Low Noise Amplifier Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

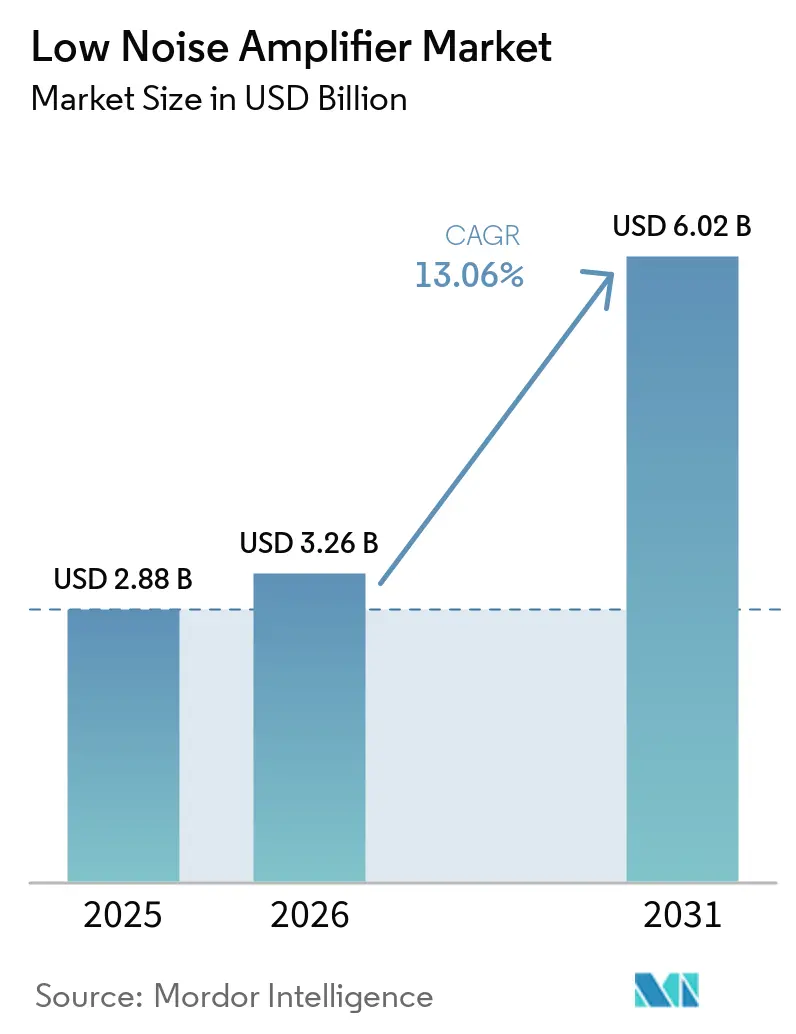

| Market Size (2026) | USD 3.26 Billion |

| Market Size (2031) | USD 6.02 Billion |

| Growth Rate (2026 - 2031) | 13.06% CAGR |

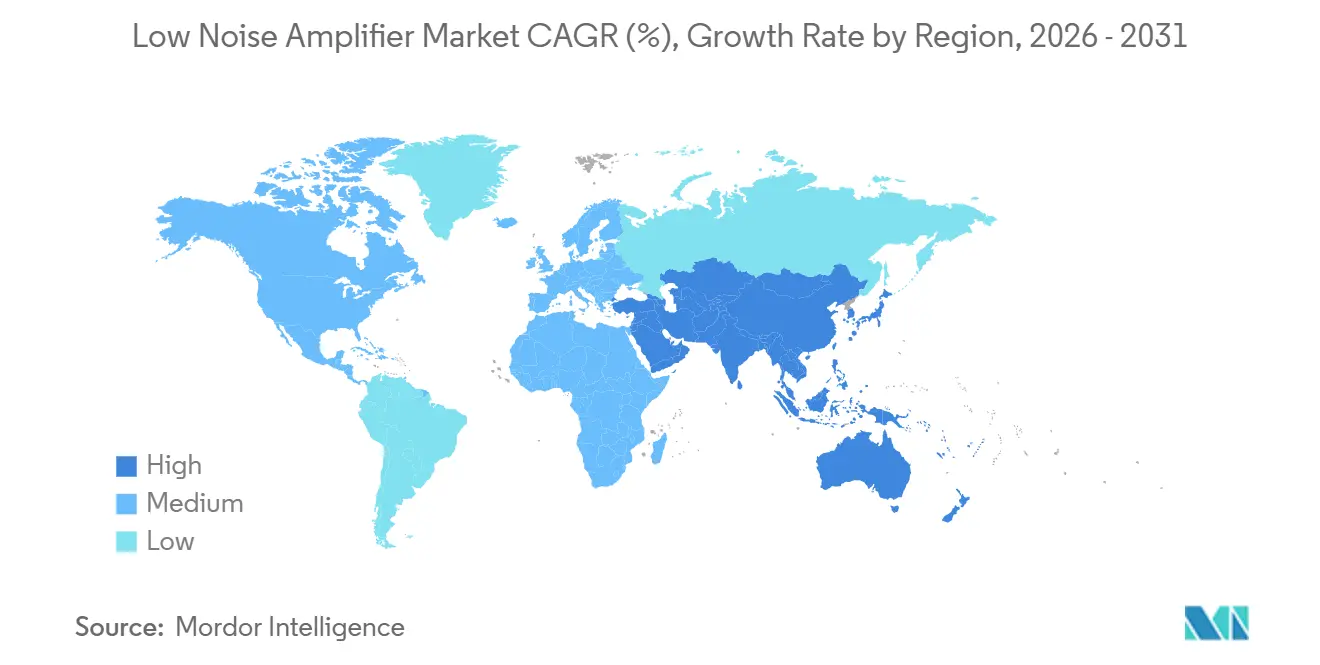

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Low Noise Amplifier Market Analysis by Mordor Intelligence

The Low noise amplifier market size is expected to increase from USD 2.88 billion in 2025 to USD 3.26 billion in 2026 and reach USD 6.02 billion by 2031, growing at a CAGR of 13.06% over 2026-2031. Growth is being shaped by 5G massive-MIMO deployments, LEO satellite buildouts, automotive radar upgrades, and early commercial quantum programs, all of which draw on the same compound-semiconductor base. The low-noise amplifier market is unusual because demand is rising faster than available GaAs and GaN wafer capacity, keeping supply tight even as more applications move to higher-frequency, lower-noise receive chains. 5G radio units in n77 and n79 bands need low noise figures across wider channels, and that raises the LNA count per site well beyond what earlier mobile generations required. Satellite gateways, satellite buses, automotive ADAS platforms, and cryogenic readout chains are also broadening the buyer base, meaning the Low noise amplifier market now serves both large-volume and high-reliability programs simultaneously. Competitive strength, therefore, depends on wafer access, qualification depth, and the ability to support discrete, module, and specialized cryogenic or space-grade designs without losing delivery speed.

Key Report Takeaways

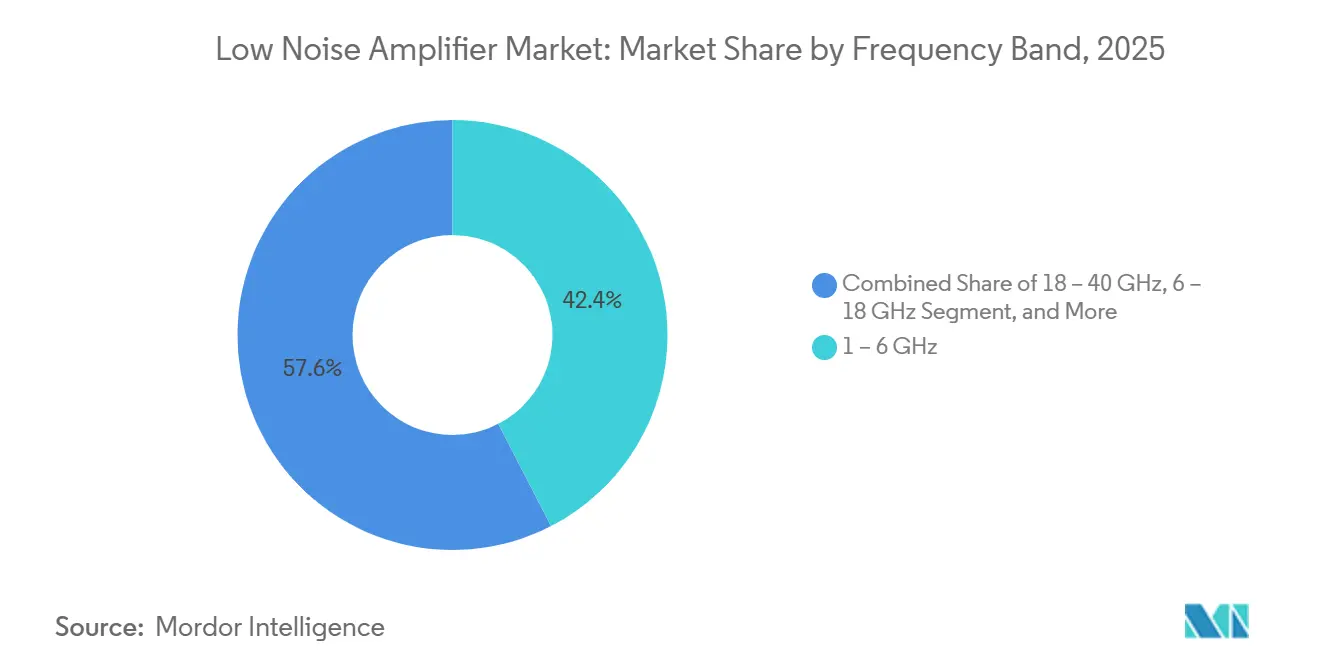

- By frequency band, the 1-6 GHz segment led with a 42.42% share in 2025, while the 18-40 GHz segment is projected to expand at a 16.53% CAGR through 2031.

- By semiconductor technology, GaAs held the largest share at 38.52% in 2025, while GaN is expected to record the fastest growth at 15.65% through 2031.

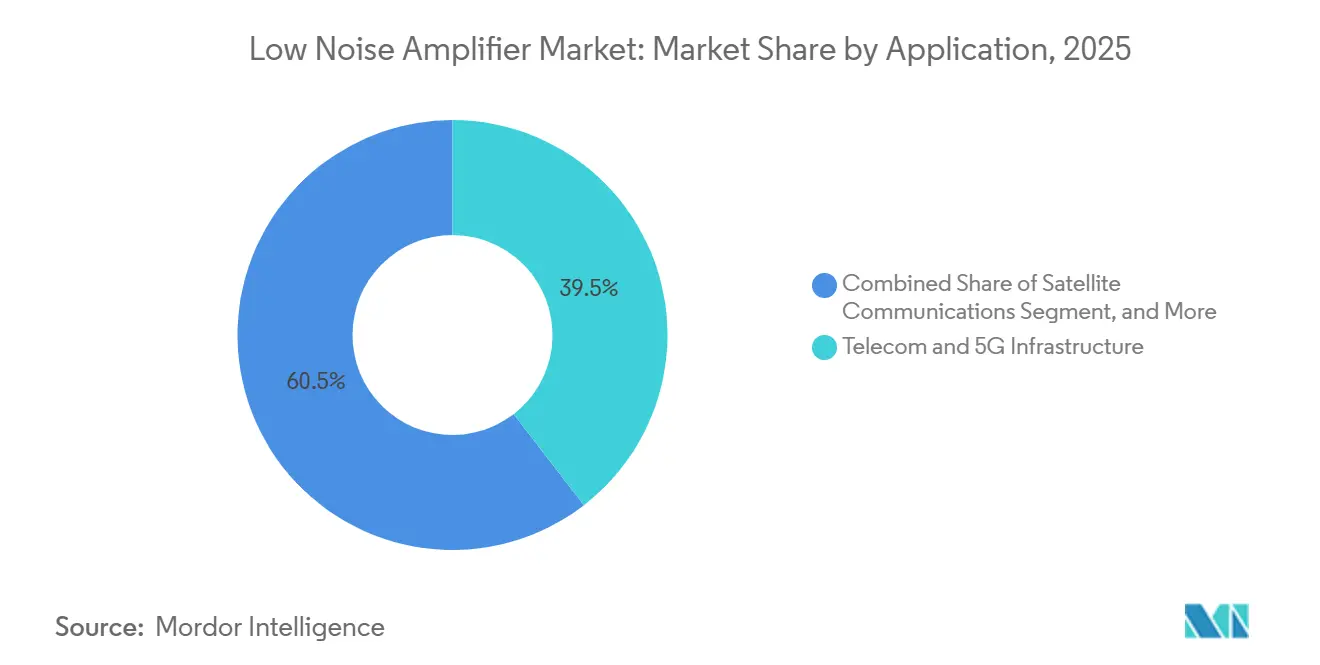

- By application, Telecom and 5G Infrastructure captured 39.53% of Low noise amplifier market size in 2025, while Satellite Communications is projected to advance at a 17.42% CAGR through 2031.

- By architecture and form factor, MMIC LNAs accounted for 41.34% in 2025, while cryogenic LNA architectures are projected to grow at a 15.75% CAGR through 2031.

- By geography, Asia-Pacific held 40.75% of the Low noise amplifier market share in 2025, while the Middle East and Africa are projected to expand at a 17.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Low Noise Amplifier Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G and mm Wave Base-Station Rollout | +3.2% | Global, with early gains in North America, China, and South Korea | Medium term (2-4 years) |

| Proliferation of LEO Satellite Constellations | +2.8% | Global, concentrated in North America and Europe for deployment infrastructure | Long term (≥ 4 years) |

| Automotive Radar Migration to 77-79 GHz ADAS | +2.1% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Growing GNSS and IoT Device Install-Base | +1.9% | Asia-Pacific core, with spillover to Middle East and Africa and South America | Short term (≤ 2 years) |

| Cryogenic LNAs for Quantum-Computing Scale-Up | +1.4% | North America and Europe research hubs | Long term (≥ 4 years) |

| Weather and Earth-Observation Micro-Sat Programs | +1.2% | Global, led by government-backed programs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G and mmWave Base-Station Rollout Accelerates Infrastructure Demand

Commercial 5G deployments in n77 and n79 bands now require receive chains with noise figures below 2.5 dB while sustaining high linearity across 100 MHz-plus channel widths. Massive-MIMO arrays multiply LNA counts per radio unit, and recent 70 nm GaN-on-SiC devices achieve 2.8 dB at 83 GHz, proving GaN’s suitability for mmWave base stations.[1]Fabian Thome et al., “A Wideband E/W-Band Low-Noise Amplifier MMIC,” ieee.org The FCC’s revised out-of-band emission limits in the 24 GHz bands favor architectures with stronger rejection filtering. Simultaneously, envelope-tracking power amplifier techniques are elevating receive-path sensitivity requirements, further boosting demand for Low Noise Amplifiers. That result matters in the Low noise amplifier market because it supports a wider set of material and process choices for dense radio front ends that must balance noise, power, and thermal performance. Tighter filtering requirements in higher-frequency receive paths are also raising front-end sensitivity requirements, making LNA specifications more demanding than the radio standard alone would suggest. Vendors that can pair low noise figures with repeatable production at scale are therefore better placed as the Low noise amplifier market continues to follow 5G radio density rather than just subscriber growth.

LEO Satellite Constellations Drive Multi-Band LNA Innovation

Latency advantages of 6–30 ms, compared with 280 ms for geostationary links, compel satellite operators to specify LNAs that switch rapidly across Ku-, Ka-, and Q-bands. Fraunhofer’s 1.0–1.2 dB noise-figure devices at 54 GHz on the Arctic Weather Satellite highlight demand for ultra-low-noise, radiation-tolerant designs.[2]Qorvo, “Advancing Communication: The Role of LEO Satellites,” qorvo.com 3GPP Release 18 endorsement of non-terrestrial networks mandates dual-mode LNA operation, spurring wideband MMIC innovation. As a result, the Low noise amplifier market is increasingly shaped by commercial space programs that move faster than traditional government procurement cycles and demand both frequency breadth and certified delivery discipline.

Automotive Radar Evolution Beyond 77 GHz Unlocks ADAS Potential

The automotive sector’s shift from 24 GHz to 77-79 GHz has catalyzed new LNA requirements; STMicroelectronics reports escalating shipments of RFCMOS radar chipsets optimized for multi-channel beamforming. imec’s R&D on 140 GHz radar prototypes underscores future gains in resolution, though regulatory harmonization remains pending. Centralized radar-processing zones in software-defined vehicles now require LNAs capable of streaming 1 Gbit/s of data, pushing the Low Noise Amplifier market toward higher-efficiency, high-throughput solutions. That product direction shows how LNA value in vehicles is shifting from a standalone-chip decision to a transceiver-level integration decision, with automotive qualification built in from the start. The qualification path also differs from defense practice because AEC-Q100 standards require a different reliability and validation discipline than MIL-STD-oriented programs. This gives suppliers an edge in the low-noise amplifier market by enabling them to support both automotive-volume economics and stricter high-reliability design methods without sacrificing performance at mmWave frequencies.

Growing GNSS and IoT Device Install-Base

The expanding base of GNSS-enabled receivers and connected endpoints is adding a large-volume and cost-sensitive layer to the Low noise amplifier market, especially in wearables, asset tracking, smart agriculture, and compact navigation devices. These products require LNAs that preserve sensitivity under very low power budgets, pushing CMOS and SiGe designs into roles once dominated by GaAs in narrow receiver chains. Multi-constellation devices are also increasing the need for wideband coverage because many receivers now support GPS, Galileo, BeiDou, and GLONASS in the same product family. JSTAGE and IEICE published a 2025 study on a CMOS single-ended-to-differential LNA for BeiDou applications that delivered 18.2 dB gain and a 2.2 dB noise figure at 2.491 GHz in a 65 nm CMOS process optimized for constrained power use. That type of design progress supports a broader shift in the Low noise amplifier market from narrowband front ends toward wider integrated receive chains with filtering and low-current operation built closer to the silicon. Asia-Pacific remains the center of this pull because consumer electronics production, regional positioning ecosystem development, and demand for BeiDou-compatible devices all reinforce the move toward wideband, low-cost receiver architectures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor Supply-Chain Volatility | -2.3% | Global, concentrated in Asia-Pacific supply base | Short term (≤ 2 years) |

| High R&D Cost of Sub-0.5 dB Noise-Figure Designs | -1.8% | Global, most acute in North America and Europe design centers | Long term (≥ 4 years) |

| Stringent Qualification and Compliance Costs | -1.2% | Aerospace and defense markets globally | Long term (≥ 4 years) |

| Thermal-Management Limits In mm Wave Modules | -0.9% | North America, Europe, and Asia-Pacific mmWave deployment zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Semiconductor Supply-Chain Volatility Constrains Production Capacity

Gallium export curbs reduced China’s outbound volumes to zero in August 2024, throttling GaAs and GaN wafer availability and inflating lead times. SDCE projects that a 67,000-engineer talent deficit in the United States by 2030 could exacerbate fabrication bottlenecks. Although SEMI forecasts USD 137 billion in 300 mm fab equipment spending by 2027, capacity will favor logic and memory, rather than mature RF process nodes critical to the Low Noise Amplifier market.[3] SEMI, “300 mm Fab Equipment Spending Forecast,” semi.orgThat response shows that supply resilience is no longer a background issue in the Low noise amplifier market and has become a central strategic choice for telecom, defense, and satellite-linked production. Until more domestic and diversified compound-semiconductor capacity becomes available, suppliers with captive fabs or privileged foundry access are likely to keep a durable advantage in cost control and schedule reliability.

High R&D Cost of Sub-0.5 dB Noise-Figure Designs

The cost of achieving sub-0.5 dB noise figures at frequencies above 6 GHz remains a major barrier in the Low noise amplifier market, as it requires advanced device structures, multiple tape-outs, and expensive foundry access. These programs often require sub-100 nm pHEMT or other specialized process nodes, and each design iteration can consume substantial sums before a product is ready for qualification or customer sampling. The burden becomes even heavier in cryogenic operation, where designers must control noise temperature, bias behavior, and stability in conditions not well supported by standard commercial design kits. IEEE Microwave and Wireless Technology Letters reported a 2025 cryogenic 40 nm CMOS LNA with a measured minimum noise figure of 0.4 dB at 3.2 GHz and 4K, demonstrating both the technical progress and the custom design discipline required to achieve that level. High entry costs keep the innovation frontier concentrated in the hands of large IDMs and well-funded fabless designers, while smaller suppliers focus more on packaging, catalog depth, and delivery in established bands. This means the Low-noise amplifier market keeps a clear performance hierarchy at the top, even as silicon-based alternatives improve below 6 GHz and in lower-cost applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Frequency Band: Mid-Band Scale Meets mmWave Disruption

The 1-6 GHz segment held 42.42% of the Low noise amplifier market share in 2025, reflecting the very large installed base of cellular networks, Wi-Fi equipment, and GNSS devices that operate across this range. That position is supported by broad deployment rather than by a single end market, which makes this band more resilient when demand softens in one device class but continues in another. The sub-1 GHz band kept steady relevance in LPWAN, smart metering, and other IoT uses where current draw often matters as much as headline gain or noise performance. At the other end, the Low noise amplifier (LNA) market size for the 18-40 GHz segment is projected to expand at a 16.53% CAGR through 2031 as 5G mmWave radios, Ka-band terminals, and higher-resolution automotive radar systems move into volume production. That growth pattern shows a market shifting from its mid-band core into a broader portfolio where millimeter-wave demand is rising faster than the legacy base but still depends on supply discipline and integration know-how.

MDPI Electronics reported a 17-38 GHz cascode LNA on 150 nm GaAs pHEMT that achieved flat 20-23 dB gain and a 1.1-2.1 dB noise figure through simultaneous noise and input matching, which illustrates how the design barriers at these frequencies are being reduced. The 6-18 GHz range remains important for defense radar, microwave backhaul, and satellite intermediate-frequency chains, where procurement is tied more to program timing than consumer replacement cycles. Above 40 GHz, the market is still narrower, but it is being pushed forward by inter-satellite links, specialized instrumentation, and early sub-THz sensing needs. MDPI Aerospace also showed 59-71 GHz GaN/Si HEMT front-end performance with a 4 dB noise figure, which supports near-term migration of more demanding satellite crosslink designs into these upper bands. Across bands, the Low noise amplifier market is also being reshaped by front-end modules that package LNA, filter, and switch functions together, which can reduce the role of pure discrete chips while increasing RF content at the subsystem level.

By Semiconductor Technology: GaAs Leads As GaN Compounds Its Advantage

GaAs held 38.52% of the market in 2025 because its process maturity, stable noise performance, and broad foundry availability continue to make it the default choice for a wide share of receiver designs. That leadership is strongest in GNSS, satellite front ends, and cellular LNAs across 1-18 GHz, where GaAs balances low noise performance with a cost profile the market already understands well. The low-noise amplifier market for GaN is projected to expand at a 15.65% CAGR through 2031, making it the fastest-growing material platform as mmWave, thermal, and power-handling demands rise. This shift is supported by vendor roadmaps to 8-inch wafer production, which could narrow the historical cost gap between GaN and GaAs in the 6-40 GHz range. The low-noise amplifier industry is therefore moving toward a more mixed-material structure, where GaAs maintains its broad base while GaN gains share in applications that require higher breakdown voltage and greater heat tolerance.

Springer Nature’s Arabian Journal for Science and Engineering reviewed tunable LNA design in Ku- and Ka-band SATCOM systems and confirmed that both GaAs and GaN remain strongly positioned in this satellite receiver window. SiGe BiCMOS continues to occupy a useful middle ground because it combines near-GaAs noise performance with the integration density of silicon foundries, which is valuable for automotive radar and multi-band GNSS products. Advanced CMOS nodes are also extending their reach in IoT and consumer designs where power, footprint, and integration often matter more than absolute best noise performance. The United States Department of Commerce support package for MACOM’s USD 345 million expansion plan underlines how policy is now helping shape material competition by backing domestic GaAs and GaN capacity for telecom and defense-linked supply needs. InP still holds a narrow but defensible role above 100 GHz in instrumentation, radio astronomy, and early-stage sensing, which means the Low noise amplifier industry continues to span very different performance and cost tiers under one product category.

By Application: 5G Infrastructure Anchors Demand While Satellite Connectivity Accelerates

Telecom and 5G Infrastructure accounted for 39.53% share of the Low noise amplifier market size in 2025, and that lead came from the dense receiver architecture of massive-MIMO systems rather than from handset demand alone. A sub-6 GHz 5G antenna panel can include 64 to 192 receive chains, and each chain requires a dedicated LNA, creating a component multiplier that earlier wireless generations did not require. Fixed Wireless Access is widening this base further because customer-premises equipment adds another receive-path requirement that behaves more like consumer electronics procurement than defense or carrier core-network procurement. Satellite Communications is projected to advance at a 17.42% CAGR through 2031, driven by new gateway terminal construction, direct-to-device programs, and wider broadband coverage in areas with limited terrestrial infrastructure. The low-noise amplifier market is therefore seeing its two most visible application engines driven by 5G density on the ground and satellite network expansion in orbit and at the edge of coverage.

EECL’s multiband ultra-low-noise amplifiers entered in-orbit service on ESA’s HydroGNSS twin climate satellites after their November 2025 launch, which showed that space-qualified LNA performance can hold under orbital thermal cycling and radiation exposure. Aerospace and Defense remains a high-value application because AESA radar and electronic warfare programs value certified performance and long procurement cycles more than low initial component cost. Automotive and Transportation continues to widen as 77-79 GHz radar moves from premium vehicles into more mainstream platforms, which introduces tighter cost discipline into specifications. IoT and Consumer Devices generate the largest unit volumes, though at lower average selling prices, as CMOS and SiGe designs spread across wearables, trackers, and connected home devices. Industrial and Test and Measurement stays smaller in revenue share, but it supports premium pricing where verified low-noise performance is essential, which keeps margins attractive in parts of the Low noise amplifier industry.

By Architecture / Form Factor: MMIC Integration Leads, Cryogenic Designs Gain Momentum

MMIC LNAs accounted for 41.34% in 2025 because they offer repeatable noise performance, smaller footprints, and cleaner integration into phased arrays and front-end modules than many discrete alternatives. Their lead also reflects how current GaAs pHEMT and related MMIC processes can integrate matching networks and bias circuitry on-chip, reducing board-level loss that would otherwise degrade receive sensitivity. RF front-end modules are changing the split within the Low noise amplifier market because LNA, switch, and filter functions are increasingly being packaged together in consumer and cellular products. That trend shifts value away from standalone parts in some designs, but it also raises the total RF content per device and rewards suppliers that can sell more complete front-end building blocks. Cryogenic LNA architectures are projected to grow at a 15.75% CAGR through 2031 as commercial quantum hardware scales to larger qubit counts and needs more parallel readout channels operating at very low temperatures.

Qorvo launched next-generation Ku-band beamformer ICs in March 2025 with integrated transmit and receive functionality, eliminating the need for certain external LNA stages in SATCOM terminals, demonstrating how system integration is redefining product boundaries. At the same time, the cryogenic side of the Low noise amplifier market remains one of the least mature supply chains because readout performance depends on a narrow set of specialized designs and packaging methods. IEEE cryogenic CMOS work confirms that meaningful noise reduction is possible at low temperatures, but it also highlights the custom biasing and layout effort needed to make these parts commercially useful. Discrete transistor LNAs still hold a place in defense and laboratory equipment where engineers value field-level tuning and replacement flexibility. Even so, the broader Low noise amplifier market keeps moving toward integrated module and chip-level architectures, while cryogenic formats create a specialized growth pocket with much higher design barriers.

Geography Analysis

Asia-Pacific held 40.75% of the Low noise amplifier market share in 2025, and that scale stemmed from its strong position in 5G infrastructure manufacturing, consumer electronics assembly, and compound semiconductor supply chains. China plays a dual role: it is both a large assembler of RF systems that use LNAs and a critical upstream source of gallium-linked material flows, giving the region structural influence over global supply conditions. South Korea and Taiwan remain important as foundry and semiconductor hubs that support fabless LNA vendors serving telecom, GNSS, and consumer applications across several regions. Japan also keeps a meaningful role in GNSS and IoT receiver components, where process maturity and product reliability matter more than headline wafer scale. India is adding another layer of demand as 5G rollout expands and connected device use rises in sectors such as logistics and precision agriculture, which broadens the Low noise amplifier market beyond traditional East Asian manufacturing centers.

North America and Europe together anchor the highest-value, most qualification-intensive portion of demand. In North America, domestic compound-semiconductor capacity is becoming more strategic, and MACOM’s July 2025 transfer of full operational control of its Research Triangle Park GaN-on-SiC wafer facility added Trusted Foundry-aligned capacity to the local base. In Europe, automotive radar remains a major pull factor because Infineon continues to target L2+ to L4 vehicle platforms with its 28 nm CMOS radar MMIC roadmap. European space programs also support procurement for qualified LNA assemblies, and the in-orbit performance of EECL’s amplifiers on ESA HydroGNSS shows how certification and mission heritage still shape supplier access in this part of the Low noise amplifier (LNA) market.

The Middle East and Africa is projected to grow at a 17.98% CAGR through 2031, making it the fastest-growing regional block as mobile broadband investment rises across the Gulf Cooperation Council and several African markets. Gulf operators are adopting 5G with meaningful mmWave exposure in selected deployments, which supports demand for 28 GHz-class receive components at a faster pace than in some European rollouts. Nigeria and South Africa are also expanding LTE and early 5G infrastructure enough to support more direct RF component demand rather than relying only on fully integrated imported systems. South America remains centered on Brazil and Argentina, where cellular upgrades and satellite broadband are joined by GNSS needs in precision agriculture, which gives the Low noise amplifier market a region-specific demand stream outside pure telecom growth.

Competitive Landscape

The Low noise amplifier market remains moderately consolidated because a small group of compound-semiconductor IDMs, including Skyworks Solutions, Qorvo, MACOM, and Analog Devices, operates alongside fabless MMIC designers and specialized cryogenic or space-grade vendors. That structure creates a clear top layer for process capability and customer access, but it does not eliminate competition, as catalog suppliers, module specialists, and application-focused firms still shape many purchasing decisions. Strategy at the leading edge has moved steadily toward vertical control of wafer supply and qualified production, a practical response to tighter compound-semiconductor availability and longer approval cycles. The strongest public example remains MACOM’s USD 345 million, five-year modernization plan, backed by up to USD 70 million in direct CHIPS and Science Act support, which is designed to expand domestic GaAs and GaN capacity and strengthen telecom and defense supply resilience. In the Low noise amplifier market, companies that can secure wafer flow, prove quality systems, and shorten customer qualification cycles hold a more durable position than firms that compete only on list price.

Portfolio expansion is also becoming more important because many buyers prefer signal-chain depth instead of sourcing separate RF functions from multiple vendors. Marki Microwave’s April 2026 acquisition of Saetta Labs added ultra-low phase-noise oscillator technology to a broader platform aimed at defense, test, and satellite communication applications. Qorvo’s 2025 launch of Ku-band beamformer ICs with more integrated transmit and receive capability also showed how system-level design is narrowing the space for external standalone LNAs in some SATCOM platforms. These moves show that competition in the Low noise amplifier market is increasingly tied to how much of the RF path a company can influence, not just how well one discrete amplifier performs in isolation.

The most open opportunities sit at the extremes of performance. Cryogenic readout chains for quantum systems remain a high-barrier and high-margin niche because very few commercial products can meet the thermal and RF limits needed for superconducting qubit platforms, and this keeps the supplier field narrow. Above 40 GHz, especially in V-band inter-satellite links and related front ends, demand is moving faster than qualified supply, which leaves room for companies with advanced process control and certified manufacturing. Firms with ISO 9001 and EN 9100 credentials also enjoy a structural advantage in satellite work because component-level certification has become a purchasing requirement rather than a differentiator. Overall, the Low noise amplifier market rewards a mix of process ownership, integration capability, and application-specific credibility rather than pure scale alone.

Low Noise Amplifier Industry Leaders

Skyworks Solutions Inc.

Infineon Technologies AG

Qorvo Inc.

NXP Semiconductors N.V.

Analog Devices, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: ERZIA completed delivery of 216 New Space RF microwave amplifiers, including LNAs and high-power amplifiers, for an undisclosed LEO satellite constellation program, executing the full program in 24 weeks from purchase order to delivery. The units, certified to ISO 9001 and EN 9100, combined standard COTS and customized modules, demonstrating industrial scalability for commercial New Space missions with concurrent schedule and cost requirements.

- March 2026: Guerrilla RF launched the GRF2118 ultra-low-noise X-Band LNA for satellite communications, defense electronics, and space-borne platforms, achieving a 0.57 dB noise figure in low-bias mode, 3 V and 42 mA, and 0.67 dB in high-bias mode, 5 V and 79 mA, across 6.0-8.5 GHz. The device is fabricated on GaAs pHEMT and packaged in a 2.0 × 2.0 mm QFN-12, requiring no external matching components.

- February 2026: Teledyne HiRel Semiconductors unveiled the TDLNA0840EP, described as the industry’s lowest-power 4 GHz wideband LNA at launch, delivering 29 dB typical gain and 1.5 dB noise figure across 0.3-4.0 GHz from a single 1.5 V supply. The device targets LEO satellite payloads, military communications, and battery-constrained avionics, addressing size, weight, and power reduction requirements in mission-critical RF systems.

- November 2025: EECL’s multiband ultra-low-noise amplifiers entered in-orbit operational service on ESA’s HydroGNSS twin climate satellites following their launch from Vandenberg Space Force Base in November 2025. Six custom multiband LNAs, designed for the GNSS-Reflectometry payload under contract with Surrey Satellite Technology Ltd., amplify weak reflected signals for earth surface hydrology measurements at extremely low noise levels.

Global Low Noise Amplifier Market Report Scope

A Low Noise Amplifier is an electronic amplifier used at the front end of a receiver to boost very weak signals received by an antenna while adding minimal additional noise of its own. It is designed with a very low noise figure (NF) so that the desired signal is amplified above the noise floor without significantly degrading the signal-to-noise ratio (SNR). LNAs are critical in RF and microwave systems such as 5G base stations, satellite communication, radar, GPS, aerospace and defense, and test equipment, where maintaining signal integrity from the antenna is essential. They typically operate across specific frequency bands and are built using semiconductor technologies like GaAs, GaN, SiGe BiCMOS, or CMOS, in forms such as discrete transistors, MMICs, or integrated RF front-end modules.

The Low Noise Amplifier Market Report is Segmented by Frequency Band (Less Than 1 GHz, 1-6 GHz, 6-18 GHz, 18-40 GHz, and Above 40 GHz), Semiconductor Technology (GaAs, GaN, SiGe BiCMOS, CMOS, and InP and More), Application (Telecom and 5G Infrastructure, Satellite Communications, Aerospace and Defense, Automotive and Transportation, IoT and Consumer Devices, and Industrial, Test and Measurement), Architecture / Form Factor (Discrete Transistor LNAs, MMIC LNAs, RF Front-End Modules (with LNA), and Cryogenic / Ultra-low-temp LNAs), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Less than 1 GHz |

| 1 - 6 GHz |

| 6 - 18 GHz |

| 18 - 40 GHz |

| Above 40 GHz |

| GaAs |

| GaN |

| SiGe BiCMOS |

| CMOS |

| InP and Other Semiconductor Technology |

| Telecom and 5G Infrastructure |

| Satellite Communications |

| Aerospace and Defense |

| Automotive and Transportation |

| IoT and Consumer Devices |

| Industrial, Test and Measurement |

| Discrete Transistor LNAs |

| MMIC LNAs |

| RF Front-End Modules (with LNA) |

| Cryogenic / Ultra-low-temp LNAs |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Frequency Band | Less than 1 GHz | ||

| 1 - 6 GHz | |||

| 6 - 18 GHz | |||

| 18 - 40 GHz | |||

| Above 40 GHz | |||

| By Semiconductor Technology | GaAs | ||

| GaN | |||

| SiGe BiCMOS | |||

| CMOS | |||

| InP and Other Semiconductor Technology | |||

| By Application | Telecom and 5G Infrastructure | ||

| Satellite Communications | |||

| Aerospace and Defense | |||

| Automotive and Transportation | |||

| IoT and Consumer Devices | |||

| Industrial, Test and Measurement | |||

| By Architecture / Form Factor | Discrete Transistor LNAs | ||

| MMIC LNAs | |||

| RF Front-End Modules (with LNA) | |||

| Cryogenic / Ultra-low-temp LNAs | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the Low Noise Amplifier market size in 2026 and how large will it be by 2031?

The market reaches USD 3.26 billion in 2026 and is projected to reach USD 6.02 billion by 2031 at a 13.06% CAGR over 2026-2031.

What is driving growth in low noise amplifiers right now?

The main demand drivers are 5G massive-MIMO deployments, LEO satellite constellations, 77-79 GHz automotive radar adoption, and rising GNSS and IoT receiver volumes.

Which frequency band leads demand and which one is growing the fastest?

The 1-6 GHz band led with 42.42% share in 2025 because of cellular, Wi-Fi, and GNSS scale, while the 18-40 GHz band is projected to grow fastest at 16.53% CAGR through 2031.

Which semiconductor technology is gaining share the fastest?

GaN is projected to grow fastest at 15.65% CAGR through 2031 as mmWave, thermal, and power-handling demands rise, even though GaAs still held the largest share at 38.52% in 2025.

Why is supply chain risk so important for this space?

The category depends heavily on compound-semiconductor materials and qualified wafer capacity, so suppliers with captive fabs or secure foundry access are better positioned on cost, lead times, and customer delivery.

Which region leads the market and which region is growing fastest?

Asia-Pacific held the largest share at 40.75% in 2025, supported by manufacturing scale and supply-chain depth, while the Middle East and Africa is projected to grow fastest at 17.98% CAGR through 2031.

Page last updated on: