combining multiple algae species provide comprehensive nutrition while simplifying consumer choices, as each species contributes distinct nutritional compounds and functional benefits.

Environmental Sustainability of Algae Production

Algae cultivation provides significant environmental benefits that align with environmentally conscious consumers. According to the United States Department of Energy data from 2024 [2]United States Department of Energy, “Algae SAF Techno-Economic Analysis”, www.energy.gov, algae production requires substantially less land and water compared to traditional agriculture while actively sequestering carbon dioxide during growth. Life cycle assessments demonstrate that algae-based omega-3 production has a considerably lower carbon footprint than fish oil extraction, effectively supporting corporate sustainability goals and environmental initiatives. Algae can be efficiently cultivated using non-potable water and non-arable land, which prevents direct competition with food production systems and addresses resource utilization concerns. Current technologies enable comprehensive algae cultivation using various waste streams, creating substantial opportunities to convert environmental waste into high-quality nutrition products. This environmental advantage continues to gain significant importance as regulations incorporate detailed environmental impact assessments and consumers increasingly choose brands based on demonstrated environmental performance and sustainability practices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Production and Extraction Costs Impede Market Expansion | -3.1% | Global, particularly affecting emerging market penetration | Short term (≤ 2 years) |

| Market Competition from Traditional Fish-Based Omega-3 And Alternative Supplements | -2.2% | North America and Europe established markets | Medium term (2-4 years) |

| Limited Consumer Awareness in Developing Regions | -1.8% | Asia-Pacific developing markets, Middle East and Africa, Latin America | Medium term (2-4 years) |

| Regulatory and Labeling Challenges | -1.4% | Global, with varying regional compliance requirements | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Production and Extraction Costs Impede Market Expansion

Production economics remain the primary constraint limiting algae supplement market penetration, with spirulina powder pricing significantly exceeding conventional protein sources and constraining mass market adoption. Cultivation infrastructure requirements, including specialized photobioreactors and controlled environment systems, create substantial capital barriers for new market entrants while limiting production scalability. However, recent technological breakthroughs in hydrodynamic cavitation extraction methods demonstrate potential for dramatic cost reductions, achieving high phycocyanin yields. The development of hybrid open-closed cultivation systems and automated production technologies suggests production costs may decline significantly over the forecast period. Companies achieving production scale advantages through vertical integration and technological innovation will likely capture disproportionate market share as cost structures improve.

Market Competition from Traditional Fish-Based Omega-3 And Alternative Supplements

Fish oil supplement manufacturers maintain market advantages through lower production costs, established distribution networks, and consumer brand recognition, which creates competitive pressure for algae-based alternatives. These traditional omega-3 producers use economies of scale and existing supply chains to maintain competitive pricing while investing in marketing that highlights bioavailability and research findings. The growth of plant-based omega-3 alternatives, such as flaxseed and chia products, increases market competition and affects positioning options for algae producers. However, algae-based supplements offer distinct benefits, including consistent potency, no fish-related odors, and vegetarian-friendly formulations. As production costs decrease and consumer awareness grows, regulatory approval of new algae species and improved extraction technologies may gradually strengthen the market position of algae supplements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Spirulina Dominates the Market While Chlorella Segment Accelerates

Spirulina holds a 38.74% market share in 2025, supported by established consumer trust and robust distribution networks. Chlorella exhibits the highest growth rate with a 15.27% CAGR through 2031, primarily due to increased recognition of its detoxification and immune-boosting properties. The spirulina segment benefits from substantial clinical research supporting its nutritional value, particularly its 55-70% protein content and complete amino acid profile, which attracts health and fitness-focused consumers.

Astaxanthin products serve specific market segments focused on antioxidant and skin health benefits. Natural astaxanthin commands higher prices than synthetic versions due to better bioavailability and consumer preference for natural sources. The combination supplements category combines multiple algae species to offer comprehensive nutrition profiles, while allowing manufacturers to create distinct product formulations. The market favors companies that achieve vertical integration across algae species production while meeting quality and regulatory requirements across their product range.

By Form: Powder Formats Lead Market Share While Capsules Show Rapid Growth

Powder formulations hold a 38.92% market share in 2025, supported by established consumer preferences and efficient production processes. Simultaneously, capsule formats demonstrate strong growth with a 14.32% CAGR, driven by convenience and improved palatability that addresses common taste and odor concerns. Powder formats offer versatility in applications, allowing integration into smoothies, protein shakes, and food products while maintaining lower per-serving costs. Recent microencapsulation technology developments have enhanced powder stability and reduced oxidation, resulting in longer shelf life and preserved bioactive compounds.

Capsule formulations resolve taste and texture concerns while providing precise dosing and improved compliance, particularly for therapeutic applications requiring consistent intake. DSM-Firmenich's Life's DHA B54-0100 in 2025, offering 620mg of omega-3s per serving in compact capsules, showcases product development aligned with consumer demand for convenient, concentrated formulations. Tablet formats meet specific market requirements for standardized dosing and extended release properties, while liquid formulations provide rapid absorption benefits. Gummy formats represent a new development in making algae supplements accessible to younger consumers while maintaining nutritional benefits.

By Distribution Channel: Specialty and Health Stores Lead Market Share as E-Commerce Growth Continues

Specialty and health stores hold the largest market share at 58.05% in 2025. These stores maintain their dominance through expert consultation services and established consumer trust in specialized retail environments. Meanwhile, online retailers demonstrate the highest growth rate at 14.58% CAGR, driven by increased e-commerce adoption and direct-to-consumer strategies that strengthen brand differentiation and customer relationships. Specialty retailers benefit from trained staff who educate consumers about algae supplement benefits and address questions regarding taste, dosing, and health regimen compatibility. These stores also play a crucial role in testing new algae products and formulations, offering valuable market insights, and supporting product development.

Online distribution channels allow smaller algae manufacturers to target specific consumer segments while offering detailed information about sourcing, manufacturing processes, and third-party testing, factors that significantly influence purchase decisions. The digital platform supports subscription-based models, enhancing customer retention and ensuring regular product availability for daily supplement users. Supermarkets and hypermarkets offer broad market access but primarily stock established brands and competitively priced products, which limits the presence of premium algae supplements. Alternative distribution channels, including pharmacies and direct sales, cater to specific consumer groups and regions where traditional retail coverage is minimal.

Geography Analysis

Asia-Pacific topped regional rankings with 37.95% of global sales in 2025 and a projected 15.12% CAGR to 2031, underwritten by cultural familiarity with sea-vegetable consumption and national policies that classify microalgae as strategic food resources. Japan’s supplement shoppers weigh EPA/DHA ratios more heavily than price, fostering a premium subsegment within the algae supplements market. China’s expanding middle class channels higher discretionary income toward preventive nutrition, and India’s urban millennials adopt plant-centric diets that accommodate spirulina capsules for daily vitality.

North America, while mature, leverages robust clean-label preferences and sizable vegan populations to sustain medium-single-digit growth. The algae supplements market share of sustainably certified products is accelerating as grocers integrate environmental scorecards into planograms. Federal rulings allowing new color additives such as Galdieria extract blue broaden algae’s application portfolio, indirectly reinforcing supplement awareness by raising walk-by exposure in multiple food aisles, according to the Federal Register data from 2025 .

Europe’s trajectory benefits from the European Commission’s 2024 clearance of more than 20 additional algae species for food uses, a decision calculated to save the sector at least USD 11.7 million in compliance costs. This accelerated access to diverse strains prompts local formulators to experiment with niche carotenoids and novel polysaccharides, deepening product variety in the algae supplements market. Conversely, Middle East & Africa and South America remain nascent; pilot consumer campaigns coupled with regional cultivation trials, notably in East Africa for DHA-rich microalgae, aim to close awareness gaps and localize supply.

Competitive Landscape

The algae-based supplements market has a moderate concentration, where established companies maintain strong positions while new entrants can access specialized market segments. Companies such as DSM-Firmenich AG, Cyanotech Corporation, AlgaeCal Inc., EID Parry (Parry Nutraceuticals), and Far East Bio-Tec Co., Ltd, among others, aim to implement vertical integration across cultivation, extraction, and formulation processes to maintain quality standards and strengthen supply chain operations. This integration approach addresses the technical requirements of algae cultivation and quality consistency challenges.

The market presents opportunities in specialized formulations targeting specific health areas such as cognitive function and immune support, where algae's nutritional composition provides benefits compared to synthetic alternatives. Small-scale manufacturers have established market presence through specialized organic-certified products with transparent supply chains, responding to consumer preferences for sustainable and traceable products.

Technological capabilities have emerged as a key competitive factor, as improvements in cultivation and extraction methods enhance product effectiveness and reduce operational costs. The United States Food and Drug Administration's 2024 GRAS Notice for docosahexaenoic acid (DHA)-rich oil from Schizochytrium sp. marks an important regulatory milestone, confirming its safety for use in infant formulas and general food products, which may expand market applications for qualified manufacturers.

Algae Supplements Industry Leaders

-

DSM-Firmenich AG

-

Cyanotech Corporation

-

AlgaeCal Inc.

-

EID Parry (Parry Nutraceuticals)

-

Far East Bio-Tec Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Nature's Bounty introduced Plant-Based Omega-3, a supplement containing algae-derived EPA and DHA. The product contains 1,000 mg of vegetarian algae oil and is available through major retailers including Amazon, CVS, Walgreens, Publix, and Kroger.

- June 2024: MD Logic Health and AvalonX collaborated to launch a vegan dietary supplement, Spirulina. The United States-made supplement contained no stearates, palmitates, rice products, soy, phthalates, or artificial colors and flavors.

- June 2024: Apokra announced the launch of a range of algae-based omega-3 products, including Omega-3 DHA & EPA tablets. These products build on the success of their Kids DHA Drops, and feature a unique formulation that enhances bioavailability while maintaining vegan credentials and freedom from artificial additives.

- May 2023: SOUL +FIX, a Singapore-based supplement brand, announced plans to enter the Southeast Asian market with its recently launched product, blue spirulina powder supplement. The brand also plans to undertake research & development activities to create new formulations.

Global Algae Supplements Market Report Scope

Algae-based supplements are manufactured using microalgae like spirulina, chlorella, or astaxanthin and are found to improve the overall well-being of an organism.

The algae supplements market is segmented by product type into chlorella, spirulina, astaxanthin, and combination supplements. By form, the market is segmented into powder, capsules, tablets, and liquids. By distribution channels, the market is segmented into supermarkets/hypermarkets, specialty & health stores, online retailers, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

The market sizing has been done in value terms in USD for all the abovementioned segments.

| Chlorella |

| Spirulina |

| Astaxanthin |

| Combination Supplements |

| Powder |

| Capsule |

| Tablet |

| Liquid |

| Supermarkets/Hypermarkets |

| Specialty and Health Stores |

| Online Retailers |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Chlorella | |

| Spirulina | ||

| Astaxanthin | ||

| Combination Supplements | ||

| By Form | Powder | |

| Capsule | ||

| Tablet | ||

| Liquid | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty and Health Stores | ||

| Online Retailers | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the algae-based supplements market?

The market stands at USD 0.96 billion in 2026 and is projected to reach USD 1.79 billion by 2031.

Which product type leads the algae-based supplements market?

Spirulina holds the largest 2025 share at 38.74%, though chlorella is growing fastest at a 15.27% CAGR through 2031.

Which region is expanding most rapidly?

Asia-Pacific combines a 37.95% 2025 share with a 15.12% forecast CAGR, driven by cultural familiarity and rising health awareness.

Why are algae-based omega-3 supplements gaining popularity?

They deliver EPA/DHA without marine contaminants, satisfy vegetarian diets, and support sustainability goals.

Page last updated on: