Financial Services and Investment Intelligence

29th JulyWealth Management Intelligence for the Middle East

4 Min Read

The United States Venture Capital Market Report is Segmented by Industry Type (Fintech, Pharma and Biotech, Consumer Goods, Industrial/Energy, IT/Hardware and Services, Other Industries), Startup Stage (Angel/Seed Investing, Early Stage Investing, Later Stage Investing), Investor Type (Local, International), and Geography (West, Northeast, Midwest, South). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

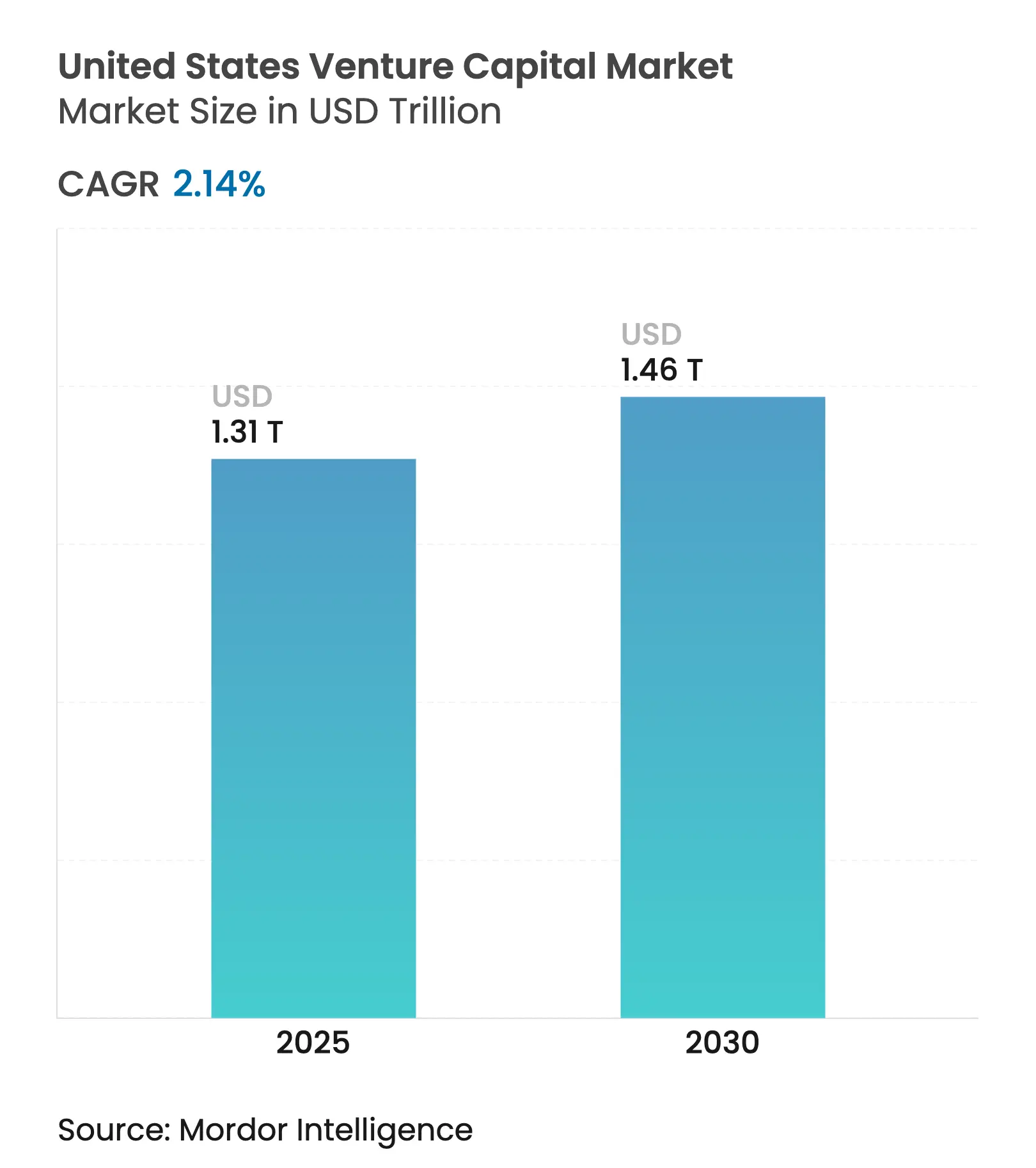

| Market Size (2025) | USD 1.31 Trillion |

| Market Size (2030) | USD 1.46 Trillion |

| Growth Rate (2025 - 2030) | 2.14 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The United States venture capital market size reached USD 1.31 trillion in 2025 and is forecast to reach USD 1.46 trillion by 2030, expanding at a 2.14% CAGR over 2025-2030. This trajectory reflects continued institutional commitment, strong artificial-intelligence deal flow, and resilient early-stage formation even as exit windows remain selective[1]CNBC Staff, “Venture-backed IPOs Rebound in 2024,” CNBC, cnbc.com. Banking and Financial Services retain the largest industry allocation, early-stage rounds dominate capital deployment, and corporate venture investors widen participation as strategic technology priorities intensify. Regional diversification accelerates as founders and funds migrate toward lower-cost ecosystems in the South and Midwest, while secondary-market liquidity products gain relevance for fund managers balancing longer time-to-liquidity cycles. Competitive intensity rises as the United States venture capital market accommodates mega-rounds led by technology giants, micro-fund proliferation, and government funding directed at critical technologies.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Accelerating exit activity via IPO and

SPAC pathways

Accelerating exit activity via IPO and

SPAC pathways

| +0.8% | West & Northeast corridors | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+0.8%

|

Geographic Relevance

:

West & Northeast corridors

|

Impact Timeline

:

Medium term (2-4 years)

|

Record institutional dry-powder

commitments

Record institutional dry-powder

commitments

| +0.6% | National | Long term (≥ 4 years) | |||

Deepening ecosystems beyond Silicon

Valley

Deepening ecosystems beyond Silicon

Valley

| +0.4% | South & Midwest | Long term (≥ 4 years) | |||

Surging demand for AI-native business

models

Surging demand for AI-native business

models

| +1.2% | West & Northeast tech hubs | Short term (≤ 2 years) | |||

Untapped corporate venture participation

in climate-tech

Untapped corporate venture participation

in climate-tech

| +0.5% | Global, with latent potential in industrial, manufacturing, and energy-dense regions | Medium to Long term (2–5 years) | |||

Tokenization of private-market positions

enabling secondary liquidity

Tokenization of private-market positions

enabling secondary liquidity

| +0.3% | Emerging in financial and fintech hubs (e.g., NYC, London, Singapore) | Short to Medium term (1–3 years) | |||

| Source: Mordor Intelligence | ||||||

Accelerating Exit Activity via IPO and SPAC Pathways

Selective reopening of the public markets is lifting sentiment, with venture-backed IPOs delivering average first-day returns of 73% in 2024. Deal quality rather than volume drives value as high-growth software and life sciences firms meet profitability benchmarks required by public investors. SPAC redemptions have normalized, allowing well-structured vehicles to complete mergers on tighter timelines. Large strategic buyers, illustrated by Stripe’s USD 1.1 billion purchase of Bridge Network, continue to provide premium exits for differentiated assets. Secondary-transaction platforms also expand, adding liquidity options for limited partners facing extended fund durations.

Record Institutional Dry-Powder Commitments

Institutional investors maintain substantial uncalled capital commitments despite cyclical market corrections, with United States pension funds and endowments preserving venture capital allocations to capture long-term technology transformation opportunities. Fundraising exhibits pronounced bifurcation, with growth in micro funds (under USD 10 million) now representing over 40% of new closes compared to 25% in 2020, while mega funds (over USD 100 million) constitute 12% of H1 2025 closes. Top-tier firms, including Founders Fund, Lightspeed, Andreessen Horowitz, and Khosla Ventures, continue raising multi-billion dollar funds, though the median time-to-close for United States funds exceeded 15 months, reflecting increased due diligence and selectivity among limited partners[2]PitchBook Analysts, “US VC 2025 Outlook,” PitchBook, pitchbook.com. Approximately a dozen firms raised over half of the venture capital in H1 2025, indicating market concentration that favors established general partners with proven track records and differentiated investment strategies.

Deepening Startup Ecosystems Beyond Silicon Valley

Austin, Miami, and Atlanta have become focal points for venture formation as talent relocates and operating costs remain lower than coastal peers. Federal broadband investments totaling USD 42.5 billion stimulate infrastructure startups, while state-level incentives bolster localized accelerator networks[3]Moss Adams, “Broadband Industry Trends 2023 Update,” Mossadams.com. University commercialization pipelines in the Midwest add engineering talent to deep-tech ventures. As a result, the South’s share of the United States venture capital market is rising alongside a 9.64% CAGR. Investors benefit from reduced competition for deals and proximity to corporate partners in logistics, energy, and advanced manufacturing.

Surging Demand for AI-Native Business Models Across Verticals

Artificial intelligence investment fundamentally reshapes venture capital allocation, with AI funding reaching USD 26.8 billion across 498 deals in 2024 year-to-date, representing a 140% increase in average round size compared to 10% for non-AI ventures. Technology giants, including Microsoft, Amazon, Alphabet, and Nvidia, directly fund capital-intensive generative AI startups with resources traditional venture firms cannot match, exemplified by Amazon's USD 4 billion commitment to Anthropic and Nvidia's USD 100 billion partnership with OpenAI. Late-stage AI companies command approximately 100% valuation premiums at Series C compared to non-AI peers, while AI's share of total fundraising increased from 12% in 2023 to 27% in 2024 year-to-date. Venture capital firms adapt by investing "up the stack" into application-layer startups requiring less capital, utilizing special-purpose vehicles to participate in mega-rounds, and developing sector-specific expertise in healthcare AI, fintech automation, and enterprise productivity tools.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising interest rates lifting cost of

capital

Rising interest rates lifting cost of

capital

| -0.9% | National | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

-0.9%

|

Geographic Relevance

:

National

|

Impact Timeline

:

Medium term (2-4 years)

|

Heightened antitrust scrutiny on

large-tech M&A

Heightened antitrust scrutiny on

large-tech M&A

| -0.5% | National tech sector | Long term (≥ 4 years) | |||

Limited LP risk appetite after 2022–2023

markdown cycle

Limited LP risk appetite after 2022–2023

markdown cycle

| -0.6% | National, most pronounced in traditional LP hubs | Short to Medium term (1–3 years) | |||

State-level ESG disclosure rules adding

compliance drag

State-level ESG disclosure rules adding

compliance drag

| -0.4% | Primarily U.S., with early impacts in states with aggressive ESG mandates | Medium term (2–4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Interest Rates Lifting Cost of Capital

Elevated federal funds rates have reshaped venture capital dynamics by compressing valuation multiples and prolonging fundraising timelines across all stages. Venture debt markets are especially impacted, with lenders tightening underwriting standards, raising interest rates, and demanding greater warrant coverage post-SVB collapse. Early-stage venture debt deals dropped 39% from 2022 to 2023, as capital shifted toward later-stage companies with stronger revenue and investor support. Capital-intensive sectors like climate tech and biotech face greater financing strain due to long development timelines and high infrastructure costs. Bridge financing now commonly includes secured debt, milestone-based tranches, and downside protections. Founders are increasingly forced to accept down rounds or improve operational efficiency to extend their runway.

Heightened Antitrust Scrutiny on Large-Tech M&A

Regulatory scrutiny from the FTC and DOJ has introduced uncertainty around strategic acquisitions by major tech companies, historically a key exit route for venture-backed startups. Agencies are closely examining vertical integration and data concentration, especially in AI-related partnerships between cloud giants and startups[4]CNBC Staff, “Tech M&A Under Scrutiny,” CNBC, cnbc.com. In response, the “Magnificent Seven” tech firms have reduced M&A activity, opting instead for venture-style investments that avoid regulatory thresholds. As a result, alternative exit strategies like SPACs, direct listings, and management buyouts are gaining traction, though they demand greater scale and maturity. Venture firms are adapting by rethinking portfolio strategies and preparing for longer holding periods. Startups are increasingly prioritizing public market readiness to reduce reliance on acquisition-based exits.

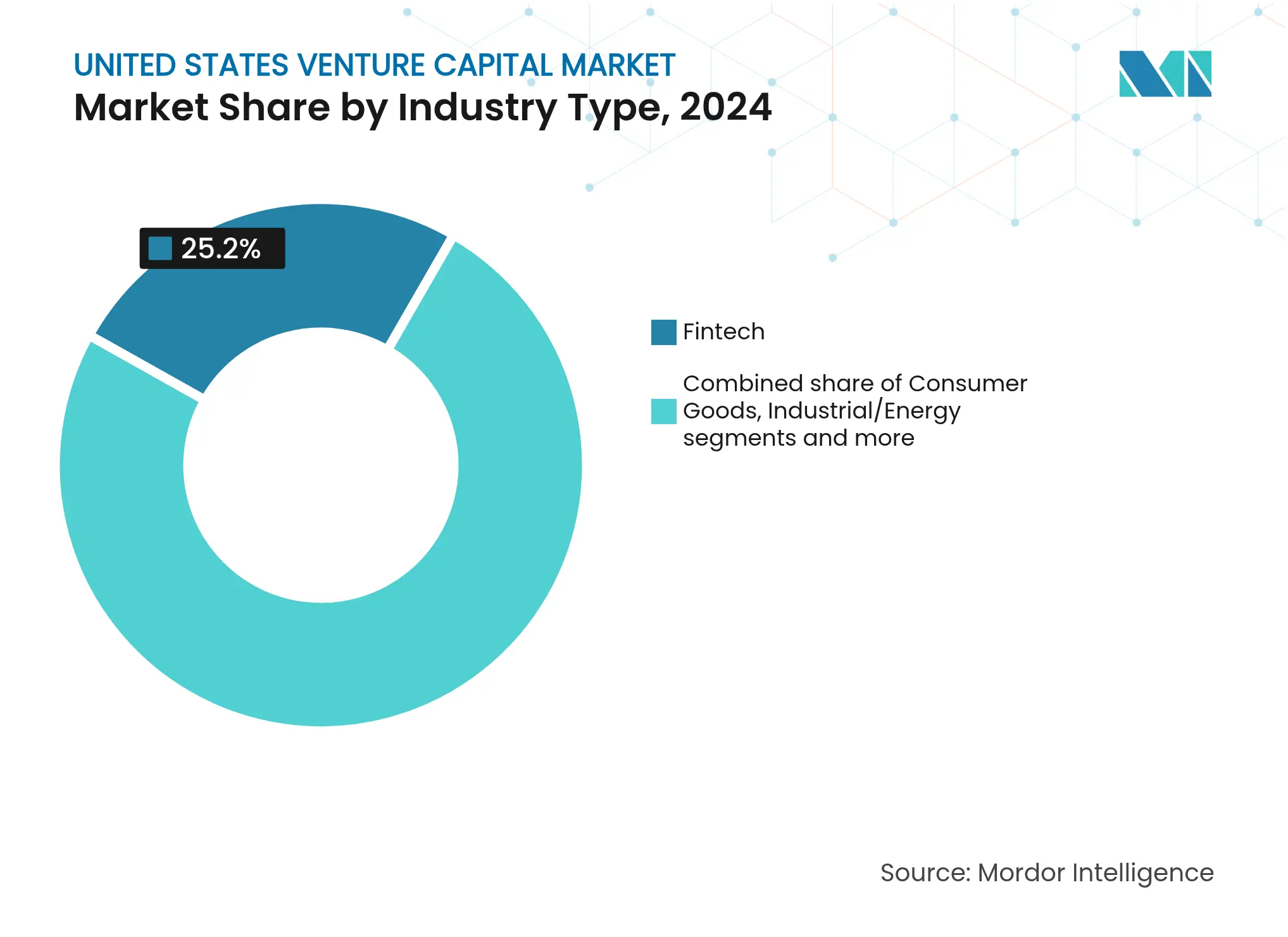

By Industry Type: Fintech Dominance Faces Biotech Acceleration

Fintech maintains its leadership position with 25.2% market share in 2024, driven by embedded finance adoption and regulatory modernization initiatives, including open banking frameworks and digital asset infrastructure development. The sector's maturity enables predictable revenue models through transaction fees and subscription services, attracting institutional investors seeking stable returns amid market volatility. However, Pharma and Biotech emerge as the fastest-growing segment at 12.27% CAGR through 2030, propelled by AI-enabled drug discovery platforms that compress development timelines from 10-15 years to 5-7 years while reducing failure rates through predictive modeling.

Consumer Goods and Industrial/Energy sectors demonstrate steady growth patterns, with Consumer Goods benefiting from direct-to-consumer e-commerce platforms and Industrial/Energy gaining momentum through climate technology investments and infrastructure modernization. IT/Hardware and Services maintains a significant market presence through cloud infrastructure and cybersecurity investments, while Other Industries captures emerging sectors, including space technology and advanced manufacturing. The convergence of AI capabilities across all industry verticals creates cross-sector investment opportunities where traditional boundaries blur, enabling venture firms to develop thematic investment strategies that span multiple industry classifications.

Note: Segment shares of all individual segments available upon report purchase

By Startup Stage: Angel/Seed Investing Stage Captures Dual Leadership

Angel/Seed Investing demonstrates remarkable dual performance, commanding 27.2% market share in 2024 while simultaneously achieving the highest growth rate at 15.72% CAGR through 2030. This phenomenon reflects the democratization of early-stage capital through micro-funds and rolling fund structures that enable smaller investors to participate in venture ecosystems previously dominated by institutional players. The seed stage expansion also benefits from reduced startup costs through cloud infrastructure and open-source software, allowing entrepreneurs to achieve product-market fit with smaller initial capital requirements.

Early Stage Investing maintains substantial market presence through Series A and B rounds, where institutional venture firms establish significant ownership positions before valuation inflation occurs in later stages. Later-stage investing faces headwinds from interest rate sensitivity and extended exit timelines, though growth equity firms continue deploying capital in profitable companies with clear public market trajectories. The stage dynamics reflect a barbell strategy where investors concentrate on very early opportunities with high optionality and later-stage companies with proven business models, while avoiding the middle market where valuations often exceed risk-adjusted return expectations.

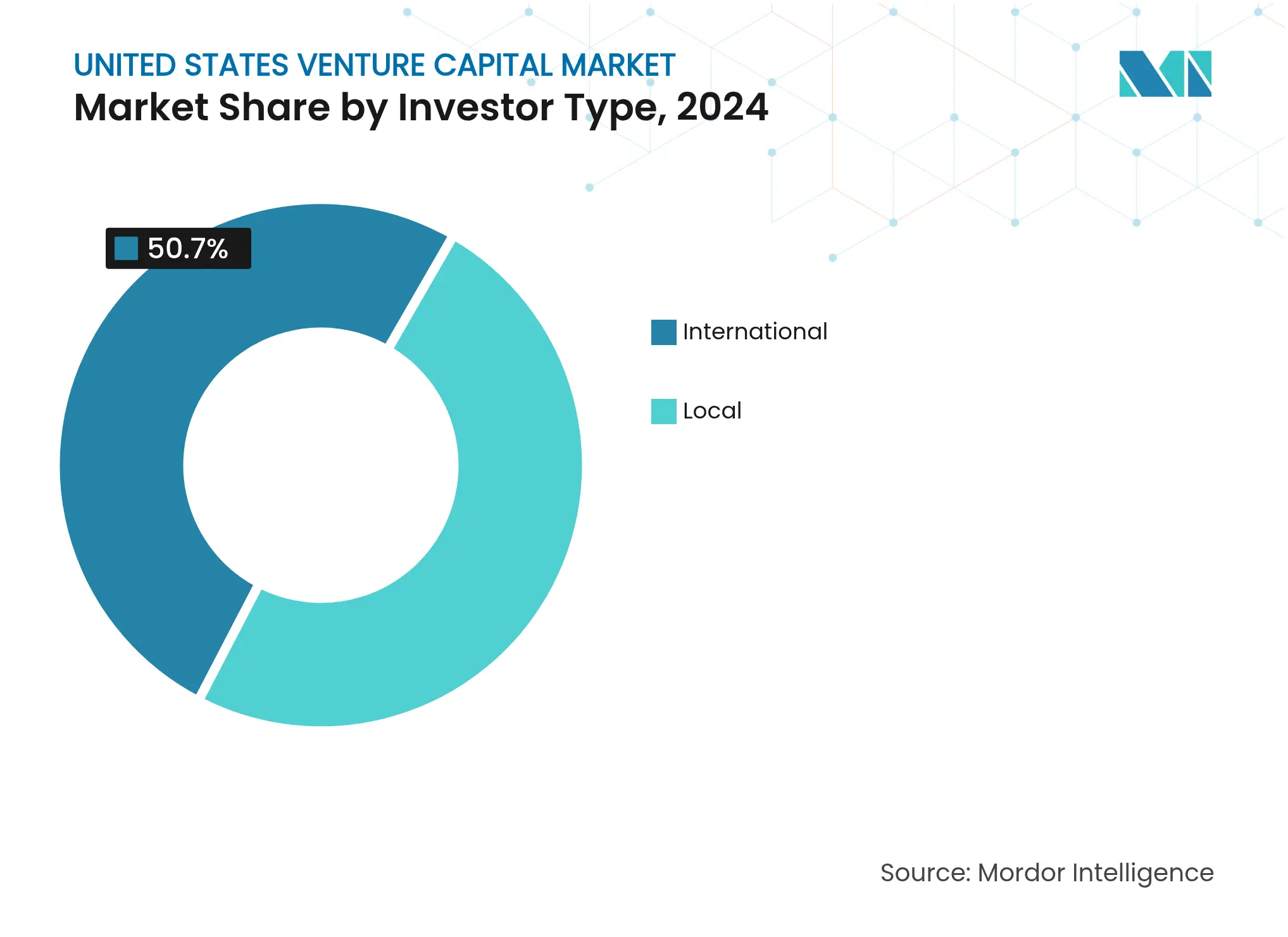

By Investor Type: Local Capital Dominance Challenged by International Growth

Local investors maintain overwhelming market control at 49.3% share in 2024, reflecting the importance of geographic proximity for due diligence, board participation, and portfolio company support in the venture capital ecosystem. This domestic concentration provides advantages through regulatory familiarity, cultural alignment, and established network effects that enable deal sourcing and co-investment opportunities. However, International investors demonstrate the fastest growth at 12.17% CAGR through 2030, driven by sovereign wealth funds seeking diversification and foreign corporations pursuing strategic technology access.

The international capital influx includes Middle Eastern sovereign funds targeting AI and climate technology investments, Asian conglomerates establishing United States venture arms for market intelligence, and European family offices seeking dollar-denominated assets as inflation hedges. Regulatory frameworks under CFIUS review create compliance overhead for international investments in sensitive technology sectors, yet the strategic value of United States market access continues to attract foreign capital despite regulatory friction. The geographic capital flow patterns suggest continued internationalization of the United States venture ecosystem, though domestic investors retain structural advantages through local market knowledge and operational expertise.

Note: Segment shares of all individual segments available upon report purchase

In 2024, the West region holds a 33.3% market share, highlighting Silicon Valley's strong position in technology venture capital. Collaborations with university research programs, a well-established network of skilled professionals, and proximity to public market investors support this leadership. These investors play a crucial role in providing the necessary growth capital and ensuring liquidity for exits, which further strengthens the region's dominance in the market.

The South region, on the other hand, is experiencing the fastest growth, with a projected CAGR of 9.64% through 2030. This rapid expansion is driven by favorable tax policies, lower operational costs, and a high quality of life that attracts both entrepreneurs and venture capital professionals. Texas is at the forefront of this growth, with the Austin-Dallas-Houston triangle creating a thriving ecosystem. Successful business exits in this area are generating local angel investments and fostering networks of experienced entrepreneurs, further fueling the region's development.

Other Southern states are also contributing to this growth. Florida is emerging as a key player, with Miami benefiting from its international connectivity and a regulatory environment that supports cryptocurrency ventures. North Carolina and Georgia are developing specialized hubs around their research universities and corporate headquarters. Meanwhile, the Northeast remains a significant market, with New York's focus on fintech and Boston's strength in biotech. The Midwest is also attracting investments in industrial technology and agricultural innovation. This geographic diversification helps reduce risks associated with concentrating investments in one area while unlocking new talent pools and customer bases, providing scaling companies with a competitive advantage.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Market Concentration

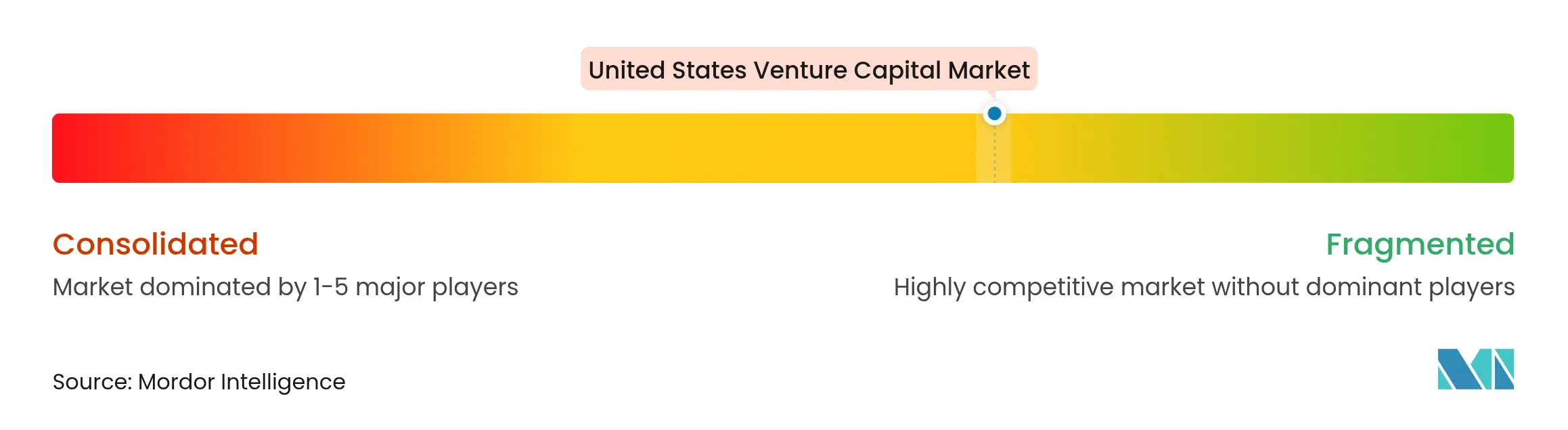

The United States venture capital market in 2024 exhibits moderate concentration, with a handful of top-tier firms maintaining a significant share of overall activity. Leading players like Sequoia Capital, Andreessen Horowitz, Tiger Global, Lightspeed, and Accel continue to dominate, leveraging their brand strength, broad networks, and long-standing relationships with limited partners to access the most competitive deals. This concentration reflects a market where established firms hold a clear advantage in sourcing and winning top opportunities. At the same time, the presence of strong incumbents creates a high barrier to entry for newer players. Meanwhile, emerging managers are carving out niches through sector specialization and regional focus. The market exhibits a “barbell” structure, with both micro funds (under USD 10 million) and mega funds (over USD 100 million) growing, while mid-sized funds face institutional pressure for proven scale and returns. This structural bifurcation is reshaping how capital is raised and deployed across the ecosystem.

Strategic responses to AI market shifts include traditional venture firms focusing on application-layer investments to counterbalance tech giants’ dominance in infrastructure-focused mega-rounds. Special purpose vehicles (SPVs) are increasingly used to secure allocations in billion-dollar financings examples include Menlo Ventures’ SPV in Anthropic and Inovia’s in Cohere. Firms are also targeting white-space opportunities in vertical AI, climate tech commercialization, and underserved geographic markets beyond coastal hubs. The evolving regulatory environment, particularly new SEC private fund rules, creates compliance burdens that established firms are better equipped to manage. As such, operational scale and compliance infrastructure are becoming key differentiators.

Disruptive forces in the venture ecosystem include corporate venture arms offering strategic synergies, as well as government-backed funds focused on critical tech like semiconductors and clean energy. Alternative investment platforms are also democratizing access to VC through tokenization and secondary markets, unlocking new capital sources. These trends are expanding the competitive set beyond traditional VCs and reshaping funding dynamics. Startups are increasingly evaluating investors not only on capital but also on regulatory readiness, strategic alignment, and distribution leverage. As venture evolves, firms that combine domain expertise, flexible structures, and institutional-grade operations are best positioned to lead.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size & Growth Forecasts

6. Competitive Landscape

7. Market Opportunities & Future Outlook

A Venture Capital firm is a group of investors who gain income from wealthy people who want to grow their wealth. They use this money to invest in more risky businesses than a traditional bank is willing to take on. Because the investments are risky, the venture capital firm typically charges a higher interest rate to the businesses it invests in than other lenders.

The United States Venture Capital Market is segmented by investments ( banking & financial services, healthcare, telecommunications, government agencies, and others), stage of investment (seed stage, startup stage, first stage, expansion stage, and bridge stage), and major states (California, New York, Massachusetts, Washington, and others). The report offers market size and forecasts for the United States Venture Capital Market in value (USD) for all the above segments.

Wealth Management Intelligence for the Middle East

4 Min Read

Driving Growth in the Embedded Insurance Market

4 Min Read

Wealth Management Intelligence for the Middle East

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.