Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

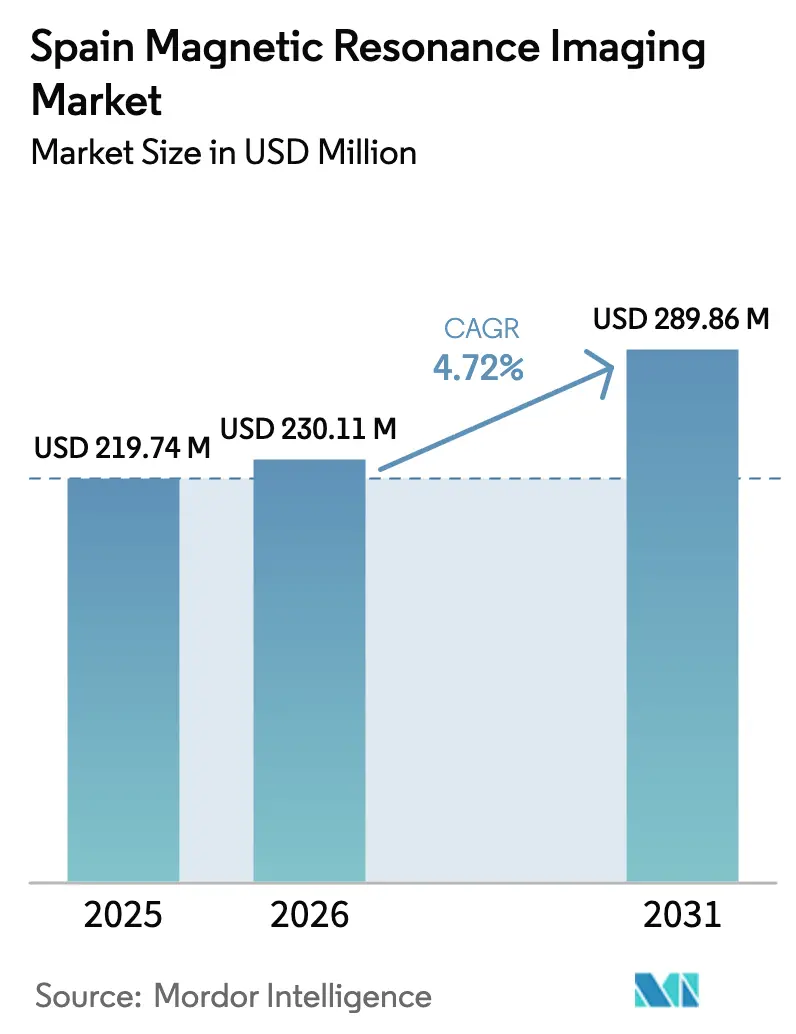

| Base Year Market Size (2025) | USD 219.74 Million |

| Market Size (2026) | USD 230.11 Million |

| Market Size (2031) | USD 289.86 Million |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Magnetic Resonance Imaging Market Analysis by Mordor Intelligence

The Spain magnetic resonance imaging market size in 2026 is estimated at USD 230.11 million, growing from 2025 value of USD 219.74 million with 2031 projections showing USD 289.86 million, growing at 4.72% CAGR over 2026-2031. The steady trajectory reflects parallel public- and private-sector modernization programs, generous EU-backed capital grants, and a maturing digital-health ecosystem. Government spending under the INVEAT fund has accelerated equipment turnover, while the PERTE Salud de Vanguardia initiative channels research subsidies toward AI-enabled imaging workflows. On the demand side, population aging and a chronic disease burden dominated by neurodegeneration and cardiovascular disorders continue to swell referral volumes. Private operators seize the opportunity created by 67-day public waiting lists, pushing utilization toward 90% and spurring differentiation on patient experience, helium-free magnets, and rapid cardiac protocols. Vendors able to pair high-field performance with sustainability credentials have carved out early advantages in the Spain Magnetic Resonance Imaging market, especially across high-density regions such as Madrid and Catalonia where scanner penetration already exceeds the national average.

Key Report Takeaways

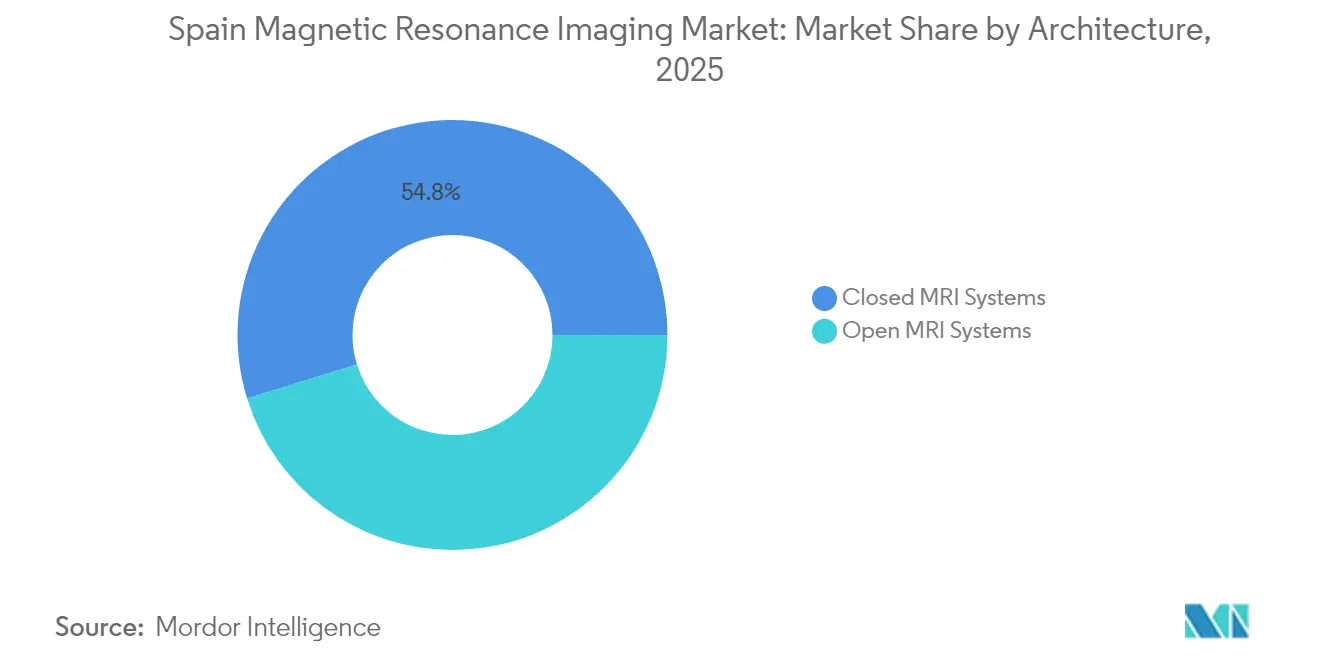

- By architecture, closed systems captured 54.78% Spain Magnetic Resonance Imaging market share in 2025, while open systems are on track to post the fastest 6.41% CAGR through 2031.

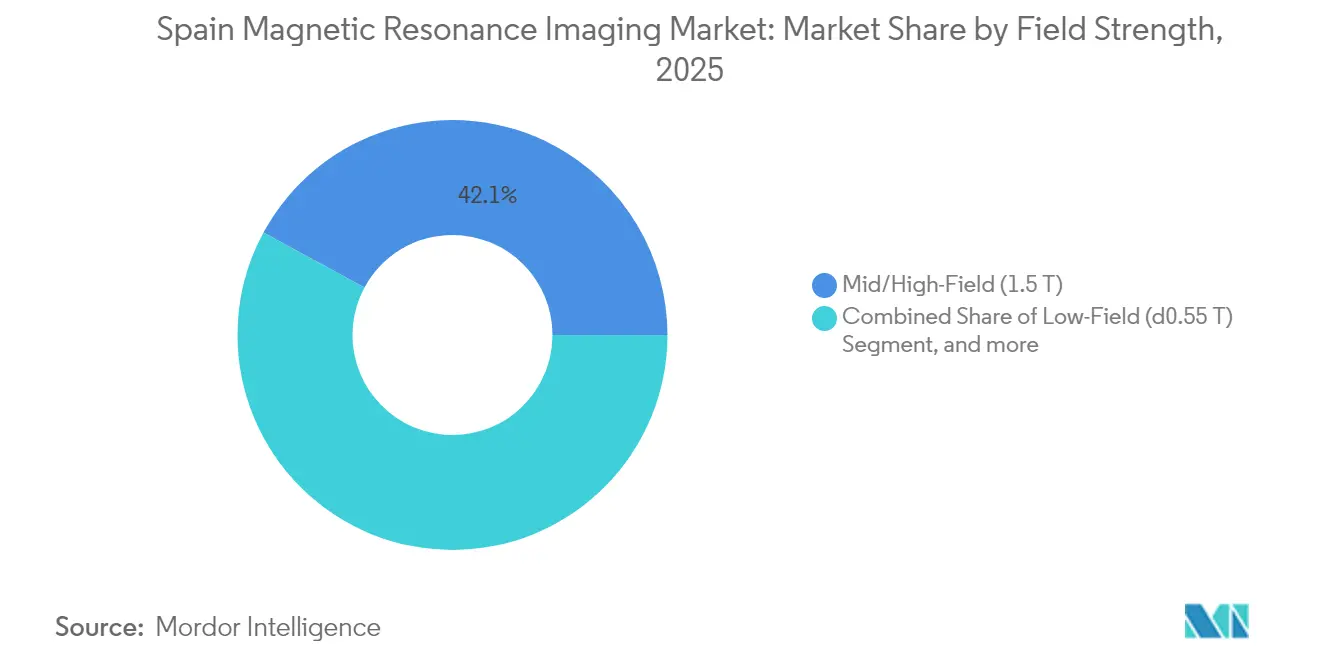

- By field strength, 1.5 Tesla platforms held 42.10% of the Spain Magnetic Resonance Imaging market size in 2025, yet sub-0.55 Tesla units will grow at 12.18% CAGR on the back of helium-free technology mandates.

- By application, neurology accounted for 32.40% of the Spain Magnetic Resonance Imaging market size in 2025, whereas cardiology will advance at a 5.18% CAGR to 2031 as preventive imaging protocols scale nationally.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Magnetic Resonance Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of chronic & degenerative diseases | +1.8% | National, aging regions such as Castilla y León and Asturias | Long term (≥ 4 years) |

| Government INVEAT program renewing obsolete scanners | +1.2% | National, underserved autonomous communities | Medium term (2-4 years) |

| AI-enhanced high-field scanners improve throughput & image quality | +0.9% | Madrid, Barcelona, Valencia | Short term (≤ 2 years) |

| Expansion of private imaging centers amid long public waiting lists | +1.1% | Madrid, Andalusia, Catalonia | Medium term (2-4 years) |

| EU-funded portable/low-field MRI prototypes (NEXTMRI) | +0.6% | Pilot sites in Valencia, Madrid, Navarra | Medium term (2-4 years) |

| Sustainability push for helium-free 0.55 T systems | +0.7% | Nationwide hospitals pursuing net-zero targets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic & Degenerative Diseases

Cancer incidence reached 287,000 new cases in 2024 and sits alongside cardiovascular mortality of 28.3%, creating a dual-pathway surge in MRI referrals that solidifies the Spain Magnetic Resonance Imaging market as an essential diagnostic backbone[1]Sociedad Española de Cardiología, “Estadísticas de mortalidad cardiovascular,” secardiologia.es. Compounded multimorbidity means many cancer survivors now require routine cardiac follow-up, further lifting scan volumes. Dementia prevalence is projected to triple by 2050 as the over-65 cohort grows from 20.1% to 31.4%, magnifying demand for diffusion tensor and functional MRI sequences that depend on high-field stability. Spain’s public-health expenditure of EUR 108.3 billion (USD 115.2 billion) in 2022 underscores fiscal headroom to absorb the added volume[2]OECD, “Health at a Glance: Europe 2024,” oecd.org. The combined disease trajectory therefore contributes a 1.8 percentage-point uplift to forecast growth, ensuring the Spain Magnetic Resonance Imaging market retains long-term momentum.

Government INVEAT Program Renewing Obsolete Scanners

INVEAT allocated EUR 796 million (USD 846.7 million) and procured 144 scanners during 2024, cutting the average public-hospital magnet age from 18 to 10 years[3]Ministerio de Sanidad, “Acuerdos Marco AMAT-I,” mscbs.gob.es. New platforms embed AI engines that elevate daily throughput by up to 30%, alleviating radiologist shortages without proportionate head-count growth. Follow-on AMAT-I framework funds worth EUR 86 million (USD 91.5 million) cement a multiyear replacement cadence that penetrates rural regions where equipment had surpassed end-of-life thresholds. The program adds 1.2 percentage points to the Spain Magnetic Resonance Imaging market CAGR through predictable tender volumes and standardized technical specifications that shorten procurement cycles.

AI-Enhanced High-Field Scanners Improve Throughput & Image Quality

Spain counts only 4.2 radiologists per 100,000 inhabitants versus the EU average of 6.1, so workflow automation is a strategic requirement, not a luxury. Leading networks such as Quirónsalud Madrid report 50% shorter brain protocols after deploying AI-driven sequence optimization. National research hubs extend domestic capability: VHIO’s DISCERN reaches 78% accuracy in brain-tumor classification, and Quibim’s prostate solution surpasses 90% sensitivity. Energy optimization delivers a further 32% reduction in scanner power draw, directly addressing hospital decarbonization targets. The combined operational gains deliver a 0.9 percentage-point fillip to the Spain Magnetic Resonance Imaging market growth outlook over the short term.

Expansion of Private Imaging Centers Amid Long Public Waiting Lists

Public waiting times average 67 days, yet private clinics secure appointment windows within 48 hours, attracting insured and self-pay cohorts willing to absorb premium tariffs. Capacity utilization at private hubs rises to 90%, compared with 65% in public hospitals, enhancing return on capital for chains that cluster high-field magnets around Madrid and Barcelona. Murcia’s EUR 20 million public-private framework with Siemens Healthineers exemplifies a model that outsources volume peaks while modernizing the regional fleet. Private players now own 52-56% of installed units but carry only 39% of national throughput, pointing to latent upside once referral funnels widen. The structural shift delivers a 1.1 percentage-point boost to the Spain Magnetic Resonance Imaging market CAGR through 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High purchase & lifecycle costs | -0.8% | National, acute in smaller autonomous communities | Long term (≥ 4 years) |

| Stringent EU-MDR / AEMPS approvals & post-market vigilance | -0.5% | Nationwide within EU regulatory framework | Medium term (2-4 years) |

| Radiologist workforce shortages slow scan throughput | -0.6% | National, pronounced in rural regions | Short term (≤ 2 years) |

| Over-diagnosis backlash from incidental findings | -0.4% | National, academic medical centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Purchase & Lifecycle Costs

A helium-cooled 1.5 Tesla unit costs EUR 2-4 million (USD 2.1-4.3 million) and demands annual service fees equal to 10% of acquisition price. Helium spot prices have risen 300% since 2020, inflating operating budgets and prompting interest in magnet-free refrigeration. Budget disparities compound the strain, with Andalusia spending EUR 1,200 per capita on health versus EUR 1,800 in the Basque Country, delaying scanner refresh cycles outside Spain’s wealthiest regions. Rural hospitals serving fewer than 50,000 residents often post utilization below 50%, rendering traditional ownership models uneconomic and stalling deployment, subtracting 0.8 percentage points from the Spain Magnetic Resonance Imaging market CAGR.

Stringent EU-MDR / AEMPS Approvals & Post-Market Vigilance

EU-MDR tightens evidence thresholds, raising per-product compliance outlays by as much as EUR 500,000 (USD 532,000) for algorithm-driven upgrades. Hospitals report tender timelines elongated by four months as dossiers must include post-market surveillance and cybersecurity plans. Smaller vendors struggle to absorb the overhead, nudging the competitive field toward multinationals and delaying new-feature rollouts, shaving 0.5 percentage points off Spain Magnetic Resonance Imaging market growth through 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Architecture: Closed Systems Dominate, Open Systems Accelerate

Closed scanners captured a commanding 54.78% share of the Spain Magnetic Resonance Imaging market in 2025, driven by superior signal-to-noise performance that underpins complex neuro and cardiac applications. Public hospitals rely on enclosed bores to meet high throughput targets, and these sites represent 78% of closed-system placements nationwide. The Spain Magnetic Resonance Imaging market size tied to closed scanners equaled USD 120.32 million in 2025, underscoring their revenue weight. Open platforms, however, are advancing at a 6.41% CAGR as private centers target claustrophobic and pediatric cohorts, banking on wider bores and interventional flexibility to enhance patient satisfaction. GE’s wide-bore SIGNA™ Creator and similar systems blur the comfort-performance trade-off, positioning the open category to win incremental volume. Manufacturers couple open geometries with AI-based motion correction to narrow historical image-quality gaps, a shift likely to recalibrate procurement criteria within private-hospital chains.

Ownership economics also diverge. Open magnets priced below EUR 1.5 million (USD 1.6 million) entice outpatient franchises whose cash-purchase cycles differ from public tenders. Still, EU-MDR evidence requirements favor closed systems with deep clinical datasets, tempering open-system traction in teaching hospitals. Over the forecast horizon the Spain Magnetic Resonance Imaging market is expected to show closed-system revenue climbing steadily at 4.05% CAGR, while open-system revenue will outpace at 6.41%, gradually lifting its contribution from 45.22% in 2025 to nearly 47.95% by 2031.

By Field Strength: Mid-Field Stability, Low-Field Disruption

Mid/high-field 1.5 Tesla units controlled 42.10% of the Spain Magnetic Resonance Imaging market in 2025, equating to USD 92.51 million in revenue. Hospitals appreciate their balance of diagnostic versatility and manageable siting costs, especially as helium capture systems improve sustainability metrics. The Spain Magnetic Resonance Imaging market share for very-high-field 3.0 Tesla remains stable near 25%, anchored in oncology centers that run diffusion, spectroscopy, and perfusion regimes. Conversely, low-field magnets under 0.55 Tesla headline growth at 12.18% CAGR thanks to helium-free cryostats and reduced floor-load requirements that allow installation in older buildings without structural reinforcement. GE Healthcare’s Freelium and Philips BlueSeal magnets are early beneficiaries, and the segment’s Spain Magnetic Resonance Imaging market size is projected to double from USD 23.25 million in 2025 to USD 46.3 million by 2031.

Clinicians once doubted low-field clarity, yet newer AI-based reconstruction delivers acceptable resolution for musculoskeletal and neuro follow-up scans while consuming 60% less power, a decisive advantage amid Spain’s rising electricity tariffs. Portable low-field prototypes developed by PhysioMRI and La Fe Hospital promise outreach models for rural provinces, further broadening the consumption base. High-field dominance will continue, but the disruptive economics of sub-0.55 Tesla devices could reset replacement strategies among smaller hospitals.

By Application: Neurology Leads, Cardiology Gains Pace

Neurology held 32.40% of Spain Magnetic Resonance Imaging market revenue in 2025, equal to USD 71.19 million and rooted in national stroke networks that prescribe MRI for acute ischemia triage. The segment’s entrenched workflows will keep annual growth close to the 3.92% band, sustained by the triple-digit rise anticipated in dementia cases. Cardiology, however, is forecast to grow the fastest at 5.18% CAGR, lifting its Spain Magnetic Resonance Imaging market size from USD 46.8 million in 2025 to USD 63.2 million in 2031 as guideline revisions recommend stress-perfusion MRI for asymptomatic high-risk adults. Innovations such as free-breathing cine sequences shorten exam times to 15 minutes, improving lab throughput and patient comfort.

Musculoskeletal imaging retains a resilient share driven by sports-injury referrals and an orthopedic surgery backlog exacerbated by pandemic postponements. Oncology commands steady momentum under national cancer-control plans that mandate MRI in treatment-response pathways. Emerging gastroenterology applications, notably MR enterography, post mid-single-digit growth as radiologists seek radiation-free alternatives to CT in inflammatory bowel disease surveillance. The evolving mix underlines a shift from problem-solving scans toward proactive, protocol-driven population health, directly influencing vendor R&D priorities in motion correction, cardiac mapping, and abbreviated exam design.

Competitive Landscape

Siemens Healthineers, GE Healthcare, and Philips together controlled roughly 70% of the Spain Magnetic Resonance Imaging market in 2024, with Siemens holding the lead following a EUR 20 million framework in Murcia that bundled acquisition and lifecycle services. GE leverages its helium-free Freelium architecture to court sustainability-minded customers, capturing pilot orders at Clinica Universidad de Navarra and early adopters within Quirónsalud’s network. Philips commands a niche for power-efficient BlueSeal magnets, highlighting 1.9 million liters of helium saved worldwide, a talking point resonating with Spanish hospitals pursuing net-zero roadmaps.

Domestic participants play in specialized pockets. PhysioMRI partners with La Fe Hospital on a portable prototype aiming to democratize access in rural provinces, though commercialization remains two years away. Service providers such as Medsir and Egarsat broaden the aftermarket, inking multi-lot maintenance contracts across 28 locations to secure long-tail revenue and protect uptime. AI-startup Quibim contributes high-margin software overlays that vendors bundle into tender pitches, enhancing differentiation without steep hardware discounting.

Competition increasingly centers on workflow automation, cloud-based teleradiology, and predictive maintenance modules that compress downtime below 3%. Vendors package financing solutions that defer capital outlays for cash-strapped hospitals, shifting the conversation from purchase price to total cost of ownership. As EU-MDR solidifies, the compliance moat around incumbent platforms deepens, likely preventing meaningful share erosion over the forecast horizon and reinforcing a moderately concentrated Spain Magnetic Resonance Imaging market.

Spain Magnetic Resonance Imaging Industry Leaders

GE Healthcare

Fujifilm Holdings Corporation

Canon Medical Systems Corporation

Koninklijke Philips NV

Siemens Healthcare AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: PhysioMRI achieved

- February 2024: PhysioMRI attained

Spain Magnetic Resonance Imaging Market Report Scope

As per the scope of the report, magnetic resonance imaging is a medical imaging technique, which is used in radiology to produce pictures of the anatomy and the physiological processes of the body. These pictures are further used to diagnose and detect the presence of abnormalities in the body. Spain Magnetic Resonance Imaging Market is segmented by Architecture (Closed MRI Systems, and Open MRI Systems), Field Strength (Low Field MRI Systems, High Field MRI Systems, and Very High Field MRI Systems and Ultra-high MRI Systems), Application (Oncology, Neurology, Cardiology, Gastroenterology, Musculoskeletal, and Other Applications). The report offers the value (in USD million) for the above segments.

By Architecture

| Closed MRI Systems |

| Open MRI Systems |

By Field Strength

| Low-Field (≤0.55 T) |

| Mid/High-Field (1.5 T) |

| Very-High-Field (3 T) |

| Ultra-High-Field (7 T +) |

By Application

| Neurology |

| Oncology |

| Musculoskeletal |

| Cardiology |

| Gastroenterology |

| Other Applications |

| By Architecture | Closed MRI Systems |

| Open MRI Systems | |

| By Field Strength | Low-Field (≤0.55 T) |

| Mid/High-Field (1.5 T) | |

| Very-High-Field (3 T) | |

| Ultra-High-Field (7 T +) | |

| By Application | Neurology |

| Oncology | |

| Musculoskeletal | |

| Cardiology | |

| Gastroenterology | |

| Other Applications |

Key Questions Answered in the Report

What is the current value of the Spain Magnetic Resonance Imaging market and how fast is it growing?

It is valued at USD 230.11 million in 2026 and is projected to reach USD 289.86 million by 2031, expanding at a 4.72% CAGR.

Which application segment generates the highest scan volume in Spain?

Neurology accounts for 32.40% of national MRI demand, driven by stroke and dementia pathways in an aging population.

How long do patients typically wait for an MRI in SpainÕs public hospitals?

Average public waiting times stand at 67 days, prompting many patients to choose private centers for faster access.

Why are low-field scanners gaining traction among Spanish providers?

Sub-0.55 Tesla systems cut helium use, lower power consumption by about 60%, and are forecast to grow at a 12.18% CAGR through 2031.

Which companies hold the largest share of SpainÕs MRI equipment base?

Siemens Healthineers, GE Healthcare, and Philips collectively control around 70% of installed revenue thanks to long-term hospital partnerships.

How is government funding influencing scanner replacement cycles?

The INVEAT program has injected EUR 796 million to renew 144 units since 2024, reducing the average device age in public hospitals from 18 years to 10 years.

Page last updated on: