Liquid Laundry Detergent Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

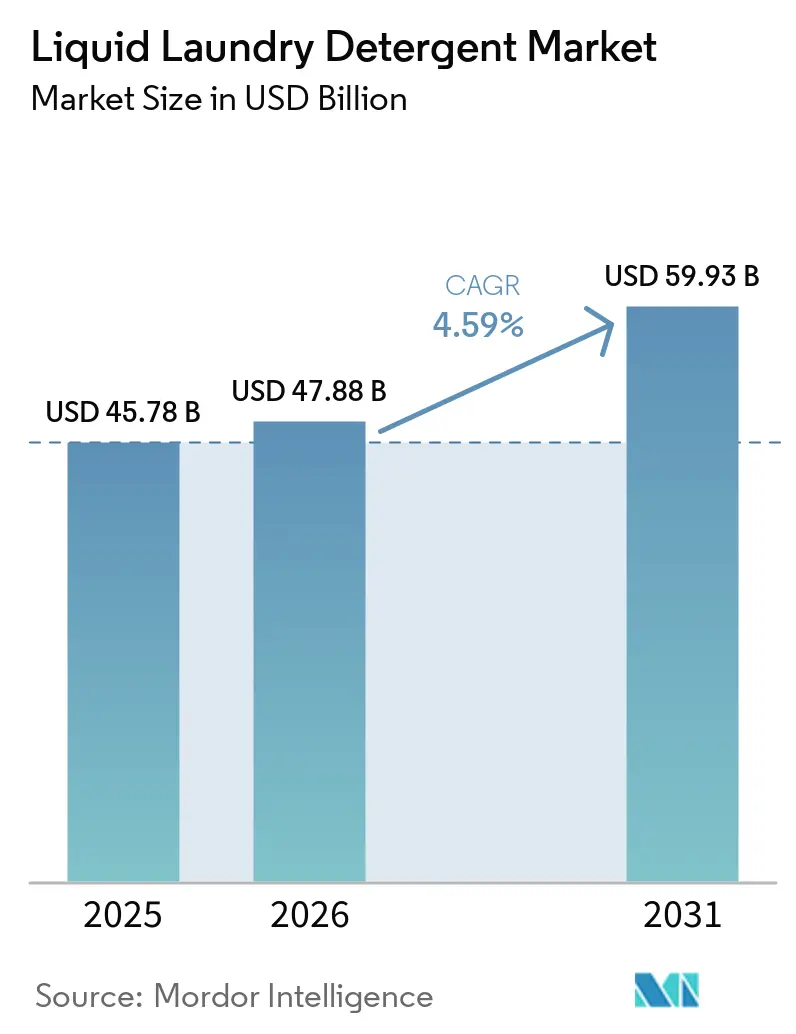

| Market Size (2026) | USD 47.88 Billion |

| Market Size (2031) | USD 59.93 Billion |

| Growth Rate (2026 - 2031) | 4.59% CAGR |

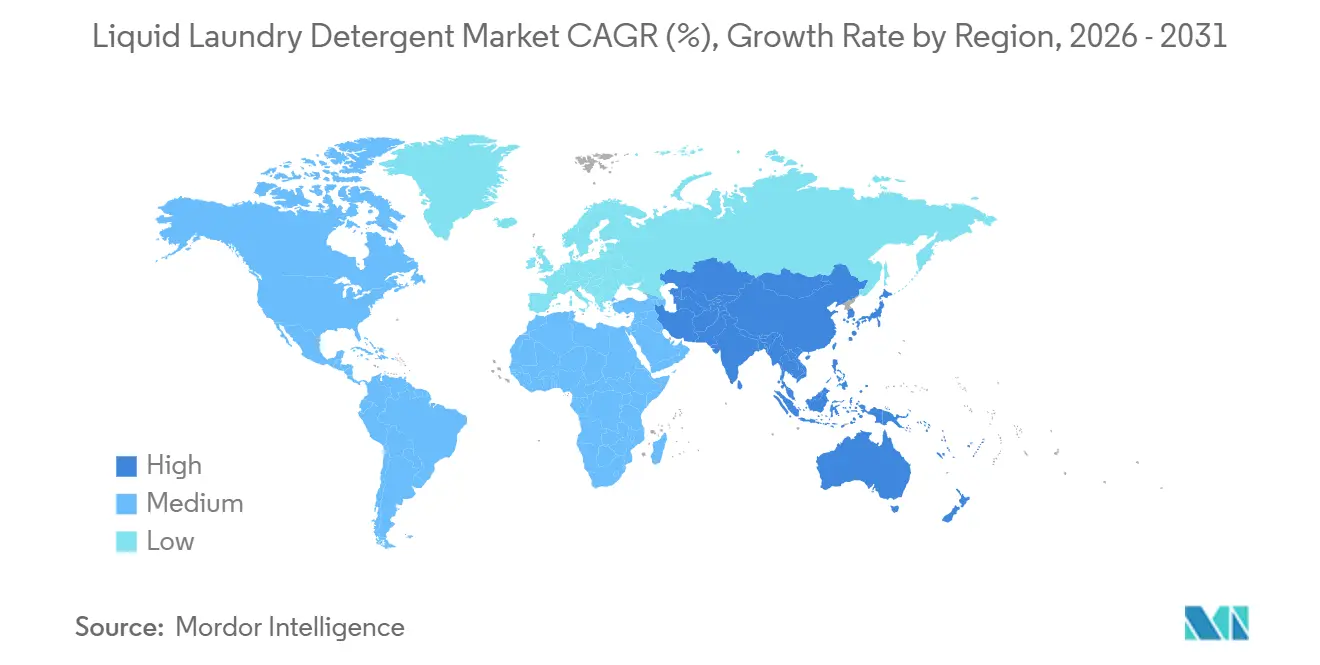

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Liquid Laundry Detergent Market Analysis by Mordor Intelligence

The Liquid Laundry Detergent Market size is projected to expand from USD 45.78 billion in 2025 and USD 47.88 billion in 2026 to USD 59.93 billion by 2031, registering a CAGR of 4.59% between 2026 and 2031. Within this aggregate growth curve, enzyme breakthroughs and highly concentrated liquids are helping incumbent brands defend shelf space, while premium water-free tiles and sheets are winning consumers who pay roughly double per load for sustainability credentials. Automatic-washer penetration, cold-water wash habits, and digital dosing alliances with appliance makers are accelerating value growth, even as precision dosing trims volume demand. Format innovation is also widening price bands: Procter & Gamble’s Tide evo tile retails at about USD 0.48 per load versus USD 0.20 for conventional liquids, confirming headroom for margin expansion despite self-cannibalization. On the cost side, reformulation to meet tighter European preservative rules and to secure certified bio-surfactants is increasing research and development outlays, but it positions early adopters to command higher price points and lower regulatory risk.

Key Report Takeaways

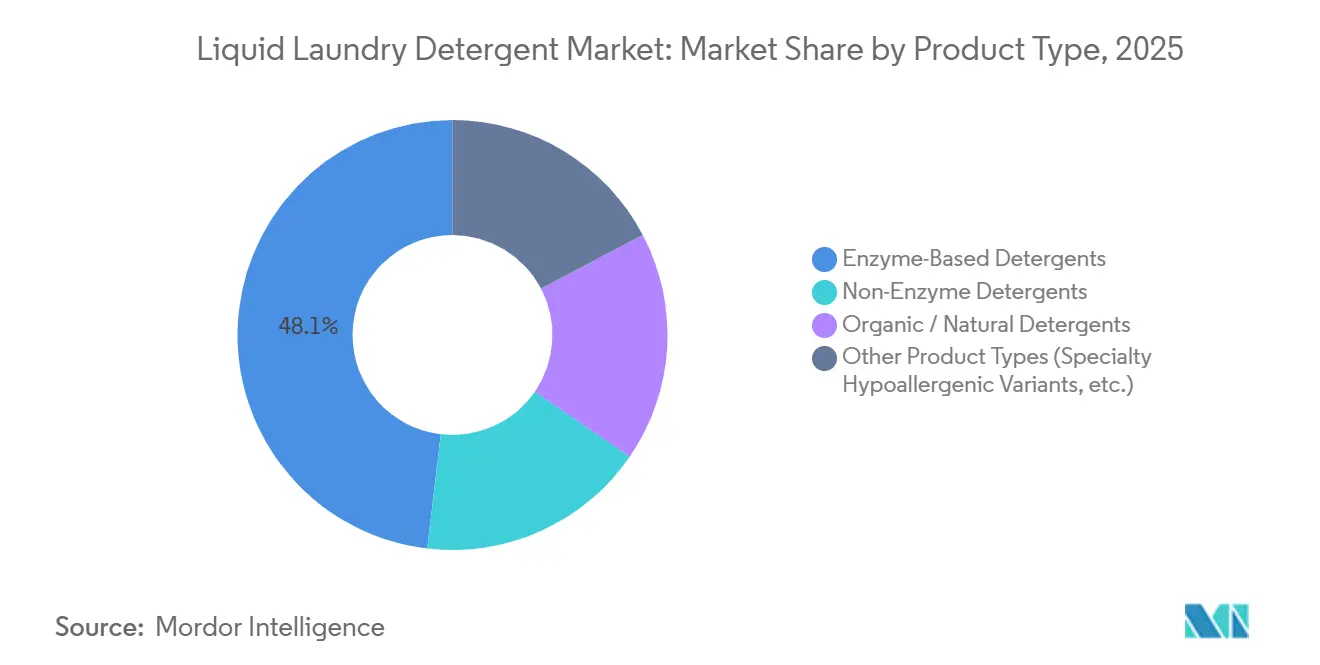

- By product type, enzyme-based liquid detergents captured 48.12% of the Liquid Laundry Detergent market share in 2025. However, the demand for organic/natural detergents is expected to rise with the fastest CAGR of 5.22% during the forecast period (2026-2031).

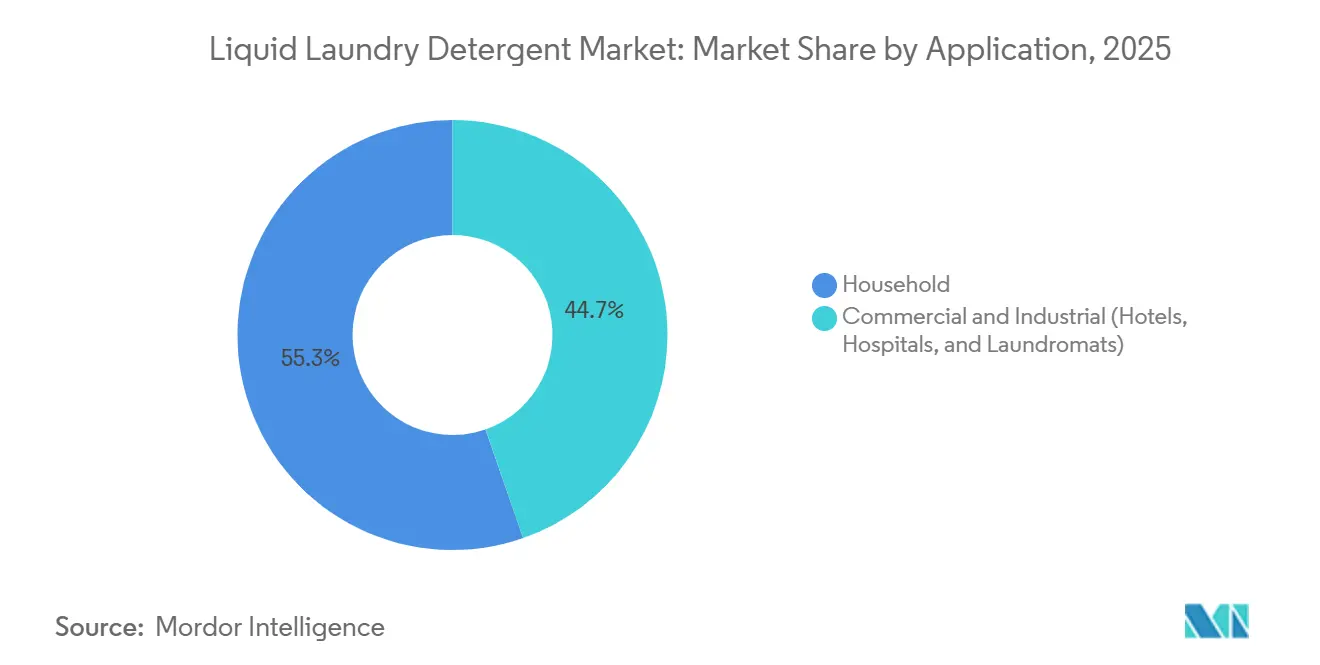

- By application, household washing accounted for 55.34% of the Liquid Laundry Detergent market size in 2025, whereas the commercial segment is advancing at the fastest CAGR of 5.56% to 2031.

- By geography, Asia-Pacific dominated with a 42.24% share of the Liquid Laundry Detergent market size in 2025 and is projected to grow at a 5.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Liquid Laundry Detergent Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urbanization-led laundry volume growth | +0.8% | APAC core, spill-over to Latin America and MEA | Medium term (2-4 years) |

| Penetration of automatic washers in emerging markets | +1.1% | China, India, ASEAN, Brazil, Mexico | Medium term (2-4 years) |

| Subscription-based refill services | +0.3% | North America & EU, early urban APAC | Short term (≤ 2 years) |

| Smart-dispenser/IoT auto-dosing adoption | +0.6% | North America, Western Europe, Japan, South Korea | Medium term (2-4 years) |

| On-premise shared laundry in multifamily housing | +0.4% | North America, Europe, urban China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Urbanization-Led Laundry Volume Growth

Rapid migration toward cities in China, India, and Southeast Asia is moving households from infrequent bucket washes to daily machine cycles, lifting per-capita detergent consumption several-fold[1]Alibaba Group, “Eco-Friendly Laundry Trends on Alibaba.com,” alibaba.com. Urban families launder garments three to five times more often than rural households because of stricter dress codes, heavier pollution, and better utility access. Liquids gain further as rising incomes push consumers away from traditional bars and powders toward convenient dosing. In Southeast Asia, eco-friendly liquid products logged month-over-month e-commerce demand growth of 25.3%, signaling willingness to pay a premium for plant-based claims. Early distribution in tier-2 and tier-3 cities offers brands an opening to lock in loyalty before multinationals saturate shelves.

Penetration of Automatic Washers in Emerging Markets

Mid-income families in Asia-Pacific and Latin America are buying automatic washers that require liquid rather than powder doses, structurally lifting demand for concentrated liquids optimized for cold-water cleaning. Auto-dosing features on mainstream washer models reduce detergent waste by 31%, reinforcing the shift. Commercial laundries, a USD 7-7.5 billion channel, are co-adopting high-efficiency machines, so liquid suppliers that co-design smart-dosing solutions can win long-term contracts and amortize research and development over larger volumes[2]Siemens AG, “i-Dos Precision Dosing Technology,” siemens.com.

Subscription-Based Refill Services

Direct-to-consumer refill programs in reusable containers are proving sticky among urban North American and European households that already subscribe to meal kits and coffee deliveries. Operators charge 10-20% premiums yet earn higher gross margins by avoiding retailer slotting fees. However, route density is critical; without enough pickups per zip code, reverse-logistics costs erode margins. Incumbents testing their own refill pilots could crowd out startups before they scale.

Smart-Dispenser/IoT Auto-Dosing Adoption

Sensor-driven washers from Siemens, LG, and Electrolux meter load size, fabric, and soil, dispensing precise liquid amounts from 1-2 liter reservoirs. Precise dosing cuts household consumption but lets formulators sell higher-margin, machine-specific refills. Japanese and Korean penetration already exceeds 40%, and local detergent makers have forged exclusive refill deals that lock competitors out of the reservoir.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from sheets and pods | -0.7% | North America, Western Europe, Australia | Short term (≤ 2 years) |

| Preservative (MI/MCI) phase-outs tighten reformulation | -0.5% | EU, spill-over to APAC & Latin America | Medium term (2-4 years) |

| Deforestation-linked supply risk in bio-surfactants | -0.3% | Global, acute in Malaysia, Indonesia, Philippines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from Sheets and Pods

Pre-measured sheets and pods are growing faster than liquids by combining dosing simplicity with low-waste packaging. Procter & Gamble’s Tide evo tile, introduced nationwide in February 2026 at USD 0.48 per load, more than doubled initial sales expectations in Colorado tests. Similar launches from Church & Dwight and Seventh Generation are fragmenting shelf space and pressuring legacy bottle formats in Western markets where e-commerce eases format experimentation.

Preservative (MI/MCI) Phase-Outs Tighten Reformulation

European Union (EU) rules now cap methylisothiazolinone in rinse-off goods at 15 parts per million, compelling brands to shift toward costlier alternatives such as phenoxyethanol or benzisothiazolinone. Henkel’s February 2025 liquid relaunch bundled preservative changes with 16% higher concentration and 50% recycled plastic, showing how compliance costs can be recouped through sustainability positioning, but smaller regional players may lack the research and development budget to keep pace.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Enzyme Formulations Anchor Share While Organic Captures Premium Growth

Enzyme-based liquids held 48.12% of the Liquid Laundry detergent market share in 2025, as years of biotech research and development delivered cold-water stain removal that is hard for surfactant-only formulas to match. Lion Corporation’s September 2025 NANOX one relaunch, the brand’s first new enzyme in its history, showcases gene-level cleaning claims that support premium pricing. Non-enzyme variants continue to cede space as consumers equate enzymes with efficacy and energy savings. Organic and natural liquids are expected to grow at a 5.22% CAGR during the forecast period (2026-2031), catalyzed by third-party ecolabels that reassure buyers on biodegradability and skin safety.

Continuous enzyme breakthroughs underpin the segment’s dominance: Novonesis introduced two new protease blends during 2025, and patents from Henkel and BASF describe additives that protect enzyme activity in highly concentrated bases. Meanwhile, International Flavors & Fragrances’ Designed Enzymatic Biomaterials platform entered large-scale use in September 2025, replacing synthetic polyquaterniums with biodegradable polysaccharides that soften fabric, pointing to enzymatic advances beyond mere stain removal.

By Application: Household Leads but Commercial Channels Offer Margin Upside

Household washing generated 55.34% of revenue in 2025, buoyed by more frequent cycles in urban Asia-Pacific and by premiumization in mature Western regions. E-commerce comprised 21.4% of Church & Dwight’s consumer sales in 2025, illustrating how online impulse purchases sustain brand loyalty. Yet private-label liquids and format disruptors crowd retail aisles, squeezing mid-tier brands.

Commercial and industrial laundry, though smaller, is growing at 5.56% CAGR to 2031 as hotels, hospitals, and laundromats adopt bulk concentrated liquids and auto-dosing systems that cut linen damage and labor. Suppliers are bundling detergent with equipment leases, driving sticky multi-year contracts. Tide evo’s water-free tile, initially a household launch, is well-suited to space-constrained laundromats, underscoring cross-channel synergies.

Geography Analysis

Asia-Pacific’s 42.24% share of the Liquid Laundry Detergent market in 2025 is projected to climb on a 5.57% CAGR through 2031, propelled by urbanization, rising incomes, and rapid washer penetration in China, India, and ASEAN. Southeast Asian e-commerce data show 25.3% monthly growth for eco-friendly liquids, suggesting stickiness of sustainable claims among new middle-class buyers. Japan and South Korea, already mature, are upgrading to IoT-enabled dosing that pairs with high-performance enzyme liquids.

North America is demand-mature, so growth hinges on format innovation and premium positioning. Tide evo’s national US roll-out in February 2026 and Church & Dwight’s ARM & HAMMER baking-soda liquid, launched in 2026, illustrate a barbell strategy of premium tiles and value bottles to capture opposite ends of the price spectrum. Nearshoring trends lift Mexican disposable income, nudging households toward liquid conversions.

Europe’s stringent November 2025 detergent law tightens biodegradability thresholds and mandates digital product passports, raising compliance costs but allowing formulators to charge higher shelf prices for verified green claims. Private-label penetration above 30% keeps headline pricing in check, forcing branded players to differentiate via enzyme advances and refill subscriptions already popular in the Nordics.

Competitive Landscape

The Liquid Laundry Detergent market is moderately consolidated. Henkel bundled preservative reformulation with higher concentration and recycled bottles in its February 2025 launch, reducing annual CO₂ emissions by 4,000 metric tons. International Flavors & Fragrances and Kemira formed Alpha Bio to commercialize enzymatic polysaccharides that replace non-biodegradable conditioning polymers, offering detergent makers a turnkey route to greener labels. Private-label growth above 30% in some European categories keeps price ceilings low, while Asia-Pacific challengers such as Blue Moon and Godrej leverage local insights to fend off global entrants.

Liquid Laundry Detergent Industry Leaders

Church & Dwight Co., Inc.

Kao Corporation

Henkel AG & Co. KGaA

Unilever

Procter & Gamble

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Procter & Gamble enhanced its Tide-branded liquid detergent, boosting the formula with a 25% increase in cleaning surfactants to effectively remove tough stains, including grease, even in cold water. Additionally, the upgrade features a 40% increase in non-ionic surfactants, specifically targeting body soils.

- April 2025: Henkel AG and Co. KGaA introduced concentrated formulas and packaging across Persil, All, and Snuggle liquid laundry brands. This enhancement includes an average 16% dose concentration across laundry detergent variants and the integration of 50% recycled plastic content into new bottle designs.

Global Liquid Laundry Detergent Market Report Scope

Liquid laundry detergent is a concentrated, water-based cleaning agent used in washing machines or for handwashing fabrics, formulated to effectively dissolve in all temperatures, especially cold water. It contains surfactants, enzymes, and builders designed to break down stains and suspend dirt, excelling at removing greasy, oily stains without leaving residues.

The Liquid Laundry Detergent market is segmented by product type, application, and geography. By product type, the market is segmented into enzyme-based detergents, non-enzyme detergents, organic/natural detergents, and other product types (specialty hypoallergenic variants, and more). By application, the market is segmented into household and commerical and industrial (hotels, hospitals, and laundromats). The report also covers the market size and forecasts for liquid laundry detergent in 17 countries across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Enzyme-Based Detergents |

| Non-Enzyme Detergents |

| Organic/Natural Detergents |

| Other Product Types (Specialty Hypoallergenic Variants, etc.) |

| Household |

| Commercial and Industrial (Hotels, Hospitals, Laundromats) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Enzyme-Based Detergents | |

| Non-Enzyme Detergents | ||

| Organic/Natural Detergents | ||

| Other Product Types (Specialty Hypoallergenic Variants, etc.) | ||

| By Application | Household | |

| Commercial and Industrial (Hotels, Hospitals, Laundromats) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will the Liquid Laundry Detergent market be by 2031?

It is projected to reach USD 59.93 billion by 2031, expanding at a 4.59% CAGR from 2026-2031.

Which product type holds the largest share of sales?

Enzyme-based liquids dominated with 48.12% share in 2025 thanks to cold-water efficacy.

Which region is growing the fastest?

Asia-Pacific is forecast to grow at a 5.57% CAGR through 2031, driven by rapid urbanization and washer adoption.

What is the main regulatory headwind in Europe?

The November 2025 EU detergents regulation tightens biodegradability rules and limits MI/MCI preservative levels.

Page last updated on: