Marine Seats Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.89 Billion |

| Market Size (2031) | USD 2.29 Billion |

| Growth Rate (2026 - 2031) | 3.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

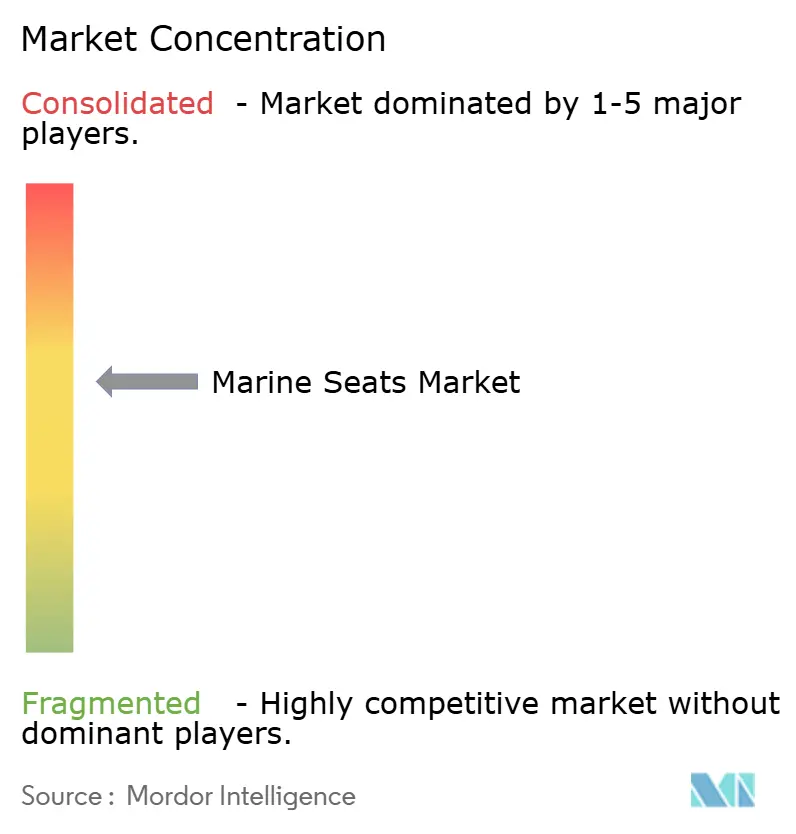

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Marine Seats Market Analysis by Mordor Intelligence

The marine seats size market size in 2026 is estimated at USD 1.89 billion, growing from 2025 value of USD 1.82 billion with 2031 projections showing USD 2.29 billion, growing at 3.89% CAGR over 2026-2031. This trajectory signals the sector’s passage from post-pandemic recovery into a maturity phase where ergonomic innovation, weight reduction, and regulatory compliance carry more weight than raw production volume. Shipowners are upgrading cabins, bridges, and passenger-area seats to meet tighter vibration and fire-safety rules. At the same time, military and offshore operators seek shock-mitigating solutions that protect crews during high-speed maneuvers. Weight-saving composite frames, embedded sensors, and 3D-printed components enable builders to differentiate themselves on comfort, sustainability, and lifecycle cost. The growing preference for premium finishes in cruise, yacht, and fast ferry builds also supports value growth even as unit shipments level out.

Key Report Takeaways

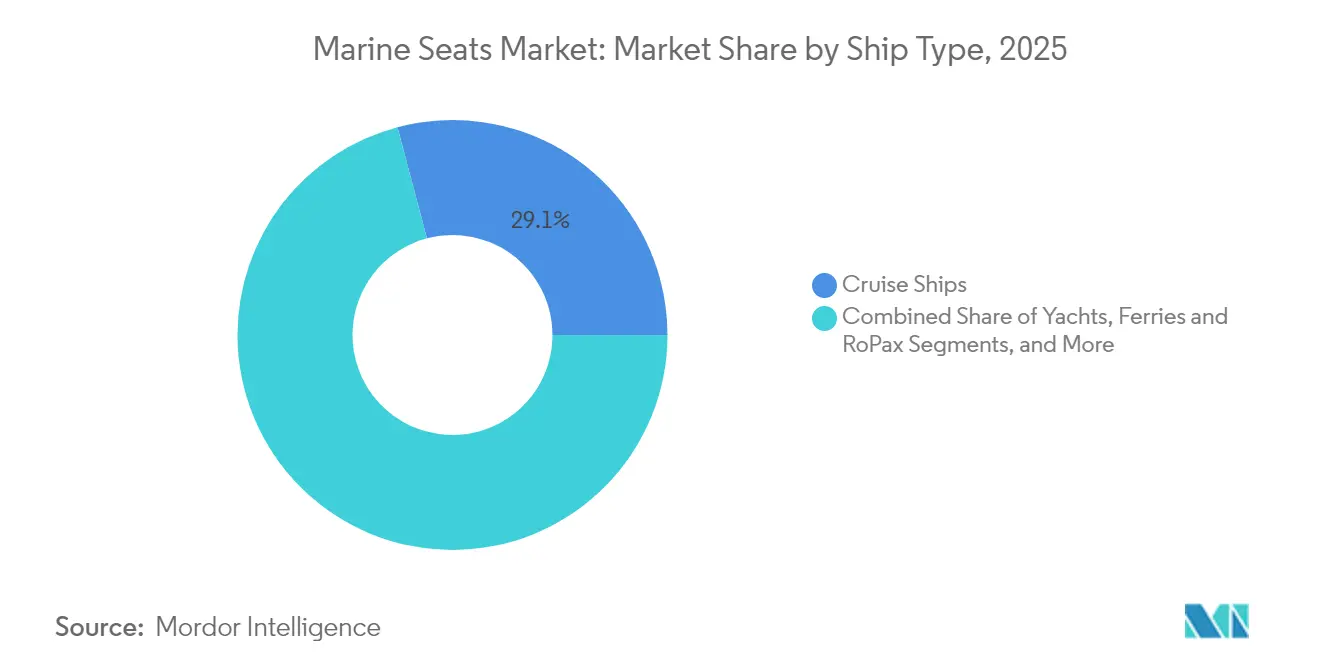

- By ship type, Cruise Ships led with 29.12% revenue share in 2025, whereas Commercial Workboats are poised to expand at a 6.78% CAGR through 2031.

- By component, Pedestals accounted for 32.60% of the marine seats market size in 2025; Suspension Systems are projected to grow the fastest at 5.12% CAGR.

- By seat technology, Manual Adjustable designs held 37.22% of the marine seats market share in 2025, while Suspension technology is set to advance at 5.55% CAGR.

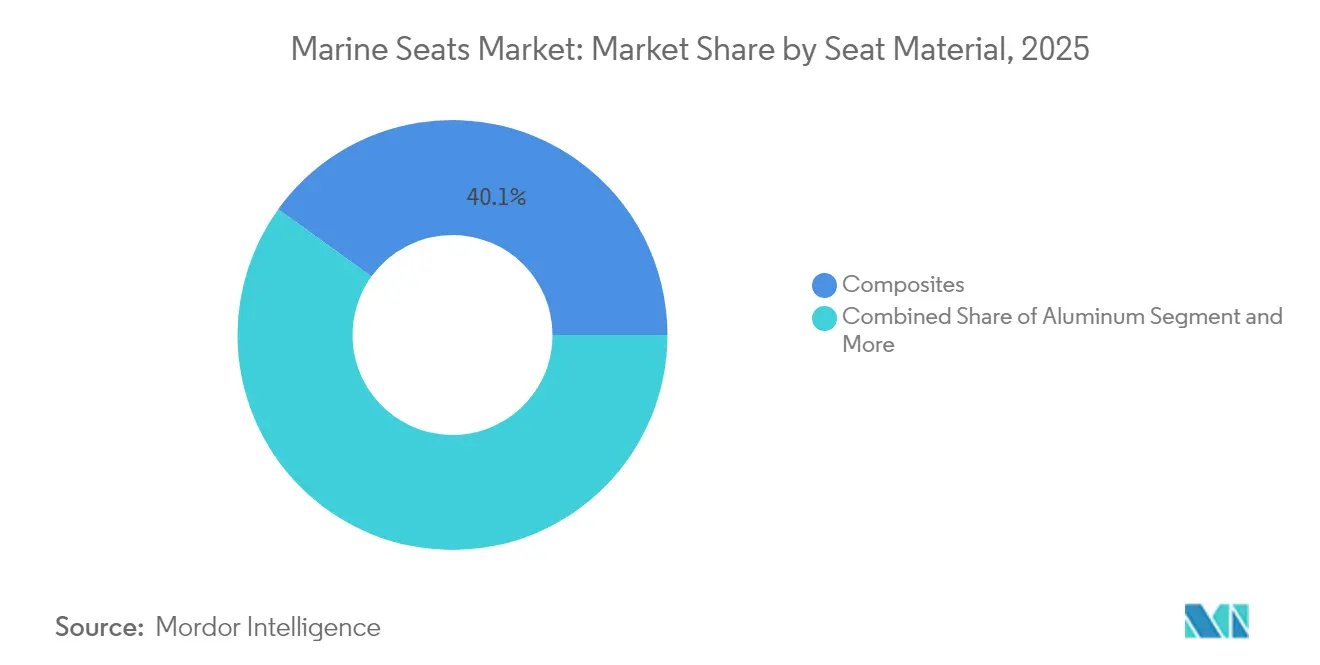

- By seat material, Composites commanded 40.05% share of the marine seats market size in 2025 and are forecast to climb at a 7.12% CAGR to 2031.

- By end user, Passenger Transport captured a 27.55% share in 2025; the Commercial segment is the fastest riser at 6.65% CAGR.

- By geography, North America dominated with a 31.70% share in 2025, whereas Asia Pacific is projected to register the highest 7.78% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Marine Seats Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cruise-liner Refurbishment Cycles | +1.2% | Global, led by North America and Caribbean routes | Short term (≤ 2 years) |

| IMO Ergonomic Safety Regulations | +0.9% | Global maritime compliance zones | Long term (≥ 4 years) |

| Premium Yacht Production Boom | +0.8% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Fast-patrol and SAR Vessel Shock-mitigation Mandates | +0.6% | North America, Europe, APAC defense sectors | Medium term (2-4 years) |

| Embedded Smart-sensor Seating | +0.4% | Premium segments globally | Long term (≥ 4 years) |

| 3-D Printed Composite Seat Structures | +0.3% | North America and Europe early adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cruise-Liner Refurbishment Cycles

Operators are spending record sums on mid-life overhauls, with Celebrity Cruises channeling more than USD 250 million into Solstice-class upgrades that include full seating replacements across dining, theater, and pool decks. According to Cruise Lines International Association (CLIA), member lines are anticipated to witness 9% rise in 2025 passenger counts, supporting these capex waves, making refurbishment the most reliable near-term catalyst for the marine seats market. Suppliers that possess turnkey design-install capabilities capture an outsized share by synchronizing deliveries with narrow dry-dock windows.

IMO Ergonomic Safety Regulations

The International Maritime Organization is broadening whole-body vibration and crew-welfare limits within its Code on Intact Stability, prompting owners to specify adjustable seats with lumbar support and automated height memory.[1]International Maritime Organization, “Code on Intact Stability Amendments,” imo.org A delayed roll-out of revised GMDSS standards until 2028 allows builders to integrate communication panels into armrests, further enriching the marine seats market value proposition.

Premium Yacht Production Boom

Global orderbooks list 633 superyachts over 30m in build, sustaining demand for bespoke seating that blends lightweight composites with luxury finishes. Shipyards such as Sanlorenzo are investing in high-margin projects after acquiring niche builders like Nautor Swan, widening the addressable marine seats market for premium solutions. Ergonomic requirements rise in parallel with green mandates, steering designers toward recyclable foams and bio-based laminates that trim emissions without sacrificing comfort.

Fast-Patrol and SAR Vessel Shock-Mitigation Mandates

Project Perfect Storm tests show advanced suspension seats cutting peak impacts by up to 40% during 50-knot transits. The UK Maritime & Coastguard Agency now requires shock-protective seating on small rescue craft under MGN 436, a rule likely to spread across NATO fleets.[2]UK Government, “MGN 436: Small Vessel High-Speed Craft Guidance,” gov.uk These mandates underpin a steady pipeline for high-end suspension modules and data-logging seat bases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Marine-grade Alloy Price Volatility | -0.7% | Global, acute in aluminum-dependent regions | Medium term (2-4 years) |

| High Certification and Testing Costs | -0.5% | Global, regulatory compliance markets | Medium term (2-4 years) |

| Specialty Foam Supply Interruptions | -0.4% | North America & Europe manufacturing hubs | Short term (≤ 2 years) |

| IMO Fire-testing Bottlenecks | -0.3% | Global maritime compliance zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Marine-Grade Alloy Price Volatility

Sudden price swings in aluminum and stainless steel squeeze margins, especially where fixed-price tenders dominate naval and ferry contracts. Builders are locking multi-year supply agreements and trialing composite-metal hybrids to curb exposure, yet these hedges tie up working capital and slow specification changes.

High Certification and Testing Costs

The American Bureau of Shipping lists more than 40 individual seat-related checks covering fire, vibration, structural, and upholstery toxicity. Full compliance often tops USD 0.2 million per seat family, discouraging small entrants and lengthening payback for novel designs.[3]American Bureau of Shipping, “Rules for Materials and Welding,” eagle.org Industry groups are pursuing common test protocols, but progress is uneven across flag states.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ship Type: Cruise Dominance Drives Premium Positioning

Cruise Ships controlled 29.12% of the marine seats market in 2025, thanks to USD 250 million retrofit programs that swapped thousands of theaters and pool-deck seats for ergonomic replacements. Refurbishment schedules guarantee short lead times between order and installation, favoring suppliers with proven global logistics. Commercial Workboats deliver the highest 6.78% CAGR as offshore energy and aquaculture operators adopt shock-mitigation seats to lower fatigue during multishift operations.

Across patrol, SAR, and naval craft, regulators such as the UK MCA now require suspension seats, putting defense programs in the premium tier of the marine seats market. Yacht builders focus on customization and lightweight frames, often blending carbon prepregs with stitched leather to secure visual appeal at displacement-friendly mass. Ferries and RoPax vessels concentrate on vandal-resistant upholstery and quick-change covers that limit downtime during daily turnarounds.

By Component Type: Suspension Systems Lead Innovation Wave

Pedestals contributed 32.60% to the marine seats market size in 2025, as every bridge and passenger seat relies on height and swivel adjustment platforms. However, Suspension Systems are set to grow 5.12% annually because owners want documented G-force reduction for crew claims and insurance compliance.

Swivels and Slides stay relevant for cabin and cockpit seating, though OEMs integrate corrosion-proof polymers to extend service life in tropical climates. Upholstery and foam suppliers face the dual challenge of resin shortages and stricter low-smoke toxicity benchmarks, making vertically integrated seat makers more attractive to shipbuilders needing guaranteed delivery windows.

By Seat Technology: Manual Adjustable Dominance Faces Suspension Challenge

Manual Adjustable models kept 37.22% of the marine seats market share in 2025 on the strength of proven durability and minimal maintenance in harsh salt environments. Budget-constrained operators favor their mechanical simplicity, yet regulatory momentum toward shock protection is accelerating orders for suspension seats that should post a 5.55% CAGR to 2031.

Smart Sensor-Integrated seats, although still a niche, capture headlines by pairing cloud-linked pressure mats with predictive maintenance dashboards. Manual fixed designs survive in utility barges and inland workboats where cost ceilings and low-speed duty cycles limit demand for advanced features.

By Seat Material: Composites Accelerate Sustainability Drive

Composites held 40.05% of the marine seats market size in 2025 and are expected to grow 7.12% annually as shipowners chase fuel savings through mass reduction. Recyclable resins and bio-fillers align with upcoming European end-of-life directives, giving composite frames an edge over aluminum for green-flag operators.

Aluminum retains its share due to global fabrication familiarity and straightforward recycling loops, whereas stainless steel serves niche fire-zone or offshore splash-zone uses. Breakthroughs in 3-D printed composite ribs cut tooling lead time and open the door to bespoke ergonomic contours at series-production prices.

By End User: Commercial Segment Drives Growth Acceleration

Passenger Transport applications, encompassing cruise vessels and ferries, owned 27.55% of the 2025 demand as lines invested in comfort upgrades to entice post-pandemic travelers. Meanwhile, Commercial operators from offshore energy, aquaculture, and crew supply constitute the fastest-growing user base, expanding at 6.65% CAGR on stronger capital spending and rising crew-welfare requirements.

Recreational buyers center on aesthetics and smart features to differentiate new-build yachts, whereas Military and government agencies procure rugged, certified shock-mitigation seats that interface with tactical displays and body armour geometry.

Geography Analysis

North America captured 31.70% of global revenue in 2025, leveraging a mature defense procurement cycle, vibrant luxury yacht yards, and a dense ferry network on the US East and West coasts. Harmonized lifejacket standards between the US Coast Guard and Transport Canada lower cross-border barriers for seat makers, and offshore wind farm expansions create fresh demand for crew-transfer-vessel seating. Shipyards value locally supported certification services, leading to sticky supplier relationships within the marine seats market.

Asia-Pacific is forecast to grow 7.78% annually through 2031 as India’s Maritime Vision 2030 and China’s dominant shipbuilding capacity funnel newbuild orders to domestic yards. Rising labor-cost awareness pushes owners to specify ergonomic seats for fatigue mitigation, and regional defense budgets add volume for fast-patrol and missile craft. Suppliers that establish regional assembly plants gain tariff advantages and quicker response times for warranty calls.

Europe prioritizes sustainability and stringent safety, maintaining a steady retrofit cycle among Mediterranean cruise fleets and North Sea wind-farm service vessels. Proximity to IMO headquarters in London encourages early compliance adoption, and EU Green Deal initiatives offer grants for recyclable seating research. The competitive landscape includes long-standing brands that pair design heritage with advanced material science, reinforcing Europe’s influence on global seating standards.

Competitive Landscape

The marine seats market shows moderate concentration, with a cluster of global manufacturers commanding scale economies while niche innovators compete on technology. United Safety’s 2024 acquisition of Allsalt Maritime merged shock-monitoring electronics with seating hardware, illustrating vertical integration aimed at lifecycle analytics. Large OEMs market full interior packages, bundling helm chairs, passenger benches, and lounge recliners to secure sole-source contracts.

R&D priorities revolve around lighter composite frames, data-rich suspension modules, and fire-safe eco-foams. RECARO’s license deal with Sun Marine Seats transfers aerospace memory-function know-how into vessel cabins, quickening the shift toward personalized comfort. Mid-tier players differentiate through fast customization, offering color-matched stitching and digital print fabrics delivered within four-week windows.

Startup challengers target retrofit fleets with plug-and-play shock-data seats sold via subscription that include analytics dashboards and firmware updates. Legacy brands respond by launching upgrade kits compatible with existing pedestals, defending installed bases while exploring pay-per-use maintenance contracts. Pricing discipline remains firm as buyers weigh safety credentials and total ownership cost over headline discounts.

Marine Seats Industry Leaders

Stidd Systems Inc.

Grammer AG

Shockwave Seats

NorSap AS

Ullman Dynamics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Shockwave Seats signed Kent Marine Equipment as exclusive French distributor, expanding service and support reach in Europe.

- September 2024: Ullman Dynamics debuted Revolutionary Suspension Seats at La Rochelle Grand Pavois, underscoring its focus on high-speed comfort.

- September 2024: Shockwave Seats broadened its S5 recreational line with stainless-steel S5-SS and lightweight S5-LW variants for freshwater craft.

- August 2024: Springfield Marine Company acquired Shark Limited to add lightweight suspension technology to its product portfolio.

Global Marine Seats Market Report Scope

The marine seats market covers the latest trends, demand by seat component type, ship type, and the market share of the major manufacturers across the world. Military ships are not covered under the scope.

| Yachts |

| Cruise Ships |

| Ferries and RoPax |

| Patrol, SAR, and Military Craft |

| Commercial Workboats |

| Pedestals |

| Swivels |

| Slides and Seat Mounts |

| Suspension Systems |

| Upholstery and Foam |

| Manual Fixed |

| Manual Adjustable |

| Suspension |

| Smart Sensor-Integrated |

| Aluminum |

| Stainless Steel |

| Composites |

| Others |

| Recreational |

| Passenger Transport |

| Commercial |

| Military and Patrol |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Ship Type | Yachts | |

| Cruise Ships | ||

| Ferries and RoPax | ||

| Patrol, SAR, and Military Craft | ||

| Commercial Workboats | ||

| By Component Type | Pedestals | |

| Swivels | ||

| Slides and Seat Mounts | ||

| Suspension Systems | ||

| Upholstery and Foam | ||

| By Seat Technology | Manual Fixed | |

| Manual Adjustable | ||

| Suspension | ||

| Smart Sensor-Integrated | ||

| By Seat Material | Aluminum | |

| Stainless Steel | ||

| Composites | ||

| Others | ||

| By End User | Recreational | |

| Passenger Transport | ||

| Commercial | ||

| Military and Patrol | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Egypt | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the marine seats market?

The market stands at USD 1.89 billion in 2026 and is projected to reach USD 2.29 billion by 2031.

Which ship type generates the highest demand for marine seating?

Cruise Ships hold the largest share at 29.12% in 2025, driven by extensive refurbishment programs.

Which component category is growing the fastest?

Suspension Systems are advancing at a 5.12% CAGR thanks to regulatory focus on shock mitigation.

Why are composites gaining popularity in marine seat construction?

Composites offer weight savings, corrosion resistance and align with sustainability goals, helping the material segment achieve a 7.12% CAGR.

Page last updated on: