Benzoic Acid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

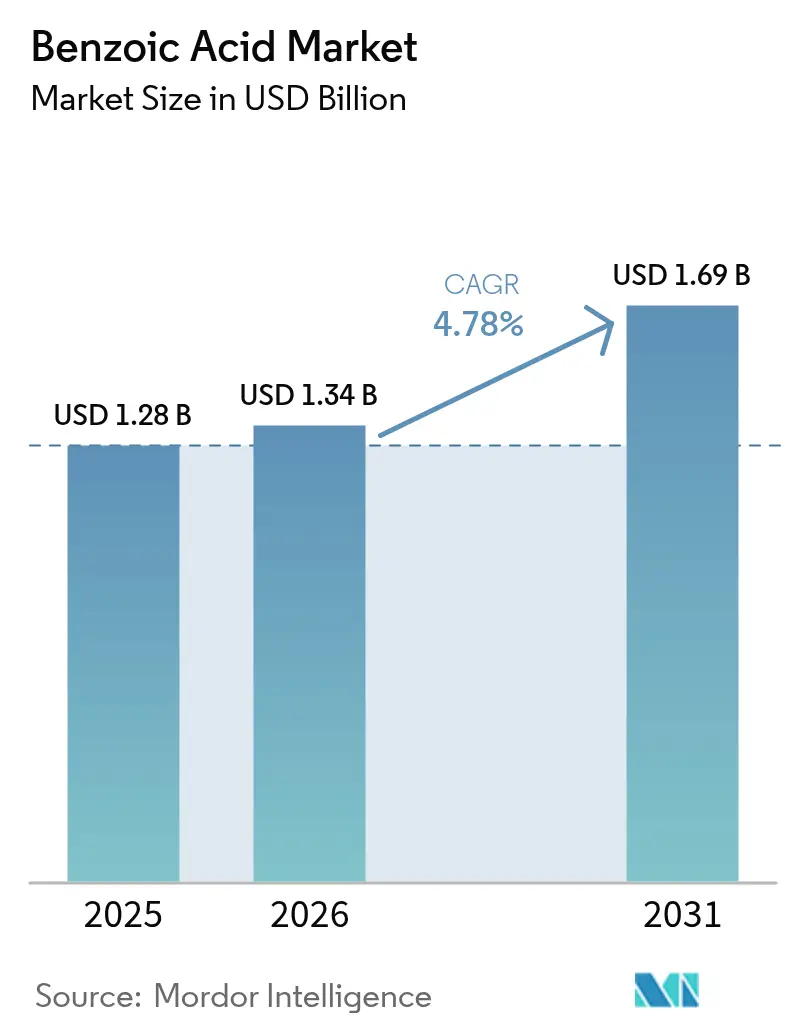

| Market Size (2026) | USD 1.34 Billion |

| Market Size (2031) | USD 1.69 Billion |

| Growth Rate (2026 - 2031) | 4.78% CAGR |

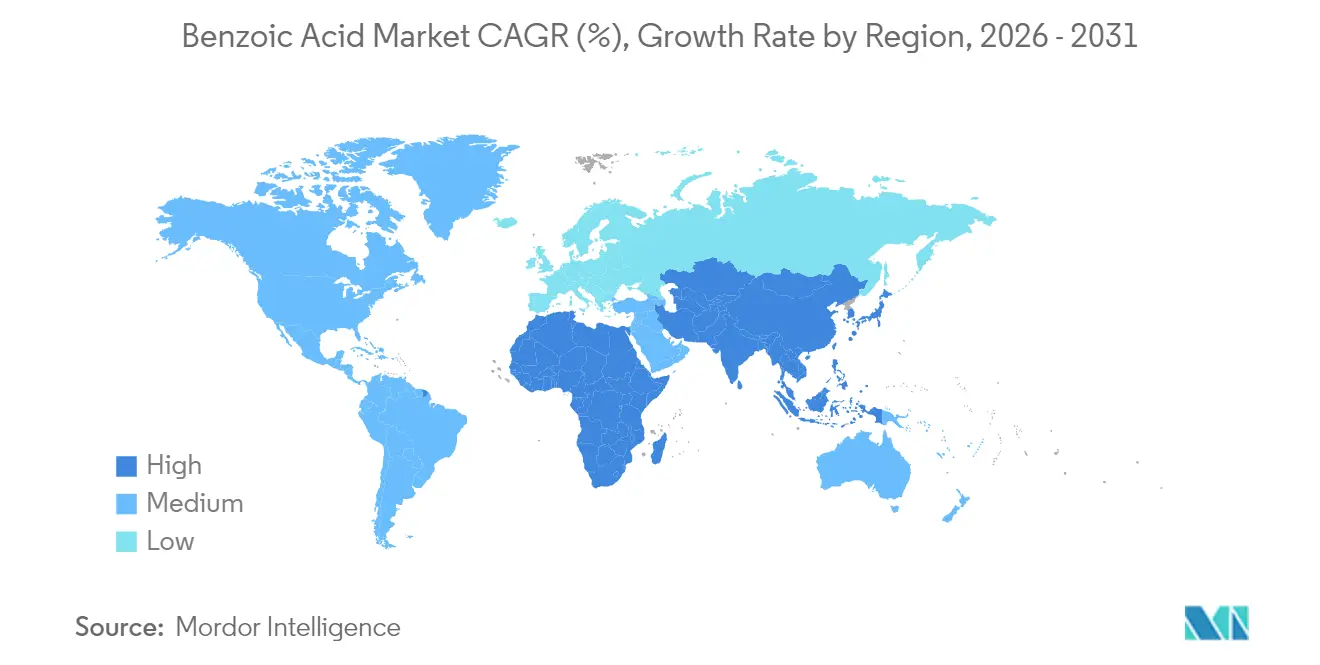

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Benzoic Acid Market Analysis by Mordor Intelligence

The benzoic acid market size is expected to grow from USD 1.28 billion in 2025 to USD 1.34 billion in 2026 and is forecast to reach USD 1.69 billion by 2031 at 4.78% CAGR over 2026-2031. The market growth is driven by regulations that focus on extended shelf-life requirements, phthalate replacement, and high-purity manufacturing processes. The European Union's stricter food-contact regulations and the United States Food and Drug Administration's removal of 25 ortho-phthalate plasticizers create new opportunities in food, pharmaceutical, and plasticizer applications. The Asia-Pacific region maintains its production dominance, while the Middle East and Africa show the highest growth rate due to food processing industrialization. The market sees increasing adoption of liquid formulations, ultra-high purity grades, and benzoate plasticizers, driven by ease of handling, pharmaceutical quality requirements, and regulatory support. The competitive landscape remains moderate, with global companies and regional suppliers sharing market presence, leading to advancements in green chemistry and continuous processing.

Key Report Takeaways

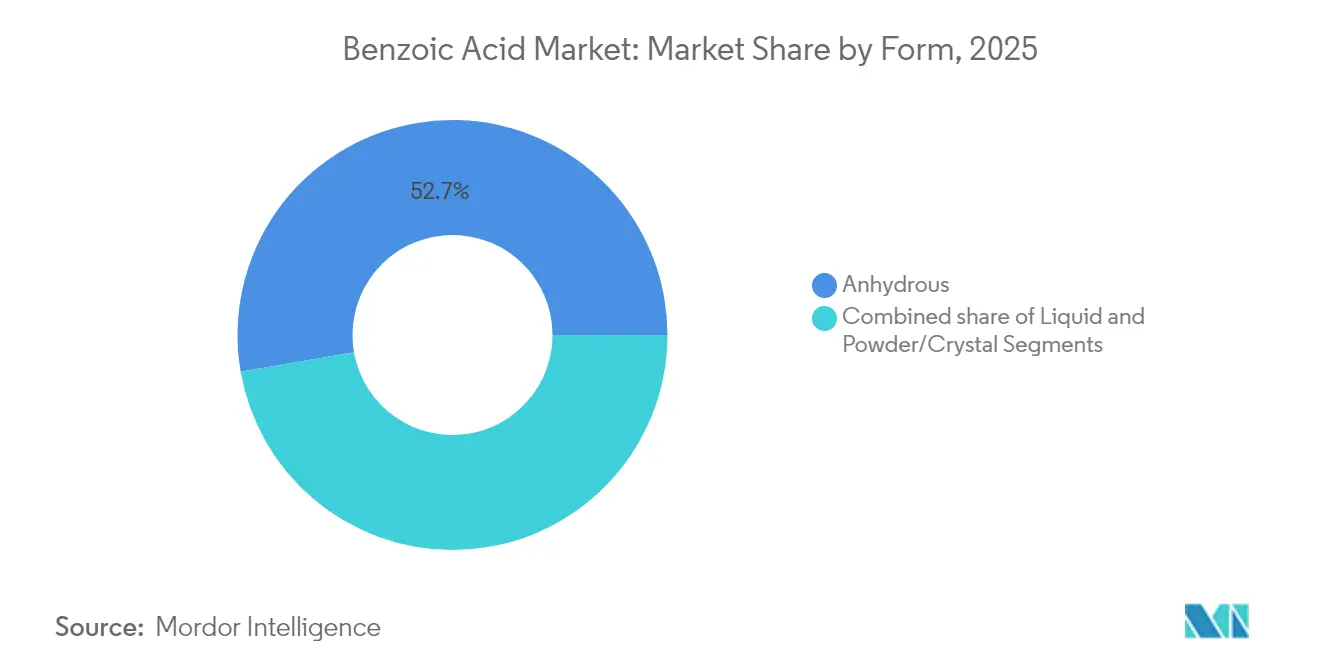

- By form, anhydrous forms led with 52.74% revenue share in 2025, while liquid formulations recorded the fastest 6.09% CAGR through 2031.

- By purity grade, 99.5-99.9% grades held 62.21% of the benzoic acid market share in 2025, and grades above 99.9% expand at a 6.88% CAGR through 2031.

- By derivative, sodium benzoate accounted for 46.21% of the benzoic acid market size in 2025, whereas benzoate plasticizers advanced at 6.58% CAGR through 2031.

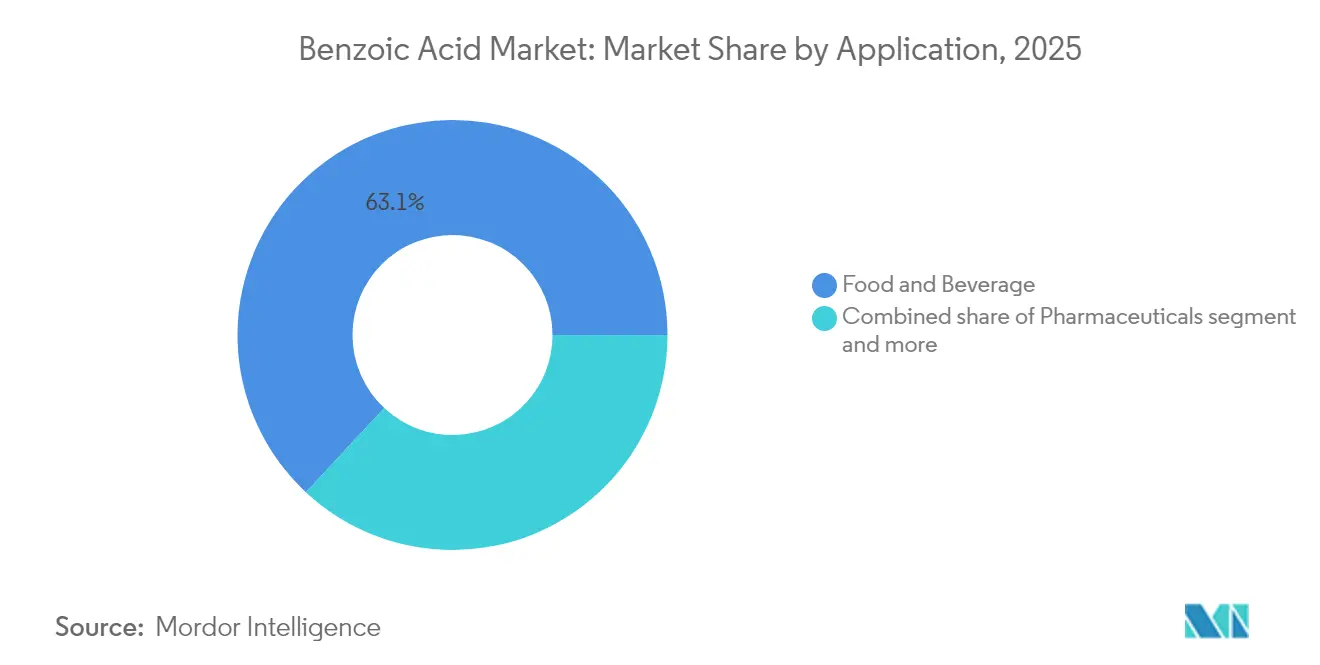

- By application, food and beverage dominated with 63.05% share in 2025; pharmaceuticals grew the fastest at 6.18% CAGR through 2031.

- By geography, Asia-Pacific captured 41.87% of the benzoic acid market share in 2025; the Middle East and Africa posts the strongest 6.49% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Benzoic Acid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory push for longer shelf-life pharmaceuticals in emerging economies | +1.2% | Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Expansion of benzoyl chloride usage in agrochemical synthesis | +0.8% | Global, concentrated in China and India | Long term (≥ 4 years) |

| Substitution of phthalate plasticizers with benzoate-based alternatives | +1.1% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Growing demand for high-purity benzoic acid for specialty coatings | +0.7% | North America and Europe | Medium term (2-4 years) |

| Rise in demand for packaged and convenience foods | +0.9% | Global | Long term (≥ 4 years) |

| Technological advancements in production | +0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory push for longer shelf-life pharmaceuticals in emerging economies

Pharmaceutical regulators in emerging markets are implementing stricter shelf-life requirements, increasing the demand for benzoic acid. The focus on extended product stability is significant in liquid formulations, where benzoic acid prevents microbial growth and extends shelf life by inhibiting bacterial and fungal contamination. This regulatory trend drives consistent demand growth in the pharmaceutical sector, particularly in countries like China, India, and Brazil, where healthcare regulations are becoming more stringent. The alignment of regulations across Asia-Pacific markets positions benzoic acid as a key preservative, particularly in oral and parenteral formulations that require compatibility with active pharmaceutical ingredients. These formulations include oral solutions, suspensions, injectable medications, and other liquid pharmaceutical products. The safety requirements for neonatal applications are increasing demand for higher purity grades, with specifications of purity, supporting growth in ultra-high purity segments. This demand is further driven by the growing focus on pediatric medications, the need for contamination-free preservatives in sensitive pharmaceutical applications, and the increasing adoption of benzoic acid in novel drug delivery systems. The pharmaceutical industry's emphasis on quality control and regulatory compliance has led to increased investment in advanced purification technologies and testing methods to ensure benzoic acid meets these stringent requirements.

Expansion of benzoyl chloride usage in agrochemical synthesis

Benzoyl chloride, a benzoic acid derivative, is a key component in manufacturing herbicides and fungicides, particularly chloramben analogs that control resistant weeds and improve crop yields. The compound's properties allow manufacturers to develop specific formulations that address pest resistance while maintaining crop safety. Indian formulators and Chinese contract manufacturers are expanding their production capabilities by implementing improved process controls and quality systems to meet global agrochemical companies' requirements for products with specific impurity profiles. These manufacturing enhancements include better filtration systems, automated monitoring, and comprehensive quality testing protocols. Research into amide-bearing sulfonate derivatives has increased due to the agricultural sector's sustainability focus. Laboratory studies show these derivatives achieve higher lethal-concentration effectiveness against target organisms compared to conventional active ingredients, potentially reducing application rates while maintaining pest control efficiency. The market growth depends on achieving cost-effectiveness while meeting environmental regulations and safety requirements, and maintaining consistent demand for benzoic acid in the agricultural chemical supply chain. The industry continues to invest in benzoyl chloride-based solutions for developing new crop protection products.

Substitution of phthalate plasticizers with benzoate-based alternatives

The FDA's decision to remove 25 ortho-phthalate plasticizers from food additive regulations has created significant market opportunities for benzoate-based alternatives.[1]Source: FDA, "Phthalates in Food Packaging and Food Contact Applications", fda.gov The agency's comprehensive post-market review of chemical safety in food applications is accelerating this transition by identifying potential health risks, establishing new safety standards, and evaluating long-term environmental impacts. The EU's Regulation (EU) 2025/351 has implemented more stringent purity requirements and specific migration limits for plastic food contact materials, providing substantial compliance advantages for benzoate plasticizers compared to traditional phthalate compounds.[2]Source: European Commission, "COMMISSION REGULATION (EU) 2025/351 ", eur-lex.europa.eu The regulation specifically addresses chemical leaching concerns and sets benchmarks for material degradation over time. California's Safer Food Packaging Act of 2025 will implement a complete ban on ortho-phthalates in food packaging from January 1, 2027, establishing a definitive timeline for industry transition and requiring manufacturers to demonstrate compliance through rigorous testing protocols.[3]Source: Bureau Veritas, "California Proposes Bill Banning Chemicals in Food Packaging", cps.bureauveritas.com These regulatory changes across multiple jurisdictions are driving the substantial growth of benzoate plasticizers, as manufacturers actively seek compliant alternatives that maintain essential performance standards while meeting sustainability goals.

Growing demand for high-purity benzoic acid for specialty coatings

The demand for ultra-high purity benzoic acid grades (above 99.9%) is increasing, primarily driven by advanced coating applications that require enhanced performance characteristics and strict regulatory compliance. These high-purity grades are essential in electronic coatings, pharmaceutical packaging, and specialized industrial applications where impurities could compromise product integrity. Cornell University's development of a process to convert polystyrene waste into benzoic acid using light and oxygen represents a significant advancement in sustainable production methods, offering potential cost advantages and reduced environmental impact. The automotive and construction industries' growing need for high-performance materials containing benzoic acid derivatives is expanding the market in developed economies, especially in applications requiring weather resistance and long-term durability. The emergence of bio-based production methods, including Covestro's development of bio-based aniline from plant biomass, indicates potential new pathways for sustainable benzoic acid production, addressing growing environmental concerns and regulatory pressures for greener manufacturing processes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift towards clean-label preservatives limiting synthetic benzoate adoption | -0.9% | North America and Europe, expanding globally | Medium term (2-4 years) |

| Price volatility of raw materials | -0.6% | Global | Short term (≤ 2 years) |

| Health and safety concerns | -0.4% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Competition from natural preservatives | -0.7% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift towards clean-label preservatives limiting synthetic benzoate adoption

The growing consumer preference for natural ingredients is compelling food manufacturers to seek alternatives to synthetic preservatives, including sodium benzoate. European market data indicates rising demand for clean-label products that offer transparency in ingredient sourcing and manufacturing processes, with consumers increasingly scrutinizing product labels and demanding natural alternatives. Natural antimicrobial compounds, including plant extracts, essential oils, and microbial metabolites, have emerged as potential replacements for synthetic preservatives. These natural compounds demonstrate effectiveness in controlling foodborne pathogens while aligning with consumer preferences for clean-label products. The meat industry has shown significant interest in natural preservatives, extensively exploring options such as bacteriophages, bacteriocins, and antimicrobial peptides as substitutes for synthetic chemicals. These alternatives have demonstrated promising results in laboratory and commercial settings. However, the widespread adoption of natural alternatives faces limitations due to standardization challenges, higher production costs, and varying antimicrobial efficacy across different food applications. The regulatory environment, particularly in the EU, is shifting toward favoring natural ingredients through stricter guidelines and approval processes for synthetic preservatives, which presents both opportunities and challenges for benzoic acid manufacturers in terms of market adaptation and product development.

Price volatility of raw materials

The market for synthetic benzoic acid faces increasing competition from naturally occurring antimicrobial compounds. Research demonstrates that organic acids from plant sources effectively extend shelf life and improve food safety by inhibiting bacterial growth and preventing spoilage. Health concerns associated with sodium benzoate, including its potential links to asthma, allergies, and hyperactivity in children, have led consumers to seek natural alternatives in food and beverage products. Antimicrobial photodynamic therapy (aPDT), which uses natural photosensitizers such as curcumin and riboflavin, has proven effective in reducing microbial growth in food products by providing preservation methods that meet clean-label requirements. The FDA's Generally Recognized as Safe (GRAS) classification for many natural preservatives strengthens their market position and consumer acceptance across various food categories, including dairy, bakery, and beverages. Synthetic benzoic acid manufacturers must now demonstrate superior cost-effectiveness and consistent performance compared to natural alternatives, particularly for applications requiring long-term preservation and broad-spectrum antimicrobial protection against bacteria, yeasts, and molds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Liquid Gains Momentum Despite Anhydrous Dominance

The benzoic acid market for anhydrous grades held a dominant 52.74% market share in 2025, supported by its extensive applications across industries. Anhydrous powders serve as the preferred choice for dry-mix foods, polymer catalysts, and granular animal-feed blends, owing to their low moisture absorption and efficient bulk storage properties. These characteristics help maintain product stability and quality during storage periods. The liquid forms segment is growing at a 6.09% CAGR, driven by processing efficiency and operational benefits. Pharmaceutical syrup manufacturers use liquid benzoic acid solutions to streamline production processes by eliminating on-site dissolution steps and maintaining precise assay tolerances, which reduces batch variations and improves product consistency. Industrial coating manufacturers achieve faster homogenization by using liquids in high-shear reactors, reducing production time and improving efficiency.

Process intensification has significantly improved liquid uptake capabilities in manufacturing processes. Comprehensive laboratory tests indicate that liquid benzoic acid functions more effectively as a chain-stop agent in alkyd resins, resulting in enhanced gloss retention and surface finish quality. These substantial performance improvements, combined with reduced dust emissions during handling and processing, support the segment's stronger growth trajectory compared to the overall benzoic acid market. The improved efficiency in liquid form has also led to reduced processing times and better integration in various industrial applications, further strengthening its market position.

By Purity Grade: Ultra-High Purity Drives Premium Applications

The 99.5-99.9% purity segment dominates with 62.21% market share in 2025, primarily due to its widespread use in critical manufacturing processes. Ultra-high purity grades above 99.9% are growing at 6.88% CAGR through 2031, driven by increasing demand from specialty coating and pharmaceutical applications requiring stringent quality specifications. The pharmaceutical industry requires higher purity grades, especially for parenteral formulations that must meet strict pharmacopeial standards for patient safety and regulatory compliance. Research into bio-based production methods is developing innovative processes for ultra-high purity levels while maintaining cost efficiency, supported by advanced purification technologies including membrane separation and chromatographic techniques.

The 99.0-99.5% purity grade meets essential requirements for food preservation and basic industrial applications, offering reliable performance at competitive price points. This grade finds extensive use in general manufacturing processes where ultra-high purity is not critical. Manufacturers are implementing sophisticated analytical methods and comprehensive quality control systems to achieve higher purity specifications consistently, supporting premium segment growth while optimizing operational efficiency and production yields.

By Derivative: Benzoate Plasticizers Lead Innovation Wave

Sodium benzoate maintained a dominant 46.21% revenue share in 2025, primarily due to its extensive use in acidic foods and beverages, including carbonated drinks, fruit juices, pickles, and condiments. The market demonstrates significant shifts, with benzoate plasticizers achieving a 6.58% CAGR as manufacturers transition away from ortho-phthalates in response to environmental and health concerns. Film manufacturers report successful transitions to benzoate esters with minimal adjustments to seal temperatures during the conversion process, typically requiring only minor equipment modifications and process parameter adjustments. The demand for potassium benzoate continues to increase in low-sodium food formulations, particularly in developed markets with strict dietary guidelines targeting reduced sodium consumption.

The market demonstrates growth through multiple segments, with benzoyl chloride derivatives driving development in agricultural chemicals, specifically in herbicide and pesticide formulations. Benzyl benzoate maintains stable demand in both scabies treatment applications and fragrance stabilization for perfumes and personal care products, despite lower volumes compared to other derivatives. Manufacturers across all segments focus on developing products with reduced volatile organic compounds (VOCs), enhanced thermal stability at processing temperatures, and controlled migration properties to comply with increasingly stringent food contact and environmental regulations, supporting continued diversification in the benzoic acid market.

By Application: Pharmaceuticals Accelerate Growth Trajectory

The food and beverage sector maintains market dominance with a substantial 63.05% share in 2025. China's implementation of new food additive standards (GB 2760-2024) has established comprehensive usage parameters for benzoic acid in pharmaceutical formulations, supporting significant market growth in the country's rapidly expanding pharmaceutical sector. This regulatory framework particularly benefits manufacturers developing oral liquid medications and injectable solutions. The pharmaceutical segment is growing at 6.18% CAGR through 2031, propelled by increasingly stringent shelf-life requirements in emerging economies and the expanding applications in liquid pharmaceutical formulations.

The personal care and cosmetics industry extensively utilizes benzoic acid for its broad-spectrum antimicrobial properties, backed by widespread regulatory approvals across major markets. In animal feed applications, the compound is increasingly recognized for its dual benefits of enhancing growth performance and improving nitrogen metabolism efficiency in livestock production systems. The chemical industry employs benzoic acid as a crucial intermediate in numerous synthesis processes, contributing to the production of various downstream chemical products. While the food and beverage segment maintains its dominant position through widespread preservation applications, its growth rate is moderating as consumer preferences shift toward clean-label products in developed markets, prompting manufacturers to explore alternative preservation methods.

Geography Analysis

Asia-Pacific held 41.87% of the global market in 2025, with China's large-scale aromatic complexes, including Zhejiang Petroleum & Chemical's 11.8 million-ton facility, providing substantial toluene feedstock supply. The region's processors utilize export-oriented regulations and integrated logistics networks to optimize distribution channels and reduce operational costs. India's expanding pharmaceutical and food-processing sectors increase demand through multiple applications, including preservatives and intermediates, while Japan's technological capabilities enable the production of high-quality grades for electronic coatings and specialized industrial applications. ASEAN countries utilize duty-free trade agreements to establish distribution centers for exports to Europe and North America, integrating the benzoic acid market into regional supply chains and creating value-added opportunities for local manufacturers.

The Middle East and Africa region exhibits the highest growth rate at 6.49% CAGR, supported by increasing urbanization driving demand for preserved food products, beverages, and personal care items, alongside government initiatives attracting polymer manufacturers through tax incentives and infrastructure development. Saudi Arabia's test facilities assess benzoate plasticizers for PVC cable insulation production, supporting domestic manufacturing requirements and reducing import dependency.

North America benefits from FDA regulatory framework and manufacturer preferences for phthalate-free packaging solutions across food, beverage, and consumer goods sectors. Europe's market adapts to Regulation (EU) 2024/3190 on bisphenol limitations, encouraging packaging manufacturers to adopt benzoate alternatives in food contact materials and consumer packaging, while recycling requirements affect cost considerations and material selection processes.

Regulatory Landscape

Benzoic acid is widely permitted for use as a preservative and intermediate, but compliance requirements vary by end use (food, feed, and food contact). In the United States, benzoic acid is affirmed as GRAS under 21 CFR 184.1021 for use as an antimicrobial and flavoring agent, subject to good manufacturing practice, and it is commonly used at levels not exceeding 0.1% in food. It also appears in FDA food contact substance frameworks (including uses referenced under 21 CFR 175.300 and 21 CFR 177.1390), which drives the specification and documentation needs for packaging-linked applications.

In the European Union, benzoic acid (E 210) is authorized as a food additive under Regulation (EC) No 1333/2008 and is governed by the common authorization procedure under Regulation (EC) No 1331/2008, with EFSA providing scientific oversight on additives and their specifications. Beyond food, the EU strengthened the feed-side regulatory anchor in June 2024 through Implementing Regulation (EU) 2024/1730, which authorizes benzoic acid as a feed additive for certain pig categories (zootechnical additive 4d210), with conditions of use and an authorization validity extending to 5 August 2030. This supports continued industrial demand tied to compliant feed applications.

Value Chain Analysis

The benzoic acid value chain starts with aromatic feedstocks, primarily toluene, and then moves through oxidation-based manufacturing (commonly liquid-phase toluene oxidation) into benzoic acid grades that are further processed into derivatives such as sodium benzoate (E 211), potassium benzoate (E 212), benzoyl chloride, benzyl benzoate, and benzoate plasticizers. Integrated petrochemical hubs that secure toluene supply underpin cost-competitive production, while downstream conversion and formulation steps (neutralization to benzoates, purification to higher grades, and liquid formulation) create differentiation across food, pharma, coatings, and polymer end markets.

Quality, safety, and environmental management requirements act as gatekeepers throughout the chain, shaping supplier qualification and route-to-market. Food and pharmaceutical-facing suppliers typically align to regulatory specifications and certifications, including FDA compliance for food use under 21 CFR 184.1021 and EU specification controls under EFSA-aligned frameworks. Operational upgrades such as DCS-controlled oxidation, FSSC 22000, and ZLD/effluent controls are used to win export and regulated-market business. For example, MiSa Finechem (India) highlights DCS-controlled toluene oxidation with FSSC 22000 and FDA certifications, while UJWAL PHARMA (India) emphasizes an FSSAI-approved facility with zero liquid discharge processes for E210/E211/E212 supply. Distribution is usually supported by direct contracts with large food, pharma, and polymer customers, with regional distributors handling smaller-lot, higher-purity, or specialty derivative demand.

Competitive Landscape

The benzoic acid market consists of large integrated chemical companies and regional suppliers operating across multiple geographies. The market concentration score of 4 indicates that the top five manufacturers control a significant share of production capacity, enabling mid-sized companies to gain market share through cost efficiencies, technical innovations, and deep customer relationships. Eastman Chemical's USD 375 million investment in a second molecular-recycling facility for producing purified aromatic feedstock for benzoic acid production demonstrates the industry's significant shift toward sustainable and circular supply chains.

The wide application scope of benzoic acid across industries has driven manufacturers to introduce new products to strengthen their market position. Major companies, including Lanxess AG, I G Petrochemicals Ltd. (IGPL), Merck Group, Chemcrux Enterprises Ltd, among others, are expanding their product portfolios to serve more application segments and increase their market share. These manufacturers have increased their research and development activities to develop specialized products that meet specific industry requirements.

Chinese manufacturers leverage economies of scale and proximity to raw materials but experience margin constraints due to domestic overcapacity, leading to substantial industry consolidation and strategic partnerships. European specialty manufacturers focus on high-purity (≥99.9%) products, maintaining extensive long-term contracts with pharmaceutical companies and investing in advanced purification technologies. Industry-wide collaborations with packaging and coating formulators help streamline derivative product approvals through comprehensive testing programs, securing downstream market adoption and strengthening the benzoic acid market structure through integrated value chains.

Benzoic Acid Industry Leaders

-

Lanxess AG

-

Eastman Chemical Company

-

Wuhan Youji Industry Co., Ltd.

-

BASF SE

-

JQC(Huayin) Pharmaceutical Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory-driven substitution in packaging and polymers continues to create opportunities for benzoate plasticizers and higher-purity benzoic acid streams, particularly where food contact and migration performance must be documented. The EU tightening of food-contact related requirements referenced in the report context (including Regulation (EU) 2025/351) and the FDA action removing 25 ortho-phthalate plasticizers from food additive regulations are pushing converters toward phthalate-free alternatives, pulling through benzoic acid demand via benzoate ester value chains. This is further reinforced by state-level timelines such as California's Safer Food Packaging Act of 2025, which bans ortho-phthalates in food packaging from January 1, 2027.

In food and beverages, the opportunity is in supporting brands under clean-label pressure while maintaining shelf-life, particularly in acidic products where benzoates remain cost-effective and widely permitted (including GRAS status under 21 CFR 184.1021 in the United States and EU authorization of E 210 under Regulation (EC) No 1333/2008). This is creating room for technical services and formulation work, including hybrid preservation strategies and dosage optimization that reduce total additive load while targeting microbial control, consistent with ongoing research into hurdle technologies and data-driven process control. A separate opportunity sits in ultra-high purity material (above 99.9%) for regulated and performance-sensitive applications, including pharmaceutical liquids and specialty coatings, where tighter impurity control and validated supply chains support premium pricing and more stable customer relationships.

Recent Industry Developments

- April 2026: Eastman implemented a price increase for specific acids in North America effective April 1, 2026. The change highlights continued feedstock and operating-cost sensitivity for organic acids, which affects benzoic acid and derivative pricing strategies and contract negotiations across the region.

- September 2025: LANXESS transitioned production of benzoic acid and key derivatives (including sodium benzoate) at its Botlek site in the Netherlands to 100% low-emission electricity. The update supports lower-product-footprint sourcing for downstream food, personal care, and industrial customers that are tightening supplier carbon requirements.

- April 2024: Eastman increased prices for benzoic acid technical grade across North America and Latin America effective April 1, 2024. This adjustment underscored the linkage between benzoic acid economics and input costs such as raw materials and energy, shaping near-term procurement behavior and supplier qualification efforts.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the benzoic acid market covers the value of commercially sold benzoic acid supplied to end users for preservation, synthesis, and industrial uses, tracked across major producing and consuming regions and valued in USD terms.

Scope exclusions: We exclude downstream finished products that contain benzoic acid, and we avoid counting benzoate salts as standalone markets when they are priced and traded separately.

Segmentation Overview

-

By Form

- Liquid

- Anhydrous

- Powder/Crystal

-

By Purity Grade

- 99.0–99.5%

- 99.5–99.9%

- Above 99.9%

-

By Derivative

- Sodium Benzoate

- Potassium Benzoate

- Benzyl Benzoate

- Benzoyl Chloride

- Benzoate Plasticizers

- Other Derivatives

-

By Application

-

Food and Beverage

- Bakery

- Confectionery

- Dairy

- Beverage

- Sauces and Dressings

- Others

- Pharmaceuticals

- Chemicals

- Personal Care and Cosmetics

- Animal Feed

- Others

-

Food and Beverage

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- United Kingdom

- Germany

- France

- Russia

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- India

- China

- Japan

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle-East and Africa

- South Africa

- Saudi Arabia

- Rest of Middle-East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the industry boundaries and to anchor the model with observable signals that can be checked year to year. We relied on public sources such as UN Comtrade trade statistics, national customs and statistical agencies, environmental and chemical safety regulators (such as the US EPA and ECHA), and peer-reviewed chemistry and process journals that discuss typical routes and yields. Where available, industry association publications and conference proceedings were used to sense-check demand patterns linked to preservatives and chemical intermediates.

To translate these signals into a usable sizing model, we combined trade and production direction with company filings, investor presentations, and reputable press that discusses capacity moves and utilization swings. A paid subscription for company financials and another for patent databases were used selectively to confirm plant ownership changes and technology focus, and then the assumptions were re-checked against public disclosures. The desk sources listed here are illustrative only, and we used additional public references to collect and validate data, and to clarify gaps.

Primary Interviews and Surveys

Primary work focused on checking how demand is actually split across preservative uses and chemical intermediate consumption, and how pricing moves through contracts and spot transactions. We spoke with manufacturers, distributors, and large buyers (such as food ingredient blenders, personal care formulators, and industrial chemical users) across APAC, EMEA, and the Americas. This input helped us confirm utilization ranges, import dependence, and the realistic price bands used in the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 12% | APAC: 40% |

| Mid tier: 49% | Functional/Unit leaders: 36% | EMEA: 36% |

| Smaller Players: 14% | Managers: 52% | Americas: 24% |

Market-Sizing & Forecasting

Sizing started with a top-down reconstruction that links benzoic acid demand to observable end-use activity, and then translates that demand pool into value using year-specific pricing logic. In practice, we used indicators such as preservative consumption direction in packaged foods and beverages, derivative pull from benzoate production, operating rates and announced capacity changes, import and export balances by major trading hubs, and typical contract price movements across regions.

Those totals were then corroborated with selective bottom-up approximations, including sampled supplier revenue ranges, distributor channel checks, and volume times ASP calculations for key applications where data was clearer. When gaps appeared, we handled them through conservative penetration assumptions and cross-checked against trade intensity and utilization ranges discussed by interviewees.

For forecasting, scenario analysis was applied around two or three sensitive variables, mainly capacity additions, feedstock and energy cost direction that impacts pricing, and substitution pressure from alternative preservatives. The scenarios were then narrowed using expert inputs on how quickly pricing and demand normalize after supply shocks, and the final series was smoothed to avoid unrealistic step changes.

Data Validation & Update Cycle

Outputs were checked against independent signals, including trade value trends, volume direction where available, and whether implied regional pricing stayed within realistic bands seen in interviews. Outliers were reviewed by a second analyst, and any large variance triggered a re-check of scope, unit conversions, and the pricing year used in the value build.

The report is refreshed annually, and interim updates are made when a material event occurs, such as a major plant shutdown, new capacity start-up, or unusual price spikes that persist across quarters. Before delivery, we do a fresh pass on key assumptions so clients receive the latest view aligned with the most recent public data and expert feedback.

Mordor Intelligence's Benzoic Acid Market Sizing Compared With Other Published Estimates

Published market sizes for benzoic acid can look far apart because the scope boundaries are not consistent, and the pricing basis is not always stated clearly. In practice, differences usually come from whether derivatives are blended into the core market, which year is treated as the starting point, and how trade flows and regional price dispersion are converted into one global value.

Trade-value direction and regional price-band checks are two signals that keep the Mordor Intelligence estimate aligned to benzoic acid traded as its own product (instead of bundling salts and esters), and they also limit inflated totals that can happen when downstream revenue pools are mixed in.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.28 B (2025) | |

| Industry Data Publisher A | USD 2.60 B (2024) | This estimate appears to include benzoic acid along with its salts and esters, and it is stated in nominal wholesale prices, which expands the value pool beyond benzoic acid sold as a distinct chemical. |

| Global Consultancy B | USD 1.26 B (2026) | The figure is presented with a different base year and may use a broader forecasting horizon and alternate pricing assumptions for 2026, which can shift the starting value even when the core product scope is similar. |

Overall, the spread is mainly explained by product boundary choices and the pricing year used for the value build. When the scope is kept to benzoic acid itself and the value is tied back to trade signals, capacity moves, and verified price bands, the market size becomes easier to replicate and track over time.

Key Questions Answered in the Report

What is the current value of the benzoic acid market?

The benzoic acid market stands at USD 1.34 billion in 2026 and is projected to reach USD 1.69 billion by 2031.

Which region holds the largest benzoic acid market share?

Asia-Pacific leads with 41.87% share as of 2025, driven by integrated aromatic production hubs.

Why are benzoate plasticizers growing faster than other derivatives?

Regulatory bans on ortho-phthalates in food packaging and consumer goods push converters to safer benzoate alternatives, resulting in a 6.58% CAGR for this derivative group.

What is the outlook for the Middle East & Africa market?

The region is forecast to expand at a 6.49% CAGR through 2031 due to rapid food-processing growth and supportive chemical regulations.

Page last updated on: