Marine Steering System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

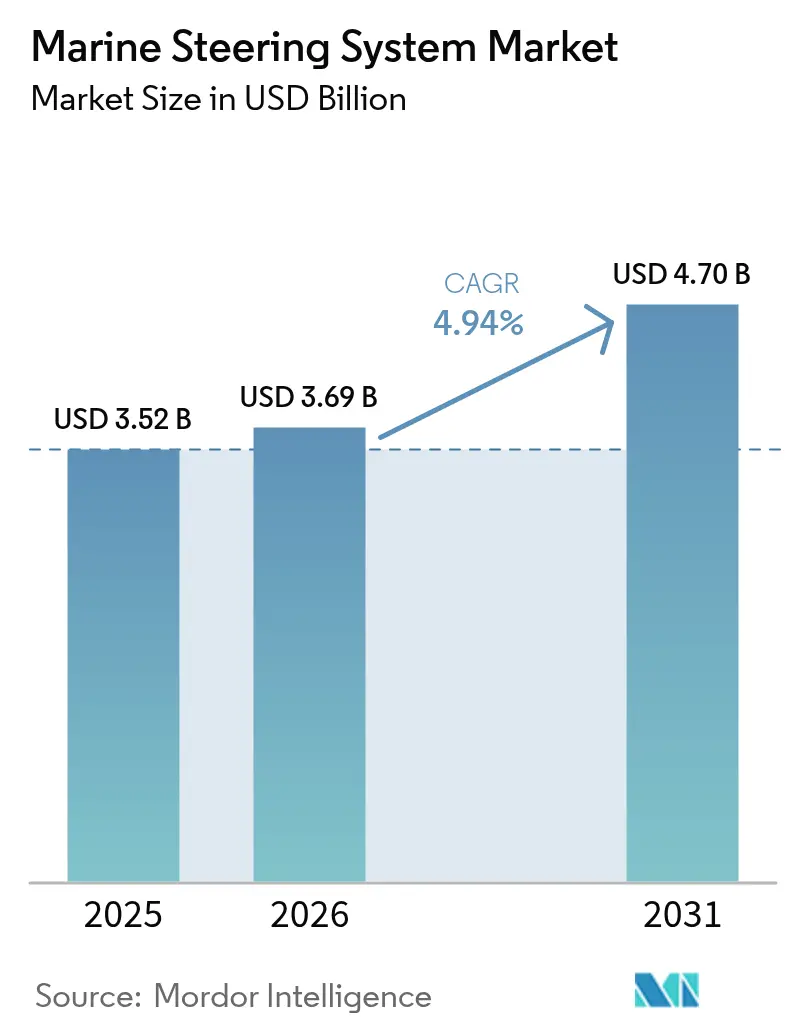

| Market Size (2026) | USD 3.69 Billion |

| Market Size (2031) | USD 4.7 Billion |

| Growth Rate (2026 - 2031) | 4.94% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Marine Steering System Market Analysis by Mordor Intelligence

The marine steering systems market size is expected to grow from USD 3.52 billion in 2025 to USD 3.69 billion in 2026 and is forecast to reach USD 4.7 billion by 2031 at 4.94% CAGR over 2026-2031. Digital integration, autonomous‐ready control architectures, and tightening regulatory oversight are the structural forces sustaining this trajectory. Vessels ranging from recreational runabouts to naval frigates now embed cyber-secure, software-defined steering gear that links seamlessly with electric propulsion and dynamic-positioning suites. Accelerated fleet renewal in Asia, steady retrofit demand in North America, and Europe’s decarbonization rules collectively ensure broad geographic pull for new-build as well as aftermarket solutions. Competitive intensity is rising as traditional hydraulic specialists race against electronics-savvy entrants to field integrated helm, actuator, and sensor packages compliant with the International Maritime Organization’s evolving steering-gear testing framework[1]“Amendments to IMO Instruments: Upcoming Entry-Into-Force Dates,” International Maritime Organization, imo.org.

Key Report Takeaways

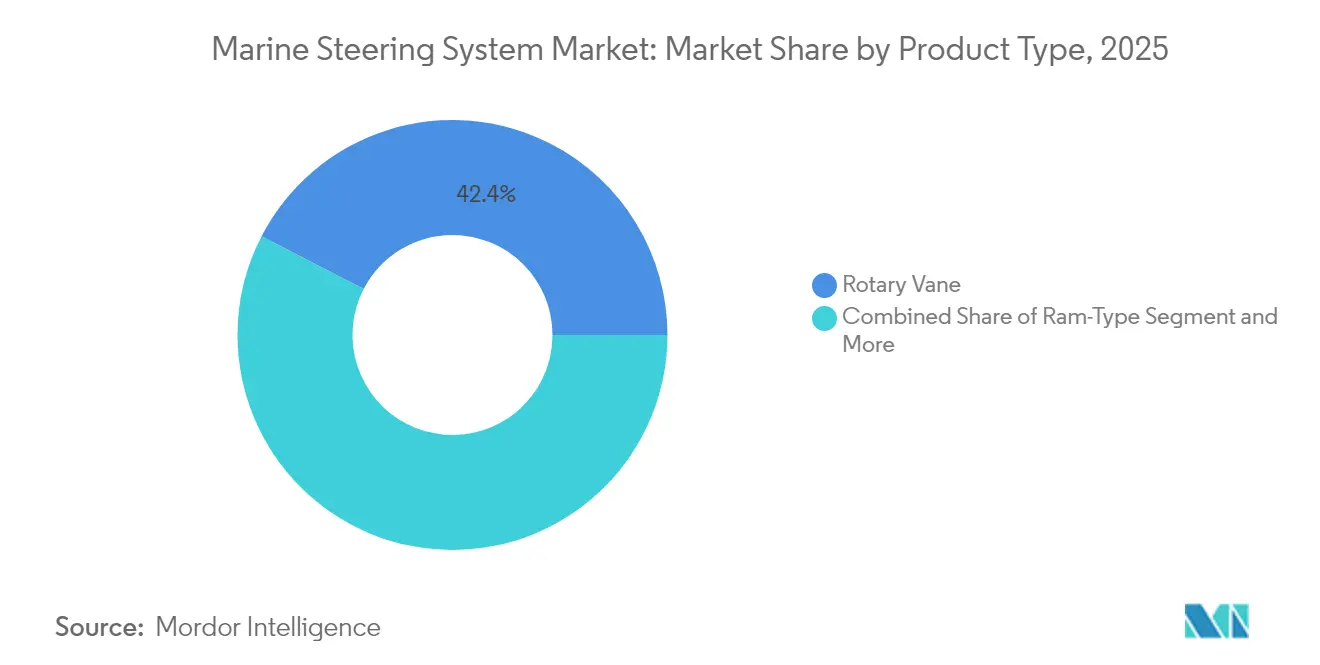

- By product type, rotary vane systems led with 42.41% of the marine steering systems market share in 2025; electro-mechanical integrated systems are projected to post the fastest 8.86% CAGR to 2031.

- By actuation technology, hydraulic platforms accounted for 51.86% share of the marine steering systems market size in 2025, while fully electric power steering is advancing at a 15.9% CAGR.

- By control mode, manual steering retained 61.12% of 2025 volumes; dynamic positioning and autonomous integration are the quickest movers at 14.12% CAGR through 2031.

- By vessel type, passenger craft captured 37.35% revenue share in 2025, whereas offshore energy support vessels are forecast to expand at 9.28% CAGR.

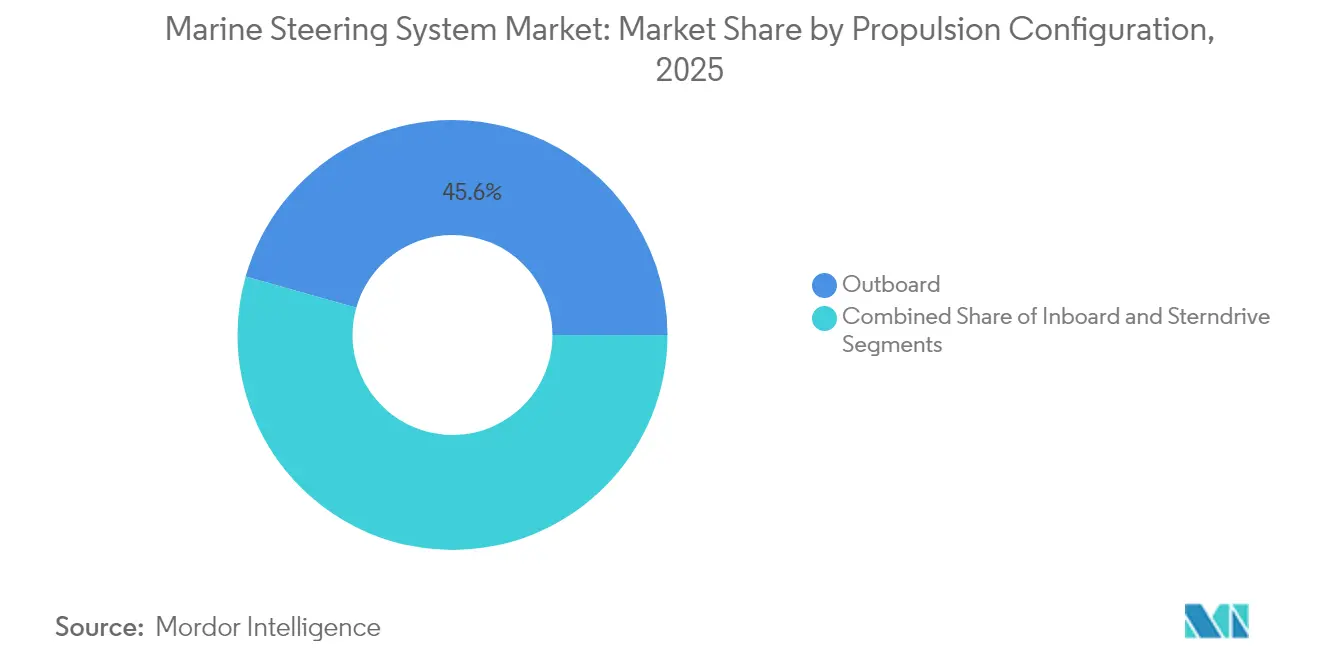

- By propulsion configuration, outboard units commanded a 45.61% share in 2025 and are projected to grow 7.52% annually to 2031.

- By distribution channel, OEM fitment represented 56.05% of sales in 2025; aftermarket retrofits show an 7.88% CAGR outlook.

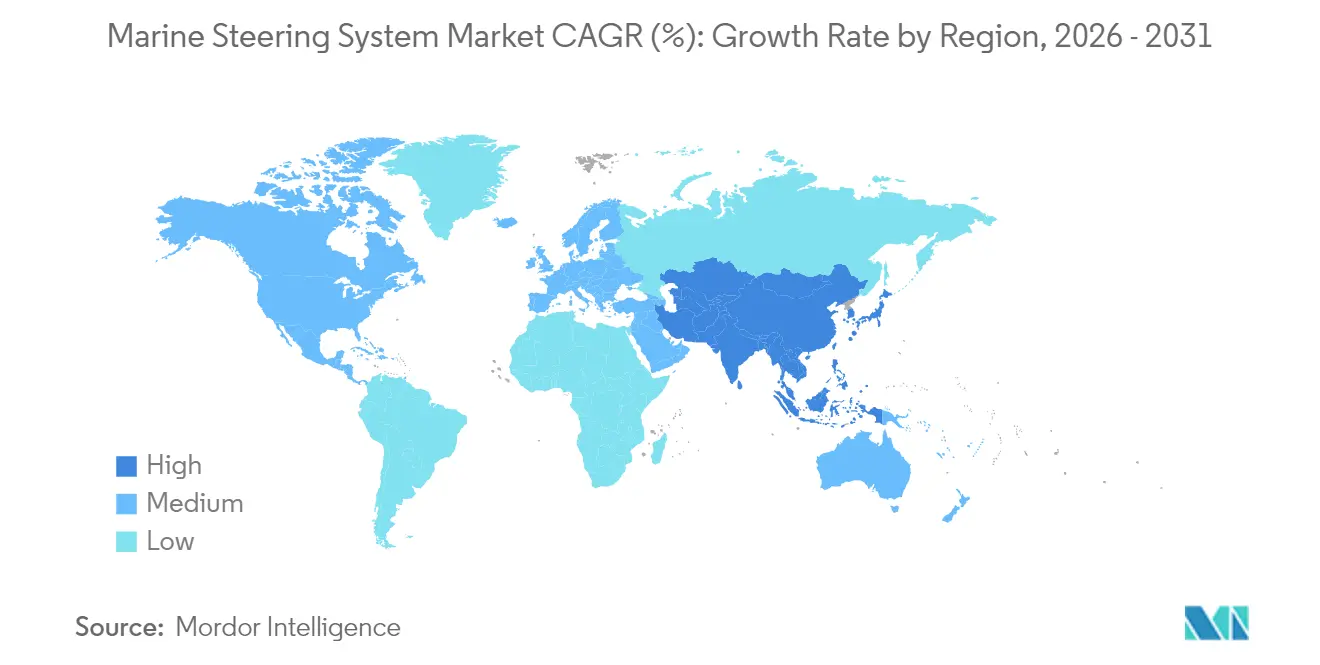

- By geography, North America held 45.98% of the market in 2025, while Asia-Pacific leads growth with an 8.27% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Marine Steering System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Naval Modernisation Programmes in Asia and Europe | +1.2% | Asia-Pacific, Europe | Medium term (2-4 years) |

| Growth in Global Recreational Boating Fleet | +0.8% | North America, Europe | Short term (≤ 2 years) |

| Retrofitting Surge Due to IMO Steering Gear Testing Mandates | +0.7% | Global | Medium term (2-4 years) |

| Push Toward Electric-Power Steering for Outboards | +0.6% | Global, with focus on North America | Short term (≤ 2 years) |

| Autonomous-Ready 'Fly-By-Wire' Rudder Actuators' Surge | +0.5% | Asia-Pacific, North America | Long term (≥ 4 years) |

| Low-Sulphur-Fuel Compatible Electro-Hydraulic Fluids' Demand | +0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Naval Modernization Programmes in Asia and Europe

Rising defense budgets propel steady procurement of multi-role frigates, amphibious carriers, and submarines across China, South Korea, Japan, Germany, and the Netherlands. Each hull specifies cyber-secure, redundancy-rich steering systems capable of mating with integrated bridge and combat-management suites. China’s People’s Liberation Army Navy operated 234 major surface combatants in 2024, outnumbering the 219 units fielded by the U.S. Navy, a fleet expansion that keeps domestic yards at full tilt and draws on steering subcontractors throughout regional supply chains[2]“Unpacking China’s Naval Buildup,” Center for Strategic and International Studies, csis.org. Parallel NATO programs in Europe reinforce demand for electric or electro-hydraulic actuators that minimize acoustic signatures, accommodate dynamic-positioning holds, and support unmanned wingman craft.

Growth in Global Recreational Boating Fleet

Powerboat and personal-watercraft sales recorded 230,000–240,000 units in the United States during 2024 as buyers sought joystick docking, wireless helm controls, and integrated autopilots that simplify skippering for novice owners[3]“Innovation Driving U.S. Boat Sales Demand,” National Marine Manufacturers Association, nmma.org. OEMs bundle smart steering with propulsion upgrades, creating a compelling aftermarket funnel for older hulls. The segment’s domestic economic footprint sustains parts, service, and electronics revenues that cushion cyclical swings in new-boat registrations.

Retrofitting Demand Driven by IMO Mandates

SOLAS amendments and IMO cybersecurity guidelines that took effect in July 2024 oblige commercial operators to verify rudder response times, emergency back-up power, and network hardening every five years. Vessels built before 2010 frequently fail these audits, prompting retrofit contracts for digital pump sets, servo-valves, and control heads that can log diagnostic data and receive over-the-air firmware patches.

OEM Push Toward Electric-Power Steering for Outboards

Outboard builders now release electric helm packages that eliminate hydraulic hoses, reduce weight, and deliver millisecond torque response. Mercury’s 7,500-watt Avator propulsion pairs with drive-by-wire steering to execute autonomous docking routines, an integration path echoed by Yamaha and ZF. These systems also satisfy zero-leak rules in protected waters and simplify installation for boatyards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyclical Downturn in Commercial Shipbuilding | -0.9% | Global, particularly Asia | Short term (≤ 2 years) |

| High Upfront Cost of Electric Steering Conversions | -0.6% | Global | Medium term (2-4 years) |

| Shortage of Marine-Grade Semiconductor Chips | -0.4% | Global | Short term (≤ 2 years) |

| Class-Society Cyber-Resilience Rules | -0.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyclical Downturn in Commercial Shipbuilding

Container-ship new-build bookings remain historically elevated, yet tanker, bulk, and general-cargo contracts softened through 2024 as operators delayed capital expenditures. Asian yards adjust output to match this mix, reducing baseline demand for standard helm sets even as retrofit work rises to offset capacity fluctuations.

High Upfront Cost of Electric Steering Conversions

Smaller workboat owners balk at rewiring vessels or swapping mechanical linkages for digital servo-motors. Return-on-investment calculations hinge on fuel savings and reduced service hours, but capital costs still deter immediate roll-outs outside subsidy programs. The economic challenge intensifies for older vessels where electric steering integration requires extensive electrical infrastructure upgrades, creating cost barriers that slow market penetration despite long-term operational benefits and regulatory compliance advantages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Electro-Mechanical Systems Lead Innovation

Rotary-vane designs retained 42.41% of the marine steering systems market share in 2025, anchored by reliability and simple service protocols. Yet electro-mechanical integrated units headline growth with a 8.86% CAGR through 2031 as shipyards specify precision control, noise reduction, and embedded diagnostics. Ram cylinders continue in heavy-lift naval and offshore support craft where extreme torque and redundancy are mandatory. Rack-and-pinion assemblies serve niche inland and small-craft segments needing compact footprints.

Demand tilts toward software-defined actuators that self-calibrate and interface with collision-avoidance algorithms. Classification societies now certify cyber-secure firmware, nudging operators toward new-generation electric or hybrid products rather than refurbishing legacy hydraulics. Consequently, the marine steering systems market sees product road-maps converge on modular electro-mechanical cartridges deployable across vessel classes.

By Actuation Technology: Electric Systems Surge Despite Hydraulic Dominance

Hydraulic circuits still delivered 51.86% of 2025 installations, yet fully electric power steering is accelerating at 15.9% annually. Hybrid electro-hydraulic packages bridge the transition, offering on-demand pumps that spin only when commanded, trimming idle losses, and enabling engine-off maneuvering. Mechanical cable systems persist in low-horsepower craft but face gradual replacement as joystick and autopilot features move down-market.

Electric actuators achieve sub-millisecond lag and integrate regenerative braking that eases hotel-load demands on hybrid vessels. As flag administrations tighten oil-to-water discharge limits, operators view fluid-free architectures as both compliance facilitators and lifecycle cost reducers. This performance-plus-sustainability mix cements electric technology as the marine steering systems market’s most disruptive trend.

By Control Mode: Autonomous Integration Transforms Manual Dominance

Manual wheels and tillers still represent 61.12% of shipped units in 2025, a legacy of regulatory insistence on human oversight. Autopilots fulfil mid-market adoption, combining course-keeping with fuel-saving algorithms. Dynamic-positioning and autonomous helm modules, however, post a 14.12% CAGR as offshore wind, survey, and research vessels demand centimeter-level station hold.

AI-stack suppliers embed sensor fusion, collision regulations, and weather routing into helm logic, lowering crew workloads and enabling reduced-manning operations. Updating software over secure channels extends feature life, reinforcing the perception that the marine steering systems market mirrors the smartphone model, where periodic upgrades supersede component replacement.

By Vessel Type: Offshore Energy Support Drives Growth

Passenger craft, including cruise liners, ferries, and yachts, held 37.35% revenue in 2025, buoyed by post-pandemic leisure demand that prizes silent, vibration-free helm response. Offshore energy service vessels claim the fastest 9.28% CAGR, reflecting expanding wind-turbine installation fleets that require dynamic-positioning precision in congested sea lanes. Commercial cargo ships and workboats provide baseline volumes, while naval and coast-guard hulls inject specification-rich orders that push technological boundaries.

The marine steering systems market, therefore, balances high-spec defense contracts, volume recreational orders, and electrically intensive offshore platforms, each influencing design priorities across the supply chain.

By Propulsion Configuration: Outboard Systems Lead Innovation

Outboard layouts delivered 45.61% of 2025 shipments and are forecast to climb 7.52% annually. The segment benefits from modular rigging, swift electrification, and widespread dealer networks. Inboard engines dominate high-horsepower commercial and defense craft, where centralized machinery favors shaft lines. Sterndrive hybrids serve niche sport-cruiser customers, combining inboard power with outboard-like trim angles.

Outboards now integrate steering motors inside the cowl, minimizing parts and enabling 360-degree joystick maneuverability. As propulsion shifts to high-voltage battery packs, helm manufacturers collaborate directly with motor OEMs, embedding torque commands over single digital lines and reshaping competitive dynamics within the marine steering systems market.

By Distribution Channel: Aftermarket Retrofit Accelerates

OEM installations comprised 56.05% of 2025 revenue, reflecting tight coordination between builders and component suppliers. Yet retrofit activity is expanding at 7.88% CAGR as fleets modernize for compliance and digital functionality. Independent dealers and service yards now market plug-and-play electric helm kits targeting vessels built since 2000 that lack CAN-bus infrastructure.

Regulatory deadlines, especially U.S. Coast Guard cyber rules entering force in July 2025, motivate commercial operators to schedule steering upgrades during routine dry-dock cycles. This dynamic ensures an enduring aftermarket pipeline even if new-build orders fluctuate.

Geography Analysis

North America held 45.98% of the marine steering system market in 2025 and is forecast to grow on robust discretionary spending and 85 million boating participants maintain high turnover in powerboat inventories, while U.S. Coast Guard cybersecurity directives accelerate the adoption of encrypted digital helms across commercial fleets. Canadian Arctic patrol programs further support the sophisticated steering demand for ice-classified hulls.

Asia-Pacific leads growth with an 8.27% CAGR to 2031. Chinese naval expansion, underscored by 234 major warships in active service, fuels domestic shipbuilding production as yards aim for self-reliance in critical subsystems. Japan, South Korea, and Singapore pioneer autonomous surface research, seeding demand for AI-compatible helm actuators. Regional electrification policies add momentum, particularly in coastal tourism and island logistics fleets where zero-emission mandates emerge.

Europe records growth, anchored by NATO frigate programs and stringent environmental statutes. The European Maritime Safety Agency’s STEERSAFE recommendations obligate continuous monitoring of rudder angle, load, and response times, leading operators to specify sensor-rich steering gear. Norway’s operational autonomous passenger ferry pilot validates real-world readiness of digital helm solutions, encouraging wider municipal deployments across the continent. Concurrently, the EU AI Act provides legal clarity for machine-learning functions embedded in steering firmware, spurring vendor investments.

Competitive Landscape

Competition features a blend of legacy hydraulics leaders and electronics-first insurgents. SeaStar Solutions leverages broad dealer networks, while ZF transfers automotive by-wire know-how to marine thrusters and helm modules. Mercury Marine integrates propulsion, steering, and cloud connectivity under a unified data ecosystem that underpins Brunswick’s “Boating Intelligence” brand proposition.

Strategic activity centers on vertically integrated packages that bundle helm wheels, actuators, sensors, and software licenses into subscription-ready platforms. Cybersecurity certification emerges as both a barrier and a differentiator, compelling suppliers to maintain in-house encryption and threat-model expertise. Start-ups focus on AI navigation overlays that ride atop open-architecture helm hardware, challenging incumbents to open their APIs without ceding market share. M&A is likely as companies seek to scale up and amortize R&D and certification costs within the marine steering systems market.

Marine Steering System Industry Leaders

Dometic Marine

ZF Friedrichshafen AG

Mercury Marine (Brunswick)

Bosch Rexroth

Kongsberg Maritime

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Yamaha Motor Corporation unveiled HARMO fully electric outboards featuring integrated digital electric steering and rim-drive architecture.

- September 2024: Honda Marine debuted a joystick steering package that couples Ultraflex helm gear with Vetus bow thrusters for seamless low-speed maneuvering.

- September 2024: Becker Marine Systems released a compact, low-pressure hydraulic steering gear optimized for space-constrained compartments in small commercial vessels.

Global Marine Steering System Market Report Scope

Marine Steering System Market is segmented by Product Type (Rotary Vane Type and Ram Type), by Means of Steering (Auto-Pilot and Manual) by Type (Hydraulic and Electric), by End-User Industry (Passenger Vessels, Defense, and Commercial), and by Geography

| Rotary Vane |

| Ram-Type |

| Rack-and-Pinion |

| Electro-Mechanical (Integrated) |

| Conventional Hydraulic |

| Electro-Hydraulic |

| Fully Electric Power Steering (EPS) |

| Mechanical/Cable |

| Manual |

| Auto-Pilot |

| DP/Autonomous Integration |

| Passenger (Cruise, Ferry, Yacht) |

| Commercial Cargo and Workboats |

| Naval and Coast-Guard |

| Offshore Energy Support |

| Inboard |

| Outboard |

| Sterndrive |

| OEM Fitment |

| Aftermarket Retrofit |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Egypt | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Rotary Vane | |

| Ram-Type | ||

| Rack-and-Pinion | ||

| Electro-Mechanical (Integrated) | ||

| By Actuation Technology | Conventional Hydraulic | |

| Electro-Hydraulic | ||

| Fully Electric Power Steering (EPS) | ||

| Mechanical/Cable | ||

| By Control Mode | Manual | |

| Auto-Pilot | ||

| DP/Autonomous Integration | ||

| By Vessel Type | Passenger (Cruise, Ferry, Yacht) | |

| Commercial Cargo and Workboats | ||

| Naval and Coast-Guard | ||

| Offshore Energy Support | ||

| By Propulsion Configuration | Inboard | |

| Outboard | ||

| Sterndrive | ||

| By Distribution Channel | OEM Fitment | |

| Aftermarket Retrofit | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Egypt | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the marine steering systems market?

The marine steering systems market size reached USD 3.69 billion in 2026 and is projected to climb to USD 4.7 billion by 2031.

Which product segment is growing the fastest?

Electro-mechanical integrated steering systems are expanding at a 8.86% CAGR through 2031, outpacing all other product categories.

How quickly are electric steering technologies being adopted?

Fully electric power steering shows a 15.9% CAGR, reflecting strong OEM commitment to energy efficiency and autonomous readiness.

Which region offers the highest growth potential?

Asia-Pacific leads with an 8.27% CAGR thanks to large-scale naval procurement and widespread investment in autonomous vessel programs.

Why is aftermarket retrofit becoming more important?

IMO safety tests and U.S. Coast Guard cyber rules require older vessels to upgrade steering gear, driving an 7.88% CAGR in retrofit sales.

Page last updated on: