Brake Fluids Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

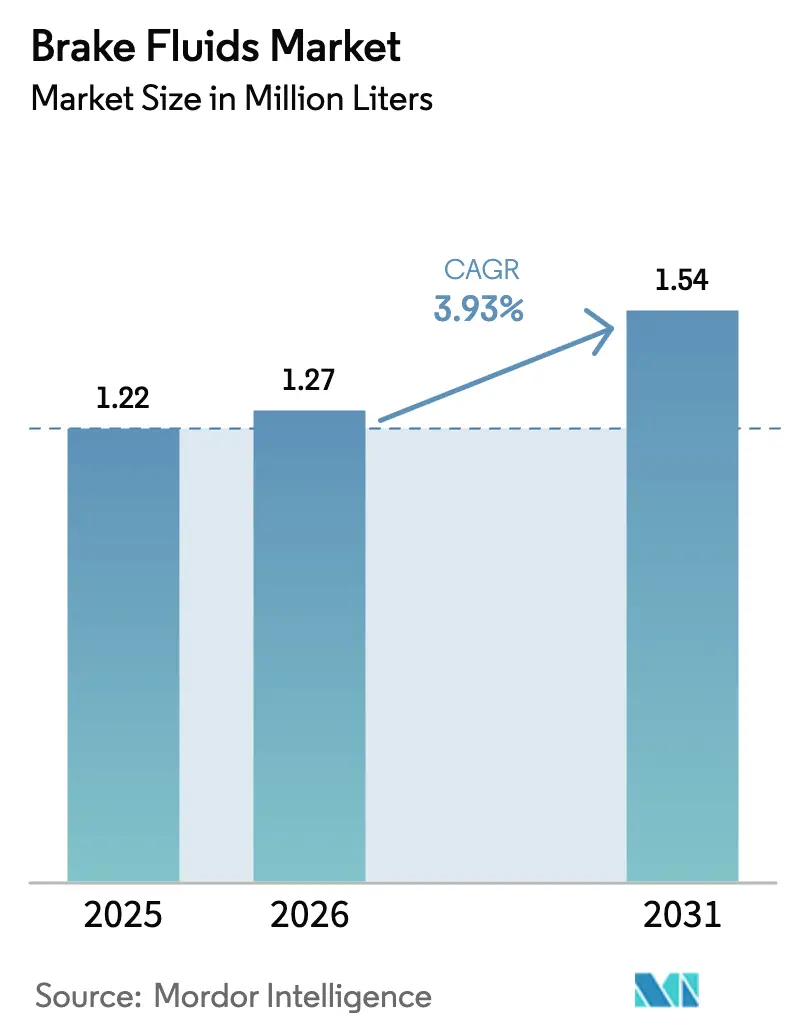

| Market Volume (2026) | 1.27 Million liters |

| Market Volume (2031) | 1.54 Million liters |

| Growth Rate (2026 - 2031) | 3.93% CAGR |

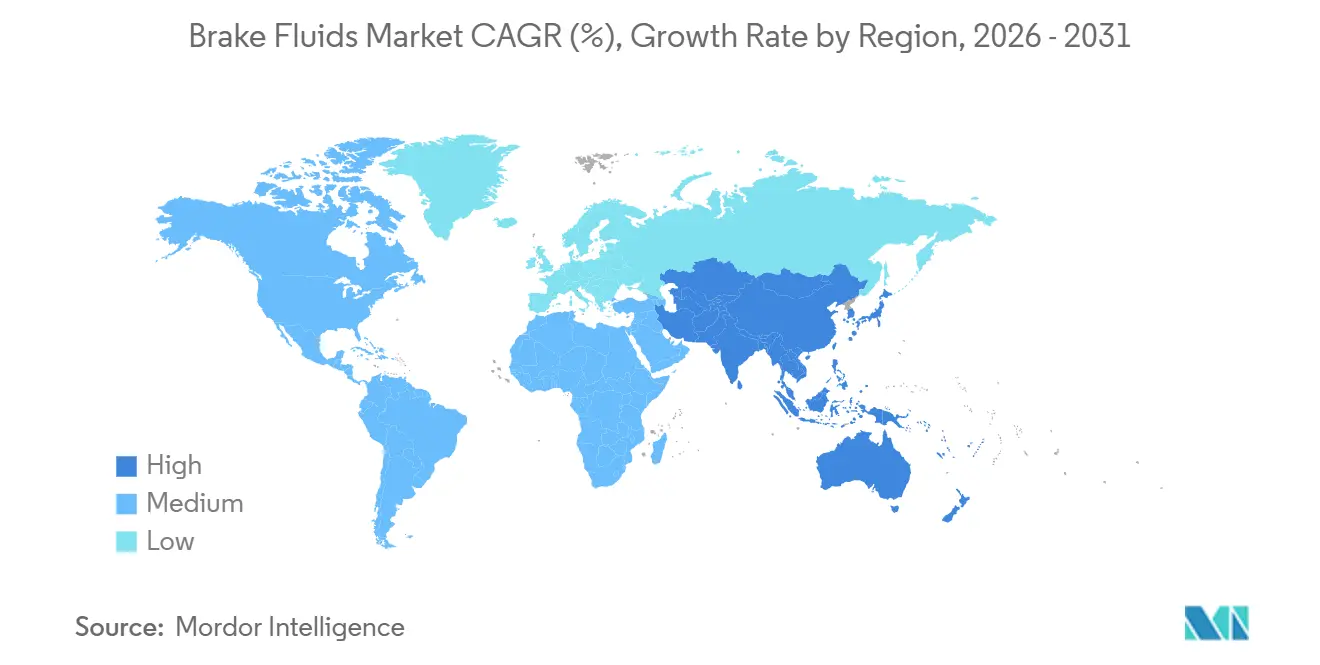

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

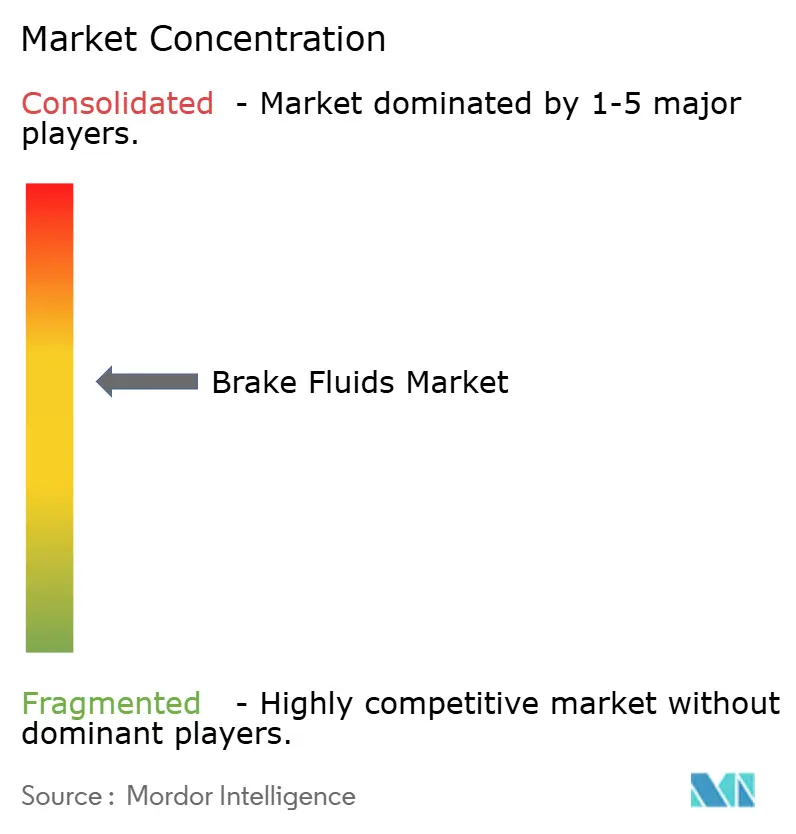

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brake Fluids Market Analysis by Mordor Intelligence

The Brake Fluids Market size is expected to grow from 1.22 Million liters in 2025 to 1.27 Million liters in 2026 and is forecast to reach 1.54 Million liters by 2031 at 3.93% CAGR over 2026-2031. Structural shifts are under way, yet robust vehicle-parc expansion in Asia-Pacific and the ongoing rollout of anti-lock braking systems (ABS) across two-wheelers support near-term growth in the brake fluid market. Rising new-energy vehicle (NEV) registrations in China, which climbed to 11.25 million units in 2024, keep original-equipment (OE) fill volumes healthy because most battery electric vehicles (BEVs) still retain hydraulic backups for redundancy. At the same time, growing adoption of advanced driver-assistance systems (ADAS) is pushing automakers to specify higher-boiling-point DOT 4 and DOT 5.1 fluids, heightening product premiumization. Regulatory drivers, such as India’s nationwide ABS mandate for all two-wheelers from April 2026, further widen demand. However, the accelerating shift to brake-by-wire in BEVs and extended service intervals created by regenerative braking limit upside potential, especially in Europe and North America. Competitive intensity also remains high: large lubricant majors face margin pressure from tier-2 blenders as glycol-ether feedstock prices fluctuate and as sustainability-led reformulations add cost.

Key Report Takeaways

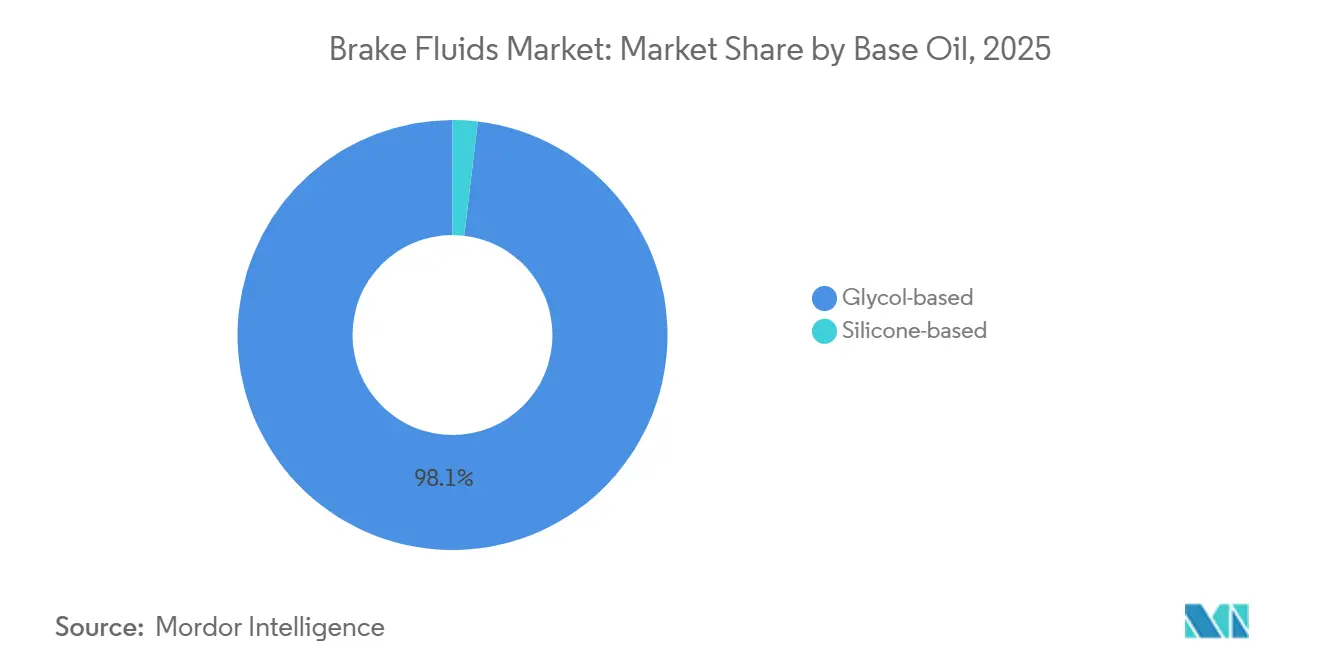

- By base oil, glycol-based held 98.12% brake fluid market share in 2025, while silicone-based DOT 5 is forecast to advance at a 12.10% CAGR through 2031.

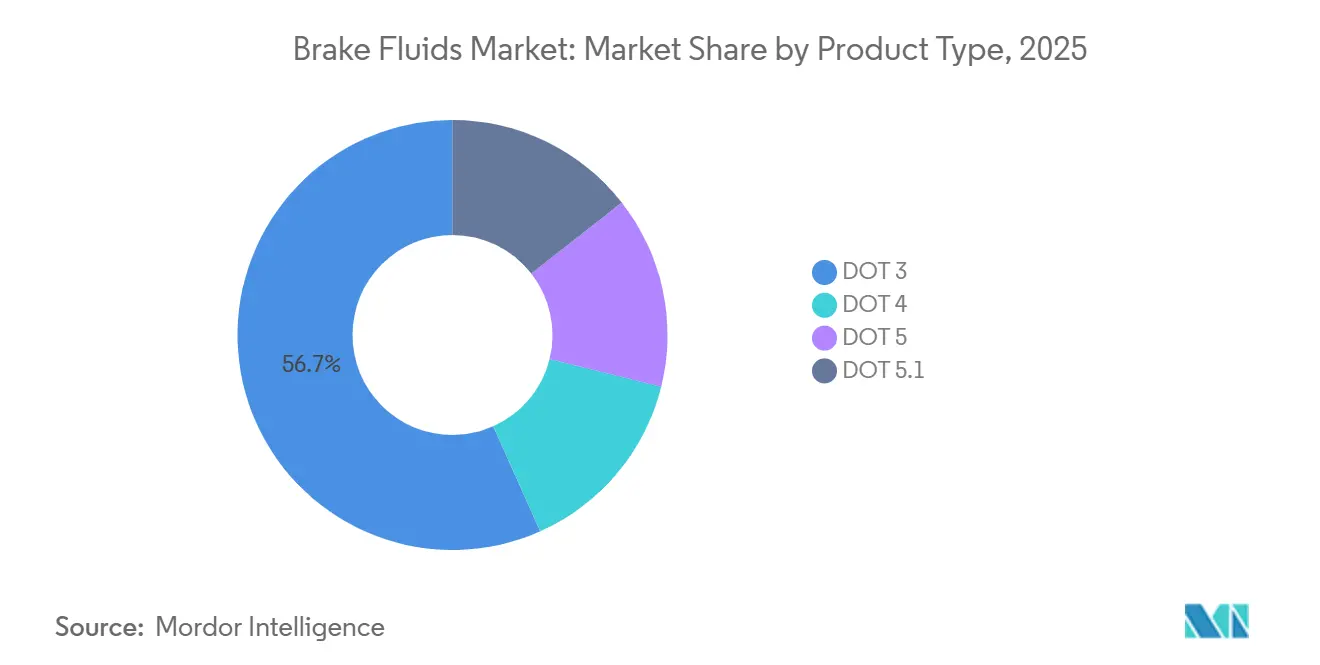

- By product type, DOT 3 captured 56.69% brake fluid market share in 2025; DOT 5.1 is projected to rise at an 11.98% CAGR over 2026-2031.

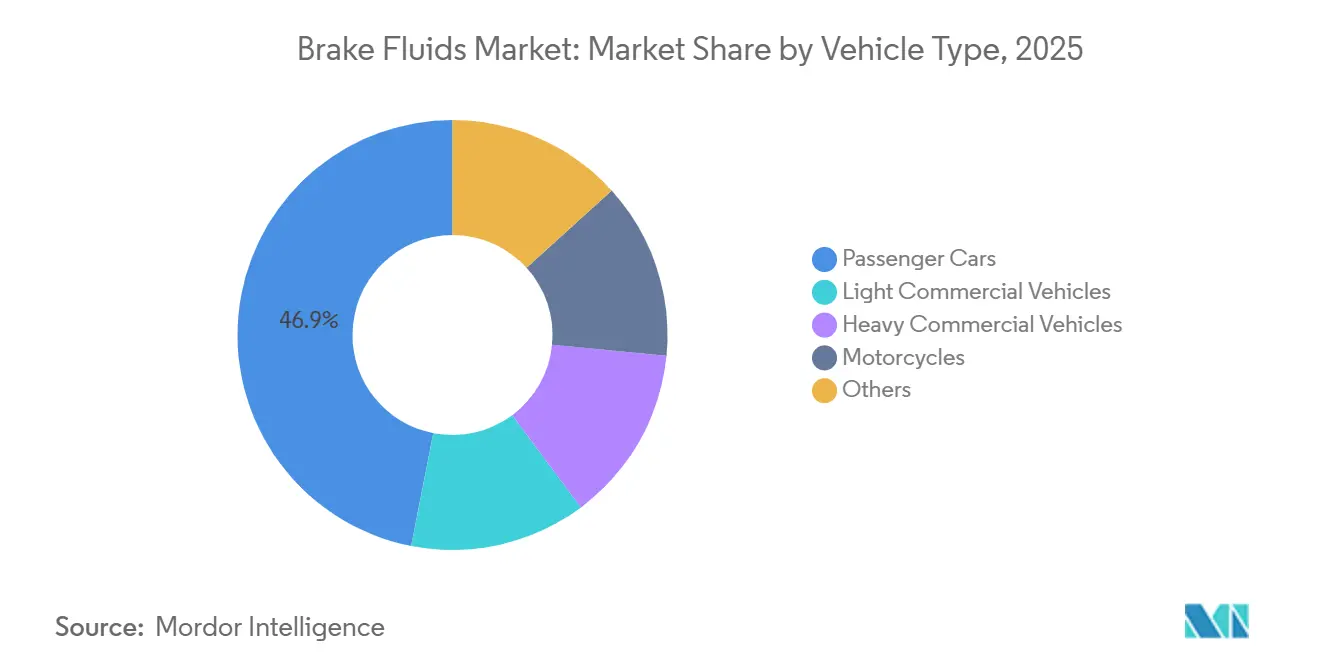

- By vehicle type, passenger cars commanded 46.92% of the brake fluid market size in 2025, whereas motorcycles are set to expand at a 5.22% CAGR to 2031.

- By geography, Asia-Pacific accounted for 47.34% of the brake fluid market size in 2025, and the region is expected to post a 5.19% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Brake Fluids Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Global Vehicle Parc in Emerging Economies | +1.2% | Asia-Pacific core (China, India, ASEAN), spill-over to South America | Medium term (2-4 years) |

| Accelerated Adoption of High-Boiling-Point DOT 4/5.1 Fluids by OEMs | +0.9% | Global, with early adoption in Europe and North America | Short term (≤ 2 years) |

| Tightening ABS/ESC Mandates in 2-Wheeler and LCV Segments | +1.1% | India, ASEAN countries, selective South American markets | Short term (≤ 2 years) |

| Regulatory Drive Toward Low-Viscosity Fluids for ADAS Quick-Response Brakes | +0.5% | North America, Europe, premium segments in Asia-Pacific | Medium term (2-4 years) |

| Niche E-Commerce Aftermarket Platforms Expanding Product Reach | +0.3% | Global, with strongest penetration in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Global Vehicle Parc in Emerging Economies

China’s vehicle stock reached 460 million units by mid-2025, including 36.89 million NEVs, cementing the country’s position as the single largest reservoir of hydraulic brake systems. India produced 31.03 million vehicles in fiscal 2025, 76.57% of which were two-wheelers, a configuration requiring more frequent fluid changes. Used-car transfers in China surpassed 37.5 million in 2024, shifting aftermarket volumes toward independent workshops with lower brand loyalty. Thailand and Indonesia continue to drive light-commercial-vehicle (LCV) growth, sustaining demand where drum brakes dominate. Combined, these fleet dynamics keep the brake fluid market growing even as per-vehicle consumption moderates.

Accelerated Adoption of High-Boiling-Point DOT 4/5.1 Fluids by OEMs

Bosch introduced borate-free DOT 4 E in September 2024, raising dry boiling points beyond 230 °C while sidestepping hazardous-substance labeling. Continental followed with ATE SecuBrake in November 2024, formulating more than 80% of the base from renewable feedstocks. These launches simplify global compliance, particularly under Europe’s REACH regulation, and propel workshops to adopt higher grades for backward compatibility. Valvoline’s 2025 EV Performance Fluids show how suppliers are tailoring DOT 5.1 blends to solve corrosion and noise issues linked to regenerative braking. As a result, premium specifications are set to displace DOT 3 faster than fleet turnover alone would dictate.

Tightening ABS/ESC Mandates in 2-Wheeler and LCV Segments

India will require ABS on all two-wheelers built after April 2026, forcing millions of motorcycles to shift from DOT 3 to DOT 4 within a short window[1]Press Information Bureau, “Mandatory ABS for Two-Wheelers from April 2026,” pib.gov.in . The mandate also raises per-vehicle fluid volumes because dual-channel ABS increases reservoir capacity. Thailand and Vietnam have introduced electronic stability control (ESC) for LCVs, though enforcement outside urban centers remains inconsistent. Counterfeit fluids pose safety risks and may trigger additional quality-assurance measures, which creates an opportunity for branded suppliers to build trust with workshops. Collectively, regulation-driven upgrades add measurable volume to the brake fluid market despite price sensitivity.

Regulatory Drive Toward Low-Viscosity Fluids for ADAS Quick-Response Brakes

Updated SAE J1703 viscosity limits, effective from late 2025, require kinematic viscosities below 1,500 mm²/s at −40 °C to ensure sub-100 ms actuation in ADAS and autonomous emergency braking. UN ECE Regulation 13-H recognizes regenerative braking and demands rapid hydraulic compensation, implicitly favoring DOT 5.1. Valvoline responds with low-temperature, noise-damping formulations for EVs, while Bosch and Pagid emphasize seal compatibility across a wider thermal envelope. As ADAS penetration exceeds 60% of new builds in developed regions by 2027, low-viscosity fluids will capture premium price points. Suppliers unable to invest in advanced additive systems risk marginalization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to Brake-By-Wire and Regenerative Systems in BEVs Reduces Fluid Service Fill | -0.8% | Global, with strongest impact in Europe, China, North America | Medium term (2-4 years) |

| Raw-Material (Glycol-Ether) Price Volatility Squeezing Tier-2 Blenders' Margins | -0.4% | Global, acute in regions dependent on imported feedstocks | Short term (≤ 2 years) |

| Stringent Hazardous-Chemical Transport and Labelling Requirements | -0.2% | Europe, North America, with gradual adoption in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift to Brake-By-Wire and Regenerative Systems in BEVs Reduces Fluid Service Fill

ZF unveiled a dry brake-by-wire module in late 2023 that removes hydraulic circuits altogether, promising shorter stopping distances and lighter assemblies. Autocar’s 2025 review anticipates mainstream adoption of such systems in premium BEVs by 2028-2030. Even when hydraulics are retained, regenerative braking lowers friction-brake use, pushing fluid-change intervals from 24 to as high as 48 months, which halves aftermarket demand per vehicle. China’s NEV fleet already tops 36.89 million units, indicating early signs of volume erosion, though dual-system designs still secure baseline usage. Suppliers must therefore hedge by investing in EV-specific formulations and by diversifying into non-automotive glycol channels.

Raw-Material (Glycol-Ether) Price Volatility Squeezing Tier-2 Blenders’ Margins

Diethylene and triethylene glycol, which form up to 80% of DOT 3 and DOT 4 blends, track ethylene oxide costs that swing with refinery outages and polyester demand. Spot prices shifted 20-30% quarter-over-quarter during 2024-2025, challenging independent blenders without long-term contracts. BASF broke ground on a 46,000 metric-ton methyl-glycol plant in Zhanjiang in March 2024 to secure captive supply and mitigate volatility[2]BASF, “Zhanjiang Integrated Site Expansion,” basf.com . Smaller players have resorted to cut-rate formulations, but this practice erodes confidence among workshops and may attract regulatory scrutiny under ISO 4925 audits. Persistent volatility encourages forward-integration strategies and favors producers with chemical-segment scale economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Base Oil: Glycol Dominance Faces Niche Silicone Incursion

Glycol-based fluids controlled 98.12% of global volume in 2025, driven by compatibility with legacy systems and a lower landed cost versus silicone alternatives. Glycol-based products typically combine polyglycol ethers with corrosion inhibitors, delivering reliable hygroscopic performance that prevents moisture pooling. The brake fluid market size associated with glycol formulations is forecast to expand steadily, although its share will dip marginally as specialty niches mature. Silicone-based DOT 5 recorded a limited but notable presence in vintage motorcycles and military vehicles. Its hydrophobic property avoids moisture-triggered corrosion, supporting multi-year service intervals. Nonetheless, incompressibility and higher viscosity historically hindered widespread ABS compatibility.

Silicone’s outlook is shifting. Engineers for brake-by-wire platforms see potential in silicone’s thermal stability because electronic actuation diminishes the need for progressive pedal feel. The segment is projected to grow at a healthy 12.10% CAGR to 2031, albeit from a small base. Suppliers such as Motul have positioned premium silicone blends at performance enthusiasts seeking year-round resilience. Meanwhile, BASF’s new feedstock facility tightens cost leadership for glycol producers, making volume displacement an uphill task. Blenders that offer dual-chemistry portfolios will be best placed to capture emerging demand without cannibalizing their core glycol franchise.

By Product Type: DOT 3 Erosion Accelerates Amid Premium Shift

DOT 3 held 56.69% of global volume in 2025, but its 205 °C dry boiling point no longer satisfies rising thermal loads from stability control systems. Commodity position and price sensitivity keep DOT 3 relevant in drum-brake applications, particularly across older fleets in India, ASEAN, and parts of Africa. Yet the April 2026 two-wheeler ABS mandate in India will rapidly convert a large portion of this base to DOT 4, leading to an anticipated step-down in DOT 3 demand over the next 24 months. Racing and high-performance niches already treat DOT 3 as obsolete, favoring boutique blends with higher boiling points.

DOT 4 and DOT 5.1 are converging in specifications, but viscosity remains the differentiator. DOT 5.1’s 900 mm²/s limit at −40 °C enables smoother ADAS actuation in Nordic and alpine climates. With automakers choosing DOT 5.1 to future-proof vehicle platforms, its volume is set to rise at an 11.98% CAGR to 2031. Premiumization adds value: price premiums of 15-20% over DOT 4 have proven sustainable in North America and Europe. The brake fluid market size attached to DOT 5.1 is therefore expected to grow faster than overall demand, widening margins for formulators with advanced additive packages. DOT 3 suppliers, largely regional blenders, face a shrinking addressable market and may pivot toward export or industrial glycol channels.

By Vehicle Type: Passenger Cars Lead, Motorcycles Accelerate

Passenger cars generated 46.92% of global fluid demand in 2025, reflecting higher reservoir capacities and the prevalence of four-wheel disc brakes. Although BEV penetration in developed markets dampens replacement frequency, OE fill volumes remain substantial in Asia-Pacific, where internal-combustion engines still dominate new sales. Disc-brake equipped SUVs further lift per-vehicle fluid requirements because of larger calipers. Hence, the brake fluid market continues to derive scale from passenger cars even as growth moderates.

Motorcycles present the fastest-rising opportunity. India alone produced 23.76 million units in fiscal 2025, and the impending ABS mandate will push hydraulic demand upward. The brake fluid market size for motorcycles is forecast to expand at a 5.22% CAGR through 2031, outstripping the overall pace. Dual-channel ABS adds reservoir volume and mandates at least DOT 4, creating an immediate specification upgrade. Light commercial vehicles (LCVs) and heavy commercial vehicles (HCVs) rely on hydraulic drum brakes in emerging markets, tying usage to freight intensity. Air-over-hydraulic hybrids entering Europe and China optimize thermal management and require DOT 5.1 to handle repeated downhill braking events, shifting value from volume to formulation complexity.

Geography Analysis

Asia-Pacific captured 47.34% of the brake fluid market size in 2025 and is on track for a 5.19% CAGR through 2031. China’s 460 million vehicle parc anchors OE and aftermarket volumes, while India’s regulatory momentum around ABS pushes demand for higher-grade fluids. ASEAN markets, notably Thailand and Indonesia, continue to add LCV capacity and maintain drum-brake architectures that demand regular fluid replacement. High humidity and dusty conditions in Southeast Asia also shorten service intervals, reinforcing volume growth.

North America and Europe contend with faster BEV uptake, which lengthens change cycles. Nonetheless, specification premiumization partially offsets the volume drag. U.S. automakers have standardized DOT 5.1 for new ADAS-equipped models since late 2025, raising average selling prices. Europe’s REACH requirements accelerate adoption of borate-free formulations, encouraging early movers like Bosch and Continental to defend margin. UN ECE Regulation 13-H ensures hydraulic backups in vehicles with regenerative braking, protecting baseline fluid use even as brake-by-wire trials expand.

South America and the Middle East and Africa combined represent a smaller slice of the brake fluid market, yet niche conditions offer upside. Brazil’s ethanol-heavy fuel mix permeates vapor lines and can contaminate braking systems, prompting more frequent fluid replacement. Gulf Cooperation Council markets in the Middle East require high dry boiling points due to ambient temperatures above 50 °C in summer. Africa’s growing e-commerce logistics sector relies on LCV fleets that retain hydraulic drums, creating localized demand spikes. Suppliers that tailor packaging sizes and fight counterfeit penetration can secure competitive advantages in these underserved regions.

Regulatory Landscape

Brake fluids are governed by a combination of performance standards and chemical-management rules that affect formulation, labeling, and market access. In the United States, NHTSA administers FMVSS 116 (49 CFR 571.116), which specifies DOT 3/DOT 4/DOT 5 performance requirements and includes container sealing and labeling rules that aftermarket brands must meet to sell at scale. Internationally, ISO 4925:2026 was published on June 8, 2026, updating specifications for non-petroleum-based brake fluids used in hydraulic brake and clutch systems and reinforcing the need for validated dry and wet boiling point and viscosity performance.

In Europe, compliance pressure also comes from chemical regulations such as REACH and CLP (EC 1272/2008), where hazard classification and safety data sheet (SDS) accuracy shape product positioning, particularly for borate-containing chemistries that can trigger more stringent labeling. This has supported the industry shift toward borate-free and renewable-content DOT 4 formulations highlighted in the competitive landscape, while increasing documentation and audit demands for blenders supplying both OEM and workshop channels.

Value Chain Analysis

The value chain begins upstream with petrochemical and specialty-chemical producers supplying glycol ethers, polyalkylene glycols, borate esters (where used), and additive packages such as corrosion inhibitors, antioxidants, and lubricity improvers. Midstream, brake-fluid manufacturers and lubricant majors carry out tightly controlled blending and purification (filtration/distillation) steps, then validate performance through testing focused on dry and wet boiling points and low-temperature viscosity, with test alignment commonly referenced to FMVSS 116 and ISO 4925. Access to consistent, high-purity glycol streams remains a key constraint, and volatility in glycol-ether-related inputs is a recurring margin pressure point for tier-2 blenders.

Downstream, products reach OEM fill and parts networks, national distributors, e-commerce marketplaces, and service workshops, where installation practices and counterfeit risks influence brand outcomes. OEM approvals and region-specific certification and labeling are the main gates for higher-grade DOT 4/DOT 5.1 products, while packaging and compliance, including sealed containers and correct labeling, are needed to prevent channel rejection and protect workshop trust. Co-development between brake-system suppliers and fluid formulators, paired with tighter documentation control under REACH/CLP in Europe, is concentrating influence among suppliers that can fund testing, audits, and stable feedstock sourcing.

Competitive Landscape

Global supply remains moderately concentrated, with the top 5 suppliers - BP Castrol, ExxonMobil, FUCHS, TotalEnergies, and Valvoline - controlling approximately 55% of 2025 volume. Multinationals lean on OE homologation, wide distributor footprints, and in-house additive science to sustain premium pricing. Tier-2 blenders compete by undercutting DOT 3 and standard DOT 4 prices, but cost leadership is eroding because of feedstock volatility and tightening chemical transport rules.

Sustainability differentiation is gaining currency. Continental’s ATE SecuBrake uses over 80% renewable raw materials, while Bosch’s DOT 4 E removes borates to avoid GHS reproductive-toxicity labeling. Such features command up to 25% price premiums in Europe and are likely to migrate to North America as ESG metrics enter procurement scorecards. Vertical integration is another trend: BASF’s Zhanjiang plant secures methyl-glycol supply, insulating the company from spot-market swings and enabling competitive tenders in Asia. M&A is reshaping the ecosystem; ABC Technologies’ 2025 acquisition of TI Fluid Systems created TI Automotive, an integrated brake-line and reservoir manufacturer with leverage to influence fluid specifications at the design stage. Digital service devices, such as LIQUI MOLY’s Brake Fluid Tronic, also reach workshops seeking labor savings, indirectly boosting premium fluid uptake where device algorithms recommend higher-boiling-point products.

White-space innovation targets EV-specific needs. Valvoline’s EV Performance Fluids range optimizes low-temperature viscosity and noise damping to address the silent cabin environment of BEVs. Motul markets racing-grade blends to track-day users who demand 300 °C-plus dry boiling points. These niches do not yet swing global volume, but they set pricing benchmarks and brand perception, forcing mainstream suppliers to keep R&D pipelines active. Overall, suppliers that invest in renewable feedstocks, digital diagnostics, and EV-tailored chemistries are best positioned to capture share as the brake fluid market evolves.

Brake Fluids Industry Leaders

Exxon Mobil Corporation

TotalEnergies

BP p.l.c (Castrol)

FUCHS

Valvoline Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Standard upgrades and regulatory convergence are opening whitespace for suppliers that can meet tighter viscosity targets and electronic-braking performance needs while simplifying compliance across regions. ISO 4925:2026, published June 8, 2026, sets an updated global benchmark for non-petroleum-based brake fluids. China also issued GB 12981-2025 in December 2025 for motor-vehicle brake fluids (effective January 1, 2027), which pushes suppliers to align test methods and documentation for large-volume markets. In parallel, SAE J1704-2025 (released October 2025) added a friction-induced wear test that better reflects electronic braking system and brake-by-wire operating conditions, supporting differentiation beyond boiling point alone.

On the supply side, cost stabilization and localized feedstock access remain a practical opportunity, especially across Asia-Pacific where the vehicle parc base is large and premiumization is gaining traction. BASF began construction in March 2024 of a 46,000 metric ton per year methyl glycols plant at Zhanjiang, China, to supply key brake-fluid precursors, and similar upstream integration or long-term sourcing approaches can help blenders stabilize costs and support OEM consistency requirements. On the demand side, India’s ABS mandate for all two-wheelers from April 2026 supports grade migration toward DOT 4 in a high-volume segment, while EU REACH/CLP-driven reformulation work favors suppliers with borate-free or lower-hazard labeling pathways and strong SDS governance.

Recent Industry Developments

- July 2026: Valvoline Global Operations expanded its collaboration with Horse Powertrain (the Geely, Renault, and Aramco joint venture) to supply lubricant solutions and support a broader aftermarket footprint in Asia-Pacific. The tie-up strengthens channel access in a region that leads global brake-fluid consumption and reinforces bundled-fluid strategies that can influence workshop and distributor portfolios.

- November 2025: Ravensberger Schmierstoffvertrieb GmbH launched its R 340+ racing brake fluid with DOT 4 approval and a stated 342 C dry boiling point for high-performance applications. This reinforces premium niches that set performance benchmarks and can pull higher-grade fluids into enthusiast and specialist workshop demand.

- November 2024: Continental AG introduced ATE SecuBrake, a DOT 4 brake fluid formulated with over 80% renewable base stocks and designed without borate esters. The product supports sustainability-led procurement and offers a compliance-friendly pathway in markets influenced by REACH and CLP labeling considerations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers brake fluid used in hydraulic braking systems, measured by the fluid volume sold and consumed across original equipment fill and aftermarket top-ups in road vehicles. It includes common DOT grades and base chemistries that meet prevailing safety and performance references.

Scope exclusions: We exclude brake system hardware, brake pads and rotors, and wider automotive lubricants that are not used as brake fluid.

Segmentation Overview

- By Base Oil

- Glycol-based

- Silicone-based

- By Product Type

- DOT 3

- DOT 4

- DOT 5

- DOT 5.1

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Motorcycles

- Others

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research set the guardrails for the model by mapping where brake fluid demand comes from and how it typically tracks with the vehicle parc and service cycles. We used public sources such as vehicle production and registration statistics from organizations like OICA and national transport agencies, road safety and inspection publications, and standards bodies that publish DOT and brake fluid performance references. We also reviewed trade and customs statistics such as UN Comtrade to understand cross-border flows for chemical intermediates and finished fluids in key regions.

We relied on company annual reports, investor decks, and product technical data sheets to understand grade mix and the pace of product transitions such as DOT 3 to DOT 4 in certain applications. Patent databases were checked to spot major shifts in formulations and compatibility claims, since those changes can alter average replacement cycles. Where available, paid subscription materials covering company financials and news were used to confirm plant expansions, distribution changes, and regional demand signals. These sources are illustrative and not exhaustive, and many other public and paid references were also used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on validating real-world consumption patterns, especially how much fluid is used per vehicle in OE fill, how often it is replaced, and what drives the share of DOT grades by vehicle category. We spoke with a mix of fluid formulators, distributors, service channel experts, and fleet maintenance contacts across major consuming regions so gaps from desk research could be closed and assumptions could be adjusted before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 16% | APAC: 48% |

| Mid tier: 50% | Functional/Unit leaders: 25% | EMEA: 29% |

| Smaller Players: 21% | Managers: 59% | Americas: 23% |

Market-Sizing & Forecasting

Our sizing is built using a top-down demand pool reconstruction where the global vehicle parc, annual miles traveled trends, and service interval guidance are converted into a yearly brake fluid consumption volume by region. Since the market is reported in liters, the model is anchored on vehicle stock by type, estimated hydraulic brake penetration where needed, and typical drain and fill volumes per service event.

To keep the totals realistic, we corroborated results with selective bottom-up checks such as sampled channel volume discussions, distributor mix insights, and a simple ASP times volume conversion to sanity-check what the implied value would look like for major regions. Key inputs that were tested and refreshed during modeling include the share of vehicles serviced in the organized versus independent channel, the mix of DOT 3, DOT 4, and higher grades, average replacement frequency in hot and humid climates, and the shift in new vehicle build toward safety features that still rely on hydraulic backup systems. For forecasting, we used scenario analysis guided by expert views on vehicle parc growth, two-wheeler and passenger car servicing intensity, and the pace at which longer drain intervals are adopted, which is then rolled into the regional volume outlook through 2031. Where bottom-up signals were thin in smaller markets, we applied proxy service intensity indicators and then re-checked the output against import dependency and vehicle parc patterns.

Data Validation & Update Cycle

Validation was done through step-by-step checks so large variances could be explained before sign-off. Analysts compared regional outputs against independent signals such as vehicle parc growth, service and inspection cadence, and trade flow direction to confirm that the implied consumption was reasonable. When an outlier appeared, assumptions like drain intervals, grade mix, or climate-adjusted service frequency were revisited, and in some cases primary contacts were re-approached to confirm the change.

A multi-step internal review was followed so the logic, calculations, and units remained consistent across regions and years. Reports are refreshed annually, and interim updates are triggered when material events occur such as regulation changes, sharp shifts in vehicle production, or supply disruptions that can affect availability and pricing. Before delivery, a final analyst pass is completed so the output reflects the latest confirmed inputs.

Mordor Intelligence's Brake Fluids Market Estimate Compared With Other Published Estimates

Published market sizes for brake fluids often do not match because teams choose different units, boundaries, and update timing, and those choices flow through the model. The spread can look large even when everyone is describing the same end use, since some estimates lean on value in USD and others prioritize volume in liters.

Key gaps typically come from whether the scope is limited to brake fluids only or expanded to include adjacent hydraulic fluids, whether OEM fill is separated from aftermarket consumption, and how DOT grade mix is handled as vehicles age. By tracking vehicle parc changes, service interval behavior, and grade mix shifts, Mordor Intelligence converts the market into liters first and then checks the implied pricing logic, which reduces overstatement that can come from applying a single global ASP trend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.00 B (2025) | |

| Trade Publisher A | USD 3.52 B (2024) | Value-first estimate, and the public summary does not clarify if hydraulic clutch fluids or non-automotive uses are bundled, which can inflate the addressable pool versus a brake-fluid-only view. |

| Global Data Publisher B | USD 1.82 B (2024) | Uses a vehicle brake fluid framing with mixed end uses and a revenue focus, and the year-to-year translation from volume to value depends heavily on assumed average pricing and currency timing. |

The table shows that differences are mainly driven by what is counted and how liters are converted into dollars, rather than a disagreement on underlying vehicle activity. A transparent model that ties demand to vehicle parc, service cycles, and DOT grade adoption makes the estimate easier to reproduce and easier to pressure-test when conditions change.

Key Questions Answered in the Report

How large will global demand for brake fluid be by 2031?

Consumption is forecast to reach 1.54 million liters in 2031, expanding at a 3.93% CAGR from 2026 levels.

Which region generates the highest brake fluid volumes?

Asia-Pacific leads with 47.34% of 2025 demand and will keep growing at a 5.19% CAGR through 2031, driven by China and India.

What product grades are gaining popularity?

DOT 4 and DOT 5.1 are displacing DOT 3 because they meet higher boiling-point and low-temperature viscosity requirements for ABS and ADAS.

How will brake-by-wire influence future fluid sales?

Fully dry brake-by-wire systems eliminate hydraulic circuits, which could reduce global brake fluid volumes by up to 0.8 percentage points on CAGR forecasts over the medium term.

Page last updated on: