Active Noise Cancellation Headphones Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

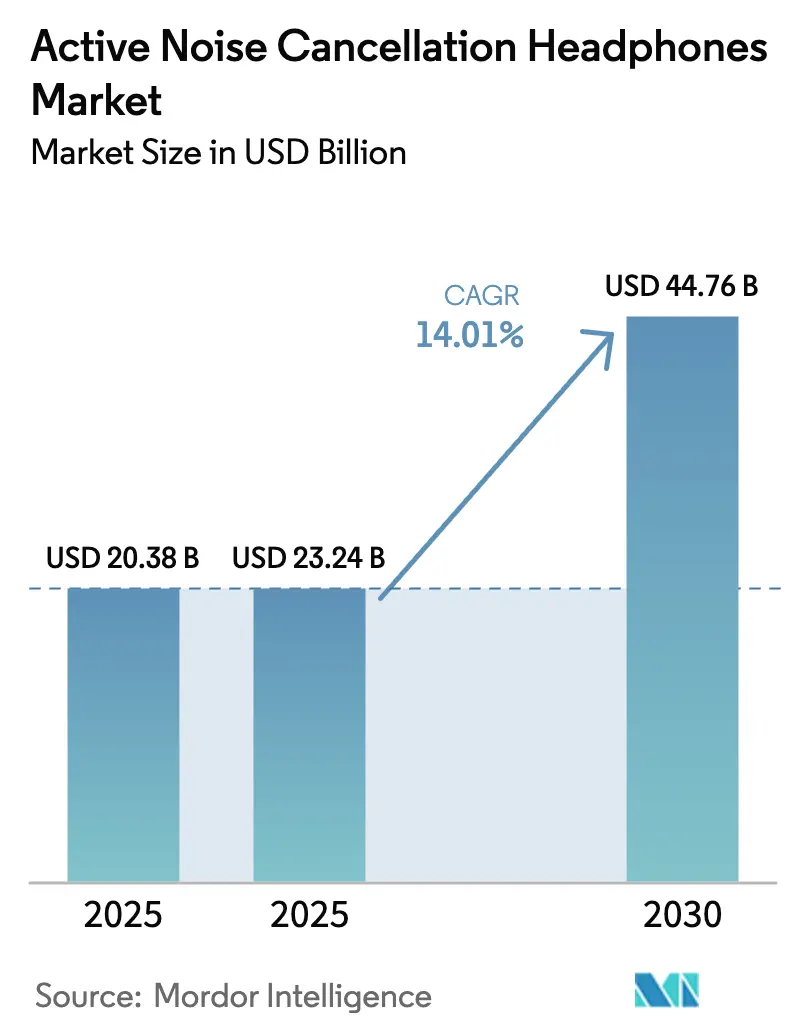

| Market Size (2025) | USD 23.24 Billion |

| Market Size (2030) | USD 44.76 Billion |

| Growth Rate (2025 - 2030) | 14.01% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Active Noise Cancellation Headphones Market Analysis by Mordor Intelligence

The active noise cancellation headphones market size is expected to grow from USD 20.38 billion in 2025 to USD 23.24 billion in 2026 and is forecast to reach USD 44.76 billion by 2031 at a 14.01% CAGR over 2026-2031. Adoption in hybrid workspaces, premium audio ecosystems, and component-level cost engineering all reinforce demand. Online channels now let brands push firmware updates that continually improve attenuation, which in turn extends product life. Spatial-audio catalogs are expanding, prompting users to trade up to devices that render immersive content accurately. Meanwhile, MEMS microphones reduce bill-of-materials costs, enabling sub-USD 100 models to offer features once reserved for flagship tiers. Rare-earth magnet volatility and stricter supply-chain audits have tempered growth but have not derailed long-term momentum in the active noise-cancellation headphones market.

Key Report Takeaways

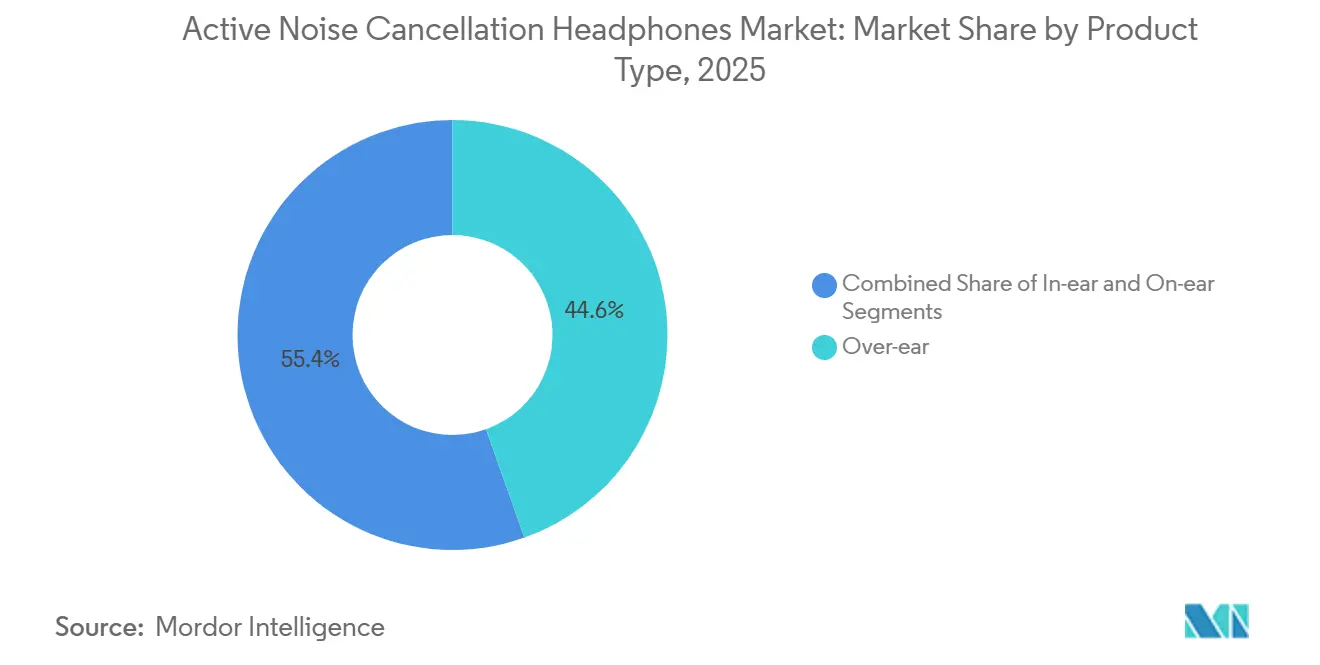

- By product type, over-ear models led with 44.56% of active noise cancellation headphones market share in 2025, while in-ear designs are projected to expand at a 14.68% CAGR through 2031.

- By price range, the premium tier accounted for 53.72% of active noise cancellation headphones market share in 2025, whereas the low-price segment is forecast to grow at a 14.63% CAGR to 2031.

- By distribution channel, online sales accounted for 57.91% of the active noise cancellation headphones market share in 2025 and are advancing at a 14.49% CAGR over 2026-2031.

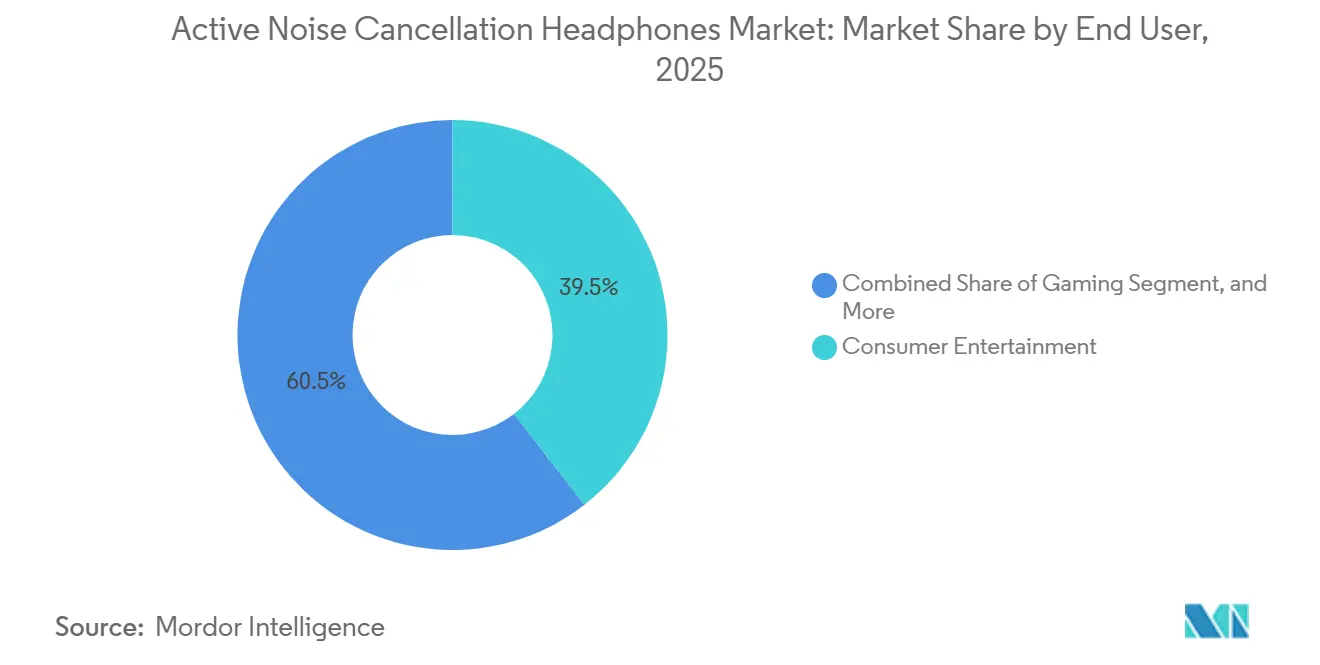

- By end user, consumer entertainment accounted for 39.47% of the active noise cancellation headphones market share in 2025, yet gaming is set for the fastest growth with a 15.11% CAGR through 2031.

- By ANC technology, hybrid architectures commanded 48.83% of the active noise cancellation headphones market share in 2025 and are increasing at a 14.66% CAGR during 2026-2031.

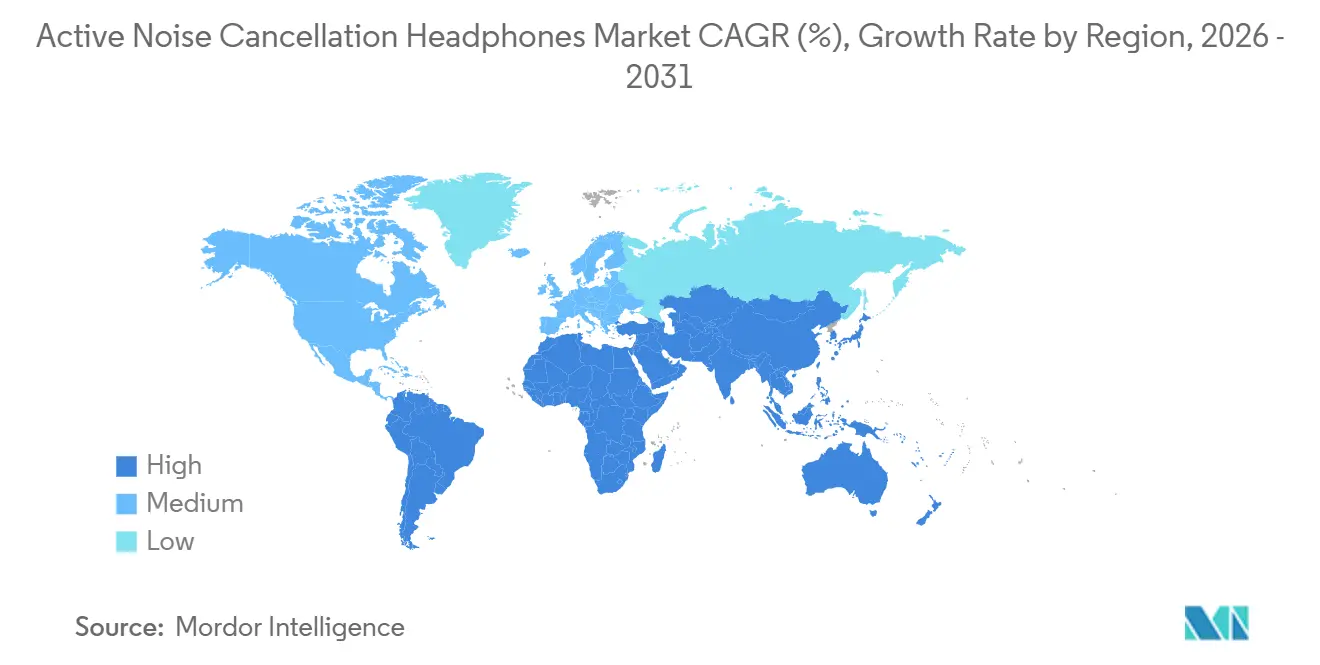

- By geography, Asia-Pacific dominated the active noise cancellation headphones market with 36.29% market share in 2025, while the Middle East is projected to register the highest regional growth at a 15.07% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Active Noise Cancellation Headphones Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of ANC Headphones for Hybrid Work Environments | +3.2% | Global, concentration in North America and Europe | Short term (≤ 2 years) |

| Millennial Preference for Premium Audio Experiences | +2.8% | Global, notably urban centers across three major regions | Medium term (2-4 years) |

| Expansion of Spatial-Audio and Immersive-Media Ecosystems | +2.5% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Advancements in MEMS-Microphone Arrays Lowering BOM Costs | +2.1% | Global, with supply-chain leverage in Asia-Pacific | Long term (≥ 4 years) |

| Airline Cabin Retrofits With Bluetooth Broadcasting Enabling BYOD ANC Listening | +1.8% | Global aviation hubs, early adoption in Europe | Medium term (2-4 years) |

| Workplace Wellbeing Regulations Setting Decibel Exposure Limits for Remote Staff | +1.6% | North America and Europe, regulatory spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of ANC Headphones for Hybrid Work Environments

Hybrid work has recast ANC headsets as essential productivity gear rather than discretionary tech accessories. Frost and Sullivan estimated that 94% of companies will outfit employees with professional-grade headsets by 2026, up 12 percentage points from 2024, as employers link acoustic isolation to measurable gains in task accuracy.[1]Frost and Sullivan, “Professional Headset Deployment Trends,” healthyhearing.com Enterprises now bundle headsets into ergonomic stipends, and call-center operators have raised procurement volumes to protect service-level targets during remote shifts. Jabra and Plantronics together held roughly 75% of the call-center submarket in 2025, leveraging DSP tuned to the 300 Hz-3.4 kHz voice band to maximize intelligibility. Short-cycle firmware updates that refine microphone beamforming strengthen the hardware’s role as living infrastructure rather than fixed assets. Regulators in North America and Europe have begun citing decibel exposure thresholds for home offices, accelerating mandated deployments of ANC headsets across white-collar roles.

Millennial Preference for Premium Audio Experiences

Millennials and Gen Z buyers equate superior sound with self-care, pushing premium models to 53.72% revenue share in 2025. Apple’s USD 249 AirPods Pro 3 pairs heart-rate monitoring with real-time ANC adjustments every 0.1 second, fusing wellness data with immersive listening.[2]Apple Inc., “AirPods Pro 3 Press Release,” apple.com Sony’s USD 449 WH-1000XM6 employs a QN3 processor seven times faster than its predecessor, enabling dynamic attenuation that updates 700 times per second. Bose counters with the QuietComfort Ultra, delivering USB-C lossless playback and 30-hour battery life to placate audiophiles skeptical of Bluetooth compression. Social-media culture amplifies these launches, turning unboxing videos and audio-quality comparisons into proxy status symbols for upwardly mobile consumers. As a result, spending on premium ANC headphones increasingly mirrors the historical upgrades in smartphone camera specifications.

Expansion of Spatial-Audio and Immersive-Media Ecosystems

Spatial audio converts headphones into three-dimensional content gateways that deepen user engagement. Apple’s head-tracking implementation, combined with Dolby Atmos mixes, lets listeners experience positional cues that mimic home-theater setups on the go. Sony’s 360 Reality Audio partners with streaming services such as Tidal to deliver object-based tracks that place instruments around the listener, creating a “virtual venue” effect.[3]Sony Corporation, “WH-1000XM6 Specifications,” sony.com The virtuous cycle is clear: as hardware adoption grows, labels invest more in spatial masters, which, in turn, drive additional hardware upgrades among enthusiasts. Gaming underscores this loop; titles like Valorant encode directional footsteps that reward players using low-latency ANC headsets with faster reaction times. Enterprise simulation platforms for aviation and healthcare are now tapping the same spatial pipelines to create realistic training environments, broadening the commercial canvas.

Advancements in MEMS-Microphone Arrays Lowering BOM Costs

MEMS microphones with on-die analog-to-digital conversion trimmed board space by 40% and pushed signal-to-noise ratios to 72 dB, slashing the cost of hybrid ANC architectures. Infineon’s XENSIV line priced dual-mike solutions below USD 0.50 per sensor by late 2025, making feedforward-plus-feedback designs viable for sub-USD 100 earbuds. ZillTek’s edge-AI firmware now classifies ambient noise, wind, traffic, and voices within the microphone package, enabling earbuds to optimize attenuation without waking the main processor and extending battery life. These efficiencies moved attenuation once locked to USD 300 flagships into budget tiers offered by Anker and Xiaomi, enlarging the addressable consumer base. Component commoditization also reduces entry barriers for new brands, intensifying price competition and quickening product-refresh cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital and DSP Engineering Expertise Requirements | -2.3% | Global, acute in emerging markets and smaller ODMs | Long term (≥ 4 years) |

| Counterfeit and Low-Cost Substitutes Diluting Brand Equity | -1.9% | Global, clustered in Asia-Pacific and South America | Medium term (2-4 years) |

| Rare-Earth Magnet Price Volatility Impacting Driver Costs | -1.5% | Global supply chain, strongest in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Supply Chain ESG Audits Delaying Time-to-Market for ODMs | -1.2% | Global, particularly Asia-Pacific ODMs serving Western brands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and DSP Engineering Expertise Requirements

Cutting-edge ANC demands proprietary silicon, multi-microphone calibration rigs, and vast acoustic datasets, costs that smaller challengers cannot absorb. Sony’s QN3 ASIC took seven years of R&D and access to full-size anechoic chambers to perfect real-time adaptive filtering across 12 microphones. Bose trained neural models on more than 10,000 hours of ambient recordings to cancel impulse sounds like door slams, a multimillion-dollar annotation effort. Manufacturing lines must match microphone tolerances to within fractions of a decibel, pushing capital outlays to USD 5-10 million per facility before the first unit shipment. Smaller original design manufacturers often resort to licensing Qualcomm or MediaTek DSP cores at royalty rates of 5-8%, eroding already-thin margins. Consequently, incumbent leaders fortify their moats while many mid-tier aspirants exit or pivot to lower-spec audio accessories.

Counterfeit and Low-Cost Substitutes Diluting Brand Equity

Counterfeit ANC headphones represented 15-20% of online unit sales in parts of Asia-Pacific and South America during 2025, flooding marketplaces with look-alike AirPods and Sony models that deliver subpar attenuation. Apple responded by spending USD 50 million on blockchain-enabled authentication and customs partnerships in India, Brazil, and Nigeria, yet porous e-commerce channels limit the effectiveness of interdiction efforts. Legitimate low-cost challengers intensify the squeeze; Anker’s USD 99 Liberty 4 NC achieves 98.5% noise reduction, compressing the premium-versus-value performance gap. As fakes and aggressive budget players proliferate, mid-range brands struggle to articulate clear reasons to pay USD 150-USD 250. Over time, the market bifurcates into protected ecosystems offering proprietary perks and cost-optimized alternatives competing strictly on price-per-decibel metrics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Miniaturization Spurs In-Ear Uptake

Over-ear models accounted for 44.56% of the active noise cancellation headphones market share in 2025, reflecting their superior passive isolation, large-format drivers, and 30-hour battery endurance. Corporate studios, broadcasters, and call-center operators continue to specify circumaural headsets because the closed-back design provides a flat frequency response that preserves voice clarity during long sessions. Yet commuters and frequent flyers increasingly see bulky earcups as a trade-off, prompting a pivot toward pocketable alternatives weighing less than 6 g per ear. Samsung’s February 2026 launch of a planar-magnetic true wireless earbud proved that premium fidelity no longer requires over-ear bulk, shrinking the use-case moat that once protected the larger form factor.

In-ear designs, therefore, post the fastest trajectory, advancing at a 14.68% CAGR through 2031 as hybrid dual-mike topologies overcome the limited passive seal of silicone tips. Adaptive algorithms now cancel 30 dB of cabin drone even in compact housings, letting travelers wear the buds continuously without neck strain. On-ear products occupy a narrowing middle ground, favored mainly for fashion aesthetics; absent meaningful acoustic advantages, their volume lags behind the two extremes. Across all categories, MEMS microphone arrays and denser battery chemistries compress size without sacrificing runtime, reshaping buyer expectations for everyday, all-day wearability.

By Price Range: Value Tier Narrows The Feature Gap

The premium tier captured 53.72% of the active noise cancellation headphones market share in 2025, underpinned by the Apple, Sony, and Bose ecosystems that enable seamless device switching, spatial audio, and lossless USB-C playback. Affluent users regard these features as table stakes, sustaining a willingness to pay USD 249-USD 449 for flagships. However, chipset commoditization has armed budget challengers with hybrid ANC, Bluetooth 5.3 LE Audio, and 10-hour single-charge endurance at sub-USD 100 price points, blurring perceived performance boundaries. Mid-priced SKUs, ranging from USD 100 to USD 250, now struggle to find an identity as consumers polarize between top-shelf exclusivity and “good-enough” frugality.

Low-price models are set to expand at a 14.63% CAGR over 2026-2031, propelled by vertically integrated brands that absorb compliance costs and flood online channels during seasonal flash sales. Premium incumbents respond by layering health sensors and proprietary codecs onto hardware to justify margins, yet every budget cycle erodes that moat a little further. Modest-tier vendors increasingly chase niche audiophile tunings, studio-flat signatures, or haptic bass gimmicks to avoid direct price wars with the high-volume value segment. Overall, intensifying bifurcation forces brands to articulate clearer benefits per dollar or risk being squeezed from both ends.

By Distribution Channel: Firmware Economics Favors Online First

Online platforms accounted for 57.91% of the active noise cancellation headphones market in 2025 and are growing at a 14.49% CAGR, as over-the-air updates now extend a product’s functional life well beyond unboxing. Registration inside companion apps enables overnight firmware pushes that sharpen adaptive filters, add spatial-audio profiles, or unlock Bluetooth LE Audio broadcast reception, all without customer intervention. Amazon, JD.com, and Flipkart sweeten conversion with streaming-service bundles and same-day returns, lowering the psychological risk of buying unheard hardware. These perks steadily siphon traffic from brick-and-mortar stores.

Physical retail still earns relevance through tactile trials, side-by-side comparisons, and personalized ear-tip fittings that reassure undecided shoppers. Premium flagships often see their first sales spike after in-store demos that showcase head-tracking or lossless playback under controlled conditions. Specialty chains cultivate authority by curating twenty-plus models on a single wall, but overhead forces a 10-15% markup that price-sensitive buyers avoid once they know their preferred fit. Looking ahead, experiential differentiation, acoustic isolation booths, audiology consultations, and custom engraving must deepen if storefronts expect to defend share against app-centric ecosystems that keep refining value long after checkout.

By End User: Gaming Overtakes Entertainment In Growth Pace

Consumer entertainment remained the largest slice at 39.47% in 2025, driven by commuters, binge-streamers, and air travelers who crave portable silence for music and video. The segment’s unit expansion stays tied to urban transit patterns, airline seat occupancy, and subscription video growth, making it a reliable but maturing base. By contrast, competitive esports and casual gaming collectively post a 15.11% CAGR through 2031, the fastest in the matrix, as directional audio coding inside titles now rewards players who wield sub-20 ms low-latency ANC headsets.

Tournament organizers and streaming influencers legitimize such gear as performance equipment, normalizing USD 200-USD 300 outlays among a Gen Z cohort that already considers keyboards and mice as necessary upgrades. Enterprise and call-center deployments continue to climb in absolute dollars because organizations must protect voice intelligibility and employee well-being across hybrid teams, yet the procurement cadence follows three-to-five-year replacement cycles rather than the annual refresh typical in gaming. Studio and broadcast users buy fewer units, but at the highest ASPs, sustaining boutique engineering lines that prioritize ±1 dB frequency flatness over noise-floor bragging rights. Altogether, these divergent rhythms keep manufacturers juggling contrasting priorities: mass-volume robustness, competitive lag reduction, and reference-grade fidelity.

By ANC Technology: Hybrid Architectures Set The Performance Benchmark

Hybrid ANC systems dominated the active noise cancellation headphones market with 48.83% market share in 2025 and are advancing at a 14.66% CAGR, as dual-mike arrays cancel broadband noise more evenly than single-topology peers. Feedforward sensors outside the earcup target high-pitched chatter while internal feedback microphones correct low-frequency rumble, achieving 30-35 dB attenuation across octave bands. Once exclusive to USD 300 flagships, these configurations now populate USD 60-USD 100 models after MEMS mic prices fell below USD 0.50.

Feedforward-only designs persist in ultra-budget headsets aimed at office cubicles, where rumble is minimal, while feedback-only circuits persist in stage in-ear monitors that must avoid wind artifacts outdoors. Adaptive hybrids employing machine-learning classification push the frontier by predicting transient spikes from door slams or keyboard clicks and inverting them in real time. Regulatory standards effective January 2026 force brands to disclose octave-band performance, nudging laggards toward at least dual-mike implementations to stay competitive. As component sizes shrink further, triplex hybrids with specialized wind or bone-conduction channels are emerging, signaling the next leap in acoustic precision.

Geography Analysis

Asia-Pacific accounted for 36.29% of the active noise cancellation headphones market share in 2025, blending a massive manufacturing base with rising local consumption. Vietnam’s contract assemblers shipped roughly 40% of global unit volume, a scale that helped the country post 8.22% GDP growth in Q3 2025. China’s domestic scene matured as Xiaomi and Anker together held a 30% share in the sub-USD 100 tier, while India’s new Apple stores in Mumbai and Delhi sparked a 22.1% month-on-month spike in premium true wireless demand during late 2025. Emerging Southeast Asian markets such as Indonesia and the Philippines logged 18%-25% annual unit growth, driven by e-commerce flash sales and the adoption of installment payments. These tailwinds keep the region firmly in the lead for both production volumes and first-time buyers.

North America and Europe remain innovation hubs even as growth steadies at roughly 12% CAGR. U.S. employers subsidize headsets to comply with OSHA’s 85 dB exposure limit for remote workers, thereby expanding the market for active noise-cancellation headphones. The European Union’s REACH and RoHS directives add USD 2-5 per unit in compliance costs, favoring vertically integrated brands that can internalize testing overhead. Frankfurt Airport’s January 2026 Auracast pilot demonstrated how public infrastructure rollouts can unlock broadcast audio opportunities that drive headset upgrades among frequent flyers. Together, these policies and pilots turn regulation into a stealth growth lever for premium devices.

The Middle East and Africa delivered the fastest regional outlook at a projected 15.07% CAGR through 2031. The United Arab Emirates and Saudi Arabia treat headphones as luxury fashion, with Bang & Olufsen boutiques offering personalized acoustic fittings in flagship malls. Nigeria leads volume gains as mobile-money platforms let consumers finance USD 99 earbuds in weekly installments, widening access beyond salaried elites. Fragmented Gulf Cooperation Council certification rules can add 3 to 6 months to product launches, disadvantaging smaller newcomers that lack dedicated regulatory teams. South America, anchored by Brazil and Argentina, grows more slowly because currency volatility inflates retail prices by 30%-50% against U.S. equivalents, leaving the region reliant on older inventory clearances.

Competitive Landscape

The sector shows moderate concentration: Apple, Sony, and Bose together accounted for roughly 50%-55% of premium-tier revenue in 2025, underscoring their dominance in the active noise cancellation headphones market. Each giant relies on proprietary silicon, Apple’s H2, Sony’s QN3, Bose’s neural ANC, and tight vertical integration to keep attenuation leadership and ecosystem stickiness. High switching costs allow these brands to maintain USD 249-USD 449 list prices despite aggressive discounting elsewhere. They also push over-the-air firmware that continually refines algorithms, turning hardware into subscription-like assets that remain current for several years.

Below USD 150, fragmentation intensifies as Anker, Xiaomi, and dozens of regional original design manufacturers fight on cost-per-decibel metrics. Qualcomm and MediaTek chipsets now let sub-USD 100 earbuds deliver hybrid ANC and Bluetooth 5.3 LE Audio, eroding the performance gulf once monopolized by flagships. Counterfeit units still account for 15%-20% of online volume in parts of Asia-Pacific and South America, diluting brand equity and forcing incumbents to invest in blockchain tags and in customs seizures. Standards evolution also shifts competitive lines: the Auracast broadcast protocol demonstrated in Frankfurt enables any LE Audio headset to receive public announcements, threatening Apple’s seamless ecosystem moat if the feature scales.

White-space niches are forming around bone-conduction designs for industrial safety, open-ear formats for cyclists, and hybrid ANC plus speech amplification for mild hearing loss. These specialties require fresh ASIC work and new acoustic datasets, so only firms with deep R&D budgets or licensing savvy can scale quickly. Samsung’s planar-magnetic Galaxy Buds 4 Pro shows that Android ecosystem leaders now own premium component supply chains, compressing Sony and Bose’s historical hardware advantage. Meanwhile, transparency-focused challengers like Nothing compete by stripping away proprietary lock-ins and publishing repair manuals, appealing to right-to-repair advocates. All told, incumbents fortify their strongholds through silicon and software, yet price disruptors and niche innovators keep pressure on every tier of the active noise cancellation headphones market.

Active Noise Cancellation Headphones Industry Leaders

Apple Inc.

Bose Corporation

Sony Group Corporation

Samsung Electronics Co., Ltd.

Harman International Industries, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Samsung Electronics launched Galaxy Buds 4 and Galaxy Buds 4 Pro at USD 179 and USD 249, adding planar magnetic tweeters and 24-bit/96-kHz playback in a 5.2-gram form, with the Pro model offering 12 microphones and 30-hour total battery life.

- January 2026: Frankfurt Airport, GN Audio, and Sittig Technologies piloted Auracast broadcast audio for boarding calls, letting Bluetooth LE Audio headsets receive gate announcements without apps.

- November 2025: Sennheiser introduced HDB 630 in India at INR 44,990 (USD 540), bundling 60-hour battery life, hi-res accreditation, and moisture-resistant hybrid ANC tuned for tropical conditions.

- September 2025: Apple debuted AirPods Pro 3 at USD 249 with heart-rate sensors, upgraded ANC, and USB-C charging, powered by the custom H2 chip.

Global Active Noise Cancellation Headphones Market Report Scope

The Active Noise Cancellation Headphones Market Report is Segmented by Product Type (In-ear, On-ear, Over-ear), Price Range (Premium, Moderate, Low), Distribution Channel (Retail, and Online), End User (Consumer Entertainment, Professional/Studio and Broadcasting, Travel and Commuter, Enterprise and Call Center, Gaming), ANC Technology (Feedforward, Feedback, Hybrid), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| In-ear |

| On-ear |

| Over-ear |

| Premium |

| Moderate |

| Low |

| Retail |

| Online |

| Consumer Entertainment |

| Professional / Studio and Broadcasting |

| Travel and Commuter |

| Enterprise and Call Center |

| Gaming |

| Feedforward |

| Feedback |

| Hybrid |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | In-ear | ||

| On-ear | |||

| Over-ear | |||

| By Price Range | Premium | ||

| Moderate | |||

| Low | |||

| By Distribution Channel | Retail | ||

| Online | |||

| By End User | Consumer Entertainment | ||

| Professional / Studio and Broadcasting | |||

| Travel and Commuter | |||

| Enterprise and Call Center | |||

| Gaming | |||

| By ANC Technology | Feedforward | ||

| Feedback | |||

| Hybrid | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will the active noise cancellation headphones market be by 2031?

The market is forecast to reach USD 44.76 billion by 2031, rising from USD 23.24 billion in 2026.

Which region is projected to grow the fastest through 2031?

The Middle East and Africa are expected to post a 15.07% CAGR, outpacing all other regions.

What technology dominates current headset designs?

Hybrid ANC, which blends feedforward and feedback microphones, held 48.83% share in 2025 and is expanding at 14.66% CAGR.

Why are online channels outperforming retail?

Direct-to-consumer sales allow over-the-air firmware updates that continually enhance attenuation, creating long-term stickiness.

Which user segment will expand the quickest?

Gaming headsets are set to grow at a 15.11% CAGR as esports professionalization demands low-latency, high-attenuation gear.

How is rare-earth pricing affecting the supply chain?

A 15% rise in neodymium prices between 2025 and 2026 tightens driver margins, pressuring brands to diversify magnet sourcing.

Page last updated on: