Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

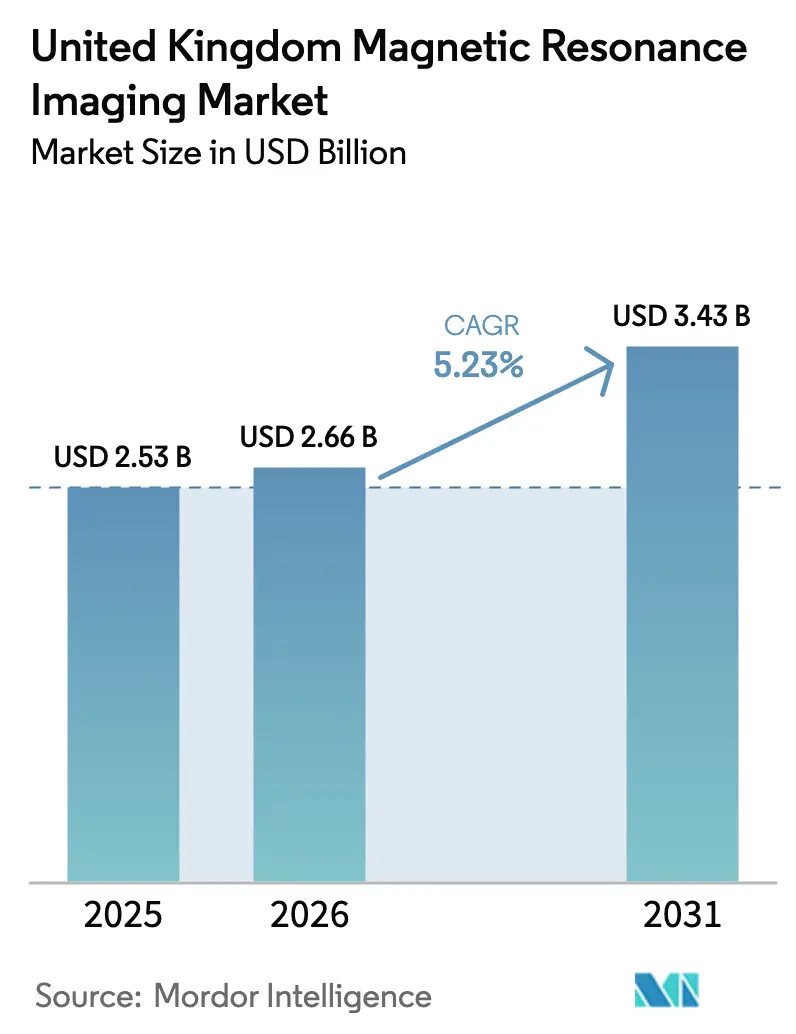

| Base Year Market Size (2025) | USD 2.53 Billion |

| Market Size (2026) | USD 2.66 Billion |

| Market Size (2031) | USD 3.43 Billion |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Magnetic Resonance Imaging Market Analysis by Mordor Intelligence

The United Kingdom magnetic resonance imaging market size was valued at USD 2.53 billion in 2025 and estimated to grow from USD 2.66 billion in 2026 to reach USD 3.43 billion by 2031, at a CAGR of 5.23% during the forecast period (2026-2031). This expansion is fueled by centrally coordinated NHS procurement frameworks that deliver predictable order volumes, volume-discount pricing, and standardization benefits that lower the total cost of ownership for trusts. Rapid adoption of 3 tesla (3 T) platforms is accelerating throughput in neuro-oncology and musculoskeletal pathways, while AI-driven image reconstruction is reducing average scan times, thereby expanding daily slot capacity. In parallel, low-field, virtually helium-free systems are gaining traction as mobile and point-of-care solutions capable of servicing rural populations that experience historically long wait times. Intensifying vendor competition around helium-efficient magnets, integrated software ecosystems, and lifecycle service packages is likely to reinforce buyer bargaining power but will also favor manufacturers investing in domestic production footprints that mitigate post-Brexit logistics risks.

Key Report Takeaways

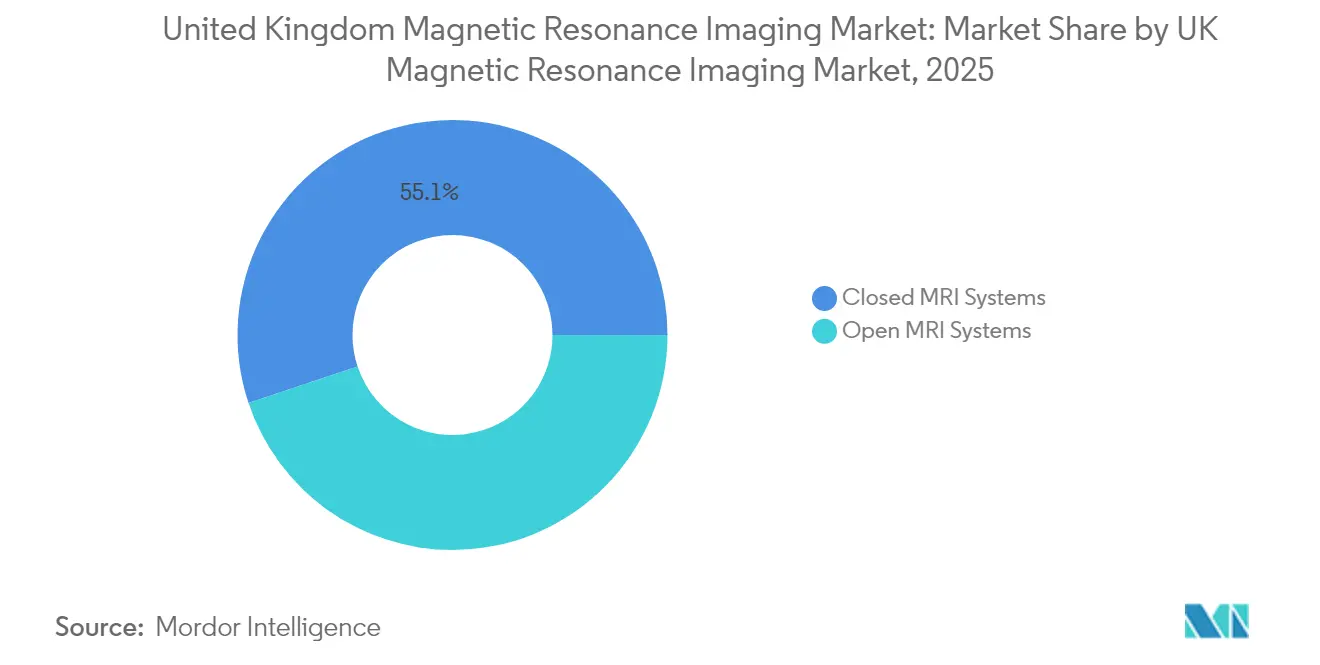

- By architecture, closed systems held 55.12% of the United Kingdom magnetic resonance imaging market share in 2025, while open systems are set to grow at a 6.88% CAGR through 2031.

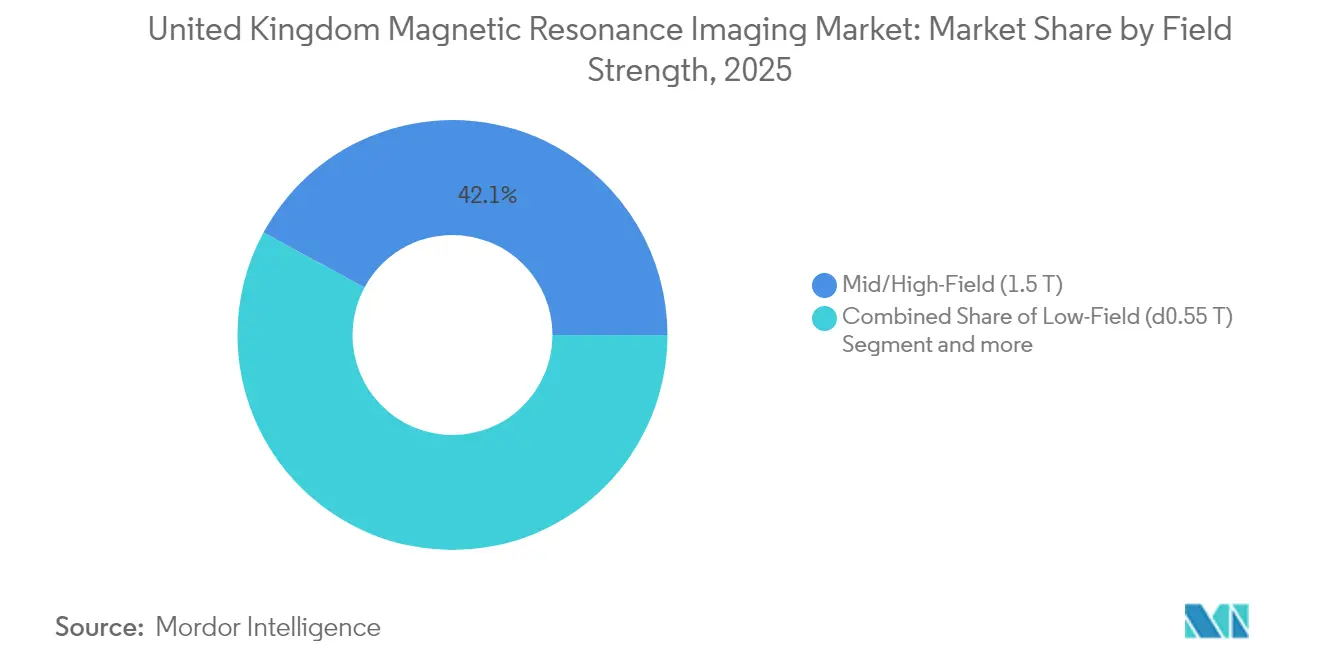

- By field strength, 1.5 T scanners accounted for 42.10% share of the United Kingdom magnetic resonance imaging market size in 2025, whereas low-field systems are projected to expand at a 6.19% CAGR through 2031.

- By application, neurology led with 31.10% revenue share in 2025 and cardiology is advancing at a 6.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Magnetic Resonance Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic and age-related diseases | +1.2% | National, concentrated in aging populations | Long term (≥ 4 years) |

| Rapid adoption of 3 T scanners across NHS estates | +1.8% | National, NHS trust networks | Medium term (2-4 years) |

| AI-driven image reconstruction and workflow optimization | +1.1% | National, early adoption in teaching hospitals | Medium term (2-4 years) |

| Growth of point-of-care low-field MRI pilots in community settings | +0.7% | Regional, rural and underserved areas | Long term (≥ 4 years) |

| Expansion of intra-operative MRI suites for neuro-oncology surgery | +0.4% | National, tertiary care centers | Long term (≥ 4 years) |

| NHS imaging networks’ centralized procurement driving fleet standardization | +0.9% | National, NHS framework agreements | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic and Age-Related Diseases

The proportion of U.K. residents aged 65 years and older reached 19% in 2024 and is projected to climb to 22% by 2030, sharply increasing the incidence of neurodegenerative and musculoskeletal disorders that require advanced MRI diagnostics. MRI procedure volumes already exceed 4.3 million annually, and longitudinal NHS data show double-digit growth in dementia-related scans across northern England and Scotland. High-resolution 3 T systems provide the superior contrast needed for early Alzheimer’s and Parkinson’s detection, which shortens diagnostic odysseys and reduces downstream healthcare costs. Ultra-high-field research at the University of Cambridge demonstrates lesion-level sensitivity improvements that could translate into routine clinical protocols over the forecast period[1]University of Cambridge, “7 Tesla MRI Enhances Brain Lesion Detection,” cam.ac.uk. The linkage between demographic change and escalating neurological morbidity therefore places MRI at the center of age-friendly health-system planning. Vendor strategies that bundle geriatric-focused imaging protocols with AI-enriched post-processing are likely to secure procurement preference as trusts compete to meet government wait-time targets.

Rapid Adoption of 3 T Scanners Across NHS Estates

Centralized buying consortia now award multi-year lots for 3 T platforms, evidenced by recent installations at Imperial College Healthcare and University Hospital Southampton, both of which reported 20% reductions in repeat scans after commissioning higher field strengths[2]Imperial College London, “Implementation of 3 T MRI in Complex Clinical Pathways,” imperial.ac.uk. These outcomes validate the NHS assumption that superior signal-to-noise ratios reduce indeterminate findings that would otherwise trigger follow-up appointments. Capital risk is mitigated by framework contracts that lock in service pricing for up to 12 years, enabling trusts to amortize premium scanners over predictable budgets. By embedding AI-assisted protocols such as Siemens Deep Resolve, hospitals have shown throughput gains of up to 50%, directly addressing an average national MRI wait of 23 days NHS.UK. Vendors offering field-upgrade paths—for example, from 1.5 T to 3 T—are expected to capture incremental share because the strategy preserves legacy infrastructure investments while boosting diagnostic breadth.

AI-Driven Image Reconstruction and Workflow Optimization

Artificial intelligence is emerging as a force multiplier for constrained workforces, with early adopters reporting that machine-learning reconstruction algorithms shorten head and spine examinations by 40% without compromising diagnostic integrity[3]King’s College London, “AI Reconstruction Reduces MRI Scan Times,” kcl.ac.uk. Automated slice planning, artifact suppression, and protocol selection minimize operator variability, which is critical in centers that rotate junior radiographers across multiple modalities. Workflow engines using natural-language order entry now preemptively flag mismatched protocols, trimming non-productive time between patients. Teaching hospitals in London and Manchester are piloting AI-driven scheduling dashboards that dynamically re-allocate idle slots to urgent outpatients, effectively squeezing an extra two cases per scanner each day. Over the forecast horizon, trusts that pair AI software with helium-efficient magnets can defer capital expenditure on additional systems, aligning technology rollout with financial sustainability directives.

Growth of Point-of-Care Low-Field MRI Pilots in Community Settings

Hyperfine’s CE-marked 0.064 T portable scanner, first deployed at King’s Health Partners in 2024, has validated bedside neuroimaging for stroke triage in intensive care units, shaving 25 minutes off door-to-diagnosis time and minimizing inter-facility transfers. Cornwall’s relocatable 1.5 T unit processes 7,000 scans annually and has cut average travel distances for rural patients by 90 miles, demonstrating a robust health-equity case for mobile models. The U.K.’s inaugural virtually helium-free MRI truck, unveiled at UKIO 2024, combines low-field magnets with closed-loop cooling to eliminate vent stacks, enabling parking outside community clinics without infrastructure upgrades. These pilots are informing NHS policy proposals that re-define imaging as a distributed service spanning hospitals, ambulatory centers, and mobile fleets. A successful scale-up could unlock a contiguous low-field segment that co-exists with the high-field hospital tier, reshaping vendor portfolios toward modular, ruggedized platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront and lifecycle costs of MRI equipment | -1.40% | National, budget-constrained trusts | Medium term (2-4 years) |

| Stringent UKCA/CE regulatory and HTA approval processes | -0.80% | National, post-Brexit compliance | Short term (≤ 2 years) |

| Shortage of radiographers and MR-qualified physicists | -1.10% | National, acute in rural areas | Long term (≥ 4 years) |

| Volatile global helium supply affecting uptime | -0.60% | Global supply chain impact | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront and Lifecycle Costs of MRI Equipment

Even with framework discounts, a new 3 T scanner and room build-out can exceed USD 3.5 million, stretching the capital envelopes of smaller district hospitals. Lifecycle economics further deteriorate when helium prices spike, as evidenced by Oxford Instruments’ disclosure that cryogen costs eroded its MRI service margins in 2024. Infrastructure retrofits—RF shielding, chiller upgrades, and cable rerouting—often add 35% to total spend, forcing trusts to defer replacements beyond the manufacturer’s recommended 10-year timeline. A secondary-market ecosystem has therefore emerged, offering certified refurbished 1.5 T systems at one-third the new-build price, although guarantees of uptime and software updates remain contentious.

Stringent UKCA/CE Regulatory and HTA Approval Processes

Post-Brexit divergence has compelled manufacturers to secure both UKCA and CE marks, doubling certification-testing fees and elongating launch timelines by up to nine months. The devolved administrations’ Health Technology Assessment committees add another review layer, requiring local clinical-effectiveness dossiers before capital allocation. Smaller manufacturers of specialty coils and contrast agents face disproportionate compliance burdens, potentially curbing innovation in ancillary technologies. While convergence initiatives are under discussion, near-term friction persists, slowing the entry of niche solutions that could alleviate workflow bottlenecks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Architecture: Closed Systems Drive Premium Applications

Closed-bore systems generated USD 1.39 billion in 2025, equal to 55.12% of the United Kingdom magnetic resonance imaging market, owing to their superior magnetic homogeneity that supports functional brain mapping, spectroscopy, and time-resolved cardiac imaging. Institution-level evidence shows that closed platforms reduce motion artifacts in pediatric sedation cases, a critical KPI for trusts that benchmark image-repeat rates. Though the initial purchase price is higher, refurbishment cycles reveal that closed systems retain residual value 25% above open counterparts, which influences leasing strategies. In mobile deployments, logistical trade-offs around weight and cooling are increasingly offset by diagnostic versatility and patient throughput, leading mobile fleet operators to favor closed 1.5 T units over lighter, open low-field alternatives.

Open designs, typically operating at 0.3–0.5 T, captured USD 1.14 billion in 2025 and are projected to grow at a 6.88% CAGR until 2031, the fastest of any architecture category. The growth rate stems from patient-centric factors such as claustrophobia mitigation and bariatric accommodation, which win favor in community hospitals and imaging centers that compete on comfort scores. AI-based denoising is narrowing the image-quality gap with closed systems, expanding the clinical indications suitable for open magnets beyond simple orthopedic scans. As the U.K. health-service strategy pivots toward community-based diagnostics hubs, open platforms will likely see pilot funding, yet their absolute market share gain remains capped by limitations in advanced neuro and cardiac protocols.

By Field Strength: Low-Field Gains Traction Despite 1.5 T Leadership

Mid/high-field 1.5 T scanners contributed USD 1.07 billion, representing 42.10% of the United Kingdom magnetic resonance imaging market size in 2025, and remain the cornerstone for routine head, spine, and abdominal imaging. The modality’s mature workflow, abundant coil inventory, and favorable reimbursement profile support a utilization rate that exceeds 22 exams per day in high-volume centers. Economical helium-sparing upgrades and hybrid-system field-strength ramps are elongating fleet life, reinforcing 1.5 T dominance in the medium term.

Low-field systems at or below 0.55 T accounted for USD 162 million in revenue but will advance at a 6.19% CAGR, driven by their compatibility with plug-and-play electrical installations and helium independence. Pilot programs in Yorkshire demonstrated that low-field neuro protocols can triage stroke candidates within ambulances, compressing time-to-thrombolysis by six minutes on average. Vendor roadmaps illustrate a pipeline of multi-nuclear capabilities for low-field units, potentially expanding into metabolic imaging that sidesteps high-license-fee contrast agents.

At the other end, 3 T systems crossed USD 920 million in 2025 and will gain share in tertiary and private segments because of superior signal-to-noise performance, which translates into sub-five-minute neuro exams when paired with compressed-sensing software. Ultra-high-field platforms at 7 T and above remain niche but strategically important. The Nottingham 11.7 T initiative, funded at USD 52 million, exemplifies public-private collaboration that carries spillover benefits for domestic magnet manufacturers and cryogenics suppliers.

By Application: Cardiology Accelerates While Neurology Leads

Neurological imaging accounted for USD 787 million in 2025, equal to 31.10% of the United Kingdom magnetic resonance imaging market share, reflecting high prevalence of dementia, multiple sclerosis, and epilepsy diagnoses. Functional MRI and diffusion-tensor protocols are becoming routine for presurgical planning, driving demand for machines equipped with multichannel head coils and advanced gradient designs. NHS England’s Rapid Diagnostic Centre model integrates neuroimaging with genomics and blood biomarkers, positioning MRI as the central confirmatory tool for pathway triage.

Cardiac MRI generated USD 338 million but is poised to grow at a 6.05% CAGR, the fastest among applications. The British Heart Foundation and Society for Cardiovascular MRI advocate guideline updates that elevate MRI over CT for ischemia and cardiomyopathies, catalyzing procurement of scanners with wide-bore geometry and motion-correction algorithms. AI-enabled reconstruction reduces breath-hold requirements, making the modality accessible to frail or pediatric patients. Musculoskeletal and oncology indications collectively contributed more than USD 600 million, supported by sports-medicine demand ahead of the 2028 European Championships and expanding precision-oncology trial pipelines that rely on whole-body diffusion protocols.

Competitive Landscape

Siemens Healthineers, GE Healthcare, and Philips collectively capture roughly 60% of the United Kingdom magnetic resonance imaging market, leveraging integrated hardware-plus-software portfolios, nationwide service teams, and strong vendor-financing arms. Siemens’ USD 313 million dry-cool magnet plant in Oxford engineers helium-light cryostats that shave 30% off running costs, a differentiator amid tightening NHS budgets. GE’s collaboration with the University of Manchester embeds multi-nuclear spectroscopy capabilities in select 3 T models, appealing to oncology research consortia. Philips, through its Eindhoven-to-Cambridge innovation corridor, has fast-tracked AI-powered cardiac packages that achieved NICE technology appraisal endorsement in 2025.

Domestic firms occupy strategic niches. Tesla Engineering’s superconducting magnet business, headquartered in Storrington, won the USD 52 million contract to build the 11.7 T magnet for Nottingham, spotlighting sovereign capability in ultra-high-field components. Oxford Instruments supplies cryogenic accessories while pursuing helium-recycling skids that could retrofit legacy fleets. Hyperfine and United-Imaging aggressively court the low-field and value segments, but face regulatory friction and service-network deficits.

Competitive dynamics are shifting toward total cost of ownership, with trusts assigning 30% tender weighting to service uptime metrics. Vendors now bundle AI licenses, coils, contrast-injector interfaces, and cloud PACS seats into subscription models that convert lumpy capital budgets into predictable operational expenditure. Strategic alliances with cloud-service providers deliver edge-compute resources for on-scanner inference, further blurring the lines between equipment and software suppliers.

United Kingdom Magnetic Resonance Imaging Industry Leaders

Canon Medical Systems Corporation

GE Healthcare

Siemens Healthcare AG

Koninklijke Philips NV

Esaote SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: FUJIFILM Europe GmbH launched the new FUJIFILM ECHELON Synergy ZeroHelium 1.5T MRI system in the United Kongdom. This next-generation magnetic resonance imaging technology delivers advanced clinical performance while completely eliminating the use of liquid helium, a scarce and costly natural resource.

- May 2024: Siemens Healthineers opened a USD 313 million low-helium magnet manufacturing hub in Oxford, tripling European production capacity for dry-cool MRI systems.

- April 2024: University of Nottingham selected Tesla Engineering and Philips UK to develop a bespoke 11.7 T scanner for the UKRI-funded national facility, a USD 52 million project that will deliver the most powerful MRI in Britain

- February 2023: Canon Medical Systems launched its Auto Scan Assist, artificial intelligence (AI) software, to streamline the MRI exam workflow. The software will assist United Kingdom National Health Service (NHS) radiology departments in streamlining their planning of MRI exams and enable the automated slice alignment for anatomical

United Kingdom Magnetic Resonance Imaging Market Report Scope

As per the scope of the report, magnetic resonance imaging is a medical imaging technique used in radiology to produce pictures of the anatomy and the physiological processes of the body. These pictures are further used to diagnose and detect the presence of abnormalities in the body. United Kingdom Magnetic Resonance Imaging Market is Segmented by Architecture (Closed MRI Systems and Open MRI Systems), Field Strength (Low Field MRI Systems, High Field MRI Systems, and Very High Field MRI Systems and Ultra-high MRI Systems), Application (Oncology, Neurology, Cardiology, Gastroenterology, Musculoskeletal, and Other Applications). The report offers the value (in USD) for the above segments.

By Architecture

| Closed MRI Systems |

| Open MRI Systems |

By Field Strength

| Low-Field (≤0.55 T) |

| Mid/High-Field (1.5 T) |

| Very-High-Field (3 T) |

| Ultra-High-Field (7 T +) |

By Application

| Neurology |

| Oncology |

| Musculoskeletal |

| Cardiology |

| Gastroenterology |

| Other Applications |

| By Architecture | Closed MRI Systems |

| Open MRI Systems | |

| By Field Strength | Low-Field (≤0.55 T) |

| Mid/High-Field (1.5 T) | |

| Very-High-Field (3 T) | |

| Ultra-High-Field (7 T +) | |

| By Application | Neurology |

| Oncology | |

| Musculoskeletal | |

| Cardiology | |

| Gastroenterology | |

| Other Applications |

Key Questions Answered in the Report

How large is the United Kingdom magnetic resonance imaging market in 2026?

The United Kingdom magnetic resonance imaging market size is USD 2.66 billion in 2026.

What is the expected growth rate for MRI equipment demand in the U.K. over the next five years?

Demand is projected to rise at a 5.23% CAGR, taking revenue to USD 3.43 billion by 2031 (2026-2031).

Which MRI application segment is expanding the fastest across NHS trusts?

Cardiac imaging shows the highest growth trajectory, advancing at a 6.05% CAGR through 2031, fueled by British Heart Foundation research investments.

Why are low-field MRI systems gaining attention in the United Kingdom?

Low-field platforms enable mobile and point-of-care imaging that addresses rural access gaps and operate with little or no helium, lowering total operating costs.

What is driving the switch from 1.5 T to 3 T scanners in England?

Centralized NHS procurement favors 3 T systems because they reduce repeat scans, improve diagnostic confidence in neurology and oncology, and pair effectively with AI reconstruction tools that cut scan times.

How are manufacturers addressing helium supply challenges?

Major vendors are investing in dry-cool and low-helium magnet designs, exemplified by Siemens HealthineersÕ new Oxford plant that focuses on helium-efficient cryostats.

Page last updated on: