Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

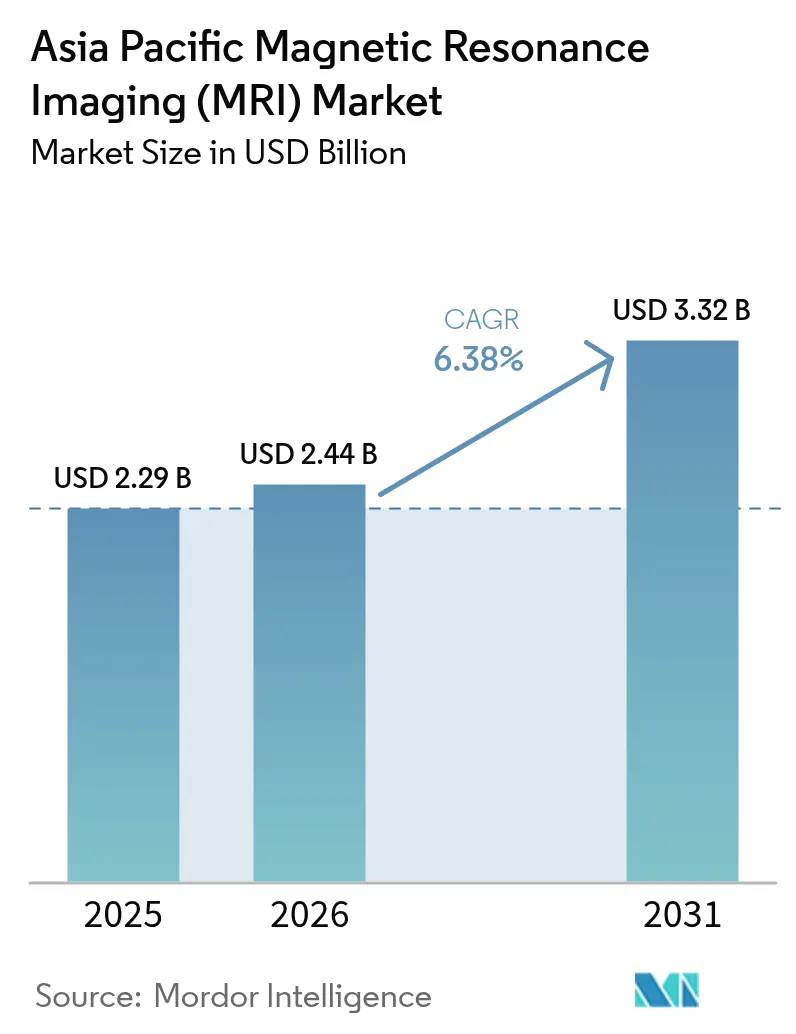

| Base Year Market Size (2025) | USD 2.29 Billion |

| Market Size (2026) | USD 2.44 Billion |

| Market Size (2031) | USD 3.32 Billion |

| Growth Rate (2026 - 2031) | 6.38% CAGR |

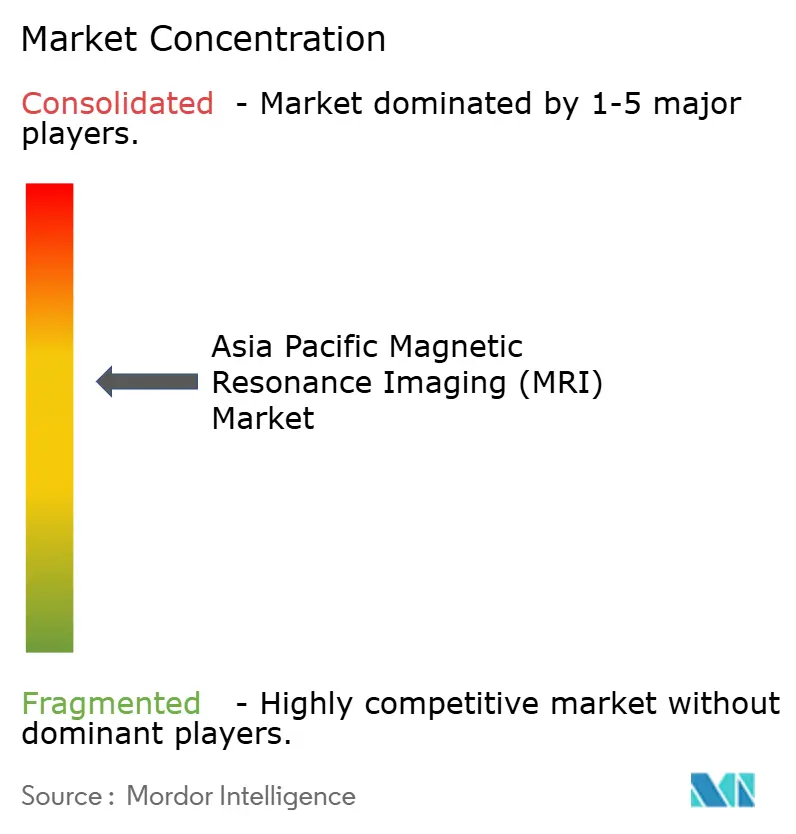

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Magnetic Resonance Imaging (MRI) Market Analysis by Mordor Intelligence

The Asia Pacific magnetic resonance imaging market size is expected to grow from USD 2.29 billion in 2025 to USD 2.44 billion in 2026 and is forecast to reach USD 3.32 billion by 2031 at 6.38% CAGR over 2026-2031. Continuous expansion of universal health-coverage programs, the rising incidence of chronic diseases, and breakthroughs in low-field magnet technology underpin this trajectory. Increasing hospital budgets for diagnostic imaging across China, India, and Southeast Asia align with new reimbursement codes for cardiac and neurological MRI, accelerating system installations. At the same time, AI-enabled reconstruction software is shortening scan times and lifting scanner utilization rates, improving provider economics. Regional manufacturers enjoy policy incentives that promote domestic assembly of helium-light or helium-free systems, further reshaping competitive dynamics. Collectively, these forces sustain a balanced growth environment where advanced 3 T scanners and portable low-field units coexist to serve diverse clinical settings across the Asia Pacific magnetic resonance imaging market.

Key Report Takeaways

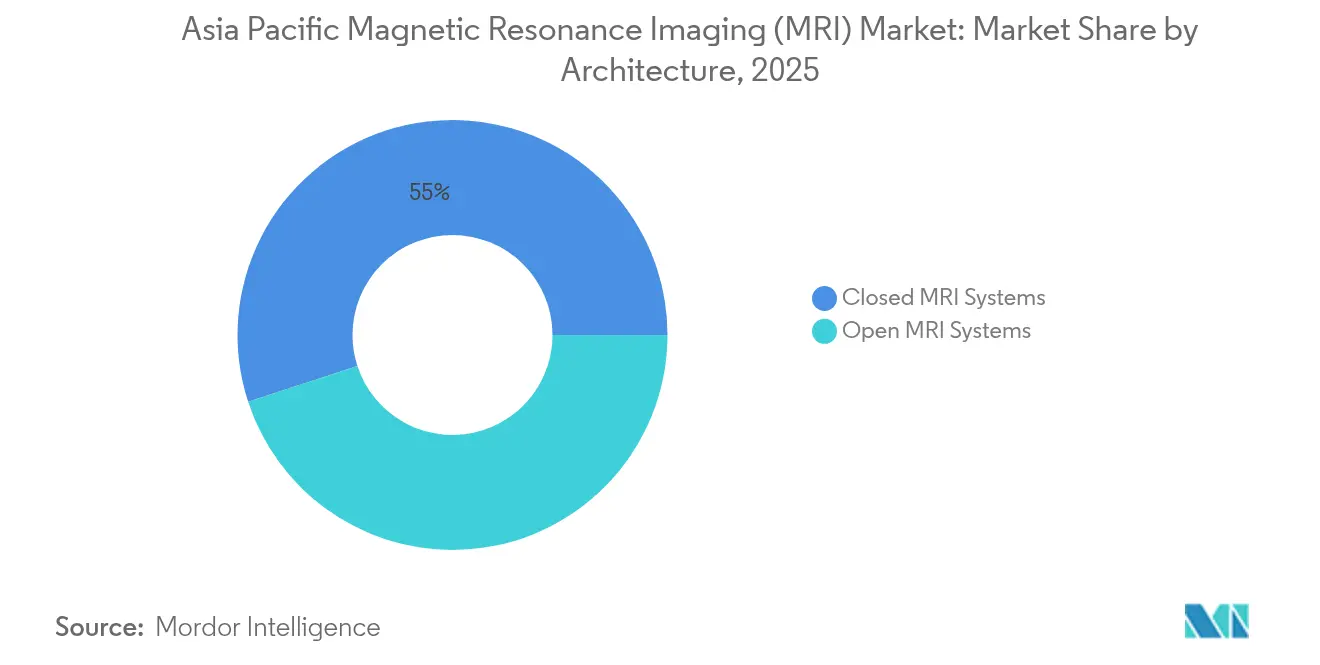

- By architecture, closed systems commanded 55.02% of the Asia Pacific magnetic resonance imaging market size in 2025, whereas open systems are advancing at an 8.27% CAGR.

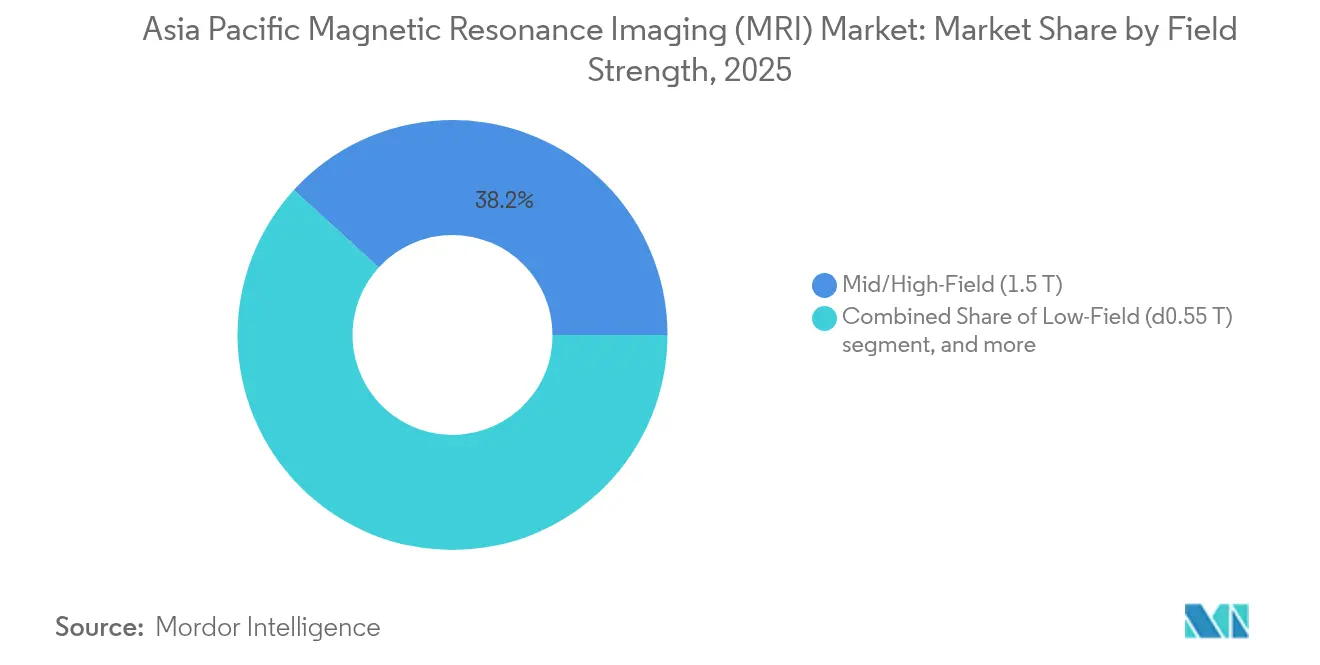

- By field strength, 1.5 T scanners held 38.21% revenue share of the Asia Pacific magnetic resonance imaging market in 2025, and ≤0.55 T platforms exhibit the fastest 7.56% CAGR.

- By application, neurology accounted for 28.32% of the Asia Pacific magnetic resonance imaging market size in 2025, while cardiology is growing at an 8.51% CAGR.

- By country, China led with 28.31% of Asia Pacific magnetic resonance imaging market share in 2025, while India is forecast to expand at a 7.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific Magnetic Resonance Imaging (MRI) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing burden of chronic diseases | +1.2% | China, India, Japan | Long term (≥ 4 years) |

| Universal-health-coverage expansion in Asian nations | +0.9% | India, Southeast Asia | Medium term (2-4 years) |

| Introduction of hybrid MRI systems in emerging markets | +0.7% | China, India, South Korea, Australia | Medium term (2-4 years) |

| Rapid growth in aging population & imaging demand | +1.1% | Japan, South Korea, Singapore, urban China | Long term (≥ 4 years) |

| AI-enabled accelerated image reconstruction cuts scan time | +0.8% | Japan, South Korea | Short term (≤ 2 years) |

| Domestic magnet / cryogen manufacturing incentives | +0.6% | China, India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Burden of Chronic Diseases

Asia’s rising prevalence of cardiovascular, oncologic, and neuro-degenerative disorders directly lifts annual MRI exam volumes. Diabetes-related neuropathy and stroke screening require high-resolution brain and vascular imaging more frequently than five years ago, driving procurement of both 1.5 T workhorse scanners and premium 3 T platforms. Large tertiary hospitals in China now embed MRI into standardized care pathways for oncology staging, boosting average scans per installed unit to more than 5,500 per year, compared with 4,200 in 2021. As chronic disease management shifts toward early intervention, health ministries continue to subsidize advanced imaging capacity, sustaining baseline growth for the Asia Pacific magnetic resonance imaging market[1]Ministry of Health China, “National Imaging Capacity Report 2025,” moh.gov.cn.

Universal-Health-Coverage Expansion in Asian Nations

National insurance schemes such as India’s Ayushman Bharat have increased covered outpatient imaging, expanding the addressable patient pool by up to 63 million lives since 2023. The immediate effect is a rise in entry-level and refurbished MRI purchases at district hospitals that previously relied on CT or patient referrals to metropolitan centers. Portable ≤0.55 T systems attract administrators because they operate without shielded rooms, reducing installation cost by nearly 45% compared with conventional 1.5 T suites. Taken together, expanded coverage and cost-optimized hardware enlarge the Asia Pacific magnetic resonance imaging market[2]National Health Authority India, “Ayushman Bharat Mission Dashboard 2025,” nha.gov.in.

Introduction of Hybrid MRI Systems in Emerging Markets

Combined PET/MRI and SPECT/MRI scanners offer clinicians metabolic, functional, and anatomic information in a single session, improving diagnostic accuracy for oncology and cardiology cases. Flagship academic centers in Seoul, Shanghai, and Sydney adopted hybrid models in 2024, documenting a 22% drop in diagnostic ambiguity compared with separate sequential exams. These early results justify the premium pricing of hybrid platforms, attracting tier 2 hospitals that handle complex oncology workloads. Manufacturers such as United Imaging Healthcare capitalize by bundling hybrid technology with AI-based workflow tools, reinforcing revenue diversity inside the Asia Pacific magnetic resonance imaging market[3]Nature Medicine Editorial Board, “PET/MRI Accuracy in Cardiovascular Imaging,” nature.com.

AI-Enabled Accelerated Image Reconstruction Cuts Scan Time

Deep learning reconstruction software now integrates seamlessly with scanners older than 10 years, cutting acquisition time by as much as 59% without hardware replacement. Japan’s regulatory pathway for third-party AI modules, guided by the Pharmaceuticals and Medical Devices Agency, fast-tracks clinical implementation and sets a regional precedent. Hospitals report 37% higher daily throughput after activating AI recon, generating additional billable exams that shorten equipment payback periods. These efficiencies bolster demand for software-retrofit subscriptions alongside new-system purchases, deepening vendor-provider partnerships throughout the Asia Pacific magnetic resonance imaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High System Acquisition & Maintenance Costs | -1.8% | Emerging Asia Pacific markets | Long term (≥ 4 years) |

| Helium Supply-Chain Vulnerability | -1.2% | Global, acute in high-field installations | Medium term (2-4 years) |

| Shortage of Sub-Specialty Radiologists | -0.9% | India, Indonesia, Philippines, rural China | Medium term (2-4 years) |

| Hospital CAPEX Diversion to CT & PET During Economic Slowdowns | -0.7% | Developing Asia Pacific economies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High System Acquisition & Maintenance Costs

New 1.5 T installations carry an average ten-year total cost of ownership exceeding USD 2.8 million once facility retrofit, preventive maintenance, and software upgrades are included. Public hospitals in Indonesia and the Philippines allocate less than 6% of operating budgets to capital equipment, highlighting affordability barriers. Providers increasingly turn to subscription-based “imaging-as-a-service” models, shifting upfront investment to multiyear operating leases indexed to scan volume, a strategy pioneered by Philips and regional financing partners. Such models mitigate, but do not eliminate, cost restraints on the Asia Pacific magnetic resonance imaging market.

Helium Supply-Chain Vulnerability

Helium price spikes of 35% in 2024 raised annual running costs for superconducting magnets, prompting providers to retrofit zero-boil-off technology or evaluate permanent-magnet alternatives. The University of Hong Kong demonstrated a 0.05 T whole-body prototype that operates entirely without cryogen, validating clinical utility when combined with AI-based denoising algorithms. Vendors now market “helium-light” 1.5 T systems holding under 70 liters, down from 1,500 liters a decade earlier, easing logistics but not fully resolving supply risk. Persistent helium uncertainty tempers purchasing in smaller economies, restraining the Asia Pacific magnetic resonance imaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Architecture: Patient-Centric Design Drives Open System Adoption

Open scanners delivered 8.27% CAGR between 2026 and 2031, outpacing the overall Asia Pacific magnetic resonance imaging market although closed configurations retained 55.02% share in 2025. Hospitals value the 270-degree patient access of open bores for interventional procedures and for cohorts prone to claustrophobia. Portable iterations weighing under 3 tons are now dispatched to rural clinics in Sichuan Province under provincial tele-imaging pilots, confirming that form factor flexibility converts directly into expanded patient reach. As reconstruction software compensates for lower field strength, diagnostic confidence in musculoskeletal and pediatric cases matches closed-bore benchmarks. Growth remains strongest in Southeast Asia, where outpatient imaging centers differentiate with comfort-oriented marketing.

Open architecture suppliers are layering cloud-based protocol libraries and automated positioning aids, reducing technologist learning curves. Meanwhile, closed systems continue to dominate research and high-end neurological applications because of superior gradient performance and coil ecosystem depth. Vendors have started offering hybrid service contracts allowing providers to mix open and closed units under a single uptime guarantee, a model gaining traction in Japan’s private hospital groups. Consequently, both sub-segments reinforce the Asia Pacific magnetic resonance imaging market, with open systems supplying incremental volume while closed platforms preserve high-resolution leadership.

By Field Strength: Low-Field Innovation Disrupts Traditional Hierarchies

Mid-field 1.5 T units generated 38.21% of the Asia Pacific magnetic resonance imaging market share in 2025, confirming their role as universal workhorses. Yet ≤0.55 T systems recorded the fastest 7.56% CAGR as AI post-processing neutralizes inherent signal-to-noise limitations. DeepSee Technology’s shield-free bedside model, cleared by China’s NMPA in 2025, illustrates how low-field designs avoid expensive RF cages and deliver meaningful neuro imaging inside intensive-care units. Cost-conscious public hospitals in India project 32% lower five-year operating expenses when adopting low-field scanners instead of refurbishing legacy 1.5 T rooms.

High-field 3 T platforms retain momentum for cardiac mapping, whole-body diffusion, and functional MRI studies, securing budget allocations in academic institutions. At the far end, 7 T research magnets remain rare, with fewer than 15 installations across Asia Pacific, constrained by purchase price and safety protocol complexity. Overall, field-strength diversity enables providers to align equipment with case-mix realities, ensuring that each echelon contributes to the Asia Pacific magnetic resonance imaging market size growth trajectory.

By Application: Cardiology Acceleration Driven by AI Integration

Neurology retained 28.32% share in 2025, reflecting MRI’s role in stroke, glioma, and dementia management pathways. Cardiology, however, posts the quickest 8.51% CAGR as new non-contrast T1-mapping and strain quantification sequences meet rising cardiovascular disease incidence. AI vendors now bundle automated left-ventricular function reporting with scanner consoles, cutting reading time by 40% and allowing smaller centers to launch cardiac services without dedicated cardiologist staffing. Evolving reimbursement in South Korea and Australia grants separate billing codes for stress cardiac MRI, improving return on investment. Musculoskeletal and oncology segments continue steady expansion, collectively absorbing additional scanner slots during off-peak neurology scheduling. Application diversification thus sustains broad-based demand across the Asia Pacific magnetic resonance imaging market.

Geography Analysis

China accounted for 28.31% of the Asia Pacific magnetic resonance imaging market in 2025, underpinned by multi-billion-dollar provincial subsidy programs that reimburse up to 50% of scanner purchase price for county hospitals. Domestic firms benefited from preferential procurement scoring, with United Imaging Healthcare surpassing 5,000 cumulative MRI installations nationwide by mid-2025. AI-ready picture archiving platforms and a federal imaging cloud facilitate rapid algorithm deployment, reinforcing clinical adoption curves. Province-level data analytics also encourage outcome-based purchasing that favors high-throughput designs.

India is the fastest-growing national cohort, registering a 7.41% CAGR through 2031. The Ayushman Bharat scheme reimburses up to 60% of outpatient MRI cost, and public-private partnerships fast-track scanner placement in tier-2 cities. Strong medical tourism demand for orthopedic and cardiac interventions drives private chain expansion, while indigenous assembly of 0.4 T and 1.5 T systems reduces import duties by 15%. Regulatory simplification under the Medical Devices (Amendment) Rules 2024 shortened license timelines to under six months, catalyzing vendor pipeline momentum.

Japan, South Korea, and Australia constitute mature sub-markets where replacement demand prevails. Japan’s scanner density exceeds 55 units per million population, the highest globally, leading vendors to focus on software upgrades and hybrid PET/MRI adoption. South Korea shows similar saturation but pioneers operational models such as per-scan AI fees bundled into national insurance tariffs. Australia’s public hospitals stress cost-effectiveness; hence, they negotiate multiyear managed-equipment service contracts that bundle 3 T hardware, coils, and analytics dashboards.

The Rest of Asia Pacific cluster—Indonesia, Malaysia, Thailand, Vietnam, and the Philippines—adds incremental volume through greenfield private hospitals targeting middle-class segments. Portable ≤0.55 T units find early success in island geographies where road logistics complicate patient transfer. Cross-border teleradiology hubs in Singapore support these markets by interpreting scans remotely, demonstrating the region-wide interplay that sustains the Asia Pacific magnetic resonance imaging market.

Competitive Landscape

The Asia Pacific magnetic resonance imaging market features moderate concentration: the top five vendors together controlled roughly 62% revenue in 2024. GE Healthcare, Siemens Healthineers, and Philips Healthcare leverage decades-old installed bases and multivendor service teams, yet their combined share is trending downward as regional makers scale. United Imaging Healthcare recorded nearly 30% year-on-year export growth in 2025, shipping scanners to over 14,000 hospitals worldwide, while Neusoft Medical Systems broadened its ≤0.5 T portfolio for primary-care settings.

Technological race centers on helium-light magnets, AI reconstruction suites, and workflow orchestration tools. Siemens’ Deep Resolve and GE’s AIR Recon DL compete head-to-head with start-ups such as AirMedical that offer vendor-agnostic software compatible with older fleets, capturing high-margin subscription revenue. At the hardware frontier, DeepSee Technology’s shield-free bedside unit disrupts conventional siting economics, prompting incumbents to accelerate their own low-field roadmaps. Simultaneously, hybrid PET/MRI vendors are expanding reference sites to prove cost–benefit; early adopters report reduced patient transfers and accelerated oncology treatment planning.

Partnerships between manufacturers and hospital chains now emphasize shared-risk models, where leasing rates or revenue shares fluctuate with scanner utilization. This strategy mitigates cap-ex hurdles for providers while locking vendors into multiyear revenue streams. Local component sourcing mandates in China and India further compel multinational companies to invest in assembly lines, aligning with government industrial policy but eroding cost advantages linked to global supply chains. Collectively, these shifts guarantee lively strategic maneuvering within the Asia Pacific magnetic resonance imaging market over the forecast horizon.

Asia Pacific Magnetic Resonance Imaging (MRI) Industry Leaders

Siemens Healthcare

Canon Medical Systems Corporation

Koninklijke Philips NV

GE Healthcare

Fujifilm Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: DeepSee Technology obtained China NMPA Class III clearance for the wMR-510, the first no-shielding mobile head MRI that operates bedside in emergency and ICU settings

- June 2024: The University of Hong Kong published whole-body 0.05 T MRI results enhanced by deep learning, enabling shield-less imaging suites

- April 2024: AirMedical secured European and Japanese supply contracts for its SwiftMR™ AI engine, demonstrating across-vendor scan-time cuts

Asia Pacific Magnetic Resonance Imaging (MRI) Market Report Scope

As per the scope of the report, magnetic resonance imaging is a medical imaging technique that is used in radiology to produce pictures of the anatomy and the physiological processes of the body in both health and disease. These pictures are further used to diagnose and detect the presence of abnormalities in the body. The Asia-Pacific Magnetic Resonance Imaging (MRI) Market is Segmented by Architecture (Closed MRI Systems and Open MRI Systems), Field Strength (Low Field MRI Systems, High Field MRI Systems, and Very High Field MRI Systems and Ultra-high MRI Systems), Application (Oncology, Neurology, Cardiology, Gastroenterology, Musculoskeletal, and Other Applications), and Geography (China, Japan, India, Australia, South Korea, and Rest of Asia-Pacific). The report offers the value (in USD million) for the above segments.

By Architecture

| Closed MRI Systems |

| Open MRI Systems |

By Field Strength

| Low-Field (≤0.55 T) |

| Mid/High-Field (1.5 T) |

| Very-High-Field (3 T) |

| Ultra-High-Field (7 T +) |

By Application

| Neurology |

| Oncology |

| Musculoskeletal |

| Cardiology |

| Gastroenterology |

| Other Applications |

Country

| China |

| Japan |

| India |

| South Korea |

| Australia |

| Rest of Asia-Pacific |

| By Architecture | Closed MRI Systems |

| Open MRI Systems | |

| By Field Strength | Low-Field (≤0.55 T) |

| Mid/High-Field (1.5 T) | |

| Very-High-Field (3 T) | |

| Ultra-High-Field (7 T +) | |

| By Application | Neurology |

| Oncology | |

| Musculoskeletal | |

| Cardiology | |

| Gastroenterology | |

| Other Applications | |

| Country | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current size of the Asia Pacific magnetic resonance imaging market?

The Asia Pacific magnetic resonance imaging market size reached USD 2.44 billion in 2026 and is forecast to hit USD 3.32 billion by 2031.

Which country leads scanner installations across Asia Pacific?

China holds 28.31% revenue share owing to large-scale government procurement incentives and robust domestic manufacturing.

Which segment is expanding fastest within the regional MRI space?

The cardiology segment shows the highest 8.51% CAGR, supported by AI-enhanced cardiac MRI protocols.

How are low-field scanners impacting equipment budgets?

²0.55 T systems reduce siting and running costs by roughly 45%, helping resource-constrained hospitals adopt MRI.

What technological shift is most influencing purchase decisions through 2031?

AI-enabled image reconstruction that shortens scan times by up to 59% is becoming a pivotal factor in vendor selection.

How vulnerable is the market to helium supply disruptions?

Helium dependence remains a restraint, but helium-light and helium-free designs are mitigating long-term risk across new installs.

Page last updated on: