Liquid Detergent Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

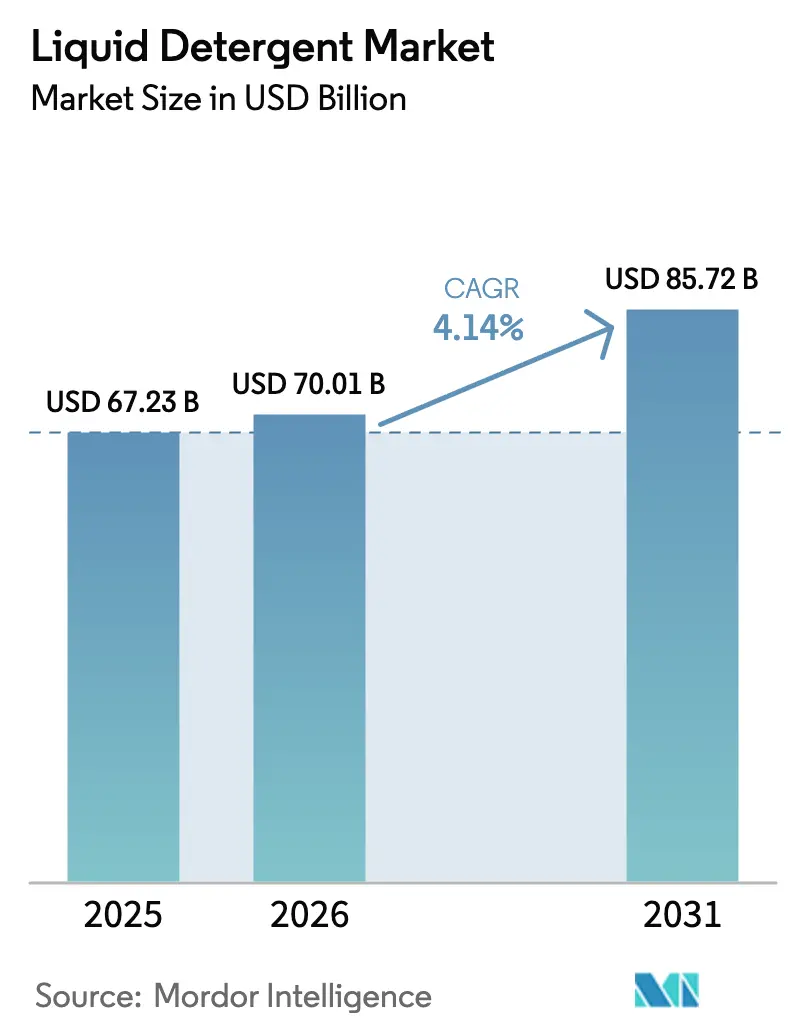

| Market Size (2026) | USD 70.01 Billion |

| Market Size (2031) | USD 85.72 Billion |

| Growth Rate (2026 - 2031) | 4.14% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Liquid Detergent Market Analysis by Mordor Intelligence

The liquid detergent market size was valued at USD 67.23 billion in 2025 and estimated to grow from USD 70.01 billion in 2026 to reach USD 85.72 billion by 2031, at a CAGR of 4.14% during the forecast period (2026-2031). This growth trajectory reflects the industry's adaptation to evolving consumer preferences for convenience, sustainability, and superior cleaning performance across both household and commercial applications. Manufacturers are responding with concentrated formats that lower per-wash costs, refill packaging that reduces plastic intensity, and plant-based surfactants that meet tightening eco-labels. Competitive pressure stays intense as multinationals protect shelf space and niche challengers build direct-to-consumer footholds that bypass traditional retailers. Regulatory pressures are intensifying across key markets, with the EU revising Detergent Regulation (EC No 648/2004) to align with the European Green Deal, emphasizing biodegradability and digital labeling requirements. California's adoption of regulations targeting nonylphenol ethoxylates in laundry detergents, effective October 2024, signals broader environmental compliance requirements.

Key Report Takeaways

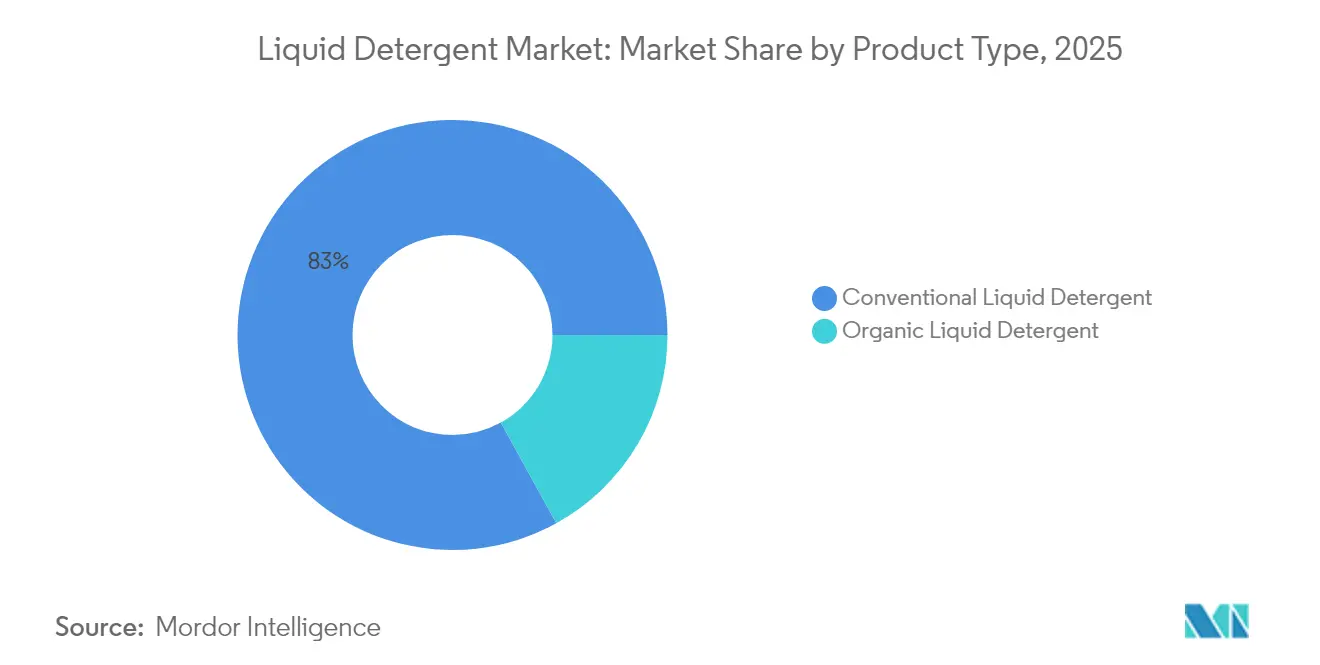

- By product type, conventional liquids led with 83.02% of liquid detergent market share in 2025, while organic variants are on track for a 4.39% CAGR through 2031.

- By application, laundry held 64.01% of the liquid detergent market size in 2025, whereas dishwashing is forecast to rise at 4.73% between 2026 and 2031.

- By end user, adults accounted for 93.42% of the liquid detergent market share in 2025, but the children’s segment will expand at 5.05% CAGR to 2031.

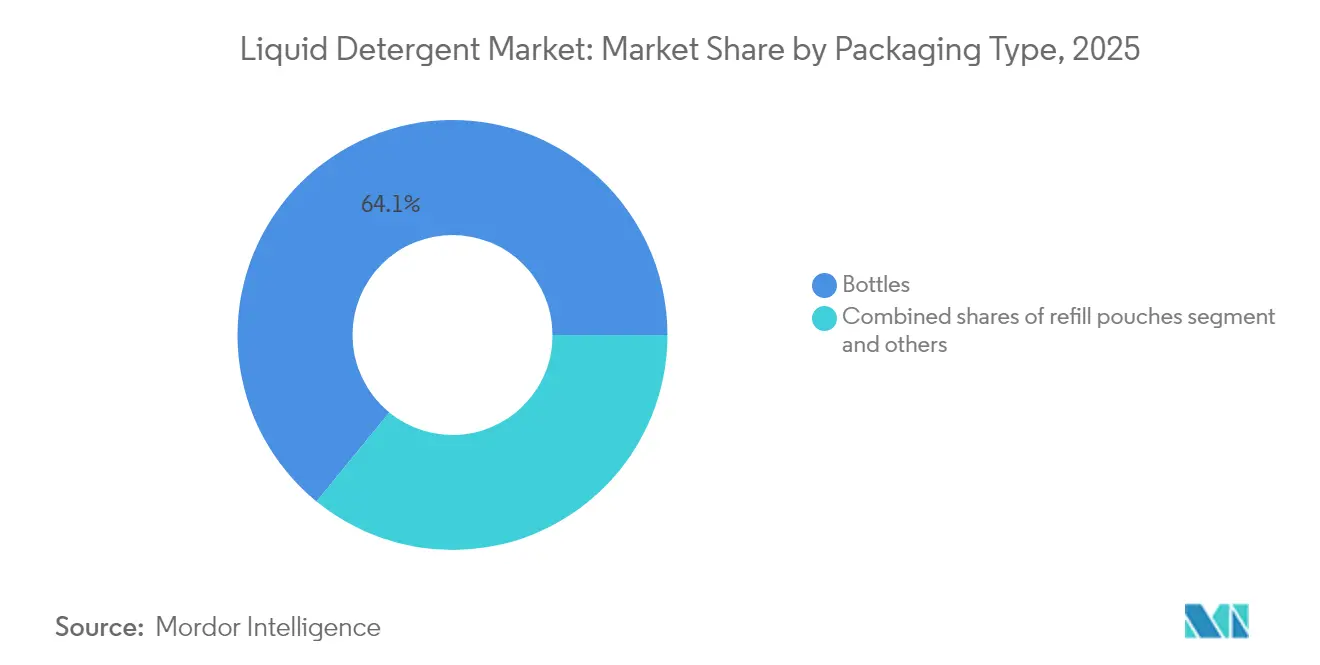

- By packaging, traditional bottles kept 64.10% of the liquid detergent market size in 2025, and refill pouches are climbing at a 5.45% CAGR.

- By distribution channel, supermarkets and hypermarkets captured 42.05% revenue in 2025, yet online stores are pacing the fastest at 5.62% CAGR.

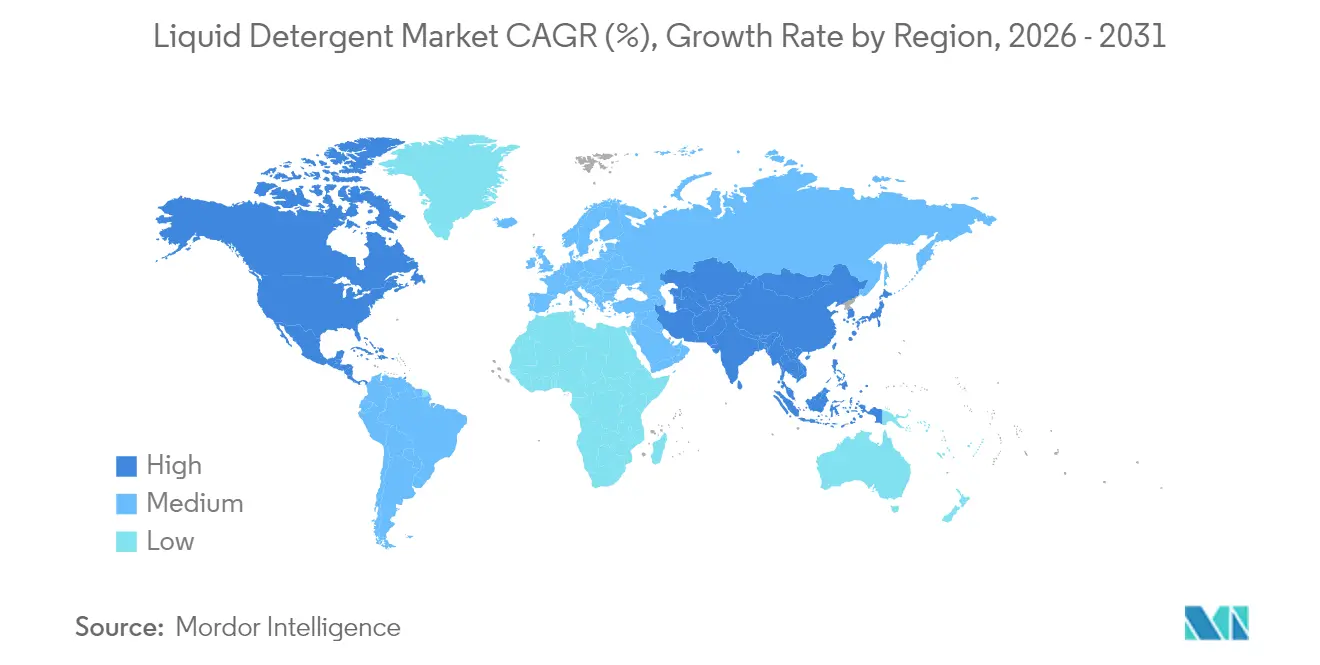

- By geography, North America captured 31.18% revenue in 2025, and Asia-Pacific are pacing the fastest at 6.21% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Liquid Detergent Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Awareness of Hygiene and Cleanliness | +0.8% | Global, with stronger impact in Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Innovation in Eco-Friendly Formulations and Packaging | +0.9% | North America and European Union leading, expanding to APAC | Long term (≥ 4 years) |

| Technological Advancements in Laundry Products | +1.2% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Growth in E-Commerce Drives Growth | +0.7% | European Union and North America core, expanding globally | Long term (≥ 4 years) |

| Superior Cleaning Performance and Stain Removal | +0.6% | Global | Short term (≤ 2 years) |

| Social Media Influence and Endorsements | +0.4% | Global, strongest in urban markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising awareness of hygiene and cleanliness drives the market

Shifts in consumer behavior driven by global health concerns have significantly influenced demand patterns for cleaning products, with liquid detergents gaining traction due to their perceived superior hygiene benefits compared to powder alternatives. According to the American Cleaning Institute, over 22 member companies are actively pursuing net-zero emissions by 2050 while maintaining high product performance standards[1]Source: American Cleaning Institute, “Cleaning Product Industry Update 2024,” cleaninginstitute.org. This dual emphasis on hygiene and sustainability presents growth opportunities, particularly in emerging markets where increasing disposable incomes align with heightened hygiene awareness. Data from India's household consumption expenditure survey shows rural MPCE rising to INR 4,122 and urban MPCE to INR 6,996 in 2023-24, reflecting growth rates of 9% and 8%, respectively[2]Source: Ministry of Statistics & Programme Implementation, “Household Consumption Expenditure Survey 2023-24,” mospi.gov.in. The intersection of growing hygiene consciousness and expanding purchasing power positions liquid detergents for sustained growth in cost-sensitive markets. Companies capitalizing on this trend through strategic marketing and product innovation are achieving notable market share gains, while those adhering to traditional strategies are experiencing margin pressures.

Innovation in eco-friendly formulations and packaging supports the market

Sustainable innovation has evolved beyond marketing positioning to become a core competitive differentiator, with manufacturers investing heavily in biodegradable surfactants and recyclable packaging solutions. Dow and Procter & Gamble's joint development of proprietary recycling technology targeting hard-to-recycle plastic packaging demonstrates the industry's commitment to circular economy principles, with the technology aimed at delivering high-quality post-consumer recycled polymer with lower greenhouse gas emissions than fossil-based alternatives. The EU's revised detergent regulation introduces product passports for traceability and digital labeling requirements, forcing manufacturers to invest in transparency and sustainability verification systems. This regulatory shift creates barriers for smaller players while rewarding established companies with robust R&D capabilities. The innovation cycle is accelerating, with companies like Unilever launching specialized products like Comfort Botanicals and Elixir to address evolving consumer preferences for sophisticated fragrances and sustainable formulations.

Technological advancements in laundry products surge growth

Cold-water washing technology is transforming the liquid detergent market. Procter and Gamble and Unilever, guided by their sustainability goals, are making substantial research and development investments in surfactant and enzyme technologies to deliver effective cleaning at lower temperatures. The 2024 American Cleaning Institute Convention emphasized the role of artificial intelligence in product development, signaling shorter innovation cycles. These advancements strengthen the competitive position of companies with advanced research and development capabilities while challenging traditional formulation methods. Patent filings related to enzyme-based granulates and surfactant innovations highlight ongoing technological progress, with firms focusing on improved stability and performance. The partnership between Unilever and Samsung to explore the future of laundry suggests technology integration will extend beyond formulation to encompass smart appliance connectivity and IoT-enabled washing solutions. Federal energy conservation standards for residential clothes washers, effective March 2028, will drive demand for concentrated detergents that perform effectively in energy-efficient machines.

Social media influence and endorsements

Social media influence and endorsements significantly drive the liquid detergent market by shaping consumer preferences and boosting brand visibility in the U.S. and Europe. Influencers on platforms like Instagram, TikTok, and YouTube showcase eco-friendly, visually appealing, or high-performance liquid detergents, leveraging aesthetic packaging and sustainability claims to attract environmentally conscious millennials and Gen Z. Celebrity endorsements and influencer-led campaigns, such as those promoting Seventh Generation or Method’s natural formulations, amplify trust and desirability, encouraging purchases through relatable content like cleaning hacks or product reviews. These digital campaigns, often featuring hashtags like #CleanGreen or #EcoLaundry, create viral trends, driving demand for premium and niche liquid detergents despite higher costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing popularity of on-demand laundry services | -0.4% | Urban developed markets | Medium term (2-4 years) |

| Environmental and regulatory pressures hamper the market | -0.3% | Asia-Pacific, Middle East and Africa | Short term (≤ 2 years) |

| High production costs hamper the market | -0.4% | Asia-Pacific, Middle East and Africa | Short term (≤ 2 years) |

| Presence of counterfeit products hampers growth | -0.3% | Asia-Pacific, Middle East and Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing popularity of on-demand laundry services

The proliferation of on-demand laundry services in urban markets represents a structural shift that could reduce household detergent consumption, particularly among younger demographics who prioritize convenience over cost considerations. This trend is most pronounced in metropolitan areas across North America, Europe, and Asia-Pacific, where busy lifestyles and disposable income levels support service-based laundry solutions. The impact varies significantly by demographic segment, with millennials and Gen Z consumers showing higher adoption rates for outsourced laundry services. However, the restraint effect is partially offset by commercial demand from laundry service providers, who often use concentrated liquid detergents for operational efficiency. The long-term implications depend on pricing dynamics and the expansion of service coverage to suburban and rural markets.

Availability of Counterfeit Products

Counterfeit liquid detergents pose a persistent challenge to brand integrity and consumer safety, particularly in emerging markets where price sensitivity creates demand for lower-cost alternatives. The U.S. Department of Homeland Security's enhanced enforcement actions against illicit trade, including increased screening of small package shipments and joint operations by Customs and Border Protection, demonstrate the scale of the counterfeit problem across multiple product categories [3]Source: U.S. Department of Homeland Security, "enforcement actions against illicit trade", dhs.gov. The Department of Commerce's investigation into certain alkyl phosphate esters from China being sold at less than fair value indicates broader concerns about unfair trade practices affecting raw material costs and product authenticity. Digital commerce platforms have inadvertently facilitated counterfeit distribution, requiring enhanced brand protection strategies and consumer education initiatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Conventional Dominance Amid Organic Acceleration

Conventional formats generated 83.02% revenue in 2025, sustaining price leadership through scale in sourcing anionic surfactants and legacy scents. Yet, as the market evolves, the dominance of conventional formats faces scrutiny. The push for sustainability is not just a trend; it's reshaping the industry's landscape. However, the organic liquid detergent segment's 4.39% CAGR for 2026-2031 signals accelerating consumer migration toward environmentally conscious alternatives, driven by regulatory pressures and sustainability awareness. This growth isn't merely a statistic; it's a testament to shifting consumer values. As awareness of environmental issues rises, so does the demand for greener products. Private labels partner with contract fillers to launch small organic runs that test demand without heavy capex. These strategic moves highlight the industry's agility in responding to market cues. The increasing presence of USDA Bio-Preferred logos confirms that certification has become a mainstream purchase cue.

Research and development teams in conventional portfolios now blend bio-based solvents such as ethyl lactate with legacy builders to meet new eco-scores. This shift underscores the industry's commitment to sustainability. As regulations tighten and consumer preferences shift, such innovations become paramount. This hybrid approach guards volume while guarding margins. It's a delicate balance, but one that could define market leaders. Competitive advantage accrues to players that share bulk infrastructure across both sub-segments and shift production lots responsive to weekly sell-through data. Such agility in operations not only boosts profitability but also positions companies as frontrunners in a competitive landscape.

By Application: Laundry Leadership with Dishwashing Momentum

In 2025, laundry applications hold a commanding 64.01% market share, reflecting the segment's established presence and consumer confidence in liquid detergents for fabric care. Conversely, the dishwashing segment is experiencing significant growth, with a projected 4.73% CAGR from 2026 to 2031. This upward trend, driven by product innovation and targeted marketing efforts, highlights a shift in consumer preference. Liquid detergents are increasingly capturing market share from traditional dishwashing liquids due to their superior grease-cutting capabilities and concentrated formulations that deliver enhanced value.

Application diversification strategies are enabling manufacturers to unlock cross-selling opportunities while reducing reliance on single-use categories that may face market saturation. Insights into consumer behavior reveal a rising demand for multi-purpose cleaning products that simplify household tasks, positioning liquid detergents as a preferred choice due to their proven effectiveness across various applications. Supporting this trend, the American Cleaning Institute emphasizes product versatility in its sustainability initiatives, citing its role in reducing packaging waste and environmental impact. Companies expanding beyond traditional laundry applications are not only gaining incremental market share but are also strengthening consumer relationships by offering products with broader utility.

By End User: Adult Segment Stability with Children's Growth Potential

Adults represent the dominant end-user segment with a commanding 93.42% market share in 2025, underscoring their pivotal role in purchasing decisions and household cleaning product selections. Conversely, the children's segment, though smaller, is set to expand at a notable 5.05% CAGR from 2026 to 2031. This anticipated growth highlights a surging demand for specialized formulations that prioritize safety and sensitivity. It also underscores manufacturers' strategic pivot towards age-specific product innovations, as parents become increasingly vigilant about minimizing chemical exposure risks.

In response to these trends, product development is increasingly leaning towards hypoallergenic formulations and milder ingredients. This shift not only addresses parental concerns but also ensures that cleaning efficacy remains uncompromised. The burgeoning children's segment is further indicative of changing household demographics and a heightened willingness to invest in child-centric products. Companies that prioritize child-safe formulations and adopt focused marketing strategies stand to gain significantly, not just in market share but also in cultivating enduring brand loyalty among family-centric consumers.

By Packaging: Bottle Dominance Challenged by Sustainable Alternatives

In 2025, traditional bottles hold a 64.10% market share, supported by strong consumer familiarity and effective retail display positioning. Conversely, refill pouches are projected to grow at a 5.45% CAGR from 2026 to 2031, driven by increasing sustainability priorities and cost-efficiency initiatives. This transition in packaging reflects heightened environmental awareness among consumers and stricter regulatory mandates aimed at reducing plastic waste. Refill pouches deliver notable environmental advantages by lowering material consumption and improving transportation efficiency, while also enabling cost reductions that appeal to price-sensitive consumers.

Innovations in packaging technology are unlocking opportunities for competitive differentiation. Companies are prioritizing investments in smart packaging solutions to enhance user experience and reduce environmental impact. Furthermore, emerging formats such as concentrated pods and advanced dispensing systems present growth opportunities for businesses focused on delivering convenience and sustainability. The shifting dynamics of the packaging segment favor companies with adaptable manufacturing capabilities, enabling them to respond to evolving consumer demands while maintaining cost efficiency across diverse packaging formats.

By Distribution Channel: Traditional Retail Resilience Amid Digital Transformation

Supermarkets and hypermarkets retain 42.05% market share in 2025, leveraging established consumer shopping patterns and extensive product display capabilities that facilitate brand comparison and impulse purchases. Online retail stores demonstrate the strongest growth momentum at 5.62% CAGR for 2026-2031, accelerated by e-commerce adoption and direct-to-consumer strategies that bypass traditional retail markups. Convenience and grocery stores maintain steady market presence through location advantages and immediate availability for emergency purchases.

The distribution channel evolution creates both opportunities and challenges for manufacturers, with online channels offering direct consumer relationships and data insights while requiring new capabilities in digital marketing and fulfillment. Other distribution channels, including specialty stores and direct sales, provide niche opportunities for premium and specialized products that require expert consultation or demonstration. Companies with omnichannel strategies that integrate traditional retail presence with digital capabilities are best positioned to capture market share across evolving consumer preferences while optimizing cost structures through channel diversification.

Geography Analysis

North America led with a 31.18% share in 2025, anchored by premiumisation and loyalty programs that tilt shoppers toward branded concentrates. Regulatory developments, including California's ban on nonylphenol ethoxylates and federal energy efficiency standards for washing machines, are driving product reformulation and creating competitive advantages for companies with advanced R&D capabilities. The American Cleaning Institute's sustainability initiatives, with 22 member companies aligning climate strategies with the 1.5°C Challenge, demonstrate industry commitment to environmental responsibility that resonates with North American consumers.

Asia-Pacific delivers the fastest expansion at 6.21% CAGR through 2031. The region's growth trajectory benefits from increasing consumer sophistication, with demand shifting toward premium formulations and eco-friendly packaging that align with global sustainability trends. Multinationals erect local enzyme plants to cut import tariffs and ensure freshness under hot, humid storage. Digital channels thrive on smartphone penetration in urban areas, funneling first-time buyers toward sachet trials that fit tight budgets.

Europe maintains steady growth supported by stringent environmental regulations and consumer preference for sustainable products, while South America and Middle East and Africa regions show promising expansion driven by improving economic conditions and increasing urbanization rates. The EU's revised detergent regulation, emphasizing biodegradability and digital labeling requirements, creates market opportunities for companies that proactively invest in sustainable chemistry and transparent supply chains. Regional growth patterns reflect varying stages of market development, with mature markets focusing on premiumization and sustainability, while emerging markets prioritize accessibility and basic functionality. The geographic distribution of growth opportunities suggests successful companies must adapt product portfolios and go-to-market strategies to address diverse regional requirements and regulatory environments.

Competitive Landscape

The liquid detergent market is moderately concentrated, with the presence of domestic and international players. As a result of these players' activities, market volatility has been on the rise. In response, these players are adopting diverse marketing strategies, including new product development, expansion, and acquisitions. Leading the charge at the top are major players like Unilever, Procter and Gamble Company, Reckitt Benckiser Group PLC, Church and Dwight Company, and Henkel AG and Co. KGaA.

Mid-tier challengers carve out their niche with innovations like scent capsules, refill subscription models, and vegan product claims. Many of these players leverage contract logistics networks, enabling them to expand without heavy asset investments. On the regulatory side, the FTC's historical interventions in cleaning mergers hint at ongoing scrutiny, especially for acquisition targets that might skew local market concentrations. Meanwhile, private-label brands are gaining strength, as retailers pursue better margins and enhanced negotiating power. For instance, First Quality Enterprises, which bolstered its portfolio by acquiring Henkel’s North-American retailer brands in February 2025.

Technology is now a pivotal factor in the industry. Companies harnessing AI to predict stain responses have reduced product development time from 40 weeks to just 26, allowing for quicker market entry. Patents on multi-enzyme systems offer a temporary exclusivity, supporting premium pricing strategies. However, initiatives like A.I.S.E.’s focus on plastic circularity highlight the industry's shift towards open innovation. Such collaborations ensure that best practices rapidly permeate licensed supply chains, diminishing any competitive advantages.

Liquid Detergent Industry Leaders

-

Unilever plc

-

Procter & Gamble Company

-

Henkel AG and Co KGaA

-

Reckitt Benckiser Group PLC

-

Church and Dwight Co., Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Henkel has unveiled concentrated formulas for its all, Persil, and Snuggle liquid laundry lines. The revamped initiative, as stated by Henkel, encompasses updated packaging and formulas, aiming to deliver enhanced cleaning and fabric care in every load.

- February 2025: Hindustan Unilever has entered into a strategic partnership with Whirlpool to enhance the laundry experience in India. This collaboration integrates Whirlpool's top-load washing machines with Surf Excel Matic Liquid Detergent.

- April 2024: Unilever has introduced "Wonder Wash," a liquid laundry detergent specifically formulated for quick wash cycles. This new detergent is formulated to perform effectively in cycles as short as 15 minutes. Wonder Wash is available in the United Kingdom, Ireland, and China, with plans for further market expansion.

- December 2023: Godrej Consumers has launched 'Godrej Fab', a new liquid detergent brand aimed at the mass market. The product has been introduced in the South Indian states of Tamil Nadu, Andhra Pradesh, Karnataka, and Kerala.

Global Liquid Detergent Market Report Scope

Liquid detergents are a mixture of surfactants that are used for effective cleaning action. The liquid detergents market is segmented by type, application, and geography. By type, the market is segmented into organic liquid detergent and conventional liquid detergent. By application, the market is fragmented into laundry and dishwashing. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online stores, and other distribution channels. It provides an analysis of emerging and established economies across the world, comprising North America, Europe, South America, Asia-Pacific, and Middle East and Africa. For each segment, the market sizing and forecasts are provided in terms of value in USD million.

| Organic Liquid Detergent |

| Conventional Liquid Detergent |

| Laundry |

| Dishwashing |

| Adult |

| Kids/Children |

| Bottles |

| Refill Pouches |

| Others |

| Supermarkets/Hypermarket |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Others Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa | |

| Middle East and Africa |

| By Product Type | Organic Liquid Detergent | |

| Conventional Liquid Detergent | ||

| By Application | Laundry | |

| Dishwashing | ||

| By End User | Adult | |

| Kids/Children | ||

| By Packaging | Bottles | |

| Refill Pouches | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarket | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Others Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current liquid detergent market size and how fast is it growing?

The market stands at USD 70.01 billion in 2026 and is set to expand to USD 85.72 billion by 2031 at a 4.14% CAGR.

Which region shows the fastest liquid detergent market growth through 2031?

Asia-Pacific leads with a projected 6.21% CAGR due to rising disposable incomes, urbanization, and increasing hygiene expectations.

How much liquid detergent market share do organic products hold today?

Organic variants represent 16.98% of revenue in 2025 and carry a 4.39% CAGR outlook as sustainability concerns steer consumers to plant-based formulas.

What packaging format is gaining the most traction in the liquid detergent industry?

Refill pouches are advancing at 5.45% CAGR because they cut plastic use and generally cost less per liter than rigid bottles.

Page last updated on: