Hyaluronic Acid Based Dermal Fillers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

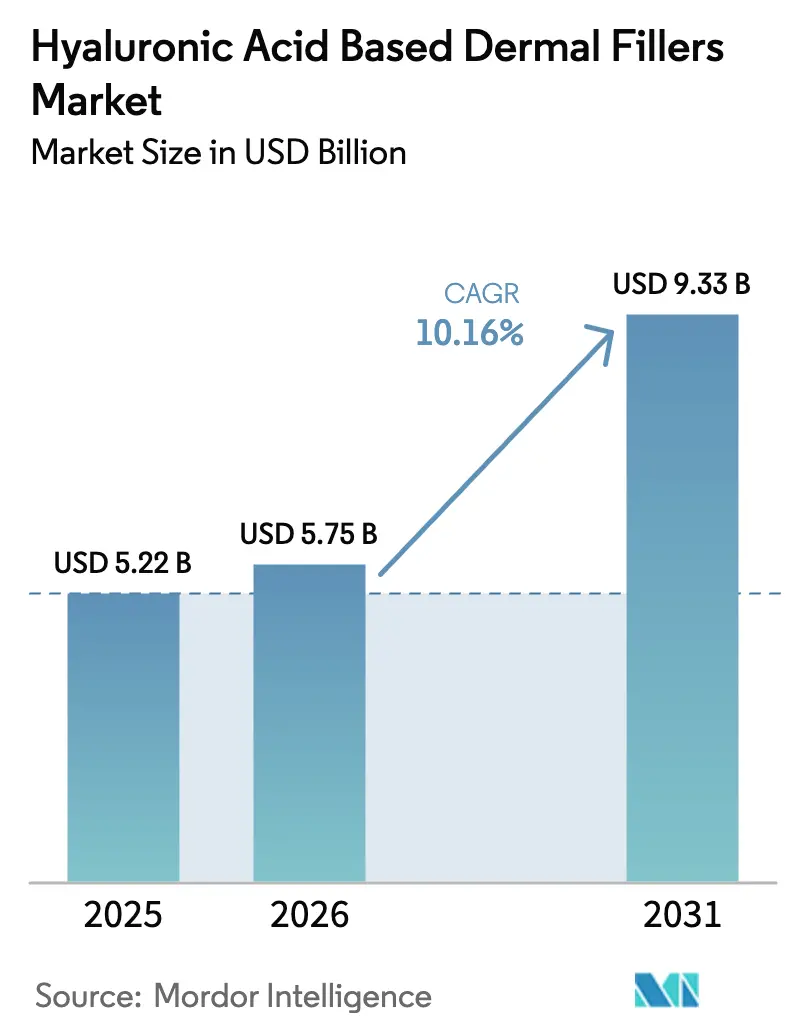

| Market Size (2026) | USD 5.75 Billion |

| Market Size (2031) | USD 9.33 Billion |

| Growth Rate (2026 - 2031) | 10.16% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hyaluronic Acid Based Dermal Fillers Market Analysis by Mordor Intelligence

The Hyaluronic Acid Based Dermal Fillers Market size is projected to be USD 5.22 billion in 2025, USD 5.75 billion in 2026, and reach USD 9.33 billion by 2031, growing at a CAGR of 10.16% from 2026 to 2031.

Uptake is fueled by a widening base of aging consumers who prefer quick office treatments, steady procedural innovation that extends filler longevity, and the rise of male and millennial “pre-juvenation” patients. Price pressure is intensifying as Asia-Pacific entrants ship lower-cost brands into mature regions, yet higher treatment volumes have more than offset fee compression in North America. Manufacturers are broadening their portfolios with thermoresponsive gels and skin boosters, while clinics court recurring revenue through maintenance-based protocols that promote quarterly touch-ups rather than once-a-year bulk injections. Consolidation among suppliers of pharmaceutical-grade hyaluronic acid is helping stabilize input costs and improve purity controls.

Key Report Takeaways

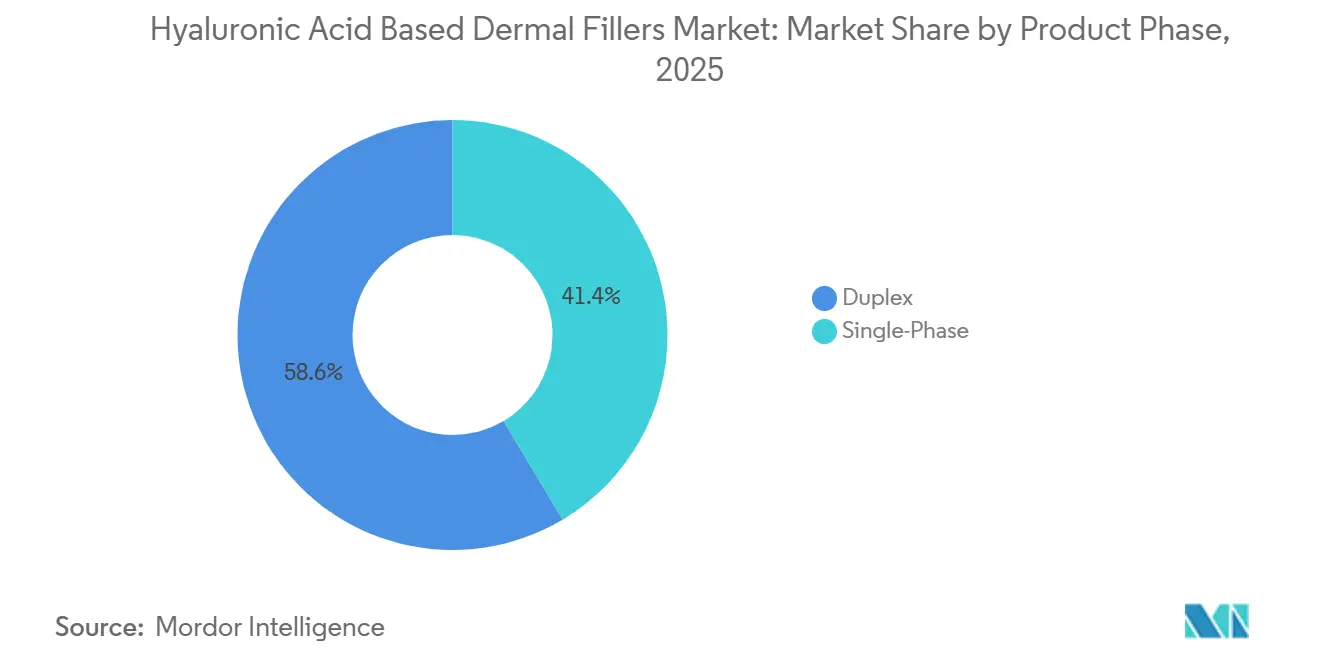

- By product phase, duplex formulations led with 58.56% Hyaluronic Acid Based Dermal Fillers market share in 2025, while single-phase gels are forecast to advance at an 11.25% CAGR to 2031.

- By application, wrinkle correction held 35.53% of revenue in 2025; lip augmentation is on track for a 12.85% CAGR through 2031.

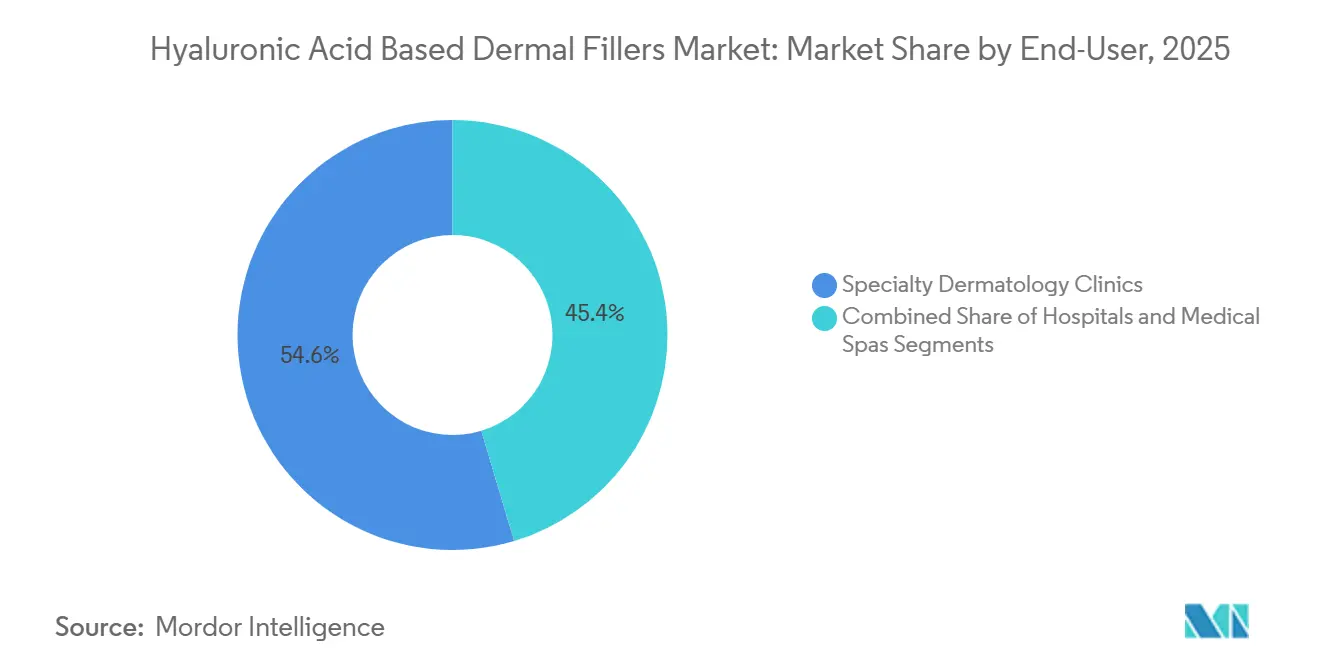

- By end-user, specialty dermatology clinics dominated with 54.63% revenue in 2025, whereas medical spas are poised for an 11.87% CAGR to 2031.

- By ingredient source, animal-derived fillers retained 45.13% share in 2025; fully-synthetic variants are expected to grow at an 11.7% CAGR to 2031.

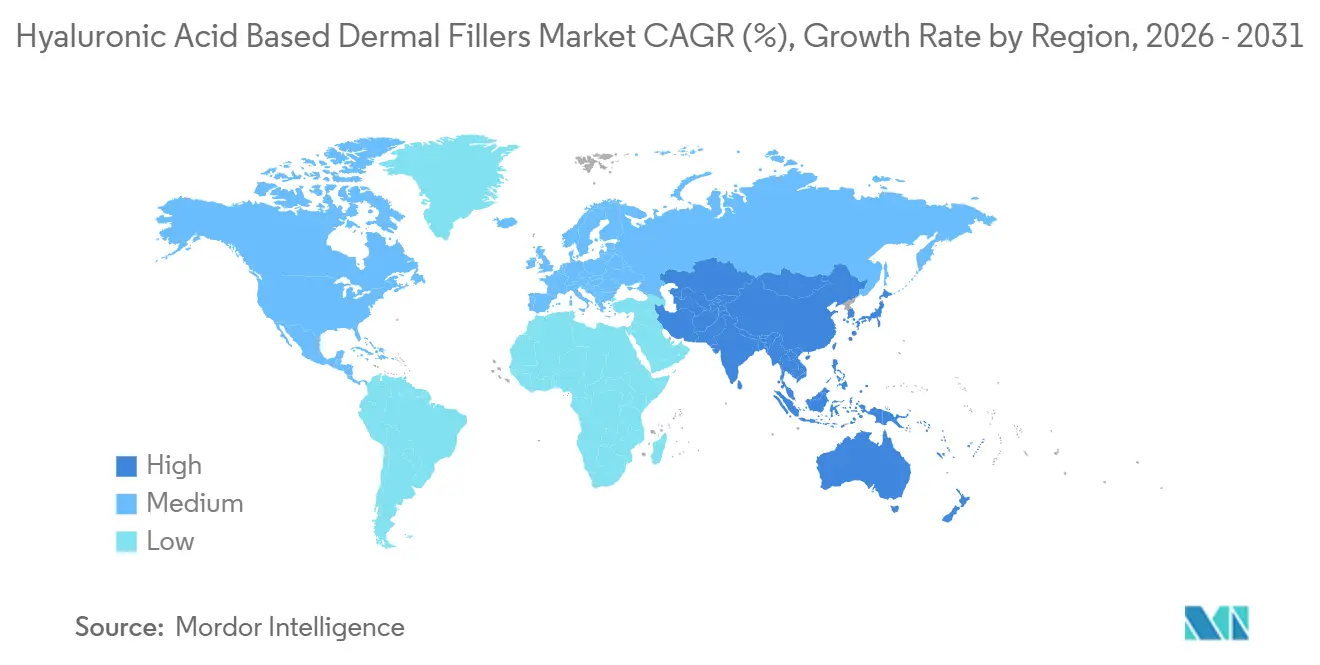

- By geography, North America contributed 42.13% of 2025 revenue, and Asia-Pacific is projected to post a 12.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hyaluronic Acid Based Dermal Fillers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for minimally-invasive aesthetic procedures among aging populations | +2.5% | Global, concentrated in North America, Europe, urban Asia-Pacific | Medium term (2 – 4 years) |

| Rapid product innovation in cross-linking chemistry extending filler longevity | +2.0% | North America and Europe, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Expansion of male & millennial “pre-juvenation” consumer segments | +1.8% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Emergence of micro-droplet skin-booster HA treatments | +1.5% | Global, early uptake in Europe and Asia-Pacific | Medium term (2 – 4 years) |

| Tariff-driven localization of bacterial-fermentation capacity | +1.2% | Asia-Pacific core, secondary in North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Minimally-Invasive Aesthetic Procedures Among Aging Populations

Demographic aging is expanding the candidate pool for fillers, and the 40-54 cohort accounted for 50% of U.S. procedures in 2024. Procedure counts climbed to 5.33 million in 2024 even as average fees slid to USD 715, confirming that convenience outweighs cost concerns for many patients. Regulatory allowances for medical-spa injections in North America and Europe are widening access, while maintenance-oriented “tweakments” support quarterly visit schedules and repeat revenue. The result is a steady cadence of injections that benefits both product suppliers and clinics.

Rapid Product Innovation in Cross-Linking Chemistry Extending Filler Longevity

Manufacturers have shifted from BDDE to PEGDE and auto-crosslinked polymer platforms that improve durability and reduce soluble fractions, with reaction thresholds above 130 mg/mL yielding better clinical performance gels. Thermoresponsive hydrogels that pass through 34-gauge needles at forces under 72 N lessen injection pain. Animal-free production strains from Novozymes and engineered Corynebacterium have produced titers of 45 g/L, lowering fermentation cost and encouraging local manufacturing.

Expansion of Male & Millennial “Pre-Juvenation” Consumer Segments

Seventy-five percent of plastic surgeons noted more sub-30 clientele in 2024, with many seeking subtle enhancement over correction. Online visibility of aesthetic results sets conservative norms - ideal lip ratios, for instance, favor upper-to-lower height of 20 - 25%. Manufacturers have refined packaging, as seen in Merz’s upgraded BELOTERO syringe earning 93% user approval.

Emergence of Micro-Droplet Skin-Booster HA Treatments Opening New Maintenance-Therapy Streams

Approvals of SKINVIVE and RHA Redensity highlight a class aimed at hydration and skin quality rather than volume. Protocols call for multiple sessions and periodic upkeep, creating dependable revenue for providers and broadening the Hyaluronic Acid Based Dermal Fillers market beyond wrinkle reduction alone. Strategic launches such as Galderma’s Restylane VOLYME in China indicate geographic tailoring of new offerings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High out-of-pocket cost versus short durability | -1.5% | Global, most acute in Asia-Pacific & Latin America | Short term (≤ 2 years) |

| Heightened regulatory scrutiny & adverse-event reporting | -1.0% | North America & Europe, rising in Asia-Pacific | Medium term (2 – 4 years) |

| Supply-chain impurity controls raising COGS | -0.8% | Global, heavier in Asia-Pacific & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Cost Versus Short Durability

Fillers last 6–18 months, and repeat fees accumulate quickly. Although U.S. prices slipped to USD 715, cost remains a deterrent, especially in regions where insurance coverage is absent. China’s aggressive competition has pushed retail prices to as low as CNY 200, hurting margins. Multinationals exit low-margin segments, as evidenced by LG Chem’s sale of YVOIRE.

Heightened Regulatory Scrutiny & Adverse-Event Reporting

Rare vascular complications prompt detailed labeling, with tenderness documented in up to 76% of FDA trials[1]U.S. Food and Drug Administration, “EVOLYSSE FORM and SMOOTH Approval,” fda.gov. The European MDR now classifies fillers as Class III devices, elongating approval cycles and raising evidence thresholds. Post-market surveillance adds recurrent costs that smaller firms struggle to absorb, nudging the Hyaluronic Acid Based Dermal Fillers market toward better-capitalized players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Phase: Duplex Formulations Anchor Deep-Tissue Procedures

Duplex gels accounted for 58.56% of 2025 revenue, giving the Hyaluronic Acid Based Dermal Fillers market size its structural backbone in cheek, chin, and jawline jobs. Their biphasic composition confers an elastic modulus above 200 Pa, enabling them to hold shape under compression. Single-phase gels, however, will post the swiftest 11.25% CAGR due to their smoother rheology, which suits superficial corrections and skin boosters.

Thermoresponsive single-phase variants, injectable via ultra-fine needles, further lower pain thresholds and shorten chair time. Regulatory traction is building; Juvederm Voluma XC’s 2024 temple label expansion validated duplex safety in vascular-rich zones[2]U.S. Food and Drug Administration, “Juvederm Voluma XC Temple Indication,” fda.gov.

By Application: Lip Augmentation Sets the Growth Pace

Wrinkle correction still ruled with 35.53% revenue in 2025, but lip augmentation will outstrip it at a 12.85% CAGR as social media aesthetics normalize fuller yet balanced lips. Teoxane RHA 3 gained an expanded FDA indication in 2023, opening regulated pathways for lip-specific lines.

Volume restoration for mid-face and chin, along with scar remediation, is expanding steadily, propelled by broader reconstructive uses. Research underpins subtlety: lip ratios above 30% upper-to-lower height were deemed unaesthetic by 88% of respondents, guiding injector training and shaping consumer expectations inside the Hyaluronic Acid-Based Dermal Fillers market.

By End-User: Medical Spas Capture Volume, Clinics Retain Complex Cases

Specialty dermatology clinics held 54.63% of 2025 sales, but medical spas will enjoy an 11.87% CAGR as state rules permit nurse-led injections under physician oversight. Hyaluronic Acid-Based Dermal Fillers market share consolidation is evident as group purchasing agreements enable spas to negotiate bulk discounts.

Clinics counter by emphasizing board-certified expertise for high-risk zones, while hospitals remain niche, largely serving reconstructive needs. Revance surpassed 7,000 active aesthetic accounts by late-2023, many located in med-spa settings, illustrating the channel’s purchasing clout.

By Ingredient Source: Fully-Synthetic Options Gain Favor Amid Purity Mandates

Animal-derived fillers still occupied 45.13% of revenue in 2025, yet fully-synthetic formats will climb at 11.7% CAGR as regulators tighten contaminant limits. Engineered Corynebacterium hit 45 g/L titers at high molecular weight, dropping cost below legacy rooster-comb extraction.

Investments like HTL’s EUR 12 million sterile line and Lifecore’s USD 150 million capacity boost show supply chains moving closer to Western demand centers, a shift likely to stabilize the Hyaluronic Acid-Based Dermal Fillers market against tariff shocks.

Geography Analysis

North America delivered 42.13% of 2025 sales, strengthened by 5.33 million U.S. procedures in 2024 despite fee declines, reflecting volume-driven growth. Medical-spa permissiveness broadens access, while FDA approvals of EVOLYSSE FORM and SMOOTH add competitive depth. Canada’s adoption of Restylane SHAYPE for body contouring and Mexico’s growing tourism trade signal spillover potential.

Asia-Pacific is set for a 12.21% CAGR to 2031, propelled by China’s streamlined NMPA approvals, South Korea’s price-competitive clinics, and Japan’s aging yet aesthetics-aware demographic. Beijing IMEIK’s USD 190 million purchase of RegenBiotech highlights strategic consolidation. Bloomage’s export sales exceeding domestic revenue in 2024 prove the region’s capacity to serve global demand.

Europe retains a sizeable slice, but MDR-driven evidence demands lengthen launch timelines, advantaging entrenched brands. Galderma’s Restylane VOLYME launch across major EU markets in 2024 shows continued appetite for high-performance gels. The Middle East, buoyed by GCC wealth and medical tourism, and Latin America, led by Brazil’s aesthetic culture, round out growth nodes, though regulatory heterogeneity complicates rollouts.

Competitive Landscape

AbbVie’s Allergan Aesthetics, Galderma, Merz, and Teoxane control a significant percentage of revenue, while Chinese firms—IMEIK, Bloomage, Haohai—erode price points with high-volume capacity. LG Chem’s 2025 divestiture of YVOIRE underscores margin pressure in commoditized tiers. Revance’s extended distribution pact with Teoxane locks in minimum purchases through 2029, revealing the Hyaluronic Acid-Based Dermal Fillers industry’s reliance on channel synergies[3]Revance Therapeutics, “Form 8-K Sixth Amendment,” sec.gov.

Technology differentiators include thermoresponsive gels and hybrid HA-biostimulator blends aimed at longer persistence. Lifecore’s 38% capacity add and HTL’s French sterile line embody a shift toward localized, GMP-compliant supply chains that can navigate stricter impurity rules. Market entry barriers rise with each regulatory tightening, nudging the field toward mid-concentration and favoring players that can finance post-market studies and global compliance.

Hyaluronic Acid Based Dermal Fillers Industry Leaders

Galderma S.A.

LG Chem Ltd.

AbbVie Inc. (Allergan Aesthetics)

Merz Pharma GmbH & Co. KGaA

Teoxane S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Galderma won FDA clearance for Restylane Lyft with Lidocaine for chin augmentation in U.S. adults.

- September 2025: Allergan Aesthetics launched “Naturally You with Injectable Hyaluronic Acid Fillers,” an education push aimed at demystifying HA injectables.

Global Hyaluronic Acid Based Dermal Fillers Market Report Scope

According to the report's scope, hyaluronic acid is a temporary dermal filler that is naturally present in the human body. Hyaluronic acid dermal fillers are widely used due to their biodegradability. Hyaluronic acid products are used to enhance the skin's contour and reduce the appearance of scars, lines, or injuries.

The hyaluronic acid-based dermal fillers market is segmented by product phase into single-phase and duplex. By application, the market is categorized into wrinkle correction, scar treatment, volume restoration, lip augmentation, and others. By end-user, the segmentation includes hospitals, specialty dermatology clinics, and medical spas. By ingredient source, the market is divided into animal-derived, non-animal fermentation, and fully-synthetic. By geography, the market is segemented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD) for the above segments.

| Single-Phase |

| Duplex |

| Wrinkle Correction |

| Scar Treatment |

| Volume Restoration |

| Lip Augmentation |

| Others |

| Hospitals |

| Specialty Dermatology Clinics |

| Medical Spas |

| Animal-Derived |

| Non-Animal Fermentation |

| Fully-Synthetic |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Phase | Single-Phase | |

| Duplex | ||

| By Application | Wrinkle Correction | |

| Scar Treatment | ||

| Volume Restoration | ||

| Lip Augmentation | ||

| Others | ||

| By End-User | Hospitals | |

| Specialty Dermatology Clinics | ||

| Medical Spas | ||

| By Ingredient Source | Animal-Derived | |

| Non-Animal Fermentation | ||

| Fully-Synthetic | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Hyaluronic Acid-Based Dermal Fillers market today?

The market reached USD 5.75 billion in 2026 and is forecast to hit USD 9.33 billion by 2031.

What CAGR is expected for hyaluronic acid fillers between 2026 and 2031?

The compound annual growth rate is projected at 10.16%.

Which application segment will expand fastest through 2031?

Lip augmentation is forecast to grow at a 12.85% CAGR as social-media aesthetics drive demand.

Why are single-phase gels gaining momentum?

Their smooth rheology suits superficial wrinkle correction and skin-booster protocols, supporting an 11.25% CAGR outlook.

Which region offers the highest growth potential?

Asia-Pacific is projected to post a 12.21% CAGR, led by China, South Korea, and Japan.

What is driving regulatory scrutiny of fillers?

Reports of rare vascular occlusions and delayed inflammatory reactions have prompted agencies to mandate stricter safety labeling and post-market surveillance.

Page last updated on: