Marine Electronics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 6.62 Billion |

| Market Size (2030) | USD 8.91 Billion |

| Growth Rate (2025 - 2030) | 6.14% CAGR |

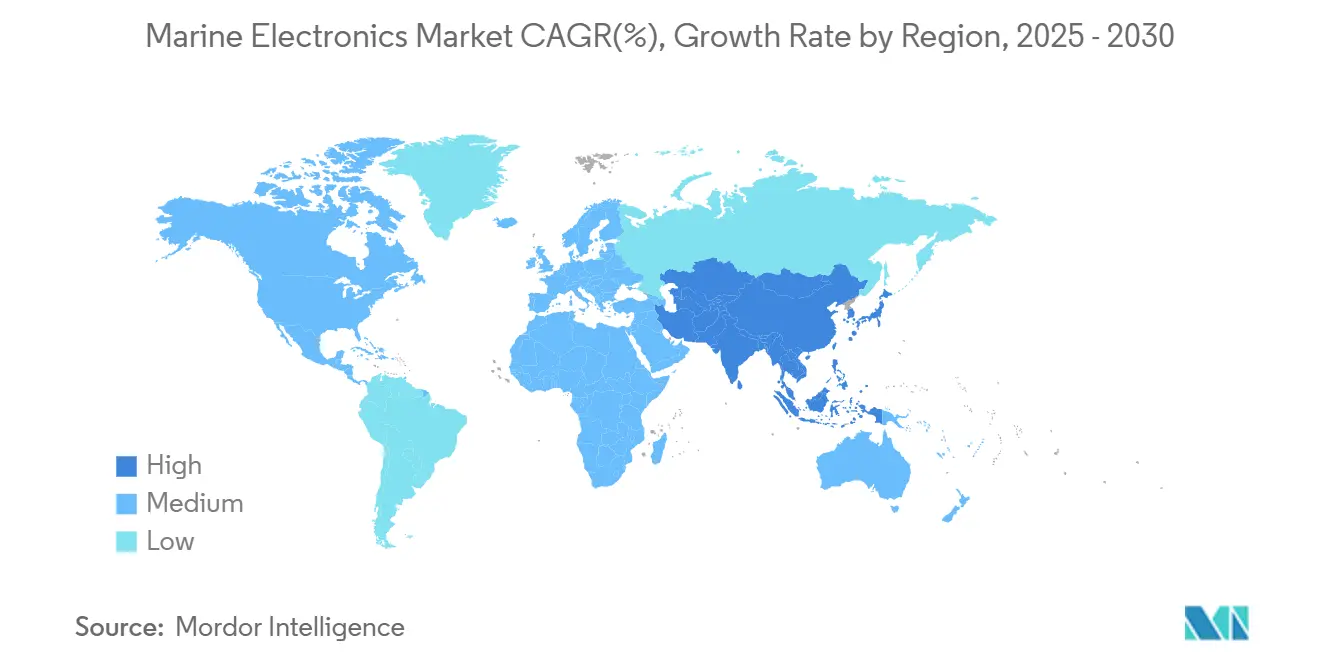

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

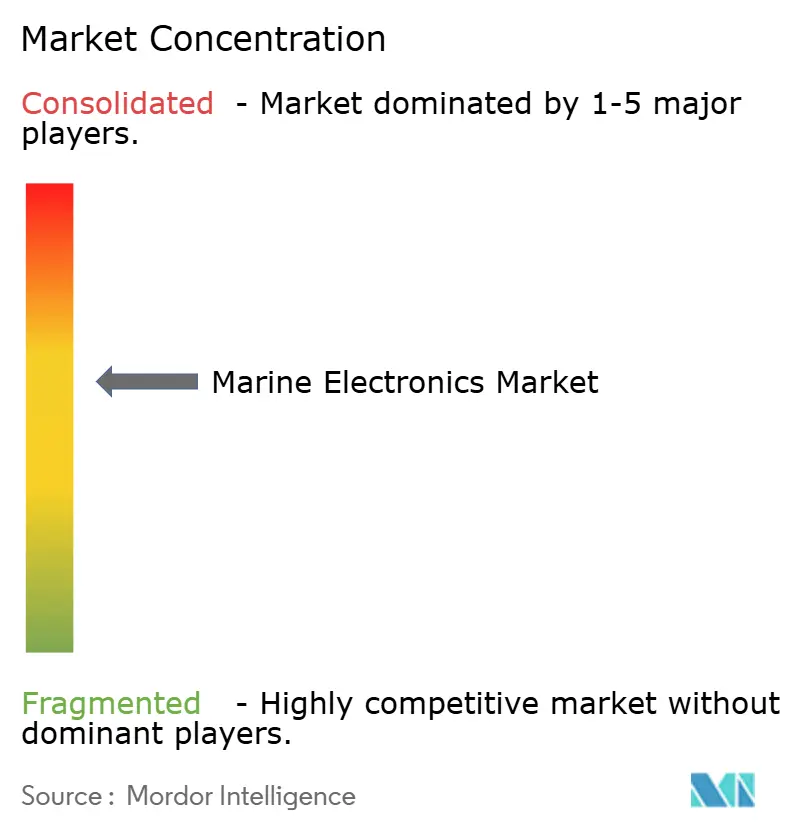

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Marine Electronics Market Analysis by Mordor Intelligence

The marine electronics market size stands at USD 6.62 billion in 2025 and is forecast to reach USD 8.91 billion by 2030, advancing at a 6.14% CAGR. Strong replacement demand triggered by new International Maritime Organization (IMO) and classification‐society rules, the insurance sector’s pivot toward AI-verified situational awareness, and premiumization in recreational boating converge to create sustained momentum for the marine electronics market. Vessel operators view integrated bridge, satellite broadband, and predictive-maintenance packages as direct levers for cutting fuel costs, limiting crew headcount, and controlling insurance premiums. Leading suppliers reply with modular, software-defined platforms that slash total installed cost and shorten certification cycles. Heightened geopolitical risk and polar‐route traffic further cement always-on connectivity and cyber-secure navigation as core buying criteria, widening the addressable customer base far beyond traditional blue-water shipping.

Key Report Takeaways

- By component, hardware retained 53.52% of the marine electronics market share in 2024, while services are set to expand at an 8.21% CAGR to 2030.

- By product type, navigation systems led the marine electronics market, with 37.21% of the size in 2024; automation systems show the highest projected CAGR, at 9.23% through 2030.

- By vessel type, merchant vessels held 47.29% of the marine electronics market share in 2024, whereas recreational boats and yachts are forecast to grow at an 8.78% CAGR to 2030.

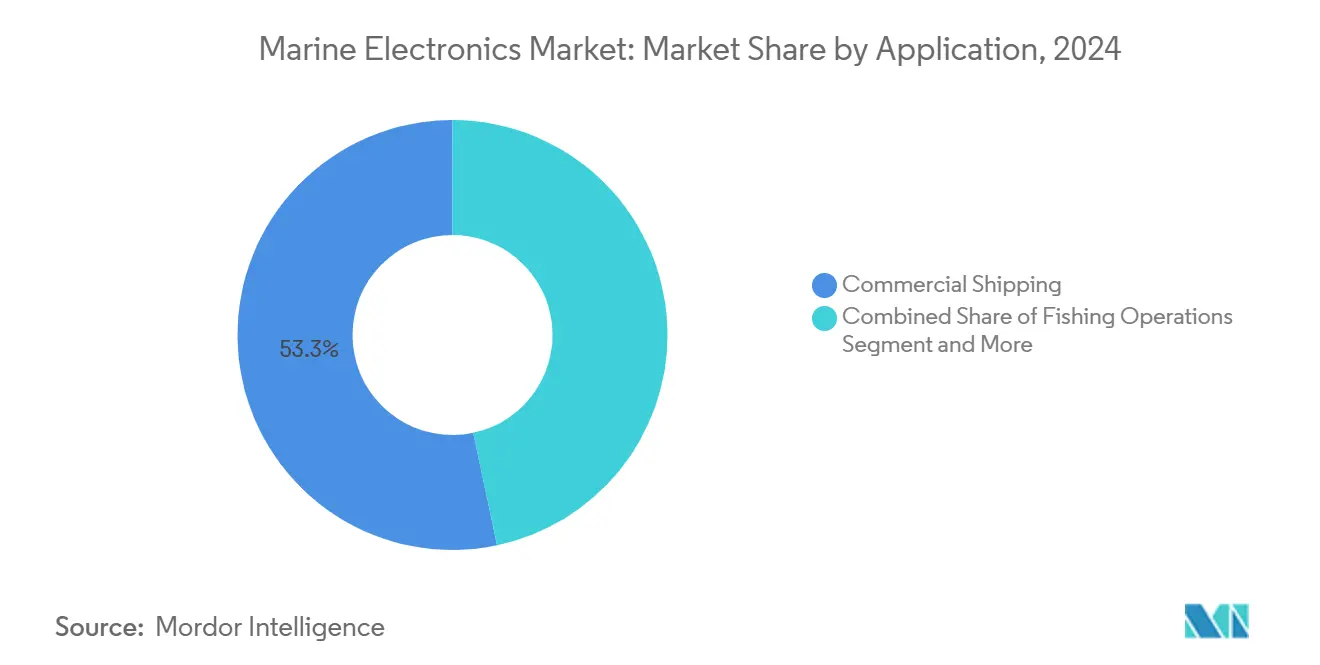

- By application, commercial shipping commanded a 53.31% share of the marine electronics market in 2024, and leisure and recreation are advancing at a 9.27% CAGR through 2030.

- By geography, Asia-Pacific captured 41.62% of the marine electronics market share in 2024 and is moving ahead at an 8.35% CAGR toward 2030.

Global Marine Electronics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Push for Integrated Navigation and Comms Safety | +1.8% | Global, EU and IMO spearheading | Medium term (2-4 years) |

| Automation and Bridge Systems Boost Efficiency | +1.2% | Asia-Pacific nucleus; Europe and North America next | Long term (≥ 4 years) |

| Recreational Boating Fuels Premium Demand | +0.9% | North America and EU; luxury Asia-Pacific niches | Short term (≤ 2 years) |

| Always-On Satellite Connectivity Needs Rising | +0.7% | Global, polar routes emphasized | Medium term (2-4 years) |

| AI-Driven Situational Awareness Mandates (Insurers) | +0.6% | Global, high-value vessels first | Medium term (2-4 years) |

| Small Craft Electrification Lifts Sensor Adoption | +0.4% | Europe and North America leaders | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Push for Integrated Navigation and Communication Safety Systems

SOLAS Chapter IV amendments effective 2024 obligate enhanced VHF and unified distress functions, triggering a worldwide retrofit upcycle that the marine electronics market quickly converted into orders[1]“SOLAS Consolidated Edition 2024,”, International Maritime Organization, imo.org. Cyber-secure architecture built on IACS UR E26/E27 further widens the scope, forcing owners to replace legacy radar and ECDIS units that cannot meet encryption and patch-management criteria. Europe’s extension of its Emissions Trading System to offshore vessels from January 2025 layers in continuous monitoring equipment that must feed verified CO₂ reporting portals[2]“FuelEU Maritime Regulation,”, European Commission, europa.eu. Because insurers refuse to underwrite non-compliant tonnage, procurement cycles compress, and even small tugs or pilot boat operators join the buying wave.

Rising Adoption of Automation and Integrated Bridge Systems for Fuel and Crew Efficiency

MAN Energy Solutions has shown that by unifying advanced technologies—like real-time route optimization, automatic trim control, and predictive engine tuning—into a single human-machine interface, fuel efficiency can be enhanced [3]“ECOPAC Fuel Optimization White Paper,”, MAN Energy Solutions, man-es.com. Asia-Pacific shipowners face acute deck-officer shortages; adopting certified bridge-automation suites helps them qualify for reduced manning notation and lower payroll outlays.

AI-Driven Situational-Awareness Mandates by Insurers From 2026

A Lloyd’s syndicate has introduced a new underwriting clause that is reshaping insurance standards for oceangoing vessels. This clause mandates that ships must have advanced collision-avoidance systems to qualify for the most favorable hull and machinery insurance rates. Specifically, vessels above a certain tonnage are required to be outfitted with AI-powered modules, which combine optical radar with real-time decision support, by the end of the compliance period. Early pilot deployments of SEA.AI technology have yielded promising results, notably in reducing near-miss incidents, which in turn has granted immediate premium benefits to participating operators. This shift underscores an increasing focus on safety, automation, and risk mitigation within maritime operations.

Electrification of Small Craft Accelerating Demand for Low-Power Sensor Networks

European inland-waterway operators shift to electric propulsion to meet emissions ceilings, yet battery endurance hinges on ultra-efficient sensors that draw <50 mW. Suppliers now roll out CAN-open nodes powered by wave energy harvesters, trimming hotel-load drain while providing 24/7 bilge, temperature, and structural-health data feeds. The marine electronics market, therefore, expands into energy-management microgrids—a revenue pool largely absent five years ago.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex for Next-Gen Multi-Function Systems | -1.1% | Global, smaller operators hit hardest | Short term (≤ 2 years) |

| Semiconductor Supply Chain Disruptions | -0.8% | Global, Asia-Pacific manufacturing hub | Medium term (2-4 years) |

| IoT Ship Systems Face Cybersecurity Bottlenecks | -0.6% | EU and North America spearheading | Medium term (2-4 years) |

| RF Spectrum Congestion Hits Radar & Comms | -0.4% | Major global ports, Asia-Pacific acute | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Costs for Next-Gen Multi-Function Systems

Many single-ship owners postpone retrofitting integrated bridge systems on their Panamax bulkers, viewing it as a significant investment, unless classification deadlines press them. The financial commitment doesn't end with the initial upgrade; ongoing expenses like software subscriptions, chart updates, and AI analytics further strain budgets. Even in areas with promising freight earnings, these mounting costs deter owners from adopting upgrades across their entire fleet, underscoring the delicate balance between modernizing operations and managing budgets in the shipping sector.

Cyber-Security Certification Bottlenecks for IoT Ship Systems

Under the IACS UR E26/E27 regulations, every device linked to a vessel must undergo penetration testing and provide a detailed software bill of materials. Yet, accredited testing labs operate at limited capacity, leading to a substantial backlog of products waiting for certification.

This delay is especially burdensome for smaller vendors, who typically don't have the financial means to undergo testing multiple times. Consequently, this has reduced product diversity and increased costs for class-approved equipment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Outpaces Hardware Dominance

Hardware contributed a 53.52% marine electronics market share in 2024 due to mandatory radar, ECDIS, and AIS installations. Most equipment has a 7-to-10-year replacement cycle, ensuring baseline demand stability even during freight downturns. Vessel digitization nonetheless elevates services revenue, projected to rise at an 8.21% CAGR. Predictive-maintenance dashboards, digital twins, and cybersecurity patch management move spending toward cloud-hosted platforms that charge monthly fees, shifting revenue from bookings to recurring.

Shipowners increasingly bundle sensors with multi-year service contracts that guarantee software upgrades and 24/7 remote diagnostics. This “hardware-plus-X-as-a-service” bundle lowers lifecycle cost and locks in supplier relationships. Consequently, service margins surpass hardware margins by 5-8 percentage points, enticing hardware incumbents to buy analytics startups—mirroring DNV’s 2024 acquisition of CyberOwl to sell threat-intelligence subscriptions alongside class surveys.

By Product Type: Automation Systems Accelerate Past Navigation Leadership

Due to SOLAS carriage mandates, navigation systems still comprise 37.21% of the marine electronics market, and demand will remain stable through replacement. Yet automation units—from smart autopilots to dynamic-positioning controllers—lead growth at a 9.23% CAGR as crew shortages and decarbonization drive enthusiasm for machine control. Automation packages increasingly integrate propulsion, hotel load, and route planning on one processor, yielding cross-selling opportunities into older fleets.

Communication suites benefit from rising data-exchange mandates that embed GMDSS, VDR replay, and high-throughput satellite in a single rack, while premium audio/video options ride the recreational wave. Overall, the marine electronics market progresses toward multifunction consoles where software unlocks new capabilities, compressing physical footprint and simplifying vessel refits.

By Vessel Type: Recreational Segment Drives Premium Technology Adoption

Merchant vessels delivered 47.29% of the share in 2024, absorbing compulsory electronic charts, long-range tracking, and voyage data recorders that keep fleets insurable. However, the recreational cohort propels incremental top-line growth by 8.78% adopting commercial-grade sonar, augmented-reality head-up displays, and wireless docking. Yacht builders now order factory-prewired NMEA 2000 backbones to accelerate MFD drop-in, cutting yard time.

The marine electronics market capitalizes on lifestyle shifts enabling remote work aboard boats and two-to-three-week cruising itineraries. These use cases need cloud route-sync and entertainment streaming, feeding demand for satellite and 5G systems once limited to superyachts. Manufacturers gain brand cachet in recreation, then leverage it when pitching bridge retrofits to small coastal traders run by former yacht captains.

By Application: Leisure Growth Outpaces Commercial Shipping Foundation

Commercial shipping retains a 53.31% share of the marine electronics market, and its compliance timetable virtually guarantees steady retrofits even in cyclical earnings troughs. Fleet-wide digitalization strategies focus on fuel analytics and condition-based maintenance, making connected sensors a table stakes.

Leisure and recreation stretch at a 9.27% CAGR, powered by charter operators standardizing AI collision-avoidance and 360-degree camera docking aids to reassure novice helms. The line between commercial and leisure solutions blurs as families expect yacht dashboards to mirror automotive UX, prompting suppliers to refine touchscreen ergonomics that later migrate to workboat product lines.

By Technology: IoT Systems Lead Digital Transformation

GPS and radar maintain a 43.21% market share but cede the growth mantle to IoT and smart-ship platforms, clocking a 9.35% CAGR. Bluetooth-low-energy temperature tags, vibration MEMS, and edge AI chips populate engine rooms, creating datasets that feed centralized analytics. The marine electronics market generates new revenue from selling sensor nodes at cost and monetizing data portals via subscription.

Fish-finder sonar advances with wider chirp bandwidth and real-time 3-D displays, lifting catch yield in artisanal fleets. Marine autopilots integrate machine learning to compensate for load conditions and wave dynamics, halving route deviation. Satellite connectivity remains an accelerant across all tech categories, furnishing the uplink bandwidth necessary for big-data models and over-the-air firmware updates.

Geography Analysis

Asia-Pacific held 41.62% marine electronics market share in 2024 and is expected to expand at an 8.35% CAGR into 2030. China’s shipyards delivered 5,804 export vessels in 2024—a 25.1% jump—embedding local radar, ECDIS, and AI cameras into newbuild specs. South Korea and Japan add R&D muscle, pioneering dual-fuel automation centers and uncrewed surface vessel (USV) testbeds that raise regional content value. ASEAN yards in Vietnam and the Philippines increasingly source low-cost solid-state radars, widening the downstream aftermarket for spares and software.

North America demonstrates a high willingness to pay for premium recreational electronics and cyber-secure bridge retrofits. The United States Coast Guard cyber rule, effective July 2025, pushes owners to replace unencrypted network switches, sustaining a backlog for class-certified offerings. Great Lakes operators leverage Starlink broadband to coordinate just-in-time dockage, cutting wait fees and validating ROI for high-throughput antennas.

Europe uses environmental policy as its growth lever. FuelEU Maritime and the expanded EU ETS mandate continuous emissions data collection, driving the brisk uptake of sensor gateways and carbon-calculator dashboards. Norway leads MASS trials, issuing provisional regulations that let autonomous ferries operate in commercial lanes and promptly ordering advanced lidar-fusion packages.

The Middle East bolsters demand through mega-port expansions at Jebel Ali and Dammam. Africa’s opportunity centers on offshore support vessels installing hybrid power monitoring to satisfy international oil-major tenders.

Competitive Landscape

Market structure is moderately concentrated: more than 200 niche suppliers compete in sensors, displays, and connectivity add-ons. Garmin broadened its footprint by integrating Lumishore RGBW lighting into its OneHelm ecosystem, delivering a cohesive “plug-and-play” stack that cuts installer hours by 30%. Furuno partnered with Panasonic to embed cyber-secure processors inside its NavNet platform, meeting UR E26 requirements ahead of peers. Raymarine pivoted to an ecosystem model, signing OEM deals with WATCHIT, Maretron, and CMC Marine to reduce per-boat integration cost and lock in accessories revenue.

Emergent players such as SEA.AI and Avikus specialize in neural-network collision-avoidance, winning pilot contracts with LNG carrier owners seeking insurance discounts. Kongsberg Maritime leverages its defense pedigree to supply ultra-reliable maritime broadband radio, supporting autonomous survey fleets without satellite links. Patent filings center on sensor-fusion, edge computing, and cyber-secure remote patching—capabilities expected to dictate long-term share capture as the marine electronics market gravitates toward autonomy.

Marine Electronics Industry Leaders

Garmin Ltd.

Furuno Electric Co., Ltd.

Navico Group

Raymarine

Kongsberg Maritime

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Raymarine formalized WATCHIT, Maretron, and CMC Marine integrations, advancing open-ecosystem strategy.

- May 2024: Raymarine teamed with ePropulsion to merge electric-drive telemetry into helm displays.

Global Marine Electronics Market Report Scope

| Hardware |

| Software |

| Services |

| Navigation Systems |

| Communication Equipment |

| Automation Systems |

| Audio & Video Equipment |

| Merchant Vessels |

| Fishing Vessels |

| Recreational Boats / Yachts |

| Military Vessels |

| Commercial Shipping |

| Fishing Operations |

| Leisure & Recreation |

| Defense & Surveillance |

| GPS and Radar Systems |

| Fish Finders and Sonar |

| Marine Autopilots |

| Satellite Connectivity |

| IoT & Smart Ship Systems |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Product Type | Navigation Systems | |

| Communication Equipment | ||

| Automation Systems | ||

| Audio & Video Equipment | ||

| By Vessel Type | Merchant Vessels | |

| Fishing Vessels | ||

| Recreational Boats / Yachts | ||

| Military Vessels | ||

| By Application | Commercial Shipping | |

| Fishing Operations | ||

| Leisure & Recreation | ||

| Defense & Surveillance | ||

| By Technology | GPS and Radar Systems | |

| Fish Finders and Sonar | ||

| Marine Autopilots | ||

| Satellite Connectivity | ||

| IoT & Smart Ship Systems | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the marine electronics market?

The marine electronics market size is USD 6.62 billion in 2025 and is projected to grow to USD 8.91 billion by 2030.

Which region leads demand?

Asia-Pacific holds 41.62% marine electronics market share and is also the fastest-growing region at an 8.35% CAGR.

How are regulatory changes influencing demand?

New IMO safety, cybersecurity, and emissions rules compel owners to replace legacy hardware, accelerating market growth through mandatory compliance cycles.

What role does satellite connectivity play?

Affordable LEO services transform connectivity from optional to essential, enabling real-time reporting and supporting new digital-service revenue streams.

Which segment is expanding most quickly?

Automation systems register the highest growth at a 9.23% CAGR, driven by crew-reduction and fuel-efficiency goals.

Page last updated on: