Malic Acid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

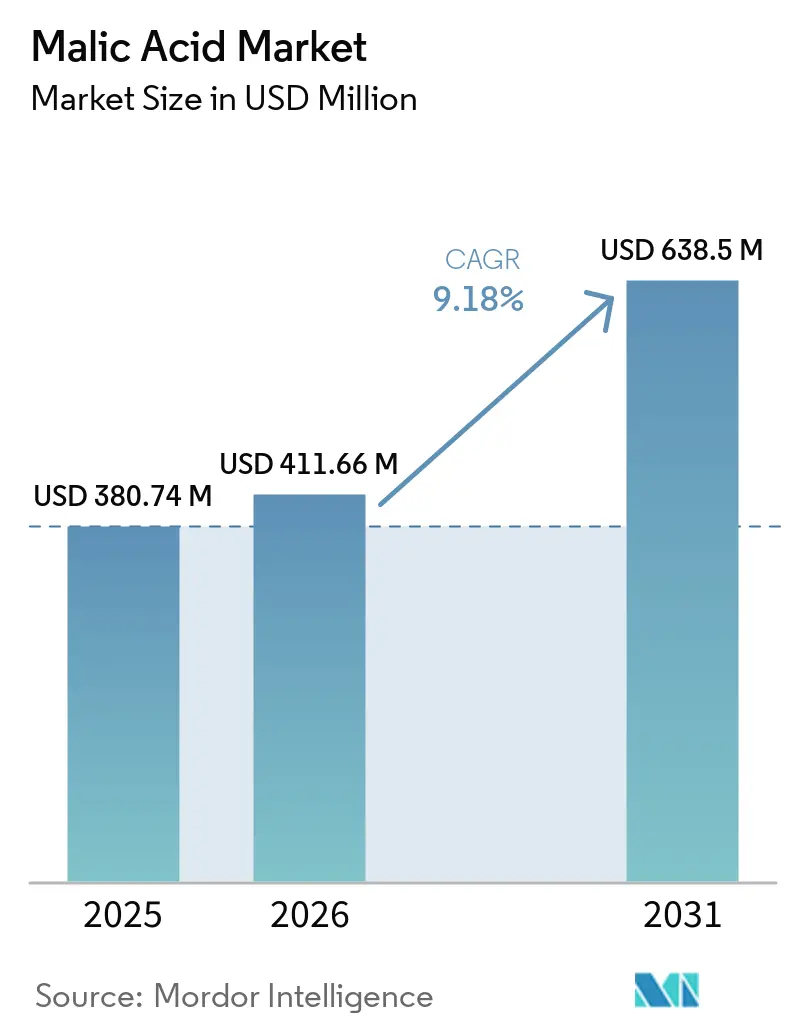

| Market Size (2026) | USD 411.66 Million |

| Market Size (2031) | USD 638.5 Million |

| Growth Rate (2026 - 2031) | 9.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

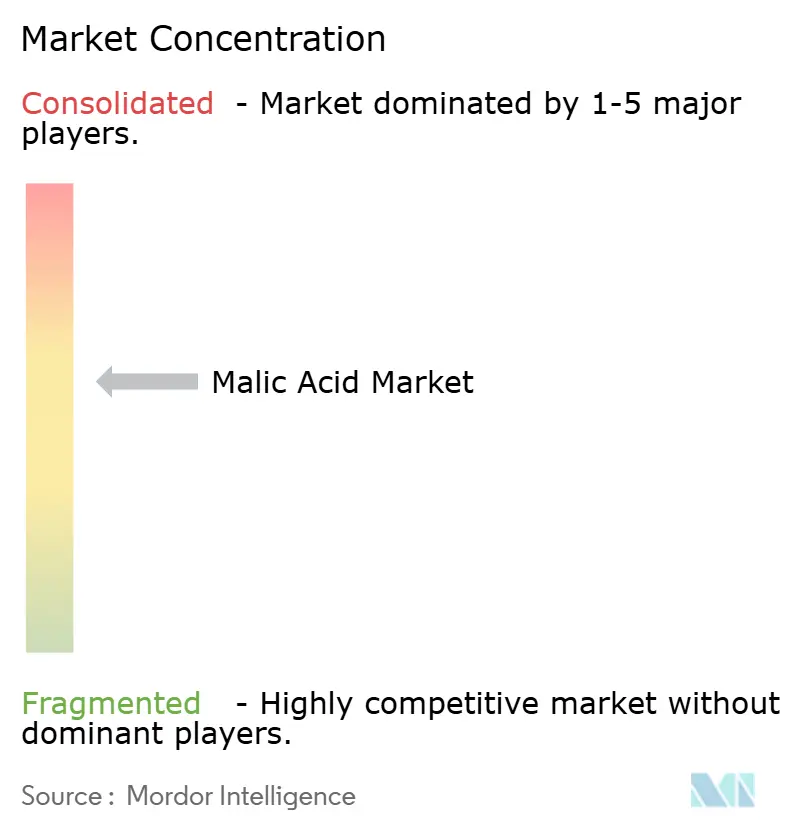

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Malic Acid Market Analysis by Mordor Intelligence

The malic acid market is expected to grow from USD 380.74 million in 2025 and USD 411.66 million in 2026 to USD 638.50 million by 2031, registering a CAGR of 9.18% between 2026 and 2031. The malic acid market is entering a high-growth phase, supported by strong momentum in clean-label reformulations and functional food and beverage applications. Rising adoption is driven by increased use of natural acidulants in sports drinks, nutraceuticals, and pharmaceuticals, where malic acid enhances stability and taste profiles. Regulatory harmonization across key markets, including GRAS recognition in the United States, E296 classification in Europe, and FSSAI approval in India, continues to streamline product commercialization. On the supply side, strategic investments and partnerships, such as capacity expansions in North America and Asia-Pacific, are strengthening production capabilities while improving sustainability metrics. Additionally, industry consolidation and vertical integration initiatives are reshaping competitive dynamics, with established manufacturers and biotech players focusing on efficiency, low-carbon processes, and differentiated applications to capture future growth.

Key Report Takeaways

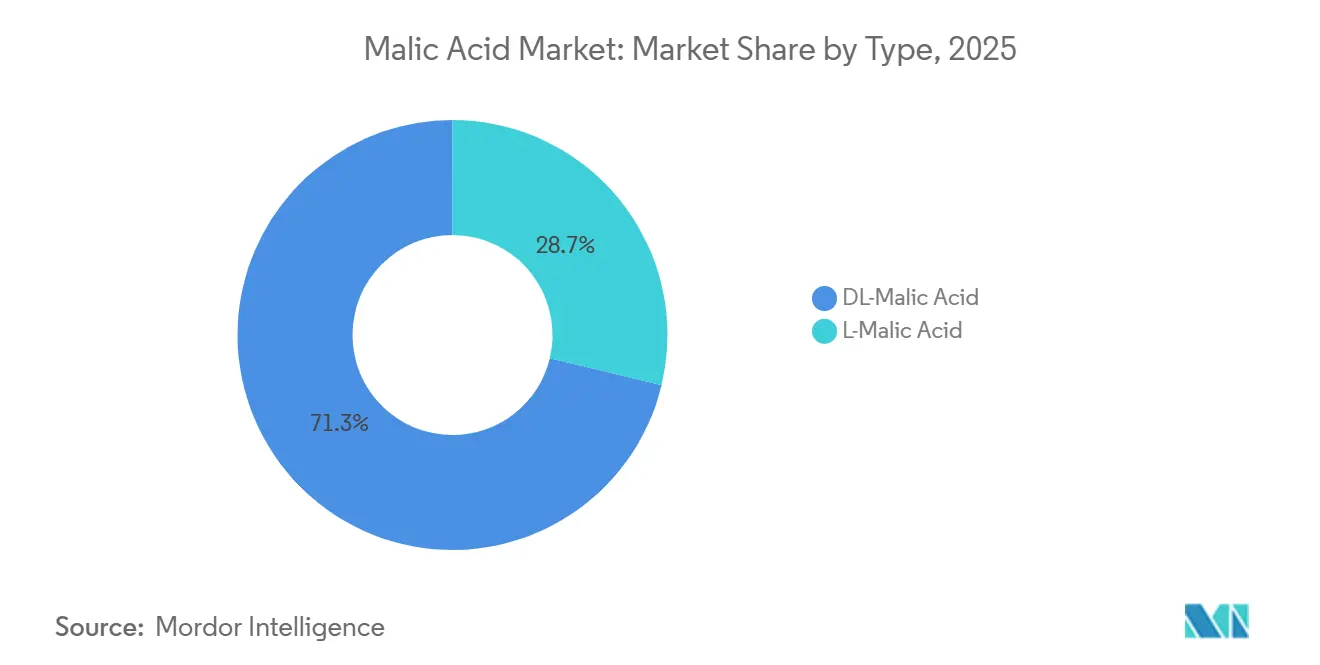

- By type, DL-malic acid led with 71.25% of malic acid market share in 2025, while L-malic acid is forecasted to be the fastest-growing type at a 10.12% CAGR to 2031.

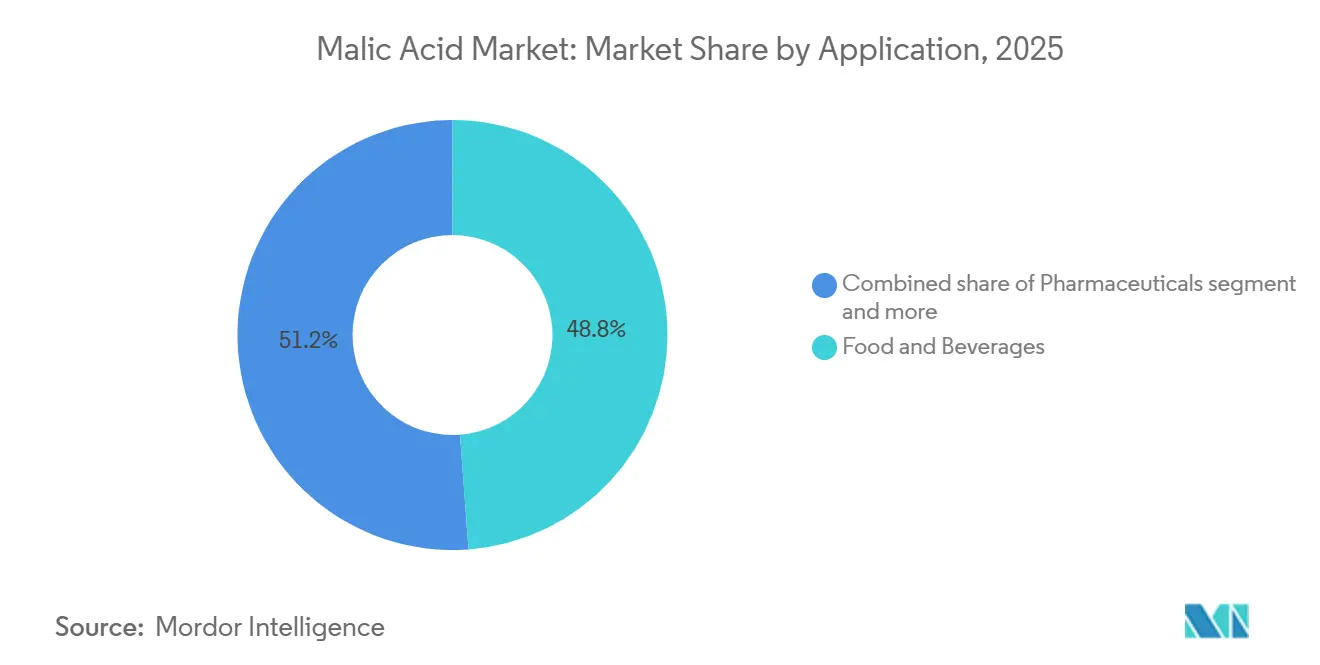

- By application, food and beverages commanded 48.82% of the malic acid market size in 2025 whereas pharmaceuticals are poised to register the highest application CAGR at 9.52% through 2031.

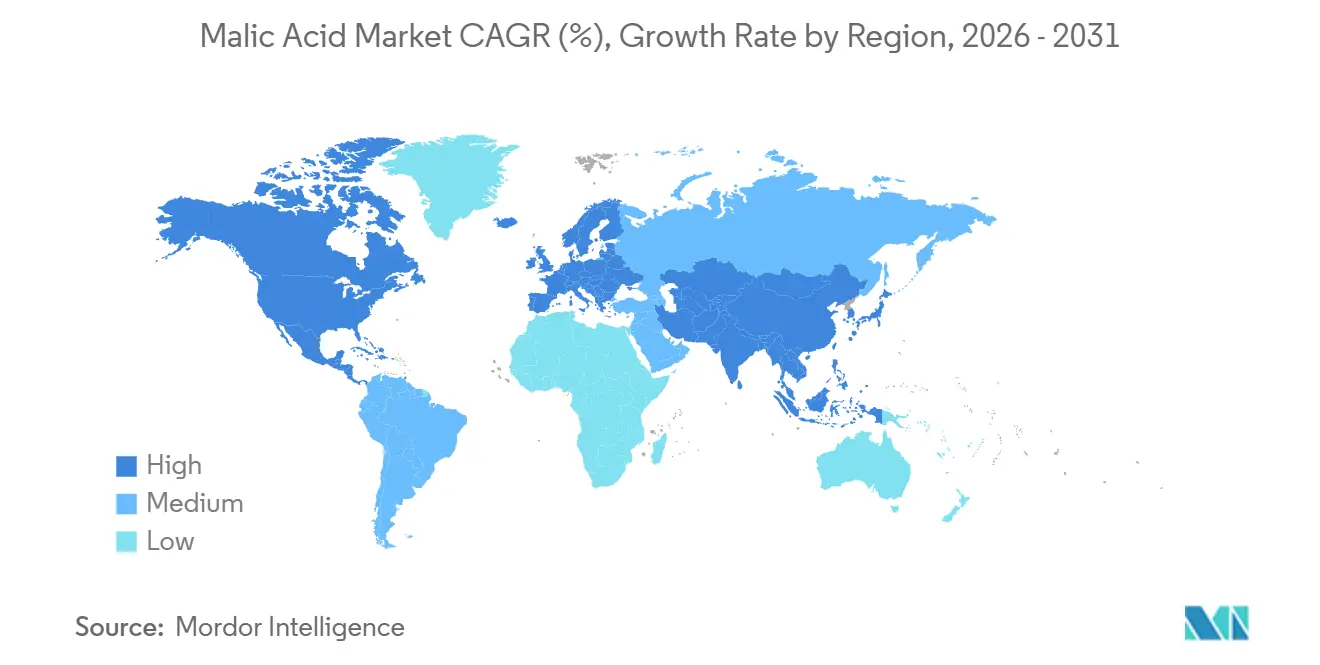

- By geography, North America accounted for 38.45% of malic acid market share in 2025, while Asia-Pacific is projected to match the global 9.18% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Malic Acid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in demand for clean-label and natural food additives | +1.80% | Global, with strongest uptake in North America and Europe | Medium term (2-4 years) |

| Rising global consumption of beverages and confectionery products | +1.50% | Global, led by Asia-Pacific and Latin America | Long term (≥ 4 years) |

| Regulatory push toward natural acidulants | +1.20% | North America, Europe, and Asia-Pacific (India, China) | Short term (≤ 2 years) |

| Surge in low/no-sugar food and beverage products | +1.40% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Cost and performance advantages over alternatives | +1.00% | Global, particularly in cost-sensitive emerging markets | Long term (≥ 4 years) |

| Fermentation-derived "Green" malic acid demand | +1.30% | Europe and North America, early adoption in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in demand for clean-label and natural food additives

Rising demand for clean-label foods is prompting manufacturers to move away from artificial additives toward familiar, naturally sourced ingredients. In this context, malic acid, commonly found in fruits like apples and a key component of metabolic pathways, has emerged as a preferred solution for delivering acidity and flavor balance. Its recognized safety status by the United States Food and Drug Administration (FDA), along with approvals across global regulatory bodies such as European Food safety Authority (EFSA) and Food Safety and Standards Authority of India (FSSAI), provides manufacturers with confidence to incorporate it into diverse formulations. This regulatory clarity supports faster product reformulation, particularly in premium and organic segments where transparency and simplicity drive purchasing decisions. Notably, malic acid is increasingly being used in beverages as a substitute for citric acid, offering a smoother, more rounded tartness that aligns with consumer taste expectations. The International Food Information Council (IFIC) reported in 2024 that 26% of United States consumers define "healthy food" primarily by the term "Natural," while 16% prioritize "Non-GMO" [1]Source: International Food Information Council, "2024 IFIC Food & Health Survey," ific.org. These evolving preferences are reinforcing the adoption of bio-based malic acid, positioning it as a key ingredient in clean-label product innovation.

Rising global consumption of beverages and confectionery products

Rapid growth in beverage and confectionery segments across emerging economies is being fueled by urbanization, rising incomes, and evolving dietary preferences influenced by global trends. In this landscape, malic acid is increasingly favored due to its multifunctional role in enhancing flavor longevity, improving mouthfeel, and stabilizing product quality across applications such as fruit drinks, carbonated beverages, and sour candies. Its relatively higher acidity compared to citric acid enables manufacturers to achieve the desired taste profile with lower inclusion levels, offering a clear cost advantage in price-sensitive markets across Asia-Pacific and Latin America. In reduced-sugar and low-calorie beverages, malic acid plays a critical role in balancing sweetness while maintaining a sharp, refreshing taste, aligning with health-conscious consumer demands. The confectionery sector, particularly gummies and hard candies, is also witnessing strong adoption due to malic acid’s ability to deliver sustained tartness and enhance sensory appeal. Growth is further supported by increasing product innovation and premiumization trends in developing regions. In the United Kingdom, non-alcoholic beverage consumption grew by approximately 10.3% over four years, rising to 15,095 million liters in 2023, reflecting sustained demand growth [2]Source: UNESDA, "United-Kingdom-UNESDA-2024-external," unesda.eu. Additionally, the shift toward functional and fortified beverages is creating new opportunities, as malic acid supports flavor stability and improves mineral uptake in these formulations.

Regulatory push toward natural acidulants

Across global markets, tightening regulations on synthetic additives are accelerating the shift toward naturally sourced acidulants, positioning malic acid as a preferred solution. Reviews conducted by European Food Safety Authority under Regulation (EU) No 257/2010 have reaffirmed the safety and stability of malic acid (E296), strengthening its acceptance in food applications. In the United States, the Food and Drug Administration continues to classify malic acid as GRAS under multiple CFR provisions, enabling flexible usage across formulations. India’s Food Safety and Standards Authority of India also permits its use across diverse food categories, supporting expansion in packaged and processed foods. These aligned regulatory frameworks lower compliance complexity and speed up product commercialization for manufacturers. Importantly, regulatory distinctions between naturally derived and synthetic variants, particularly in the United States, are creating a dual market structure. As a result, fermentation-based L-malic acid is increasingly favored, commanding premium positioning in clean-label and sustainability-driven product segments.

Surge in low/no-sugar food and beverage products

Rising concerns around obesity and diabetes are accelerating the global transition toward reduced-sugar diets, encouraging manufacturers to innovate in low- and no-sugar product formulations. In this landscape, malic acid has emerged as a key ingredient, helping to offset the bitterness or metallic aftertaste of high-intensity sweeteners such as stevia and sucralose while enhancing overall flavor balance. Its smooth and lingering tartness improves sensory appeal, particularly in categories like sports drinks, energy beverages, and functional waters. Beyond taste, malic acid also contributes to metabolic processes by supporting energy production through the citric acid cycle, making it relevant for non-stimulant energy formulations. In 2024, the International Diabetes Federation (IDF) reported that 589 million adults (aged 20–79) were living with diabetes globally, equivalent to nearly 1 in 9 adults, with the condition responsible for 3.4 million deaths, or about one every nine seconds [3]Source: International Diabetes Federation (IDF), "The Diabetes Atlas," diabetesatlas.org. This growing health burden is driving demand for sugar-reduced and functional products, where malic acid plays a dual role as both a flavor enhancer and functional ingredient. Additionally, increasing adoption in pharmaceutical and nutraceutical applications, along with supportive regulatory frameworks promoting sugar reduction, is further strengthening the demand for malic acid across industries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intense competition from alternative acidulants | -1.20% | Global, particularly in cost-sensitive segments | Short term (≤ 2 years) |

| Relentless price undercutting pressuring industry margins | -0.90% | Asia-Pacific and emerging markets | Medium term (2-4 years) |

| Uncertain GRAS limits in functional cosmetics | -0.40% | North America and Europe | Long term (≥ 4 years) |

| Risk of supply-chain concentration | -0.60% | Global, with acute exposure in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intense competition from alternative acidulants

Malic acid faces sustained competitive pressure from structurally similar organic acids such as citric acid, tartaric acid, and fumaric acid across food, beverage, and pharmaceutical applications. Among these, citric acid dominates due to its large-scale production through Aspergillus niger fermentation, enabling significant cost efficiencies that are difficult for malic acid producers to replicate. Fumaric acid further intensifies competition in select applications, particularly in bakery and meat preservation, where its stronger antimicrobial properties provide a functional edge. Meanwhile, tartaric acid continues to hold a strong position in wine production due to its critical role in stabilization processes. The high degree of functional overlap among these acids creates pricing pressure, especially in commodity-grade applications where switching costs remain minimal. Additionally, recent capacity expansions in upstream intermediates like maleic anhydride have led to supply imbalances, compressing malic acid margins. As a result, manufacturers are increasingly focusing on differentiation strategies, highlighting malic acid’s smoother and longer-lasting sourness profile along with its nutritional benefits. However, such value-driven positioning is more effective in premium segments, while cost competition continues to dominate in high-volume markets.

Relentless price undercutting pressuring industry margins

Volatility in key feedstocks, particularly maleic anhydride, continues to exert significant pressure on malic acid producers, with raw materials accounting for nearly half of total production costs for non-integrated players. The market has become increasingly competitive due to aggressive capacity expansions by Chinese manufacturers such as Anhui Sealong and Changmao Biochemical Engineering, who are leveraging scale to offer lower prices and capture global share. This has resulted in a structural decline in unit pricing, as evidenced by rising output but weakening revenues across the industry. Overcapacity in synthetic DL-malic acid has further intensified commoditization, limiting differentiation and forcing producers to compete primarily on cost. Smaller and non-integrated manufacturers remain particularly exposed, as they lack control over upstream inputs and cannot absorb fluctuations in feedstock pricing. In contrast, vertically integrated companies such as Bartek Ingredients and Dialog Group are better positioned to manage cost pressures through secured supply chains. Overall, sustained pricing pressure, combined with uneven cost structures, continues to compress margins and challenge profitability across the global malic acid market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: DL-Malic Acid Dominates Through Cost Efficiency

DL-malic acid continues to dominate the market, accounting for approximately 71.25% share in 2025, primarily due to its cost-effective production through established chemical synthesis routes and its versatility across large-scale food and beverage applications. Its widespread adoption is driven by consistent quality, scalability, and suitability for high-volume usage where pricing efficiency remains a critical factor. Additionally, ongoing capacity expansions in upstream inputs such as maleic anhydride are expected to support steady supply and align DL-malic acid growth with increasing global beverage consumption. This positions the segment as the backbone of the overall market, particularly in applications where functional performance outweighs the need for stereochemical specificity.

In contrast, L-malic acid is emerging as the fastest-growing segment, projected to expand at a CAGR of 10.12% through 2031, fueled by advancements in fermentation technology and rising demand for naturally derived ingredients. Improvements in bio-based production, including high-yield microbial fermentation processes, are gradually reducing cost barriers and enhancing commercial viability. The segment is gaining traction in premium food, nutraceutical, and pharmaceutical applications where stereochemical purity and metabolic compatibility are valued. As consumer preference shifts toward clean-label and non-GMO ingredients, and production efficiencies improve, L-malic acid is expected to capture a larger market share, potentially moderating the dominance of DL variants over the long term.

By Application: Food and Beverages Lead While Pharmaceuticals Accelerate

The food and beverages sector continues to dominate the malic acid market, accounting for 48.82% share in 2025, supported by its widespread application in soft drinks, sour confectionery, and processed food products. Its strong acidulant profile and high solubility make it particularly effective in enhancing tartness while maintaining formulation stability, especially in reduced-sugar and functional beverage categories. Growing demand for sour flavor profiles in confectionery, including gummies and coated candies, has further accelerated usage. Additionally, meat and processed food manufacturers are leveraging malic acid for its antimicrobial properties, enabling shelf-life extension without reliance on synthetic preservatives. This broad applicability across sub-categories reinforces its position as a core ingredient in food processing innovation and product differentiation.

In contrast, the pharmaceutical segment is emerging as the fastest-growing application, projected to expand at a CAGR of 9.52% through 2031, driven by its increasing incorporation in drug formulations, syrups, and effervescent tablets. Its ability to improve taste masking and stabilize active pharmaceutical ingredients enhances its attractiveness in oral dosage forms. Beyond pharma, malic acid is also gaining traction in personal care and cosmetics, where it is used for pH balancing and mild exfoliation, as well as in animal feed, where it supports gut health and feed efficiency. This diversification across high-value and functional applications highlights a clear shift toward multi-industry adoption, strengthening long-term market resilience and opening new growth avenues beyond traditional food uses.

Geography Analysis

North America remains the leading regional market for malic acid, accounting for approximately 38.45% of global share. This strong position is driven by highly integrated production ecosystems, including large-scale facilities that enhance capacity while significantly lowering environmental impact. Strategic industry developments, such as partnerships and acquisitions, are further enabling product portfolio expansion and cross-industry synergies in food ingredients. Demand is reinforced by the region’s mature food and beverage sector, where clean-label formulations and premium ingredients are increasingly prioritized. Additionally, regulatory clarity and well-defined safety standards support consistent adoption across applications. Continuous innovation in beverages and processed foods also sustains downstream demand across the region.

Asia-Pacific is emerging as the fastest-growing region, projected to expand at a CAGR of 9.18% through 2030. Growth is fueled by large-scale capacity additions across key manufacturing hubs, improving the region’s role as a global supply base. Countries like China continue to dominate production, although pricing dynamics are influenced by periods of oversupply. Meanwhile, markets such as Japan focus on specialized, high-purity variants catering to pharmaceuticals and performance nutrition segments. Rapid urbanization, rising disposable incomes, and increasing consumption of packaged food and beverages further drive demand. Advancements in fermentation-based production technologies are also helping reduce costs and improve product efficiency, strengthening regional competitiveness.

Europe maintains a stable and well-established presence in the malic acid market, supported by stringent regulatory frameworks and a strong preference for high-quality, compliant ingredients. The region emphasizes sustainability, encouraging the shift toward bio-based production processes and environmentally responsible sourcing. Ongoing investments in product innovation and application development, particularly in confectionery and specialty food segments, support steady demand. At the same time, diversification strategies among key manufacturers are expanding their ingredient portfolios beyond traditional organic acids. In contrast, South America and the Middle East & Africa represent early-stage but promising markets, where growing urban populations, increasing consumption of packaged products, and gradual industrial development are expected to unlock future growth opportunities.

Competitive Landscape

The global malic acid market exhibits a moderately consolidated structure, with a handful of leading producers accounting for a significant share of installed capacity. Key companies such as Bartek Ingredients Inc., Fuso Chemical Co., Ltd., Jungbunzlauer Suisse AG, Tate & Lyle PLC, Thirumalai Chemicals, and Anhui Sealong Biotechnology leverage strong operational scale, integrated supply chains, and extensive distribution networks to sustain competitive advantage. Strategic backward integration, particularly in feedstock sourcing, enables cost control and protects margins from raw material price fluctuations. This concentration results in a balanced competitive intensity, where established players maintain dominance while still facing pressure from regional manufacturers.

Sustainability and process innovation are increasingly shaping competitive positioning within the industry. Leading manufacturers are prioritizing low-emission production techniques and alternative feedstock utilization to reduce environmental impact and improve cost efficiency. At the same time, advancements in biotechnology are accelerating the shift toward fermentation-based production methods. The development of engineered microbial strains capable of producing high yields of L-malic acid at commercial scale is opening new avenues for bio-based manufacturing. This transition not only aligns with global sustainability goals but also introduces new entrants focused on green chemistry and fermentation expertise.

Competitive dynamics are further influenced by pricing strategies and regulatory requirements. Manufacturers in China are intensifying price competition, although limited vertical integration can expose smaller players to volatility in input costs. Additionally, compliance with international quality and safety standards such as ISO and food safety certifications has become essential for accessing global markets, creating entry barriers for new participants. Recent strategic investments and acquisitions, including capacity expansions and consolidation moves by larger chemical groups, indicate growing confidence in long-term demand. Emerging opportunities are particularly strong in high-value applications such as pharmaceuticals and cosmetics, as well as in rapidly expanding regions like Asia-Pacific and Latin America.

Malic Acid Industry Leaders

-

Bartek Ingredients Inc.

-

Fuso Chemical Co., Ltd.

-

Tate & Lyle PLC

-

Jungbunzlauer Suisse AG

-

Anhui Sealong Biotechnology

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: ICL Group announced the acquisition of Bartek Ingredients to strengthen its position in specialty food ingredients, particularly malic and fumaric acid used in food and beverages. The deal is structured in two phases, starting with a approximate USD 90 million investment for a 50% stake (Q1 2026), with full acquisition planned later to expand capacity and global market reach.

- November 2024: NNB Nutrition launched a moisture-resistant DL-malic acid using FlowTech™ technology to prevent clumping and ensure free-flowing stability in humid conditions. The innovation claims to enhance shelf life, blending consistency, and processing efficiency for food and beverage applications like drinks, confectionery, and baked goods.

- September 2024: Bartek Ingredients completed its malic and fumaric acid facility in Stoney Creek, Ontario, becoming the largest such facility globally. The plant, constructed in partnership with WSP engineering, doubled the company's production capacity. The facility achieved an 80% reduction in greenhouse gas emissions per unit of production, establishing new environmental standards in acidulant manufacturing.

Global Malic Acid Market Report Scope

| L-Malic Acid |

| DL-Malic Acid |

| Food and Beverages | Beverages |

| Bakery and Confectionery | |

| Meat Produts | |

| Other Food and Beverages | |

| Personal Care and Cosmetics | |

| Pharmaceuticals | |

| Animal Feed |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | L-Malic Acid | |

| DL-Malic Acid | ||

| By Application | Food and Beverages | Beverages |

| Bakery and Confectionery | ||

| Meat Produts | ||

| Other Food and Beverages | ||

| Personal Care and Cosmetics | ||

| Pharmaceuticals | ||

| Animal Feed | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the market size of malic acid in 2025 and what is its projected market size?

The malic acid market size is projected to expand from USD 380.74 million in 2025 to USD 638.50 million in 2031.

Which region leads global demand?

North America holds the largest share at 38.45%, supported by clean-label regulations and advanced food processing infrastructure.

Which application is expanding fastest?

Pharmaceuticals are projected to record the highest growth at 9.52% CAGR on rising excipient demand.

Why is L-malic acid gaining momentum?

Fermentation cost breakthroughs and consumer preference for naturally derived ingredients drive L-malic acid’s 10.12% CAGR.

Page last updated on: