Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

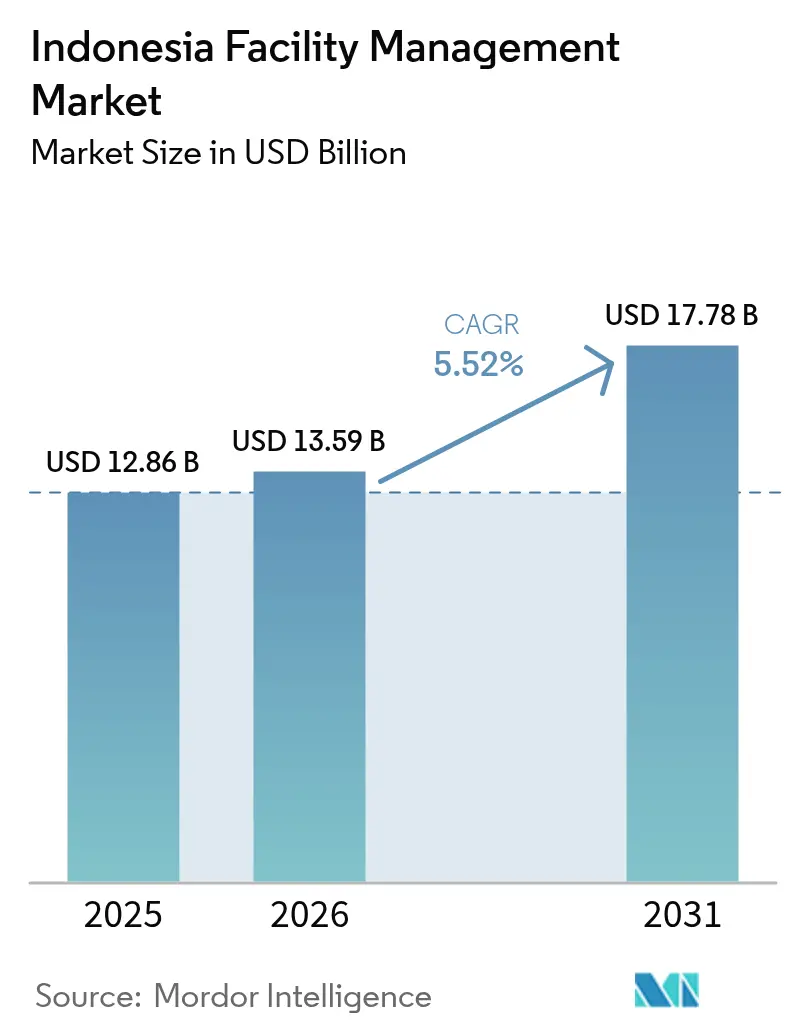

| Base Year Market Size (2025) | USD 12.86 Billion |

| Market Size (2026) | USD 13.59 Billion |

| Market Size (2031) | USD 17.78 Billion |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

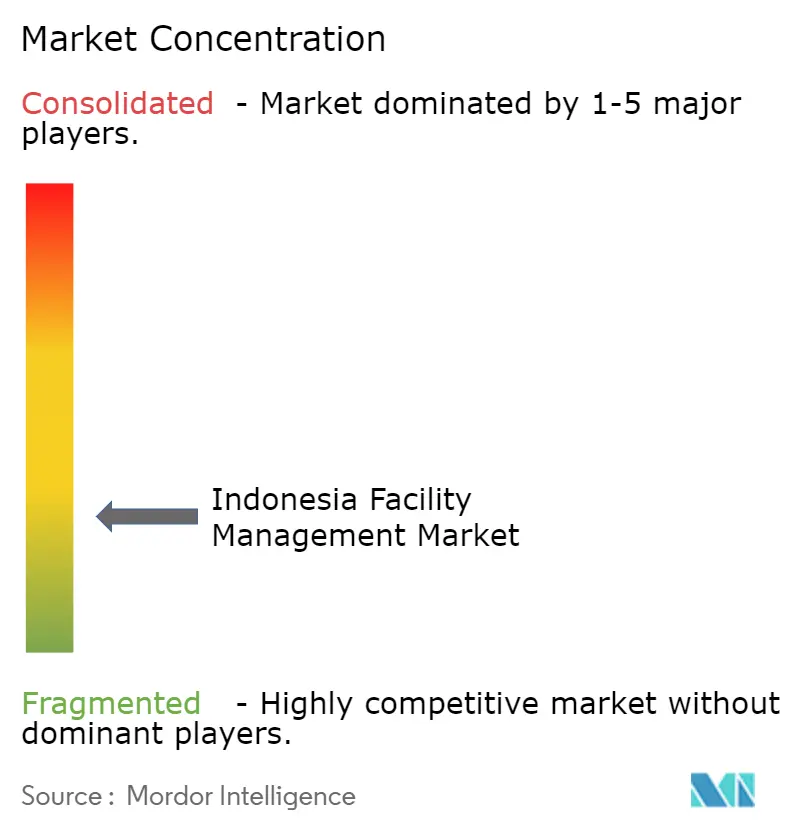

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Facility Management Market Analysis by Mordor Intelligence

The Indonesia facility management market size is expected to increase from USD 12.86 billion in 2025 to USD 13.59 billion in 2026 and reach USD 17.78 billion by 2031, growing at a CAGR of 5.52% over 2026-2031. Jakarta’s shift from ad-hoc maintenance contracts to outcome-based service models, backed by availability-based payment terms that reward uptime and energy savings, is redefining value propositions for vendors. An infrastructure budget of USD 25.5 billion for 2025 is channeling recurring facility management demand into toll roads, mass-transit hubs and industrial estates. Multinational occupiers continue to favor ISO 41001-compliant integrated providers, while domestic specialists defend niche verticals such as hospitals and airports. Wage inflation for certified HVAC and fire-safety technicians remains the primary cost headwind, yet ESG-linked loans that offer interest-rate discounts for green-certified assets are enlarging budgets for energy-efficient retrofits and predictive maintenance.

Key Report Takeaways

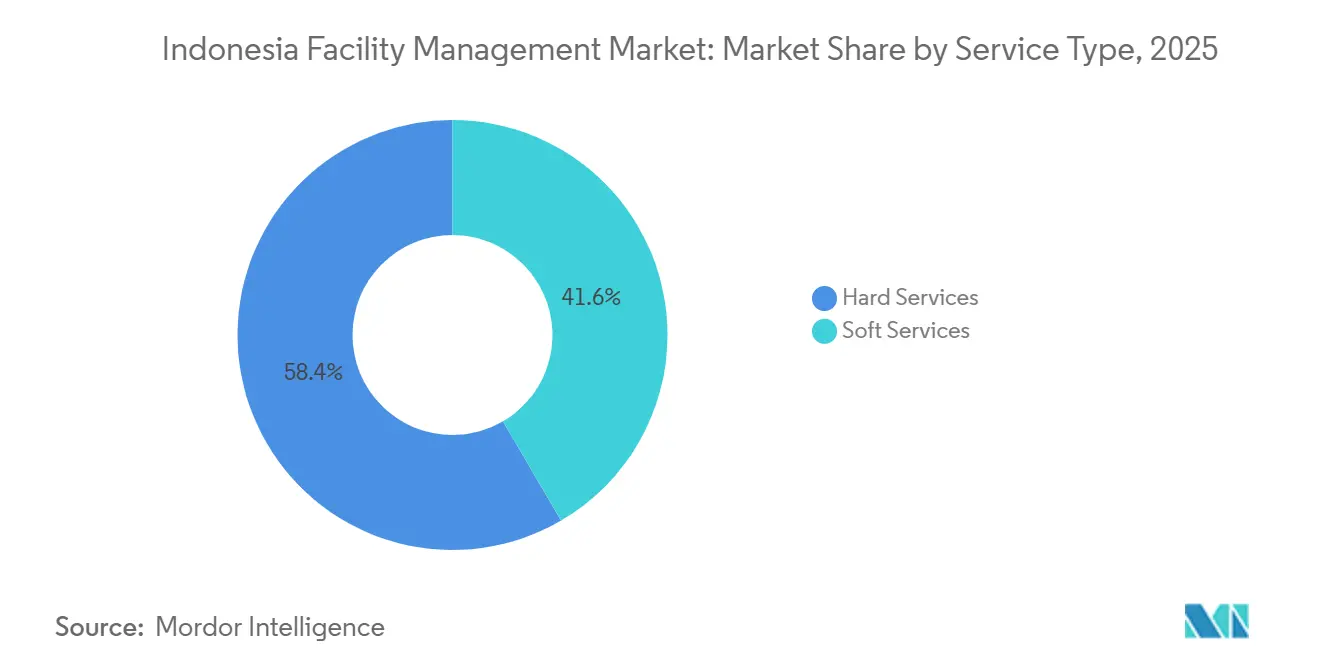

- By service type, hard services led with 58.42% of the Indonesia facility management market share in 2025; soft services are projected to expand at a 5.87% CAGR through 2031.

- By offering type, in-house delivery accounted for 57.36% of the Indonesia facility management market size in 2025, while outsourced integrated models are advancing at a 5.73% CAGR to 2031.

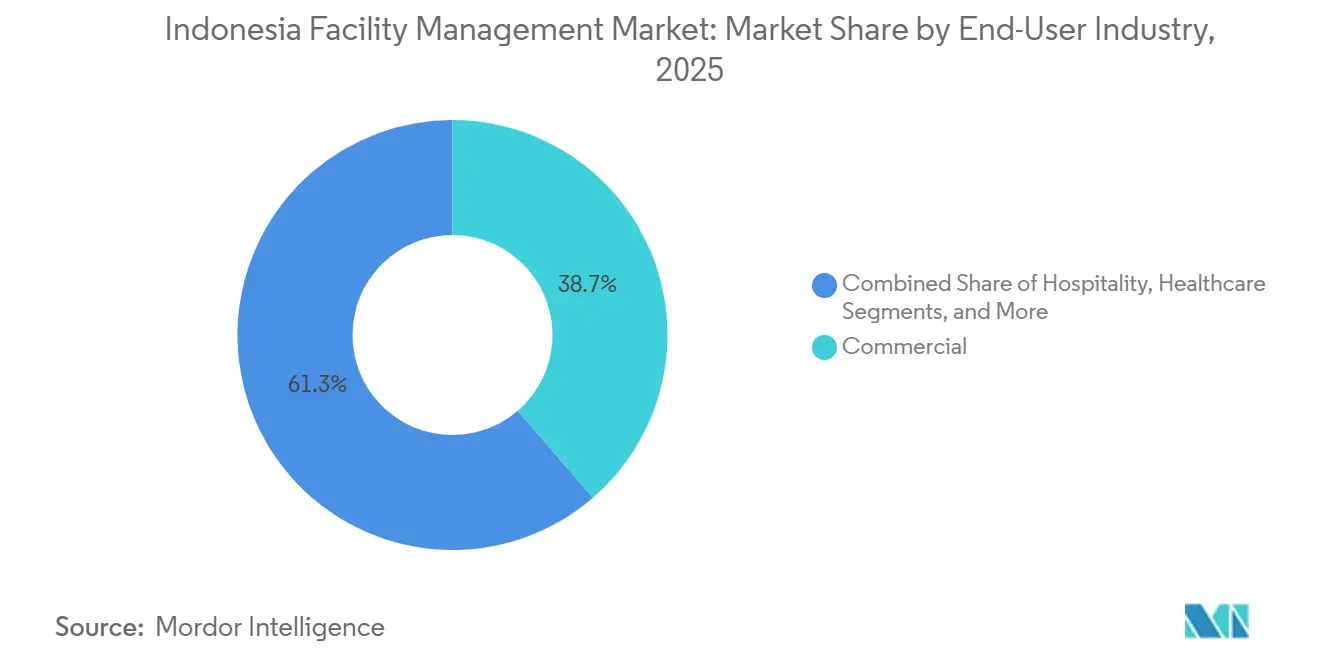

- By end-user industry, commercial facilities captured 38.67% of revenue in 2025, whereas industrial and process sites are forecast to grow at 6.12% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact On CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In ESG-Linked Financing Favoring Green-Certified Facilities | +1.2% | National, Concentrated In Jakarta, Surabaya, Bandung | Medium Term (2–4 Years) |

| Urbanization In Major Metros | +1.1% | Greater Jakarta, Surabaya, Bandung, Medan, Makassar | Long Term (≥ 4 Years) |

| Infrastructure Pipeline Investment | +1.0% | National, Priority Corridors In Java, Sumatra, Kalimantan | Medium Term (2–4 Years) |

| Proliferation Of Mixed-Use Mega-Developments In Secondary Cities | +0.9% | Surabaya, Bandung, Semarang, Medan | Medium Term (2–4 Years) |

| Rising Occupancy Optimization | +0.7% | National, Led By Jakarta CBD And Industrial Estates | Short Term (≤ 2 Years) |

| Labor And Safety Regulation | +0.6% | National, Enforced By Ministry Of Manpower | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Surge In ESG-Linked Financing Favoring Green-Certified Facilities

Indonesia’s commercial banks tied USD 4.8 billion of real-estate loans to EDGE, LEED or GREENSHIP ratings in 2025, lowering borrowing costs by up to 60 basis points. Developers used the savings to fund HVAC retrofits, LED relamping and water-recycling projects that require vendors capable of documenting carbon and energy metrics for quarterly audits. Certified floor space reached 11 million m² across 385 projects, with 62% located outside Jakarta, demonstrating how secondary-city landlords employ green credentials to court multinational tenants.[1]Green Building Council Indonesia, “Certified Projects Database 2025,” gbcindonesia.org

Urbanization In Major Metros

Greater Jakarta’s density climbed to 15,342 residents per km² in 2025, accelerating vertical mixed-use towers that stack offices, hotels and residences within a single footprint. Each property depends on integrated facility management to synchronize disparate service-level agreements, driving bundled contracts that replace fragmented vendor rosters. Surabaya’s Pakuwon Mall expansion alone added 120,000 m² of leasable space, supported by a district-cooling plant that trimmed operating costs by 19% relative to standalone chillers.[2]Statistics Indonesia, “Urban Population and Density Statistics 2025,” bps.go.id

Infrastructure Pipeline Investment

The 2025 state budget directs USD 25.5 billion toward toll roads, ports and industrial estates, many of which require 10-15-year facility management concessions anchored in ISO 55000 asset-management standards. Patimban Deep Sea Port awarded a 12-year integrated package for cargo equipment upkeep, perimeter security and hazardous-material compliance, illustrating how long-dated agreements create annuity-like cash flows for service providers.[3]Angkasa Pura Supports, “Facility Management Services Portfolio,” angkasapurasupports.co.id

Proliferation Of Mixed-Use Mega-Developments In Secondary Cities

Surabaya, Bandung and Semarang launched 27 projects exceeding 50,000 m² between 2024-2025, decentralizing demand away from Jakarta. Integrated providers now manage cleaning, security and HVAC zoning across office, hospitality and retail podiums under single contracts that consolidate as many as 14 legacy vendors. Labor costs in these cities run 22% below Jakarta, but shortages of technicians certified in advanced fire-alarm and chiller optimization require apprenticeship programs with local polytechnics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Margin Pressure on Leading Firms | -0.8% | National, Acute in Jakarta and Industrial Zones | Short Term (≤ 2 Years) |

| Skilled Labor Shortages | -0.7% | National, Severe in HVAC and Fire-Safety Trades | Medium Term (2–4 Years) |

| Dependency on Imported Building Automation Hardware | -0.4% | National, Influencing Smart-Building Deployments | Medium Term (2–4 Years) |

| Fragmented Provincial Regulatory Oversight | -0.3% | Multi-Province Operators, Mainly Java and Sumatra | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Margin Pressure on Leading Firms

Average wages for skilled technicians rose 14% in 2025 as automotive and electronics plants absorbed technical labor, compressing operating margins at major vendors to 4.2% from 5.8% a year earlier. Minimum-wage hikes of up to 9% in Jakarta further squeezed profitability, prompting smaller operators to exit low-margin cleaning and security contracts. Integrated providers countered by cross-subsidizing soft services with higher-margin MEP maintenance and energy-management offerings.[4]Ministry of Manpower, “Decree KEP-226/2024 on Minimum Wages,” kemnaker.go.id

Skilled Labour Shortages

Vocational institutes produced 38,000 facility management graduates in 2025 against industry demand for 62,000, leaving a 24,000-person gap concentrated in HVAC troubleshooting, fire-alarm programming and BAS integration. Contract penalties for unfilled technician posts averaged 2% of monthly fees, forcing providers to recruit retired military personnel and sponsor dual-certification courses that combine technical training with English proficiency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Anchor Revenue, Soft Services Accelerate

Hard services contributed 58.42% of revenue in 2025, reflecting ongoing demand for MEP, HVAC and fire-safety work that must comply with SNI 03-3989 standards. The Indonesia facility management market size for soft services is set to expand faster at 5.87% through 2031 as mixed-use towers outsource cleaning, security and catering. Growth is amplified in Surabaya and Bandung, where recent mega-developments require mechanized cleaning systems and certified security guards.

Asset-management solutions linked to ISO 55000 computerized systems now underpin factories in Cikarang and Karawang, cutting unplanned downtime by 23%. Meanwhile, fire-safety services advanced 6.1% in 2025 after regulators mandated biannual drills for high-rise buildings, creating predictable inspection and training revenue. Robotic scrubbers deployed by one multinational reduced labor hours 34%, demonstrating how technology offsets wage inflation.

By Offering Type: Outsourced Models Gain as Complexity Rises

In-house management maintained 57.36% share in 2025, favored by ministries and family-owned conglomerates that value direct oversight. Integrated outsourced contracts, however, are advancing at 5.73% as multinationals seek single-point accountability backed by ISO 41001 certification. Bundled contracts already represent 19% of outsourced spend, appealing to landlords that want cost transparency without relinquishing critical system control.

Integrated agreements increasingly peg 30% of fees to uptime and energy-saving targets, aligning provider incentives with tenant satisfaction. A recent airport concession granted a 10-year term contingent on achieving 99.5% HVAC uptime and 15% energy savings against 2023 baselines. Such outcome-based models position technology-enabled vendors for outsized share gains as service complexity rises.

By End-User Industry: Industrial Segment Surges On EV Investments

Commercial buildings generated 38.67% of revenue in 2025, underpinned by Jakarta’s Grade-A office stock where facility spending averages USD 4.20 per m² per month. Industrial facilities linked to electric-vehicle supply chains are projected to expand at 6.12%, the fastest across end-users, as battery and cathode plants in Karawang and Subang demand cleanroom environments and predictive maintenance for lithium-processing equipment.

Hospitality rebounded to 87% of pre-pandemic spending in 2025 but faces margin squeeze because long-term contracts cap price escalations below wage growth. Healthcare remains a high-potential niche thanks to infection-control requirements that few providers can meet, evidenced by a 5-year network contract that cut hospital-acquired infections by 29% through UV-C disinfection and HEPA-filtered HVAC.

Geography Analysis

Java accounted for 68% of national revenue in 2025, anchored by Greater Jakarta’s 23.4 million m² of professionally managed office and retail space. West Java’s manufacturing corridor attracted USD 18.3 billion of investments during 2024-2025, driving mandatory ISO 14001 and ISO 45001 certifications for facility service bids. East Java’s logistics and mixed-use clusters grew spending 8.2%, beating the national average.

Sumatra expanded 6.7% as Medan’s new offices and Palembang’s sports complexes outsourced multi-year security and MEP contracts, although differing provincial fire-audit cycles inflate compliance costs. Kalimantan and Sulawesi captured only 9% of revenue, yet the emerging Nusantara capital project is forecast to require USD 1.2 billion of cumulative services through 2035, promising scale opportunities for early entrants. Bali’s hospitality-centric market has already recovered to 92% of 2019 spending, with resort operators prioritizing solar-thermal water heating and organic-waste composting to secure green credentials.

Government policy is redirecting 31% of a IDR 387 trillion infrastructure budget toward regions outside Java, funding toll roads in Sumatra, ports in Kalimantan and airports in Papua. Regional tenders now favor bidders that hire at least 90% local staff, enabling domestic mid-tier players to undercut multinationals on labor costs. A new decree that all government buildings above 5,000 m² achieve minimum EDGE certification further boosts demand for vendors with IoT sensors and cloud analytics that monitor energy and water performance in real time.

Competitive Landscape

The top five international operators held a combined 28% share in 2025, leaving ample headroom for domestic specialists. Competition centers on portfolio breadth, technology adoption and certification credentials. AI-driven predictive maintenance at 34 sites reduced emergency repairs by 27% for one leading multinational, strengthening its position in outcome-based tenders. Another global provider’s mobile dashboard that consolidates occupancy, air quality and energy data helped it renew 89% of expiring contracts.

Healthcare facilities represent the most attractive white-space: fewer than 12 local providers hold the required infection-control and medical-gas certifications, yet the segment is projected to grow 8.1% through 2031. New entrants from Japan and Singapore are recruiting biomedical technicians and leveraging regional cost advantages to capture hospital and government tenders. The market is bifurcating as leading firms invest in IoT sensors, cloud CMMS and robotic cleaners while price-focused operators continue to rely on manual workflows, a gap that widens as tenants request ESG-aligned reporting based on GRI standards.

Indonesia Facility Management Industry Leaders

PT Shield On Service Tbk (SOS)

PT Patra Jasa

PT. Spektra Solusindo

Renno Indonesia

AEON Deligh Indonesia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: ISS A/S signed a 10-year integrated contract with the Ministry of State-Owned Enterprises covering 27 office buildings across three cities, valued at EUR 340 million (USD 383 million).

- December 2025: Sodexo Indonesia secured a 12-year bundled contract for Jakarta MRT Phase 2 stations worth USD 87 million, with penalties tied to PM2.5 thresholds.

- November 2025: PT Shield On Service acquired PT Citra Mandiri Sejahtera for IDR 420 billion (USD 27 million) to expand its West Java footprint.

- October 2025: CBRE Indonesia launched a joint venture with Surbana Jurong targeting Nusantara Capital City facility and smart-city contracts worth USD 200 million over five years.

Indonesia Facility Management Market Report Scope

The study tracks the facility management (FM) industry-related trends in Indonesia by analyzing the demand for FM services in the country. Facility management confines multiple disciplines to ensure functionality, comfort, safety, and efficiency of any building by integrating people, place, process, and technology. The Indonesia facility management market is defined based on the revenues generated from the services that are being used by various end-users, such as commercial, institutional, public/infrastructure, industrial, and other end users across the country. The analysis is based on the market insights captured through secondary research and the primaries. The report also covers the major factors impacting the growth of the market in terms of drivers and restraints.

The Indonesia Facility Management Market Report is Segmented by Service Type (Hard Services including Asset Management, MEP and HVAC Services, Fire Systems and Safety, Other Hard Facility Management Services; Soft Services including Office Support and Security, Cleaning Services, Catering Services, Other Soft Facility Management Services), Offering Type (In-house, Outsourced including Single Facility Management, Bundled Facility Management, Integrated Facility Management), End-User Industry (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, Industrial and Process, Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

By Offering Type

| In-house | |

| Outsourced | Single Facility Management |

| Bundled Facility Management | |

| Integrated Facility Management |

By End-User Industry

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process |

| Other End-User Industries |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| By Offering Type | In-house | |

| Outsourced | Single Facility Management | |

| Bundled Facility Management | ||

| Integrated Facility Management | ||

| By End-User Industry | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is the current value of the Indonesia facility management market and its expected growth?

The market is valued at USD 12.86 billion in 2025 and is projected to reach USD 17.78 billion by 2031, registering a 5.52% CAGR.

Which service category dominates spending in Indonesian facilities?

Hard services such as MEP, HVAC and fire systems account for 58.42% of 2025 revenue, reflecting the need for compliant mechanical upkeep.

Why are integrated facility management contracts gaining popularity?

Multinationals prefer single-point accountability, and outcome-based agreements link payments to uptime and energy-saving metrics that reduce overall costs.

How is ESG financing influencing facility management budgets?

Banks offer interest-rate discounts for green-certified buildings, spurring investments in energy-efficient retrofits that increase demand for certified vendors.

Which end-user segment is forecast to grow the fastest?

Industrial and process facilities tied to electric-vehicle supply chains are expected to expand at 6.12% through 2031.

What challenges do providers face when operating across multiple provinces?

Differing fire-safety and labor regulations require parallel documentation systems, adding compliance costs for multi-site operators.

Page last updated on: