Noise Monitoring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

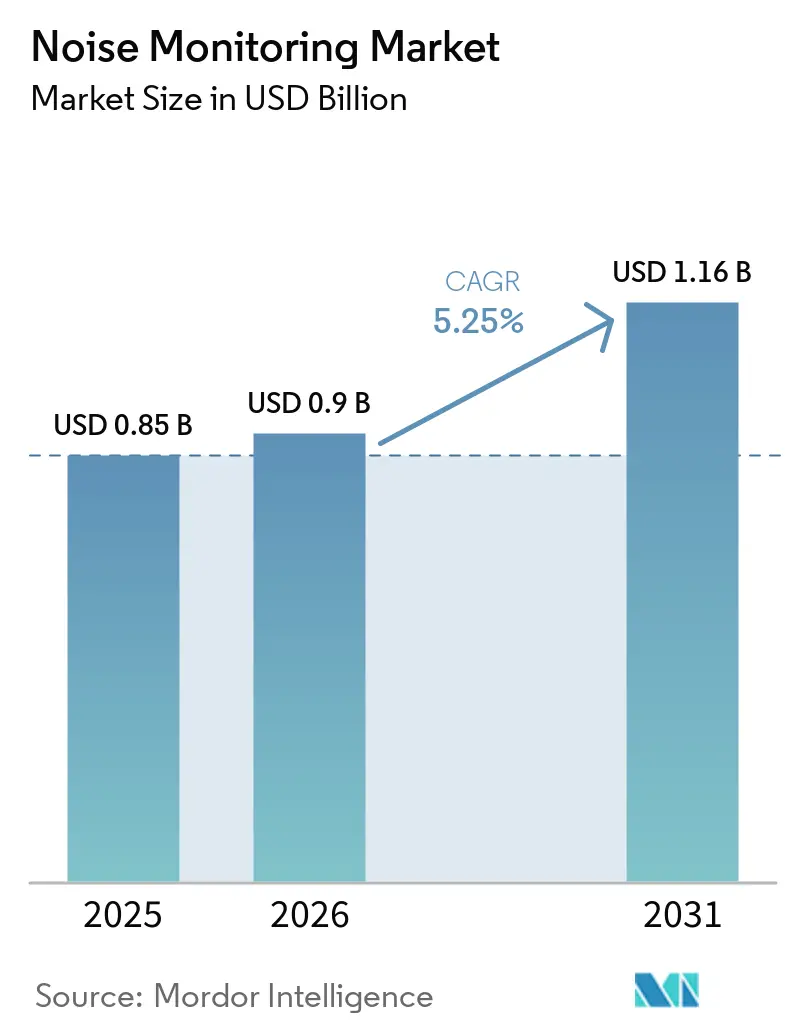

| Market Size (2026) | USD 0.9 Billion |

| Market Size (2031) | USD 1.16 Billion |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

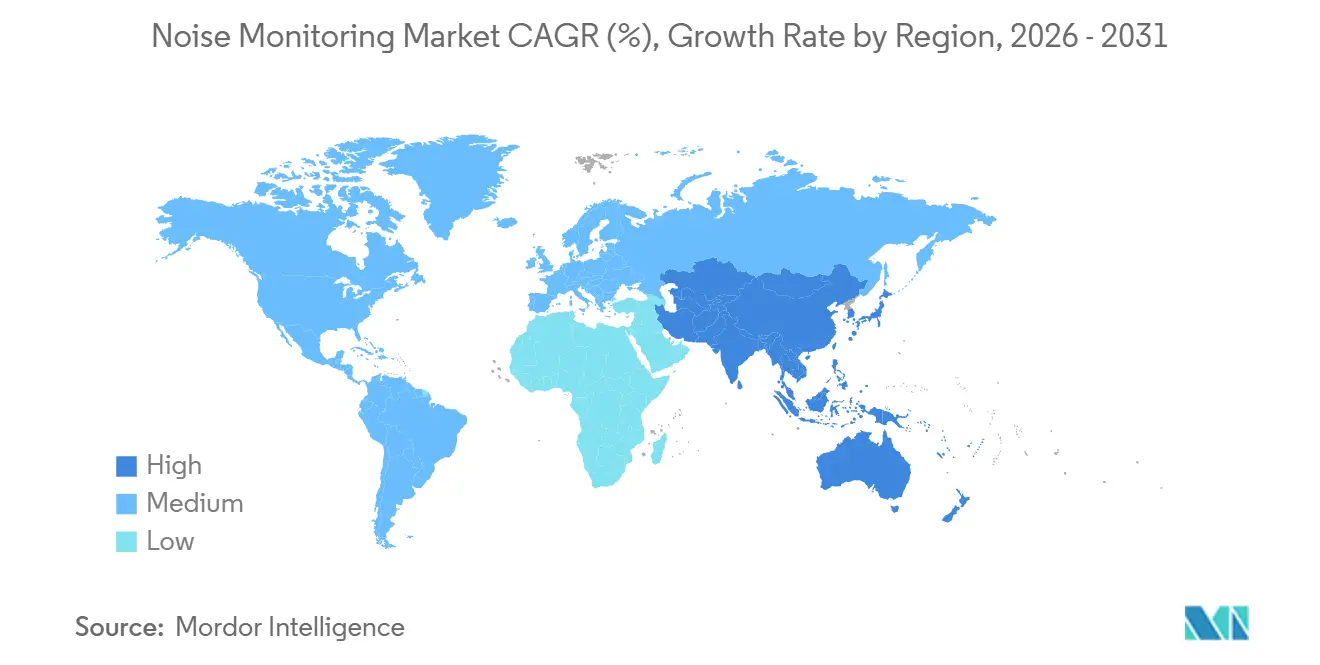

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Noise Monitoring Market Analysis by Mordor Intelligence

The noise monitoring market size is projected to expand from USD 0.85 billion in 2025 and USD 0.90 billion in 2026 to USD 1.16 billion by 2031, registering a 5.25% CAGR between 2026 and 2031. Tightening global regulations, the convergence of smart-city programs with environmental intelligence and rising public health concerns elevate noise measurement from a discretionary study to an essential infrastructure layer. Vendors that combine hardware accuracy with cloud-native analytics, open APIs, and cybersecurity controls are securing multiyear contracts as municipalities move from periodic surveys to continuous feeds. Competitive pressure now revolves around algorithmic differentiation and compliance with updated standards rather than sensor precision alone.

Key Report Takeaways

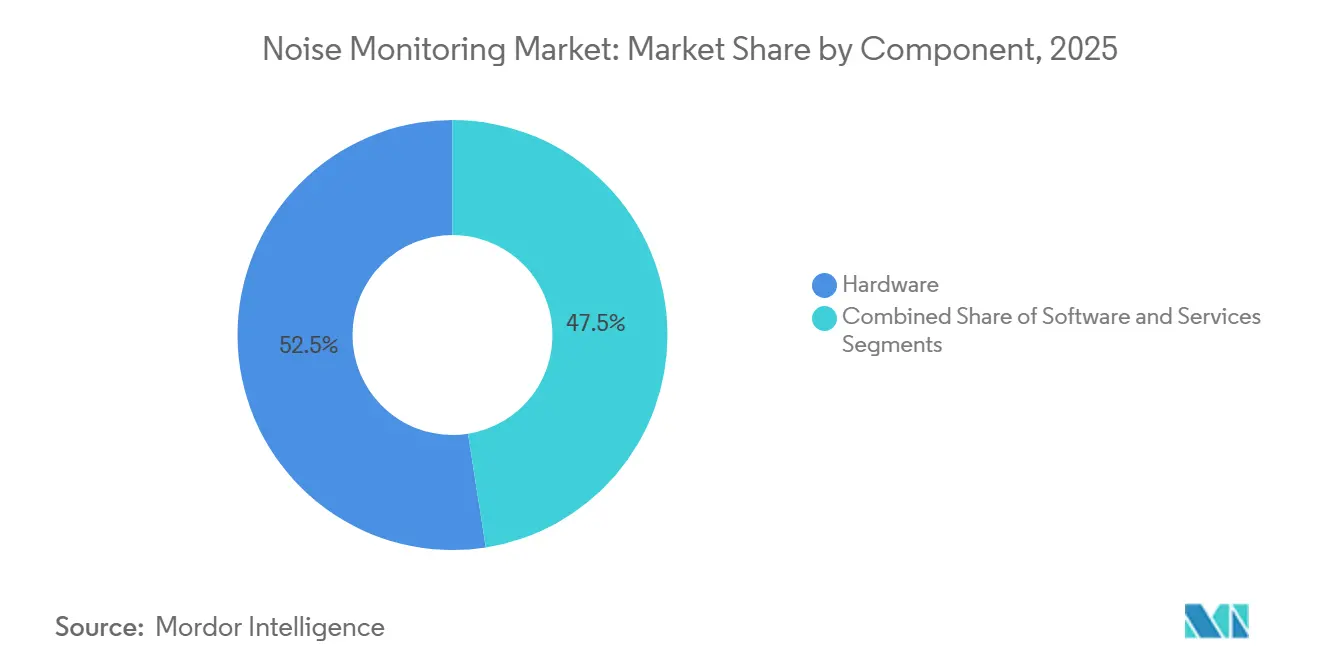

- By component, hardware led with 52.48% noise monitoring market share in 2025, while services are projected to expand at a 6.08% CAGR through 2031.

- By product type, fixed and permanent systems accounted for 37.53% of the noise monitoring market size in 2025; wearable personal dosimeters are forecast to grow at 5.97% CAGR between 2026-2031.

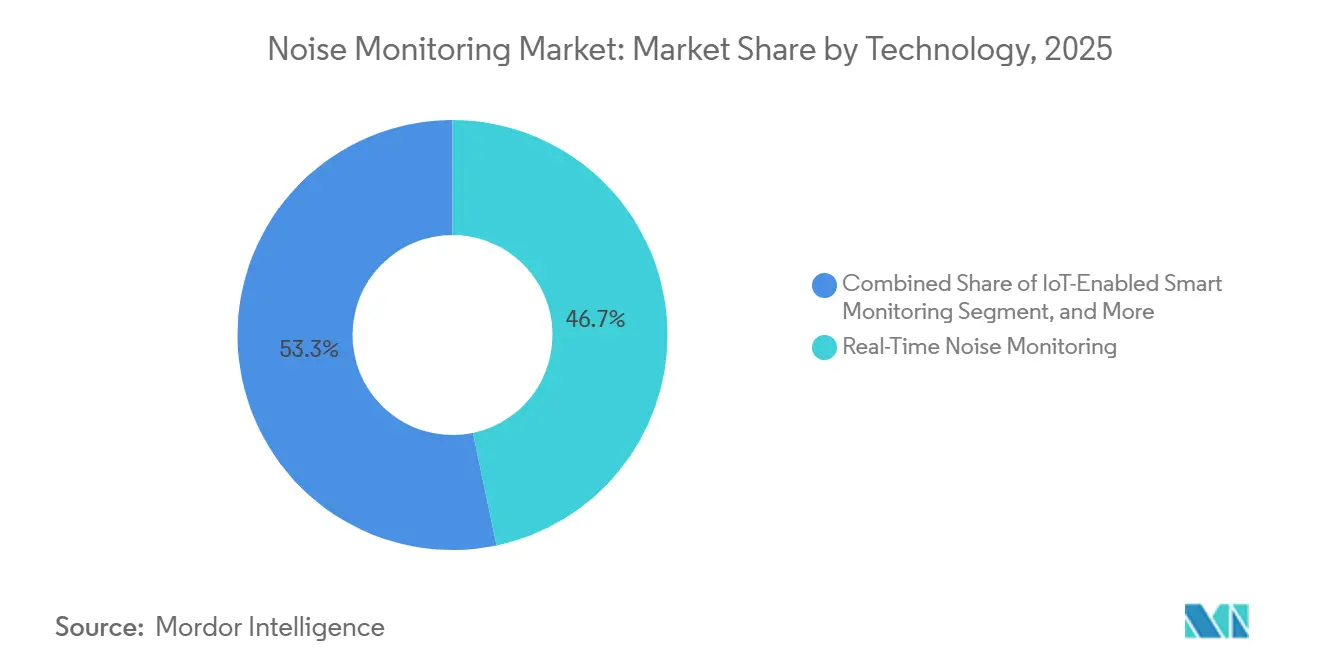

- By technology, real-time monitoring captured 46.72% share of the noise monitoring market size in 2025, and AI-powered predictive analytics is advancing at a 5.91% CAGR to 2031.

- By application, construction and demolition sites held 28.41% revenue share in 2025, whereas entertainment and event venues are set for the fastest 5.88% CAGR through 2031.

- By geography, Europe represented 32.19% revenue share in 2025, and Asia-Pacific is the fastest-growing region with a 6.11% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Noise Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Environmental Noise Regulations | +1.2% | Global, with accelerated enforcement in EU and North America | Medium term (2-4 years) |

| Growth of Smart Cities and Urban Expansion | +1.0% | Asia-Pacific core, spillover to Middle East and Africa | Long term (≥ 4 years) |

| Expansion of Construction and Infrastructure Projects | +0.9% | Global, concentrated in Asia-Pacific and Middle East | Short term (≤ 2 years) |

| Rising Public Awareness of Noise-Related Health Impacts | +0.7% | Europe and North America, emerging in Asia-Pacific urban centers | Medium term (2-4 years) |

| ESG-Linked Acoustic Compliance Mandates | +0.6% | Global, led by Europe and North America | Medium term (2-4 years) |

| Real-Time Noise Data for Dynamic Traffic Management | +0.5% | Europe and Asia-Pacific smart cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter Environmental Noise Regulations

New regulations convert once-optional monitoring into a procurement requirement. Ireland’s draft guidance mandates CNOSSOS-EU methodology, recent input data, and validation of candidate mitigation areas, which expands demand for precision sensors and modeling tools.[1]Environmental Protection Agency (Ireland), “Guidance Note for Strategic Noise Mapping,” epa.ie In the United States, the Federal Highway Administration proposes state-level inventories and model validation within ±3 dB, pushing agencies to deploy continuous networks that feed approved software.[2]Federal Highway Administration, “Procedures for Abatement of Highway Traffic Noise and Construction Noise,” federalregister.gov Municipal rules such as New York City’s 2026 mandate for automated API uploads further accelerate the adoption of cloud-integrated devices. Vendors that certify to IEC 61672-1 and EN ISO 3744:2010 secure preferential status in public tenders.

Growth of Smart Cities and Urban Expansion

Noise sensors are now embedded within multiparameter platforms that also track traffic, air quality, and micro-climate data. Barcelona’s TRAFFIC-NOISE project links acoustic and visual analytics to manage congestion in real time, illustrating how municipalities buy integrated stacks rather than stand-alone meters.[3]Bettair Cities, “TRAFFIC-NOISE Urban Challenge,” bettaircities.com Australia’s OpenAIR program funds networked sensors across 13 local councils, using open protocols to future-proof procurement.[4]NSW Government, “OpenAIR SmartNSW Case Study,” nsw.gov.au Early adopters prefer suppliers offering ready-to-consume APIs and dashboard widgets that fit existing city operating systems, reshaping competition toward software openness.

Expansion of Construction and Infrastructure Projects

Megaprojects in mining, aviation, and transportation fuel short-term surges for rugged, mobile stations. Continuous networks at Kalgoorlie’s Fimiston South and OceanaGold’s Macraes Phase 4 mines demonstrate the shift toward year-round compliance logging even in remote areas. The Federal Aviation Administration funds tools that tie community complaints to measured data, broadening the customer base to airport authorities. Suppliers that bundle solar power, satellite backhaul, and rapid-install tripods gain share in these time-sensitive contracts.

Rising Public Awareness of Noise-Related Health Impacts

Health agencies now cite environmental noise as the second-largest environmental risk after particulate pollution, prompting local governments to map exposure hotspots and designate quiet zones. Scotland’s latest Noise Action Plan embeds equity indicators, prioritizing mitigation in densely populated, lower-income areas. Research initiatives like Fraunhofer’s NoiseProtect allow residents to hear simulated before-and-after soundscapes, boosting community support for investments. This reframes monitoring as a preventive health service, unlocking budgets beyond traditional environmental departments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital and Maintenance Costs | -0.8% | Global, acute in emerging markets and smaller municipalities | Short term (≤ 2 years) |

| Data-Privacy Hurdles in Continuous Monitoring | -0.5% | Europe and North America, driven by GDPR and state privacy laws | Medium term (2-4 years) |

| Interoperability Gaps in Multi-Vendor IoT Networks | -0.4% | Global, concentrated in smart cities with legacy systems | Short term (≤ 2 years) |

| Shortage of Acoustic-Data Analytics Talent | -0.3% | Global, most acute in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital and Maintenance Costs

Class 1 instrumentation, calibrated microphones, and secure cloud subscriptions strain small-city budgets. New York City’s specification for outdoor-rated devices with compliant mounting heights illustrates how premium hardware and periodic recalibration inflate lifecycle cost. Vendors respond with subscription models that convert capex to opex, such as fleet-based pricing in the mining sector. Yet emerging markets still gravitate toward lower-accuracy alternatives, risking data gaps that undermine policy decisions.

Data-Privacy Hurdles in Continuous Monitoring

Edge recording of raw audio collides with strict privacy regimes. Moscow’s “Efir” network awaits legislative approval before full deployment, underscoring how surveillance concerns can stall rollouts. European agencies now emphasize cybersecurity and anonymization in their reporting portals. Suppliers offering on-device classification that transmits only metrics, not waveforms, gain preference in privacy-sensitive bids.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Drives IoT Integration

Services outpace hardware as clients seek turnkey compliance and analytics. Although equipment sales dominated the noise monitoring market in 2025, recurring contracts for calibration, cloud dashboards, and expert interpretation are forecast to grow faster, pushing the overall services share upward. Cirrus Research’s expanded NoiseTools suite exemplifies how software upgrades anchor installed devices and create upsell paths. Government agencies such as the European Environment Agency earmark dedicated budgets for data processing and machine-learning pilots, reinforcing demand for specialized consultancies.

Service providers leverage long-term agreements to bundle hardware leasing, remote diagnostics, and standards compliance audits, buffering revenue against hardware refresh cycles. This migration aligns vendor incentives with customer outcomes, supporting higher margins and stickier relationships across the noise monitoring market.

By Product Type: Wearables Broaden Use Cases

Fixed networks remain indispensable for urban noise maps, yet wearable dosimeters are gaining traction in occupational health programs. Continuous exposure tracking for mobile workers in aviation maintenance, mining haulage, and manufacturing floors accelerates uptake of clip-on sensors that log personal sound dose. New regulations in construction hotspots, such as New York City’s rule for projects within 50 feet of residences, still favour rugged fixed stations with weatherproof microphones.

Wearables complement these networks by confirming individual compliance with exposure limits and delivering real-time vibration or sound feedback to workers. Vendors integrating Bluetooth connectivity and cloud synchronization position wearables as an extension of enterprise safety platforms, smoothing data correlation with area monitors and widening the addressable noise monitoring market.

By Technology: AI-Driven Analytics Gain Momentum

Real-time Leq logging remains the baseline, but AI-powered predictive analytics is the fastest-growing slice. Machine-learning engines that categorize sound events, forecast exceedances, and recommend mitigations reduce analyst workload and speed regulatory reporting. Svantek’s SvanNET AI, already classifying 27 sound categories in production networks, demonstrates a shift toward embedded intelligence.

Regulators themselves now pilot AI for noise-map gap-filling, signalling institutional acceptance. Open-API architectures that stream data into city dashboards heighten the value of cloud-based models, and vendors accumulate proprietary training sets that reinforce competitive moats across the noise monitoring market.

By Application: Entertainment Venues Accelerate Post-Pandemic

Construction sites still dominate deployments, driven by mandatory monitoring during excavation, piling, and demolition. Yet entertainment and event venues are the fastest climbers as nightlife districts reopen under tighter ordinances that limit late-night decibels. Portable stations with 1-minute logging and instant SMS alerts help festival operators prove compliance, expanding procurement beyond traditional engineering firms.

Industrial facilities, transportation corridors, and mining operations maintain sizeable footprints, but venue operators offer new recurring demand tied to seasonal calendars and sponsor branding. This diversifies revenue streams, spreading the noise monitoring market across public and private buyers.

Geography Analysis

Europe anchors global revenues through the Environmental Noise Directive’s five-year reporting cadence and standardized CNOSSOS-EU methodology, which obliges cities to refresh noise maps and public action plans. National initiatives such as Italy’s highway abatement program and Scotland’s designation of quiet areas reinforce pipeline visibility.

Asia-Pacific is the fastest-growing region, buoyed by smart-city pilots and megaprojects. Australia’s OpenAIR network and the University of Technology Sydney’s noise-camera trial exemplify government-funded deployments that blend low-cost sensors with advanced analytics. Rapid urbanization across Southeast Asia and India adds municipal customers focused on affordable, scalable nodes and cloud dashboards.

North America benefits from updated federal guidance and stringent city ordinances. New York City’s continuous monitoring rule spurs immediate procurement, while the Federal Highway Administration’s forthcoming inventory mandate primes state departments for multiyear hardware and software purchases. South America and the Middle East and Africa trail in revenue but show momentum in mining belts and infrastructure corridors where environmental permits hinge on continuous sound logging. Regional diversity in standards drives demand for modular platforms that adapt firmware and reporting templates without wholesale hardware swaps, safeguarding vendor margins within the noise monitoring market.

Competitive Landscape

The market remains moderately fragmented. Legacy acoustic majors such as Acoem and Hottinger Brüel and Kjaer compete with software-first entrants that leverage IoT stacks and machine-learning IP. Cirrus Research expanded its portfolio with dual-level calibrators and Bluetooth-enabled meters, pairing 15-year warranties with lifetime data validation archives to lock in users.

Regulatory shifts, notably the EU’s mandate of EN ISO 3744:2010 from 2025, force all suppliers to update firmware and calibration workflows, levelling the technical field but widening differentiation on cloud security and API quality. Early adopters of edge AI gain data feedback loops that refine classification accuracy, creating barriers for late entrants.

Managed-service models that bundle hardware leasing, private LTE connectivity, and analytics dashboards are emerging as a preferred procurement route for municipalities lacking in-house acousticians. Vendors able to certify cybersecurity, privacy safeguards, and standards compliance at the platform level are winning multi-city frameworks, consolidating share in the evolving noise monitoring market.

Noise Monitoring Industry Leaders

Hottinger Brüel & Kjaer GmbH

Acoem Group

Pulsar Instruments

Soft dB

RION Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: New York City Department of Environmental Protection enforced continuous noise monitoring with automated API uploads for large construction sites, triggering immediate demand for Class 2, weatherproof stations.

- March 2026: Moscow announced citywide rollout of the “Efir” automated road-noise system by 2027 following legislative clearance.

- February 2026: Scottish Government adopted the Round 4 Agglomerations Noise Action Plan, widening CNOSSOS-EU mapping and prioritizing mitigation zones.

- February 2026: U.S. Environmental Protection Agency rescinded the 2009 GHG Endangerment Finding, an indirect driver that could modify future urban noise profiles.

Global Noise Monitoring Market Report Scope

The Noise Monitoring Market Report is Segmented by Component (Hardware, Software, Services), Product Type (Fixed/Permanent, Portable, Wearable Dosimeters, Remote Kiosks, Other), Technology (Real-Time, IoT-Enabled, Cloud-Based Analytics, AI-Powered Predictive Analytics, Other), Application (Construction, Industrial, Transportation, Urban Mapping, Mining and Energy, Entertainment, Other), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| Services |

| Fixed/Permanent Noise Monitoring Systems |

| Portable Noise Monitoring Systems |

| Wearable Personal Noise Dosimeters |

| Remote Noise Monitoring Kiosks |

| Other Product Types |

| Real-Time Noise Monitoring |

| IoT-Enabled Smart Monitoring |

| Cloud-Based Noise Analytics Platforms |

| AI-Powered Predictive Acoustic Analytics |

| Other Technologies |

| Construction and Demolition Sites |

| Industrial Manufacturing Facilities |

| Transportation Hubs and Corridors |

| Urban / Community Noise Mapping |

| Mining and Energy Operations |

| Entertainment and Event Venues |

| Other Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Product Type | Fixed/Permanent Noise Monitoring Systems | ||

| Portable Noise Monitoring Systems | |||

| Wearable Personal Noise Dosimeters | |||

| Remote Noise Monitoring Kiosks | |||

| Other Product Types | |||

| By Technology | Real-Time Noise Monitoring | ||

| IoT-Enabled Smart Monitoring | |||

| Cloud-Based Noise Analytics Platforms | |||

| AI-Powered Predictive Acoustic Analytics | |||

| Other Technologies | |||

| By Application | Construction and Demolition Sites | ||

| Industrial Manufacturing Facilities | |||

| Transportation Hubs and Corridors | |||

| Urban / Community Noise Mapping | |||

| Mining and Energy Operations | |||

| Entertainment and Event Venues | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the noise monitoring market by 2031?

The noise monitoring market is forecast to reach USD 1.16 billion by 2031.

How fast will the Asia-Pacific region grow to 2031?

Asia-Pacific is projected to record a 6.11% CAGR, the fastest regional pace through 2031.

Which component segment is expanding quickest?

Services are growing at 6.08% CAGR as clients outsource calibration, analytics, and compliance reporting.

Why are entertainment venues adopting noise monitoring solutions?

Post-pandemic reopening under stricter municipal ordinances drives venues to deploy real-time systems that verify compliance during events.

How are AI technologies influencing noise monitoring deployments?

AI-powered analytics automate source classification and predictive alerts, reducing manual analysis time and improving regulatory reporting accuracy.

What is the biggest restraint facing new buyers?

High upfront and maintenance costs for Class 1 or Class 2 compliant equipment and ongoing calibration remain the most significant barrier, especially for small municipalities.

Page last updated on: