Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Magnetic Refrigeration Market Report is Segmented by Product Type (Refrigeration Systems, Air-Conditioning Systems, Heat Pumps, and More), Cooling Capacity (Sub 100 W, 100-1 KW, 1-10 KW, and Above 10 KW), Application (Commercial Refrigeration, Residential Appliances, and More), End-Use Industry (Food and Beverage, Automotive and Mobility, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

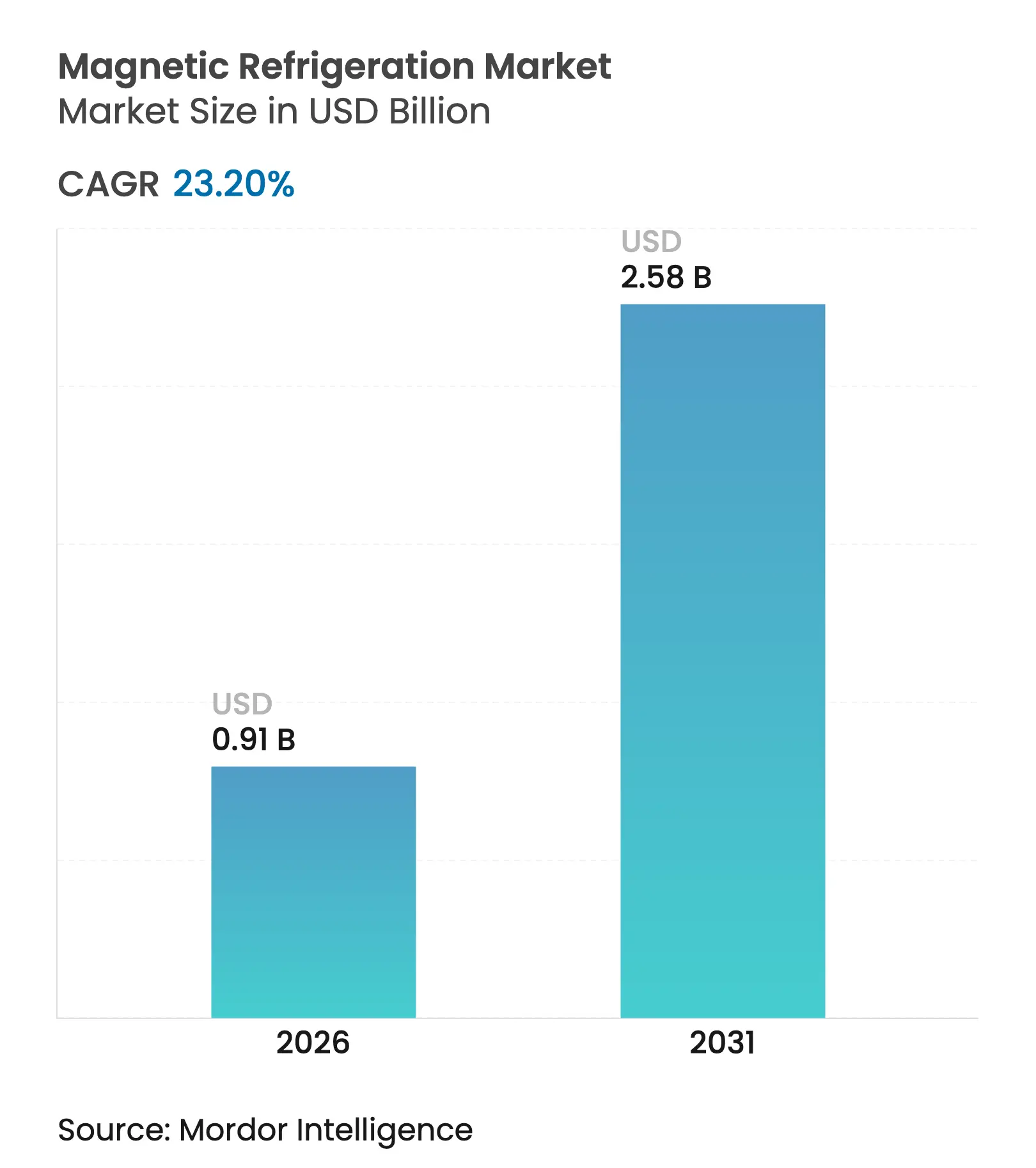

| Market Size (2026) | USD 0.91 Billion |

| Market Size (2031) | USD 2.58 Billion |

| Growth Rate (2026 - 2031) | 23.20 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Magnetic Refrigeration Market size was valued at USD 0.74 billion in 2025 and estimated to grow from USD 0.91 billion in 2026 to reach USD 2.58 billion by 2031, at a CAGR of 23.2% during the forecast period (2026-2031). This strong trajectory follows the magnetocaloric effect’s ability to deliver cooling without fluorinated gases, an advantage that aligns with tightening global climate regulations. Rapid progress in magnetocaloric materials, along with falling magnet costs, continues to shorten payback periods for early adopters. Europe retains leadership because its F-gas phase-down rules compel end users to abandon hydrofluorocarbon systems, while Asia-Pacific moves up the adoption curve on the back of hyperscale data-center expansion. As commercialization gains speed, system vendors broaden their portfolios to span capacities from laboratory-scale cryocoolers to multi-kilowatt industrial heat pumps, further anchoring the magnetic refrigeration market on a steep growth path.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing Adoption of Magnetocaloric Wine and Beverage Coolers in EU HoReCa Sector Growing Adoption of Magnetocaloric Wine and Beverage Coolers in EU HoReCa Sector | 3.20% | Europe, North America | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:3.20% | Geographic Relevance:Europe, North America | Impact Timeline:Medium term (2-4 years) |

Rapid R&D Funding for Cryogen-Free ULT Freezers in North America Rapid R&D Funding for Cryogen-Free ULT Freezers in North America | 4.10% | North America, Global | Long term (≥ 4 years) | |||

Decarbonisation Mandates Boosting Industrial Heat-Pump Pilots in Nordics Decarbonisation Mandates Boosting Industrial Heat-Pump Pilots in Nordics | 2.80% | Nordic countries, Europe | Medium term (2-4 years) | |||

EU F-Gas Phase-Down Accelerating Replacement of Synthetic Refrigerants EU F-Gas Phase-Down Accelerating Replacement of Synthetic Refrigerants | 5.30% | Europe, Global | Short term (≤ 2 years) | |||

Data-Centre Cooling Energy-Efficiency Targets in Asian Hyperscale Campuses Data-Centre Cooling Energy-Efficiency Targets in Asian Hyperscale Campuses | 4.70% | Asia-Pacific, Global | Medium term (2-4 years) | |||

Aerospace Thermal-Management Needs for Electrified Aircraft Platforms Aerospace Thermal-Management Needs for Electrified Aircraft Platforms | 1.90% | Global | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Growing Adoption of Magnetocaloric Wine and Beverage Coolers in EU HoReCa Sector

European restaurants and hotels now deploy magnetocaloric wine cabinets that trim energy use by 20-30% while keeping temperature within ±0.5 °C, performance that satisfies both efficiency benchmarks and sommeliers’ quality expectations.[1]Royal Society of Chemistry, “Gadolinium – Element Information, Properties and Uses,” periodic-table.rsc.org Quiet, vibration-free operation enhances the dining experience, prompting premium outlets to accept higher capital outlay in exchange for lower lifetime costs. Government incentives for low-GWP equipment shorten payback times and stimulate wider rollouts. International hotel chains replicate the concept in North America, adding further scale to the magnetic refrigeration market. Vendors report lower maintenance calls because the systems omit mechanical compressors.

Rapid R&D Funding for Cryogen-Free ULT Freezers in North America

U.S. federal programs channel capital into magnetocaloric freezers that cool to 560 µK without liquid helium, an approach that removes supply-chain risk for critical research labs.[2]Raba et al., “Aluminum Nuclear Demagnetization Refrigerator for Powerful Continuous Cooling,” doi.org Universities and biotech firms adopt early prototypes to preserve vaccines and genomic samples. The design freedom gained from eliminating cryogens allows footprint reductions that release valuable laboratory floor space. Material breakthroughs such as YbNi1.6Sn raise entropy density, enabling compact systems with higher power density. Accelerated funding keeps development teams on aggressive timelines, moving the magnetic refrigeration market toward larger production runs.

EU F-Gas Phase-Down Accelerating Replacement of Synthetic Refrigerants

Regulation EU 2024/573 mandates an 85% cut in hydrofluorocarbon consumption by 2036, propelling European retailers to replace HFC-based equipment well before sunset dates climate.[3]Overview Source: European Commission, “EU-Rules – Fluorinated Greenhouse Gases – Climate Action,” climate.ec.europa.eu Quota scarcity already inflates HFC prices, tilting total cost of ownership calculations toward magnetocaloric technology. Supermarket chains conducting fleet renewals prioritise installations that ensure lifelong regulatory compliance. Equipment makers advertise “future-proof” branding, a message that resonates with investors seeking to avoid stranded assets. The regulation creates an immediate pull that benefits the magnetic refrigeration market across commercial, industrial, and residential channels.

Data-Centre Cooling Energy-Efficiency Targets in Asian Hyperscale Campuses

China’s Eastern Data, Western Compute program and similar initiatives in Japan demand power usage effectiveness below 1.2, pressing operators to explore refrigerant-free cooling.[4]The Onero Institute, “Rethinking China’s Data Center Strategy for AI Dominance,” oneroinstitute.org Magnetocaloric chillers integrate with waste-heat recovery loops, delivering up to 21% carbon savings compared with standard air-cooled setups. Operators value the absence of refrigerant leaks that can trigger environmental penalties. Modular system design matches the phased expansion plans typical of hyperscale campuses. Asia-Pacific therefore emerges as a pivotal growth arena for the magnetic refrigeration market over the next five years.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Critical Material Supply Risk for Gd-Based Alloys Critical Material Supply Risk for Gd-Based Alloys | -3.80% | Global | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-3.80% | Geographic Relevance:Global | Impact Timeline:Medium term (2-4 years) |

Scalability Challenges in High-Flux Permanent-Magnet Assemblies Scalability Challenges in High-Flux Permanent-Magnet Assemblies | -2.90% | Global | Short term (≤ 2 years) | |||

Limited OEM and Installer Skillset for AMR Systems Limited OEM and Installer Skillset for AMR Systems | -1.70% | Global | Medium term (2-4 years) | |||

Absence of Global Performance Standards and Test Protocols Absence of Global Performance Standards and Test Protocols | -1.40% | Global | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Critical Material Supply Risk for Gd-Based Alloys

Gadolinium processing is concentrated in a handful of Chinese facilities, exposing buyers to export controls and price swings that threaten production schedules. United States policy now classifies rare earths as strategic, yet domestic mining at Mountain Pass remains capacity-limited. Research teams accelerate work on La-Fe-Si-H compounds that replicate performance while cutting gadolinium demand. Recycling programs for decommissioned MRI magnets offer supplementary supply but require new value-chain coordination. Although alternative chemistries advance, near-term sourcing volatility still weighs on the magnetic refrigeration market.

Scalability Challenges in High-Flux Permanent-Magnet Assemblies

Commercial units target flux densities beyond 1.4 T, levels that necessitate intricate Halbach arrays assembled with tight tolerances. Magnet costs can reach 40% of bill of materials, so manufacturers seek simplified geometries to ease automation. Recent prototypes use segmented blocks instead of fully nested cylinders, trimming material waste by 15%. Suppliers experimenting with SmCo magnets gain thermal stability but confront higher raw-material expenses. Until repeatable high-volume assembly lines mature, this restraint will temper unit-cost reductions across the magnetic refrigeration market.

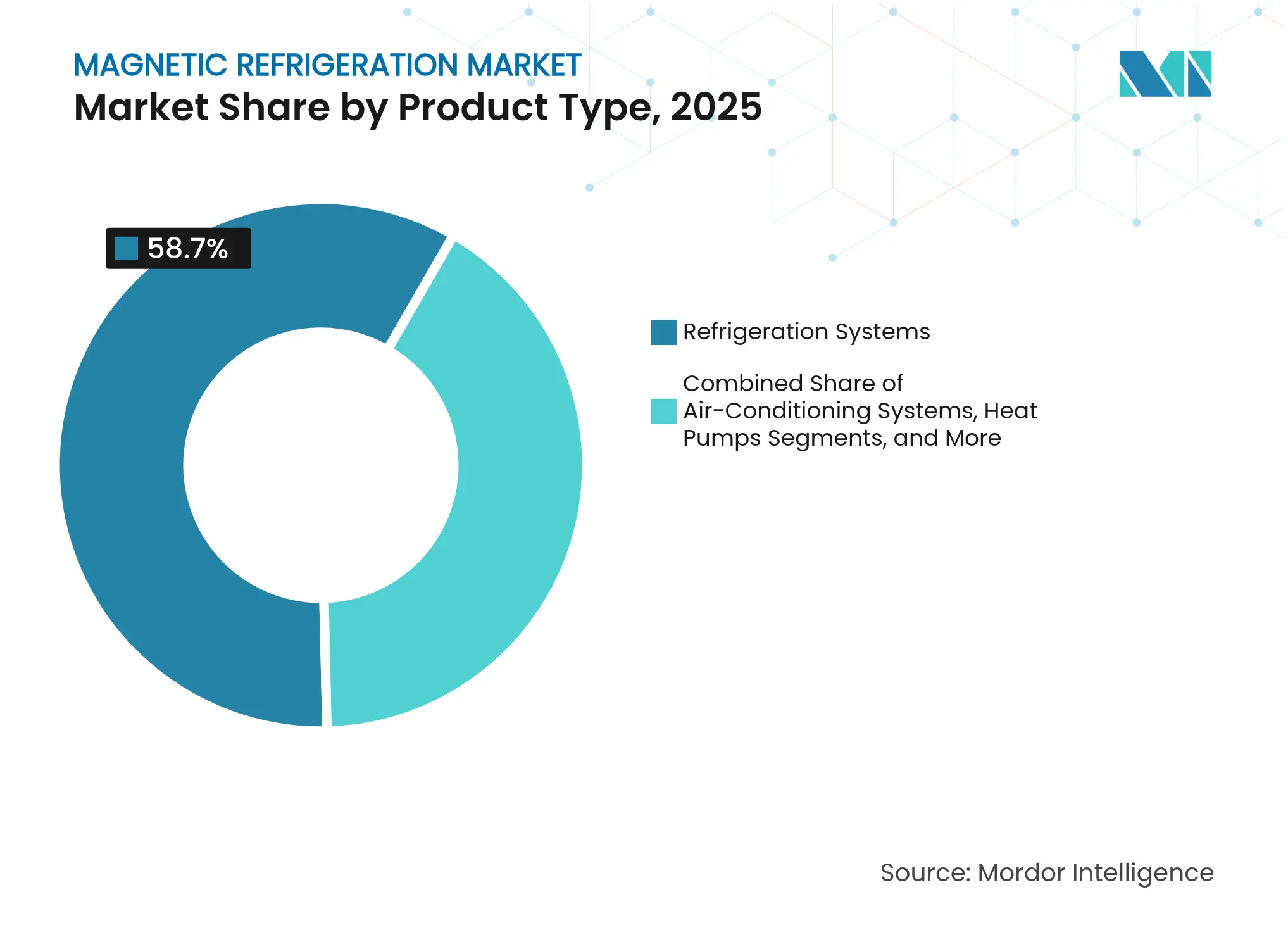

By Product Type: Heat Pumps Accelerate Commercial Viability

Refrigeration systems represented 58.70% of 2025 revenue as food service, retail, and beverage sectors opted for drop-in replacements that exploit existing form factors. Unit economics continue to improve through magnet cost declines, solidifying the magnetic refrigeration market in core refrigeration use cases. Heat pumps recorded a 26.1% CAGR forecast, reflecting strong industrial and residential decarbonization mandates. The segment’s higher operating temperatures complement district heating grids, positioning vendors for larger contract values. Air-conditioning solutions compete where dual heating-cooling performance is valued but still trail heat-pump efficiency at upper temperature lifts. Premium wine coolers carve out a small yet visible niche in luxury hospitality, signalling consumer-facing potential once manufacturing costs fall. Cryogenic and ULT freezers claim early adoption in research campuses that seek helium independence, validating ultra-low temperature viability for the magnetic refrigeration industry. Across categories, the drive to eliminate synthetic refrigerants ensures sustained product diversification within the magnetic refrigeration market.

Innovations in heat-pump architectures now enable inlet temperatures up to 280 °C, unlocking chemical and paper-mill applications previously unreachable by compressor-based alternatives. Pilot units integrated into Nordic district heating loops supply 200 GWh of renewable heat annually, providing high-profile demonstrations that draw interest from other European utilities. Vendors stress modularity, offering cartridges that scale output without redesigning the hydraulic backbone. System integrators collaborate with building-information-modeling platforms to streamline design approvals, reducing soft costs for installers. As OEM skill sets mature, after-sales networks grow, meaning buyers gain confidence in long-term service availability. The magnetic refrigeration market therefore builds momentum in both existing refrigeration formats and emergent heat-pump deployments.

Note: Segment shares of all individual segments available upon report purchase

By Cooling Capacity: Mid-Range Dominance With Industrial Upswing

The 100-1 kW class retained 45.10% share of the magnetic refrigeration market size in 2025 by fitting seamlessly into convenience-store cases, under-counter chillers, and laboratory units. These volumes give suppliers the economies of learning needed to drive magnet optimization programs. Sub-100 W devices address point-of-care diagnostics and portable vaccine carriers, where silent operation eliminates acoustic shielding requirements. The 1-10 kW tranche increasingly serves edge data rooms and back-of-house hospitality functions that require moderate loads and footprint flexibility. Above-10 kW systems, though only emerging, are projected to log 24.1% CAGR as industrial users scale demonstration projects. Their ability to dovetail with existing glycol loops reduces the engineering burden of plant retrofits, attracting early adopters keen on low-GWP credentials.

Demonstrator units now exceed 15 kW while retaining 60% of the theoretical Carnot limit, a performance milestone that signifies readiness for process industries. Higher capacities benefit from linear magnet cost scaling, creating favorable USD/kW trajectories compared with smaller machines. Research consortia push flux density uniformity to minimise parasitic losses, thereby boosting system COP. Integrators overlay digital twins to track temperature glide dynamics, informing predictive maintenance routines that extend system life. As supply chains stabilise, capacity brackets will incrementally move upward, enlarging the addressable share of the magnetic refrigeration market.

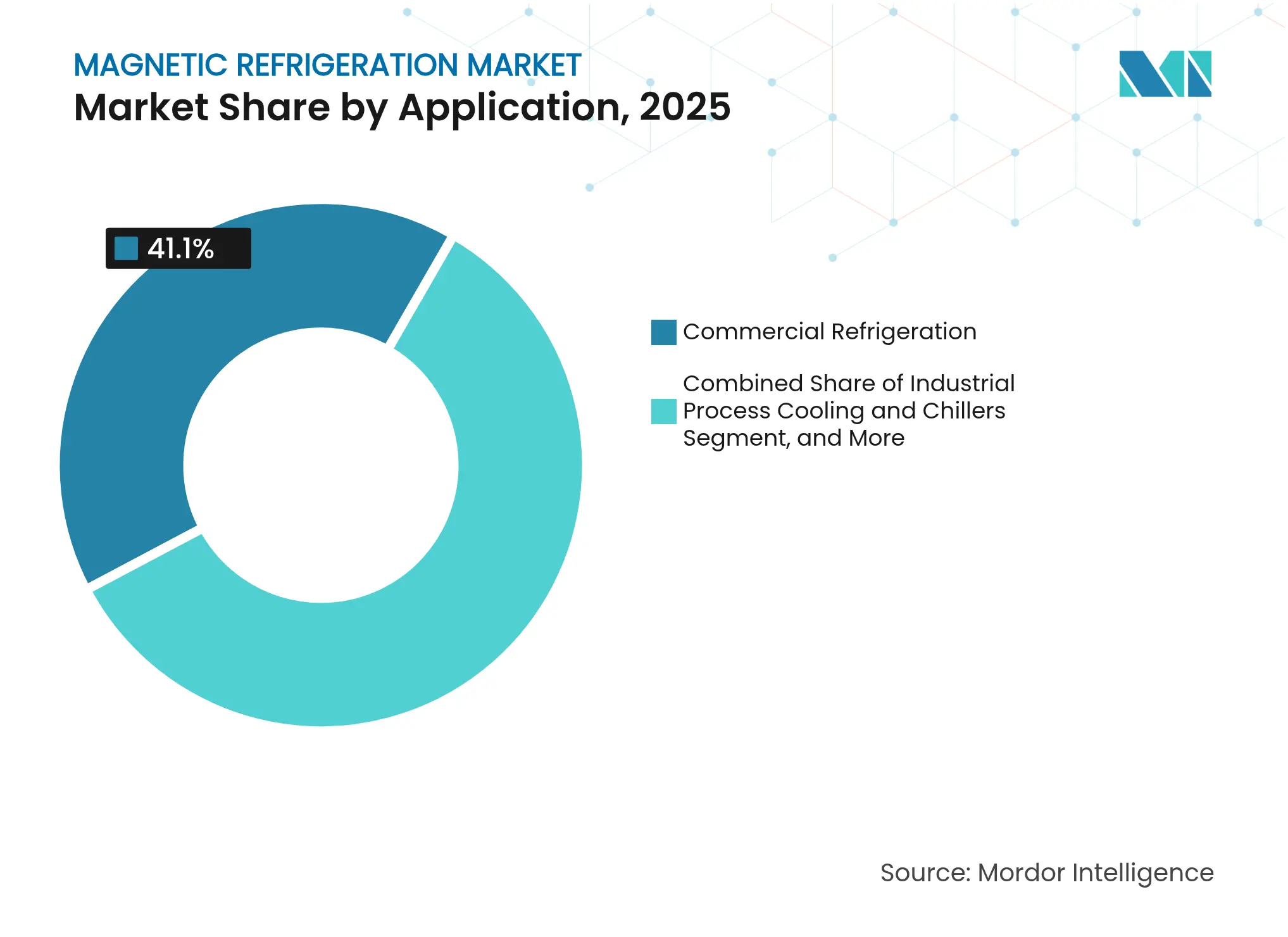

By Application: Data-Centre Cooling Drives New Demand

Commercial refrigeration still accounted for 41.10% of 2025 deployments, buoyed by supermarket chain retrofits and quick-service restaurant rollouts. Energy-intensive verticals confront mounting electricity tariffs, making 20-30% efficiency gains economically compelling. Yet data-centre and electronics cooling chalks up a 30% CAGR outlook, positioning the segment as the single fastest demand generator within the magnetic refrigeration market. Hyperscalers execute multi-megawatt expansions that call for precision temperature control and leak-free coolants. Magnetic chillers interlock with waste-heat redistribution circuits, enabling operators to sell reclaimed heat to district networks. Industrial process cooling also grows as manufacturers pursue Scope 1 emission cuts under net-zero pledges, though adoption remains gated by capacity scaling.

Medical and laboratory equipment continues to value helium-free operation, an attribute that shields users from supply disruptions and volatile pricing. Transportation applications, especially electric buses and rail carriages in densely populated corridors, explore magnetocaloric HVAC modules to curb top-up refrigerant requirements. Residential appliances lag because price premiums are still high, but early-adopter households in high-income regions buy premium refrigerators for their silent operation. Combined, these disparate applications diversify revenue streams and reduce reliance on any single vertical, reinforcing stability in the magnetic refrigeration market.

Note: Segment shares of all individual segments available upon report purchase

By End-Use Industry: Healthcare Surges Ahead

Food and beverage retained 37.40% share of the magnetic refrigeration market in 2025 thanks to widespread cold chain investment linked with e-grocery growth. Retailers adopt storewide magnetocaloric display cases to meet ESG commitments and secure utility-rebate incentives. Meanwhile healthcare and life-sciences is on track for 24.9% CAGR as biobanks, pharma manufacturers, and gene therapy labs widen their cryogen-free infrastructure. Hospitals appreciate the low vibration profile that protects sensitive imaging equipment housed nearby. Automotive OEMs look to magnetocaloric cabin conditioning and battery thermal management to extend electric-vehicle range, though mass-market release will hinge on further cost downs.

Aerospace firms weigh the technology for lightweight hydrogen-electric propulsion cooling needs, an application where every kilogram saved translates to mission range gains. Semiconductor fabs investigate spot cooling at lithography stages to stabilise resist performance, further broadening the magnetic refrigeration market footprint. Supermarket retrofits in Europe set the tone for emerging regions that plan to leapfrog legacy refrigerants, thereby promising new volume pockets. Across end users the common theme remains regulation-driven urgency to exit high-GWP refrigerants, an imperative that positions magnetocaloric systems as a secure long-term asset.

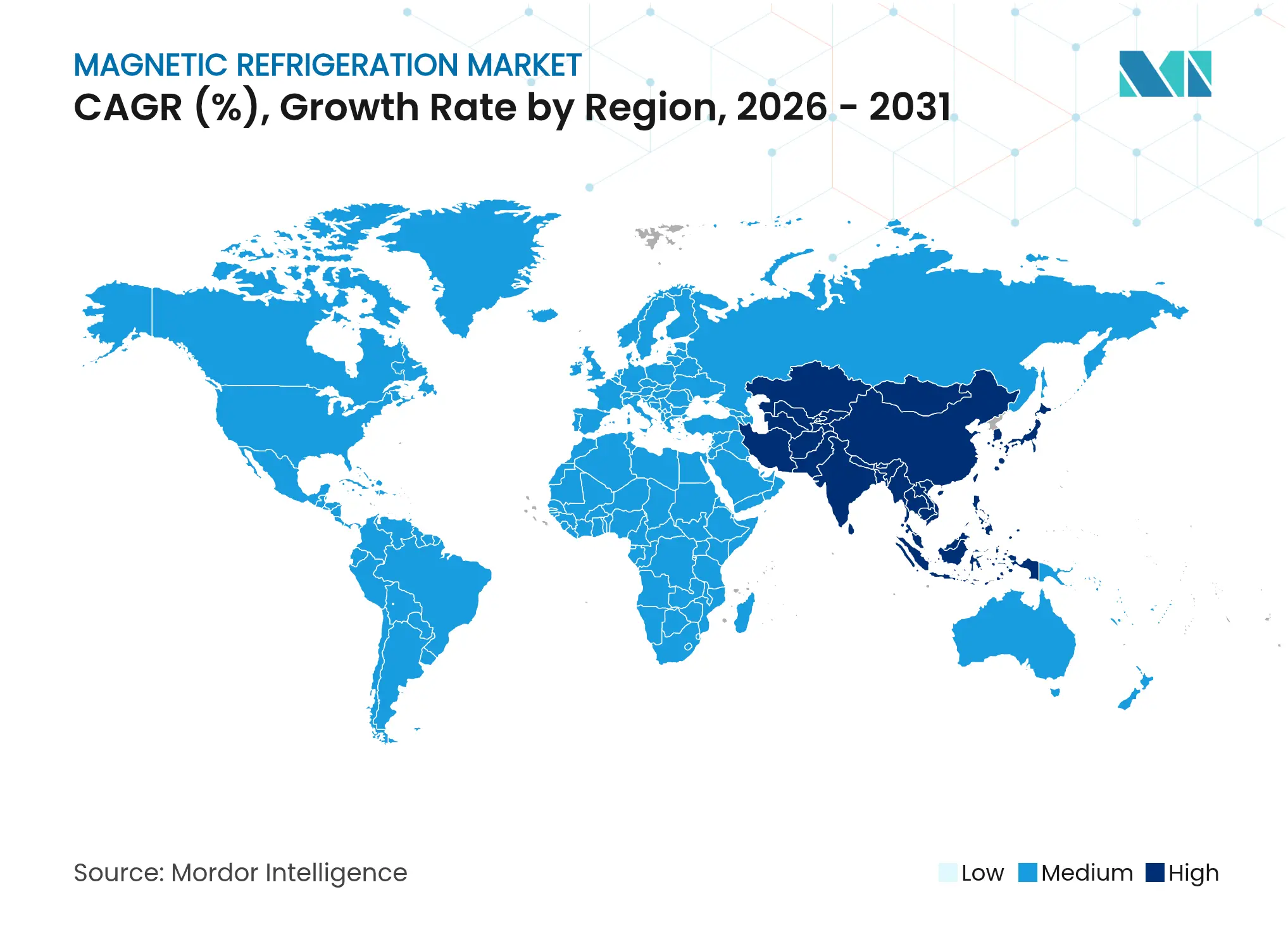

Europe led with 40.20% revenue share in 2025 because its F-gas legislation accelerates procurement of refrigerant-free systems. Regional utilities now launch tenders that bundle district heating upgrades with magnetocaloric heat pumps, creating large single-buyer volumes. Germany and France channel public funds into pilot lines for advanced magnet materials, nurturing a competitive supplier base. Southern European hospitality operators adopt magnetocaloric beverage coolers to comply with building-energy codes yet maintain front-of-house ambiance.

Asia-Pacific, already the world’s largest data-centre build market, posts a 25.6% CAGR outlook through 2031. China’s tier-two cities mimic hyperscale construction seen in coastal hubs, amplifying demand for high-efficiency cooling. Japan’s Green Transformation initiative earmarks subsidies for equipment that improves grid stability while cutting greenhouse-gas intensity. South Korea’s semiconductor expansion adds laboratory-grade cryogenic needs, while Australia’s hospitality sector pursues emission abatement in remote off-grid resorts. Collectively these factors ignite the magnetic refrigeration market across the region.

North America benefits from deep R&D pipelines, federal grants, and aerospace demand for lightweight thermal management. Government laboratories collaborate with start-ups to refine active magnetic regenerator stacks, accelerating technology readiness levels. Canada’s carbon pricing framework nudges supermarkets toward refrigerant-free upgrades, and Mexico’s maquiladora factories pilot magnetocaloric process chillers to differentiate export products. South America and the Middle East & Africa trail in adoption but plan demonstrators aligned with national energy-efficiency roadmaps, indicating a widening future footprint for the magnetic refrigeration market.

Market Concentration

Competition remains fragmented, with no single brand exceeding a double-digit global share. Specialist developers such as Cooltech Applications and MAGNOTHERM Solutions advance proprietary materials and regenerator geometries that yield higher temperature spans. Appliance giants including GE Appliances and Whirlpool Corporation license or partner to fast-track consumer-grade offerings that can leverage existing distribution channels. Asian electronics groups add internal R&D programs to secure in-house magnet expertise, thereby guarding against supply bottlenecks.

Strategic moves include vertical integration. General Engineering & Research scales bulk La-Fe-Si-H production to kilogram batches at sub-USD 1,000 /kg, narrowing the cost gap with legacy refrigerant compressors. MAN Energy Solutions wins flagship district-heating projects, showcasing large-scale magnetocaloric heat pumps as drop-in replacements for gas boilers. Delft University spinoff Magneto capitalizes on research depth to create modular 500 W cassette units marketed to hospitality buyers.

Patent filings concentrate on magnet topologies and multi-material regenerator beds that flatten the ΔT curve across the cycle, extending life and efficiency. Companies race to establish service footprints able to guarantee uptime in commercial settings, a key purchase criterion for retail and data-centre operators. Because total addressable demand spans several verticals, new entrants still find room to specialise, ensuring the magnetic refrigeration market stays dynamic as it scales.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUES)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

The magnetic refrigeration market involves the development and commercialization of cooling systems that use the magnetocaloric effect to transfer heat without the need for traditional refrigerants. These systems offer energy-efficient, eco-friendly, and low-maintenance alternatives to conventional refrigeration technologies. The market spans various applications, including commercial refrigeration, air conditioning, and industrial cooling, driven by the demand for sustainable solutions.

The Magnetic Refrigeration Market is segmented by product type (refrigeration systems, air conditioning systems, heat pumps, and other product types), application (commercial refrigeration, residential refrigeration, industrial cooling, medical and laboratory equipment, transportation cooling, and other applications), end-use industry (food and beverage, healthcare, automotive, electronics, aerospace, and other end-use industries), and geography (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Wealth Management Intelligence for the Middle East

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.