Market Overview

| Study Period | 2020 - 2031 |

|---|---|

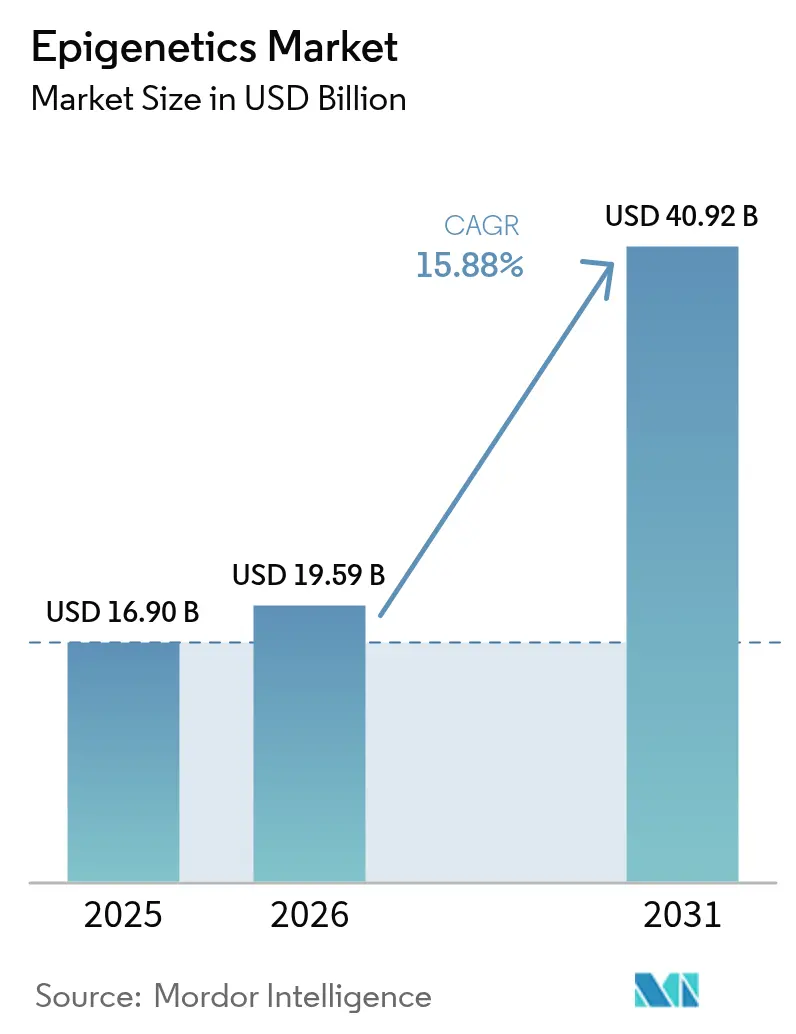

| Market Size (2026) | USD 19.59 Billion |

| Market Size (2031) | USD 40.92 Billion |

| Growth Rate (2026 - 2031) | 15.88% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Epigenetics Market Analysis by Mordor Intelligence

The Epigenetics market size is expected to grow from USD 16.90 billion in 2025 to USD 19.59 billion in 2026 and is forecast to reach USD 40.92 billion by 2031 at 15.88% CAGR over 2026-2031. Advancing artificial-intelligence algorithms that mine DNA-methylation signatures, long-read sequencing breakthroughs that map complex epigenomic patterns, and faster regulatory clearance for blood-based companion diagnostics are converging to lift demand. Pharmaceutical alliances that embed epigenetic controllers into metabolic and immunological pipelines reinforce near-term commercial traction. The Epigenetics market also benefits from stronger intellectual-property filings around single-cell multi-omics platforms, while venture capital inflows accelerate laboratory automation and cloud bioinformatics ecosystems. North America continues to dominate, yet Asia Pacific shows the steepest uptake as governments subsidize precision-medicine infrastructure and local start-ups adopt pay-per-use sequencing models.

Key Report Takeaways

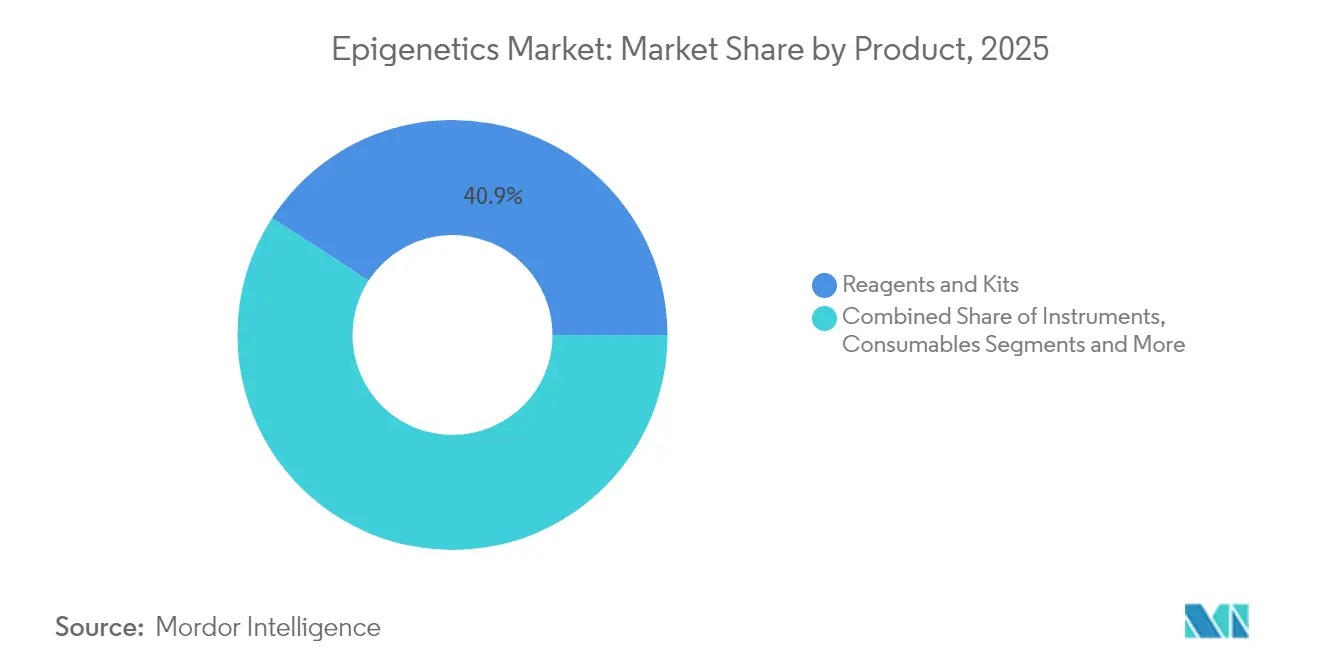

- By product, reagents and kits held 40.85% of the Epigenetics market share in 2025, whereas bioinformatics tools and services are forecast to expand at a 19.62% CAGR to 2031.

- By application, oncology led with 59.65% revenue share in 2025; neurology and CNS disorders are advancing at a 15.99% CAGR through 2031.

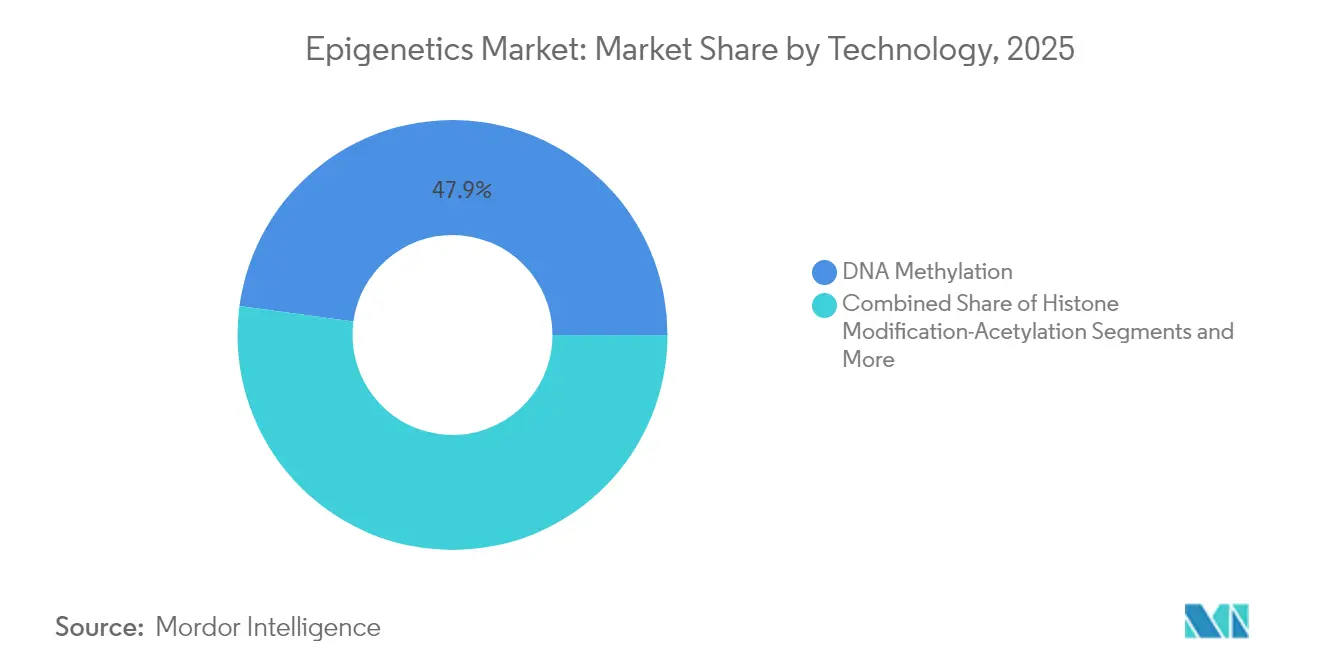

- By technology, DNA methylation analysis commanded 47.85% of Epigenetics market size in 2025 and non-coding RNA analysis is projected to rise at a 18.76% CAGR between 2026-2031.

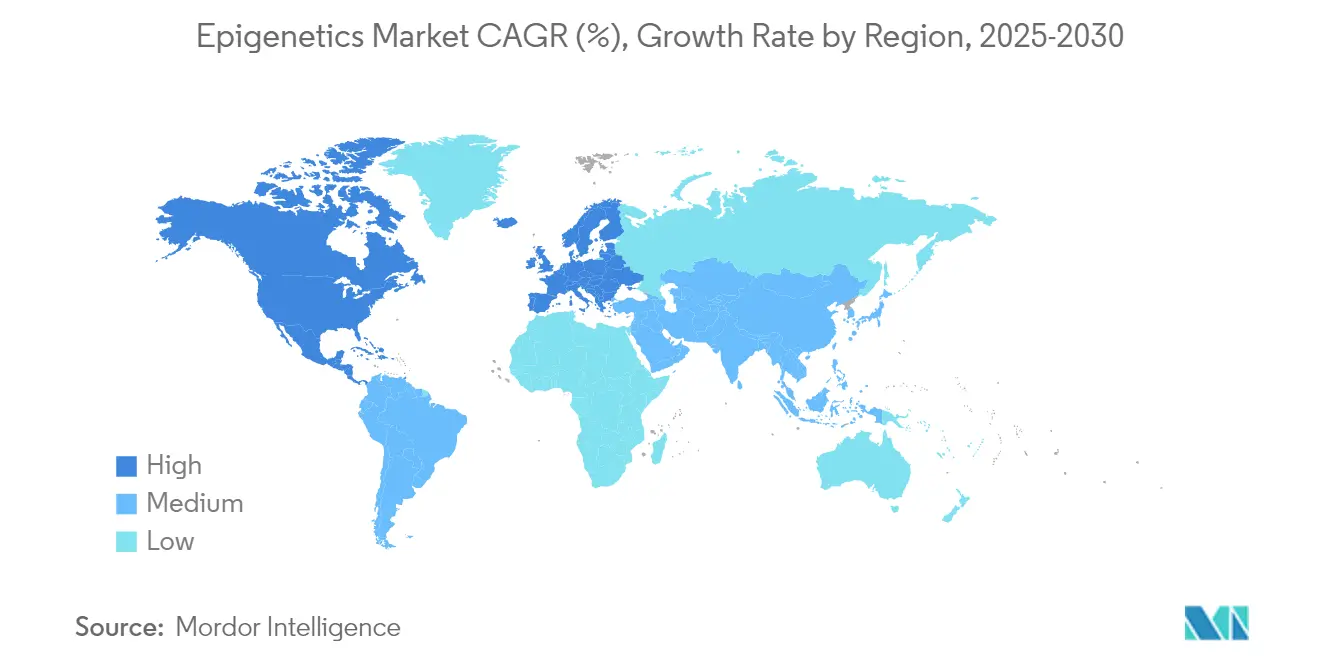

- By region, North America captured 42.95% share of the Epigenetics market in 2025, while Asia Pacific is set to grow at a 16.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Epigenetics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Cancer Incidence & Precision-Medicine Adoption | +4.20% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Expansion Of Epigenetic Applications In Non-Oncology Application | +3.10% | Global, early adoption in North America & Asia Pacific | Long term (≥ 4 years) |

| Surge In Multi-Omics R&D Funding & Collaborative Consortia | +2.80% | North America & Europe primarily, expanding to Asia Pacific | Short term (≤ 2 years) |

| Regulatory Support For Companion Diagnostics | +2.40% | North America & Europe, gradual adoption in Asia Pacific | Medium term (2-4 years) |

| AI-Enabled Epigenetic Biomarker Discovery Accelerators | +2.10% | Global, led by North America tech hubs | Short term (≤ 2 years) |

| Venture Investments In Single-Cell & Long-Read Epigenomics Platforms | +1.40% | North America & Europe, emerging in Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Cancer Incidence & Precision-Medicine Adoption

Escalating global cancer prevalence amid aging populations fuels demand for epigenetic biomarkers that stratify patients and track minimal residual disease. Illumina’s expanded TruSight Oncology portfolio now reports methylation-informed variant calls that refine therapy selection.[1]Illumina Inc., “Illumina transforms multiomic research with new technologies to unlock deeper understanding of biology,” illumina.com Multi-cancer early detection blood tests that read methylation signatures, such as Galleri, move from research to clinics, enabling earlier intervention. In hematological malignancies, integrated epigenomic-genomic profiling is identifying resistance-associated subtypes, thereby broadening indications for epigenetic drugs. The cumulative momentum positions methylation panels as foundational elements in next-generation companion diagnostics.

Expansion of Epigenetic Applications in Non-Oncology Application

Breakthrough studies show long non-coding RNAs regulate neuroinflammation in Alzheimer’s disease, opening therapeutic windows for epigenetic editing.[2]Center for Devices and Radiological Health, “Shield – P230009,” fda.gov Novo Nordisk and Omega Therapeutics are co-creating epigenomic controllers that modulate thermogenesis for obesity treatment. Cardiometabolic pipelines now incorporate integrated genetic-epigenetic risk algorithms that outperform standard lipid tests. Epigenetic re-writing tools that suppress mutant alleles without DNA cuts are entering early-phase trials for Huntington’s disease. Such cross-disciplinary momentum diversifies revenue streams for the Epigenetics market beyond its oncology core.

Surge in Multi-Omics R&D Funding & Collaborative Consortia

The United Kingdom has partnered with Oxford Nanopore Technologies and the UK Biobank to sequence 50,000 epigenomes, an initiative valued at close to USD 300 million.[3]Neuroglia, “The synergistic roles of glial cells and non-coding RNAs in the pathogenesis of Alzheimer's disease and related dementias,” neuroglia.com Venture investors backed Turn Bio with USD 300 million for re-programming platforms, while Tune Therapeutics raised USD 175 million for hepatitis B epigenome editing. Cross-institutional consortia are standardizing read-depth, base-calling, and metadata pipelines, lowering reproducibility barriers. Cloud-based multi-omics workspaces now integrate methylome, transcriptome, and proteome layers, accelerating biomarker validation. Collectively, these investments shorten the bench-to-bedside cycle that underpins the Epigenetics market growth.

Regulatory Support for Companion Diagnostics

The FDA green-lit Guardant’s Shield test marked the agency’s first approval of a blood assay that reads both genetic mutations and methylation alterations for colorectal cancer screening. Europe advanced the Health Data Space regulation, creating explicit lanes for epigenomic data sharing across borders. The FDA’s Biomarker Qualification Program is reviewing multiple methylation signatures for solid tumors and neurodegeneration, signaling a predictable evidentiary path. Pharmaceutical sponsors now embed epigenetic endpoints from Phase I onward, reducing regulatory risk for eventual companion diagnostics. The streamlined environment lifts confidence in the Epigenetics market commercialization timelines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of NGS & Single-Molecule Instruments | -2.80% | Global, particularly affecting emerging markets | Medium term (2-4 years) |

| Shortage Of Skilled Bioinformaticians | -2.10% | Global, acute in Asia Pacific & emerging markets | Long term (≥ 4 years) |

| Data-Privacy Hurdles For Population-Scale Epigenomic Datasets | -1.70% | Europe & North America primarily, expanding globally | Short term (≤ 2 years) |

| Limited Reimbursement Pathways For Epigenetic Diagnostics | -1.40% | Global, varying by healthcare system maturity | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of NGS & Single-Molecule Instruments

Even as whole-genome sequencing trends toward the USD 100 threshold, comprehensive epigenomic workflows still need higher coverage, specialized library kits, and robust long-read platforms that keep per-sample costs elevated. Oxford Nanopore’s PromethIon, for instance, requires sophisticated fluidics upkeep and high-end GPUs. Single-cell methylome pipelines add separate tagmentation steps, proprietary reagents, and expanded compute clusters. Depreciation charges and recurring service contracts strain clinical labs in Brazil, South Africa, and Indonesia, slowing adoption in those high-burden cancer territories. Bundled leasing and reagent-rental schemes are emerging but have yet to close the affordability gap fully.

Shortage of Skilled Bioinformaticians

Demand for coders proficient in Python, machine-learning frameworks, and graph databases far outstrips supply across the biopharma value chain. Hospitals aiming to introduce methylation panels confront hiring bottlenecks because clinical geneticists rarely possess advanced computational training. Academic programs struggle to refresh curricula fast enough to cover single-cell ATAC-seq, variant-aware methyl-caller algorithms, and FAIR data principles. The talent scarcity inflates salaries, making it harder for smaller start-ups in Vietnam and Kenya to retain analysts once they gain cloud-omics experience. Upskilling initiatives are underway, yet their impact will materialize only in the next five years, tempering the Epigenetics market expansion rate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Reagents Sustain Leadership While Bioinformatics Accelerates

Reagents and kits accounted for 40.85% of the epigenetics market share in 2025, propelled by continued bulk purchasing of bisulfite-conversion chemistries and chromatin-immunoprecipitation reagents. Instruments ranked second owing to rising demand for long-read sequencers that detect 5mC, 5hmC, and 6mA directly. The bioinformatics sub-segment, however, is projected to record a 19.62% CAGR through 2031, underpinned by AI-powered cloud pipelines that translate raw signal data into actionable biomarker insights. Advanced analytics vendors now offer pay-as-you-go methylome pipelines, lowering entry barriers for mid-tier hospitals. New patents around machine-learning models for epigenetic age, immune status, and treatment response continue to command premium licensing fees, reflecting the data gravity shift inside the Epigenetics market.

The Epigenetics industry is witnessing a pivot from hardware to software differentiation as sequencing accuracy plateaus. Multi-omics dashboards integrate methylation, chromatin accessibility, and long-read transcript counts in a single user interface. Subscription revenues from informatics suites are outpacing reagent sales growth. Consequently, instrument suppliers have begun bundling analytics credits with sequencer purchases, a tactic that influences total cost-of-ownership decision calculus among clinical labs. Given these currents, bioinformatics platforms are positioned to overtake consumables in revenue contribution by the late forecast horizon.

By Application: Oncology Dominance Faces Neurological Challenge

Oncology applications secured 59.65% of the Epigenetics market revenue in 2025 due to the broad adoption of tumor-agnostic companion diagnostics and minimal residual disease monitoring. Liquid-biopsy products that combine mutation and methylation calling now inform adjuvant-chemotherapy decisions in colorectal cancer. Even so, neurology and CNS disorders are rising at a 15.99% CAGR, spurred by discoveries that chromatin dysregulation underlies Alzheimer’s and autism spectrum pathology. Academic spin-outs are trialling epigenetic-editing approaches that silence toxic gain-of-function alleles without permanent genome cuts, appealing to regulators who prefer reversible interventions.

Metabolic and autoimmune pipelines further diversify revenue sources. Epigenetic risk scores for non-alcoholic steatohepatitis are under validation in North American and Japanese cohorts. In cardiovascular research, integrated methylation plus SNP panels exceed 80% diagnostic accuracy for coronary artery disease, suggesting new clinical-laboratory revenue streams. Collectively, the data signal that oncology will remain a revenue anchor, but non-oncology trajectories will contribute a growing slice of the Epigenetics market size from 2026 onward.

By Technology: DNA Methylation Leads as RNA Innovation Gains Momentum

DNA methylation analysis captured 47.85% of the epigenetics market size in 2025, thanks to decades-long clinical familiarity and newly approved blood tests. Oxford Nanopore’s firmware update now calls 4mC modifications in bacterial pathogens, broadening infectious-disease applications. Histone-modification assays and chromatin-conformation technologies such as Hi-C are carving specialized niches in developmental biology and immuno-oncology drug discovery.

Non-coding RNA platforms, particularly long-read isoform sequencing, are on a 18.76% CAGR arc through 2031. Full-length transcript detection reveals alternative splicing events tied to tumor evasiveness and neurodegeneration. Single-cell joint profiling of chromatin accessibility plus transcriptome deepens understanding of lineage decisions during induced pluripotent stem-cell therapies. As analytical pipelines mature, microRNA-based liquid biopsies are expected to enter regulatory pathways, aggregating incremental value to the Epigenetics market.

Geography Analysis

North America retained 42.95% of the Epigenetics market share in 2025, thanks to FDA clearances for methylation-informed diagnostics and NIH funding that subsidizes multi-omics population studies. Venture investors pumped unprecedented capital into platform start-ups, exemplified by Tune Therapeutics’ USD 175 million raise, securing rapid clinical translation tracks for hepatitis B epigenome-silencing therapies. Academic clusters in Boston, San Francisco, and Durham incubate cross-disciplinary talent pools that sustain regional dominance.

Asia Pacific is forecast to grow at 16.62% CAGR through 2031 as aging demographics elevate cancer incidence and governments underwrite precision-oncology test reimbursements. China anchors regional sequencing capacity with industrial-scale nanopore facilities, while Japan’s national whole-genome program stimulates secondary epigenome analysis demand. Start-ups in Singapore and India are launching culturally tailored prostate-cancer methylation panels that align with local screening norms. Such initiatives expand the Epigenetics market penetration into previously underserved populations.

Europe exhibits balanced expansion. GDPR-compliant data federations delay cross-border joint analyses, yet the European Health Data Space regulation is harmonizing consent clauses, thereby unlocking consortium trials that integrate epigenomic endpoints. The United Kingdom’s GBP 250 million bilateral project with Oxford Nanopore to profile 50,000 biobank epigenomes exemplifies public-private investment intensity. Germany and France sustain pharmaceutical research into LSD1 and EZH2 inhibitors, amplifying regional Epigenetics market engagement despite reimbursement heterogeneity across member states.

Competitive Landscape

The epigenetics market features moderate fragmentation in which top sequencing vendors coexist with rapidly capitalized start-ups that specialize in editing or AI analytics. Illumina reinforced platform stickiness by embedding real-time 5-base methylation detection on NextSeq and NovaSeq systems. Thermo Fisher’s partnership on the myeloMATCH trial aligns NGS hardware with regulatory-grade companion diagnostics, potentially swaying hospital procurement preferences.

Emerging players such as Tune Therapeutics and nChroma Bio deploy compact lipid-nanoparticle delivery systems that deposit transient epigenetic editors targeting hepatitis pathogens. Oxford Nanopore consolidates its unique value proposition around direct detection of modified bases and ultra-long reads, penetrating both clinical and field-deployable settings. Meanwhile, QIAGEN leverages a consumables-heavy revenue mix that finances acquisitions in digital PCR and methylation-specific assay kits. Competitive intensity is migrating toward software ecosystems and proprietary algorithms, where barriers to entry arise from access to high-quality training datasets rather than from instrument patents alone.

Start-ups that secure exclusive clinical-grade datasets through hospital alliances are positioned to command data-network effects similar to those observed in radiology AI. Strategic collaborations, such as Novo Nordisk’s engagement with Omega Therapeutics to co-develop obesity-targeted epigenomic controllers, illustrate how large-cap pharma validates specialized epigenetics technology while accelerating go-to-market pathways. Consequently, sustained innovation across wet-lab and dry-lab arenas defines future Epigenetics market leadership.

Epigenetics Industry Leaders

Thermo Fisher Scientific

Agilent Technologies

F. Hoffmann-La Roche Ltd

PerkinElmer Inc.

QIAGEN N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Illumina released 5-base methylation analysis kits enabling concurrent genetic and epigenetic variant calls, with broad commercial rollout slated for 2026.

- January 2025: Tune Therapeutics raised USD 175 million to progress TUNE-401 for chronic hepatitis B epigenome silencing.

- January 2025: Chroma Medicine and Nvelop Therapeutics merged to form nChroma Bio, securing USD 75 million to advance CRMA-1001 for viral hepatitis.

- November 2024: Illumina expanded its TruSight Oncology 500 assay for faster, deeper variant detection in solid tumors.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the epigenetics market as every commercial product or service, including instrument platforms, reagents and kits, bioinformatics tools, dedicated consumables, and laboratory services, used to detect, map, or modulate heritable changes in gene expression that occur without altering the DNA sequence. Value is captured at the manufacturer invoice level and, as per Mordor Intelligence, is reported in USD across 17 nations.

Scope exclusion: research-only sequencing systems sold for non-epigenomic assays and agriculture-specific epigenome tools remain outside the scope.

Segmentation Overview

- By Product

- Instruments

- Reagents & Kits

- Bioinformatics Tools & Services

- Consumables & Accessories

- By Application

- Oncology

- Neurology & CNS Disorders

- Metabolic Diseases

- Autoimmune Diseases

- Cardiovascular Diseases

- Infectious Diseases

- Others

- By Technology

- DNA Methylation Analysis

- Histone Modification (Acetylation, Methylation, Phosphorylation)

- Non-coding RNA Analysis

- Chromatin Accessibility & Conformation

- Other Technologies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held in-depth interviews with epigenetic instrument engineers, reagent procurement heads, hospital molecular pathologists, and Asia-Pacific CRO managers. These conversations validated volume assumptions, uncovered unreported kit pricing shifts, and highlighted region-specific reimbursement hurdles that secondary sources overlook.

Desk Research

We began by consolidating time-series data on cancer incidence, single-cell sequencing uptake, grant disbursements, and reagent ASPs from sources such as NIH SEER, Global Cancer Observatory, ClinicalTrials.gov, IHEC dashboards, and WIPO patent trends. Corporate filings, FDA 510(k) archives, and peer-reviewed journals then helped us profile price movements and technology inflection points.

Paid databases (D&B Hoovers for revenue splits, Questel for patent counts, Dow Jones Factiva for deal flow) supplied structured inputs that anchored regional baselines. This list is illustrative; many other public and subscription feeds were referenced for cross-checks and clarification.

Market-Sizing & Forecasting

We applied a top-down and bottom-up construct. A demand pool built from oncology and rare-disease test volumes, single-cell system installed base, and consumable pull-through rates was reconciled with selective supplier roll-ups and distributor channel checks. Key variables, like global cancer caseload, median sequencing cost per gigabase, federal multi-omics funding, lab automation penetration, and reimbursement coverage ratios, drive the model. A multivariate regression, stress tested through scenario analysis, projects value from 2025 to 2030 while gap-filling rules adjust for missing bottom-up detail.

Data Validation & Update Cycle

Outputs pass two analyst reviews; we've included variance thresholds that trigger recalculation, and anomalies are re-checked with key experts. Reports refresh annually, with interim updates for material events. A final pre-publication pass ensures clients receive the latest view.

Why Mordor's Epigenetics Baseline Numbers Are Widely Trusted

Published estimates vary because firms choose different product baskets, apply divergent ASP curves, and refresh at uneven intervals. Our disciplined scope selection, higher geographic granularity, and annual update cadence narrow these gaps for decision makers.

Key gap drivers include some publishers limiting coverage to research reagents, others applying flat price erosion across regions, or forecasting from historic patent filings without validating current installed bases, which can compress or inflate totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 16.90 B (2025) | Mordor Intelligence | |

| USD 16.69 B (2024) | Global Consultancy A | Does not adjust for oncology kit price compression seen in 2025 |

| USD 2.24 B (2025) | Regional Consultancy B | Focuses only on kits and excludes instruments and services |

| USD 19.55 B (2025) | Trade Journal C | Applies uniform 10% annual ASP decline, inflating early-year value |

These comparisons show that Mordor's balanced variable mix and continual source validation produce a transparent, repeatable baseline that clients can rely on when allocating R&D spend or sizing investments.

Key Questions Answered in the Report

What is the projected value of the Epigenetics market by 2031?

The Epigenetics market is forecast to reach USD 40.92 billion by 2031.

Which application segment is growing fastest in the Epigenetics market?

Neurology and CNS disorders are expanding at a 15.99% CAGR through 2031 due to breakthroughs in epigenetic editing and RNA-based biomarkers.

Why is Asia Pacific’s Epigenetics market expanding rapidly?

Aging populations, rising cancer incidence, and government investments in precision-medicine infrastructure are driving a 16.62% CAGR in Asia Pacific.

What technology currently holds the largest Epigenetics market share?

DNA methylation analysis maintains leadership with 47.85% market share owing to regulatory-approved methylation assays.

What key restraint could slow Epigenetics market adoption?

High capital expenditure for next-generation and single-molecule sequencers remains a critical barrier, especially in emerging markets.

Page last updated on: