Magnetic Resonance Angiography Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

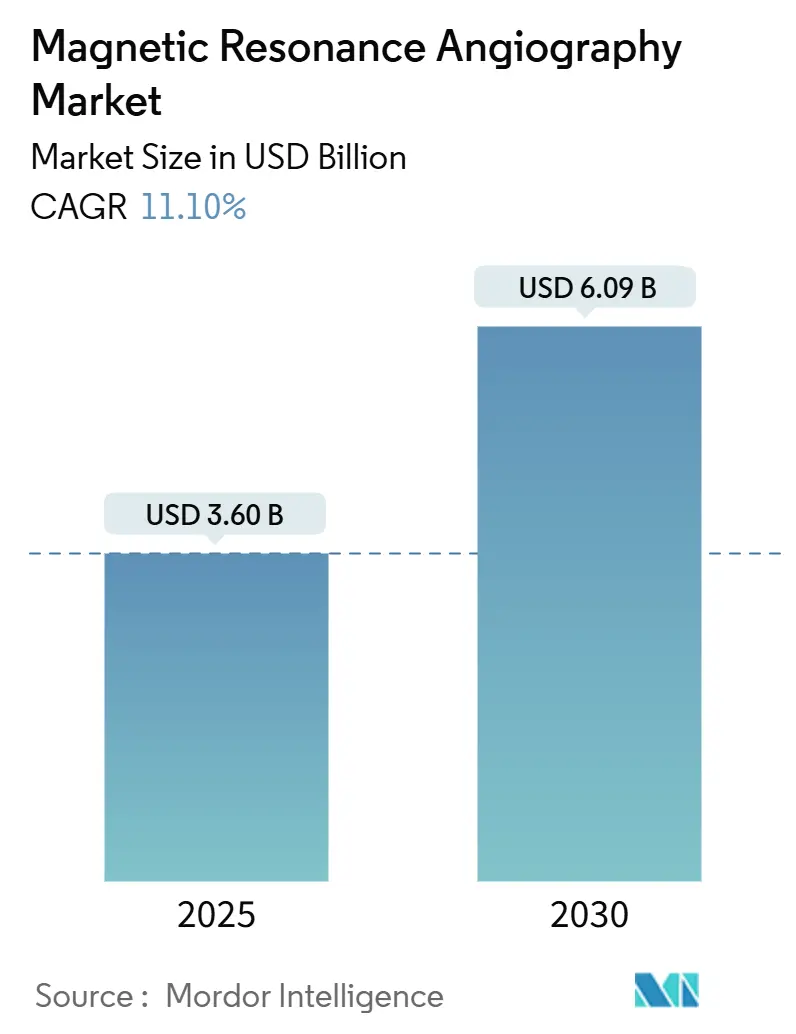

| Market Size (2025) | USD 3.60 Billion |

| Market Size (2030) | USD 6.09 Billion |

| Growth Rate (2025 - 2030) | 11.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Magnetic Resonance Angiography Market Analysis by Mordor Intelligence

The magnetic resonance angiography market size stood at USD 3.60 billion in 2025 and is forecast to reach USD 6.09 billion by 2030, reflecting an 11.10% CAGR over the period. Demand accelerates as aging populations, rising cardiovascular disease prevalence and widening healthcare access converge to make non-invasive vascular imaging an essential diagnostic service. Momentum is reinforced by continuous innovation in high-field magnets, artificial-intelligence-driven workflows and helium-saving hardware that expands clinical capability while lowering lifecycle cost. Providers also favor MRA because it avoids ionizing radiation, a trait that aligns with preventive-care agendas and supports repeated imaging when long-term monitoring is required. Meanwhile, expanded insurance reimbursement for AI-enhanced flow quantification improves economic returns, prompting hospital systems and outpatient networks to prioritize scanner upgrades.

Key Report Takeaways

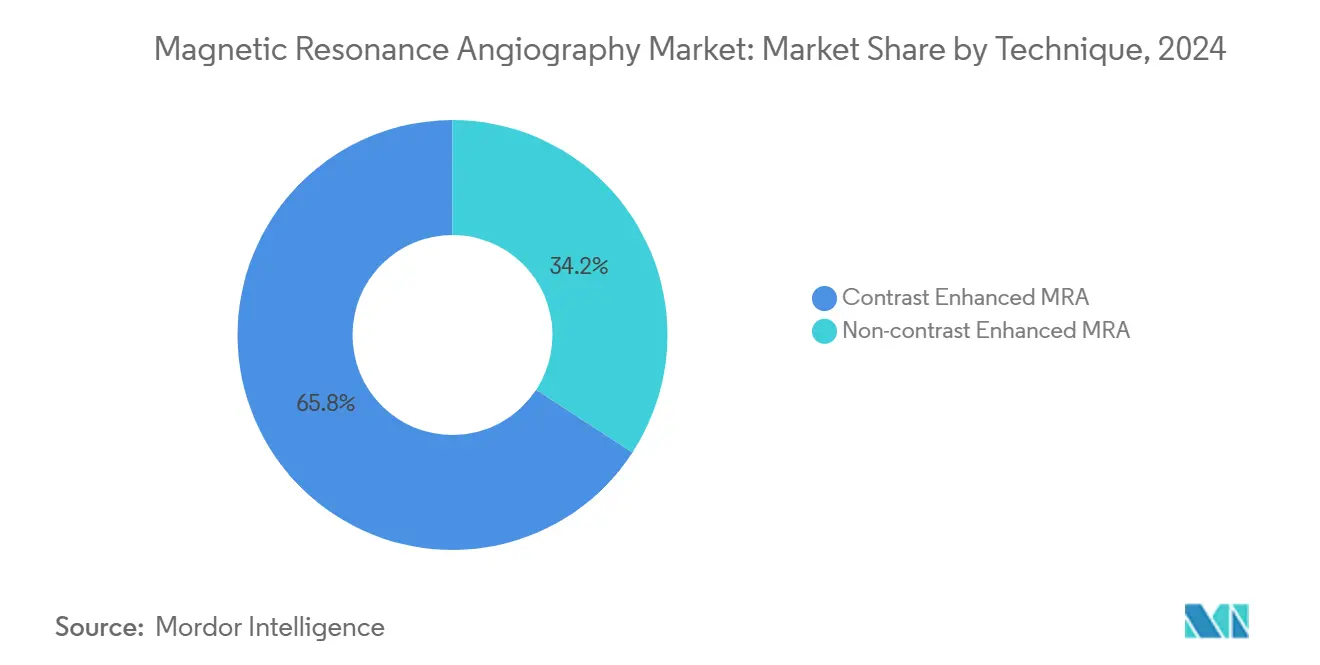

- By technique, contrast-enhanced scans dominated with a 65.8% revenue contribution in 2024, while non-contrast modalities are forecast to grow 8.5% annually through 2030.

- By application, neuro-vascular imaging captured 40.3% of the market size in 2024; cardiac and thoracic vessel exams are expanding at a 9.6% CAGR for the same horizon.

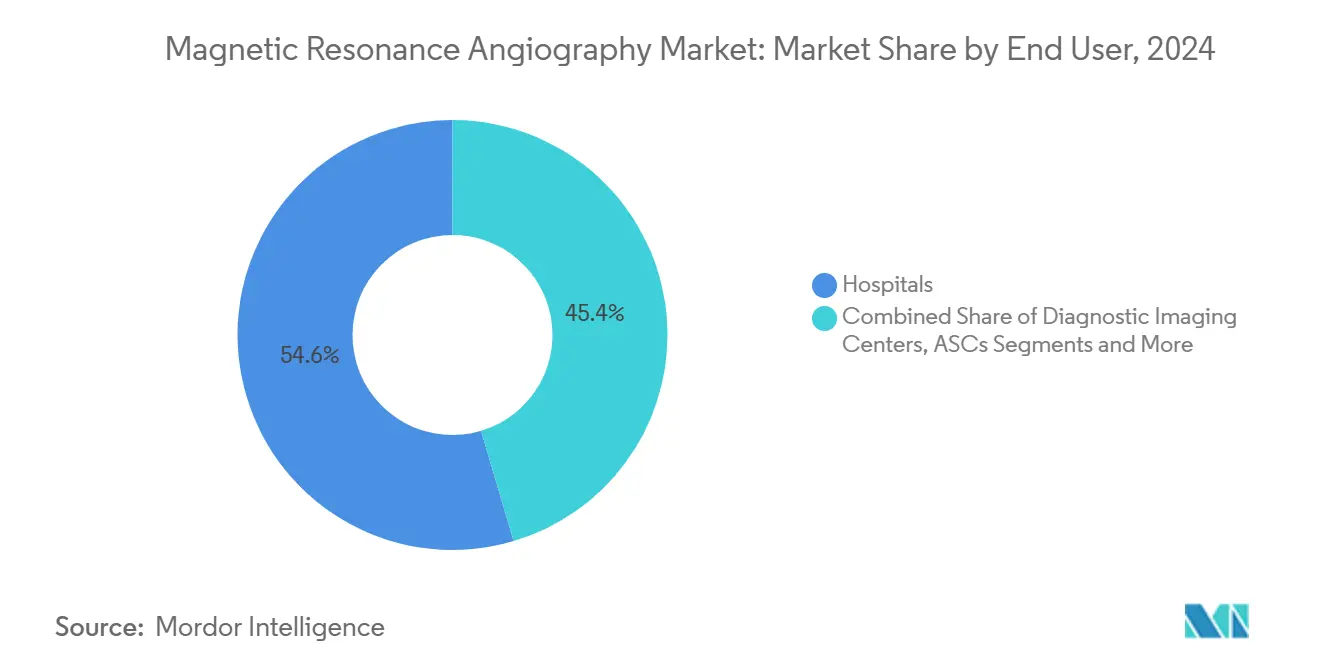

- By end user, hospitals held a 54.6% share during 2024, whereas ambulatory surgical centers recorded the highest CAGR at 8.9% through 2030.

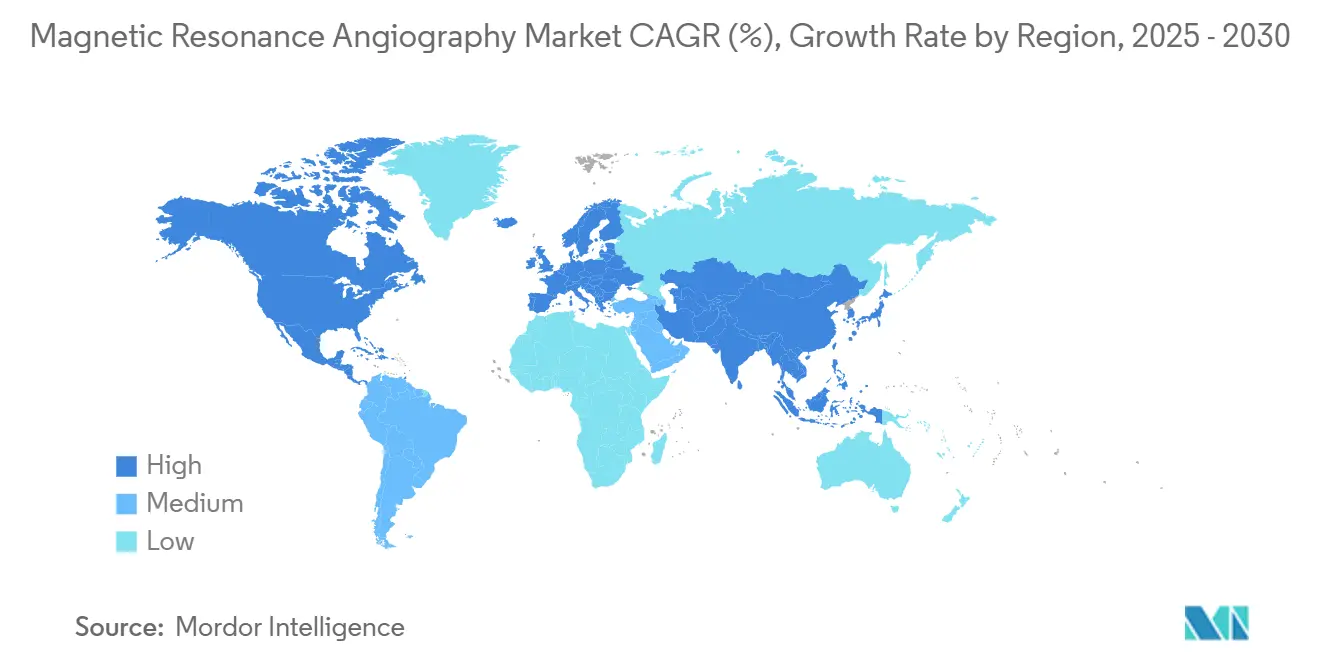

- By geography, North America controlled 34.2% of the market share in 2024; Asia Pacific is projected to post the fastest regional growth at a 7.4% CAGR to 2030.

Global Magnetic Resonance Angiography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of cardiovascular & cerebrovascular disorders | +2.80% | North America & Europe strongest | Long term (≥ 4 years) |

| Technological advances in high-field MRI & vascular coils | +2.10% | Global tier-1 markets | Medium term (2-4 years) |

| Growing geriatric population in developed & emerging regions | +2.50% | Worldwide | Long term (≥ 4 years) |

| Expansion of outpatient imaging centers | +1.90% | APAC, Latin America, MEA | Medium term (2-4 years) |

| AI-assisted flow quantification lifting reimbursement | +1.40% | North America, Europe | Short term (≤ 2 years) |

| Rising adoption of non-contrast 4D flow imaging | +1.10% | Early-adopter markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Cardiovascular & Cerebrovascular Disorders

Worldwide mortality data show heart and brain vessel diseases at the top of the chart, and incidence climbs steeply after age 60. Health systems, therefore, press for earlier, safer vascular screening programs that can intercept pathologies such as intracranial aneurysms and peripheral arterial disease before symptoms arise.[1]Jian’an Wang, “Impact of Aging on Cardiovascular Diseases,” JACC: Asia, jacc.org The market answers this call because scans deliver high-resolution vessel maps without radiation exposure or iodinated contrast. Newer 4D flow sequences even reveal subtle hemodynamic shifts, broadening clinical use beyond classic luminal assessment.

Technological Advances in High-Field MRI & Vascular Coils

Commercial 7 Tesla platforms provide spatial resolution once reserved for research labs, letting radiologists visualize sub-millimeter arterial segments, plaque morphology, and micro-aneurysms.[2]Burkett B.J., “7 T MRI in Cerebrovascular Disorders,” ScienceDirect, sciencedirect.com Vendors complement field strength gains with digital RF coils and compressed-sensing acceleration to cut exam time from 20 minutes to less than 5, a leap that reduces motion artifacts and increases daily throughput.

Growing Geriatric Population in Developed & Emerging Markets

The 65-plus cohort represents the fastest-growing demographic and consumes the most diagnostic imaging per capita. In emerging economies, the same group grows even faster because of improved life expectancy and urban lifestyle shifts. Health ministries dedicate funds to vascular screening and chronic-disease management, creating sustained equipment demand across both tertiary hospitals and smaller regional sites.

AI-Assisted Flow-Quantification Improving Diagnostic Reimbursement

Deep-learning models now auto-detect intracranial aneurysms, grade stenoses and quantify wall shear stress, often outperforming manual reads.[3]Wen Zhongjian, “Artificial Intelligence in Intracranial Aneurysm Images,” frontiersin.org U.S. Medicare has begun to issue specific payment codes recognizing added diagnostic value, raising the return on investment for centers that deploy AI-ready scanners.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & operating cost | -1.80% | Stronger in lower-income regions | Long term (≥ 4 years) |

| Contra-indications with implants & claustrophobia | -0.90% | Aging populations globally | Medium term (2-4 years) |

| Helium & RF component supply-chain volatility | -1.20% | High-field systems worldwide | Medium term (2-4 years) |

| Limited site readiness (shielding, power) | -0.70% | APAC, LatAm, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital & Operating Cost of MRI Systems

A full-featured 3 Tesla scanner often exceeds USD 1 million, and ongoing helium consumption can reach USD 100,000 annually when prices spike. Budget-constrained hospitals delay purchases, stretching replacement cycles beyond 10 years and temporarily slowing unit shipments in developing regions.

Helium & RF Component Supply-Chain Volatility

Helium scarcity caused prices to rise roughly 250% over the past decade as industrial demand surged and the U.S. Federal reserve exited the market. Some hospitals face rationing that forces temporary shutdowns. The situation accelerates vendor investment in zero-boil-off magnets and alternative cooling methods, a trend expected to reshape the market by 2030.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technique: Non-Contrast Acceleration Anchors Growth

Contrast-enhanced exams held 65.8% of 2024 revenue, favored for complex vascular mapping where gadolinium agents amplify signal intensity. Safety concerns drive fast uptake of non-contrast options such as Silent MRA and Quiescent-Interval Single-Shot, which grow at an 8.5% CAGR. Silent sequences reduce acoustic noise to under 75 dB and deliver superior visualization of slow-flow cerebral vessels. These benefits position non-contrast modalities to gain incremental share, although gadolinium-based protocols will remain essential for arterial-venous malformation work-ups.

The competitive landscape rewards vendors offering full portfolios that let clinicians toggle between contrast and non-contrast modes without workflow disruption. Low-field research prototypes at 0.05 T signal potential expansion into rural clinics, though resolution constraints currently limit use to larger vessels.

By Application: Cardiac Imaging Leads the Upside

Neuro-vascular exams retained 40.3% revenue in 2024 on the back of robust stroke and aneurysm screening programs. Cardiac and thoracic vessels now set the growth pace at 9.6% as 4D flow MRI quantifies complex hemodynamics in valvular disease and congenital defects. Clinical guidelines increasingly recommend MRA when CT angiography is contraindicated due to radiation burden or iodinated contrast allergy, widening the referral base.

Peripheral vascular disease imaging also benefits from non-contrast advances that allow safe assessment in diabetic patients with renal impairment. Abdominal and renal artery studies gain ground where MRA’s soft-tissue contrast helps surgeons plan minimally invasive interventions. AI-based risk-stratification tools further broaden implementation by turning raw velocity data into actionable treatment pathways.

By End User: Outpatient Surge Reshapes Modality Mix

Hospitals remained the primary purchaser with 54.6% of 2024 system installations. However, ambulatory surgical centers show an 8.9% CAGR as payers steer appropriate cases to lower-cost outpatient sites. Diagnostic imaging chains add capacity by deploying magnet-light systems that fit into standard office space and run on 50% less power, improving economics for high-volume studies. Academic and research institutions maintain an outsized role in pioneering ultra-high-field and AI protocols that later migrate into routine clinical practice.

Private-equity-backed groups accelerate capital deployment, installing next-generation scanners across multi-state networks to deliver full-body preventive packages priced under USD 1,000. Their scale and marketing budgets raise consumer awareness of self-referred vascular screening, indirectly boosting equipment demand across the broader market.

Geography Analysis

North America booked 34.2% of 2024 revenues thanks to mature reimbursement systems and high modality penetration. Regular guideline updates support consistent usage rates, while FDA clearances for head-only or low-helium magnets keep the product pipeline fresh. Government stimulus aimed at replacing aging rural infrastructure also sustains unit sales.

Asia Pacific, growing 7.4% annually, reflects heavy investment by China and India in tertiary hospitals and tier-2 city outpatient centers. Regional vendors introduce helium-free magnets tailored for lower operating-cost environments, broadening access. Government schemes that subsidize diagnostic imaging in public-sector facilities create further pull. Mature APAC markets such as Japan concentrate on replacing end-of-life 1.5 T units with AI-ready 3 T platforms, keeping long-term demand steady.

Europe maintains moderate growth as hospitals pivot from raw capacity expansion to workflow optimization and sustainability, targeting magnets that cut helium usage by up to 80%. Latin America, Middle East and Africa trail in absolute volume yet show rising order intake once macroeconomic stability aligns with multilateral funding to improve imaging infrastructure. Portable and low-field concepts are being piloted to extend service reach where full shielding rooms are not feasible.

Competitive Landscape

Five vendors—Siemens Healthineers, GE HealthCare, Philips, Canon Medical and Fujifilm—control the bulk of system shipments, making the space moderately concentrated. Differentiation now hinges less on peak gradient strength and more on software ecosystems that automate protocol selection, noise reduction and real-time quality checking. Siemens invested heavily to expand superconducting magnet capacity and accelerate helium-light product roll-outs. GE secured FDA clearance for its head-only 3 T, targeting neuro-vascular research while cutting magnet weight by 30%.

Strategic alliances multiply: Philips’ tie-up with NVIDIA drives foundation AI models that power zero-click scan planning. Canon’s new innovation center leverages academic partnerships to fast-track cardiac and neuro applications. Disruptors such as Hyperfine push portable, battery-operated units that deliver point-of-care vascular checks in emergency settings. Retail entrants underline how consumer demand for preventive imaging is opening direct-to-patient business lines.

Magnetic Resonance Angiography Industry Leaders

Siemens Healthineers

GE HealthCare

Philips Healthcare

Canon Medical Systems

Fujifilm Healthcare (Hitachi)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Philips partners with NVIDIA to embed large-language-model AI across the MR workflow, enabling zero-click protocols, interactive resolution enhancement, and automated finding detection.

- May 2025: Function Health acquired Ezra and launched USD 499 full-body MRI exams across 100 U.S. sites, cutting scan time to 22 minutes and expanding consumer access to preventive MRA screening

- November 2024: GE HealthCare secured FDA clearance for the SIGNA MAGNUS 3.0 T head-only MRI system, which features a specialized gradient design that enhances neuro-vascular imaging performance in MRA studies.

Global Magnetic Resonance Angiography Market Report Scope

| Contrast Enhanced MRA |

| Non-contrast Enhanced MRA |

| Neuro-Vascular Imaging |

| Cardiac & Thoracic Vessels |

| Peripheral Vascular Disease |

| Abdominal & Renal Arteries |

| Others (e.g., Pediatric, Oncology) |

| Hospitals |

| Diagnostic Imaging Centers |

| Ambulatory Surgical Centers |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technique | Contrast Enhanced MRA | |

| Non-contrast Enhanced MRA | ||

| By Application | Neuro-Vascular Imaging | |

| Cardiac & Thoracic Vessels | ||

| Peripheral Vascular Disease | ||

| Abdominal & Renal Arteries | ||

| Others (e.g., Pediatric, Oncology) | ||

| By End User | Hospitals | |

| Diagnostic Imaging Centers | ||

| Ambulatory Surgical Centers | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast size of the Magnetic resonance angiography market by 2030?

It is expected to reach USD 6.09 billion, up from USD 3.60 billion in 2025, translating to an 11.10% CAGR.

Which technique is growing fastest in Magnetic resonance angiography?

Non-contrast-enhanced MRA leads with an 8.5% CAGR as safety and cost advantages appeal to providers.

Why is Asia Pacific considered the high-growth region for Magnetic resonance angiography?

Government investment in imaging infrastructure, rising disposable income and widening disease burden drive a 7.4% CAGR through 2030.

How are helium shortages influencing MRI purchasing decisions?

Volatile helium pricing accelerates adoption of zero-boil-off or helium-free magnets, steering capital toward systems with lower operating costs.

What role does artificial intelligence play in Magnetic resonance angiography today?

AI automates scan planning, enhances image reconstruction and delivers quantitative flow analytics that qualify for higher reimbursement codes and speed diagnostic turnaround.

Page last updated on: