Market Overview

| Study Period | 2020 - 2031 |

|---|---|

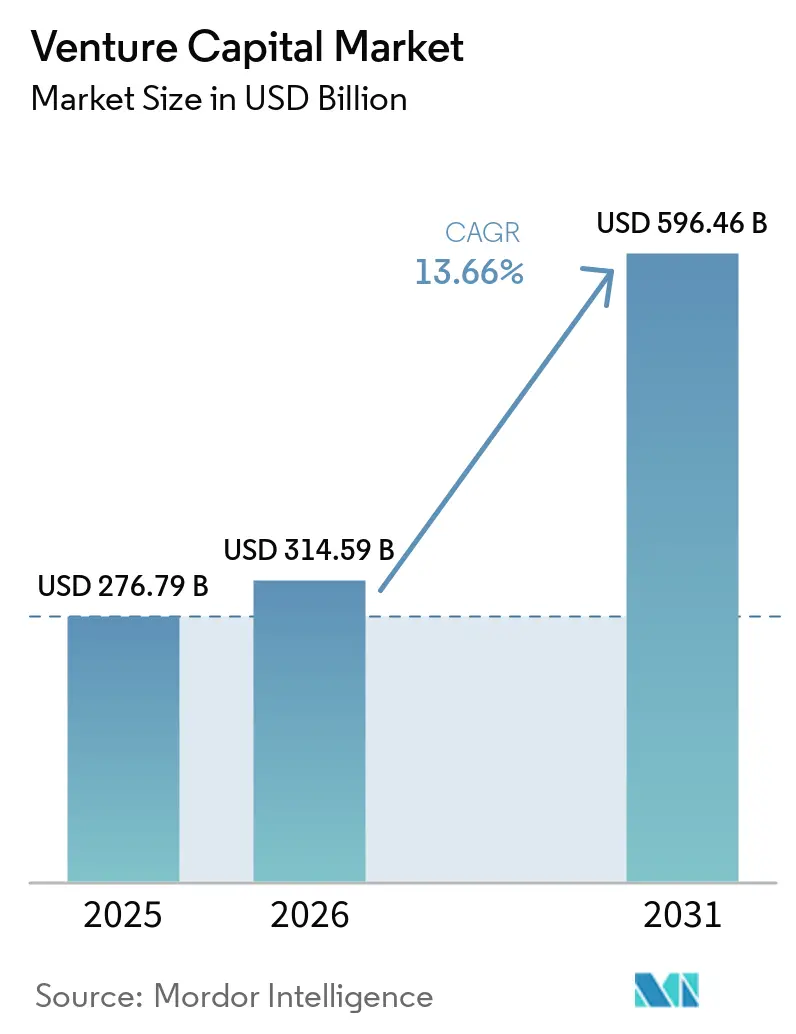

| Market Size (2026) | USD 314.59 Billion |

| Market Size (2031) | USD 596.46 Billion |

| Growth Rate (2026 - 2031) | 13.66% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Venture Capital Market Analysis by Mordor Intelligence

The Venture Capital Market size is projected to be USD 276.79 billion in 2025, USD 314.59 billion in 2026, and reach USD 596.46 billion by 2031, growing at a CAGR of 13.66% from 2026 to 2031.

Investors are chasing artificial-intelligence-native start-ups, sovereign wealth funds are reallocating capital overseas, and corporate venture arms are accelerating deal velocity to secure technological moats. Secondary trading platforms that improve liquidity for limited partners are also sustaining momentum in the venture capital market. Institutional portfolios continue to view the asset class as offering superior risk-adjusted returns over traditional equities and bonds[1]Anirban Sen, “Investors Stick to VC Despite Rate Rise,” Reuters, reuters.com. Competitive intensity is therefore rising as traditional firms contend with sovereign funds, corporate investors, and crypto-native vehicles for premium deal flow.

Key Report Takeaways

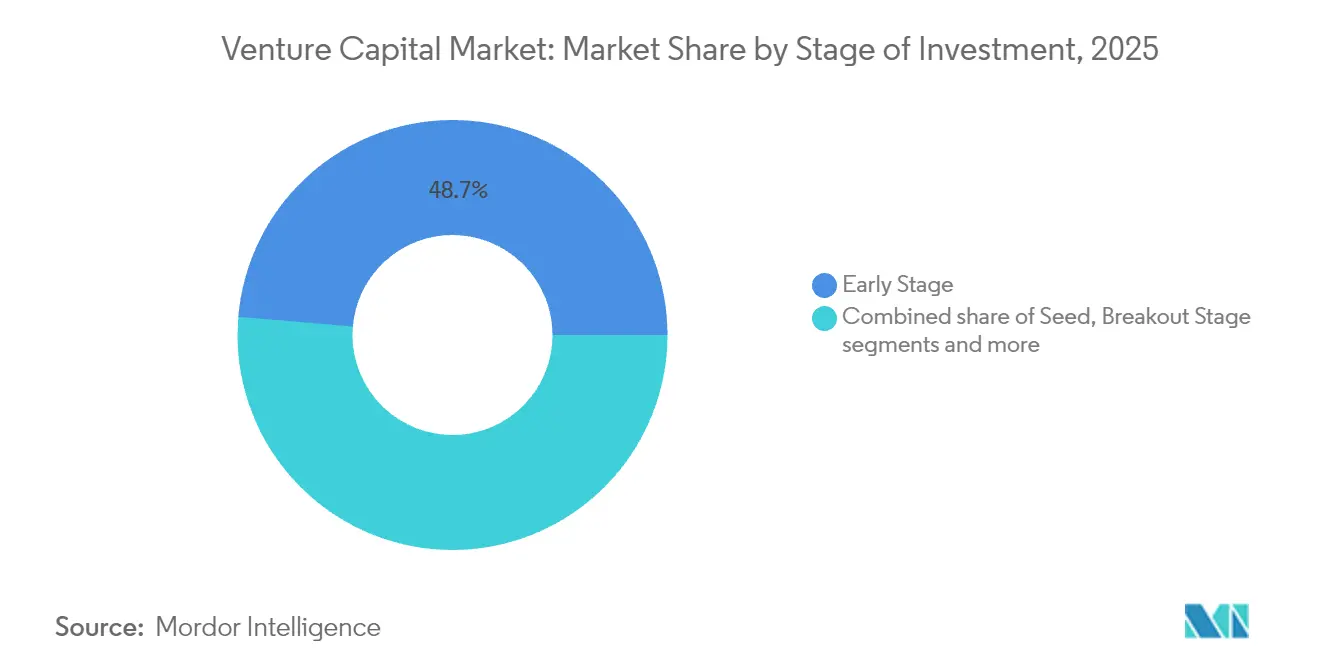

- By stage of investment, early-stage deals held 48.65% venture capital market share in 2025, while scale-up financing is projected to expand at a 9.05% CAGR through 2031.

- By industry, enterprise software commanded 26.65% of the venture capital market size in 2025, whereas robotics is forecast to grow at a 8.86% CAGR to 2031.

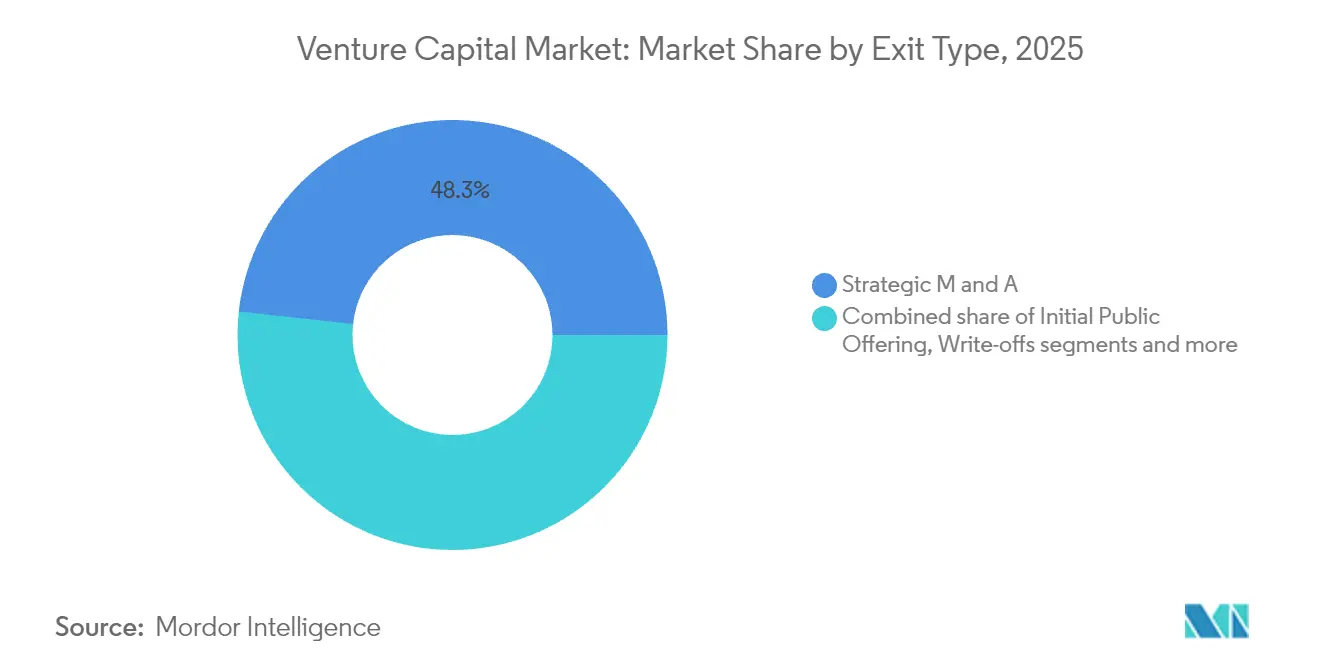

- By exit type, mergers and acquisitions captured 48.25% of total exits in 2025, and initial public offerings are expected to rise at a 9.45% CAGR as public markets normalize.

- By geography, North America accounted for 46.20% venture capital market share in 2025, yet Asia-Pacific is set to climb at a 9.92% CAGR as hard-tech ecosystems mature.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Venture Capital Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-native start-ups demanding larger seed rounds | +2.8% | Global, concentrated in North America & Asia-Pacific | Medium term (2-4 years) |

| Sovereign wealth funds enlarging non-domestic VC allocations | +2.1% | Global, with focus on cross-border investments | Long term (≥ 4 years) |

| Corporate VC arms accelerating strategic deal count | +1.9% | North America & Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Secondary marketplaces improving liquidity for LPs | +1.6% | Global, early adoption in North America & Europe | Medium term (2-4 years) |

| Token-based fundraising models converging with traditional VC | +1.4% | Global, regulatory-dependent adoption | Long term (≥ 4 years) |

| Geopolitical re-shoring incentives for critical tech sectors | +1.2% | North America, Europe, select Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Native Start-ups Demanding Larger Seed Rounds

Seed-stage rounds for artificial-intelligence companies jumped from USD 2.1 million in 2019 to USD 8.7 million in 2024, reflecting steep compute and talent costs[2]Patrick McGee, “AI Start-ups Rewrite Seed Economics,” Financial Times, ft.com. The venture capital market is bifurcating between AI-first businesses that need USD 5–15 million seed funding and traditional software firms that still operate on USD 1–3 million. Corporate investors such as Google Ventures and Amazon’s Alexa Fund collectively deployed more than USD 3.2 billion into AI seeds during 2024. Venture firms are opening offices in Montreal, Tel Aviv, and Singapore to chase localized talent clusters. Fund lifecycles are stretching from 10 to 12 years to accommodate longer AI commercialization timelines, reshaping the venture capital market’s return horizon.

Sovereign Wealth Funds Enlarging Non-Domestic VC Allocations

Sovereign wealth funds committed USD 47 billion to overseas technology deals in 2024, a 43% annual jump[3]Katie Roof, “Sovereign Funds Hunt Tech Abroad,” Wall Street Journal, wsj.com. Saudi Arabia’s Public Investment Fund launched a USD 8 billion vehicle targeting North American and European start-ups, and Singapore’s GIC grew its venture team by 65%. Patient capital from these funds is crowding traditional institutional investors out of marquee rounds. Regulatory regimes in recipient countries now balance economic openness with national-security screens for semiconductors and quantum computing deals. Consolidation among fund managers is intensifying because sovereign funds prefer large, multi-vintage platforms in the venture capital market.

Corporate VC Arms Accelerating Strategic Deal Count

In 2024, strategic investors participated in 47% of all venture rounds, a notable increase from 31% in 2019. Highlighting the trend, Amazon wrote a USD 4 billion check to Anthropic, while Meta expanded its Reality Labs portfolio. Corporates are now establishing dedicated funds, inviting external limited partners, and combining strategic alignment with financial gains. Meanwhile, independent venture firms are carving a niche by prioritizing governance neutrality and offering broader exit options. The healthcare technology sector is witnessing heightened interest, with Roche and Novartis boosting their venture allocations by over 80% in 2024.

Secondary Marketplaces Improving Liquidity for LPs

Private-shares platforms processed more than USD 12 billion of transactions in 2024, up 34% year over year. Services now include growth-capital advances, employee option liquidity, and advisory support that supplement traditional venture stewardship. Pension funds are earmarking up to 20% of their private-market buckets for secondaries to manage capital calls. Standardized pricing tools are tightening bid-ask spreads, widening participation to smaller institutions. Blockchain settlement is expected to compress clearance times, enhancing transparency across the venture capital market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher interest-rate environment compressing valuations | -2.3% | Global, most pronounced in North America & Europe | Short term (≤ 2 years) |

| Exit drought extending fund-raising cycles | -1.8% | Global, concentrated in mature markets | Medium term (2-4 years) |

| Heightened antitrust scrutiny of tech M&A | -1.5% | North America & Europe, selective impact in Asia-Pacific | Medium term (2-4 years) |

| Limited partner shift toward private credit funds | -1.2% | Global, led by North America & Europe institutional investors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Interest-Rate Environment Compressing Valuations

Average late-stage valuations fell 32% from 2021 highs after central banks kept policy rates above 5% through 2024[4]Tabby Kinder, “Rate Hikes Hit VC Valuations,” Financial Times, ft.com. Down rounds surged 67% during the year, cutting some enterprise-software prices by 25–40%. Venture investors have pivoted to profitability metrics, rewarding firms with durable margins and cash generation. Mark-to-market hits are complicating new fund raises, lengthening the capital-recycling cycle in the venture capital market. Analysts expect only gradual multiple expansion as rates drift lower in 2026.

Exit Drought Extending Fund-Raising Cycles

Only 47 venture-backed IPOs were priced in 2024 versus 174 in 2021, a 73% decline that stalled liquidity. Billion-dollar tech acquisitions also fell 45% as regulatory reviews lengthened by up to two years. Funds are resorting to continuation vehicles to hold mature assets while offering partial liquidity. Secondary-sale volumes jumped 89% as limited partners sought cash in lieu of scarce distributions. Start-ups, meanwhile, are tightening budgets to survive protracted private lifecycles within the venture capital market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Stage of Investment: Scale-up Momentum Accelerates

Scale-up financing is projected to compound at 9.05% through 2031, reflecting the venture capital market size required for USD 50–200 million rounds that propel proven companies to international scale. Early-stage deals still dominate with 48.65% in 2025 because AI innovation pipelines remain robust. Seed rounds have inflated as AI founders demand larger checks to cover compute expenses and elite talent, reshaping expectations across the venture capital market. Breakout deals face tougher diligence as investors prioritize clarity on profitability. Stage distinctions are blurring, with some Series A rounds exceeding USD 100 million when product-market fit is unmistakable.

Early-stage investors are concentrating on capital-efficient models that can weather longer exit horizons without excessive dilution. Scale-up funds hedge risk by co-investing with corporate partners that provide distribution advantages. Seed specialists use rolling-fund structures to lock recurring commitments while remaining agile in the venture capital market. Continuation vehicles now extend fund life for high-performing assets that miss the IPO window. Regulators are updating accredited-investor definitions to reflect a broader pool of sophisticated participants.

By Industry: Robotics Disrupts Enterprise Software Dominance

Enterprise software retained 26.65% of the venture capital market size in 2025 because cloud migration and cybersecurity remain foundational enterprise spend. Robotics, however, is climbing at a 8.86% CAGR as labor shortages in logistics and healthcare catalyze demand for automation. Fintech continues to secure hefty allocations for embedded finance and regulatory-tech platforms that plug into global payment rails. Healthcare technology is reallocating toward AI diagnostics and personalized medicine with clear regulatory pathways. Energy-transition themes span grid-scale storage and carbon capture, reflecting policy-driven incentives within the venture capital market.

Specialized managers are spinning up funds that focus exclusively on quantum computing, space technology, or advanced materials. Robotics investors emphasize full-stack solutions that integrate hardware, software, and data services. Enterprise-software multiples have compressed but remain premium when retention metrics exceed 120% net-revenue retention. Fintech investors are navigating tighter compliance regimes while chasing cross-border scale in under-banked segments. Deep-tech sectors demand longer tenors and larger reserves, prompting syndicates to pool capital for milestone-based follow-ons.

By Exit Type: IPO Revival Challenges M&A Dominance

Mergers and acquisitions captured 48.25% of exits in 2025, confirming their status as the primary liquidity path for the venture capital market. IPO windows are reopening, with a 9.45% growth trajectory as public multiples stabilize, enticing mature unicorns back to the tape. Secondary-sale structures provide interim liquidity for funds that wish to hold outperformers longer. Buyouts by private-equity sponsors are increasing for firms with durable cash flows but limited hyper-growth potential. Write-offs have normalized to historical baselines as investors adopt stricter pre-investment filters.

Antitrust reviews have extended to 24 months, compelling acquirers to either pay higher premiums or provide reverse break-fees. Despite facing regulatory scrutiny, corporate buyers like Microsoft and Amazon remain active, driven by strategic benefits that justify their elevated valuations. Continuation funds are now serving as a link between growth equity and conventional IPO exits. Meanwhile, secondary platforms allow employees to cash in on options without the need to raise new capital. These hybrid exit avenues are broadening the liquidity landscape within the venture capital market.

Geography Analysis

North America held 46.20% venture capital market share in 2025, anchored by Silicon Valley yet increasingly supported by emergent hubs like Austin, Miami, and Toronto. Artificial-intelligence clusters and deep-capital pools continue to draw founders. Canada logged USD 8.3 billion in investments, bolstered by university research commercialization. Mexican fintechs such as Clip attracted multiregional backers as digital payments expanded across Latin America. Regulatory refinements permit innovative fund structures, including rolling funds and DAO-based vehicles.

Asia-Pacific is the fastest-growing region with a 9.92% CAGR, powered by China’s hard-tech resurgence and Japan’s maturing start-up scene. Chinese funds raised USD 23 billion in 2024 after data-security guidance clarified investment boundaries. Japan’s USD 4.7 billion in venture inflows underscores policy success in encouraging entrepreneurship. India’s USD 11.8 billion haul reflects continued fintech and SaaS momentum even amid global tightening. Southeast Asian economies such as Indonesia and Vietnam draw capital to e-commerce and logistics arenas.

Europe attracted USD 89 billion despite macro headwinds, consolidating around London, Berlin, and Stockholm. Deep-tech funds target quantum and advanced materials sourced from university spin-offs. Brexit clarity sustains cross-border flows, though many firms maintain dual operating entities. Germany advances industrial-tech leadership by leveraging engineering heritage. EU regulators refine alternative-investment directives to maintain investor safeguards while supporting the venture capital market.

Competitive Landscape

The top 10 firms control a very low percent of assets, underscoring moderate fragmentation in the venture capital market. Sequoia Capital, Andreessen Horowitz, and SoftBank Vision Fund are diversifying sector coverage and geographic reach to keep pace with sovereign wealth and corporate competitors. Rolling funds and syndicate platforms democratize access, eroding traditional fee structures. Technology adoption differentiates leaders, with AI-driven deal-sourcing tools shortening diligence cycles. Emerging managers exploit underserved niches in Southeast Asia, Latin America, and Africa.

Impact-oriented mandates allow funds to align with environmental and social goals while satisfying return thresholds. Corporate venture arms test hybrid vehicles that invite external limited partners, blending strategic optionality with financial discipline. Compliance frameworks evolve to mitigate governance conflicts when corporates co-invest alongside independents. Traditional asset managers like BlackRock and Fidelity are building private-market franchises, intensifying competition for limited-partner capital. Domain-specific expertise in quantum computing, synthetic biology, and advanced manufacturing is becoming a key moat within the venture capital industry.

Forerunner firms deploy proprietary platforms to assist portfolio companies with talent recruitment, go-to-market acceleration, and regulatory navigation. Secondary-market specialists are adding credit lines to give founders non-dilutive financing alternatives. Sovereign wealth vehicles employ longer investment horizons, positioning them competitively in cap-intensive arenas. Crypto-native funds leverage on-chain analytics for early momentum detection. Overall, the venture capital market is evolving toward a multi-polar structure where thematic specialization and technology leverage determine long-run competitiveness.

Venture Capital Industry Leaders

Sequoia Capital

Andreessen Horowitz

SoftBank Vision Fund

Tiger Global Management

Accel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Amazon announced a USD 4 billion strategic investment in Anthropic, pairing capital with AWS compute credits to fortify AI capabilities.

- October 2024: Tiger Global Management closed a USD 12.7 billion vehicle targeting late-stage technology franchises, its largest raise to date.

- September 2024: Andreessen Horowitz launched a USD 600 million Europe-focused fund to back enterprise software, fintech, and AI start-ups.

- August 2024: General Catalyst completed its merger with Venture Highway, creating a USD 25 billion platform with expanded reach in South and Southeast Asia.

Global Venture Capital Market Report Scope

The Global Venture Capital Market is one of the most widely demanded investment industries for small and medium-sized enterprises. A complete background analysis of the global Venture Capital Market, which includes an assessment of the economy, market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles, are covered in the report. The Global Venture Capital Market is Segmented By Type (Local Investors, International Investor), By Industry (Real Estate, Financial Services, Food & Beverages, Healthcare, Transport & Logistics, IT & ITeS, Education, and Other Industries), and By Geography (North America, Latin America, Europe, Asia-Pacific, and Middle-East and Africa).

By Stage of Investment

| Seed |

| Early Stage |

| Breakout Stage |

| Scale-up |

By Industry

| Health |

| Fintech |

| Enterprise Software |

| Energy |

| Transportation |

| Robotics |

| Other Industries |

By Exit Type

| Initial Public Offering (IPO) |

| Strategic M&A |

| Secondary Sale / Buy-out |

| Write-offs |

By Geography

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Stage of Investment | Seed | |

| Early Stage | ||

| Breakout Stage | ||

| Scale-up | ||

| By Industry | Health | |

| Fintech | ||

| Enterprise Software | ||

| Energy | ||

| Transportation | ||

| Robotics | ||

| Other Industries | ||

| By Exit Type | Initial Public Offering (IPO) | |

| Strategic M&A | ||

| Secondary Sale / Buy-out | ||

| Write-offs | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | ||

| NORDICS | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What CAGR is forecast for global venture capital through 2031?

Aggregate capital is projected to advance at a 13.66% CAGR between 2026 and 2031, taking deployed funds from USD 314.59 billion to USD 596.46 billion.

Which investment stage is expanding the fastest?

Scale-up financing shows the strongest momentum with a 9.05% CAGR as companies raise USD 50–200 million rounds to reach international scale.

How are artificial-intelligence start-ups reshaping seed funding?

Average seed rounds for AI companies climbed to USD 8.7 million in 2024, more than triple the 2019 levels, to cover compute costs and high-priced talent.

Which geography is expected to post the quickest growth rate?

Asia-Pacific is set to record a 9.92% CAGR through 2031, driven by China’s hard-tech rebound and Japan’s maturing start-up ecosystem.

What exit route currently dominates venture-backed liquidity events?

Strategic mergers and acquisitions account for 48.25% of exits, outpacing IPOs, secondaries, and buyouts.

How fragmented is the competitive landscape among venture firms?

The top 10 managers hold roughly 23% of assets, giving the sector a moderate concentration score of 4 on a 10-point scale.

Page last updated on: