Marine Propulsion Engine Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

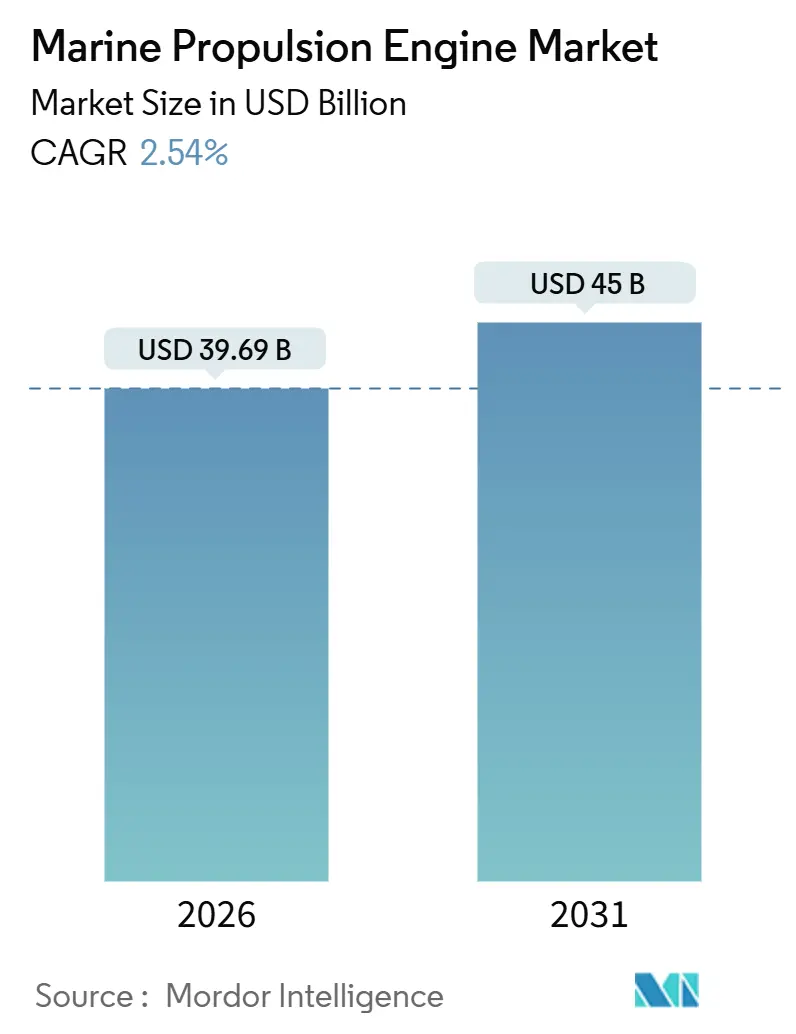

| Market Size (2026) | USD 39.69 Billion |

| Market Size (2031) | USD 45 Billion |

| Growth Rate (2026 - 2031) | 2.54% CAGR |

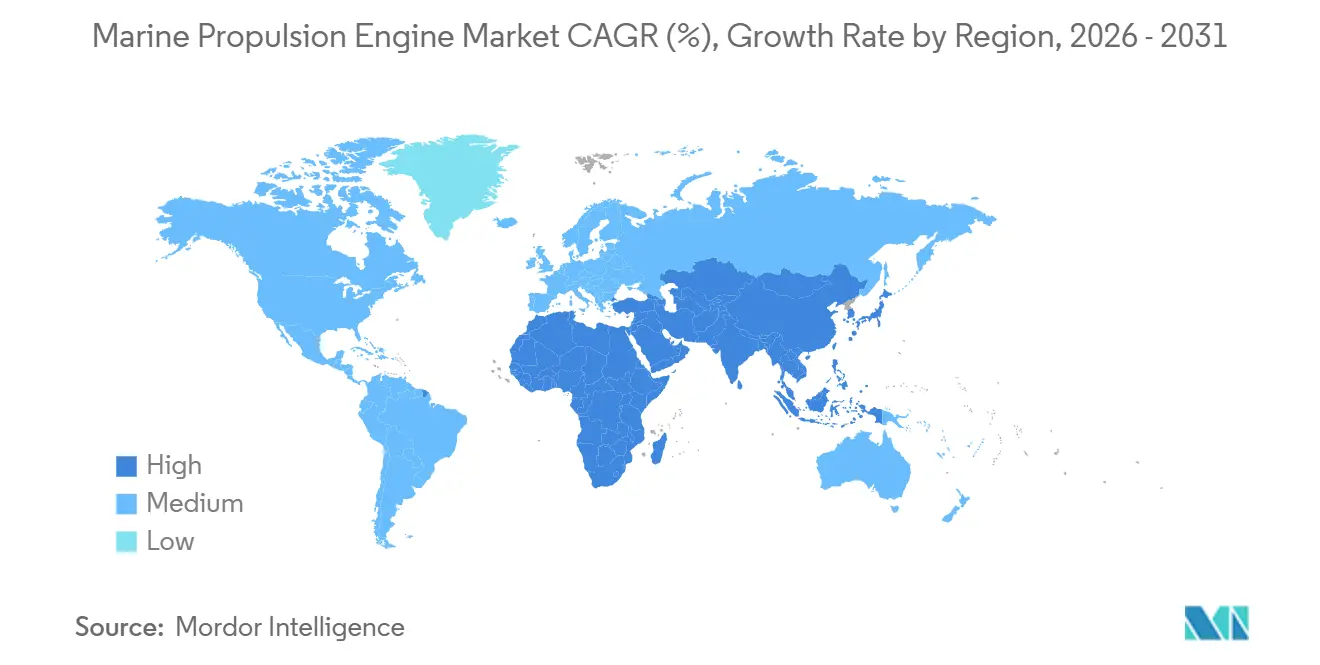

| Fastest Growing Market | Middle East |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Marine Propulsion Engine Market Analysis by Mordor Intelligence

The marine propulsion engine market size stood at USD 39.69 billion in 2026 and is projected to reach USD 45 billion by 2031, registering a 2.54% CAGR over the forecast period (2026-2031). The measured expansion reflects operators’ preference for repowering existing hulls rather than building new tonnage, as IMO Tier III nitrogen-oxide limits and the Energy Efficiency Existing Ship Index drive capital toward dual-fuel and hybrid platforms. Dual-fuel orders that toggle between LNG, methanol, and traditional fuel oil now dominate backlogs, while hybrid-electric auxiliaries gain traction in emission-control areas. Asia-Pacific continues to underpin demand thanks to Chinese and South Korean yards, but sovereign investment in the Middle East is the fastest-growing regional catalyst. Heightened bunker-price volatility and limited alternative-fuel infrastructure are expected to temper the near-term pace; however, digital-twin maintenance platforms and fuel-agnostic engine architectures are anticipated to sustain long-term efficiency gains across the marine propulsion engine market.

Key Report Takeaways

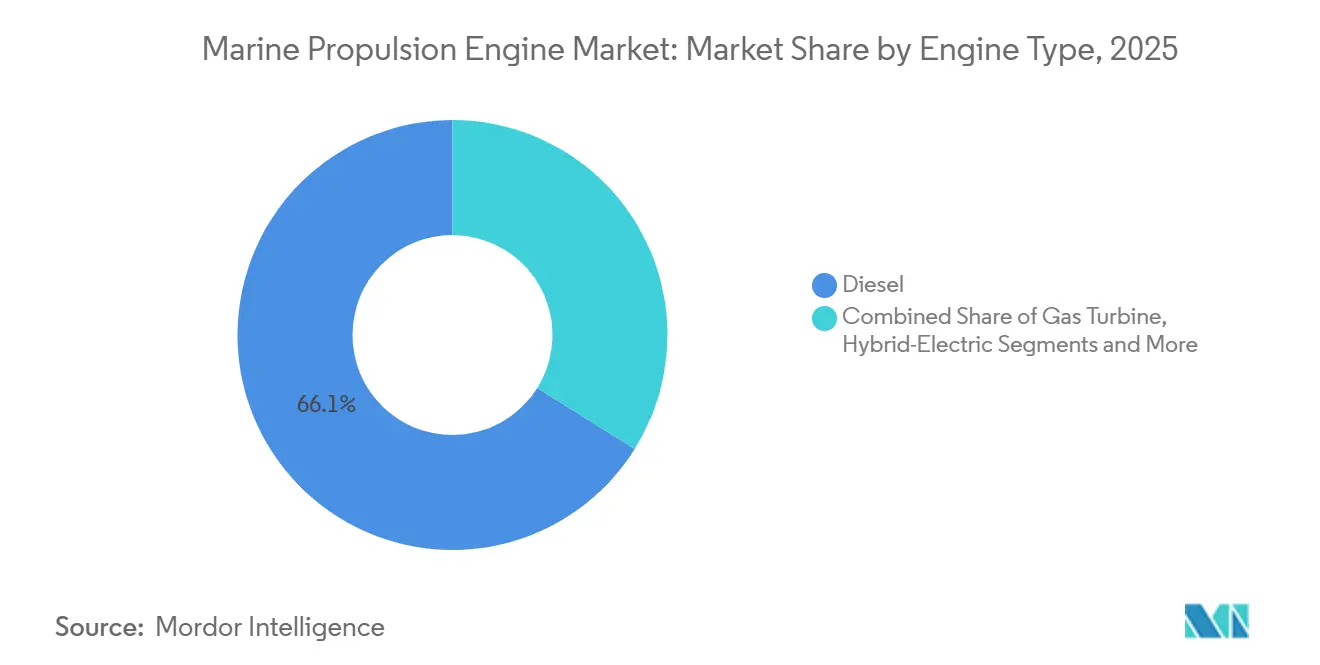

- By engine type, diesel commanded 66.12% of the marine propulsion engine market share in 2025, while fuel-cell systems are projected to grow at a 2.76% CAGR to 2031.

- By application, commercial cargo held 57.37% of the marine propulsion engine market size in 2025; passenger shipping is set to expand at a 2.41% CAGR through 2031.

- By ship type, bulk carriers led with 31.28% revenue share in 2025; offshore support vessels are poised for a 3.12% CAGR during the forecast window.

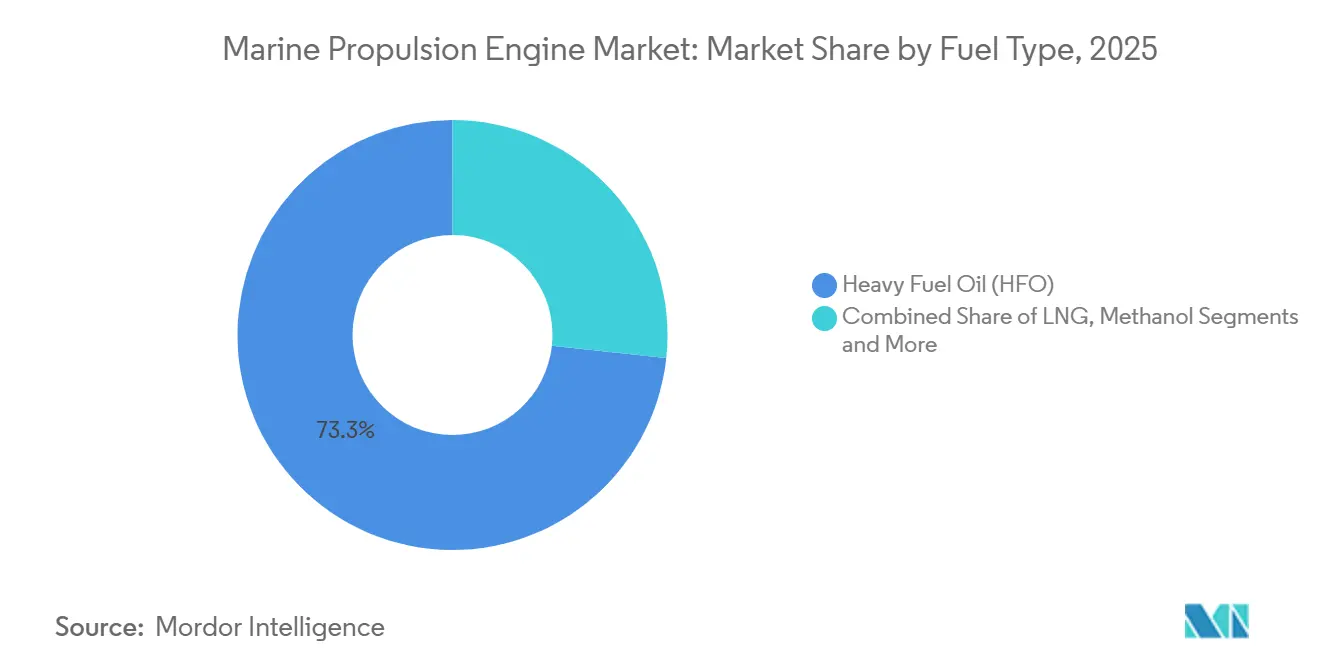

- By fuel type, HFO accounted for a 73.25% share of the marine propulsion engine market size in 2025, whereas methanol is forecast to advance at a 2.88% CAGR to 2031.

- By power range, engines with a capacity of 10,001-20,000 kW captured 37.11% of the marine propulsion engine market size in 2025; units above 20,000 kW are projected to post the fastest growth rate of 3.24% through 2031.

- By geography, the Asia-Pacific region accounted for 43.36% of the marine propulsion engine market share in 2025; the Middle East and Africa are projected to grow at a 3.37% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Marine Propulsion Engine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Engine Retrofits Accelerated by IMO Tier III and EEXI | +0.6% | Global, strongest in EU and North America | Short term (≤ 2 years) |

| Asia-Pacific Surge in Container and LNG Orders | +0.5% | China, South Korea, Japan, Southeast Asia | Medium term (2–4 years) |

| Rapid Uptake of LNG & Methanol Dual-Fuel | +0.4% | Europe, North America, Asia-Pacific | Medium term (2–4 years) |

| Zero-Emission Auxiliary Propulsion in Port Zones | +0.3% | Rotterdam, Antwerp, Hamburg, California, Singapore | Short term (≤ 2 years) |

| Digital-Twin Predictive Maintenance Cuts Ownership Costs | +0.2% | Global, early lead in North America and Northern Europe | Long term (≥ 4 years) |

| Defense CODAD and CODAG Procurement Boom | +0.2% | North America, Europe, India, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

IMO Tier III and EEXI Compliance Push Retrofits

Owners of vessels built before a specific period are required to install SCR or EGR systems to comply with nitrogen-oxide limits in emission-control zones. Many owners are also implementing dual-fuel conversions alongside these upgrades to achieve operational flexibility [1] “Energy Efficiency Existing Ship Index Guidelines,” International Maritime Organization, imo.org. The Energy Efficiency Existing Ship Index assigns letter grades to ship hulls, and vessels with lower grades have faced charter penalties in European markets. Retrofit orders for SCR units have increased at MAN Energy Solutions, reflecting carriers' focus on upgrading existing assets rather than commissioning new builds during freight rate fluctuations. FuelEU Maritime will enforce stricter limits on greenhouse-gas intensity, driving European-bound tonnage toward engines capable of transitioning to fuels like methanol or ammonia [2]“FuelEU Maritime Regulation Text,” European Commission, europa.eu. Current classification regulations integrate emissions monitoring into engine control software, providing financiers and insurers with compliance data and contributing to the trend of retrofitting.

Asia-Pacific Container and LNG New-Build Boom

Chinese and South Korean shipyards increased container capacity deliveries, driven by orders for large vessels equipped with advanced dual-fuel two-stroke engines. LNG carrier orderbooks reached new heights, supported by charter commitments tied to Qatar’s North Field expansion and export terminals in the United States. Hanwha Ocean invested significantly to enhance its Geoje engine-integration line, focusing on methanol-ready modules designed for future deliveries to Maersk. Japanese shipyards shifted their focus to ammonia-fueled coastal tankers, successfully delivering the prototype to Nippon Yusen. While the concentration of engine production in Northeast Asia has reduced lead times, it has also heightened geopolitical risks due to tighter export restrictions on advanced control electronics from the United States.

LNG/Methanol Dual-Fuel Uptake

Maersk has added methanol-capable container ships to its orderbook, each equipped with MAN B&W engines that can operate on bio-methanol, e-methanol, and fuel oil. CMA CGM has introduced LNG-powered ships, achieving significant reductions in CO₂ emissions compared to heavy-fuel baselines. Dual-fuel contracts now account for a notable portion of Wärtsilä’s marine backlog, reflecting shipowners’ increasing preference for fuel flexibility. Rotterdam has established Europe’s first large-scale green methanol bunkering hub, while Singapore has initiated a pilot program to address supply chain constraints. Although capital costs are higher, lifecycle fuel savings become apparent when the prices of methanol or LNG are more favorable compared to marine gas oil.

Port-Entry Zero-Emission Zones

EU regulations require core ports to offer shore power, while California imposes fines on ships running auxiliary diesels at the pier. In response, cruise lines are adopting battery packs capable of powering hotel loads for extended periods, thereby reducing emissions at the port. ABB’s Onboard DC grid demonstrates how batteries and generators work together to enable silent maneuvering and recharging during journeys. Singapore’s Green Port Programme incentivizes ships with tariff rebates for achieving zero auxiliary emissions, encouraging hybrid retrofits in ferry fleets across the Asia-Pacific. These regulatory measures are driving hybrid-electric auxiliaries into prominence within the marine propulsion engine market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fuel-Price Volatility Complicates Engine Choice | -0.3% | Global, most acute where fuel contracts lack hedging | Short term (≤ 2 years) |

| High CAPEX for SCR, EGR & After-Treatment | -0.2% | Global, especially fleets built before 2010 | Medium term (2–4 years) |

| Limited Green-Methanol & Ammonia Bunkering | -0.2% | Infrastructure concentrated in Northern Europe | Medium term (2–4 years) |

| Rare-Earth Magnet Supply Risk for Motors | -0.1% | Global, high reliance on China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fuel-Price Volatility Complicates Engine Choice

Marine gas oil prices experienced significant fluctuations, creating challenges for dual-fuel payback models. LNG bunker costs in key markets negated the anticipated savings that had driven many LNG orders. Methanol prices increased substantially in certain regions, driven by tight supply and rising demand from the chemical and shipping industries [3]“Methanol Supply Still Tight,” ICIS, icis.com. A portion of dual-fuel vessels shifted to operating exclusively on fuel oil due to unfavorable LNG pricing. Limited availability of hedging tools for methanol or ammonia left operators exposed to price volatility during the period between contract signing and delivery.

High Capex for SCR/EGR After-Treatment

Installing an SCR on a diesel engine can be a significant expense, often surpassing the residual value of older ships. Adding an EGR increases the cost of a new engine and requires additional cooling capacity. Catalyst cartridges, which need periodic replacement, further inflate operational expenditure forecasts. These rising costs make it difficult for smaller carriers to fund retrofits, leading some to exit the market or merge, thereby reshaping regional fleets. The International Chamber of Shipping estimates the global retrofit expenses to be substantial, excluding losses incurred during dry-dock idle periods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Engine Type: Diesel Reliance Meets Fuel-Cell Momentum

Diesel engines accounted for 66.12% of the marine propulsion engine market share in 2025, primarily due to their familiarity with service and a widespread network of parts. Leadership is eroding at the margins as dual-fuel engines take orders that were once committed to straight diesel engines. Gas turbines once reserved for naval craft are re-entering commercial designs in hybrid pairings, where a turbine supplements cruise diesels for occasional high-speed needs. Hybrid-electric architectures integrating batteries with medium-speed gensets gained ground in European ferries that must cut port-side emissions.

Fuel-cell packages, though embryonic, posted the fastest climb at a 2.76% CAGR through 2031 on the back of European ferry pilots and Ballard’s 50,000 operating hours milestone. Regulatory clarity is improving, as DNV and Lloyd’s Register have published guidelines for fuel cells and ammonia. Container fleets with predictable routes tend to convert to dual-fuel more quickly than bulk carriers that operate on tramp schedules. Nuclear propulsion remains strictly naval, sustaining niche demand that is insulated from commercial cycles. Overall, fuel-agnostic modular engines are the future revenue sweet spot for the marine propulsion engine market.

By Application: Commercial Cargo Dominance and Passenger Upside

Commercial cargo accounted for 57.37% of the marine propulsion engine market share in 2025, reflecting the volume of commodities and competitive fuel-cost pressures. Cargo operators prioritize thermal efficiency and bunker optionality, resulting in a higher uptake of dual-fuel two-stroke engines on container and LNG carriers. Passenger vessels, which are growing at a rate of 2.41%, are also chasing low-emission credentials to attract environmentally conscious travelers. Cruise lines integrate batteries and shore-power interfaces that slash in-port emissions, and vibration-damped crankshafts protect guest comfort at sea. Defense and coast-guard procurement follows distinct criteria, such as redundancy and sprint speed, locking in multi-year engine contracts once a design is selected.

Power-takeoff arrangements that drive reefer compressors on cargo ships reduce auxiliary generator fuel consumption by 15%, providing a quick savings win. Short-sea ferries in Norway operate on fully battery-electric propulsion, demonstrating viability for crossings under one hour. Cargo operators adopt digital-twin scheduling to further reduce fuel costs, whereas passenger lines market hybrid capability as a brand differentiator. Naval platforms embed CODAD and CODAG combinations to deliver both efficiency and combat survivability, bolstering demand stability within the marine propulsion engine industry.

By Ship Type: Bulk Carrier Scale vs Offshore Support Agility

Bulk carriers supplied 31.28% of the marine propulsion engine market demand in 2025. Long replacement cycles and marginal freight rates slow technology refresh, so many bulk carriers will run Tier II diesels until forced to retrofit. Container ships adopt dual-fuel two-strokes at a faster clip to satisfy cargo owners’ emission mandates on scheduled liner routes. Tankers, with lower design speeds, continue to favor robust low-speed diesels that function efficiently at 80 RPM.

Offshore support vessels posted the top CAGR of 3.12% through 2031, as deepwater drilling campaigns require dynamic positioning drives with variable-speed diesel-electric systems. Naval vessels maintain CODAG and CODLAG mixes to balance patrol endurance with high-speed sprints. Passenger and cruise segments, although small in terms of units, deliver outsized visibility because shore-side regulators spotlight them for urban air-quality compliance. Bulk carriers will lag in hybrid adoption until global iron-ore and coal routes deploy methanol or ammonia bunkers; however, offshore units will continue to adopt next-generation engines as oil majors finance low-carbon retrofits into their supply contracts.

By Fuel Type: HFO Incumbency Meets Methanol Momentum

Heavy fuel oil remained dominant, with 73.25% of the marine propulsion engine market share in 2025, due to its cost advantages and the massive installed fleet. Scrubbers or 0.5% sulfur blends enable many operators to stay within the IMO 2020 sulfur caps without switching to a different fuel type. LNG supplied 8% of the fleet's energy, concentrated in large container and dedicated LNG carriers, where cryogenic bunkers are readily available. Methanol rose the fastest at a 2.88% CAGR through 2031, propelled by Maersk’s 25-ship orderbook and new bunkering hubs in Rotterdam and Copenhagen.

Ammonia and hydrogen remain at pilot scale yet anchor the industry’s 2050 decarbonization roadmap, aided by MAN’s ammonia-ready Type Approval. Conversion costs are substantial: LNG retrofits can exceed USD 10 million per mid-size container vessel, while methanol’s corrosive properties necessitate the use of stainless piping. Fuel-density penalties reduce cargo capacity, pushing operators to secure long-term low-carbon fuel supply contracts before committing. Agencies like the International Energy Agency forecast ammonia could cover 30% of shipping energy by 2050, contingent on scaling green-ammonia production from today’s sub-million-tonne base.

By Power Range: Mid-Range Stability, Ultra-High Growth

The 10,001–20,000 kW bracket accounted for 37.11% of the marine propulsion engine market size in 2025, primarily serving core to mid-sized container ships and tankers that rely on four-stroke diesel engines. Engines above 20,000 kW are expected to expand at a 3.24% CAGR through 2031, driven by the need for ultra-large container ships to operate at 22 knots, requiring 60,000-80,000 kW of power. Hybrid-electric configurations are gaining traction in the 1,000–5,000 kW class for offshore supply and patrol vessels, as batteries can effectively handle low-speed loads during port operations.

Small craft under 1,000 kW remain fragmented, with service networks provided by Yanmar, Cummins, and Caterpillar dealers. Ultra-high-power two-stroke diesels operate at cylinder pressures exceeding 200 bar, necessitating the use of exotic coatings that increase overhaul costs but deliver unmatched fuel economy. Dual-fuel penetration is most pronounced in the top power tier, where compliance benefits justify the 20% capital premium. Battery packs complement diesel generators in the 1,000–5,000 kW range, and ABB’s recent contracts demonstrate how integrated grids are expanding hybrid adoption beyond ferries.

Geography Analysis

The Asia-Pacific region led the marine propulsion engine market with a 43.36% share in 2025. Chinese yards supplied nearly half of global deadweight deliveries, and South Korean builders dominated the high-value container and LNG niches. Japan’s pivot toward ammonia-ready propulsion underscores the region’s push for zero-carbon leadership, while India’s defense shipbuilding programs bolster CODAG demand for combined diesel and gas-turbine engines. Southeast Asian yards fill offshore support vessel backlogs as exploration intensifies in the South China Sea. Vertical integration enables Hyundai Heavy Industries Engine & Machinery to supply its own shipbuilding lines, thereby compressing delivery times and securing margins.

The Middle East, forecasted to grow at a 3.37% CAGR through 2031, benefits from Saudi and Emirati sovereign capital targeting LNG carriers that will transport volumes from new liquefaction trains. Saudi Aramco’s long-term charters could require 20–30 hulls with dual-fuel two-stroke engines above 25,000 kW. Abu Dhabi invests in hybrid-electric harbor craft to cut port emissions. Turkish yards capture offshore support orders by offering cost quotes 20% lower than those of European competitors, although they still source Tier III engines from Western OEMs. Regional demand remains closely tied to Brent crude trajectories, as a slide toward USD 60 may defer deepwater commitments.

Europe held a significant share in 2025, driven by Norway’s demand for offshore wind support vessels and Germany’s naval frigate programs, which specify Tier III diesels. FuelEU Maritime tightens greenhouse-gas limits annually, pushing European owners toward dual-fuel or hybrid power, or face fines of up to one million euros per hull by 2031.

North America’s engine demand stems from the United States Navy’s new frigates and Alaskan fishing fleets, where Cummins and Caterpillar engines dominate remote-port service networks. South America and Africa remain smaller but strategic markets. Brazil’s FPSO expansions require medium-speed gensets, and Nigerian coastal shipping operates aging engines that are ripe for Tier III retrofits when financing becomes available.

Regulatory Landscape

Regulation is anchored by the International Maritime Organization (IMO) through MARPOL Annex VI and its NOx Technical Code, which drive Tier III-compliant propulsion in Emission Control Areas (ECAs) and reinforce demand for SCR/EGR and dual-fuel-ready engine platforms. Recent IMO MARPOL Annex VI amendments entered into force on 1 August 2025 (including provisions tied to low-flashpoint fuels and strengthened reporting in the IMO Ship Fuel Oil Consumption Database), and new ECA designations for the Canadian Arctic and the Norwegian Sea are scheduled to enter into force on 1 March 2026. This broadens the set of operating zones where compliant engine and after-treatment configurations become mandatory.

In Europe, Regulation (EU) 2023/1805 (FuelEU Maritime) applied from 1 January 2025, after monitoring-plan requirements began on 31 August 2024. It tightens greenhouse-gas intensity constraints for energy used on board. In the United States, the Environmental Protection Agency regulates marine engine emissions under 40 CFR Part 1042 (compression-ignition) and 40 CFR Part 1045 (spark-ignition), with certification submissions routed through EV-CIS ahead of commercial introduction. For certain Tier 4 marine compression-ignition engines, assigned deterioration factors remain available for use through model year 2026, which influences OEM compliance planning and configuration choices.

Competitive Landscape

Competition remains moderate, with the top suppliers controlling a significant portion of the revenue share. Wärtsilä’s modular engine block allows operators to easily attach methanol injectors without the need to swap crankcases. This flexibility has boosted dual-fuel contracts, now making up a notable part of its backlog. MAN Energy Solutions has obtained IMO Type Approval for its ammonia-ready two-stroke engines. This positions the company as an early mover, allowing clients to place orders now and convert later as bunkering becomes more prevalent. In a strategic move, Rolls-Royce has taken a minority stake in a Norwegian battery integrator, indicating a push to combine propulsion systems with energy storage solutions.

Patent filings underscore the industry's next wave of innovations: Ballard has secured multiple marine fuel-cell patents, emphasizing membrane durability in saline conditions. Meanwhile, ABB's patents focus on algorithms optimizing battery charge cycles during port dockings. Chinese firms, such as Weichai and CSSC Diesel, enjoy a cost advantage but lag in emissions-control technology by a few years. High switching costs arise from service contracts and digital-twin data lock-ins. For instance, Wärtsilä oversees engines on numerous vessels across Asia, while Rolls-Royce’s Intelligent Awareness technology monitors hundreds of hulls worldwide. Emerging opportunities lie in hybrid-electric systems for coastal fishing fleets and the budding ammonia engine supply market.

Marine Propulsion Engine Industry Leaders

MAN Energy Solutions SE (Everllence)

Rolls-Royce plc

HD Hyundai Heavy Industries Co., Ltd.

Wärtsilä Corporation

Yanmar Holdings Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term opportunities center on OEM capacity, localization, and service readiness for multi-fuel engine families and retrofit-compatible packages that address tightening emissions requirements and fuel flexibility needs. In May 2026, Wärtsilä announced an approximately EUR 90 million investment to increase technical production capacity by 30% at its Sustainable Technology Hub in Vaasa, Finland, and across its global supply chain, building on a separate 35% capacity expansion announced in February 2026, with commissioning targeted for the first quarter of 2028. The scale of these additions points to a whitespace for component suppliers and authorized channels that can support higher throughput of dual-fuel, hybrid-ready, and digitally enabled engine configurations, while maintaining compliance documentation and delivery lead times.

Alternative-fuel propulsion development also supports differentiated offerings by vessel type and duty cycle, particularly as rules and class guidance converge around non-carbon fuels. Japan Engine Corporation (J-ENG) has disclosed a schedule toward completion of its UEC50LSJA ammonia-fueled engine (September 2025) and a hydrogen-fueled UEC35LSGH program on its FY 2026 timeline, with demonstration operations outlined for FY 2027. In parallel, IMO work on mid-term GHG measures and the IMO Net-Zero Framework (including mandatory emissions limits and GHG pricing) keeps attention on engines that can transition from conventional fuels to methanol, ammonia, or hydrogen through staged upgrades, which supports demand for fuel-agnostic architectures, after-treatment integration, and controls or software packages that can document compliance under evolving reporting regimes.

Recent Industry Developments

- July 2026: Rolls-Royce announced delivery of 40 mtu 16V 4000 M33S engines to power ten new hybrid offshore vessels for Petrobras, being built by Detroit Brasil Ltda. The program links high-speed engine supply to hybrid offshore logistics, supporting operators that want lower-emission operating profiles without sacrificing mission availability. The delivery also expands Rolls-Royce's installed base in Brazil for long-tail service revenues as the vessels enter service across 2026-2028.

- June 2026: Rolls-Royce secured a framework contract with yacht builder Overmarine for the integration of yacht bridges and engines. The agreement links automation and propulsion packages under a repeatable commercial structure, supporting standardized configurations across a premium segment where owners demand performance, integration quality, and lifecycle support. It also reinforces bundling strategies that can lift share-of-wallet beyond the engine itself.

- February 2026: MAN Energy Solutions released the MAN D3872 auxiliary engine for onboard power generation and diesel-electric propulsion, adding a new 30-litre portfolio variant. The platform is positioned for IMO Tier II, IMO Tier III, and EU Stage V compliance pathways, aligning auxiliary and diesel-electric propulsion needs with emission-control requirements across vessel categories. This broadens MAN Energy Solutions' offering for fleets pursuing repowering and standardization of engine families to reduce maintenance complexity.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the revenue generated from marine propulsion engines that deliver thrust to ships and workboats, covering engines sold for newbuild vessels and full engine replacements across ocean-going, coastal, and inland fleets.

Scope exclusions: We exclude auxiliary gensets, propellers, shaftlines, gearbox-only retrofits, and shore-power equipment from the market totals.

Segmentation Overview

- By Engine Type

- Diesel

- Dual-Fuel (LNG, Methanol, Ammonia ready)

- Gas Turbine

- Hybrid-Electric

- Fuel-Cell

- Nuclear (Naval)

- By Application

- Passenger

- Commercial Cargo

- Defense / Coast Guard

- By Ship Type

- Container Ship

- Tanker

- Bulk Carrier

- Offshore Support Vessel

- Naval Ship

- Passenger / Cruise

- By Fuel Type

- Heavy Fuel Oil (HFO)

- Marine Diesel/Gas Oil

- Liquefied Natural Gas (LNG)

- Methanol

- Ammonia/Hydrogen

- By Power Range (kW)

- Up to 1,000 kW

- 1,001 kW to 5,000 kW

- 5,001 kW to 10,000 kW

- 10,001 kW to 20,000 kW

- Above 20,000 kW

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting data backbone and to keep assumptions realistic across ship types and operating regions. We mainly relied on public sources such as IMO publications on emissions rules, UN Comtrade trade statistics, UNCTAD maritime transport updates, International Energy Agency fuel and emissions indicators, and World Bank macro and trade series.

Along with these, we reviewed company annual reports and investor presentations, shipbuilding and port authority releases, and coverage in reputed maritime press so the demand narrative and timing of regulations were not overstated. Where helpful, a paid subscription for company financials and news, plus patent databases, was used to validate engine platform direction and investment signals. This list is not exhaustive, and many other sources were referred to for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on filling gaps that public data cannot answer well, such as typical replacement timing, propulsion choice shifts, and realistic price movement by power class. We spoke with a mix of engine ecosystem participants, vessel operators, repair and overhaul stakeholders, and marine engineers across APAC, EMEA, and the Americas so that regional ordering cycles and regulatory impacts could be cross-checked and then reconciled.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 21% | APAC: 47% |

| Mid tier: 48% | Functional/Unit leaders: 21% | EMEA: 31% |

| Smaller Players: 21% | Managers: 58% | Americas: 22% |

Market-Sizing & Forecasting

For sizing, we used top-down and bottom-up logic together, starting from the global vessel build and renewal activity, and then mapping it to propulsion engine demand using power needs and adoption rates by fuel and ship type. When the demand pool was constructed, it was converted to value using typical OEM net price bands, which vary by power range and engine configuration.

Inputs that shaped the model included newbuild deliveries and orderbook direction, repowering intensity in the active fleet, IMO and local emissions compliance timelines, fuel availability signals for LNG and emerging fuels, and observed engine power-class mix shifts. To keep totals grounded, selective bottom-up checks were run using sampled ASP times volume for a few major vessel categories, and also using channel checks on lead times and pricing movement where data was thin.

Forecasting was built using scenario analysis with a light multivariate regression overlay, where macro trade growth, shipbuilding cycle indicators, and regulation timing were treated as key drivers. If bottom-up detail was missing for smaller vessel groups, we bridged gaps using calibrated shares from similar ship classes and then re-tested the totals with interview feedback before locking the final series.

Data Validation & Update Cycle

Validation is done through several passes so the final number is not driven by a single data series. We reconcile outputs against independent signals such as ship deliveries and orderbook direction, trade and seaborne demand trends, and the pace of regulatory compliance, and then check for unusual jumps in pricing or volume by region.

When a variance looks too high, assumptions are reviewed again and, if needed, follow-up calls are triggered to confirm what changed in ordering behavior or engine mix. Before sign-off, the model and narrative are reviewed by another analyst for internal consistency, and a final pre-delivery refresh is completed so clients get the most current view. The report is updated annually, with interim updates added when major policy shifts, supply disruptions, or step-changes in newbuild activity materially affect the outlook.

Mordor Intelligence's Marine Propulsion Engine Market Size Compared Against Other Published Estimates

Published market sizes for marine propulsion engines often differ, even when they look like they are tracking the same ships and the same time period. The differences usually come from what is counted as an engine sale, which vessel and power ranges are included, and how replacement demand is treated versus newbuild demand.

The main gap comes from whether adjacent propulsion hardware and service revenue get mixed into the engine number, where Mordor Intelligence counts only factory-built main propulsion engines sold for newbuilds and complete replacements at OEM net prices and leaves out items such as shaftlines, propellers, and gearbox-only retrofits. Differences also show up when one estimate uses a broad average price for all engines, versus pricing that moves by power class and fuel configuration, and when currency timing and update cadence are not aligned with recent shipyard ordering and repowering activity.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 39.69 B (2026) | |

| Global Consultancy A | USD 21.48 B (2025) | Uses a narrower value pool tied to selected engine types and applications, and it may exclude parts of the high-power main engine demand while applying a more uniform pricing curve across power ranges. |

| Trade Publisher B | USD 38.70 B (2025) | Uses a different base year and may blend broader propulsion system categories and assumptions on repowering pace, which can shift totals when fleet replacement cycles are treated more aggressively or conservatively. |

The spread across the three values mostly traces back to scope choices and to how pricing and replacement cycles are translated into dollars. By keeping inclusions specific to main engines, pressure-testing repowering assumptions, and aligning price bands to power and fuel configuration, the estimate stays easier to track and re-check as market conditions change.

Key Questions Answered in the Report

What is the current value of the marine propulsion engine market?

The marine propulsion engine market size reached USD 39.69 billion in 2026.

Which fuel type is growing fastest in new marine engines?

Green methanol is on the steepest rise, with a projected 2.88% CAGR through 2031 and mounting dual-fuel orders.

Which engine type currently holds the largest market share?

Diesel engines lead with 66.12% of the marine propulsion engine market share as of 2025.

Why are dual-fuel engines gaining market share?

They let operators switch between LNG, methanol, and conventional fuel to hedge fuel-price swings and meet tightening emissions rules.

Who are the top suppliers in the sector?

MAN Energy Solutions, Wärtsilä, Rolls-Royce Power Systems, Hyundai Heavy Industries Engine & Machinery, and Caterpillar hold the largest combined share.

How will IMO Tier III regulations impact older vessels?

Pre-2016 ships must retrofit SCR or EGR systems or face speed and charter penalties, fueling a rapid retrofit market.

Page last updated on: