Legal Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

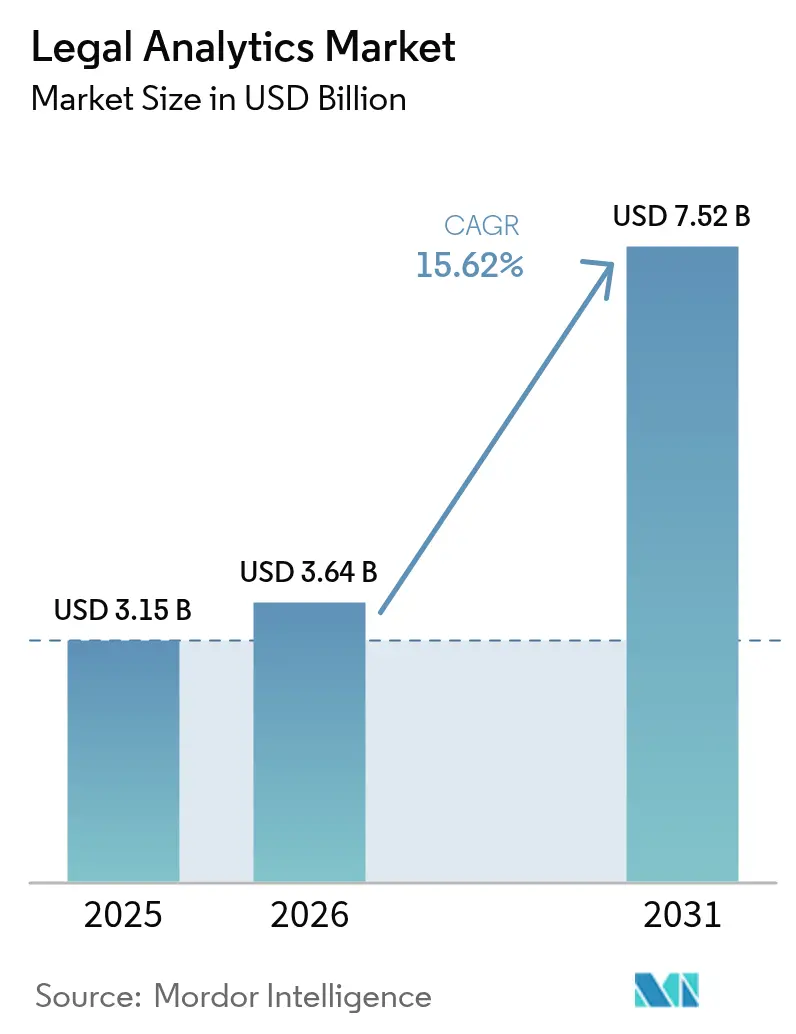

| Market Size (2026) | USD 3.64 Billion |

| Market Size (2031) | USD 7.52 Billion |

| Growth Rate (2026 - 2031) | 15.62% CAGR |

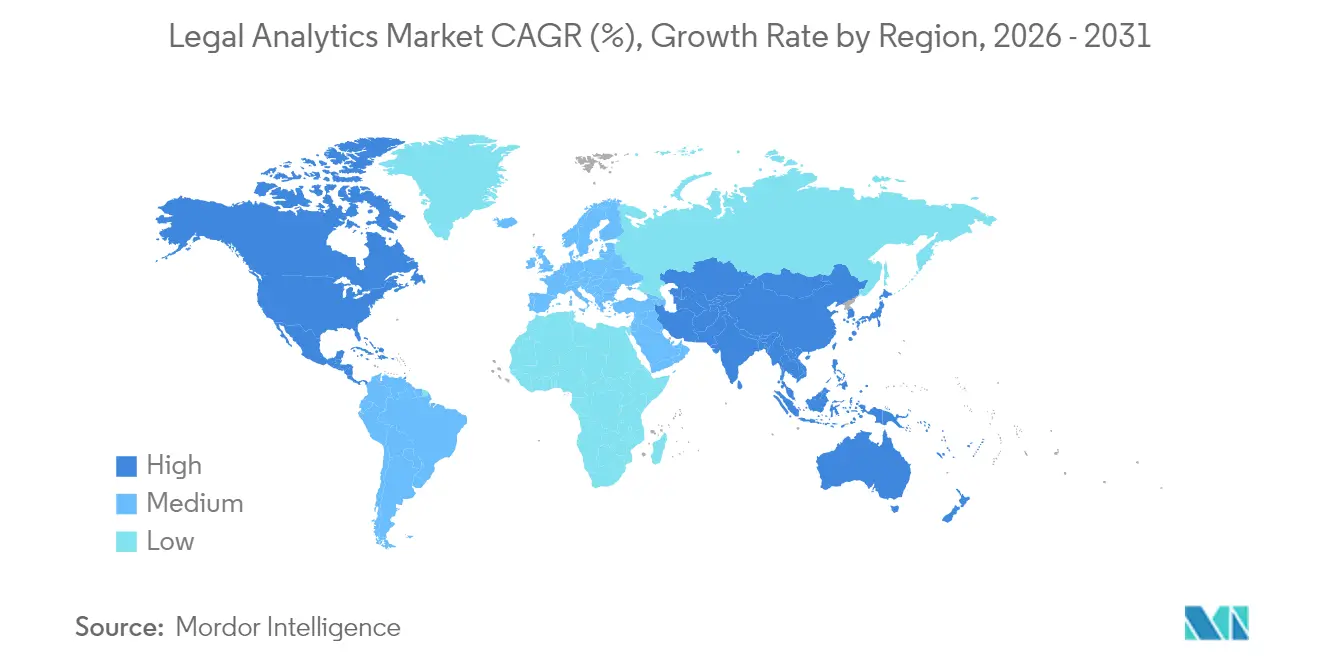

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Legal Analytics Market Analysis by Mordor Intelligence

The legal analytics market size was valued at USD 3.15 billion in 2025 and estimated to grow from USD 3.64 billion in 2026 to reach USD 7.52 billion by 2031, at a CAGR of 15.62% during the forecast period (2026-2031). Demand is rising as corporate counsel embed artificial intelligence in routine workflows, pushing data-driven strategy to the center of legal operations. Larger law firms are scaling cloud-hosted platforms to trim infrastructure expense, while in-house teams accelerate adoption to meet board-level reporting expectations. Europe’s stringent privacy regime is driving analytics spending on compliance automation, and litigation funders are utilizing predictive tools to price risk more accurately. The competitive field remains moderately concentrated yet open to niche entrants that offer intuitive user interfaces and narrow, high-value use cases.

Key Report Takeaways

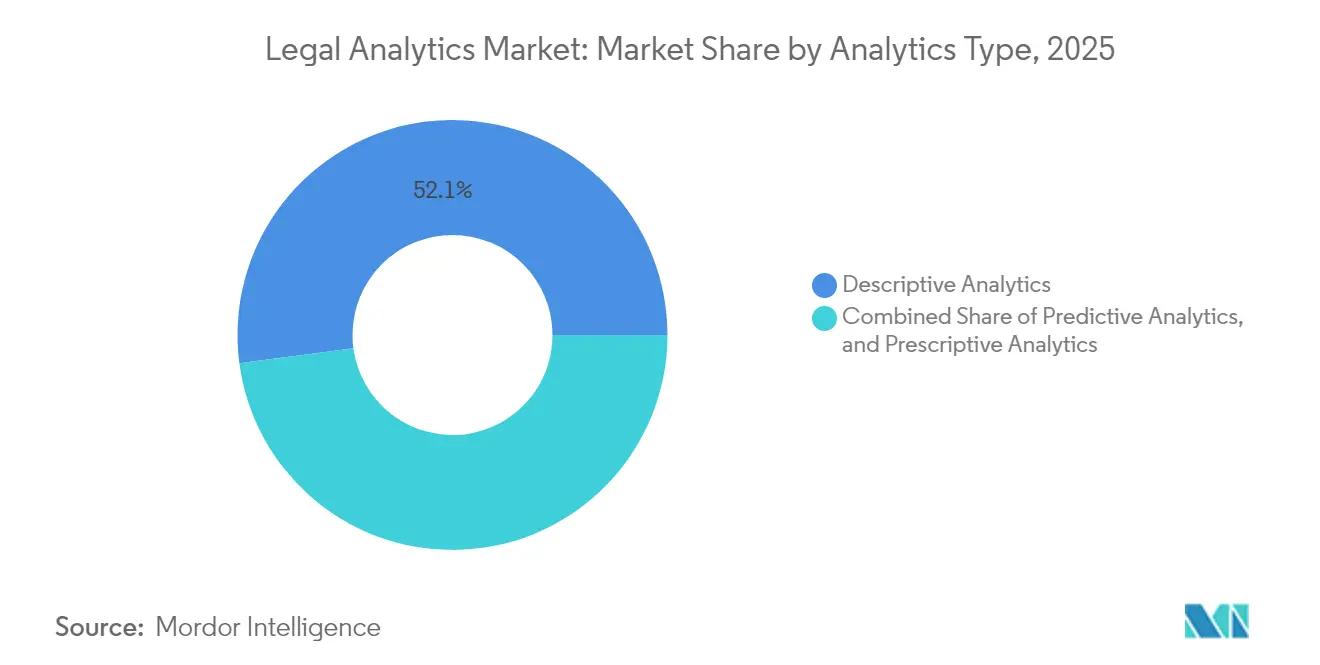

- By analytics type, descriptive analytics commanded 52.10% revenue share of the legal analytics market in 2025, whereas predictive analytics is forecast to expand at 16.02% CAGR through 2031.

- By deployment mode, cloud solutions accounted for 68.45% of the legal analytics market size in 2025, with the segment projected to advance at a 16.5% CAGR through 2031.

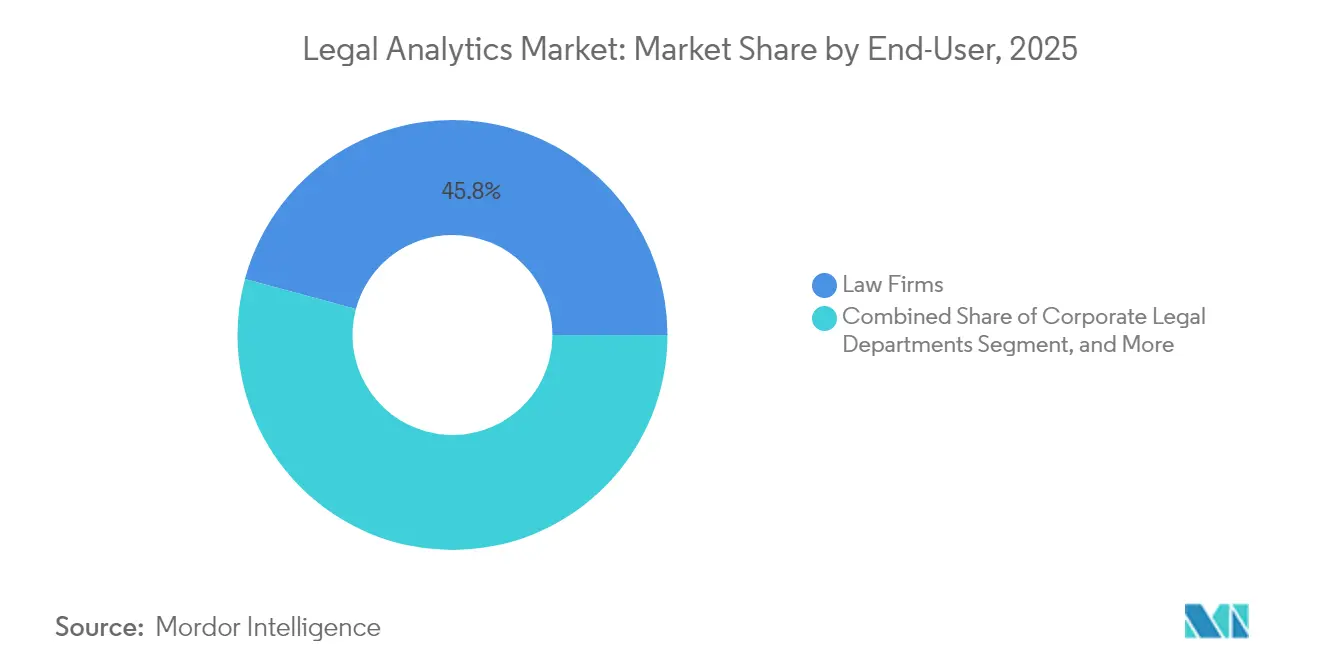

- By end-user, law firms led the legal analytics market with a 45.80% share in 2025, while corporate legal departments were projected to register the fastest CAGR of 16.9% through 2031.

- By practice area, intellectual property management held 29.40% of the legal analytics market share in 2025; case management is projected to grow at 16.4% CAGR to 2031.

- By geography, North America contributed 38.35% revenue in 2025, yet Europe shows the highest regional CAGR at 16.55% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Legal Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of AI and machine learning | +4.2% | Global; North America and Europe lead | Medium term (2-4 years) |

| Growing demand for data-driven decision making | +3.8% | Global; strongest in corporate legal departments | Short term (≤ 2 years) |

| Shift toward cloud-based legal solutions | +3.1% | North America and Europe core; APAC emerging | Medium term (2-4 years) |

| Emergence of litigation funding platforms | +2.3% | North America and United Kingdom | Long term (≥ 4 years) |

| Expansion of alternative legal service providers | +1.9% | Major global legal hubs | Medium term (2-4 years) |

| Integration of generative AI into pricing tools | +1.4% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of AI and Machine Learning

Corporate counsel reports that 47% of contract-review tasks now rely on machine learning models, a leap made possible by vendor-led implementation playbooks that cut deployment cycles by two-thirds. Document-review cost declines of 60-80% are routinely cited as justification for broader rollouts, especially in high-volume patent searches where algorithms process prior-art references ten times faster than manual review. These efficiency gains free attorney time for complex advisory work and sharpen competitive positioning during fee negotiations. Law schools and bar associations are now incorporating AI literacy programs, thereby expanding the talent pipeline. As adoption normalizes, vendors are shifting focus from point solutions to unified analytics suites that consolidate search, prediction, and outcome tracking.

Growing Demand for Data-Driven Decision Making

Boards expect legal departments to quantify risk in the same granular terms used for financial forecasting. Seventy-three percent of chief legal officers now mandate predictive dashboards when selecting outside counsel. [1]Association of Corporate Counsel, “2024 Legal Operations Survey,” Acc.com Litigators consult historical judge analytics to refine forum strategy, while transactional lawyers benchmark clause language against success rates in comparable deals. Alternative fee arrangements increasingly rely on outcome probabilities, forcing firms to disclose data that was once proprietary. This transparency is pressuring under-invested practices to modernize or exit contested segments. Vendors targeting this demand differentiate themselves on the breadth of data and interpretability, rather than pure algorithmic sophistication.

Shift Toward Cloud-Based Legal Solutions

Remote work proved a stress test for on-premise systems, and 68.97% of legal analytics deployments now sit in the cloud. Certifications such as ISO 27001 and SOC 2 Type II have mitigated privilege-related objections, enabling large firms to report 40-50% IT cost savings once legacy servers are retired. Cloud architecture accelerates product iteration, enabling monthly feature releases that keep pace with fast-evolving privacy laws. Smaller firms gain affordable entry to enterprise-grade analytics, tightening competition across firm tiers. Hybrid models remain for highly regulated niches, but the direction of travel is decisively cloud-first.

Emergence of Litigation Funding Platforms

The global litigation-finance pool surpassed USD 15.2 billion as funders turned to predictive analytics to triage caseloads and calibrate return thresholds. [2]Burford Capital, “Litigation Finance Survey 2024,” Burfordcapital.com Algorithms analyze judge histories, opposing counsel's track records, and docket trends to assign probability-weighted valuations within hours, rather than weeks. Plaintiffs benefit from faster access to capital, while funders hedge their risks with data-backed diversification strategies. Law firms servicing funded matters adopt the same toolsets to align fee structures with investor metrics. The feedback loop intensifies demand for model accuracy, nudging vendors to refine natural-language processing tuned to regional legal dialects.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation costs for SMEs | -2.8% | Global; most acute in emerging markets | Medium term (2-4 years) |

| Data privacy and security concerns | -2.1% | Europe and North America | Short term (≤ 2 years) |

| Limited structured case data in emerging markets | -1.6% | Asia-Pacific and Latin America | Long term (≥ 4 years) |

| Ethical and bias governance requirements | -1.3% | Global; regulatory focus in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Implementation Costs for SMEs

Solo and small practices make up 76% of the profession but contribute only 23% of analytics spending, hamstrung by annual subscription bundles that can exceed USD 100,000. Beyond licensing, data migration, and staff training disrupts billable hours for up to six months. Without scale economies, per-user costs remain stubborn, widening a technology gap that fuels consolidation as mid-tier firms seek merger partners to access shared platforms. Innovative pricing models, such as consumption-based pricing, are emerging but remain untested at scale.

Data Privacy and Security Concerns

Attorney-client privilege rules impose stricter handling protocols than those for general enterprise data, and 34% of firms have tightened vendor assessments following recent breaches. [3]International Association of Privacy Professionals, “Legal Analytics and Privacy,” Iapp.org European operators juggle GDPR localization mandates that complicate cross-border analytics workflows. Cloud vendors respond with regional data centers and granular user-access controls, but lingering uncertainty slows adoption in highly sensitive practice areas. Demonstrable encryption, audit logs, and explainable AI reports have become table stakes for market entry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Analytics Type: Predictive Models Drive Strategic Advantage

Predictive engines are shifting client conversations from past performance to forward-looking strategy. In 2025, descriptive tools still accounted for 52.10% of the legal analytics market, yet the predictive sub-segment is growing at 16.02% CAGR and is forecast to narrow that gap rapidly. Users cite 70-85% accuracy in routine commercial disputes, which heightens trust and spurs repeat usage. The legal analytics market size for predictive applications was measured at USD 1.03 billion in 2025 and is expected to double by 2031 if current spending patterns persist. Over the past year, firms have embedded outcome scores directly into matter-budget templates, allowing partners to tailor fee structures to quantified risk. Descriptive dashboards remain vital for billing and utilization metrics, but their value increasingly lies in feeding historical datasets to predictive algorithms. Prescriptive analytics, though nascent, is attracting pilots in outside-counsel selection, signaling an eventual move toward closed-loop decision support.

Second-order effects reinforce the momentum. Courts are digitizing judgments, expanding the training corpus for supervised models. Insurers underwriting litigation risk now request predictive-model documentation during policy negotiation, injecting further demand. Software vendors integrate visualization layers that translate probability curves into plain-language guidance, making insights digestible for non-technical stakeholders. Collectively, these trends position predictive capabilities as the next battleground for competitive differentiation within the legal analytics market.

By Deployment Mode: Cloud Security Concerns Yield to Economic Benefits

Cloud installations captured 68.45% of total deployments in 2025 and are projected to grow at 16.5% CAGR through 2031, underpinned by evidence of 40-50% lifecycle cost savings once legacy on-premise systems are decommissioned. The legal analytics market share for on-premise stacks fell below 30% for the first time in 2025 as firms faced mounting expenses to patch aging infrastructure. Vendors tailor region-specific data-residency options to reassure privacy regulators, and leading platforms now pass annual SOC 2 Type II audits as a baseline credential. Hybrid patterns persist for government agencies that must retain sovereign control; however, even in these cases, non-sensitive workloads are migrating to the cloud.

The cloud shift democratises advanced functions. Smaller firms can now access natural-language processing and visualization tools once limited to global players, thereby compressing the competitive distance. Continuous integration pipelines shorten feature-release cycles from quarterly to weekly, ensuring rapid policy-compliance updates. However, reliance on multitenant environments introduces shared-fate risk, prompting insurers to develop cyber-coverage riders specifically for legal data exposures. Overall, the cloud trajectory appears irreversible, cementing subscription economics and data-network effects at the heart of the legal analytics market.

By End-User: Corporate Legal Departments Accelerate Technology Adoption

In-house teams account for just under one-third of 2025 revenue but will expand at 16.9% CAGR to surpass law-firm spending mid-decade. Legal operations managers cite integration with enterprise resource planning platforms as the primary catalyst, enabling line-item tracking of outside counsel spend and matter outcomes. The legal analytics market size for corporate buyers reached USD 1.07 billion in 2025 and is projected to climb steeply as boards demand quantitative risk dashboards. Law firms, which hold a 45.80% share, face billing-related friction that slows the full-suite deployment; however, market-share erosion is not imminent because firms retain complex litigation expertise.

A two-speed ecosystem is emerging. Fortune 500 legal departments pilot generative AI for clause redlining, while mid-sized practices focus on time-entry analytics to improve realization rates. Government and regulatory bodies remain the smallest segment but record steady gains as digital-transformation grants fund case-management modernization. The divergence suggests continued development of client-driven features rather than attorney-centric workflows, amplifying pressure on external counsel to prove value through data.

By Practice Area: IP Management Leads Analytics Integration

Intellectual property applications comprise 29.40% of revenue, thanks to patent-landscape analytics and automated trademark surveillance that cut research cycles by up to 80%. The legal analytics market size allocated to IP functions was USD 0.93 billion in 2025 and is forecasted to experience healthy expansion as R&D-intensive industries protect their innovation pipelines. Predictive claim-charting tools achieve 80% accuracy in examiner outcome forecasts, encouraging corporations to redirect prosecution budgets toward a portfolio strategy.

Case-management analytics is the fastest riser, with 16.4% CAGR, underwritten by litigation-fund vectorization that cross-references judge sentiment and settlement ranges. Capital markets lawyers utilize text-extraction models for prospectus verification, while environmental practices identify regulatory overlaps across jurisdictions. Financial documentation services integrate with generative AI to reconcile clause inconsistencies, reducing post-closing risk. Collectively, practice-specific modules deepen vendor moats and signal a shift from one-size dashboards to tailored vertical solutions within the legal analytics market.

Geography Analysis

North America retained a 38.35% revenue share in 2025, driven by established e-discovery spending and mature vendor ecosystems. Yet Europe is advancing at 16.55% CAGR, narrowing the gap each year as firms automate GDPR compliance checks and standardize cross-border workflows. Several European bar associations now require explainability audits for algorithms used in litigation strategy, prompting accelerated platform upgrades. Federal court digitization grants in the United States continue to funnel docket data into public repositories, giving domestic vendors a training-data advantage that sustains local dominance.

Asia-Pacific markets display uneven adoption. Japan and Australia deploy cloud-hosted analytics suites, whereas many Southeast Asian jurisdictions grapple with sparse case-law digitization. Multinationals operating regionally demand unified dashboards, spurring partnerships between global vendors and local data aggregators. Governments in Singapore and South Korea subsidize legal-tech sandboxes, nurturing domestic start-ups that may challenge incumbent suppliers in specialized niches.

The Middle East and Africa post the highest percentage growth, albeit from a small base. International arbitration hubs in Dubai, Abu Dhabi, and Johannesburg introduce model clauses that recommend analytics-driven risk assessment, creating pull-through demand among regional law firms. Infrastructure-related disputes underscore the need for bilingual natural-language processing covering Arabic, English, and French. World Bank justice-modernization projects earmark funds for court-record digitization, laying the groundwork for future predictive-analytics deployment. Overall, regional trajectories suggest a gradual rebalancing of the legal analytics market toward markets once considered technology laggards.

Regulatory Landscape

Legal analytics adoption is increasingly conditioned by AI governance and data-transfer controls that shape how privileged content and personal data are processed in cloud analytics stacks. In the European Union, the EU AI Act (Regulation (EU) 2024/1689) raises the bar for risk management, transparency, and documentation for AI-enabled legal workflows, reinforcing demand for explainability and auditability features already becoming table stakes in Europe under GDPR-driven scrutiny.

In the United States, data-governance requirements are tightening alongside regulators expanding their own analytics capabilities. A January 2025 U.S. rule restricting access to U.S. sensitive personal data by countries of concern adds compliance complexity for cross-border data use, while a June 2026 final joint rule by U.S. financial regulators sets standardized, interoperable data standards with an October 2026 effective date, accelerating momentum toward machine-readable data and consistent reporting formats. Regulator use of examination analytics, such as the SEC National Exam Analytic Tool (NEAT), further normalizes analytics-led oversight and influences vendor security, privacy, and data-lineage expectations.

Value Chain Analysis

The legal analytics value chain starts with data creation and aggregation (court dockets, judgments, filings, corporate transaction documents, contracts, and firm know-how), followed by curation and enrichment by legal information providers and data aggregators, then model development and productization by software vendors. Large publishers such as Thomson Reuters and RELX/LexisNexis monetize proprietary content libraries by layering analytics and generative AI workflows, while specialty providers contribute focused capabilities in areas such as contract intelligence, internal knowledge search, and judge or docket analytics. Cloud and AI infrastructure (including hyperscalers and foundation-model ecosystems) underpin training and inference, and implementation partners and ALSPs help with data migration, workflow redesign, and governance needed to operationalize tools inside law firms and corporate legal departments.

Distribution and monetization are primarily subscription SaaS, increasingly bundled into broader legal productivity suites and embedded directly in document and matter workflows. Partnerships have become a core scaling mechanism across the chain, illustrated by LexisNexis aligning with Harvey (June 2025) to bring authoritative content and citations into a third-party AI workflow, and Thomson Reuters partnering with Icertis and Accenture (September 2025) to connect CoCounsel to contract intelligence with systems integration support. Key bottlenecks remain access to high-quality structured internal data (to make firm-specific insights reliable), privilege-safe security controls (SOC 2/ISO-style assurance), and affordability for smaller practices where total subscription and implementation costs can be prohibitive.

Competitive Landscape

Competition balances between legacy information providers and agile point-solution vendors. Thomson Reuters, Wolters Kluwer, and LexisNexis extend proprietary content libraries into analytics layers, capitalizing on entrenched law-firm relationships. Their scale supports continuous R&D investment; however, user surveys criticize the interface complexity compared to newer entrants. Specialized vendors deliver streamlined user experiences focused on single pain points such as judge analytics or contract-risk scoring, often onboarding clients in days instead of months.

Consolidation is underway. Wolters Kluwer’s 2024 acquisition of Klarity expanded contract-review capability, while Thomson Reuters rolled out CoCounsel 2.0 with generative drafting functions. Everlaw’s USD 202 million Series D round valued the company at USD 2.1 billion, underscoring investor conviction in the company's sustained expansion. Patent filings linked to legal analytics innovations have increased by 340% since 2024, with a focus on multilingual natural-language processing that supports global dockets.

Regulation increasingly shapes competitive edges. Providers tout SOC 2 and ISO certifications as differentiators, and the European Commission's draft AI rules are prompting the rollout of bias-audit dashboards. Firms lacking resources to adapt may exit or merge, foreshadowing a market structure where half a dozen full-suite platforms coexist with a long tail of niche specialists. The net effect positions the legal analytics market as moderately concentrated but dynamic, with clear pathways for both incumbents and disruptors to flourish.

Legal Analytics Industry Leaders

Wolters Kluwer NV

Thomson Reuters Corporation

Mindcrest Inc.

Lexisnexis ( RELX plc )

Abacus Data Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear opportunity is emerging around production-grade, workflow-embedded analytics that combine authoritative content with firm and enterprise data under stronger governance controls. Consolidation and platform build-outs signal where buyers are allocating budget: Thomson Reuters completed its acquisition of Noetica in February 2026 to add transactional data, semantic benchmarking, and risk analysis into CoCounsel, and RELX agreed to acquire French legaltech company Doctrine in April 2026 to strengthen legal AI workflows in Europe. These moves highlight demand for deeper domain datasets (deal terms, case law, and citations) that translate directly into benchmarking, risk scoring, and decision support across research, drafting, and transactional work.

Another whitespace sits in cross-border compliance and machine-readable regulatory change management, as regulators and standards bodies push toward structured reporting and digitally consumable rules. The UK FCA selecting FinregE (March 2026) to host and manage the official FCA Handbook website using an intelligent taxonomy and machine-readable regulation library provides a concrete reference point for tools that track regulatory change and map obligations to policies, controls, and evidence. Vendors that package secure data residency options, model audit artifacts (bias and explainability reporting), and integrations into existing legal and enterprise systems have an opening to move beyond point analytics into governed operating layers for corporate legal departments, law firms, and regulated-industry legal teams.

Recent Industry Developments

- July 2026: Wolters Kluwer integrated its Legal Intelligence multi-content-provider platform with the Libra by Wolters Kluwer AI workspace in the Netherlands. The integration brings broader legal content into a single AI-assisted environment, reinforcing the shift toward unified workspaces that combine research, drafting, and analytics. It enables cross-content search and streamlined collaboration across legal teams.

- February 2026: Thomson Reuters completed the acquisition of Noetica, an AI-native platform focused on corporate transaction intelligence, to integrate transactional data, benchmarking, and risk analysis into its CoCounsel offering. The deal strengthens Thomson Reuters ability to deliver analytics for deal workflows, expanding beyond litigation and research into transaction-centric decision support. The acquisition also expands CoCounsel with benchmark data and risk scoring capabilities.

- October 2024: Thomson Reuters launched CoCounsel 2.0 and committed USD 50 million to embed generative AI into contract analysis and legal research workflows. The release accelerated product competition around AI-assisted legal work and raised baseline expectations for integrated drafting, research, and analytics within major vendor platforms.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the legal analytics market covers software and related services that use structured and unstructured legal data to support decisions, improve workflows, and measure outcomes for legal work across organizations.

Scope exclusions: We exclude generic business intelligence tools that are not built for legal data and legal workflows, and we also exclude pure legal staffing and advisory-only services.

Segmentation Overview

- By Analytics Type

- Descriptive Analytics

- Predictive Analytics

- Prescriptive Analytics

- By Deployment Mode

- Cloud

- On-Premise

- By End-User

- Law Firms

- Corporate Legal Departments

- Government and Regulatory Agencies

- By Practice Area

- Intellectual Property Management

- Capital Markets and Corporate Governance

- Case Management

- M&A and Environmental Law

- Financial Documentation Services

- Other Practice Area

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work is used to set the market boundary, map demand indicators, and anchor assumptions that can be checked later in interviews. We typically start with public sources such as US Bureau of Labor Statistics data on legal services employment, US Courts and other court administration statistics on caseloads, and government procurement portals that show legal tech buying patterns.

We also review sources such as WIPO patent databases for analytics and legal-tech related filings, SEC filings and annual reports for revenue commentary, and association and policy sources such as the ABA and data protection regulators for adoption constraints. News and financials subscriptions are used to track funding, product launches, and M&A activity, and a patent database subscription is used to reduce misses in fast-moving analytics categories. These examples are not exhaustive, and many other public and paid sources were also referred to for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test what desk sources cannot confirm well, especially pricing ranges, deployment mix shifts, and typical buying units inside legal teams. We speak with solution providers, channel partners, law firm operations teams, corporate legal departments, and government and regulatory users across major regions so that adoption drivers and blockers can be sized with real-world context.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 14% | APAC: 41% |

| Mid tier: 57% | Functional/Unit leaders: 40% | EMEA: 33% |

| Smaller Players: 17% | Managers: 46% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the addressable demand pool by linking legal activity to analytics spend potential, and then it is split by region and buyer type to match how budgets are actually set. The model uses inputs such as the number of practicing attorneys and legal staff, litigation and regulatory caseload intensity, cloud adoption levels in legal IT, typical contract lengths, and observed price bands for enterprise and SMB deployments.

Once the demand pool is formed, it is corroborated with selective bottom-up checks, such as sampled vendor revenue disclosures where available, channel feedback on deal sizes, and simple ASP times estimated user counts for common use cases like case analytics and contract analytics. Where a bottom-up view is incomplete, gaps are handled by applying interview-backed penetration rates by buyer cohort and by validating that the implied spend per user stays within realistic procurement thresholds.

For forecasting, we rely on scenario analysis supported by a light multivariate view of the strongest drivers, including expected changes in caseload volumes, AI feature adoption, cloud migration pace, and compliance and privacy requirements that can slow deployments. The final outlook is adjusted only after expert feedback confirms that the assumed price progression and adoption timing fit procurement cycles in legal teams.

Data Validation & Update Cycle

Validation is done by triangulating outputs against independent signals, and then by checking if the implied adoption and spend levels look reasonable across regions and end users. Outliers are flagged, reviewed, and traced back to the assumption level, after which the relevant inputs are rechecked in desk sources or clarified through follow-up calls.

Before sign-off, the model and key assumptions go through multi-step analyst reviews so that errors from double counting, currency timing, or unrealistic penetration are removed. Reports are refreshed annually, with interim updates triggered when material events occur, such as major regulation changes, large acquisitions, or clear pricing shifts. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Legal Analytics Market Size Versus Other Published Estimates

Published market values for legal analytics can differ quite a bit, even when the topic name looks the same. In most cases, the spread comes from what is counted as legal analytics, how services are treated, and how aggressively adoption is assumed to expand.

The table shows a wide range in 2025 values, and in Mordor Intelligence's model the total is built around legal-specific analytics offerings tied to law firms, corporate legal departments, and government and regulatory usage, rather than folding in broader legal tech adjacencies that sit outside analytics. Differences also come from how fast cloud mix is assumed to shift, whether prescriptive analytics is fully priced in early years, and how currency conversion timing is handled for multi-region totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.15 B (2025) | |

| Global Consultancy A | USD 5.93 B (2025) | The figure appears to apply a broader scope that can pull in adjacent legal technology spend, and it may assume faster near-term enterprise adoption and higher bundled pricing across use cases. |

| Industry Publisher B | USD 3.77 B (2025) | This estimate likely differs in how it treats services and platform add-ons, and it can vary based on a higher assumed cloud share and a quicker ramp in predictive analytics penetration. |

Across the three values, most of the gap can be explained by scope boundaries and the pace of adoption used in the early years, which then compounds in forecasts. By tying assumptions to observable legal activity signals and then validating pricing and penetration with interviews, the market total remains traceable to clear steps and adjustable when new evidence shows up.

Key Questions Answered in the Report

What is the current size of the legal analytics market?

The legal analytics market size reached USD 3.64 billion in 2026.

How fast is the sector growing?

Revenue is forecast to increase at a 15.62% CAGR, taking the market to USD 7.52 billion by 2031.

Which region is expanding the quickest?

Europe shows the fastest regional CAGR at 16.55%, driven by GDPR compliance automation.

Which analytics type is gaining ground fastest?

Predictive analytics is projected to grow at 16.02% CAGR as firms shift toward forward-looking insights.

Who leads in deployment preference?

Cloud solutions dominate with 68.45% share thanks to lower total cost of ownership and rapid feature updates.

Why are corporate legal departments investing heavily now?

In-house teams need real-time spend and risk dashboards to meet board-level transparency mandates, fueling 16.9% CAGR growth.

Page last updated on: