Litigation Funding Investment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

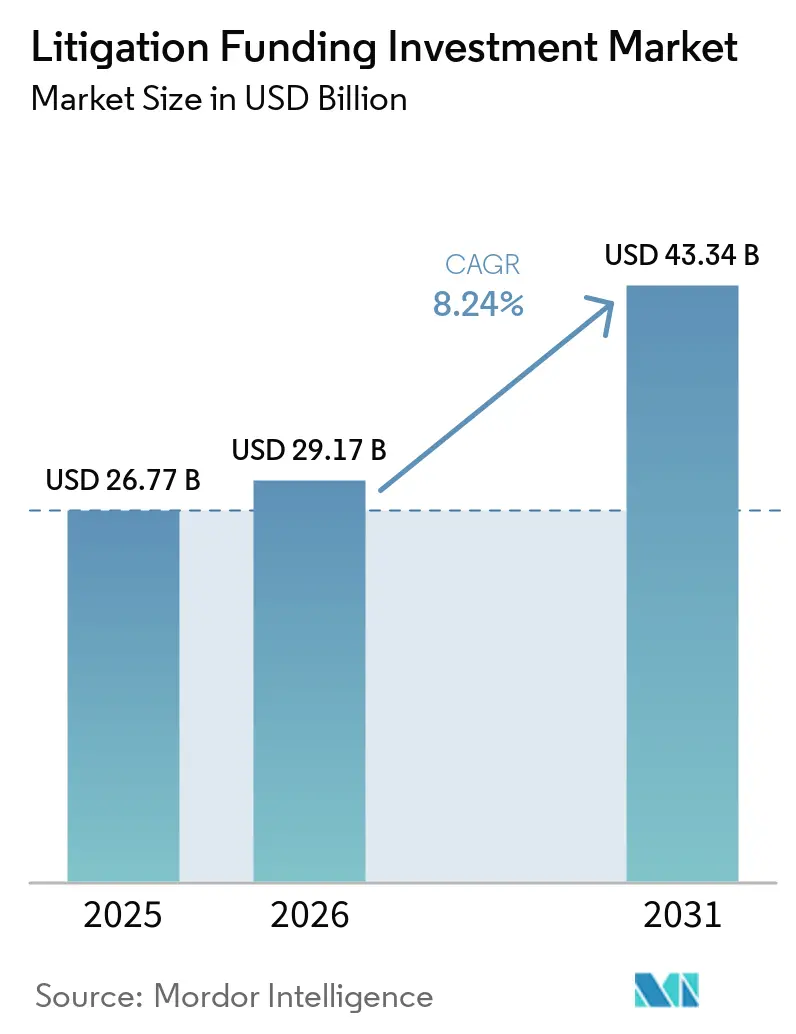

| Market Size (2026) | USD 29.17 Billion |

| Market Size (2031) | USD 43.34 Billion |

| Growth Rate (2026 - 2031) | 8.24% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Litigation Funding Investment Market Analysis by Mordor Intelligence

The Litigation Funding Investment Market size is projected to expand from USD 26.77 billion in 2025 and USD 29.17 billion in 2026 to USD 43.34 billion by 2031, registering a CAGR of 8.24% between 2026 to 2031.

The litigation funding investment market is moving further into mainstream dispute planning as claimants, law firms, and large corporates use outside capital to manage cost, timing, and risk across long-running matters. That shift is supported by broader acceptance of third-party capital in complex disputes and by the growing use of funding across sovereign claims, Fortune 500 portfolios, and multi-year law firm contingency books. Cost pressure also matters because cross-border disputes now require sustained legal budgets that compete directly with internal capital priorities, which makes funding a balance-sheet decision as much as a legal one. The litigation funding investment market is also becoming more institutional as portfolio structures gain share and corporates expand their use of funding for both live claims and monetization of awarded but not yet recovered proceeds. At the same time, competitive intensity is rising as large funders are trying to scale faster, specialist entrants are using technology in underwriting, and regulators across major jurisdictions are tightening disclosure expectations, creating both opportunities and execution risks.

Key Report Takeaways

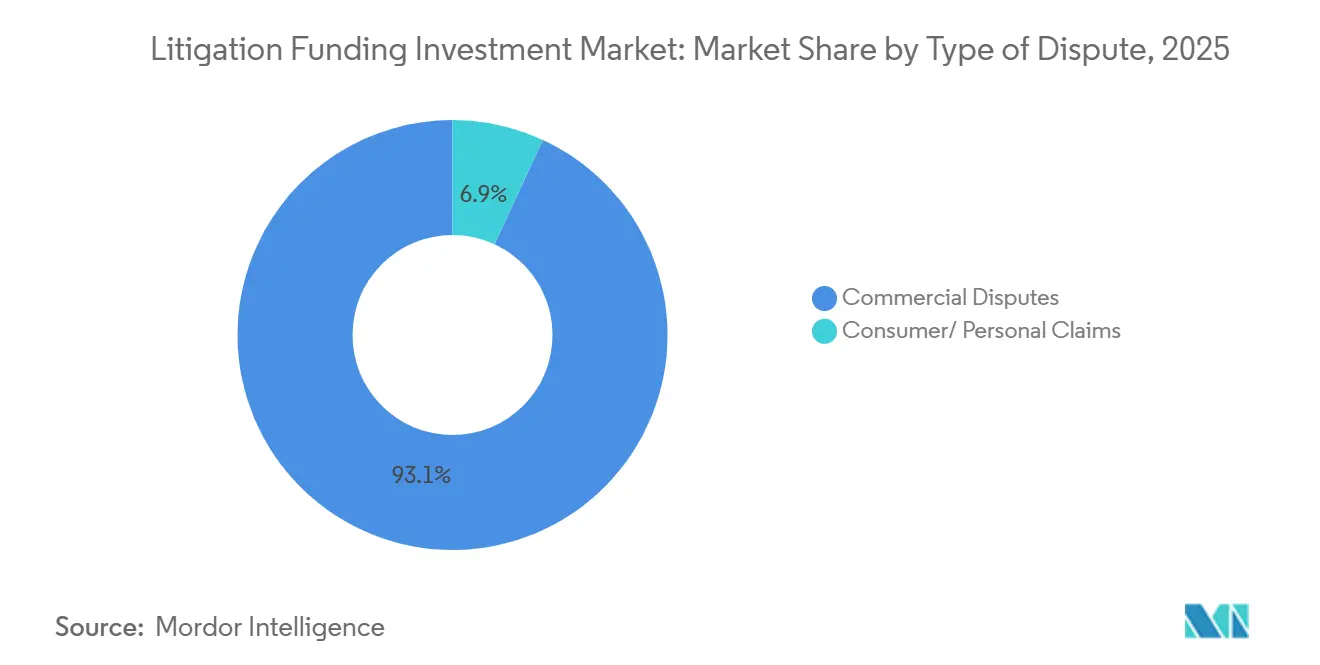

- By type of dispute, commercial disputes led with 93.1% share of the litigation funding investment market in 2025, and the same category is projected to record the fastest growth at 8.5% through 2031.

- By stage of funding, active litigation funding held 62.2% share of the litigation funding investment market in 2025, while post-litigation funding is forecast to expand at 11.9% through 2031.

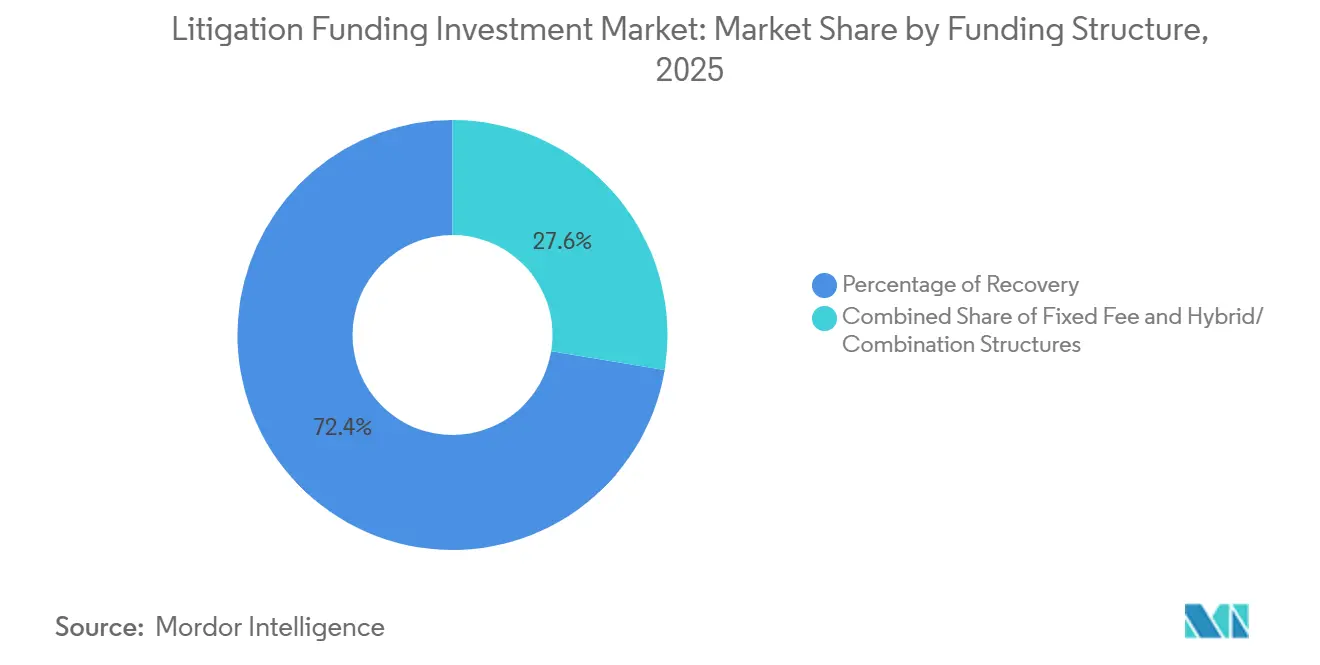

- By funding structure, percentage-of-recovery agreements accounted for 72.4% share of the litigation funding investment market in 2025, while hybrid and combination structures are projected to grow at 10.2% through 2031.

- By client type, law firms held 44.3% share of the litigation funding investment market in 2025, while corporates are expected to post the highest CAGR at 10.4% through 2031.

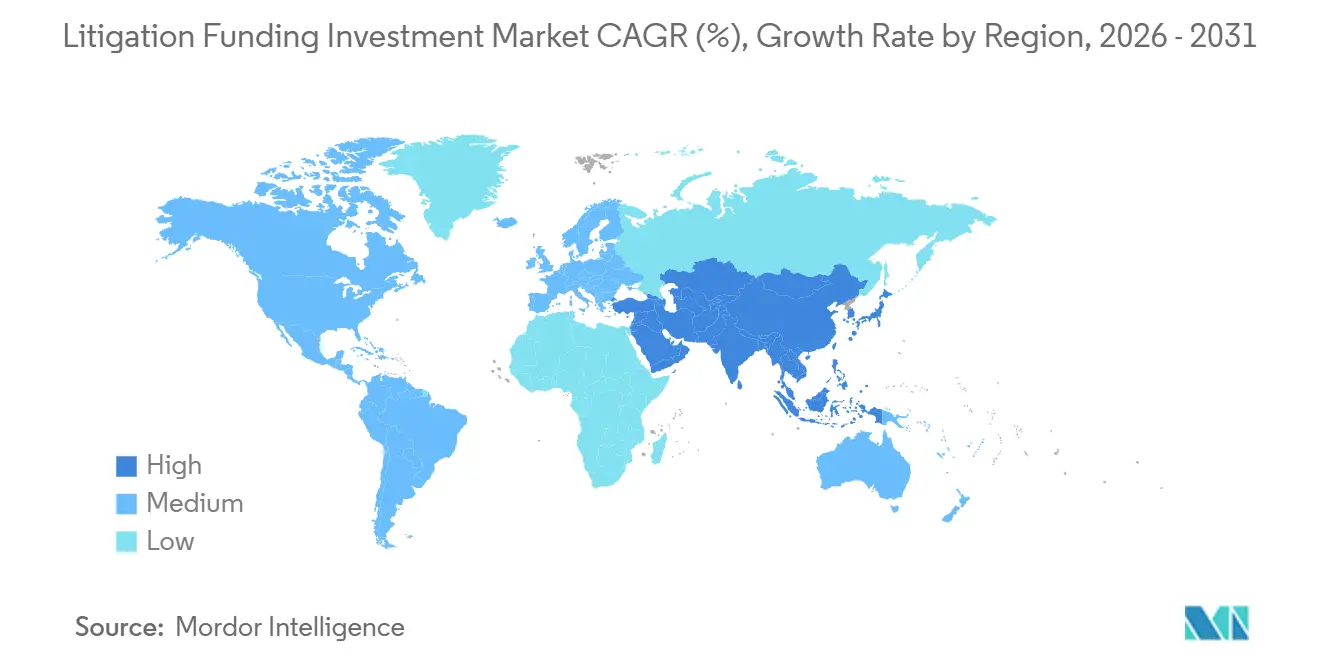

- By geography, North America captured 58.6% share of the litigation funding investment market in 2025, while Asia-Pacific is set to grow the fastest at 11.5% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Litigation Funding Investment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstreaming of Third-Party Risk Transfer in Complex Disputes | +2.1% | Global | Medium term (2–4 years) |

| Rising Legal Costs in Multi-Jurisdiction Matters | +1.8% | North America & Europe | Medium term (2–4 years) |

| Expansion of Portfolio Funding Across Mixed Claim Sets | +1.5% | Global | Short-term (≤ 2 years) |

| AI-Assisted Case Selection and Underwriting Precision | +1.2% | North America, APAC | Long term (≥ 4 years) |

| Growth In Enforcement and Award Monetization | +1.0% | Global, with early gains in MEA & APAC | Medium term (2–4 years) |

| Increasing Adoption of Litigation Funding by Corporations for Balance-Sheet Management | +0.9% | North America, Europe, APAC | Short-term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mainstreaming of Third-Party Risk Transfer in Complex Disputes

The litigation funding investment market is no longer defined solely by distress funding. The product now sits alongside other risk-transfer tools in complex dispute planning, especially in large commercial matters and arbitration. Chambers described the user base as extending well beyond distressed claimants to include sovereign states, Fortune 500 companies, and law firms managing multi-year contingency portfolios. Burford Capital reported USD 872 million in new definitive commitments for FY 2025, up 39% from FY 2024, which shows that wider client acceptance is being matched by larger capital deployment. Chambers also noted that Bench Walk Advisors had committed more than USD 1.3 billion across more than 250 investments by 2026, which shows how quickly second-generation funders can scale once adoption broadens[1]Chambers and Partners, “Litigation Funding 2026 Practice Guide,” Chambers and Partners, chambers.com. As a result, the litigation funding investment market is increasingly treated as part of a financial strategy rather than a last-resort legal product.

Rising Legal Costs in Multi-Jurisdiction Matters

The litigation funding investment market is also benefiting from the simple fact that complex disputes have become expensive to run across multiple jurisdictions. High legal fees, long case durations, and the need for coordinated counsel teams are pushing claimants and law firms to compare litigation spending against other uses of capital. That shift is especially relevant in commercial arbitration and large cross-border claims where legal budgets can remain elevated for years. FORIS AG expanded its fund to cover national and international arbitration proceedings in February 2026, following record ICC pending cases of 1,869 at the end of 2025[2]FORIS AG, “Fonds erweitert Finanzierung Auf Schiedsverfahren,” FORIS AG, foris.com. Rising cost pressure also favors platforms with stronger diligence discipline because more expensive matters leave less room for weak underwriting. In that setting, the litigation funding investment market is rewarding funders that can combine larger balance sheets with sharper case screening.

AI-Assisted Case Selection and Underwriting Precision

The litigation funding investment market is starting to reflect a more technology-led underwriting model. AI tools are being used to shorten case review cycles, improve screening consistency, and widen the range of claims that can be assessed without fully manual processes. That matters because a lower diligence cost can make smaller-ticket disputes more economical for funders than they were in earlier years. The competitive effect is also important because technology-enabled entrants can challenge legacy sourcing models by finding claims earlier and organizing them more efficiently. Over time, the litigation funding investment market may broaden beyond the largest and most obvious claims if AI-assisted review continues to reduce origination friction. This shift is still uneven across regions, but it is becoming part of the operating model rather than a side experiment.

Growth in Enforcement and Award Monetization

The litigation funding investment market is seeing one of its clearest growth lanes in post-award enforcement and judgment monetization. GLS Capital identified appellate monetization as the fastest-growing subcategory in 2026, following a sharp rise in inquiries in 2025. Harbor Litigation Funding also pointed to stronger demand for secondary sale and post-judgment insurance as award creditors seek immediate liquidity rather than waiting through lengthy enforcement processes[3]Harbour Litigation Funding, “The Paper Award Problem, Why Enforcement Risk Now Shapes Arbitration Funding in Claims Against Nation States,” Harbour Litigation Funding, harbourlitigationfunding.com. This demand is stronger where cross-border enforcement is slow or politically difficult, because winning an award does not guarantee quick cash recovery. The litigation funding investment market, therefore, gains not just from more disputes, but from the financing gap that appears after a claimant has already won. That makes monetization products an increasingly durable part of funder portfolios.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Disclosure and Ethics Rules Across Jurisdictions | -1.5% | North America, Europe, APAC | Short term (≤ 2 years) |

| Long Duration and Capital Lock-Up Risk | -1.2% | Global | Medium term (2-4 years) |

| Adverse Costs Exposure and Security for Costs | -0.8% | UK, Australia, EU | Medium term (2-4 years) |

| Concentration In High-Value, Hard-To-Underwrite Cases | -0.5% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Disclosure and Ethics Rules Across Jurisdictions

The litigation funding investment market now faces a more complex compliance burden across major legal systems. The main challenge is not regulation in a single country, but the growing overlap of disclosure, ethics, and discoverability rules across the United States, Europe, and parts of the Asia-Pacific. In the United States, several state-level disclosure rules were already in place through 2025, and federal proposals in early 2026 added more pressure around transparency in large proceedings and aggregated claims. France also formalized third-party funding in group actions in 2025 under a tighter transparency framework, while the United Kingdom Civil Justice Council recommended broad regulatory reform in June 2025. These developments can strengthen legitimacy over time, but in the near term, they raise operating costs and increase execution risk for smaller funders. For the litigation funding investment market, the result is a more uneven compliance environment that favors larger platforms with stronger legal and reporting infrastructure.

Long Duration and Capital Lock-Up Risk

Long case timelines and the resulting capital lock-up also constrain the litigation funding investment market. Litigation assets often take years to resolve, and an appeal, enforcement delay, or adverse interim ruling can materially extend holding periods beyond initial expectations. That makes fundraising harder because investors compare illiquid litigation exposure against alternative products that offer clearer duration and exit profiles. The pressure is already visible in portfolio management behavior, with greater attention to secondary sales, seasoned assets, and structures that reduce exposure to single, long-dated matters. This is one reason portfolio funding continues to gain appeal over isolated single-case deployment, because diversified pools can smooth both timing and valuation outcomes. Even so, the litigation funding investment market remains exposed to duration risk whenever recovery timing slips faster than capital can be recycled.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Dispute: Commercial Dominance Anchors Capital Deployment

Commercial disputes accounted for 93.1% of the litigation funding investment market share in 2025, underscoring the continued concentration of funder capital in claims with higher values and clearer underwriting logic. The segment includes patent litigation, international arbitration, antitrust matters, securities claims, bankruptcy disputes, and other commercial cases that can support deeper diligence and larger commitments. Consumer and personal claims accounted for the remaining 6.9% share, and that part of the market is becoming more structured through pre-settlement and other specialized products. The litigation funding investment market still leans toward commercial matters because institutions prefer claim categories in which damages, duration, and legal posture can be assessed with greater discipline. That concentration also reflects the greater fit between large disputes and the portfolio-return targets sought by funders and their investors.

Commercial disputes are projected to grow at 8.5% through 2031, making the largest dispute class the fastest-expanding in the current forecast window. That outlook reflects demand from high-cost cross-border enforcement, multi-party trade, and tariff disputes, as well as restructuring claims linked to weaker corporate balance sheets. The litigation funding investment industry is therefore still being shaped by commercial complexity rather than by simple case-count growth. Omni Bridgeway said its global enforcement capability remained a core differentiator, supported by 20 locations across 15 countries and a 2.5x MOIC across 60 full and partial completions in FY 2025. The litigation funding investment market benefits from this mix because the same claims that are hardest to prosecute without funding are often the ones that justify institutional capital.

By Stage of Funding: Post-Litigation Monetization Outpaces Case Origination

Active litigation funding accounted for 62.2% of deployments in 2025, maintaining its position as the largest stage in the litigation funding investment market. This position reflects the comfort funders have with live cases where pleadings, evidence, expert work, and early court signals provide a better basis for pricing risk. Pre-litigation structures are also gaining relevance in portfolios, especially where law firms or corporates want committed capital before filing and prefer to build funding into case strategy from the start. Post-litigation funding, however, is the fastest-growing stage, and it is projected to deliver the fastest growth in the litigation funding investment market, with a 11.9% CAGR through 2031. That shift matters because it shows demand is no longer limited to originating new cases, but extends to monetizing won claims that still face delayed cash recovery.

Post-litigation funding is growing from a smaller base, but its role is expanding because the enforcement gap has become more financially visible to claimants and counsel. Award monetization enables a funded party to sell part of a final or near-final award for immediate liquidity, which is useful when debtors resist payment or when enforcement must proceed across borders. Harbor Litigation Funding emphasized that complex sovereign and cross-border enforcement requires asset tracing, interim relief, and the ability to operate across multiple jurisdictions simultaneously. The litigation funding investment market is also seeing a secondary layer emerge, as seasoned legal assets can be sold or refinanced rather than held until final resolution. That makes post-litigation capital important not only for claimants but also for funders seeking more flexible portfolio management.

By Funding Structure: Recovery Percentages Dominate, Hybrids Gain Ground

Percentage-of-recovery agreements held a 72.4% share in 2025, keeping them the standard structure across the litigation funding investment market. The appeal is straightforward because the claimant and funder returns are tied to the same successful outcome, which keeps incentives aligned through trial, settlement, or enforcement. Fixed-fee models remain in use, but they fit better in shorter-duration or lower-risk matters where the provider is acting more like a capital source than a risk partner. Hybrid and combination structures are projected to post the fastest growth in litigation funding investment market size, at a 10.2% CAGR through 2031. That growth suggests clients want more flexible economics that can balance upside sharing with fee certainty or downside protection.

Hybrid structures are becoming more relevant because law firms face higher technology, cybersecurity, and talent costs and need financing that goes beyond paying case expenses. GLS Capital pointed to stronger interest in structures that support law firm operations while preserving alignment on legal outcomes[4]GLS Capital LLC, “2026 Litigation Funding Trends,” GLS Capital, glscap.com. The market is also moving toward larger and more tailored arrangements, with average portfolio transaction size rising to USD 19.6 million in 2025 from USD 16.5 million in 2024, while single-matter deal size fell to USD 4.5 million from USD 6.6 million. The litigation funding investment market is therefore shifting toward more structured deployment, where capital terms are tailored to the portfolio mix, expected duration, and investor return needs. That direction reinforces the advantage of funders who can design products across a wider risk-return spectrum.

By Client Type: Corporate Adoption Shifts Market Center of Gravity

Law firms held a 44.3% share of commitments in 2025, making them the largest client type in the litigation funding investment market. Their lead reflects the capital demands of contingency-fee portfolios and the need to finance large books of ongoing matters without overloading firm balance sheets. Individual plaintiffs, insolvency practitioners, trustees, and other users also remain relevant, especially where distress or restructuring creates a clear need for outside capital. Corporations, however, are projected to post the fastest growth in litigation funding investment market size at a 10.4% CAGR through 2031. That change shows that general counsels and finance leaders are increasingly treating legal claims as deployable assets rather than unavoidable cost centers.

Corporate adoption is rising because portfolio facilities can spread litigation risk across several matters and improve budget visibility. The same logic also supports single-claim monetization, which turns an awarded but not yet collected judgment into earlier liquidity. Big Law's use of litigation funding fell to 24% of total commitments in 2025 from 37% in 2024, but that does not necessarily indicate weaker demand. Instead, the litigation funding investment market is moving toward deeper capital relationships, including structures that sit closer to law firm finance and operating support than traditional one-case funding. The shift in client mix therefore suggests a more mature buyer base that is using funding in more deliberate, financially structured ways.

Geography Analysis

Geography Analysis

North America accounted for 58.6% of the litigation funding market share in 2025, making it the clear regional anchor for global deployment. The United States remains the core of that position because it combines a large commercial litigation base, an established funder ecosystem, and a deeper pool of institutional capital than other regions. The litigation funding investment market in North America also benefits from high-value disputes tied to contracts, intellectual property, bankruptcy, and arbitration, which fit the underwriting models of larger funders. Canada and Mexico add to the regional pipeline through cross-border supply-chain disputes, while South America offers a selective opportunity in complex sovereign and commercial enforcement matters. Burford’s exposure to the YPF arbitration shows how attractive, but also how legally complex, sovereign recovery can be in the Americas.

Europe remains strategically important even though the operating environment is more contested. The United Kingdom continues to act as the leading hub. Still, debates over enforceability following PACCAR and the Civil Justice Council’s reform agenda have made contract design and compliance more important for active funders. Germany’s May 2026 trucks cartel ruling restricted one aggregation model while confirming that bundled claims enforcement through assignment remains lawful, thereby constraining and validating the market at the same time. France also formalized third-party funding in group actions in 2025, followed by an implementing decree in December 2025, which provided the region with greater legal clarity but under tighter transparency requirements. The litigation funding investment market in Europe, therefore, offers scale and sophistication, but it also demands more careful jurisdictional navigation than earlier in the decade.

Asia-Pacific is projected to grow at 11.5% through 2031, making it the fastest-growing litigation funding market among major regions. That pace is tied to stronger arbitration infrastructure, wider regulatory acceptance, and rising corporate demand in markets such as Singapore, Hong Kong, South Korea, Japan, and Australia. The litigation funding investment market in APAC is also supported by the role of Singapore and Hong Kong as enforcement and arbitration hubs where cross-border disputes can be structured more efficiently. Australia remains one of the most mature funding jurisdictions and continues to expand into areas such as construction defects, data breaches, and environmental claims. The Middle East and Africa still sit at an earlier stage. Still, they matter more as enforcement destinations for funded awards, especially where asset tracing and recovery strategy are as important as case origination itself.

Competitive Landscape

The litigation funding investment market is fragmented, with a diverse mix of global litigation finance firms, regional funders, specialist arbitration financiers, and niche providers serving commercial, arbitration, insolvency, and consumer claims. Although established players such as Burford Capital and Omni Bridgeway hold strong positions in high-value commercial disputes, no single firm dominates the overall market. Burford Capital continues to set the benchmark through its extensive portfolio, large capital commitments, and broad geographic presence. Its FY 2025 performance, which included USD 872 million in new definitive commitments and 20% growth in its portfolio base, demonstrates the continued expansion of leading funders within an otherwise fragmented competitive landscape. Meanwhile, Omni Bridgeway remains a key competitor due to its multinational footprint and strong track record across commercial litigation, international arbitration, and enforcement matters. As the market evolves, competitive differentiation is increasingly driven by capital availability, case selection expertise, legal networks, and cross-border execution capabilities rather than by scale alone.

The next layer of competition in the litigation funding investment market is shaped by specialization. Some players focus on appellate monetization and enforcement, while others target intellectual property, antitrust, restructuring, or law firm finance. Longford Capital closed its most recent fund at USD 682 million in February 2026. It said total AUM moved above USD 1.2 billion, reinforcing the strength of focused strategies in IP, antitrust, fiduciary duty, fraud, and commercial contract claims. FORIS AG also widened its scope in February 2026 by expanding funding to large-scale national and international arbitration proceedings, suggesting a more deliberate push toward arbitration as a distinct subcategory.

Competition is also shifting because product design and operating model now matter as much as balance-sheet size. The litigation funding investment market is rewarding firms that can offer portfolio capital, hybrid structures, and enforcement support rather than single-matter funding. Technology-enabled entrants are using AI to shorten screening time and address claims that were previously too small or too expensive to diligence manually. Large funders, meanwhile, are pursuing broader strategic moves that include portfolio scaling, deeper law firm relationships, and more structured solutions for corporates. This leaves the litigation funding investment market with a two-level contest, where scale still matters at the top. Still, operating flexibility matters more in the middle tier and at the edge of newer claim categories.

Litigation Funding Investment Industry Leaders

Burford Capital Limited

Omni Bridgeway Limited

Harbour Litigation Funding Limited

Therium Group Holdings Limited

Litigation Capital Management Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Burford Capital reported USD 872 million in new definitive commitments for FY 2025, a 39% increase over FY 2024, and portfolio base growth of 20% for the year, well ahead of the pace required for its "Burford 2030" goal of doubling the investment portfolio

- February 2026: FORIS AG expanded its fund to finance large-scale national and international arbitration proceedings following record ICC pending cases of 1,869 at the end of 2025. This marks the fund's broadest scope to date and reflects growing funder interest in arbitration as a distinct funding sub-category.

- April 2026: Deminor raised EUR 100 million (approximately USD 108 million) for the continued expansion of its litigation portfolio across Continental Europe, the United Kingdom, and Asia, and became the first litigation funder outside the United States to achieve Certified B Corporation status.

- June 2025: Experity Ventures closed a USD 116 million securitization facility arranged by Triumph Capital Markets and rated by DBRS Morningstar, deploying over USD 500 million to more than 85,000 clients and marking one of the first rated securitizations of consumer litigation finance assets.

Global Litigation Funding Investment Market Report Scope

In the Global Litigation Funding Investment Market, specialized investors inject capital into plaintiffs, law firms, or businesses, aiding them with legal expenses. In return, these investors receive a portion of any future settlement or court award.

Such investments empower parties to pursue legal claims, alleviating them from the complete financial burden of litigation. This market encompasses funding for a range of legal scenarios, including commercial disputes, class actions, arbitration, insolvency cases, and judgment enforcement, spanning various jurisdictions.

The Litigation Funding Investment Report is Segmented by Type of Dispute (Commercial, Consumer/Personal), Stage of Funding (Pre-Litigation, Active, Post-Litigation), Funding Structure (% of Recovery, Fixed Fee, Hybrid/Combination), Client Type (Individuals, Law Firms, Corporates, Insolvency Practitioners, Others), and Geography (North America, South America, Europe, APAC, MEA). Market Forecasts are Provided in Terms of Value (USD).

| Commercial Disputes |

| Consumer / Personal Claims |

| Pre-Litigation Funding |

| Active Litigation Funding |

| Post-Litigation Funding |

| Percentage of Recovery |

| Fixed Fee |

| Hybrid / Combination Structures |

| Individual Plaintiffs |

| Law Firms |

| Corporates |

| Insolvency Practitioners and Trustees |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Turkey |

| Israel | |

| Saudi Arabia | |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type of Dispute | Commercial Disputes | |

| Consumer / Personal Claims | ||

| By Stage of Funding | Pre-Litigation Funding | |

| Active Litigation Funding | ||

| Post-Litigation Funding | ||

| By Funding Structure | Percentage of Recovery | |

| Fixed Fee | ||

| Hybrid / Combination Structures | ||

| By Client Type | Individual Plaintiffs | |

| Law Firms | ||

| Corporates | ||

| Insolvency Practitioners and Trustees | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Turkey | |

| Israel | ||

| Saudi Arabia | ||

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of litigation funding investment in 2026?

The litigation funding investment market is valued at USD 29.2 billion in 2026 and is forecast to reach USD 43.3 billion by 2031 at an 8.2% CAGR.

Which dispute type attracts the most capital?

Commercial disputes are the clear leader, accounting for 93.1% of total value in 2025 because funders favor larger claims with stronger underwriting visibility.

Which funding stage is growing the fastest through 2031?

Post-litigation funding is expanding the fastest at 11.9% CAGR, driven by award monetization and the need to bridge long enforcement timelines.

Why are corporates using litigation funding more often?

Corporations are using it to manage legal spend, smooth budget pressure, and treat claims as financial assets. This client group is projected to grow at 10.4% through 2031.

Which region leads globally, and which region is growing fastest?

North America led with 58.6% share in 2025, while Asia-Pacific is forecast to grow the fastest at 11.5% through 2031.

What is changing competition among funders?

Scale still matters, but competition is also shifting toward portfolio funding, hybrid structures, enforcement capability, and technology-led underwriting models.

Page last updated on: