Marine Fasteners Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.44 Billion |

| Market Size (2030) | USD 1.78 Billion |

| Growth Rate (2025 - 2030) | 5.36% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Marine Fasteners Market Analysis by Mordor Intelligence

The marine fasteners market was USD 1.44 billion in 2025 and is projected to reach USD 1.78 billion by 2030, advancing at a 5.36% CAGR. Accelerating global shipbuilding programs, offshore wind build-outs, and stringent corrosion-prevention mandates are expanding the addressable base of high-specification fastening products. The pivot toward sensor-embedded “smart” fasteners, paired with coatings engineered for 25-year salt-spray endurance, is widening profit pools for vendors that can integrate materials engineering with digital monitoring.

Key Report Takeaways

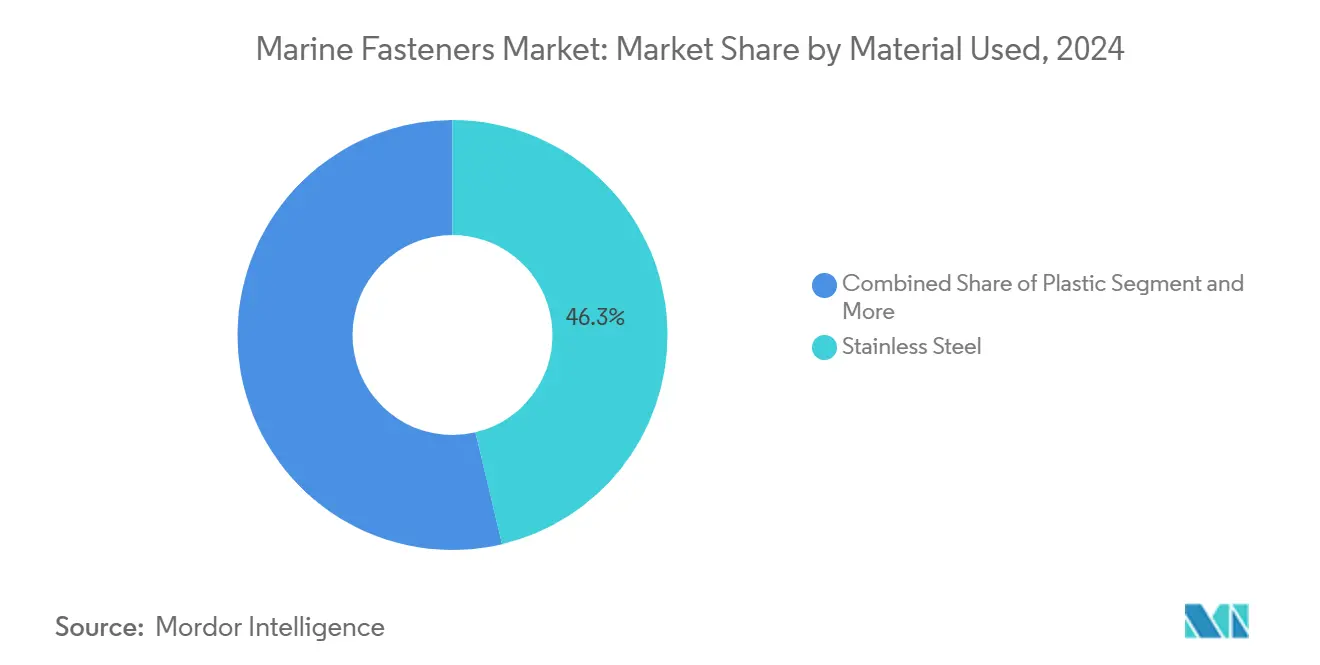

- By material, stainless steel held 46.27% of the marine fasteners market share in 2024; plastic fasteners are projected to expand at a 6.83% CAGR through 2030.

- By product type, bolts commanded 28.14% of the marine fasteners market size in 2024, whereas togglers are forecast to register a 7.92% CAGR to 2030.

- By application, merchant marine vessels accounted for 31.08% share of the marine fasteners market size in 2024; offshore support vessels are anticipated to advance at an 8.61% CAGR during the forecast window.

- By coating, hot-dip galvanized treatments captured 38.22% of the marine fasteners market share in 2024, while PTFE/Xylan fluoropolymer coatings are expected to grow at a 7.46% CAGR to 2030.

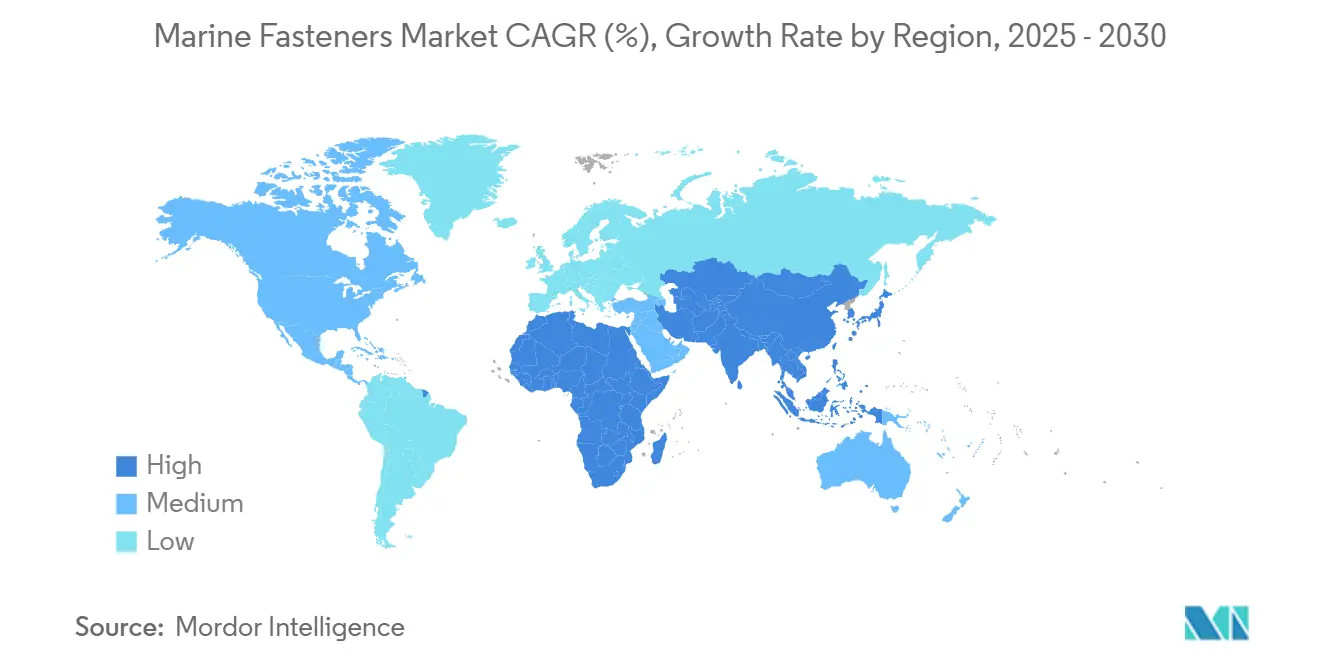

- By geography, Asia-Pacific led with 42.35% revenue share in 2024; North America is projected to post the fastest regional CAGR at 7.12% up to 2030.

Global Marine Fasteners Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global Shipbuilding Rebound and Fleet Renewal Programs | +1.8% | Asia-Pacific Core, Spillover to Europe and North America | Medium Term (2-4 Years) |

| Offshore Wind Farm Build-Out Demands Heavy-Duty Corrosion-Resistant Fasteners | +1.2% | North America and Europe, Emerging in Asia-Pacific | Long Term (≥ 4 Years) |

| Stringent IMO Corrosion-Prevention Rules Driving Stainless-Steel Retrofits | +0.9% | Global | Short Term (≤ 2 Years) |

| Increased Yacht and Recreational Boat Sales in High-Income Regions | +0.6% | North America and Europe | Medium Term (2-4 Years) |

| Sensor-Embedded “Smart” Fasteners for Naval Structural-Health Monitoring | +0.4% | North America and Europe, Selective Asia-Pacific | Long Term (≥ 4 Years) |

| Vendor-Managed-Inventory Kits Shortening Dock-Repair Turnaround | +0.3% | Global | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Global Shipbuilding Rebound and Fleet Renewal Programs

The shipbuilding industry's remarkable recovery has created unprecedented demand for marine fasteners, with global orderbooks reaching historic peaks as commercial operators accelerate fleet modernization programs. South Korean shipyards reported record delivery schedules through 2024, while Chinese yards maintained robust production capacity despite supply chain disruptions. This surge extends beyond traditional cargo vessels to specialized offshore support vessels, where fastener specifications demand enhanced corrosion resistance and structural integrity. The replacement cycle for aging merchant fleets, particularly those approaching 20-year operational limits, is driving systematic upgrades to higher-grade stainless steel and composite fastening systems. Fleet renewal programs increasingly prioritize long-term operational efficiency over initial capital costs, creating opportunities for premium fastener suppliers who can demonstrate total cost of ownership advantages through reduced maintenance intervals and enhanced durability performance.

Offshore Wind Farm Build-Out Demands Heavy-Duty Corrosion-Resistant Fasteners

Offshore wind installations are reshaping fastener specifications as turbine foundations and support structures require unprecedented corrosion resistance in harsh marine environments. The transition to larger turbine platforms, with some installations exceeding 15 MW capacity, demands fastening systems capable of withstanding extreme loads while maintaining structural integrity over 25-year operational lifespans. Advanced coating technologies, particularly PTFE-based fluoropolymer systems, are becoming standard specifications for offshore wind fasteners due to their superior salt spray resistance and low friction characteristics[1]William Hartley-James, "The benefits of PTFE Coated A2 Stainless Steel fasteners?" High Performance Polymer, highperformancepolymer.co.uk. . The sector's growth trajectory is accelerating demand for specialized fasteners in the 316L stainless steel grade and above, with some applications requiring exotic alloys like Inconel for extreme exposure conditions. Regulatory frameworks governing offshore wind installations are driving standardization around ISO 3506 specifications, creating opportunities for suppliers who can demonstrate compliance with evolving certification requirements while maintaining competitive pricing structures.

Stringent IMO Corrosion-Prevention Rules Driving Stainless-Steel Retrofits

International Maritime Organization regulations are compelling vessel operators to upgrade fastening systems as part of broader corrosion prevention mandates, particularly for vessels operating in corrosive environments. The implementation of enhanced inspection protocols has revealed widespread fastener degradation in aging fleets, triggering systematic replacement programs that favor stainless steel over traditional carbon steel alternatives. Recent regulatory guidance emphasizes the importance of galvanic compatibility in fastener selection, driving the adoption of 316-grade stainless steel for applications involving dissimilar metals[2]"Stainless Steel vs. Brass Fasteners: What’s Best for Saltwater Boats?," baitalnuhas.com. . Compliance frameworks under SOLAS and MARPOL conventions are creating standardized procurement requirements that benefit suppliers with established certification processes and quality documentation systems. The regulatory push extends to coating specifications, where traditional zinc plating is being replaced by more durable alternatives like zinc-flake and fluoropolymer systems that provide extended service life in marine environments.

Increased Yacht and Recreational Boat Sales in High-Income Regions

The luxury marine segment is experiencing sustained growth as high-net-worth individuals increase recreational vessel ownership, creating demand for premium fastening solutions that combine performance with aesthetic considerations. Yacht manufacturers specify advanced fastener materials and coatings to meet owner expectations for low-maintenance operation and superior corrosion resistance in saltwater environments. The trend toward larger, more sophisticated recreational vessels is driving the adoption of aerospace-grade fasteners and exotic alloy specifications previously reserved for commercial applications. Custom yacht builders increasingly request color-coded fastener systems and specialized coatings that maintain appearance while providing long-term durability[3]"Specialty PTFE Coated Fasteners," lightningboltandsupply.com.. This market segment's willingness to pay premium prices for superior performance is encouraging fastener suppliers to invest in advanced coating technologies and specialized alloy development programs that can command higher margins while meeting demanding aesthetic and performance requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-Material Price Volatility (Stainless Steel and Aluminum) | -0.8% | Global | Short Term (≤ 2 Years) |

| Cyclical Slowdown in Merchant-Marine New-Build Orders | -0.6% | Asia-Pacific Core, Global Spillover | Medium Term (2-4 Years) |

| Influx of Low-Cost Counterfeit Fasteners Causing Safety Recalls | -0.5% | Global with Higher Incidence in Emerging Markets | Short Term (≤ 2 Years) |

| Certification Delays for Novel Alloy Fasteners Under Evolving IMO/ISO Norms | -0.4% | Global with Stricter EU and North America Oversight | Medium Term (2-4 Years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility (Stainless Steel and Aluminum)

Stainless steel and aluminum price fluctuations are creating significant cost pressures across the marine fasteners supply chain, with nickel price volatility particularly impacting 316-grade stainless steel specifications. Trade tensions and tariff implementations have disrupted traditional sourcing patterns, forcing manufacturers to diversify supplier networks while managing inventory costs. Raw material cost increases of 15-20% in affected product categories are compressing margins for fastener manufacturers who face resistance to price increases from cost-sensitive marine operators. The situation is complicated by supply chain disruptions that have extended lead times for specialty alloys, forcing some manufacturers to maintain higher inventory levels that tie up working capital. Alternative sourcing strategies, including increased procurement from Taiwan and other non-Chinese suppliers, are helping mitigate some cost pressures but require significant supply chain restructuring investments.

Cyclical Slowdown in Merchant-Marine New-Build Orders

The merchant marine sector's cyclical nature creates periodic demand contractions that impact fastener consumption, particularly as shipping companies delay new vessel orders during economic uncertainty. Container shipping overcapacity concerns and freight rate volatility are causing operators to extend existing vessel lifespans rather than invest in new construction programs. This trend is partially offset by regulatory-driven retrofits and maintenance requirements, but new-build fastener demand remains vulnerable to broader economic cycles. The shift toward larger, more efficient vessels is reducing the total number of new builds while increasing fastener content per vessel, creating a complex demand dynamic that requires suppliers to adapt their capacity planning and inventory management strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Used: Stainless Steel Dominance Faces Plastic Innovation

Stainless steel maintains commanding market leadership with 46.27% share in 2024, reflecting its superior corrosion resistance and structural integrity in marine environments, while plastic fasteners are emerging as the fastest-growing segment at 6.83% CAGR through 2030. The stainless steel segment's dominance stems from regulatory requirements and operator preferences for long-term durability, particularly in critical structural applications where failure consequences are severe. Aluminum fasteners serve specialized applications where weight reduction is paramount, though their use is limited by galvanic corrosion concerns when paired with dissimilar metals. The "Others" category encompasses exotic alloys like Inconel and Hastelloy for extreme service conditions, representing a small but high-value market segment.

Plastic fasteners are gaining traction as composite hull construction proliferates and weight reduction becomes increasingly important for fuel efficiency optimization. Advanced polymer formulations, including glass-filled nylon and PEEK materials, are enabling plastic fasteners to meet structural requirements previously reserved for metal alternatives. The material selection process increasingly considers total lifecycle costs, including maintenance requirements and replacement intervals, rather than initial purchase price alone. ISO 3506 standards continue to influence material specifications, particularly for stainless steel grades, while emerging standards for composite materials are creating new certification pathways for plastic fastener adoption.

By Product Type: Bolts Lead While Togglers Surge

Bolts command the largest market share at 28.14% in 2024, serving as the backbone for structural connections across all marine applications, yet togglers represent the fastest-growing product category at 7.92% CAGR through 2030. The bolt segment's leadership reflects its universal applicability in hull construction, machinery mounting, and structural assemblies where permanent connections are required. Screws maintain a steady demand for secondary attachments and equipment mounting, while nuts and washers follow bolt demand patterns as complementary components. The washers segment benefits from increased specification of specialty washers with integrated sealing capabilities for improved weather resistance.

Togglers are experiencing rapid growth as modular construction techniques gain adoption in offshore installations and yacht manufacturing, where quick-release mechanisms enable efficient assembly and maintenance procedures. The trend toward modular offshore platforms, particularly in wind farm construction, is driving demand for specialized toggle fasteners that can withstand marine environments while providing reliable quick-disconnect functionality. Smart fastener technologies are beginning to influence product development, with sensor-embedded bolts and nuts enabling real-time monitoring of structural integrity and preload conditions. The "Others" category includes specialized products like captive fasteners and quarter-turn mechanisms that serve niche applications but command premium pricing due to their specialized functionality.

By Application: Merchant Marine Leads as Offshore Support Vessels Accelerate

The merchant marine segment holds the largest market share at 31.08% in 2024, driven by global trade volumes and fleet modernization programs, while offshore support vessels emerge as the fastest-growing application at 8.61% CAGR through 2030. Merchant marine dominance reflects the sheer scale of global shipping operations and the ongoing replacement of aging fasteners in existing fleets as operators comply with enhanced maintenance protocols. Fishing vessels represent a stable market segment with specialized requirements for corrosion resistance and rapid maintenance capabilities during short port calls. Military applications demand the highest specification fasteners with extensive documentation and traceability requirements, creating a premium market segment despite lower volumes.

Offshore support vessel growth is accelerating as energy companies expand deep-water exploration and renewable energy installations, requiring specialized fasteners capable of withstanding extreme marine conditions. The yacht and recreational boat segment benefits from increased leisure spending and the trend toward larger, more sophisticated vessels that specify premium fastening solutions. Regulatory compliance factors significantly influence application-specific fastener selection, with U.S. Coast Guard regulations under 46 CFR § 56.60-1 establishing material and specification requirements for vessel piping systems and related fasteners. The "Others" category encompasses specialized applications like aquaculture installations and research vessels, which often require custom fastener solutions tailored to specific operational requirements.

By Coating/Surface Treatment: Galvanized Standards Meet Fluoropolymer Innovation

Hot-dip galvanized coatings maintain market leadership with 38.22% share in 2024, providing cost-effective corrosion protection for standard marine applications, while PTFE/Xylan fluoropolymer treatments are expanding at 7.46% CAGR through 2030 as operators prioritize long-term performance. The galvanized segment's dominance reflects its established track record and favorable cost-performance ratio for general marine exposure conditions. Zinc-flake and mechanical plating serve applications requiring thinner coating profiles with enhanced corrosion resistance, particularly where tight tolerances must be maintained. Anodized and conversion-coated treatments primarily serve aluminum fastener applications, providing enhanced corrosion resistance and improved paint adhesion.

PTFE/Xylan fluoropolymer coatings are gaining market share as operators recognize their superior performance in extreme marine environments, with salt spray resistance exceeding 4,000 hours in testing protocols. The sherardized and thermal-spray category serves specialized applications requiring thick, durable coatings for extreme service conditions. Advanced coating development is focusing on multi-layer systems that combine sacrificial protection with barrier properties, enabling extended service life in corrosive marine environments. The "Others" category includes emerging coating technologies like ceramic-metallic systems and specialized organic coatings designed for specific marine applications, representing innovation opportunities for suppliers seeking differentiation in competitive markets.

Geography Analysis

Asia-Pacific’s 42.35% revenue dominance in 2024 stems from unparalleled yard throughput and vertically integrated casting, forging, and coating clusters clustered around Bohai Bay and Busan. Chinese state yards channel fixed-price contracts toward domestic bolt makers that can scale duplex-steel production, while South Korean consortia lock in multi-year VMI deals to support LNG carrier pipelines. Japan’s focus on high-value chemical tankers stimulates demand for exotic-alloy studs and precision-machined washers, expanding the marine fasteners market size captured by niche producers. Regulatory scrutiny of counterfeit certificates, especially on small-diameter screws, spurs adoption of blockchain traceability tools across the region.

North America, with a forecast 7.12% CAGR, benefits from overlapping wind-energy, naval-fleet, and port-infrastructure stimuli. U.S. yards in Virginia and Mississippi integrate RFID-tagged fasteners to speed QA audits, shrinking rework times by up to 12%. Canadian polar ice-class projects specify low-temperature-impact-tested bolts, opening revenue streams for vendors producing ASTM F1554-GR105 anchors. Mexico’s Baja yards seize value-ship conversions, offering labor-cost arbitrage yet relying heavily on imported coated washers. The USMCA framework eases cross-border part flows, cementing trilateral supply resilience for the marine fasteners market.

Europe preserves a stable share anchored by North Sea wind farms and luxury yacht yards in Italy and the Netherlands. German turbine OEMs stipulate 25-year bolting warranties that favor PTFE designs, whereas super-yacht builders in Viareggio pay premiums for color-matched anodized screws that complement bespoke paint schemes. Brexit customs realignment prompts U.K. distributors to bulk-import stainless studs via Rotterdam before onward shipping, mitigating documentation delays. Scandinavian ferry electrification retrofits demand insulated fastening kits that avert galvanic coupling between aluminum superstructures and stainless decks, injecting specialized niches into the marine fasteners market.

Competitive Landscape

The marine fasteners market is moderately fragmented, with the top five vendors accounting for just under 35% of global revenue, leaving ample headroom for regional specialists. Fastenal and Stanley Black & Decker leverage nationwide branch networks and digital VMI dashboards to secure high-volume contracts with major shipbuilders, bundling tooling and torque verification services to elevate switching costs. LISI Group positions on the technology frontier, showcasing sensor-embedded bolt prototypes that relay strain data to vessel health-monitoring platforms, thereby appealing to defense primes seeking predictive maintenance.

Mid-tier contenders such as LindFast Solutions and Field Fastener strengthen regional footprints through targeted acquisitions, granting localized inventory and same-day delivery capabilities prized by repair yards. Coating specialists partner with OEMs to co-engineer multi-layer PTFE systems, using proprietary resin blends to differentiate on salt-spray hours and low-friction torque behavior. Counterfeit-mitigation initiatives—ranging from laser-etched batch serialization to blockchain proof-of-origin—are becoming tender pre-requisites, advantaging suppliers able to finance traceability tech stacks.

An emerging battleground is aftermarket analytics. Würth and Hilti bundle IoT torque-monitoring tools with cloud dashboards, promising up to 20% reduction in warranty claims by flagging undertorque events before sailing. Vendors slow to digitalize risk margin erosion as buyers award multi-year blanket agreements to partners offering data-driven uptime assurances. Consolidation pressure will likely intensify, especially in Europe where capacity rationalization could unlock coating-line synergies and scale economies for stainless bar procurement.

Marine Fasteners Industry Leaders

-

Fastenal

-

Stanley Black and Decker

-

LISI Group

-

Nord-Lock Group

-

Howmet Aerospace (Arconic Fastening Systems)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: In June 2024, the U.S. Coast Guard published updates to marine engineering standards (Title 46 CFR Subchapter F), referencing revised norms for valves, fittings, and auxiliary machinery—implicating fastener manufacturers to comply with newer standards.

- May 2024: IperionX and Vegas Fastener will co-produce titanium alloy fasteners targeting marine, aerospace, and defense markets. Together with its allied company, PowerGen Components, Vegas Fastener serves a diverse array of customers in the defense, marine, power generation, etc.

Global Marine Fasteners Market Report Scope

| Aluminum |

| Stainless Steel |

| Plastic |

| Others |

| Bolts |

| Togglers |

| Washers |

| Screws |

| Nuts |

| Others |

| Fishing Vessels |

| Offshore Support Vessels |

| Merchant Marine |

| Yacht/Recreational Boat |

| Military |

| Others |

| Hot-Dip Galvanized |

| Zinc-Flake and Mechanical Plating |

| PTFE/Xylan and Other Fluoropolymer |

| Anodized and Conversion-Coated |

| Sherardized and Thermal-Spray |

| Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material Used | Aluminum | |

| Stainless Steel | ||

| Plastic | ||

| Others | ||

| By Product Type | Bolts | |

| Togglers | ||

| Washers | ||

| Screws | ||

| Nuts | ||

| Others | ||

| By Application | Fishing Vessels | |

| Offshore Support Vessels | ||

| Merchant Marine | ||

| Yacht/Recreational Boat | ||

| Military | ||

| Others | ||

| By Coating / Surface Treatment | Hot-Dip Galvanized | |

| Zinc-Flake and Mechanical Plating | ||

| PTFE/Xylan and Other Fluoropolymer | ||

| Anodized and Conversion-Coated | ||

| Sherardized and Thermal-Spray | ||

| Others | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the marine fasteners market?

The marine fasteners market size reached USD 1.44 billion in 2025 and is projected to hit USD 1.78 billion by 2030.

Which region leads global demand?

Asia-Pacific represented 42.35% of 2024 revenue owing to its dominant shipbuilding base.

Which coating technology is gaining the most traction?

PTFE/Xylan fluoropolymer systems are expanding at a 7.46% CAGR thanks to superior long-term corrosion protection.

What application segment is growing the fastest?

Offshore support vessels are forecast to post an 8.61% CAGR due to deep-water and wind-farm activity.

How are smart fasteners affecting competition?

Vendors offering sensor-embedded bolts and digital torque-monitoring solutions are winning multi-year contracts as shipowners prioritize predictive maintenance.

Page last updated on: