Acidity Regulators Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

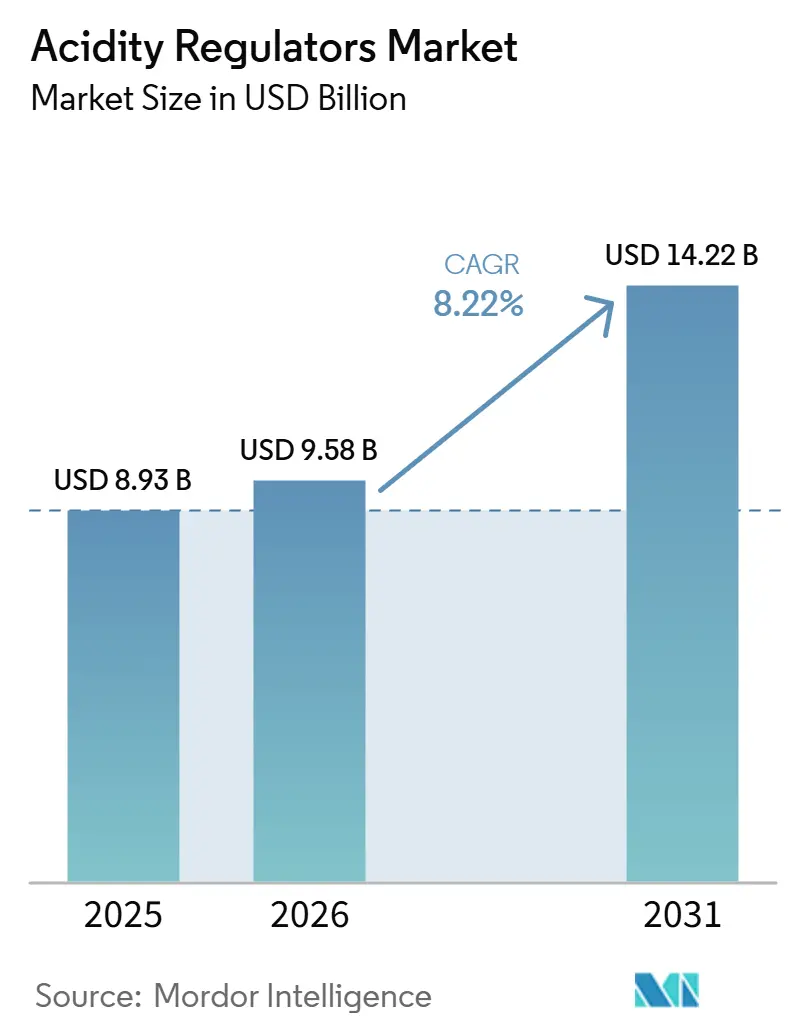

| Market Size (2026) | USD 9.58 Billion |

| Market Size (2031) | USD 14.22 Billion |

| Growth Rate (2026 - 2031) | 8.22% CAGR |

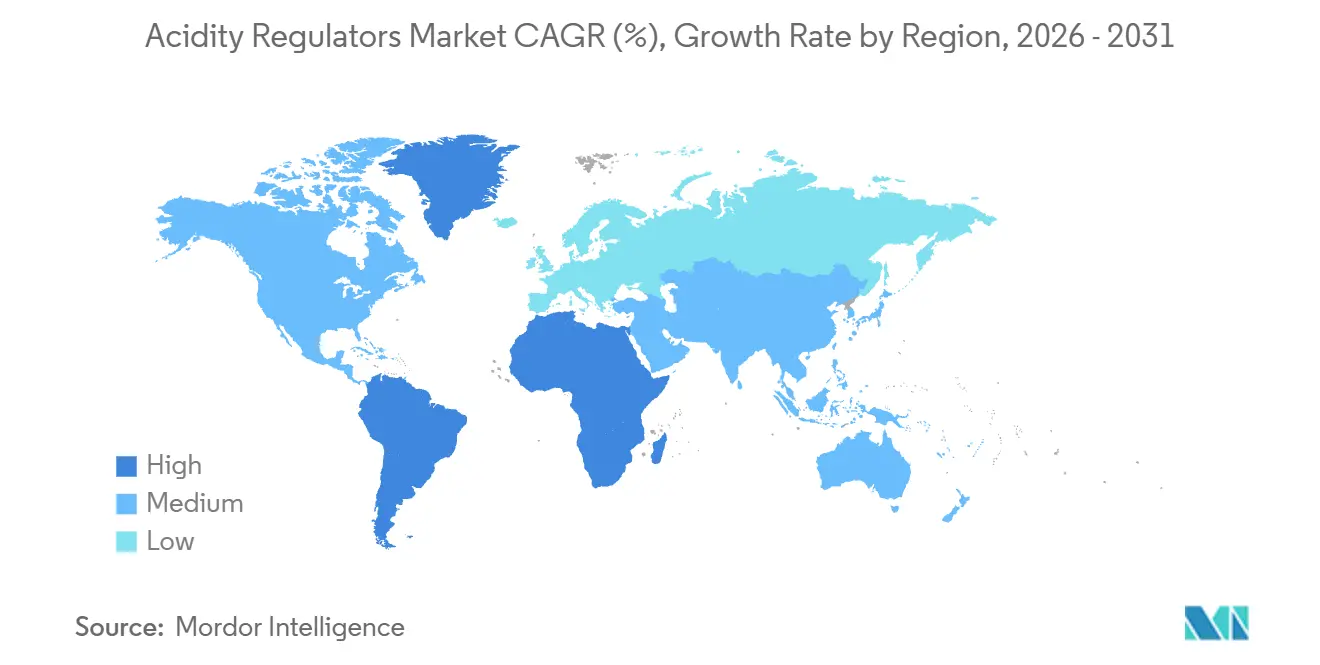

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acidity Regulators Market Analysis by Mordor Intelligence

The Acidity regulators market size is expected to grow from USD 8.93 billion in 2025 to USD 9.58 billion in 2026 and is forecast to reach USD 14.22 billion by 2031 at 8.22% CAGR over 2026-2031. The acidity regulators market is being supported by compliance-led demand because acidified food processors must maintain product pH at or below 4.6 under U.S. FDA rules, and similar controls are reinforced by Codex standards across export markets. This makes demand less exposed to discretionary consumer spending because pH control is a basic operating requirement in shelf-stable food production. The acidity regulators market is also benefiting from stronger packaged food consumption in Asia-Pacific, broader reformulation activity in beverages, and rising use in industrial cleaning and water treatment. Competition is shifting toward companies that can pair broad formulation capability with reliable supply, while the heavy concentration of citric acid fermentation in China remains the main structural supply risk for global buyers.

Key Report Takeaways

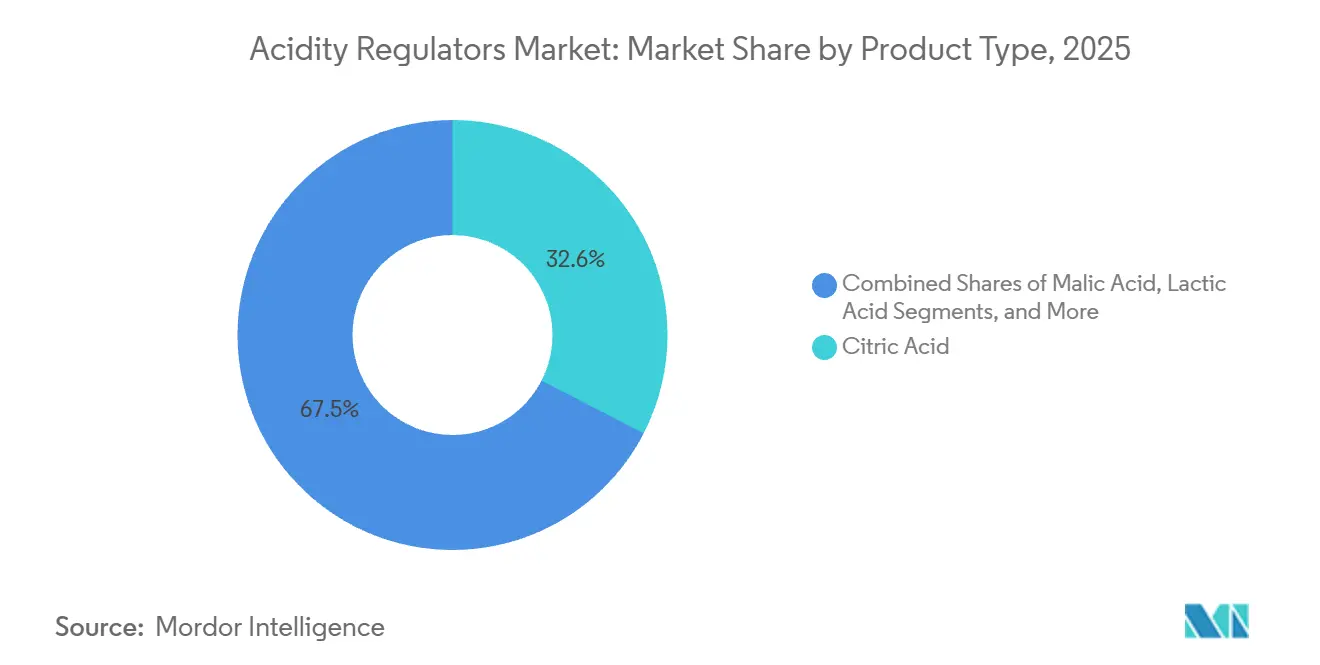

- By type, citric acid held 32.55% of the acidity regulators market share in 2025, while tartaric acid is forecast to grow at 9.55% CAGR through 2031.

- By form, dry formulations accounted for 60.36% of the acidity regulators market size in 2025, while liquid formulations are projected to expand at 8.98% CAGR through 2031.

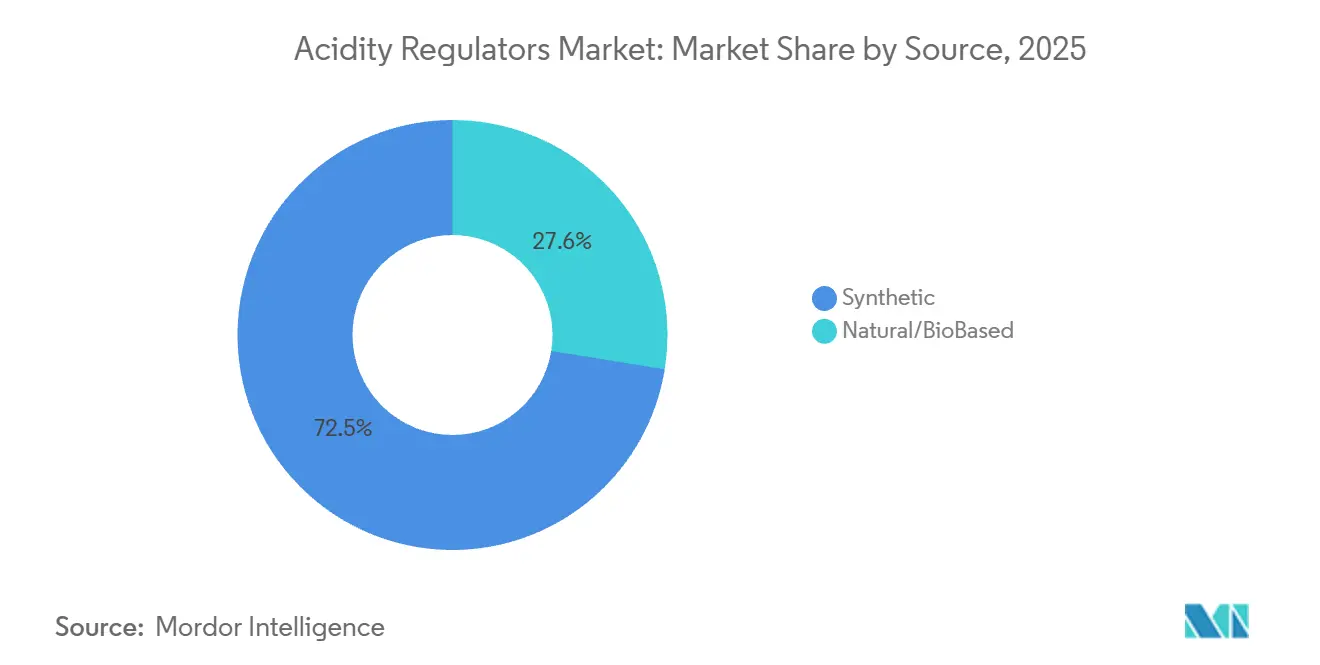

- By source, synthetic sources held 72.45% of 2025 revenue, while natural and bio-based sources are expected to advance at 10.17% CAGR through 2031.

- By application, food and beverages represented 62.3% of the acidity regulators market size in 2025, while industrial applications are projected to grow at 9.72% CAGR through 2031.

- By geography, Asia-Pacific led with 38.56% share in 2025, while the Middle East and Africa is forecast to expand at 9.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Acidity Regulators Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Processed And Convenience Foods | +2.1% | Global, concentrated in Asia-Pacific and Middle East & Africa | Medium term (2-4 years) |

| Improved Food Safety And Microbial Control | +1.5% | Global, with regulatory influence under FDA 21 CFR 114 and Codex Alimentarius | Medium term (2-4 years) |

| Flavor Enhancement In Food And Beverages | +1.3% | Global, particularly North America, Europe, and Asia-Pacific beverage industries | Medium term (2-4 years) |

| Growing Demand For Shelf-Life Extension | +1.4% | Global, highest impact in South America and Middle East & Africa | Medium term (2-4 years) |

| Shift Toward Clean-Label And Natural Additives | +1.0% | North America and Europe leading, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Growth In Natural Acidity Regulator Adoption | +0.8% | Europe and North America core, supported by EFSA and FDA compliance factors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Processed and Convenience Foods

The acidity regulators market is gaining from urbanization and tighter daily routines that are pushing more households toward packaged and shelf-stable foods. Asia-Pacific remains one of the strongest centers of processed food demand, with India and Southeast Asia seeing solid growth as modern retail reaches smaller cities and food distribution improves. A less visible change is the wider reach of cold-chain infrastructure in tier-2 and tier-3 cities across China, India, and Indonesia, bringing more consumers into formal packaged-food channels. That expansion raises demand for sauces, noodles, condiments, and prepared meals that rely on lactic acid, acetic acid, and citric acid to maintain pH-controlled stability. Producers in these categories use acidity regulators because they support product safety and consistency even where refrigeration access is uneven. This keeps the demand base tied to long-term demographic and retail changes rather than to short-lived food fads.

Improved Food Safety and Microbial Control

The acidity regulators market is also being supported by food safety rules that turn microbial control into a legal requirement rather than a voluntary quality choice. Under FDA 21 CFR Part 114, processors of acidified foods in the United States must validate that the finished equilibrium pH stays at or below 4.6 and must file a scheduled process for each container size. That rule creates a clear baseline for demand because acids used for pH control become part of routine compliance[1]Source: U.S. Food and Drug Administration, “Acidified & Low-Acid Canned Foods Guidance Documents & Regulatory Information”, fda.gov . A 2025 study in Sustainability reported that food-grade lactic acid delivered 2.0 log CFU/g reductions in E. coli and Salmonella in chilled meat matrices, which supports its role in antimicrobial control. Civil penalties tied to violations can reach nearly USD 500,000 per violation for business entities, which raises the cost of non-compliance. As a result, processors in the acidity regulators market have limited room to substitute away from these inputs where safety rules are tightly enforced.

Flavor Enhancement in Food and Beverages

The acidity regulators market is finding another source of demand in product reformulation, especially where food and beverage companies are reducing sugar and moving away from older synthetic flavor systems. Acidity regulators help control tartness, balance sweetness perception, and improve mouthfeel, which makes them useful when producers adjust recipes without changing the expected taste profile. The UAE introduced tiered taxation on sugary beverages in January 2026, and that policy is pushing beverage companies to reformulate products based on sugar content per 100 ml. In that setting, citric and malic acids help replace part of the taste balance lost when sugar levels are reduced[2]Source: Centre for the Promotion of Imports from Developing Countries, “Which Trends Offer Opportunities or Pose a Threat on the European Natural Food Additives Market?”, cbi.eu. Tartaric acid is also moving beyond wine because bakery, beverage, and specialty food formulators see it as a label-friendly option compared with acids that carry stronger synthetic associations. Malic acid remains especially relevant in sports drinks and functional beverages because its tartness profile supports reformulation while keeping flavor perception steady.

Growing Demand for Shelf-Life Extension

The acidity regulators market continues to benefit from the need to extend shelf life in regions where cold-chain coverage is incomplete or unreliable. Lowering product pH remains one of the most practical preservation approaches because it limits microbial growth, slows oxidation, and reduces enzymatic spoilage without requiring constant refrigeration. A 2025 paper in Foods showed that pH-responsive controlled-release systems using organic acids can extend the stability of perishable food systems, which points to new packaging and preservation uses beyond standard formulations. Corbion linked its 2025 performance to strong demand for natural preservation and shelf-life extension, and the company reported EUR 204.3 million in adjusted EBITDA with 26.7% organic growth. That company result shows how preservation demand is translating into commercial value for suppliers with relevant product lines. In markets across Sub-Saharan Africa, South Asia, and Latin America, the same need for durable products under ambient conditions keeps this demand durable through the forecast period.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory Compliance Requirements | -0.8% | Global, most acute under EFSA's re-evaluation program and FDA FSMA | Medium term (2-4 years) |

| Restrictions On Chemical-Based Additives | -0.6% | Europe and North America leading, with emerging friction in South Korea and Japan | Long term (≥ 4 years) |

| Supply Chain Disruptions | -0.5% | Global, concentrated in Asia-Pacific due to dependence on Chinese fermentation clusters | Short term (≤ 2 years) |

| Health Concerns Linked To Overconsumption | -0.4% | North America and Europe, with rising awareness in the Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Compliance Requirements

The acidity regulators market faces a clear restraint in the form of rising compliance costs across major jurisdictions. EFSA is re-evaluating permitted food additives, including acidity regulators such as phosphoric acid and acetic acid, and that process requires updated toxicology and risk documentation from suppliers. China is also tightening GB-series purity specifications, which can affect customs clearance and product qualification timelines for imported material. Suppliers that sell across the United States, Europe, and China therefore face parallel registration, reformulation, and documentation burdens that are difficult for smaller companies to absorb. FDA FSMA requirements add another layer because acidified food processors must maintain detailed hazard analysis and corrective action records. These requirements do not remove demand from the acidity regulators market, but they do raise operating costs and make market entry more difficult.

Restrictions on Chemical-based Additives

The acidity regulators market is also under pressure from tighter scrutiny of synthetic additives, especially in premium food and beverage categories. In Europe, regulation and consumer preference are both pushing producers toward fermentation-derived acids that are easier to position on cleaner labels. Consumer scanning apps have accelerated that response, and CBI reported that 92% of Yuka users reduced ultra-processed food consumption after using the app. The same source noted that French retailer Intermarché reformulated 900 products and removed 142 additives in response to consumer pressure shaped by ingredient transparency tools. The effect on total synthetic acid volumes is still gradual because the synthetic segment remained large in 2025, but the direction of premium reformulation is clear. For suppliers focused on synthetic phosphoric or acetic acid, portfolio expansion into fermentation-derived alternatives is becoming a practical response to this shift.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Citric Acid Sustains Scale Dominance; Tartaric Acid Leads Specialty Expansion

Citric acid held 32.55% of 2025 revenue, and that position reflects the breadth of its use across pH control, chelation, and flavor modulation in the acidity regulators market. Large fermentation networks give it a scale advantage through lower costs and reliable supply. In 2026, the U.S. Department of Commerce is expected to review citric acid imports from China and confirm no below-normal-value pricing from the major Chinese producers covered in that review. This outcome is expected to show the scale of Chinese supply and trade scrutiny around this product. Phosphoric acid continues to support cola-type beverages, although regulatory focus and health concerns limit faster growth.

Other major acids hold important positions because their end uses differ across food, pharmaceutical, and industrial applications in the acidity regulators industry. Lactic acid is gaining use in meat preservation, vegan dairy alternatives, and excipient applications as bio-based production improves quality and economics. Acetic acid remains key to vinegar-based preservation in pickled products and condiments, where flavor and shelf-life extension work together. Malic acid is gaining relevance in fruit-forward beverages and confectionery because it offers smoother, longer-lasting tartness than some alternatives. Tartaric acid is the fastest-growing type, with a CAGR of 9.55% through 2031, driven by wine production, bakery applications, and wider clean-label adoption beyond its traditional base. Its appeal is rising among formulators seeking naturally derived acids as consumer and regulatory resistance to more synthetic options grows in Europe and North America.

By Form: Dry Form Dominates; Liquid Gains in Automated Processing Lines

Dry formulations held 60.36% of 2025 revenue, which means this form represented the larger share of acidity regulators market size in the base year. Their lead comes from strong fit with bakery, confectionery, pharmaceutical blending, and spice-mix applications where moisture control matters. Dry citric acid and powdered malic acid are common in leavening systems because particle consistency and dissolution behavior affect final product performance. This form is also widely used by mid-scale processors in South and Southeast Asia that do not have large liquid dosing systems. Lower storage and transport complexity further supports dry products in processing clusters where temperature-controlled handling is less available.

Liquid formulations are the faster-growing form and are projected to expand at 8.98% CAGR through 2031 in the acidity regulators market. Beverage plants are shifting toward automation and continuous processing, which favors liquid acids because they remove the dissolution step and improve dosing precision. That operating benefit helps reduce cycle times and limits cross-contamination risk in high-volume production lines. Liquid acid systems are also gaining use in industrial cleaning and water treatment where continuous dosing is more practical than powder handling. The 2025 Foods study on pH-responsive release technologies also points to wider liquid-phase deployment in packaging and preservation systems. As precision formulation and tighter food safety control become more important, liquid forms should keep taking share from a smaller base.

By Source: Synthetic Maintains Supply Scale; Natural/Bio-based Commands the Fastest Growth

Synthetic sources accounted for 72.45% of 2025 revenue, and this segment benefited from long-established fermentation and chemical synthesis infrastructure across the acidity regulators market. The category includes fermentation-derived citric acid produced from glucose or sucrose substrates, chemically synthesized phosphoric acid, petrochemical-route DL-malic acid, and acetic acid from methanol carbonylation. This supply base remains highly competitive on cost, which keeps it important for price-sensitive processors in developing markets. China plays a central role because its fermentation ecosystem combines corn-based glucose feedstocks, large production sites, and established logistics. That structure keeps pressure on global pricing and helps explain why synthetic supply still holds the larger volume position.

Natural and bio-based sources are projected to grow at 10.17% CAGR through 2031, making them the fastest-growing source group in the acidity regulators market. CBI, citing Ingredion, stated that clean-label products are projected to exceed 70% of European food and beverage portfolios in 2025 and 2026, and 99% of European manufacturers view clean-label strategies as essential. That shift is pushing capacity investment toward bio-based acids and preservation systems. Corbion said its 2025 strategic execution included targeted investment in natural preservation, lactic acid derivatives, and the ramp-up of its new gypsum-free lactic acid facility in Thailand. Sustainability-linked procurement requirements, including interest in ISO 14064 greenhouse gas accounting, are also favoring suppliers that can document fermentation-based sourcing. These factors are expanding the role of natural acids from a premium niche into a larger structural growth lane within the acidity regulators industry.

By Application: Food and Beverages Leads by Volume; Industrial Applications Accelerates Fastest

Food and beverages held 62.33% of 2025 revenue, and this segment therefore accounted for the largest share of acidity regulators market size in application terms. Its lead reflects the basic role acidity regulators play across beverages, sauces, condiments, bakery, dairy, meat, poultry, and seafood processing. Beverage production remains the largest single consumption center for citric acid because carbonated drinks, juices, ready-to-drink teas, and functional beverages all depend on stable acidulation systems. Bakery and confectionery, dairy, meat preservation, and pickling each use different acid profiles based on pH targets, flavor requirements, and regulatory standards. Pharmaceuticals and personal care add a higher-value layer of demand through buffering and excipient uses, while feed and agriculture use organic acids as alternatives to antibiotic growth promoters in some settings.

Industrial applications are projected to grow at 9.72% CAGR through 2031, making them the fastest-growing end-use in the acidity regulators market. This rise is being driven by wider use of phosphoric acid and citric acid derivatives in industrial cleaning, descaling, water treatment, and metal surface treatment. In descaling systems, citric acid and trisodium citrate dihydrate help dissolve mineral deposits through calcium chelation while avoiding some of the compatibility issues linked to stronger mineral acids. Municipal and industrial water treatment systems in Asia and Africa are also adopting pH-adjustment compounds to meet tighter discharge and corrosion control requirements. The 2025 Foods study on pH-responsive release systems shows that organic acids are moving into technical applications beyond traditional food manufacturing. That shift matters because the acidity regulators market has long been associated with food use, yet some of the fastest marginal gains are now coming from non-food settings.

Geography Analysis

Asia-Pacific held 38.56% of acidity regulators market share in 2025, making it the largest regional market by supply and demand. The region has the world’s largest citric acid production base and a wide consumer base for processed food and beverage products. China remains central, as major fermentation groups in Shandong, Jiangsu, and Anhui supply a large share of global citric acid demand. India is adding demand through organized food processing, urban retail, and shelf-stable packaged products. Japan, South Korea, and Australia remain mature markets, where purity standards and regulatory compliance guide product choice and support demand for fermentation-derived acids.

North America and Europe remain mature regions, but reformulation and compliance continue to reshape demand in the acidity regulators market. In North America, FDA FSMA and 21 CFR Part 114 make acidity regulators essential for shelf-stable food processing. Jungbunzlauer’s planned November 2025 acquisition of a facility in Thomson, Illinois, shows that suppliers value manufacturing closer to North American customers. Europe is moving through a strong clean-label cycle, and CBI indicated that clean-label products are expected to account for more than 70% of European food and beverage portfolios in 2025 and 2026. This shift supports premium demand for naturally sourced acids in Germany, France, and Italy.

Middle East and Africa is projected to grow at a 9.27% CAGR through 2031, making it the fastest-growing regional block in the acidity regulators market. The World Bank stated that food demand in the Middle East and North Africa is projected to rise by 67% by 2050, creating a large long-term base for ingredient demand. Egypt, Saudi Arabia, and the UAE remain key food processing anchors, while GCC markets support ingredient imports and domestic capacity expansion. The UAE’s January 2026 tiered sugar tax is expected to encourage beverage reformulation and increase the need for acid-based flavor balancing in lower-sugar products. South America remains relevant through packaged food manufacturing and wine and vinegar production in Brazil and Argentina, which support tartaric and acetic acid demand.

Competitive Landscape

The acidity regulators market is consolidated, with established multinationals leading competition. However, specialized bio-based producers and regional suppliers continue to find growth opportunities. Major companies such as Archer Daniels Midland, Cargill, and Foodchem International use vertical integration across agricultural sourcing, fermentation, and global distribution. This approach supports cost control and improves supply chain reliability. These companies are also increasing their focus on sustainability. For instance, ADM supports regenerative agriculture, while Tate & Lyle aims to achieve net-zero emissions by 2050.

Technology remains a key source of differentiation, as precision fermentation and process optimization help companies improve cost efficiency and product quality. Clean-label formulations, antibiotic-free animal feed, and specialized pharmaceutical applications are creating premium opportunities. Smaller and regional players compete through technical support, customized formulations, and quick responses to local customer needs. At the same time, consolidation pressure is rising because large-scale fermentation capacity and strict regulatory compliance favor bigger companies.

Geopolitical supply chain risks are creating opportunities for non-Chinese producers to expand their presence. Patent activity in metabolic engineering and fermentation also shows strong innovation. Companies are investing in proprietary microbial strains and advanced purification technologies to improve quality, lower costs, and strengthen bio-based acidity regulator production.

Acidity Regulators Industry Leaders

Cargill Inc.

Archer Daniels Midland Company

Jungbunzlauer Suisse AG

Corbion N.V.

Foodchem International Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: ICL Group completed the first phase of its two-phase acquisition of Bartek Ingredients Inc., acquiring approximately 50% of the company via a cash investment of approximately USD 90 million. Bartek is the global leader in food-grade malic and fumaric acid, serving customers in over 40 countries with annual revenue of approximately USD 65 million, and operates the only vertically integrated maleic anhydride and food-grade acid production site in North America. A new production facility under construction is expected to materially increase Bartek's capacity and output by 2026.

- November 2025: Jungbunzlauer closed the acquisition of a multipurpose production facility in Thomson, Illinois, from International Flavors & Fragrances Inc. (IFF), marking the company's first manufacturing presence in the United States. The CHF 1.3 billion Swiss manufacturer, known primarily for citric acid, acidulants, and mineral salts, immediately commenced equipment installation and regulatory compliance activities at the facility, positioning itself to serve growing North American demand for naturally derived ingredients.

- February 2025: Prayon has unveiled plans for a new electronic-grade phosphoric acid production unit in Bex, Switzerland. This strategic move aims to double its production capacity, addressing the surging demand for ultrapure phosphoric acid. This demand is notably driven by the reshoring trend in the rapidly expanding semiconductor markets of Europe and the U.S.

- January 2025: Brenntag Pharma has expanded its partnership with Citribel to distribute citric acids and citrate pharmaceutical excipients, now covering Israel, Turkey, South Africa, in addition to France, Spain, Germany, and the Benelux region.

Global Acidity Regulators Market Report Scope

| Citric Acid |

| Phosphoric Acid |

| Acetic Acid |

| Lactic Acid |

| Malic Acid |

| Tartaric Acid |

| Others |

| Dry |

| Liquid |

| Synthetic |

| Natural/Bio-based |

| Food and Beverages | Beverages |

| Sauces, Condiments and Dressings | |

| Bakery and Confectionery | |

| Dairy and Frozen Desserts | |

| Meat, Poultry and Seafood | |

| Other Food and Beverages | |

| Pharmaceuticals and Personal Care | |

| Animal Feed and Agriculture | |

| Industrial Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Citric Acid | |

| Phosphoric Acid | ||

| Acetic Acid | ||

| Lactic Acid | ||

| Malic Acid | ||

| Tartaric Acid | ||

| Others | ||

| By Form | Dry | |

| Liquid | ||

| By Source | Synthetic | |

| Natural/Bio-based | ||

| By Application | Food and Beverages | Beverages |

| Sauces, Condiments and Dressings | ||

| Bakery and Confectionery | ||

| Dairy and Frozen Desserts | ||

| Meat, Poultry and Seafood | ||

| Other Food and Beverages | ||

| Pharmaceuticals and Personal Care | ||

| Animal Feed and Agriculture | ||

| Industrial Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected value of the acidity regulators market by 2031?

The acidity regulators market is forecast to reach USD 14.22 billion by 2031, up from USD 9.58 billion in 2026, at an 8.22% CAGR over 2026-2031.

Which product type leads acidity regulator demand today?

Citric acid led by type with 32.55% share in 2025 because of its broad use in pH control, chelation, and flavor modulation across food and beverage applications.

Which end-use is growing the fastest for acidity regulators?

Industrial applications are projected to grow at 9.72% CAGR through 2031, supported by cleaning, descaling, water treatment, and metal surface treatment uses.

Which region is strongest in the acidity regulators business?

Asia-Pacific held the largest regional share at 38.56% in 2025, while Middle East and Africa is expected to post the fastest growth at 9.27% CAGR through 2031.

Page last updated on: