Density Meter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.17 Billion |

| Market Size (2031) | USD 1.42 Billion |

| Growth Rate (2026 - 2031) | 4.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

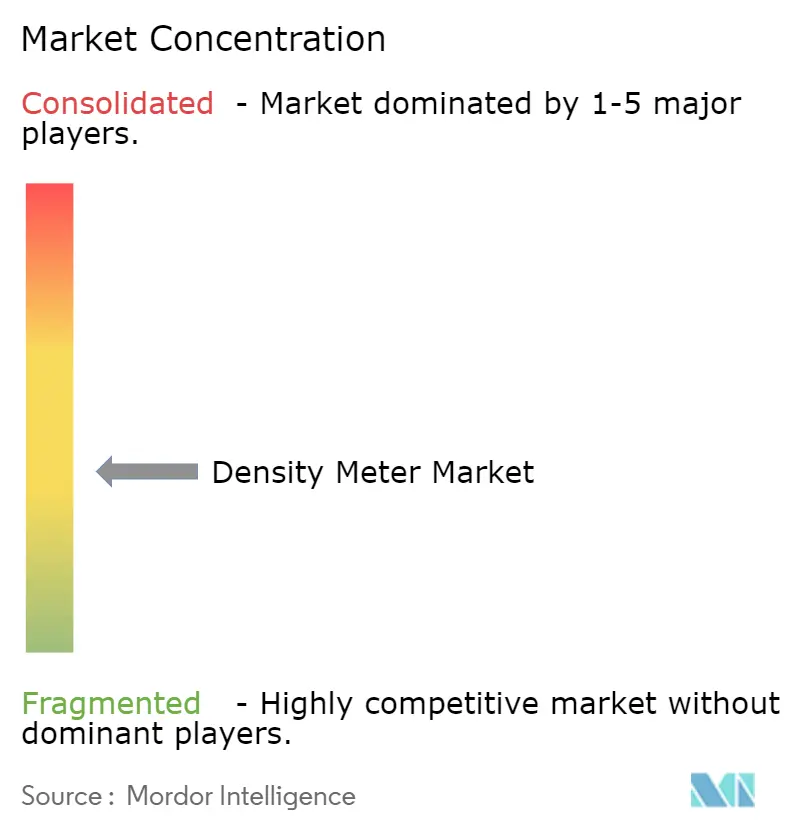

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Density Meter Market Analysis by Mordor Intelligence

The density meter market size was valued at USD 1.12 billion in 2025 and estimated to grow from USD 1.17 billion in 2026 to reach USD 1.42 billion by 2031, at a CAGR of 4.03% during the forecast period (2026-2031). Growing investment in Industry 4.0 platforms, stricter custody-transfer rules in hydrocarbons, and the expansion of continuous bioprocessing collectively sustain long-term purchasing momentum. Asia-Pacific anchors global unit volumes thanks to rapid industrialization, while the Middle East and Africa accelerates fastest on the back of desalination and mining projects. Coriolis designs dominate the installed base, yet ultrasonic systems are registering the strongest uptake as mining operators seek non-invasive monitoring for abrasive slurries. Handheld meters are reshaping field work practices, and software-enabled predictive maintenance is emerging as a key differentiator for premium brands.

Key Report Takeaways

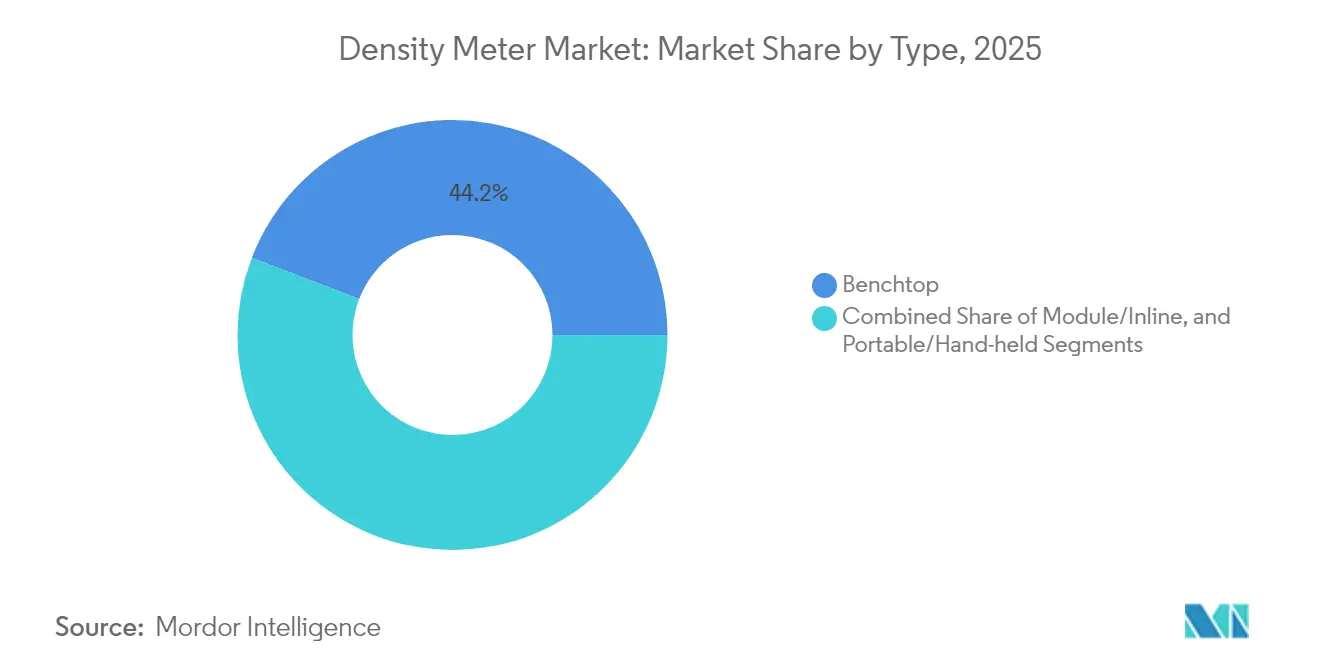

- By measurement technology, Coriolis meters led with 34.32% of density meter market share in 2025, whereas ultrasonic devices are poised for 6.78% CAGR growth through 2031.

- By instrument format, benchtop units accounted for 44.15% of the density meter market size in 2025, while handheld models are expanding at a 6.19% CAGR to 2031.

- By fluid type, liquid applications represented 67.12% of 2025 revenue; slurry monitoring is projected to grow 4.98% annually through 2031.

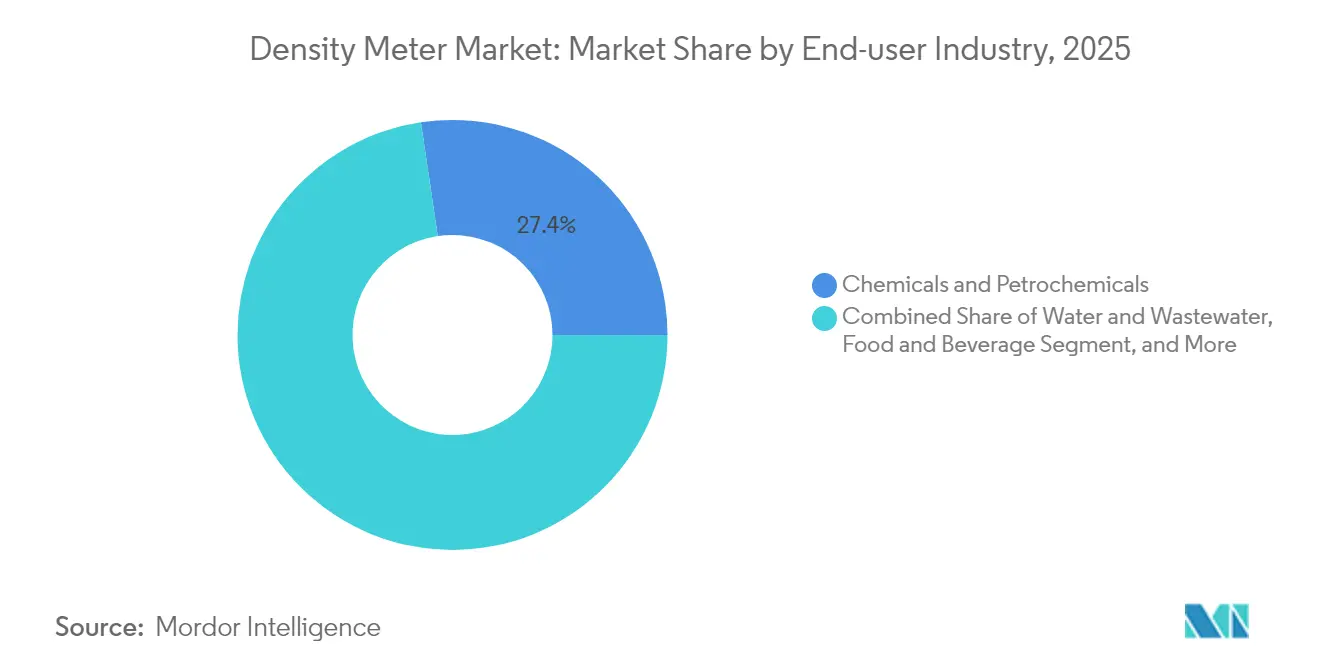

- By end-user, chemicals and petrochemicals held 27.35% revenue share in 2025, whereas water and wastewater treatment will register the fastest 5.93% CAGR to 2031.

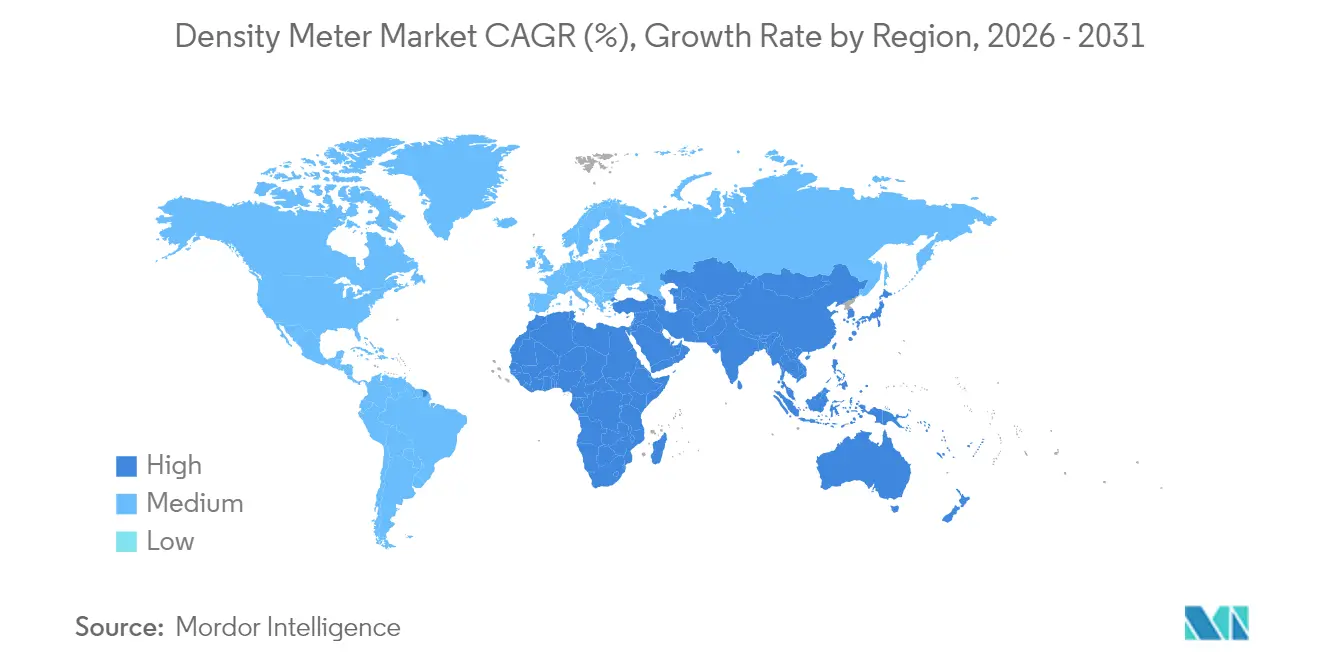

- By geography, Asia-Pacific captured 33.62% of 2025 revenue, while the Middle East and Africa is set to advance at 6.08% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Density Meter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital transformation elevating demand for real-time density monitoring | +0.8% | North America, spillover to Europe | Medium term (2-4 years) |

| Stricter custody-transfer rules in oil and gas | +0.6% | Global, focus on Middle East and North America | Short term (≤ 2 years) |

| Inline quality control in craft beverages | +0.3% | Europe, expanding to North America | Medium term (2-4 years) |

| Slurry-density optimization in mining | +0.4% | South America, applications in APAC | Long term (≥ 4 years) |

| Continuous biopharma manufacturing | +0.5% | Asia-Pacific core, spillover to West | Medium term (2-4 years) |

| Desalination projects in arid regions | +0.4% | Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital Transformation in Process Industries Elevating Demand for Real-Time Density Monitoring in North America

Factories across North America now embed smart density sensors within MES and LIMS networks, enabling predictive models that cut idle time and tighten product-quality distributions.[1]BioProcess International, “Real-Time, Data-Driven, and Predictive Modeling,” bioprocessintl.com Cloud-hosted analytics combine density, viscosity, and flow data to optimize refinery set-points, as demonstrated at Ergon Refining’s specialty plants.[2]Emerson, “Ergon Refining: A digital transformation story,” emerson.com Inline meters deliver continuous verification that supersedes lab batch tests, and embedded AI algorithms now alert technicians to drift long before off-spec batches appear. Regulatory regimes in food and pharma further accelerate uptake because digital audit trails simplify compliance reporting.

Stricter Custody Transfer Regulations in Global Oil and Gas Sector Boosting Inline Density Meter Installations

Fiscal metering rules now cap uncertainty at below 0.1% for hydrocarbon custody transfers, positioning Coriolis meters as the default solution for pipelines and floating storage units.[3]OnePetro, “Novel Application of Coriolis Meters in Custody Transfer Applications,” onepetro.orgADNOC’s sales-gas network has validated lower OPEX and wider turndown compared to legacy ultrasonic devices, while AGA and ISO standards have been amended to reference Coriolis performance benchmarks. Emerging producers in Africa and Latin America are adopting these standards, thereby expanding the addressable pool for advanced inline instruments that deliver simultaneous mass-flow and density readings.

Rising Adoption of Inline Quality Control in Craft Beverage Industry Across Europe

Micro-breweries and distilleries in Germany and the U.K. are installing compact alcohol-density meters to comply with excise rules and to minimize lab outsourcing costs. Scotch whisky distillers report 0.1%–0.4% accuracy after switching to Coriolis flowmeters, assuring consistent mouthfeel and ABV declaration. Success stories are seeding similar investments among North American craft producers seeking data-driven fermentation control.

Slurry-density optimization in mining

Copper concentrators in Chile and Peru are embedding ultrasonic probes to measure tailings density in pipelines, cutting water use and energy draw in thickening circuits. New non-invasive sensors withstand abrasive slurries and temperatures above 90 °C, yielding real-time feedback for reagent dosing and pump speed adjustments. Multinational miners aim to replicate these gains at Indonesian nickel and Australian iron-ore sites by 2027.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Radioactive-source licensing challenges for nuclear gauges | -0.3% | Europe, spillover to other developed regions | Short term (≤ 2 years) |

| High calibration costs for Coriolis meters in emerging economies | -0.4% | APAC and South America | Medium term (2-4 years) |

| Ultrasonic performance drift in hot slurries | -0.2% | Global mining and metallurgy | Long term (≥ 4 years) |

| Price pressure from low-cost Chinese suppliers | -0.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Radioactive-Source Licensing Challenges Limiting Nuclear Density Meter Uptake in Europe

Directive 2013/59/Euratom tightened safety standards, adding recurrent audits and mandatory operator training that raise lifecycle costs for nuclear gauges. Device makers must secure Part 32 licenses and track sealed sources through detailed inventory logs, discouraging small processors that once relied on gamma-ray instruments. Users now gravitate toward ultrasonic or microwave alternatives that eliminate radiological liabilities, accelerating technology substitution across bulk-solids handling and asphalt-mix plants.

High Initial Calibration Costs for Coriolis Density Meters in Emerging Economies

Traceable calibration routines require specialized rigs and reference fluids that few local labs can supply, pushing annual verification expenses beyond 10% of hardware price for many Brazilian and Indian processors. Service engineers from regional hubs add travel fees and downtime, prompting cost-sensitive buyers to opt for vibrating-tube or differential-pressure meters that meet “fit-for-purpose” accuracy thresholds. Suppliers are responding with extended calibration intervals and embedded diagnostics, but adoption gaps will persist until certified facilities proliferate in growth markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Handheld Growth Reshapes Field Measurement

Benchtop units held 44.15% of 2025 revenue, anchored in pharma QC and chemical formulation labs that value multi-parameter analysis and stringent documentation. Conversely, handheld instruments posted a 6.19% CAGR and will surpass USD 318.6 million by 2031, driven by remote pipeline surveys, on-the-spot beverage checks, and mobile mining crews. The density meter market size for portable devices is on a clear upswing as manufacturers add temperature compensation, RFID sample tracking, and Bluetooth export to LIMS platforms.

A broader push toward decentralized decision-making reinforces the shift. Operators now validate product density at the point of fill, avoiding lab queues and catching deviations early. Rugged ABS housings withstand dust and splash, while on-board lithium packs deliver eight-hour autonomy. Enhanced firmware performs automatic viscosity correction, enabling field accuracy within ±0.001 g/cm³. This versatility is expanding addressable use cases from dairy plants to biodiesel terminals, tightening quality loops and curbing rework rates.

By Measurement Technology: Coriolis Dominance Meets Ultrasonic Momentum

Coriolis instruments commanded 34.32% density meter market share in 2025, cemented by unmatched ability to capture mass-flow and density simultaneously-a boon for fiscal custody and recipe control. High-end models achieve ±0.05% density accuracy and self-diagnose coating or two-phase flow, lowering unplanned outages. Feature-rich firmware reduces recalibration frequency from yearly to triennial, trimming ownership costs.

Ultrasonic variants, however, are advancing at a 6.78% CAGR on the strength of clamp-on designs that avert downtime and sanitation worries in dairy, pulp, and mining pipelines. MEMS-powered micro-Coriolis prototypes also surface for micro-reactor and drug-delivery applications where sample volumes are measured in microliters. Suppliers that blend digital twins with inline diagnostics are best positioned as buyers prioritize predictive maintenance over mere sensor accuracy.

By End-user Industry: Water and Wastewater Lead Growth Curve

Chemicals and petrochemicals retained the largest slice at 27.35% in 2025, reliant on tight density control for blending, custody, and emissions accounting. Yet water and wastewater utilities will clock a 5.93% CAGR thanks to desalination mega-projects in Saudi Arabia and the UAE, as well as potable reuse initiatives in California. Density readings guide membrane fouling diagnostics and brine concentration, safeguarding system uptime and optimizing energy draws.

Denser adoption also permeates biological nutrient removal where mixed-liquor density links directly to aeration demand. Smart networks feed readings to AI engines that shave power costs by up to 12%, validating payback in under two years. Across municipal bids, preference now tilts toward meters offering IP68 housings and NB-IoT connectivity for buried reservoirs and sewer interceptors.

By Fluid Medium: Slurry Use-Cases Accelerate

Liquid measurement still drives 67.12% of revenue in 2025, yet slurry applications will outpace with 4.98% CAGR to 2031 as miners optimize tailings consolidation. The density meter market size for mining slurries will top USD 197.4 million by 2031. Operators deploy non-invasive acoustic meters to withstand abrasion at 20 bar line pressures.

Enhanced algorithms now factor particle size distribution and temperature, helping concentrators hit target pulp density within ±0.5% and improving downstream flotation recoveries. Gas-phase measurements remain niche but vital for LNG boil-off and HVAC refrigerant charge monitoring, where density influences energy efficiency and emissions compliance.

Geography Analysis

Asia-Pacific led with 33.62% revenue in 2025, propelled by China’s vast refining and chemical complexes, India’s surging biologics capacity, and South Korea’s semiconductor investments. The density meter market continues to benefit from government programs that reward smart-factory retrofits and sustainability reporting. Japan’s focus on zero-defect automotive fluids further sustains premium sales of laboratory instruments.

The Middle East and Africa, though smaller, deliver top-line acceleration at a 6.08% CAGR as desalination, green hydrogen, and remote pipeline monitoring gain momentum. Saudi Aramco’s upstream projects utilize Coriolis meters in multiphase separators, whereas UAE utilities employ density-based control loops to enhance reverse-osmosis recovery ratios. South African platinum miners retrofit ultrasonic probes to cut water use in tailings thickeners. North America maintains robust replacement demand as chemical and food processors digitize legacy plants. Government incentives for IIoT adoption amplify orders for Ethernet-IP-enabled meters. Europe’s stringent carbon and alcohol tax frameworks underpin steady upgrades, despite energy cost headwinds. South America’s focus on tailings dam safety catalyzes slurry-meter retrofits in Chilean copper and Brazilian iron-ore operations.

Regulatory Landscape

Density meters used for trade-relevant hydrocarbon and chemical measurements fall under national metrology and legal metrology frameworks, where recognized methods and traceable calibration support market acceptance. Key anchors include ISO 12185:2024 (oscillating U-tube method for petroleum and related products) and ASTM D4052-18 (digital density meter method), which are commonly referenced for laboratory and quality-control workflows. In China, the State Administration for Market Regulation issued JJF 2165-2024 (October 2024), a calibration specification for laboratory oscillation-type liquid density meters that took effect on April 19, 2025, tightening expectations around verification and traceability for lab-grade instruments.

For industrial and process deployments, compliance is shaped by performance and evaluation standards and regional conformity regimes. IEC published IEC 61298-1:2026, which sets general performance evaluation methods for process measurement and control devices, reinforcing harmonized test approaches that OEMs can map to inline density measurement claims. In Europe, Directive (EU) 2026/706 amended the measuring instruments framework under Directive 2014/32/EU, keeping legal metrology modernization on the agenda. Great Britain continues to apply its Measuring Instruments Regulations 2016 regime, requiring manufacturers to manage separate conformity pathways when placing instruments on EU and GB markets.

Value Chain Analysis

The value chain starts with precision sensing elements and materials, then moves through instrument design, manufacturing, calibration, integration, and lifecycle services. Upstream inputs include corrosion-resistant alloys and wetted-part materials for aggressive chemicals and high-salinity water applications, alongside specialized oscillating elements (vibrating tube or tuning fork), high-stability electronics, and embedded firmware that supports diagnostics and connectivity. Midstream manufacturing is concentrated among large automation vendors and specialists such as Emerson, Endress+Hauser, Yokogawa, Anton Paar, Bopp & Reuther, and Berthold Technologies, with differentiation tied to mechanical tolerances, temperature compensation, and metrological traceability.

Downstream, sales and delivery split between direct OEM channels (common for calibration-intensive laboratory systems and regulated process applications) and industrial distributors or instrumentation partners for process hardware. System integrators and plant engineering contractors influence specification, especially where density measurement is bundled into custody-transfer skids, desalination control loops, or mining slurry pipelines. Post-sale services, including ISO/IEC 17025-aligned calibration, field verification, spare parts, and software updates, form a recurring value pool, and suppliers increasingly use connected diagnostics to reduce onsite visits and improve uptime for installed bases.

Competitive Landscape

The market skews moderately consolidated; the top five vendors hold roughly 55% of global revenue, balancing scale benefits with room for innovative entrants. Anton Paar leverages its global service grid and recent Brabender acquisition to bundle rheology and density technologies. Emerson integrates AI-driven analytics into its Promass line and capitalizes on Roxar multiphase know-how for upstream oil and gas. Mettler-Toledo concentrates on portable and lab niches, adding CFR Part 11-ready data integrity features.

Endress+Hauser’s 2025 alliance with SICK pools gas analysis and flow expertise, offering turnkey compliance packages for emissions monitoring. Newcomers commercialize MEMS-based micro-Coriolis chips for micro-fluidics, while Asian suppliers flood commodity segments with low-cost vibrating-tube meters, intensifying price pressure but lacking deep service support. Winning strategies hinge on predictive maintenance, open-protocol connectivity, and subscription-based calibration services that bundle compliance documentation.

Density Meter Industry Leaders

Anton Paar GmbH

VWR International (Avantor)

Thermo Fisher Scientific

Emerson Electric Co.

Mettler Toledo

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear whitespace sits at the intersection of density measurement and digital quality infrastructure, where plants increasingly want audit-ready, machine-readable traceability rather than paper certificates. The 2026 body of work demonstrating Digital Calibration Certificates (DCCs) for automated metrological traceability provides a practical route to integrate density verification into MES/LIMS-driven workflows, aligning with the report theme of software-enabled predictive maintenance and compliance documentation. Vendors that package instruments with digital certificates, diagnostics, and connectivity can standardize verification across multi-site operations in chemicals, refining, and biopharma continuous manufacturing.

Application-led opportunities focus on non-invasive and difficult-media measurement, where ultrasonic and other non-nuclear approaches address abrasive slurries, hot pipelines, and the radiological licensing constraints noted for nuclear gauges. Mining use cases in Chile and Peru that embed ultrasonic probes for tailings density control, alongside desalination and water reuse programs in the Middle East and parts of North America, create pull for rugged inline meters (IP-rated housings, remote telemetry, and stable compensation over temperature and solids loading). At the product level, demand is also shifting toward portable workflows, as handheld density meters extend field verification and reduce lab queues. This creates room for differentiated offerings that combine traceable calibration, Bluetooth/LIMS export, and simplified verification routines for distributed teams.

Recent Industry Developments

- June 2026: The IEC published IEC 61298-1:2026, updating general performance evaluation methods for process measurement and control devices. The release strengthens a common framework for how vendors substantiate performance claims in industrial instrumentation, supporting more consistent qualification of inline density measurement in regulated plants.

- March 2025: Anton Paar completed an investment in a new in-house glass production facility at its headquarters in Graz, Austria, increasing capacity for borosilicate glass oscillating U-tubes used in DMA density meters. Bringing this critical component further in-house improves control over tolerances and calibration stability, which can shorten lead times and reinforce product differentiation in laboratory density measurement.

- January 2024: Anton Paar closed the Brabender acquisition, expanding its global footprint and strengthening its portfolio across laboratory and process material characterization. The combination supports broader bundled offerings where density measurement is sold alongside adjacent testing and analytics, increasing cross-selling potential into chemicals, polymers, and food applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues earned from density meters used to measure mass per unit volume of liquids, gases, and slurry streams across industrial process lines, laboratories, and field testing. It includes benchtop instruments, in-line modules, and portable meters, regardless of the measurement principle used.

Scope exclusions: Medical bone densitometers and legacy glass hydrometers are excluded from this sizing.

Segmentation Overview

- By Type

- Benchtop

- Module/Inline

- Portable/Hand-held

- By Measurement Technology

- Coriolis

- Nuclear (Gamma)

- Ultrasonic

- Microwave

- Vibrating U-Tube

- Gravimetric (Hydrometer Replacement)

- By End-user Industry

- Water and Wastewater

- Chemicals and Petrochemicals

- Mining and Metal Processing

- Food and Beverage

- Healthcare and Pharmaceuticals

- Electronics and Semiconductors

- Oil and Gas (Upstream, Midstream, Downstream)

- Power and Utilities

- Research and Academic

- By Fluid Medium

- Liquids

- Gases

- Slurries and Suspensions

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Nordics

- Rest of Europe

- South America

- Brazil

- Rest of South America

- Asia-Pacific

- China

- Japan

- India

- South-East Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Gulf Cooperation Council Countries

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a view of demand signals that push density meter purchases, and mapping where those purchases show up by industry and region. We used public references such as industrial production series from government statistical agencies, trade and tariff line data from customs authorities, calibration and metrology guidance from national standards institutes, and standards documents from bodies such as ISO and ASTM, along with safety and compliance notes from regulators relevant to chemicals and oil and gas.

To make assumptions practical, we also reviewed company filings, product catalogs, distributor line cards, and investor presentations to understand typical product positioning and replacement cycles. Where helpful, a paid subscription focused on company financials and intelligence was used to sanity check revenue ranges and ownership changes, and a patent database was used to spot technology activity in sensing principles and inline measurement designs. These desk sources are illustrative only, and other public references were also used for collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work was used to confirm what is actually bought and installed, and which applications account for most of the value, especially where public data stays limited. We spoke with a mix of manufacturers, channel partners, and end users across process industries and lab settings. We then checked the outcomes across APAC, EMEA, and the Americas so regional adoption and pricing behavior could be compared on a like-for-like basis.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 17% | APAC: 46% |

| Mid tier: 45% | Functional/Unit leaders: 23% | EMEA: 36% |

| Smaller Players: 20% | Managers: 60% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where industrial output and trade indicators are used to reconstruct the demand pool for density measurement equipment, then filtered by likely adoption in process control and lab quality routines. After forming the market total, it was corroborated with selective bottom-up approximations, such as sampled product pricing, distributor feedback on shipment mixes, and a limited roll up of supplier revenue exposure. These were then used to adjust outliers.

Key inputs that shaped the model include process industry capex cycles (chemicals, refining, and related liquids processing), the installed base and replacement timing of inline instruments, the split between lab and process use, average selling price progression by form factor (benchtop, inline, portable), and calibration and compliance intensity that tends to pull demand forward. For forecasting, scenario analysis was used so different paths of industrial activity and project execution could be reflected, and the final path was aligned to what interviewees described as the most likely planning case. When a bottom-up signal was incomplete for a country or niche application, the gap was handled using proxy ratios from similar industries and neighboring markets, and then rechecked during validation.

Data Validation & Update Cycle

Outputs were validated through several checks so one data point could not drive the final number on its own. We compared the modeled totals against independent signals like instrument shipment commentary, regional industrial production movement, and the implied spend per relevant facility type, then reviewed any sharp jumps before sign-off.

Before publication, the model and assumptions go through multiple analyst review steps, and respondents are re-contacted when a variance cannot be explained through public evidence. The report is refreshed annually, and interim updates are made when material events occur, such as major regulation shifts or demand shocks in core process industries. A final pre-delivery pass is completed so clients receive the latest updated view.

Mordor Intelligence's Density Meter Market Sizing Compared With Other Published Estimates

It is normal to see different market size numbers for density meters because publishers do not always count the same products, years, and revenue streams. Differences also show up when one study leans more on vendor narratives, while another uses external demand indicators to keep the math anchored.

The table shows a noticeable spread across 2024 to 2026 values, and in Mordor Intelligence's model the market starts from electronic density meters used for liquids, gases, and slurries across lab, field, and inline process settings, while excluding medical bone densitometers and legacy glass hydrometers, which some broader instrument tallies can accidentally pull in.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.17 B (2026) | |

| Industry Research Publisher A | USD 1.21 B (2024) | Uses a different base year and a wider planning window, and its public scope language is broader, which can blend density meters with adjacent analytical instruments when definitions are not tightly separated. |

| Market Intelligence Publisher B | USD 1.12 B (2024) | Starts from a 2024 base and projects with higher growth assumptions, and the inclusions by product and application are described at a high level, which makes it harder to verify what is counted as process density measurement versus general lab instrumentation. |

Taken together, the comparisons suggest that the biggest drivers are year selection, inclusion boundaries, and how pricing and replacement are handled over time. Our approach keeps the total traceable to clear use cases, form factors, and demand signals, which makes it easier to reproduce and to update when end markets shift.

Key Questions Answered in the Report

What is the current value of the density meter market?

The density meter market stands at USD 1.17 billion in 2026 and will rise to USD 1.42 billion by 2031.

Which measurement technology dominates density meter installations?

Coriolis instruments lead with 34.32% of 2025 revenue because they combine mass-flow and density readings in a single device.

Why are handheld density meters gaining popularity?

Field crews favor handheld units for on-the-spot verification, supported by battery power, Bluetooth data export, and lab-grade accuracy

Which end-use sector will grow fastest through 2031?

Water and wastewater treatment will expand at a 5.93% CAGR as desalination and water-reuse projects multiply.

What regions present the strongest growth potential?

The Middle East and Africa will register a 6.08% CAGR owing to desalination megaprojects, oil-and-gas investments, and mining expansions.

How are suppliers adding value beyond basic measurement?

Leading vendors embed AI-driven diagnostics, predictive maintenance, and cloud connectivity to cut downtime and simplify compliance auditing.

Page last updated on: