Marine Propeller Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

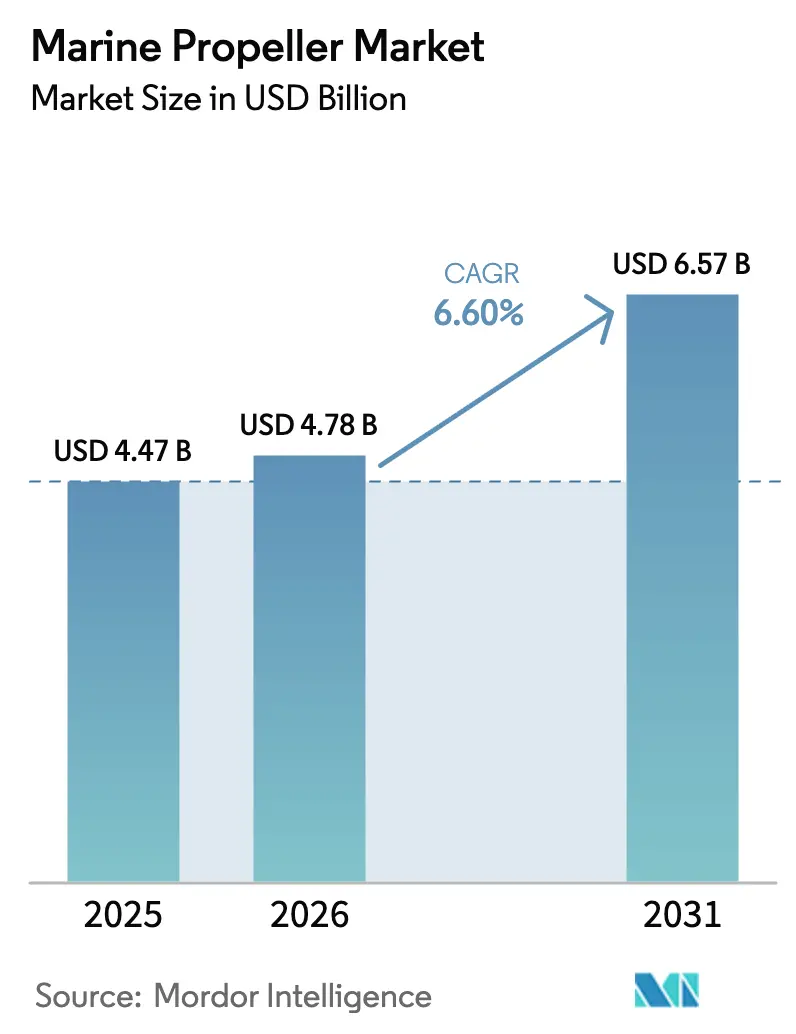

| Market Size (2026) | USD 4.78 Billion |

| Market Size (2031) | USD 6.57 Billion |

| Growth Rate (2026 - 2031) | 6.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Marine Propeller Market Analysis by Mordor Intelligence

The marine propeller market size is expected to grow from USD 4.47 billion in 2025 to USD 4.78 billion in 2026 and is forecast to reach USD 6.57 billion by 2031, growing at a CAGR of 6.60% during the forecast period (2026-2031). Owners are upgrading propulsion systems, driven by tighter IMO Energy Efficiency Existing Ship Index (EEXI) and Carbon Intensity Indicator (CII) rules.[1]International Maritime Organization, “EEXI and CII measures enter into force,” imo.org While cost pressures from volatile nickel-aluminum bronze and composite feedstocks are squeezing margins, the urgency for retrofitting keeps order books robust, even as new-build cycles show signs of softening. Integrated propulsion suppliers, which merge propellers with digital twin design tools, are now directly competing with traditional specialists, marking a significant industry shift toward comprehensive efficiency solutions.

Key Report Takeaways

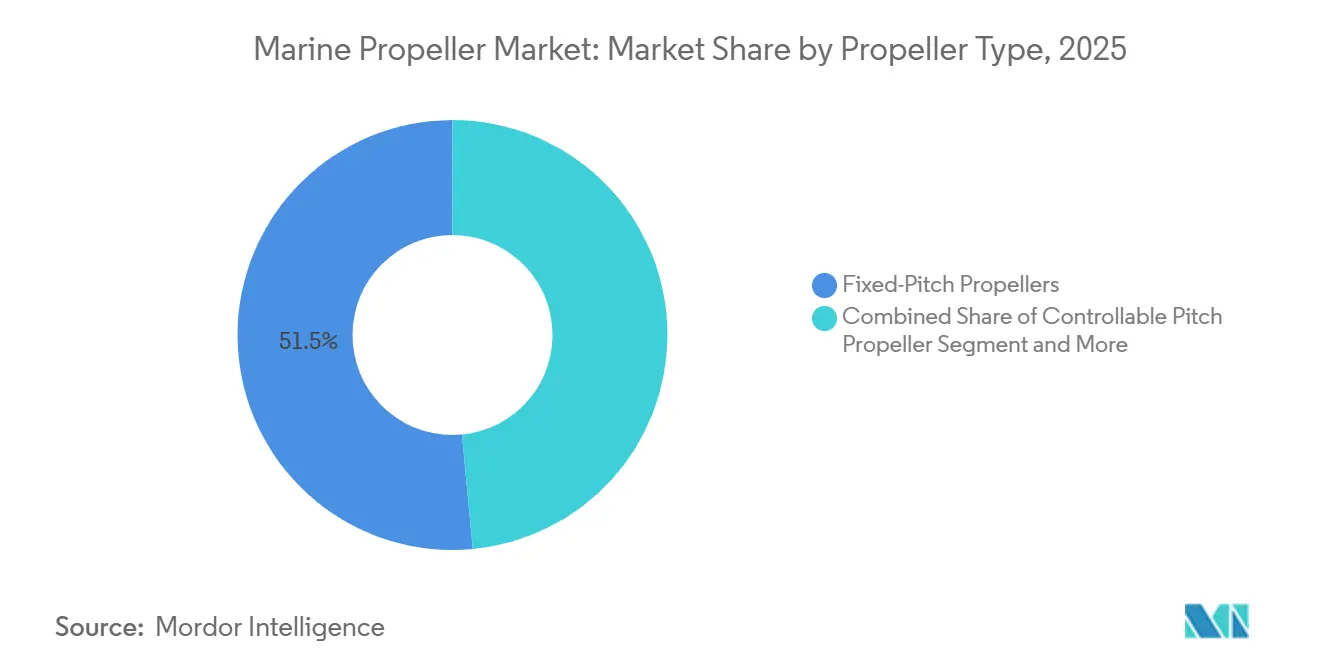

- By propeller type, fixed-pitch designs retained 51.50% of the marine propeller market share in 2025, while controllable-pitch units are projected to clock the fastest 6.70% CAGR through 2031.

- By number of blades, four-blade configurations led the marine propeller market with 39.30% of the market share in 2025; five-blade propellers are forecast to expand at a 6.06% CAGR through 2031.

- By material, nickel-aluminum bronze accounted for 43.60% of the marine propeller market in 2025; composite propellers are set to grow at a 10.50% CAGR through 2031.

- By propulsion system, inboard arrangements contributed 57.70% of the marine propeller market share in 2025, whereas electric pod systems registered the highest 11.80% CAGR through 2031.

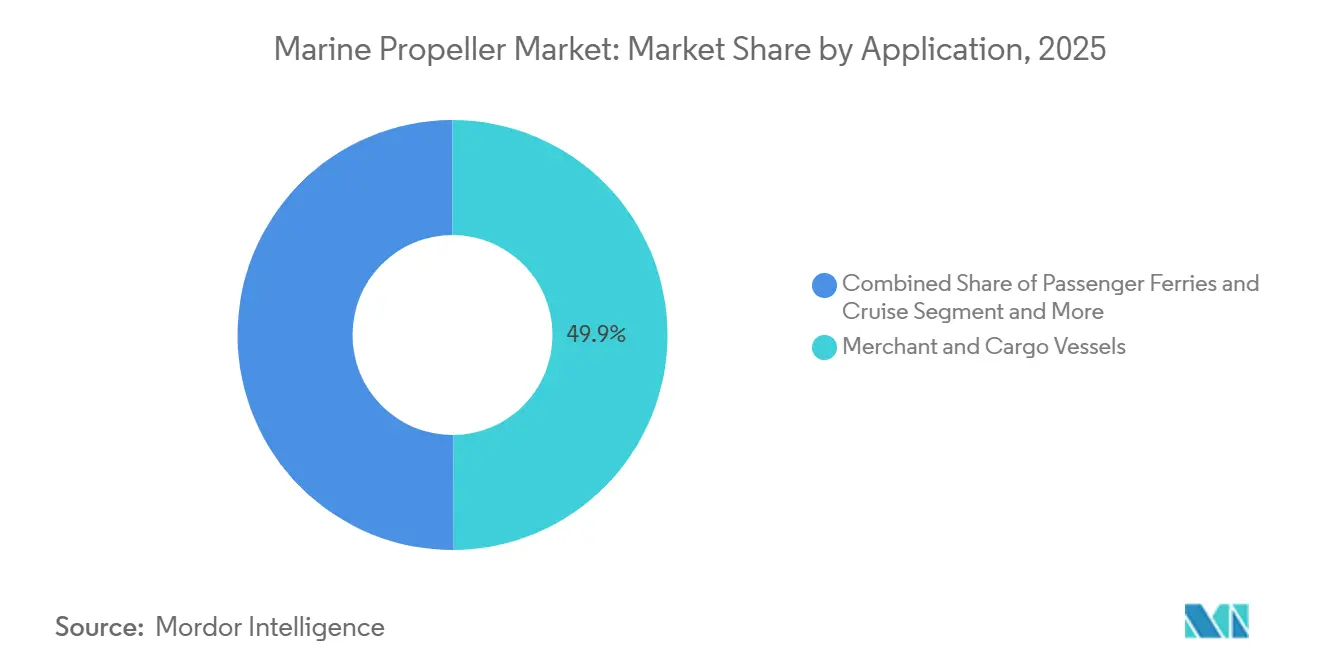

- By application, merchant and cargo vessels commanded a 49.90% share of the marine propeller market in 2025, while offshore support vessels are advancing at an 8.50% CAGR through 2031.

- By sales channel, OEM deliveries accounted for 73.20% of the marine propeller market share in 2025; the aftermarket is growing fastest at an 8.70% CAGR through 2031.

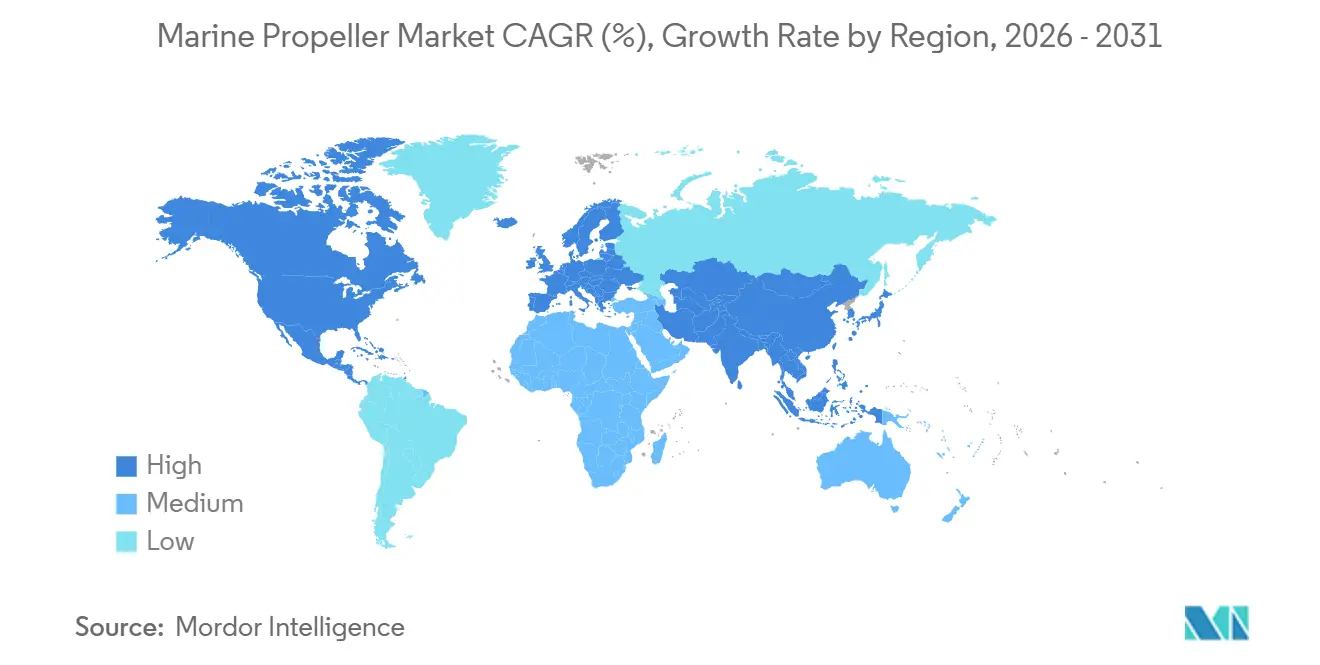

- By geography, Asia-Pacific captured 43.70% of the marine propeller market share in 2025, and is poised for the quickest 6.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Marine Propeller Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IMO EEXI and CII Efficiency Mandates | +1.2% | Global | Short term (≤ 2 years) |

| Expansion of Global Shipbuilding Capacity | +0.8% | Asia-Pacific core, spill-over to global | Medium term (2-4 years) |

| Accelerating Ferry Electrification Projects | +0.6% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Surging Offshore-Wind Vessel Orders | +0.5% | Europe and North America, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Retro-Fit Demand to Meet Underwater-Noise Limits | +0.4% | Global, concentrated in naval regions | Short term (≤ 2 years) |

| Adoption of AI-Driven Digital-Twin Hydrodynamic Design Tools | +0.3% | Global, led by advanced shipbuilding nations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

IMO EEXI and CII Efficiency Mandates

International Maritime Organization rules require annual carbon-intensity improvements, prompting roughly 13,500 ships to contemplate controllable-pitch retrofits, power limitations, or auxiliary upgrades. Only 27 shipyards can handle large-scale propeller work, resulting in an 18-month backlog that is prompting operators to consider modular blade systems assembled at quayside. Because controllable-pitch props allow for blade-angle changes while underway, operators can fine-tune thrust without docking, thereby preserving schedules while meeting compliance targets. Foundries that furnish mobile machining units and accelerated casting cycles are capturing retrofit orders ahead of the 2027 and 2030 audit milestones. As a result, the marine propeller market benefits from a sustained multi-year retrofit pipeline.

Expansion of Global Shipbuilding Capacity in China and South Korea

Hengli Group invested CNY 9.2 billion (USD 1.25 billion) in 2025 to enlarge its Dalian complex for ultra-large container and LNG vessels, each demanding propellers exceeding 10 meters. South Korean leaders Hyundai Heavy Industries and Samsung Heavy Industries continue to dominate premium gas-carrier and naval work, where nickel-aluminum bronze castings withstand cavitation pressures exceeding 3 MPa. These programs integrate controllable-pitch hubs, shaft generators, and hybrid power-take-off modules into single procurement packages, anchoring customers to long-term service deals. Unless European and North American foundries target niches such as composite surface-piercing blades for high-speed ferries, they risk a commodity squeeze.

Accelerating Ferry Electrification Projects

ABB’s Azipod system propels the Tycho Brahe and Aurora ferries with 4,160 kWh batteries, enabling emission-free sailings across the Øresund Strait. Wärtsilä has won 2025 contracts for two battery-electric ferries for Molslinjen, which feature twin azimuth thrusters designed for regenerative braking during docking. Electric drives eliminate gearboxes and allow variable motor speeds, but they also impose tight blade-tip clearances to avoid sensor interference. Shore-power gaps in smaller ports remain a hurdle. Yet, integrated motor-pod-propeller solutions give suppliers a first-mover advantage as electrification moves from Scandinavia toward Mediterranean and Asian shuttle routes.

Surging Offshore-Wind Vessel Orders

DEME’s Norse Wind, delivered in 2025, carries a 3,200-ton crane and dynamic-positioning systems that hold to within 0.5 meters in 2-meter waves using twin azimuth thrusters. Damen’s FLOW-SV design utilizes contra-rotating propellers that recover rotational energy while reducing fuel consumption. As global offshore wind targets aim for 500 GW by 2030, operators prioritize low-noise, ducted propellers that mitigate marine mammal disturbance. Patent portfolios centered on blade skew and composite hubs position Schottel and Rolls-Royce to capitalize on this acoustic imperative.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Raw-Material Price Volatility | -0.7% | Global, acute in supply-constrained regions | Short term (≤ 2 years) |

| Stringent Bio-Fouling/Anti-Cavitation Certification Costs | -0.4% | Global, concentrated in regulated markets | Medium term (2-4 years) |

| Short-Term Ship-Owner Cap-Ex Freeze | -0.3% | Global, acute in cyclical shipping markets | Short term (≤ 2 years) |

| Limited Dry-Dock Slots | -0.2% | Global, concentrated in major shipyard regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Raw-Material Price Volatility

Nickel prices swung between USD 16,000 and USD 24,000 per metric ton during 2024-2025, eroding foundry margins by up to 300 basis points. Carbon-fiber-reinforced polymer blades remain 40-60% more expensive than bronze because the aerospace and automotive sectors compete for prepreg supply. Sellers are exploring aluminum-silicon-magnesium alloys, yet fatigue limits their use in tugboats. Scrap-metal recycling and long-term nickel contracts are surfacing as hedges.

Stringent Bio-Fouling/Anti-Cavitation Certification Costs

ISO 19030 requires continuous performance monitoring, which involves adding USD 50,000-150,000 worth of sensors per vessel. New anti-fouling coatings must clear IMO field trials across multiple climates, pushing R&D spending to USD 2-5 million. Smaller foundries struggle to finance these tests and lean on coatings majors, shrinking their bargaining power within the marine propeller market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propeller Type: Controllable-Pitch Gains on Retrofit Wave

Fixed-pitch propellers accounted for 51.50% of the marine propeller market share in 2025, driven by their lower upfront cost, typically 30 to 40% below controllable-pitch equivalents, and simpler maintenance requirements, which appeal to bulk-carrier and tanker operators prioritizing capital efficiency over fuel optimization. Controllable-pitch propellers are forecast to grow at a 6.70% CAGR through 2031. Azimuth and podded propellers are carving a share in offshore-support and cruise segments, where dynamic positioning and tight-radius maneuvering justify the 50 to 70% price premium; ABB's Azipod units now power over 100 cruise ships globally, with each installation delivering approximately 10% fuel savings versus fixed-pitch shaft-line configurations.

Contra-rotating propellers, which mount two propellers on concentric shafts to cancel torque and recover rotational energy, remain a niche technology, with a market share of under 3%, due to mechanical complexity and higher failure rates in debris-laden waters. Ducted or Kort-nozzle propellers command steady demand in tugboats and inland-waterway vessels, where the shroud boosts static thrust by 25 to 35% at low speeds, though hydrodynamic losses above 12 knots limit adoption in open-ocean trades. Surface-piercing propellers, used in high-speed ferries and military patrol craft, are growing modestly as composite materials reduce weight and enable blade profiles that minimize spray and ventilation losses.

By Number of Blades: Five-Blade Configurations Reduce Noise Signatures

Four-blade propellers held 39.30% of the marine propeller market share in 2025; however, five-blade models outgrew them at a 6.06% CAGR through 2031, offering lower vibration and cavitation while preserving thrust. Rolls-Royce's Adjustable Bolted Propeller on HMS Queen Elizabeth features five blades spanning 6.7 meters in diameter, with each blade individually replaceable, extending the service life beyond 25 years.

Computational fluid dynamics simulations now enable foundries to optimize blade count and skew angle for specific hull forms and operating profiles, moving the industry away from catalog offerings toward application-engineered solutions. Nakashima Propeller's variable-pitch five-blade design, launched in 2024, adjusts blade angle hydraulically to maintain constant shaft speed across varying sea states, reducing engine wear and fuel consumption by approximately 4% on container feeders operating in the Asia-Pacific short-sea trades.

By Material: Composites Surge on Weight and Noise Benefits

Nickel-aluminum bronze held a 43.60% share of the marine propeller market in 2025, but composite propellers are projected to expand at a 10.50% CAGR through 2031. Stainless steel remains the material of choice for high-performance yachts and military patrol craft, offering superior strength-to-weight ratios and corrosion resistance in tropical waters. However, raw material costs are approximately 50% higher than bronze, limiting broader adoption.

Aluminum propellers serve niche roles in inland-waterway and shallow-draft vessels, where reduced weight lowers draft and permits operation in channels with depths of less than 2 meters. However, aluminum's lower fatigue resistance restricts its use to low-thrust applications with a power output of less than 500 kilowatts. Carbon-fiber-reinforced polymers are advancing beyond prototypes as resin suppliers develop epoxy matrices that withstand continuous immersion and impact loading; Sharrow Marine's composite propeller, featuring a looped blade geometry that eliminates tip vortices, achieved 9% fuel savings in independent trials on a 40-foot sportfishing boat.

By Propulsion System: Electric Pods Reshape Ferry and Cruise Segments

Inboard shafts accounted for 57.70% of the marine propeller market share in 2025, yet electric pod systems posted an 11.80% CAGR through 2031, the highest among all propulsion categories. Outboard propulsion dominates recreational craft under 10 meters, with Brunswick's Mercury Marine holding a leading position through its aluminum and stainless-steel propeller lines optimized for gasoline and diesel outboards.

Sterndrive units, which combine inboard engines with outboard lower units, serve the performance-boat segment where operators prioritize shallow-water capability and trailering convenience over fuel efficiency. ABB's Azipod units, which integrate electric motors directly into the pod housing, eliminate gearbox losses and enable 360-degree thrust vectoring for dynamic positioning. The company delivered 12 Azipod installations in 2025 for cruise ships and offshore support vessels, each rated between 5 and 20 megawatts.

By Application: Offshore Support Vessels Lead Growth Amid Wind-Farm Boom

Merchant and cargo vessels generated 49.90% of the marine propeller market share in 2025, yet offshore-support and tugboats register the fastest 8.5% CAGR through 2031, as floating wind projects proliferate.

Recreational and leisure boats are recovering from pandemic-era supply chain disruptions, with outboard propeller sales rebounding as the availability of aluminum and stainless steel feedstock normalizes. Inland-waterway vessels, which operate in rivers and canals with depth restrictions of less than 3 meters, favor ducted propellers that maximize static thrust at low speeds.

However, this segment remains price-sensitive and concentrated among regional foundries in Europe and Asia. Passenger ferries act as test beds for zero-emission and low-noise innovations, while inland barges prioritise shallow-draft propellers that avoid riverbed contact. Leisure craft benefits from quieter composite outboards, mirroring automotive consumer expectations for silent running.[2]ABS, “Future of offshore Support Vessels,”eagle.org

By Sales Channel: Aftermarket Resilience Amid Newbuild Slowdown

OEM sales accounted for 73.20% of the marine propeller market share in 2025. Still, retrofit activity grew more quickly at an 8.70% CAGR through 2031, as ship owners defer capital expenditures amid freight-rate uncertainty.

Mobile machining services, where technicians perform blade polishing and minor repairs afloat, are gaining traction as dry-dock slot availability tightens; Lloyd's Register estimates that only 27 yards globally can handle propeller retrofits on vessels exceeding 100,000 deadweight tons, pushing lead times beyond 18 months. Aftermarket channels also benefit from regulatory retrofits driven by IMO EEXI and underwater-noise mandates, as operators replace fixed-pitch propellers with controllable-pitch variants or upgrade blade materials to reduce cavitation. Rolls-Royce's modular Adjustable Bolted Propeller design, which allows individual blade replacement without removing the hub, is accelerating aftermarket penetration in naval fleets where operational availability is paramount.

Geography Analysis

Asia-Pacific remains the world’s largest hub for propeller demand, with 43.70% of the marine propeller market share in 2025 and expected to grow at 6.76% between 2026 and 2031. China’s CNY 9.2 billion (USD 1.25 billion) Dalian expansion targets ultra-large container vessels with 10-meter bronze propellers. South Korea still commands high-margin LNG and naval work, with propellers facing cavitation pressures above 3 MPa. Japan’s Nakashima couples controllable-pitch expertise with domestic yard tie-ups, and India’s USD 2.8 billion Maritime Development Fund backs shallow-draft projects on inland waterways. Dry-dock queues remain the primary headwind, although mobile machining offers partial relief.

Europe drives electrification. ABB’s Azipod ferries Tycho Brahe and Aurora operate on 4,160 kWh packs, removing 65,000 tCO₂ annually per ship. Wärtsilä will supply twin azimuth thrusters to Denmark’s new battery ferries due in 2027-2028. The EU’s 2030 noise rules push five- and six-blade swept designs. Offshore wind vessels in the North Sea and Baltic adopt low-noise azimuth thrusters, while congestion in Rotterdam and Hamburg forces diversions to yards in Turkey or the United Arab Emirates, inflating retrofit costs.

North America rebounds in leisure boating as Brunswick restores stainless-steel propeller supply. The United States Navy validated a 720-hour endurance for electric-drive unmanned craft, signaling the defense sector's adoption of pods. South America’s coastal ferries prioritize fixed-pitch affordability, whereas Gulf Cooperation Council offshore projects adopt dynamic-positioning thrusters; Kongsberg azimuth units on Rem Offshore vessels illustrate this trend.

Competitive Landscape

The top five players collectively hold a substantial market share. Margin pressure from nickel volatility and dry-dock scarcity is prompting majors to adopt lifecycle contracts that bundle hardware, coatings, and predictive analytics. Wärtsilä’s Fleet Operations Solution and Rolls-Royce’s Intelligent Asset Management exemplify this shift, recovering 3% fuel via data-guided blade maintenance. Composite technology is the next battleground: Sharrow Marine’s looped-blade geometry delivers 9% fuel savings in independent trials, forcing incumbents to accelerate CFD-driven designs.

M&A activity underlines this shift. Fairbanks Morse Defense acquired Rolls-Royce’s Naval Propulsors & Handling unit in 2024 to secure its only United States facility capable of casting large Navy-grade propellers. The deal reflects the rising geopolitical emphasis on localized manufacture and controlled alloy production.[3]Fairbanks Morse Defense, “Fairbanks Morse Defense Completes Acquisition of Rolls-Royce Naval Propulsors & Handling,” fairbanksmorsedefense.com

Patent filings related to digital-twin modeling and composite hubs are increasing, particularly from Rolls-Royce and Schottel, which target upcoming EU acoustic regulations. Smaller foundries lacking funds for USD 2-5 million bio-fouling trials risk exit or acquisition, consolidating share toward vertically integrated conglomerates capable of amortizing certification expenses.

Marine Propeller Industry Leaders

Wärtsilä Oyj Abp

Schottel GmbH

HD Hyundai Heavy Industries Co., Ltd.

MITSUBISHI HEAVY INDUSTRIES, LTD.

Nakashima Propeller Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: A leading global consortium launched the "Digitally Enabled Efficient Propeller" project to evaluate the feasibility of the world's first digitally enabled, additive-manufactured propeller.

- November 2024: Yamaha Motor Corporation unveiled the world’s first hydrogen-fueled outboard prototype, developed with Roush and Regulator Marine, aligning with its 2035 carbon-neutral operations target.

- October 2024: Schottel delivered EcoPellers for four zero-emission autonomous ferries built by Tersan for Norwegian operator Fjord1, integrating electrically driven SRE 340 units.

- July 2024: Brunswick Corporation launched Boating Intelligence, rebranding its I-Jet Lab to develop AI-assisted autonomous docking capabilities across the Mercury and MerCruiser lines.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the marine propeller market as all factory-built, screw-type propulsion devices installed on seagoing commercial, naval, and recreational vessels; the scope covers fixed, controllable, contra-rotating, ducted, azimuth, and surface-piercing propellers supplied through OEM and aftermarket channels in every major hull class.

Scope Exclusions: Thrusters, water-jets, impellers for inland craft below 100 GT, and aerospace or industrial propellers lie outside the boundary.

Segmentation Overview

- By Propeller Type

- Fixed Pitch Propeller

- Controllable Pitch Propeller

- Contra-Rotating Propeller

- Ducted/Kort Nozzle Propeller

- Azimuth/Podded Propeller

- Surface-Piercing Propeller

- Others

- By Number of Blades

- 2 Blades

- 3 Blades

- 4 Blades

- 5 Blades

- 6+ Blades

- By Material

- Nickel-Aluminum Bronze

- Stainless Steel

- Aluminium

- Composite/CFRP

- Others

- By Propulsion System

- Inboard

- Outboard

- Sterndrive

- Electric Pod/Azipod

- By Application (Vessel Type)

- Merchant/Cargo Vessels

- Passenger Ferries and Cruise

- Naval and Defense Vessels

- Offshore Support and Tug Boats

- Recreational and Leisure Boats

- Inland Waterway Vessels

- By Sales Channel

- Original Equipment Manufacturer (OEM)

- Aftermarket

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- Norway

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- Turkey

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed ship designers, propeller manufacturers, classification-society surveyors, and fleet technical managers across Asia-Pacific, Europe, and the Americas. These conversations validated retrofit rates, alloy substitution trends, and region-specific price premiums, filling the data gaps spotted during secondary screening.

Desk Research

We begin with longitudinal vessel and fleet statistics from tier-one public sources such as UNCTAD Review of Maritime Transport, IMO EEXI/CII compliance filings, Clarkson World Shipyard Monitor, Eurostat maritime trade tables, and U.S. Customs import records. Company 10-Ks, shipyard orderbooks, classification-society type approvals, and patent libraries accessed through Questel enrich technology and material cost insights. D&B Hoovers and Dow Jones Factiva supply financial ratios that help benchmark average selling prices. This list is illustrative; many additional open datasets were reviewed to cross-check figures and narratives.

Market-Sizing & Forecasting

A top-down build traces global new-build deliveries and scrapping volumes, then applies weighted propeller counts per vessel class and verified ASP brackets to reconstruct annual demand. Selective bottom-up roll-ups of sampled supplier sales and channel checks are used to fine-tune totals. Key variables like gross tonnage launched, aftermarket retrofit ratio, nickel-aluminum bronze price index, average blade count, and EEXI-driven replacement share feed a multivariate regression that projects value and unit demand through 2030. Where supplier splits are opaque, we bridge gaps with regional prevalence factors benchmarked during interviews.

Data Validation & Update Cycle

Outputs pass two rounds of peer review, variance testing against independent signals (for example, shipyard revenue and alloy shipment data), and senior analyst sign-off. Models refresh annually; material regulatory or macro shocks trigger interim revisions, ensuring clients receive the latest calibrated view.

Why Our Marine Propeller Baseline Commands Reliability

Published estimates often diverge because firms choose different component mixes, cost bases, and forecast cadences.

Key gap drivers include whether thrusters are pooled with propellers, the treatment of retrofit revenue, currency conversion year, and the speed at which IMO rules are assumed to influence fleet upgrades. Mordor Intelligence fixes a consistent scope, refreshes its base year every twelve months, and re-verifies variables through direct stakeholder outreach, thereby reducing hidden assumptions that inflate or deflate totals elsewhere.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.48 B (2025) | Mordor Intelligence | - |

| USD 4.85 B (2025) | Global Consultancy A | Includes bow thrusters and podded drives in revenue pool |

| USD 8.21 B (2025) | Industry Association B | Uses shipment value at distributor level; no retrofit split; broader material scope |

| USD 4.88 B (2024) | Trade Journal C | Base year differs and assumes uniform ASP across regions |

The comparison shows that when scope creep or unmatched currency years are stripped away, Mordor's disciplined variable selection and yearly refresh deliver a balanced, transparent baseline that decision-makers can replicate and audit with limited effort.

Key Questions Answered in the Report

What is the current size of the marine propeller market, and how fast is it growing?

The market stands at USD 4.78 billion in 2026 and is projected to reach roughly USD 6.57 billion by 2031, advancing at a 6.6% CAGR.

Which propeller type is expanding the fastest?

Controllable-pitch propellers lead growth with a 6.70% CAGR due to their ability to improve fuel efficiency and meet IMO EEXI and CII targets.

Which regions matter most for demand today and tomorrow?

Asia-Pacific, accounting for 43.7% of 2025 revenue, is poised to be the fastest-growing region, with projections of a 6.76% CAGR expansion from 2026 to 2031, bolstered by robust shipbuilding and retrofit activities.

What is the single most important market driver?

Mandatory IMO EEXI and CII regulations that link propulsion efficiency to operating licenses and financing, prompting widespread retrofit activity.

What cost or supply challenge most affects manufacturers?

Volatile prices for nickel-aluminum bronze and composite materials can account for up to 60% of a premium propeller’s cost, pressuring margins and complicating long-term contracts.

How concentrated is the competitive landscape?

The top five suppliers hold more than half of the combined share, giving the market a moderate concentration score of 6 while leaving room for regional specialists.

Page last updated on: