Inflatable Boat Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

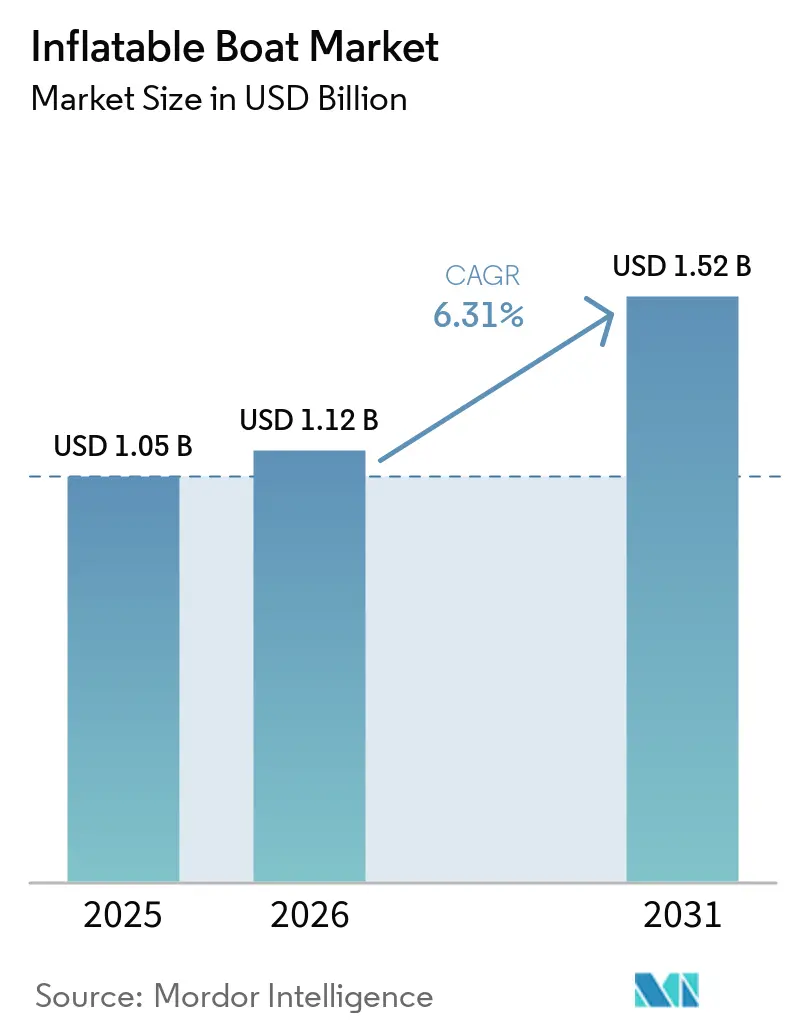

| Market Size (2026) | USD 1.12 Billion |

| Market Size (2031) | USD 1.52 Billion |

| Growth Rate (2026 - 2031) | 6.31% CAGR |

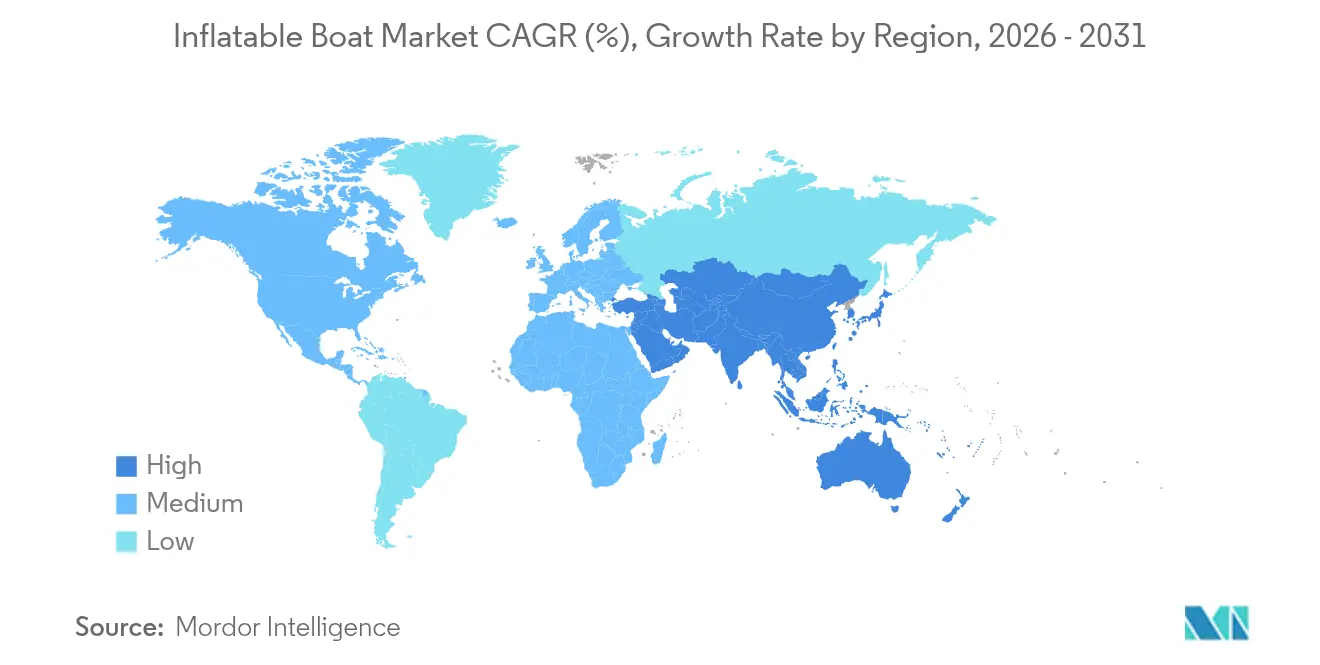

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Inflatable Boat Market Analysis by Mordor Intelligence

The Inflatable Boat market size is expected to grow from USD 1.05 billion in 2025 to USD 1.12 billion in 2026 and is forecast to reach USD 1.52 billion by 2031 at 6.31% CAGR over 2026-2031. Robust defense procurement budgets, a resurgence in coastal tourism, and material innovations such as drop-stitch fabrics are steering consistent demand across professional and leisure user groups. Europe retains volume leadership on the back of harmonized safety regulations, whereas Asia-Pacific is expanding the fastest as coastal infrastructure projects accelerate. Military agencies are broadening tender specifications to include electric and hybrid propulsion. At the same time, peer-to-peer rental platforms widen access for first-time users, reinforcing the overall trajectory of the inflatable boat market. Supply chain pressure on synthetic rubber feedstocks remains a headwind, yet leading brands mitigate risk through dual-sourcing strategies and localized component inventories.

Key Report Takeaways

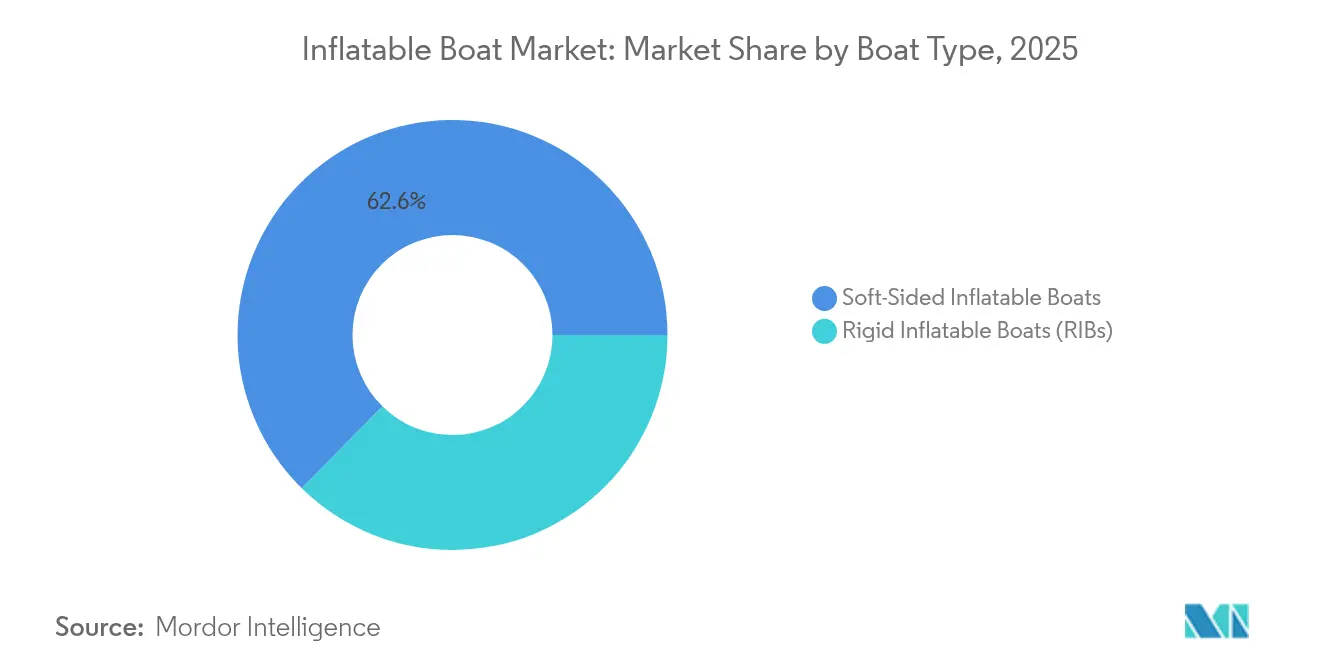

- By boat type, soft-sided models captured 62.64% of the inflatable boat market share in 2025, while rigid inflatable boats are projected to advance at a 6.62% CAGR through 2031.

- By material, PVC commanded 56.34% share of the inflatable boat market size in 2025; Hypalon is forecast to expand at a 6.49% CAGR to 2031.

- By size, medium boats (10-15 ft) held 45.05% revenue share in 2025, whereas large vessels (above 15 ft) are expected to post the quickest 6.55% CAGR through 2031.

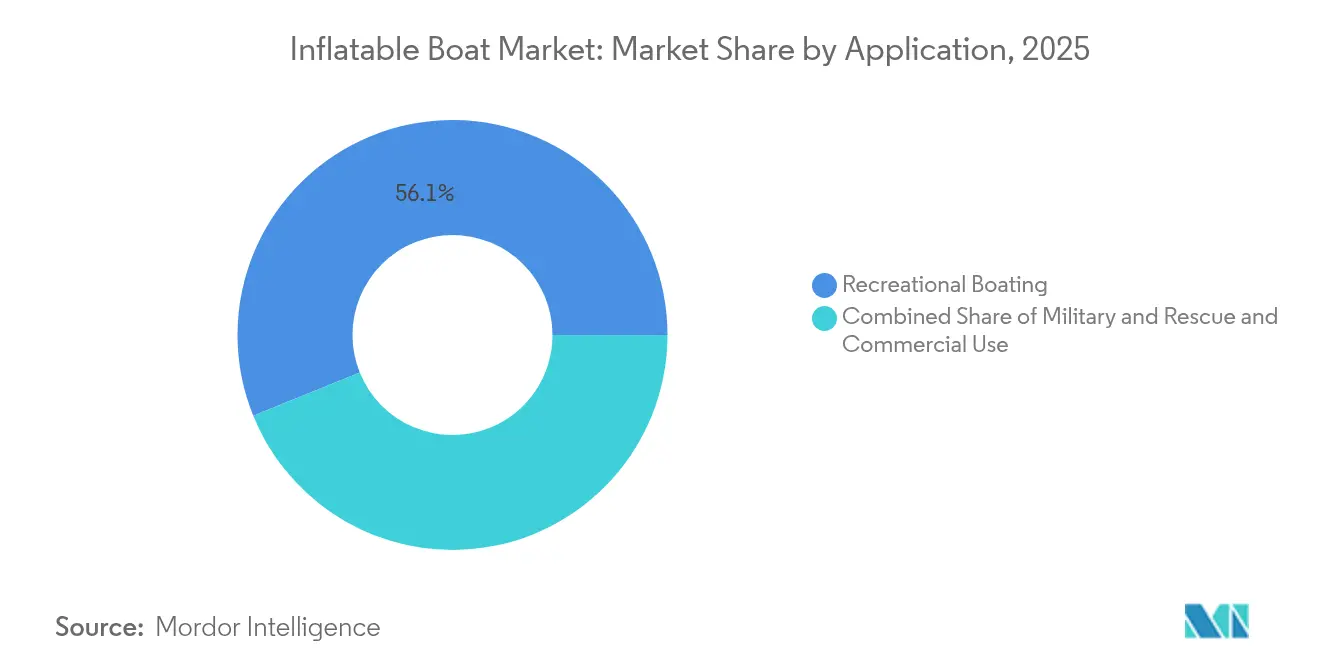

- By application, recreational boating accounted for 56.12% of the inflatable boat market size in 2025, yet military and rescue operations are pacing a 6.57% CAGR through 2031.

- By end user, individual consumers led demand with 61.74% share in 2025, while government agencies are positioned for the highest 6.42% CAGR over the outlook period.

- By geography, Europe retained a 34.12% share of the inflatable boat market in 2025, and Asia-Pacific is set to grow at a 6.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Inflatable Boat Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Diversification Of Outboard-Engine Compatible Models | +1.5% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Growth In Coastal Recreational Tourism | +1.2% | Global, strongest in Asia-Pacific and Mediterranean | Long term (≥ 4 years) |

| Advancements In Lightweight Drop-Stitch Fabric Technology | +1.1% | Global, led by European and North American manufacturers | Medium term (2-4 years) |

| Rising Adoption Of Inflatable Ribs | +0.8% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Increased Defense Spending | +0.7% | Global, concentrated in NATO countries and Asia-Pacific | Short term (≤ 2 years) |

| Surge In Peer-To-Peer Boat-Rental Platforms | +0.6% | Europe and North America, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Diversification of Outboard-Engine Compatible Models

Manufacturers re-engineered transoms and fuel systems so that one hull can accept two-stroke, four-stroke, hybrid, or fully electric units without significant refit costs. Mercury Marine’s Avator 75e and 110e electric outboards give recreational buyers a zero-emission option that slots directly onto existing brackets [1]“Avator 75e / 110e Launch Press Kit,” Mercury Marine, mercurymarine.com . Honda’s BF350 V8 adds variable valve timing for a better fuel economy, making premium horsepower more accessible to rescue agencies seeking a more extended patrol range [2]“BF350 V8 Technical Specifications,” Honda Marine, marine.honda.com . Broader propulsion choice reduces ownership barriers, supports fleet electrification mandates, and elevates residual values for the inflatable boat market. RIB builders benefit disproportionately because rigid keels can absorb higher torque from large electric units, driving faster adoption in military and commercial fleets.

Growth in Coastal Recreational Tourism

The National Marine Manufacturers Association estimates the United States recreational marine economy grew exponentially in the past few years, some of which were inflatables [3]“2024 U.S. Recreational Boating Statistical Abstract,” National Marine Manufacturers Association, nmma.org . Rising disposable income in Southeast Asia and marina expansion projects in Indonesia, Vietnam, and the Philippines extend similar tailwinds. Peer-to-peer charter platforms lengthen utilization hours and lower per-trip costs for casual users, effectively enlarging the addressable pool for the inflatable boat market. Charter operators cite lower insurance premiums—up to one-fifth below fiberglass craft—bolsters profit margins despite recent marina policy hikes. Tourism authorities co-market eco-friendly water sports, indirectly nudging demand toward quieter electric-powered inflatables.

Advancements in Lightweight Drop-Stitch Fabric Technology

Drop-stitch panels now achieve high elastic modulus values, allowing floors to feel as rigid as aluminum while still rolling up compactly for transport. In France and South Korea, automated lamination lines have significantly reduced unit production costs, pushing the technology into mid-priced recreational models. Rescue agencies note that substantial weight savings per hull enhance payload flexibility for helicopters or trucks, broadening their deployment capabilities during flood or wildfire responses. In the inflatable boat market, competitive differentiation increasingly hinges on fabric IP and process patents, leading to joint ventures between raw material suppliers and boat assemblers to secure exclusive cloth allotments.

Rising Adoption of Inflatable RIBs for Autonomous Surface Vessels

At SOFINS 2025, Zodiac Milpro showcased a hybrid craft of considerable size featuring a plug-and-play unmanned systems architecture. The U.S. Navy's SBIR Topic N25-107 is also pushing for inflatable RIB kits that can be air-dropped and transformed into autonomous patrol assets in a short timeframe. The inflatable collar designs, known for their stability, damping, and low signature, are becoming increasingly appealing for sensor-heavy missions. These missions span mine countermeasures, harbor surveillance, and disaster reconnaissance. In the realm of offshore wind maintenance, commercial entities are turning to drone-ready RIBs as a means to mitigate personnel risks. While challenges persist in areas like power management, waterproofing, and secure data links, it's noteworthy that early prototypes have successfully completed extensive autonomous sea trials without any hull issues.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vulnerability To Puncture Damage | -0.9% | Global, particularly in commercial fishing and charter operations | Short term (≤ 2 years) |

| Stringent Environmental Regulations | -0.7% | Europe and North America, expanding globally | Medium term (2-4 years) |

| Supply-Chain Disruptions | -0.6% | Global, concentrated in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Insurance Premium Hikes | -0.5% | North America and Europe, spreading to other developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vulnerability to Puncture Damage in Commercial Operations

Marine insurers have noted a rise in claims for inflatable hulls operating near coral reefs, debris, or fish-processing equipment. This increase has led to significant premium surcharges for charter fleets. Commercial skippers, aware of the downtime from patch repairs, sometimes choose aluminum hulls, even if it means dealing with a heavier displacement. In response, fabric makers have introduced triple-weave coatings and sacrificial keel guards. However, each added layer of protection comes with increased cost and weight. Asian shrimp trawlers, while experimenting with hybrid fiberglass-inflatable collars, have seen a reduction in punctures. Yet, this innovation compromises their ability to store the equipment compactly. Until the industry sees advancements like automated repair tapes or self-healing polymers, certain niches in the inflatable boat market will remain cautious about full-scale adoption.

Stringent Environmental Regulations on PVC Plasticizers

Starting November 2024, EU REACH Annex XVII enforces a minimal lead threshold in PVC. This regulation pushes formulators to shift to phthalate-free plasticizers, which are more expensive per kilogram and often necessitate re-qualification under EN ISO 6185 durability tests. Several U.S. states, led by California, are eyeing similar restrictions, hinting at escalating compliance costs for the inflatable boat sector. While Hypalon and CSM rubber emerge as pricier alternatives, they significantly increase costs, further straining the price point for entry-level models. Companies that invest early in bio-based additives can carve out a branding advantage, but they face the challenge of uncertain long-term UV stability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Boat Type: Performance-Centric RIB Surge

Soft-Sided Inflatable Boats generated a massive amount in 2025, equaling 62.64% of the inflatable boat market size, and are projected to post the leading 6.68% CAGR through 2031. Their rigid keels allow higher horsepower ratings, making them the hull of choice for coast-guard interception, fire rescue, and luxury yacht tender duties where speed and seakeeping trump portability. Zodiac’s X10CC signals consumer appetite shifting toward premium day-boats in the boat rental segment that straddle the boundary between inflatable versatility and rigid-hull comfort.

Soft-sided categories still dominate in volume due to sub-USD 10,000 entry points and rooftop-rack portability that attract first-time owners and campsite renters. Manufacturers ' share by upgrading deck stiffness with drop-stitch floors and plug-and-play seating. The inflation-deflation convenience remains unmatched for seasonal users who store boats in garages. Once buyers cross a power and payload threshold, switching costs toward RIBs diminish, nudging the overall inflatable boat market toward the higher-margin performance end.

By Material: Hypalon Steps Into the Limelight

PVC retained 56.34% of the inflatable boat market share in 2025 as mass-producers in China, Poland, and Vietnam continue to leverage cost grading and automated heat-welding. Yet the segment’s growth lags the 6.49% Hypalon trajectory, reflecting commercial and military buyers' rising durability, fuel-spill resistance, and UV exposure requirements. Italian customs, for instance, stipulate CSM rubber tubes on patrol RIBs that operate multiple hours annually under Mediterranean sun.

Environmental pressures are driving a significant shift. The EU's restrictions on phthalates and California's upcoming listings of Plastics Priority Products are nudging mid-tier brands to opt for alternatives like Hypalon or thermoplastic polyester. This shift comes even with a notable increase in bill-of-materials costs. Premium buyers justify this price hike, noting that these alternatives offer considerably longer service intervals and a higher resale value. As a result, gains from Hypalon in the inflatable boat market are being viewed as a long-term trend rather than a fleeting phase.

By Size: Shift Toward Multi-Day Platforms

Medium hulls between 10 and 15 ft delivered 45.05% of revenue in 2025, traditionally straddling tender duties and family outings. Emerging travel habits now favor above-15 ft craft that can carry camping provisions, dive tanks, or unmanned sensor kits, triggering the top 6.55% CAGR within this size class. Highfield’s plant expansion in Weihai prepares 20 ft aluminum-keel models with enclosed heads, highlighting the blurring line between inflatable and small rigid cruisers.

Small up-to-9 ft tenders defend relevance by enabling davit stowage on 30-40 ft sailboats, yet yacht builders increasingly design garages for 11-12 ft jet tenders, nudging growth away from the micro range. Regulatory crew-carrying limits and fuel-storage rules also push offshore service companies toward larger platforms, further diversifying the inflatable boat market size mix.

By Application: Defense Modernization Ups the Pace

Recreational use retained 56.12% of 2025 spend, buoyed by pandemic-driven outdoor preferences that persist into 2025. However, the Navy, Coast Guard, and Border Patrol bracket logs the fastest 6.57% CAGR, as programs like the U.S. Coast Guard’s Waterways Commerce Cutter funnel funds into rapid-response craft. Military buyers prioritize ballistic-tolerant fabrics, self-righting frames, and shock-mitigating seats, technology that later permeates civilian models via trickle-down engineering.

Commercial fishing, offshore wind, and passenger shuttle operators maintain single-digit growth, restrained by fuel volatility and puncture insurance surcharges. Still, hybrid-propulsion pilots in Denmark and Japan test inflatables as low-wake harbor taxis, foreshadowing new niches. Continuous mission overlap fosters platform modularity, enabling builders to market the same base hull to dive charters on weekends and disaster-relief NGOs during storm season, broadening the inflatable boat market relevance.

By End User: Government Agencies Accelerate

Individual buyers represented a huge slice in 2025 with a share of 61.74%, supported by accessible financing and flexible storage options, yet government outlays will rise faster at 6.42% CAGR through 2031. The UK Border Force placed multi-year framework contracts for high-speed inflatables built to the SOLAS rescue code. India’s Coast Guard budgets capex for 37 coastal interceptor boats with inflatable collars.

Commercial fleet operators navigate a middle path, scaling cautiously amid insurance scrutiny. Peer-to-peer platforms feed used-boat supply to private hands, flattening new-unit demand volatility. Public-sector capability gaps in disaster management and migrant interception sustain long-term procurement visibility, cementing agencies as the strategic demand anchor of the inflatable boat market.

Geography Analysis

In 2024, Europe commanded a significant share of the global revenue, bolstered by the Recreational Craft Directive and standardized EN ISO 6185 norms, which facilitate smoother cross-border trade and certification. Countries like Italy, Spain, and Greece, with their dense marinas and vibrant charter ecosystems, continue to thrive, ensuring a steady turnover for both leisure and professional fleets. Meanwhile, defense budgets in France, Germany, and Nordic nations are increasingly allocating funds for multi-role RIBs. These vessels, versatile enough to serve as firefighting units or for migrant support, are boosting after-sales contracts for local shipyards. Furthermore, as sustainability policies tighten, with upcoming restrictions on PVC additives, regional suppliers are pivoting towards eco-friendly composites. This shift not only underscores a commitment to sustainability but also positions tech leaders in the inflatable boat market as frontrunners.

Asia-Pacific is set to lead with robust growth through 2030, driven by the expansion of coastal economic zones, a surge in island tourism, and a push for naval modernization. In China, clusters in Shandong, Guangdong, and Fujian are reaping the benefits of scale synergies. Local governments are further sweetening the deal, subsidizing industrial parks that host everything from tube fabricators to engine OEMs. In India, the unveiling of Sagarmala port upgrades and a focus on disaster-response capabilities hint at upcoming RIB tenders. Across ASEAN nations, as marina numbers swell and import tariffs diminish, European luxury brands find a warm welcome in showrooms across Jakarta, Penang, and Phuket. With rising disposable incomes, first-time boat ownership is becoming a reality for many. Middle-class families are increasingly viewing compact inflatables as affordable leisure options, further embedding the inflatable boat market in the region.

North America witnesses steady growth, buoyed by record participation numbers from the NMMA and a robust base of adult boaters. Agencies like the U.S. Coast Guard, the Department of Homeland Security, and local fire departments engage in predictable, multi-year procurement cycles, ensuring consistent demand even amidst broader economic slowdowns. In South America, Brazil stands out with promising signs. The nation is on track to significantly boost its annual production over the years, marking notable growth. This growth hints at potential diversification across the broader Latin landscape. Meanwhile, the Middle East and Africa see selective advancements, particularly in Gulf marinas and the tourism corridors of Africa's Great Lakes. Yet, challenges like regulatory ambiguities and currency fluctuations temper the rapid expansion of the inflatable boat market in these regions.

Competitive Landscape

In 2024, the inflatable boat market showcases a moderate level of fragmentation, with the leading brands holding a significant share of unit shipments. Brands like Zodiac, BRIG, Highfield, Williams Jet Tenders, and AB Inflatables maintain their market share through diverse distribution channels, portfolios certified by CE, and swift prototyping capabilities. In early 2024, MarineMax bolstered its vertical integration by acquiring Williams Jet Tenders, ensuring a steady supply of luxury yacht tenders for its expansive motor-yacht clientele. Meanwhile, Highfield's newly established large-scale facility in China has significantly increased production capacity, signaling a strong belief in the demand for family boating, particularly for vessels of smaller lengths.

Technological collaborations are becoming pivotal for market differentiation. In the near future, Arksen's partnership with RAD Propulsion melded battery packs and rim-drive thrusters with composite-deck inflatables, a move aimed at aligning with zero-emission mandates in marinas. Mercury Marine and Brunswick are channeling data from Avator motors into Nautic-On telematics, a step that bolsters fleet management capabilities for charter businesses. Additionally, innovative start-ups like Seabound are embedding AI-driven collision avoidance systems into smaller RIBs, pushing traditional manufacturers towards necessary digital upgrades.

Asian manufacturers, capitalizing on cost benefits, are ambitiously targeting premium export markets. They're achieving this by licensing advanced Hypalon formulations and successfully passing ISO 9001 audits. In response, established Western brands are offering bespoke solutions, from custom upholstery and carbon stringer reinforcements to extended warranties spanning several seasons. This interplay has birthed a dynamic market equilibrium, where cost efficiency, regulatory compliance, and advanced capabilities converge. This balance not only allows nimble brands to seize opportunities in emerging sectors like autonomous surface vessels but also helps them safeguard their established presence in the expansive inflatable boat arena.

Inflatable Boat Industry Leaders

AB Inflatables

Ribcraft USA LLC

Zodiac Nautic

Walker’s Bay

Damen Shipyard

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: RAD Propulsion and Arksen have teamed up to jointly create electric drive kits aimed at producing zero-emission inflatables. This collaboration focuses on advancing sustainable marine technology by integrating RAD Propulsion's expertise in electric propulsion systems with Arksen's commitment to eco-friendly marine solutions. The electric drive kits are designed to reduce environmental impact while maintaining high performance, catering to the growing demand for sustainable alternatives in the marine industry.

- January 2025: At Boot Düsseldorf, Highfield unveiled its ADV 7 adventure model, now featuring modular roof racks and a reinforced chassis. Designed specifically for offshore camping enthusiasts, the model aims to enhance functionality and durability, catering to the growing demand for versatile adventure boats.

- June 2024: Mercury Marine introduced its Avator 75e and 110e electric outboards, specifically designed for inflatable transoms. These electric outboards aim to provide a sustainable and efficient solution for boating enthusiasts, aligning with the growing demand for eco-friendly marine technologies.

Global Inflatable Boat Market Report Scope

An inflatable boat is considered a lightweight boat constructed which is constructed as a flexible structure with its sides and bow made of flexible tubes carrying pressurized gas.

The Inflatable Boat Market is segmented by end-user type, boat type, and by geography. Based on end-user type, the market is segmented into leisure, defense, and others. Based on boat type, the market is segmented into rigid and soft, and based on geography, the market is segmented into North America, Europe, Asia Pacific, and the Rest of the World. For each segment, the market sizing and forecasting are based on value (USD Billion).

| Rigid Inflatable Boats (RIBs) |

| Soft-Sided Inflatable Boats |

| Hypalon |

| PVC (Polyvinyl Chloride) |

| Rubber |

| Small (up to 9 ft) |

| Medium (10 – 15 ft) |

| Large (above 15 ft) |

| Recreational Boating |

| Military & Rescue |

| Commercial Use |

| Individual Consumers |

| Commercial Operators |

| Government Agencies |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Turkey | |

| Rest of Middle East and Africa |

| By Boat Type | Rigid Inflatable Boats (RIBs) | |

| Soft-Sided Inflatable Boats | ||

| By Material | Hypalon | |

| PVC (Polyvinyl Chloride) | ||

| Rubber | ||

| By Size | Small (up to 9 ft) | |

| Medium (10 – 15 ft) | ||

| Large (above 15 ft) | ||

| By Application | Recreational Boating | |

| Military & Rescue | ||

| Commercial Use | ||

| By End User | Individual Consumers | |

| Commercial Operators | ||

| Government Agencies | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the inflatable boat market?

It is valued at USD 1.12 billion in 2026 with a forecast of USD 1.52 billion by 2031.

Which region is growing the fastest for inflatable boats?

Due to coastal infrastructure expansion, the Asia-Pacific is projected to register a 6.46% CAGR through 2031.

Which boat type is set to grow quickest?

Rigid inflatable boats are expected to post a 6.62% CAGR, benefiting from defense and premium leisure demand.

How are environmental rules affecting material choices?

EU and U.S. plasticizer limits raise costs for PVC tubes, steering buyers toward Hypalon or bio-based alternatives despite higher upfront prices.

What impact will electric propulsion have on inflatable boats?

New electric outboards such as Mercury’s Avator series enhance zero-emission compatibility, opening rental and urban marina opportunities while fueling aftermarket battery demand.

Who are the leading companies in this space?

Zodiac, BRIG, Highfield, Williams Jet Tenders, and AB Inflatibles command over 38% of global shipments, with emerging competition from electric-focused start-ups.

Page last updated on: