Marine & Shipbuilding NDT Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

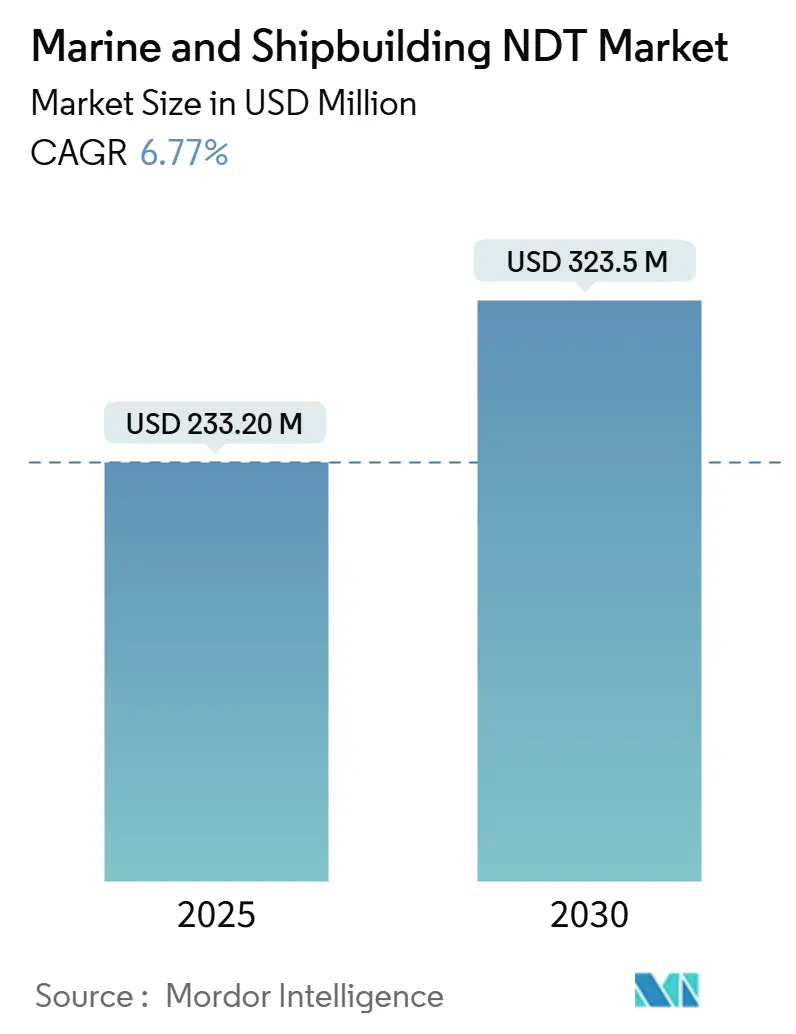

| Market Size (2025) | USD 233.20 Million |

| Market Size (2030) | USD 323.5 Million |

| Growth Rate (2025 - 2030) | 6.77% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

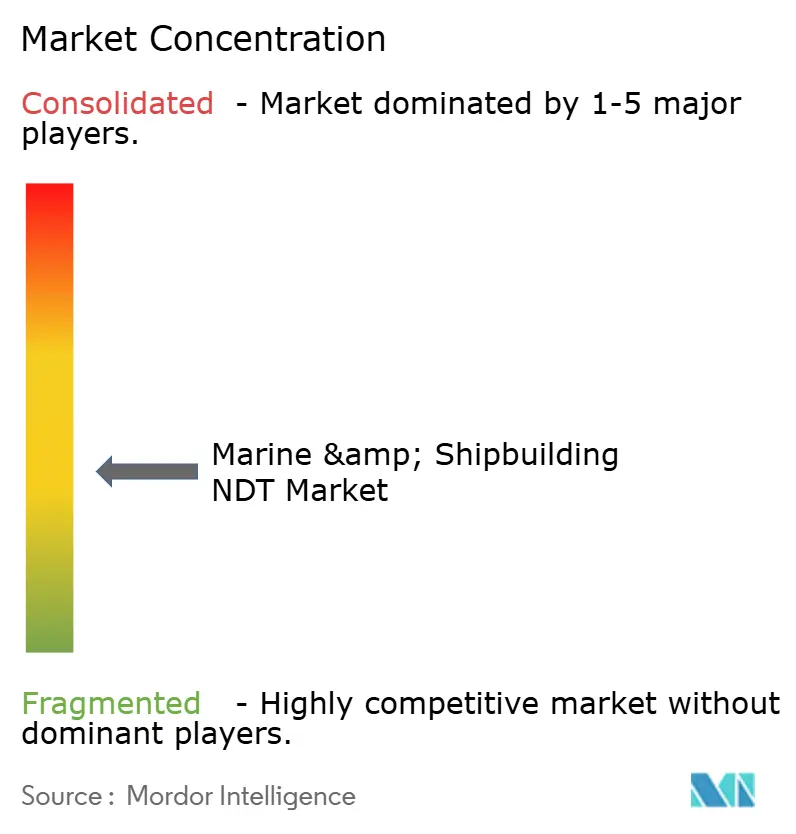

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Marine & Shipbuilding NDT Market Analysis by Mordor Intelligence

The Marine and shipbuilding NDT market size is estimated at USD 0.23 billion in 2025 and is projected to reach USD 0.32 billion by 2030, growing at a 6.77% CAGR. This growth is propelled by aging fleets that require more frequent structural assessments, stricter International Maritime Organization GHG rules, and digital inspection technologies that improve asset uptime. Rising LNG carrier construction, autonomous vessel programs, and naval modernization budgets are widening the customer base. Service providers benefit from recurring dry-dock inspections, while software vendors gain share through digital twins and AI-enabled defect analytics. Competitive differentiation is shifting toward integrated solutions that combine multiple test methods, real-time data capture, and cloud-based compliance reporting, creating fresh revenue opportunities for firms with deep marine expertise.

Key Report Takeaways

- By component, services commanded 79.1% of the Marine and shipbuilding NDT market share in 2024, while software is projected to advance at a 12.8% CAGR through 2030.

- By testing method, ultrasonic testing is expected to lead with a 27.8% revenue share in 2024; eddy-current testing is projected to expand at a 9.8% CAGR through 2030.

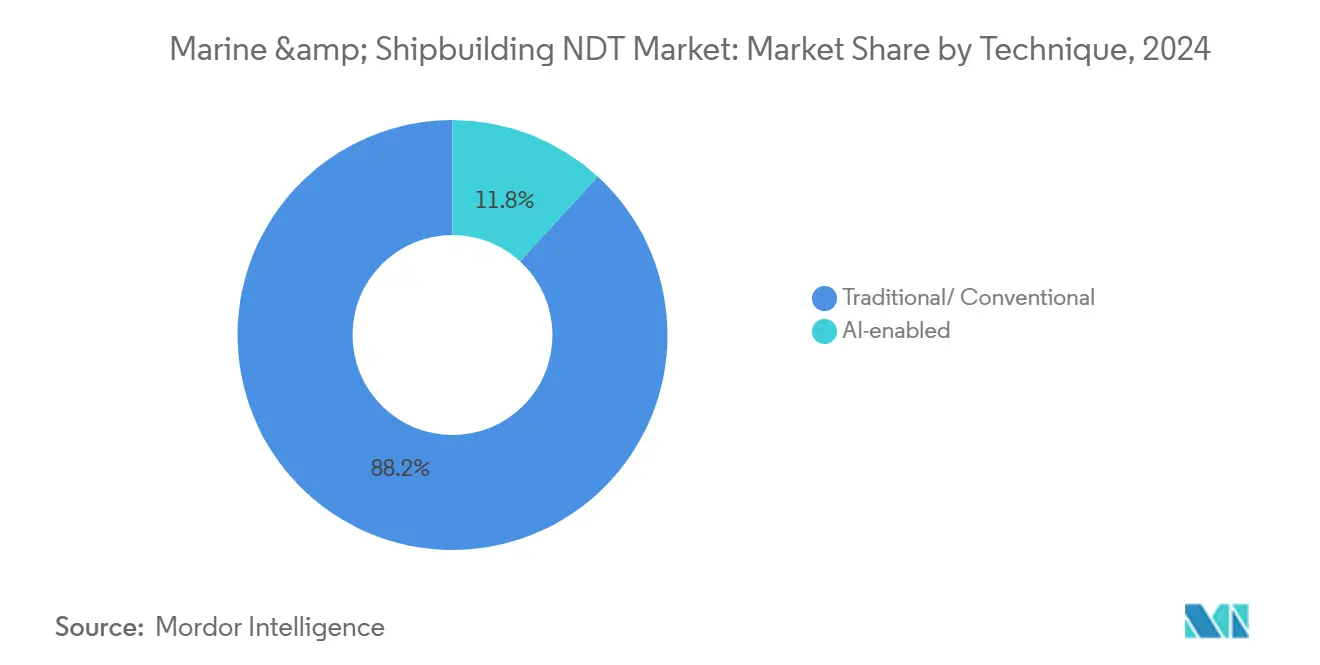

- By technique, traditional approaches accounted for 88.2% of the Marine and shipbuilding NDT market size in 2024, while AI-enabled systems are projected to grow at a 15.9% CAGR through 2030.

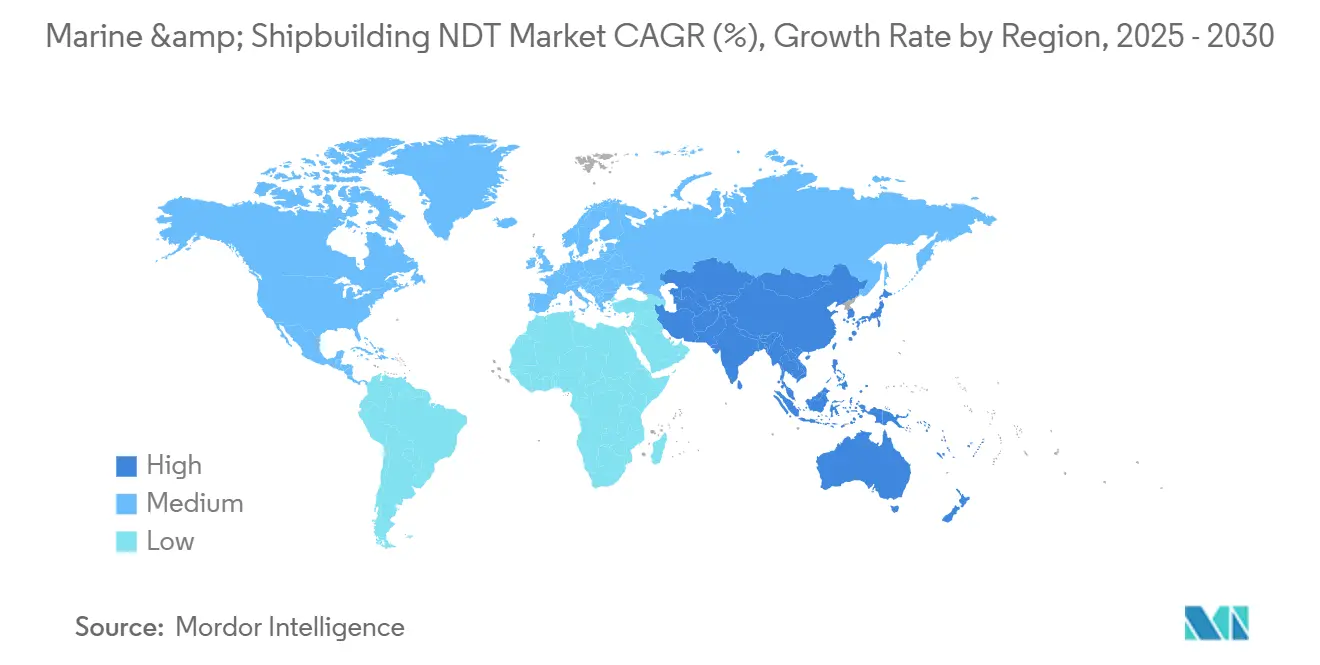

- By geography, North America held 36.1% of the Marine and shipbuilding NDT market size in 2024, and the Asia-Pacific region is set to record the fastest growth at a 7.5% CAGR through 2030.

Global Marine & Shipbuilding NDT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing focus on hull integrity in the aging global fleet | +1.8% | Global, with a concentration in Europe and North America | Medium term (2-4 years) |

| Rapidly expanding LNG tanker orderbook | +1.2% | Asia-Pacific core, spill-over to the Middle East | Short term (≤ 2 years) |

| Growing adoption of digital twin-enabled predictive maintenance | +1.5% | North America and Europe, expanding to the Asia-Pacific | Long term (≥ 4 years) |

| Stricter IMO GHG regulations are driving dry-dock inspections | +1.1% | Global | Short term (≤ 2 years) |

| Autonomous vessel development requiring real-time NDT data | +0.9% | North America and Europe | Long term (≥ 4 years) |

| Naval fleet modernization programs in the Asia-Pacific | +0.7% | Asia-Pacific, with spillover to the Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Focus on Hull Integrity in Aging Global Fleet

Global merchant vessels average 21.9 years of service, prompting owners to conduct enhanced hull-thickness checks as ships approach 25-year milestones. Classification societies now mandate ultrasonic measurements every 2.5 years for vessels older than 15 years, halving the previous interval of 5 years.[1]DNV, “Enhanced NDT Protocols for Aging Vessel Inspections,” dnv.com Traditional visual methods miss 40% of critical flaws, exposing operators to potential USD 50 million losses from emergency repairs and pollution fines. Phased-array ultrasonics and eddy-current arrays detect millimeter-scale corrosion along welds and stress hotspots, lowering unplanned downtime. Demand growth is strongest in Europe and North America, where older fleets dominate dry-dock schedules.

Rapidly Expanding LNG Tanker Orderbook

The LNG carrier backlog reached 518 vessels in 2024, a 340% surge since 2019, as Europe diversified its energy imports and Asia increased gas demand. Cryogenic containment designs using 9% nickel steel and aluminum alloys experience thermal swings of up to 200 °C, which accelerate microcracking. Specialized ultrasonics can detect flaws as small as 0.1 mm, while robotic crawlers and wireless sensors enhance access to insulated holds. LNG-specific inspections yield 2.5 times higher margins than conventional tanker work, bolstering service revenues in Korean, Chinese, and Qatari shipyards.

Growing Adoption of Digital Twin-Enabled Predictive Maintenance

Shell reduced unplanned maintenance by 35% and inspection expenses by 28% across 50 ships by pairing embedded sensors with digital twins that forecast degradation 18 months ahead. Kongsberg’s platform integrates thickness, vibration, and thermal inputs to model structural health on over 200 vessels.[2]Kongsberg, “Digital Twin Platform for Maritime Structural Health Monitoring,” kongsberg.com Classification societies are piloting remote-survey schemes that accept continuous monitoring in lieu of periodic audits, which shortens port calls and improves fleet utilization. Long-term adoption will accelerate as AI reduces false positives and regulatory frameworks mature.

Stricter IMO GHG Regulations Driving Dry-Dock Inspections

MEPC 83 rules require energy-efficiency assessments at every dry dock, broadening hull-surface and propulsion tests. A 100-micron rise in hull roughness can reduce fuel economy by 3-5%, prompting the use of laser scans and structured-light profiling to complement ultrasonic checks. Operators must submit repair logs with full NDT evidence to classification societies and flag administrations. The additional documentation increases demand for compliant data platforms and certified technicians, particularly in Asia-Pacific yards that offer turnkey retrofit packages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of marine-certified NDT technicians | -1.3% | Global, acute in Asia-Pacific and the Middle East | Medium term (2-4 years) |

| High acquisition cost of ship-grade radiography systems | -0.9% | Global, particularly impacting smaller service providers | Short term (≤ 2 years) |

| Limited wireless connectivity inside steel hull structures | -0.6% | Global | Medium term (2-4 years) |

| Stringent radiation safety rules are increasing testing time | -0.4% | Global, stricter in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Marine-Certified NDT Technicians

A 35% talent gap persists as marine projects outpace the supply of rope-access-trained, confined-space-qualified inspectors.[3]American Society for Nondestructive Testing, “Marine NDT Technician Shortage Assessment,” asnt.org Certification takes up to 24 months, and 40% of the current workforce nears retirement. Only 12 accredited academies offer ship-specific programs, prolonging lead times for LNG hull checks. Wage inflation of 15-20% and six-month service delays are now common in shipyards in Singapore, Busan, and Dubai, prompting major operators to invest in automation and remote inspection.

High Acquisition Cost of Ship-Grade Radiography Systems

Rugged digital radiography units cost USD 800,000–1.2 million, roughly triple the cost of comparable on-shore gear, due to the need for salt-spray protection, vibration tolerance, and explosion-proof certifications. Smaller firms struggle to raise capital, ceding projects to larger rivals or leasing mobile vans at premium rates. The cost barrier slows geographic expansion and fuels consolidation, especially in emerging markets where port access adds logistics overheads.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Dominate Through Specialized Expertise

Services generated 79.1% of the Marine and shipbuilding NDT market revenue in 2024 as ship surveys demand on-site experts who can navigate confined spaces and satisfy each classification society’s protocol. Recurring dry-dock cycles secure predictable income, and technicians frequently bundle rope access, cleaning, and inspection tasks into turnkey packages. Meanwhile, the software’s 12.8% CAGR reflects the growing adoption of AI-driven flaw detection and cloud dashboards that accelerate approval workflows. Equipment sales experience lumpy demand due to their capital-intensive nature, whereas consumables are driven by inspection frequency.

Software platforms now automatically generate compliance reports in near real-time, reducing administrative labor by 30%. AI-based image analytics flag suspect indications 25% faster than manual review. Digital workflows also support mixed-reality headsets that guide novices through procedure steps, easing the technician shortage. Equipment vendors are pivoting toward modular rigs that integrate ultrasonics, eddy-current, and thermography to reduce changeovers aboard crowded decks.

By Testing Method: Ultrasonic Testing Leads With Eddy-Current Gaining

Ultrasonic methods held a 27.8% market share in the marine and shipbuilding NDT market in 2024, thanks to their versatility in gauging steel thickness without requiring the removal of coatings. High-frequency probes cover hull plating, engine bedplates, and bulkhead structures, forming the backbone of statutory surveys. Eddy-current’s 9.8% CAGR arises from better surface-crack detection in aluminum superstructures and cryogenic alloys prevalent in LNG carriers.

Radiography remains indispensable for verifying root welds during new-build construction, but faces berth-access limitations due to radiation safety concerns. Magnetic particle and liquid penetrant tests offer low-cost surface flaw screening, while visual inspection gains are achieved through drones and remotely operated vehicles that capture 4K imagery of underwater hulls. Thermography identifies saturated composite decks and overheated bearings, while computed tomography advances in propeller and gear-hub quality control, where complex geometries can conceal shrinkage voids.

By Technique: AI-Enabled Solutions Challenge Traditional Methods

Traditional approaches accounted for 88.2% of 2024 revenue, reflecting regulatory conservatism and crew familiarity. Yet, AI-enhanced systems grow at a rate of 15.9% annually, as machine learning distinguishes pore porosity from benign inclusions and accelerates computed tomography review by 30 times. Automated recognition stabilizes defect sizing, reducing the need for Level III sign-offs in routine scans, and cloud training datasets expand accuracy over time. Classification societies are drafting guidance that will mainstream AI for baseline hull surveys within the next four years, particularly for commercial fleets adopting condition-based maintenance.

Geography Analysis

North America held 36.1% of 2024 revenue, underpinned by a USD 32.4 billion U.S. Navy shipbuilding budget and stringent Coast Guard inspection rules. American yards benefit from mature technician pipelines at Texas A&M and U.S. Maritime Administration academies, ensuring workforce availability despite global shortages. Canadian Arctic patrol ships and Mexican port upgrades add incremental demand, while regional classification offices in Houston and New York accelerate technology approvals.

The Asia-Pacific region is expanding at the fastest rate, with a 7.5% CAGR. China produced 47% of the global tonnage in 2024, and its naval blueprint lists six carriers and twenty destroyers before 2030, fueling the need for elite inspections. South Korea’s leadership in LNG hull fabrication calls for cryogenic-fit probes and corrosion-mapping robots, whereas Japan pioneers autonomous coaster fleets that integrate continuous structural monitoring. India’s Project-75I submarines spur indigenization of ultrasound and eddy-current tooling, stimulating domestic vendor ecosystems.

Europe shows a steady advance, powered by offshore wind parks and LNG import terminals that increase hull, monopile, and riser inspection volumes. Norway’s Maritime Robotics and Denmark’s offshore clusters pilot drone-based UT and laser scans, showcasing regulatory acceptance.[4]Maritime Robotics, “Autonomous Vessel Development and Inspection Systems,” maritimerobotics.com Middle East and African markets are smaller but are accelerating as Saudi Arabia’s NEOM port and the UAE's naval refits specify class-approved NDT, placing a premium on mobile, containerized labs. South America gains momentum through Brazil’s ProSub program and Argentine frigate upgrades, though reliance on foreign contractors remains high.

Competitive Landscape

The Marine and shipbuilding NDT market features moderate fragmentation, with no company controlling more than 8% of the revenue. This is due to regional rules and vessel diversity, which reward localized expertise. Classification societies, such as DNV, Bureau Veritas, and Lloyd’s Register, wield influence by authoring standards and offering in-house inspection crews; however, specialized firms compete by integrating robotics, AI, and multi-tech equipment.

Eddyfi Technologies and MISTRAS Group deploy crawler robots and deep-learning analytics to cut survey duration and offset labor scarcity. Interocean Marine Services’ drone-based thickness system received ABS and DNV approvals in 2024, demonstrating the viability of airborne UT. North Star Imaging focuses on high-energy CT for propeller hubs and additive-manufactured spare parts, while Olympus expands mixed-reality guidance to shorten technician onboarding.

Mergers continue as capital-heavy radiography assets push smaller outfits to exit. Ashtead Technology acquired Seatronics and J2 Subsea for USD 80.0 million, thereby expanding its rental fleet and enhancing its global reach. Bilfinger and BP’s multi-year North Sea pact highlights the demand for turnkey packages that integrate rope access, corrosion mapping, and digital reporting.

Marine & Shipbuilding NDT Industry Leaders

Bureau Veritas SA

SGS SA

MISTRAS Group, Inc.

Olympus Corporation (Evident)

Eddyfi Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Bilfinger secured a multi-year BP contract for NDT across North Sea assets, broadening its marine coverage.

- April 2025: Flyability’s Elios 3 drone earned ClassNK endorsement for confined-space maritime UT.

- March 2025: TSC Subsea launched the TRITON crawler for internal pipeline inspection.

- February 2025: Axess Group entered a master agreement with Heerema Marine Contractors for long-term inspection services.

Global Marine & Shipbuilding NDT Market Report Scope

| Equipment |

| Software |

| Services |

| Consumables |

| Ultrasonic Testing |

| Radiographic Testing |

| Magnetic Particle Testing |

| Liquid Penetrant Testing |

| Visual Inspection Testing |

| Eddy-Current Testing |

| Acoustic Emission Testing |

| Thermography / Infrared Testing |

| Computed Tomography Testing |

| Traditional / Conventional |

| AI-enabled |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Equipment | |

| Software | ||

| Services | ||

| Consumables | ||

| By Testing Method | Ultrasonic Testing | |

| Radiographic Testing | ||

| Magnetic Particle Testing | ||

| Liquid Penetrant Testing | ||

| Visual Inspection Testing | ||

| Eddy-Current Testing | ||

| Acoustic Emission Testing | ||

| Thermography / Infrared Testing | ||

| Computed Tomography Testing | ||

| By Technique | Traditional / Conventional | |

| AI-enabled | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the Marine and shipbuilding NDT market?

The Marine and shipbuilding NDT market size is USD 233.2 million in 2025.

What is the market's expected growth rate through 2030?

The market is forecast to post a 6.77% CAGR between 2025 and 2030.

Which region leads demand today?

North America holds 36.1% of 2024 revenue, driven by naval programs and strict regulatory oversight.

Which testing method is most widely used?

Ultrasonic testing leads with 27.8% revenue share because it measures hull thickness without removing coatings.

Why are digital twins gaining traction in ship inspections?

Digital twins reduce unplanned maintenance by 35% and inspection costs by 28% by predicting structural degradation 18 months in advance.

What is the main challenge limiting faster market expansion?

A global shortage of marine-certified NDT technicians results in service delays and rising wages.

Page last updated on: