Marine Fenders Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

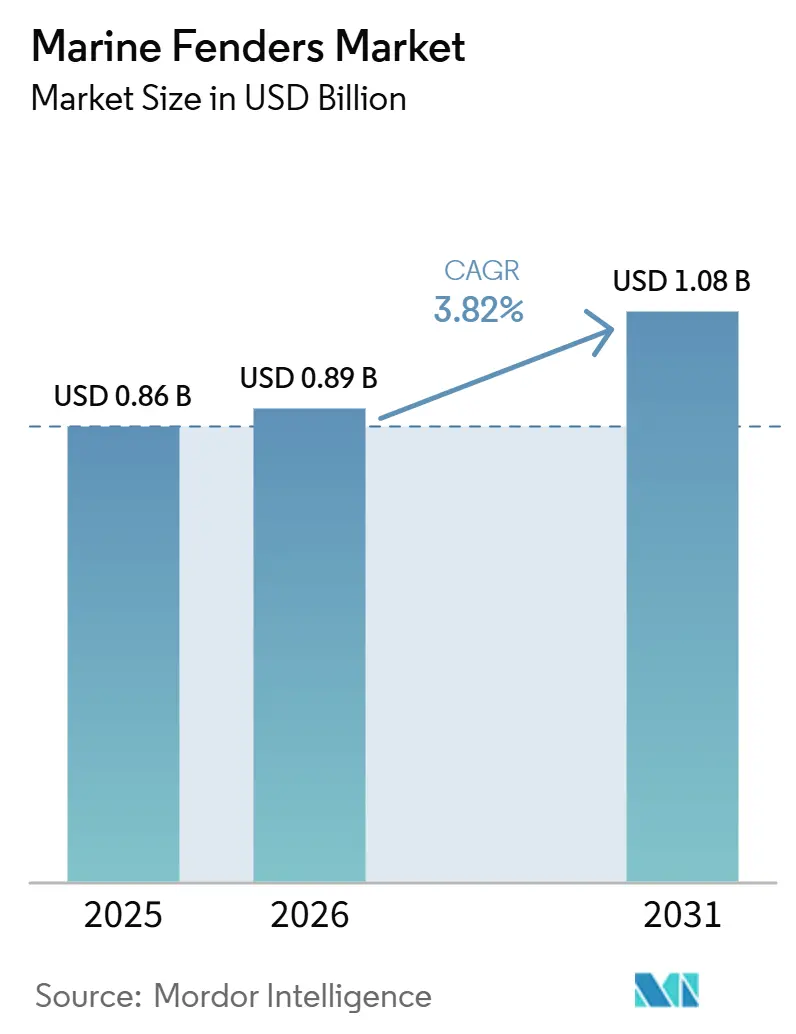

| Market Size (2026) | USD 0.89 Billion |

| Market Size (2031) | USD 1.08 Billion |

| Growth Rate (2026 - 2031) | 3.82% CAGR |

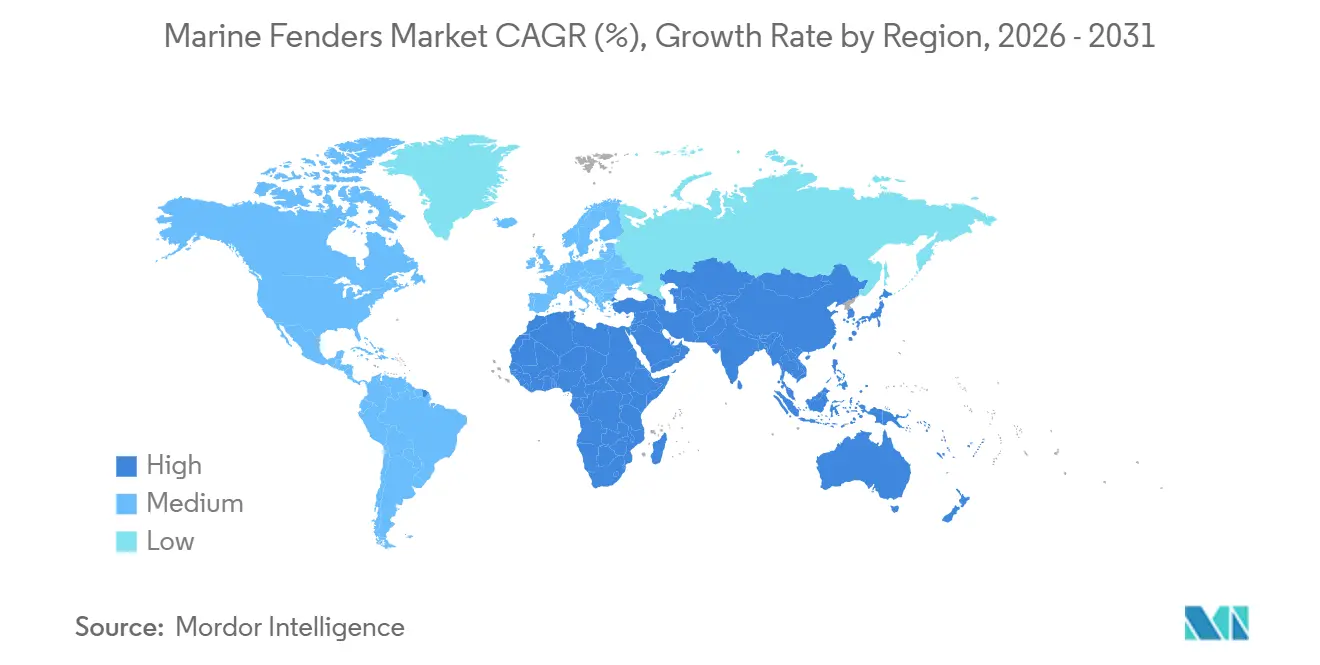

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Marine Fenders Market Analysis by Mordor Intelligence

The marine fenders market size is projected to expand from USD 0.86 billion in 2025 and USD 0.89 billion in 2026 to USD 1.08 billion by 2031, registering a CAGR of 3.82% between 2026 and 2031. As vessel dimensions grow and backlogs at berths age, coupled with tightening regulations, capital is increasingly drawn to high-energy-absorption systems, particularly at mega-terminals in the Asia-Pacific. Port operators are aligning fender upgrades with quay electrification, crane heightening, and the deployment of digital twins to reduce downtime. In the U.S., there's a noticeable funding push, highlighted by a port infrastructure development program that allocates significant resources to berth modernization, including the replacement of cell- and cone-types. The adoption of new probabilistic design rules has increased minimum energy-absorption thresholds, directing procurement towards molded rubber and advanced foam variants. While competitive intensity is moderate, with Chinese suppliers offering lower prices on standardized cylindrical units, many low-cost entrants are blocked by stringent certification requirements, full-scale testing, and defense-sector clearances [1]“Review of Maritime Transport 2025,”, United Nations Conference on Trade and Development, unctad.org.

Key Report Takeaways

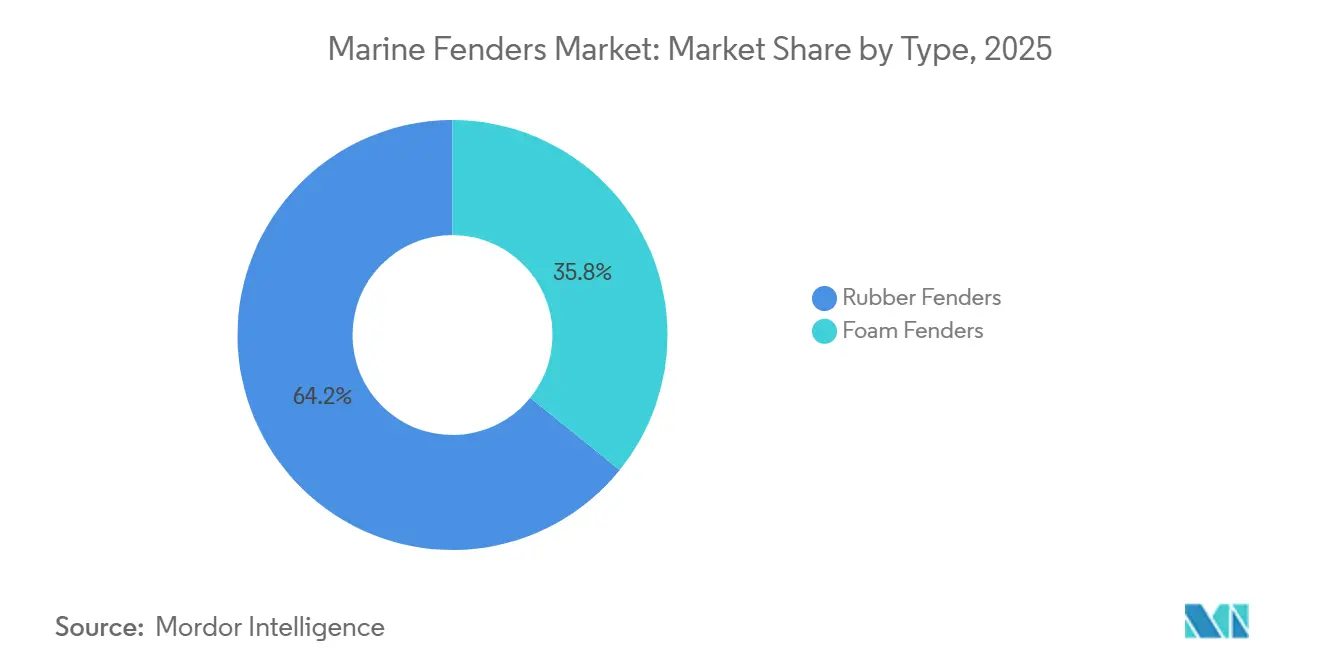

- By material type, rubber fenders led with 64.17% of the marine fenders market share in 2025, while foam fenders are forecast to expand at a 5.87% CAGR through 2031.

- By manufacturing process, extrusion accounted for 56.37% of the marine fenders market in 2025; molding methods are advancing at a 5.85% CAGR through 2031.

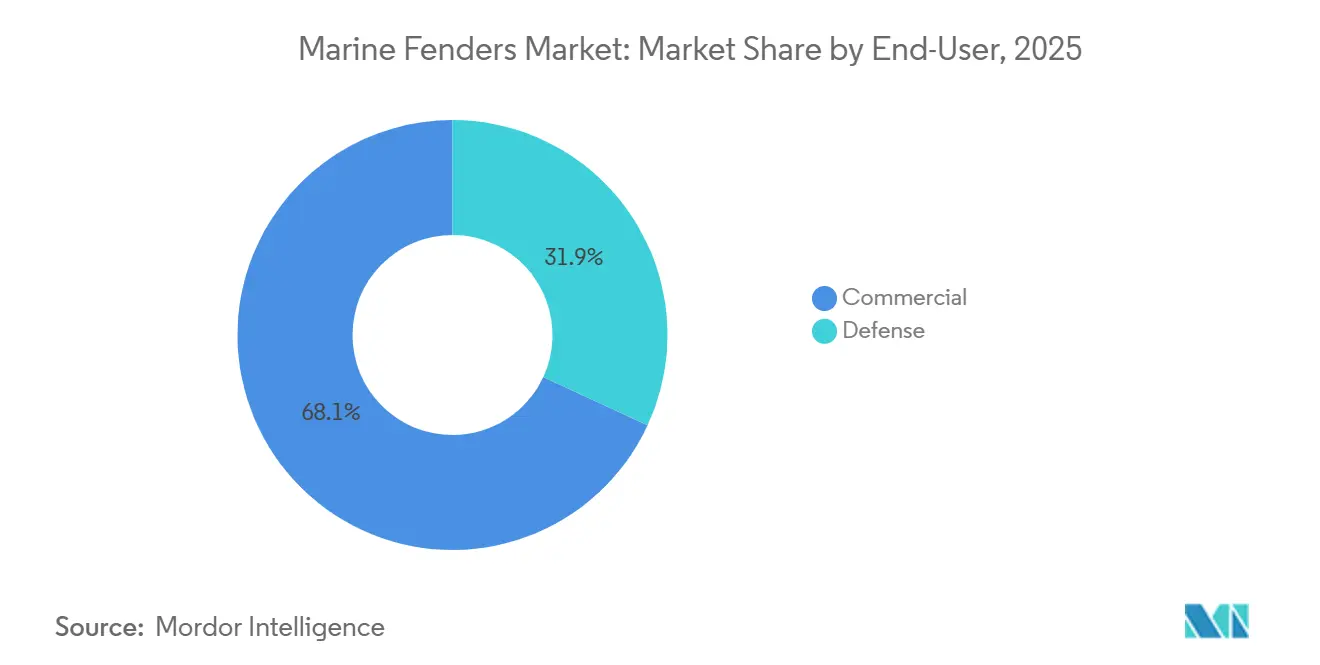

- By end-user, commercial facilities commanded 68.14% of the marine fenders market in 2025, whereas defense installations posted the fastest CAGR of 5.93% over the forecast period.

- By installation location, dock fenders accounted for 57.85% of revenue share in 2025, yet ship-mounted systems are projected to grow at a 5.98% CAGR through 2031.

- By geography, Asia-Pacific accounted for 36.73% of revenue share in 2025; the Middle East and Africa geography is the fastest-growing, with a 5.94% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Marine Fenders Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Seaborne Trade Volumes | +1.8% | Global, with Asia Pacific leading growth | Long term (≥ 4 years) |

| Expansion of Mega-Container and LNG Terminals | +1.5% | Asia-Pacific, Middle East and Africa | Medium term (2-4 years) |

| Naval Modernization Programs Boosting Defense Demand | +0.8% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Stricter PIANC/ISO Port-Safety Regulations | +0.6% | Global, with Europe leading compliance | Medium term (2-4 years) |

| Sensor-Integrated "Smart" Fenders Enabling Predictive Maintenance | +0.4% | North America, Europe, advanced Asia-Pacific ports | Short term (≤ 2 years) |

| Offshore Renewable Projects Requiring Specialty Fenders | +0.3% | Europe, North America, emerging Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Seaborne Trade Volumes

Container throughput is nearing previous levels, but port congestion remains an issue: average waiting times at key hubs have increased. In response, terminal managers are introducing parallel berths with advanced cell and cone fenders, which dissipate more kinetic energy than older models. Infrastructure grants are focusing on berth upgrades that enable higher approach velocities, reducing quay damage and shortening dwell times. With liner alliances consolidating larger vessels at fewer mega-hubs, the risk associated with single berths is heightened, speeding up the replacement cycle for marine fenders. Manufacturers, providing modular arrays with adjustable energy increments, are securing retrofit contracts, as terminals seek to avoid extended closures.

Expansion of Mega-Container and LNG Terminals

Ultra-large container projects are specifying fender panels designed to shield massive hulls and wide beams. New LNG import sites are deploying high-capacity pneumatic units. These units are designed to accommodate large carriers and are embedding compliance standards into their early FEED studies. The significant scale of these contracts locks in long production runs, favoring incumbents equipped with advanced tooling and validation capabilities. With substantial capital intensity, fender purchases are budgeted well in advance, stabilizing order books for certified suppliers.

Naval Modernization Programs Boosting Defense Demand

Defense ministries in multiple countries are upgrading submarine and carrier berths to accommodate heavier, stealth-lined hulls. One country has allocated significant funding for upgrades, including specialized fenders at key bases. In another country, a defense program requires installations capable of handling substantial submerged loads and enduring extensive fatigue cycles. Although security clearances, auditing, and quality-assurance protocols enhance profit margins, they also extend sales cycles. Geopolitical tensions in strategic regions signal a sustained defense-driven demand in the marine fenders market.

Stricter Pianc/Iso Port-Safety Regulations

Newly introduced guidelines have implemented probabilistic load-factor equations, increasing the energy absorption requirements for berths handling larger vessels. Additionally, updated standards now include long-term UV and immersion aging criteria for floating fender certification. These changes have prompted ports in certain regions to delay expansions until compliant supplies are secured. Authorities in specific areas have begun enforcing these regulations, resulting in the postponement of several terminal projects due to uncertified units being disqualified. Extended certification timelines benefit established players while pressuring smaller firms to adopt white-labeling through approved foundries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Natural-Rubber Prices | -1.2% | Global, with Asia-Pacific production centers most affected | Short term (≤ 2 years) |

| High Installation and Retrofit Costs For Legacy Berths | -0.8% | North America, Europe mature port infrastructure | Medium term (2-4 years) |

| Intense Price Pressure From Low-Cost Asian Entrants | -0.6% | Global, with Europe and North America premium markets most affected | Medium term (2-4 years) |

| Longer Life of Foam-Filled and Pneumatic Designs Reducing Replacement Cycles | -0.4% | Global, with developed markets leading adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Natural-Rubber and Petro-Chemical Input Prices

Natural rubber prices experienced significant fluctuations as supplies tightened in key regions, leading to compressed supplier margins due to fixed-price port contracts lagging behind spot market prices. This resulted in a notable decline in margins for major players in the marine sector. Synthetic inputs also faced price increases, driven by production outages, which raised the cost bases for foam fenders. Smaller firms, lacking vertical integration, postponed tenders, while ports extended service lives through increased inspections, collectively reducing the near-term demand in the marine fenders market.

High Installation and Retrofit Costs For Legacy Berths

Upgrading 1970s-era timber piles to modern cone fenders demands quay-wall drilling, resin anchoring, and berth closures that can surpass fender hardware costs by threefold. Ports in North America and Europe often defer projects, opting for patch repairs that raise maintenance budgets but delay capital outlays. Engineering studies must confirm structural reinforcement to handle higher energy ratings, extending project timelines. These hurdles slow replacement cycles at mature ports, curbing immediate growth for the marine fenders market despite clear long-term benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Rubber Dominance Faces Foam Innovation

Rubber variants delivered 64.17% of revenue in 2025, as cell and cone geometries absorbed berthing loads exceeding 2,000 kN at high-throughput terminals. Cylindrical units remained the workhorse for cost-driven bulk docks, while arch fenders protected aluminum-hulled patrol craft where a low reaction force is critical. Foam designs, although with a smaller base, are advancing at 5.87% CAGR, buoyed by floating wind and FSRU projects that favor lightweight, unsinkable cores. In Taiwan's offshore expansion, all operations and maintenance bases now feature foam-filled units designed to withstand rough seas. In LNG transfers, pneumatic hybrids are becoming the preferred choice, as they maintain consistent pressure across varying tides and outperform solid elastomers. This technological shift is reshaping the hierarchy of marine fenders market sizes, especially as offshore energy activities ramp up.

The growing preference for foam and pneumatic solutions coincides with a projected growth in the region. Notably, LNG terminals in certain areas have transitioned away from heavy rubber. While rubber continues to dominate at established container docks, energy thresholds set by industry standards are steering operators towards multi-layer foam. This shift not only prolongs service life but also simplifies maintenance. As adoption of these technologies broadens, suppliers adept at blending rubber, EVA, and polyurethane chemistries are poised to gain a larger foothold in the marine fenders market, with projections pointing to continued growth.

By Manufacturing Process: Extrusion Dominates While Molding Innovates

Extrusion retained 56.37% of the marine fenders market share in 2025, offering low unit cost for D-profile and cylindrical shapes at regional ports. Continuous runs maximize throughput but limit profile complexity, restricting use in constrained urban berths. In contrast, molded cell and cone designs, growing at 5.85% CAGR, address space-limited quays by packing higher energy absorption per linear meter. A terminal opted for molded-cell units with height-variable panels to accommodate its tide.

While molding incurs a heftier tooling expense, it's tailored for large terminal contracts surpassing significant unit volumes, guaranteeing returns over extended production runs. Suppliers boasting multi-cavity presses and in-house FEA expertise capitalize on this scale, whereas smaller retrofit tasks typically resort to extruded rubber. Newer niches in cast-polyurethane and composite lay-ups cater to icebreaker and Arctic berths, where resilience to extreme cold is non-negotiable. This division in processes reflects the broader marine fenders market, distinguishing between engineered solutions and commodity offerings.

By End-User: Commercial Dominance Amid Defense Growth

Commercial facilities absorbed 68.14% of the marine fender market size in 2025. Container hubs synchronized fender cycles with crane re-railings and berth deepening, while cruise piers favored low-pressure cylindrical designs to protect painted hulls. Bulk docks, experiencing lower approach energy, prioritize longevity over performance.

Defense berths, though a smaller base, outpace other sub-segments at 5.93% CAGR. Submarines and naval projects are enhancing fender designs to withstand significantly higher dynamic loads than commercial counterparts. Due to extended qualifications, cybersecurity audits, and export-control clearances, average selling prices (ASPs) have increased notably. Additionally, shipyards are integrating hull-attached fenders for amphibious assault craft, further expanding the addressable market for marine fenders.

By Installation Location: Dock Leads Share While Ship-Mounted Drives Growth

Dock-mounted systems accounted for 57.85% of installations in 2025, reflecting the legacy bias toward quay protection. Condition monitoring and UV-resistant compounds now stretch service intervals to 15 years, slowing replacement volume.

Ship-mounted solutions, advancing at 5.98% CAGR, ride the offshore wind surge. Equinor’s service fleet fitted pneumatic collars for Hywind Tampen, guaranteeing hull integrity during dynamic positioning. FPSOs and shuttle tankers in West Africa attach modular foam sleeves to withstand multidirectional impacts. Mixed-mount hybrids on dolphins and floating docks complete the spectrum, signaling that the distribution of impact energy between vessel and shore is the new design frontier for the marine fenders market.

Geography Analysis

Asia-Pacific accounts for 36.73% of 2025 revenue, as major ports in the region have recently expanded their capacity, revitalizing numerous cone and cell units. Countries in the region are pursuing an ambitious project to add new berths, with fender orders integrated into large-scale infrastructure packages. Some countries in the region are addressing aging infrastructure, necessitating retrofits incorporating advanced molded rubber arrays. Additionally, a regional initiative has introduced new deep-water berths that source cylindrical units from local suppliers. As supply chains shift within the region, coastal harbor expansions are accelerating, driving growth in the marine fenders market across Southeast Asia.

Europe, North America, and South America collectively account for a substantial portion of global revenues. European ports are upgrading its quay with advanced panels priced significantly higher than standard options. North America is setting new benchmarks by utilizing fender panels for larger vessels. In South America, a prominent port is modernizing its berths with cone-fender retrofits to increase capacity. In the United States, government grants are being allocated to berth enhancements to improve operational efficiency and stimulate replacement demand. European operators are also addressing regulatory requirements, driving a surge in demand for retrofits in the marine fenders market.

The Middle East and Africa, though smaller today, log the fastest CAGR at 5.94%. A major port in the region is expanding to accommodate larger vessels, incorporating advanced cell units. Another port is preparing for specialized cargo loads, having ordered a significant number of fenders across multiple berths. Ports in North Africa are adopting certified arrays to attract alliance traffic. In another region, delayed expansion projects indicate latent demand that is expected to materialize once financing is secured. As countries in the Gulf region aim to enhance their transshipment capabilities, the focus on high-capacity berths with premium fendering is driving growth in the regional marine fenders market.

Competitive Landscape

Trelleborg, ShibataFenderTeam, and Yokohama dominate the global marine fenders market. PIANC validation, advanced finite-element design suites, and a proven track record in LNG and naval projects support their market positions. Meanwhile, Chinese manufacturers, such as Qingdao Xincheng and China Deers, have gained significant market share by offering standardized cylindrical and D-profile units at considerably lower FOB prices. This pricing strategy has created two distinct value chains in the industry: one focused on certified engineering and the other on cost-centric supply, with minimal overlap.

Opportunities are emerging in sensor-integrated smart fender technology. These innovative fenders, capable of converting strain data into predictive maintenance dashboards, are set to transform the market landscape. Trelleborg's pilot project at a major port demonstrates this potential, achieving a significant reduction in unplanned downtime and commanding a premium on average selling prices (ASP)[2]“Smart Fender Pilot at Maasvlakte II,”, Trelleborg AB, trelleborg.com. Beyond smart fenders, the market also shows promise in foam fenders designed for offshore wind applications and modular emergency units intended for hurricane-affected quays. The introduction of stricter regulations by PIANC WG211 further highlights the industry's shift towards engineering excellence over pricing. Suppliers who fail to incorporate analytics or certification into their offerings may face shrinking margins, particularly as segments of the market become increasingly commoditized.

Regional OEMs in Southeast Asia are gaining attention with their agility. Some plants have reduced the shipping time for ship-mounted fenders to a fraction of the industry standard. This speed advantage is appealing to vessel owners with tight construction timelines. As sensor costs continue to decline, the trend of data-driven differentiation is expected to shift from traditionally premium markets to more price-sensitive regions in Asia. This transition is likely to significantly reshape the competitive dynamics of the marine fenders market.

Marine Fenders Industry Leaders

Trelleborg Marine & Infrastructure

Bridgestone Corp. (Marine Products)

Yokohama Rubber Co., Ltd.

ShibataFenderTeam AG

Sumitomo Rubber Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: At Kandla Port, Lion Rubber is undertaking a significant project for the Deendayal Port Authority. The initiative focuses on upgrading the fender system at the cargo berth, aiming to boost safety, operational efficiency, and accommodate increased cargo handling demands. This project underscores the commitment to modernizing port infrastructure and supporting the growing maritime trade.

- September 2025: Yokohama Rubber Co., Ltd. had confirmed its participation in the World Ports Conference 2025. As a leading manufacturer of marine fenders, Yokohama Rubber unveiled its enhanced lineup of fender products at the event. The company showcased its diverse range of offerings, which included pneumatic fenders, as well as V-type, cell-type, and cone-type solid fenders.

Global Marine Fenders Market Report Scope

| Rubber Fenders | Cell Fenders |

| Cone Fenders | |

| Cylindrical Fenders | |

| Arch Fenders | |

| Others | |

| Foam Fenders |

| Extrusion |

| Molding |

| Other Manufacturing Processes |

| Defense |

| Commercial |

| Ship Fenders |

| Dock Fenders |

| Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Spain | |

| Italy | |

| France | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Indonesia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Rubber Fenders | Cell Fenders |

| Cone Fenders | ||

| Cylindrical Fenders | ||

| Arch Fenders | ||

| Others | ||

| Foam Fenders | ||

| By Manufacturing Process | Extrusion | |

| Molding | ||

| Other Manufacturing Processes | ||

| By End-User | Defense | |

| Commercial | ||

| By Installation Location | Ship Fenders | |

| Dock Fenders | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| Spain | ||

| Italy | ||

| France | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the marine fenders market?

The marine fenders market size stands at USD 0.89 billion in 2026 and is forecast to reach USD 1.08 billion by 2031.

Which material type dominates global demand?

Rubber fenders account for 64.17% of 2025 revenue, aided by cell and cone geometries favored at high-impact container berths.

Which region is growing fastest through 2031?

The Middle East and Africa register the highest CAGR at 5.94%, led by mega-terminal projects in Saudi Arabia and the UAE.

What role do defense programs play in demand?

Naval modernization in the Indo-Pacific and North Atlantic propels defense-sector fender spending at a 5.93% CAGR, focusing on high-fatigue, corrosion-resistant designs.

How are smart-port initiatives affecting fender procurement?

Ports integrate sensors for predictive maintenance, raising specification levels and average selling prices.

Page last updated on: