Detergents Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 145.82 Billion |

| Market Size (2031) | USD 178.06 Billion |

| Growth Rate (2026 - 2031) | 4.07% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Detergents Market Analysis by Mordor Intelligence

The Detergents Market size was valued at USD 140.12 billion in 2025 and estimated to grow from USD 145.82 billion in 2026 to reach USD 178.06 billion by 2031, at a CAGR of 4.07% during the forecast period (2026-2031). Structural shifts stem from cold-water enzymes that reduce household energy use, carbon-pricing policies favoring ultra-concentrated formats, and regulatory mandates that accelerate the adoption of biodegradable surfactants. The Asia-Pacific region continues to drive demand, largely due to the rapid adoption of washing machines, while direct-to-consumer (D2C) subscription services are redefining last-mile economics in North America and China. Competitive intensity remains high: Procter & Gamble, Unilever, and Henkel leverage enzyme technology and concentrated pods to command premium pricing, whereas regional specialists gain share with sachet distribution that meets tight household budgets. Input-cost volatility in palm-kernel oil and enzymes compresses margins for mid-tier brands yet hastens investment in algae-derived and fermentation-based surfactants that bypass constrained supply chains.

Key Report Takeaways

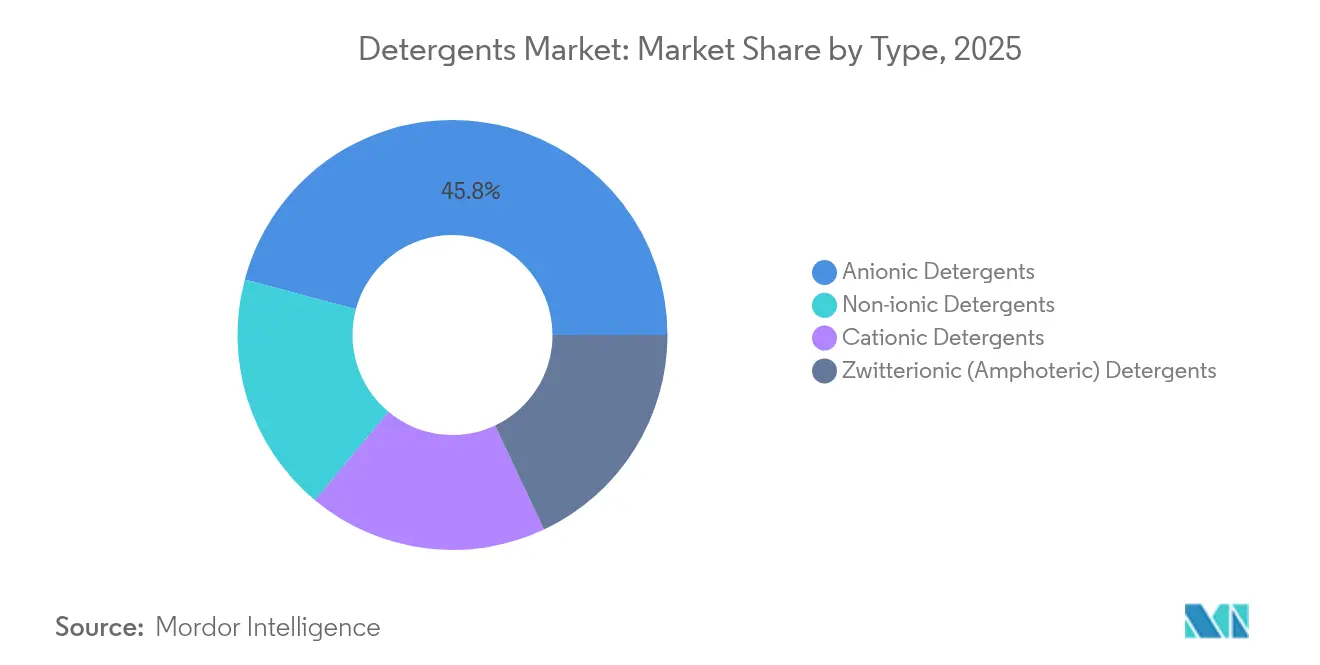

- By type, anionic surfactants captured 45.84% of the detergents market share in 2025, while non-ionic surfactants are forecast to expand at a 4.95% CAGR through 2031.

- By application, laundry cleaning products led with 56.55% of revenue in 2025; biological reagents for pharmaceutical and laboratory use are projected to grow at a 5.15% CAGR to 2031.

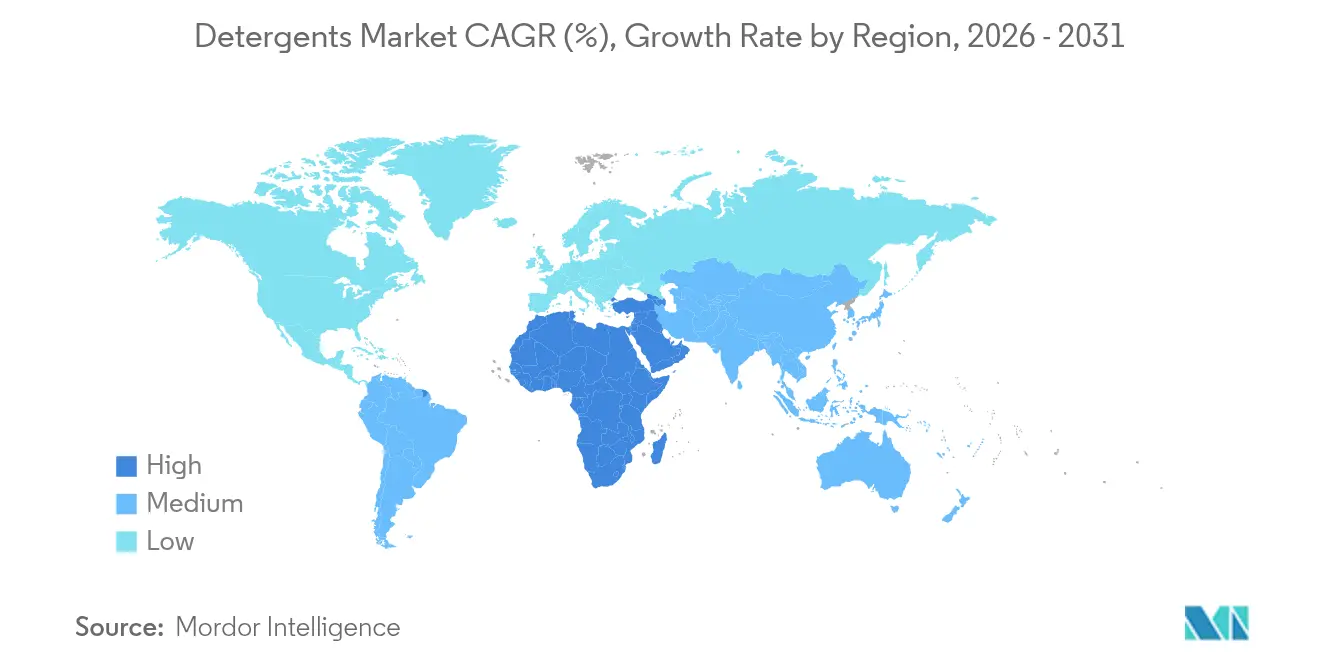

- By geography, the Asia-Pacific region held 44.10% of the 2025 volume, whereas the Middle East & Africa region is expected to record the fastest growth, with a 4.78% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Detergents Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising washing-machine penetration in emerging economies | +0.8% | Asia-Pacific core, spillover to Middle East & Africa | Medium term (2-4 years) |

| Boom in e-commerce and D2C channels for detergents | +0.6% | North America & Europe lead, expanding in Asia-Pacific urban centers | Short term (≤ 2 years) |

| Consumer shift to eco-friendly/biodegradable formulations | +0.7% | Global, strongest in Western Europe and North America | Long term (≥ 4 years) |

| Cold-water enzyme breakthroughs cut energy use | +0.9% | Global, accelerated adoption in temperate and cold climates | Medium term (2-4 years) |

| Carbon-tax driven demand for ultra-concentrates | +0.5% | European Union, California, British Columbia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Washing-Machine Penetration in Emerging Economies

Automatic washer ownership in India increased from 14% in 2020 to 28% in 2024, resulting in a rise in per-capita detergent usage, as drum cycles require 30%–40% more product than hand-washing. Smaller 250ml liquid packs and 10-wash sachets help keep entry prices low while sustaining margins above 40%. Similar adoption curves in Indonesia and Vietnam benefit from appliance subsidies and installment-payment schemes. Formulators now specify enzymes optimized for 30-minute, 20°C cycles, with BASF’s Lavergy protease delivering equivalent stain removal at 35% lower energy consumption[1]“Annual Report 2024,” BASF, basf.com.

Boom in E-Commerce and D2C Channels for Detergents

Direct-to-consumer subscriptions generated USD 4.2 billion in 2024, representing a 38% year-over-year growth as brands bypass retailers’ 25%–35% markup. Lower acquisition costs (USD 18 per subscriber) and churn below 15% after the third delivery underpin profitability. Online sales reached 32% in North America and 41% in China, driven by same-day logistics and influencer marketing that emphasize ingredient transparency. Concentrated pods and strips, 70% lighter than equivalent liquids, shave USD 0.12 from last-mile freight while reducing packaging waste by 60%.

Consumer Shift to Eco-Friendly and Biodegradable Formulations

Plant-based surfactants made up 48% of Western Europe’s 2024 detergent launches, reflecting preference for low aquatic toxicity over marginal performance gains. Evonik’s REWOFERM rhamnolipid achieved ready biodegradability under OECD 301B and ISO 14001 certification in March 2024, positioning it as a drop-in replacement for alkylbenzene sulfonates. Yet, a Journal of Cleaner Production study found that consumers use eco-detergents 22% more often or wash hotter, negating the sustainability gains. Seventh Generation closed the gap with a triple-enzyme liquid validated to match conventional efficacy at 15°C.

Cold-Water Enzyme Breakthroughs Cut Energy Use

Novozymes’ Evity protease maintains 85% activity at 15°C, enabling formulators to trim surfactant loading by 15% without sacrificing protein-soil removal. Tide Coldwater, now 12% of US liquid sales, has reduced 27 million t of CO₂ since launch. The global enzyme market for detergents reached USD 1.8 billion in 2024, expanding at a 6.2% annual rate as brands incorporate protease, amylase, lipase, and cellulase into single-dose pods. Regulatory incentives add momentum: California caps default wash temperatures at 25°C on machines sold after 2026[2]“California Energy Efficiency Standards,” California Energy Commission, energy.ca.gov .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global and regional chemical regulations | -0.4% | European Union, North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| Raw-material price volatility (surfactants, enzymes) | -0.6% | Global, acute in regions dependent on palm-oil imports | Short term (≤ 2 years) |

| Micro-plastic filtration mandates raise reformulation costs | -0.3% | European Union core, pilot programs in California and South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Global and Regional Chemical Regulations

In October 2023, the European Chemicals Agency, under REACH Annex XVII, restricted microplastics, banning their intentional use in rinse-off detergents with transition periods of 4 to 12 years. In April 2024, the US Environmental Protection Agency expanded PFAS restrictions, requiring manufacturers to certify that surfactants and processing aids contain no per- and polyfluoroalkyl substances above 1 part per billion, effectively banning legacy fluorosurfactants in industrial and institutional cleaning products. These regulations disproportionately affect smaller regional brands, which lack the R&D budgets for rapid reformulation, while multinationals spread compliance costs over global volumes exceeding 500,000 metric tons annually.

Raw-Material Price Volatility (Surfactants, Enzymes)

In 2024, palm-kernel oil, the primary feedstock for fatty alcohols in non-ionic surfactants, experienced a 39% price fluctuation due to an 8% yield drop in Malaysia and Indonesia, caused by the El Niño phenomenon. This volatility increased fatty-alcohol prices by 14% in H1 2024, compressing detergent margins and slowing growth in price-sensitive markets like India and Brazil. Enzyme suppliers faced similar challenges, with global fermentation capacity exceeding 85%, resulting in contract prices increasing by 12%. Multinationals with long-term hedging contracts secured prices 8% to 10% below spot rates, gaining a cost edge over regional competitors. In response, Unilever committed GBP 50 million in Q3 2024 to develop algae-derived surfactants, targeting production by late 2026.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Anionic Dominance Meets Non-Ionic Momentum

Anionic surfactants held 45.84% of the Detergents market share in 2025, supported by low-cost linear alkylbenzene sulfonates that anchor powder and liquid staples in South Asia and Africa. Non-ionic alcohol ethoxylates and alkyl polyglucosides, prized for rapid ultimate biodegradation, are forecast to grow at a 4.95% CAGR, lifted by EU rules requiring aerobic breakdown within 28 days. Henkel reformulated Persil Sensitive in 2024 by substituting 40% of LAS with corn-starch-derived alkyl polyglucosides, thereby lowering aquatic toxicity by 35% while retaining the product's performance.

Cationic quaternary ammonium surfactants remain niche outside fabric softeners because their positive charge limits co-formulation with anionics. EPA scrutiny of quats is prompting pilots of faster-biodegrading ester-quat alternatives. Zwitterionic cocamidopropyl betaine, 6% of 2024 volume, stabilizes foam in hard-water markets across the Middle East and North Africa, and its broad pH stability suits cold-water pods that avoid mineral chelators.

By Application: Laundry Leadership and Biological Reagents’ Ascent

Laundry retained 56.55% of revenue in 2025, as per-capita usage averages 8-12 kg in developed economies and rises alongside washing machine adoption in emerging regions. Pods and strips reached 28% of North American laundry volume, curbing overdosing and cutting plastic by 60%.

Biological reagents for pharmaceutical and laboratory protocols are projected to grow at a 5.15% CAGR, reflecting tighter endotoxin limits in monoclonal antibody production and expansion of single-use bioreactors. Surface cleaners held 22% of the 2024 volume, as antibacterial claims remain a post-pandemic priority, while dishwashing tablets with cold-active enzymes reduce energy consumption by 25%. Fuel-additive detergents grow modestly amid the adoption of electric vehicles, yet persist in heavy-duty applications.

Geography Analysis

The Asia-Pacific region accounted for 44.10% of the global 2025 volume, driven by a doubling of washing-machine ownership in India and Indonesia, robust e-commerce in China, and a shift toward premiumization of enzyme-rich liquids. Local champions such as Blue Moon and Liby hold a 38% share of China’s liquid category through direct online engagement and tailored fragrances. India’s market expanded by 7.2% in 2024, driven by affordable 250 ml packs targeting first-time machine users. Mature Japan and South Korea focus on bio-based isethionate surfactants that accelerate soil release by 30%.

The Middle East & Africa are forecast to deliver the fastest growth, with a 4.78% CAGR, as urbanization lifts per-capita consumption above 3 kg. Saudi Arabia’s Vision 2030 infrastructure push raises washer penetration toward 65%, spurring demand for hard-water-tolerant pods. South Africa’s market increased by 5.8% in volume in 2024, driven by enzyme-fortified powders that perform well in cold cycles, a necessity amid intermittent electricity supply. Sachet-priced powders dominate rural Sub-Saharan Africa, but liquid formats are gaining traction in Lagos and Nairobi as front-load adoption increases.

Europe and North America register slower growth but lead sustainability innovation. Germany’s eco-labeled segment reached 42% of 2024 detergent sales. US pods and strips command 32% of laundry volume, and refill stations in Canadian and UK grocers reduce packaging by 40%. South America grew by 4.2% in 2024; powders still hold a 68% share, but liquids are rising in urban Brazil and Argentina, alongside washer ownership above 55%.

Regulatory Landscape

Detergent formulations and claims are increasingly shaped by chemical-content restrictions, biodegradability criteria, and labeling modernization across major markets. In the European Union, Regulation (EU) 2026/405 was adopted in February 2026 to replace Regulation (EC) No 648/2004, updating requirements around surfactants and other organic ingredients and adding provisions that support digital labeling approaches aligned with Green Deal objectives.

In the United States, regulatory attention is also intensifying around ingredient residues and impurities used in laundry detergents and related cleaning products. In January 2026, the US Environmental Protection Agency received a TSCA Section 21 petition seeking risk-management action for widely used detergent ingredients and impurities (including 1,4-dioxane), while the EPA Safer Choice and Design for the Environment (DfE) program continues to provide voluntary standards that brands use to substantiate safer-chemistry positioning and facilitate retailer acceptance.

Value Chain Analysis

The detergents value chain starts with upstream feedstocks (oleochemicals and petrochemicals) and moves through intermediates such as fatty alcohols, ethoxylates, and linear alkylbenzene (LAB), before reaching surfactant and enzyme manufacturing, blending, and conversion into finished formats (powders, liquids, pods/capsules, and emerging solid formats). Ingredient suppliers and intermediates producers (for example BASF, Evonik, and Stepan Company) feed formulators and brand owners, while consumer goods companies (such as Procter & Gamble and Unilever) bring together formulation, manufacturing, and increasingly automated packaging and distribution to support concentrated and single-dose products.

Logistics and input availability continue to swing outcomes across regions. Red Sea shipping disruptions highlighted by Germany's chemical industry in early 2024 increased lead-time and freight risk for specialty chemical imports into Europe, and 2026 supply-chain cost shocks, including those cited by Procter & Gamble tied to oil-related costs and disruption, reinforced the value of dual sourcing and regionalization. Regional capacity additions also respond to import dependence, including Dangote Refinery's announced plan for a 400,000-tonnes-per-year LAB plant in Nigeria to serve African detergent chemicals demand, and Unilever's completed upgrades at Port Sunlight in the UK that link advanced capsule production with an automated distribution center for faster replenishment.

Competitive Landscape

The Detergents Market is moderately consolidated. Agile regional players meet price-sensitive demand through localized production and sachet distribution. Procter & Gamble leverages a 28% rise in cold-active enzyme patents to strengthen Tide Coldwater and secure 12% of US liquid sales. Henkel’s new EUR 120 million Düsseldorf facility adds 180,000 tonnes of ultra-concentrates and pods, trimming lead times by 30% and aligning with EU carbon border costs.

Detergents Industry Leaders

Henkel AG & Co. KGaA

Kao Corporation

Unilever

Procter & Gamble

Church & Dwight Co., Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory and retailer pressure around ingredient transparency and environmental performance is creating space for reformulation platforms that can document biodegradability and support digital labeling requirements at scale. The adoption of EU Regulation (EU) 2026/405 in February 2026, with updated requirements spanning surfactants and other high-loading organic ingredients, is lifting demand for alternative surfactant systems and enzyme-led performance that enable lower-temperature, lower-dose cleaning while maintaining performance claims.

Capacity and capability investments in surfactants and finished formats are also expanding the addressable space for premium and concentrated detergents across developed and emerging markets. In March 2026, BASF Hannong Chemicals Solutions inaugurated a new non-ionic surfactant site in Seosan, Korea, supporting regional supply of alcohol ethoxylates and related inputs used in higher-performance, lower-toxicity formulations. In Q1 2026, Hayat Kimya commissioned a USD 50 million detergent plant in Mersin, Turkey (230,000 tons annual capacity), which signals continued build-out of local production for cost-competitive supply into nearby markets, while the industry's shift toward multi-chamber capsules and higher concentrates is reinforced by Unilever's manufacturing and logistics upgrades at Port Sunlight for four-chamber laundry capsules.

Recent Industry Developments

- July 2026: Henkel launched updated Purex liquid laundry detergent formulas in North America, emphasizing more concentrated cleaning power alongside refreshed packaging using 50% recycled plastic. The launch supports portfolio premiumization and reduces packaging material intensity per wash as brands push higher concentrates.

- September 2025: Procter & Gamble upgraded Tide Original Liquid Detergent with a new formula positioned as its first major update in over two decades, including higher surfactant content designed to improve cold-water cleaning. The reformulation aligns with the industry shift toward cold-water performance enabled by enzymes and concentrated chemistry.

- March 2024: Evonik advanced its REWOFERM rhamnolipid positioning for detergents by meeting ready biodegradability under OECD 301B and aligning with ISO 14001 certification. This strengthened the commercial pathway for biosurfactants as drop-in or blend components in formulations responding to tightening aquatic-toxicity and biodegradability expectations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the detergents market covers the sales value of detergent chemicals and formulations used to remove soil and stains across end uses such as laundry cleaning, household cleaning, and dishwashing, as well as selected industrial uses where detergents are applied.

Scope exclusions: We do not treat adjacent home care items that are not detergents (for example, simple disinfectants without detergent action) as part of this market.

Segmentation Overview

- By Type

- Anionic Detergents

- Cationic Detergents

- Non-ionic Detergents

- Zwitterionic (Amphoteric) Detergents

- By Application

- Laundry Cleaning Products

- Household Cleaning Products

- Dishwashing Products

- Fuel Additives

- Biological Reagents

- Other Applications

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- Russia

- Spain

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with anchoring demand drivers and trade flows that influence detergent consumption. We reviewed public sources such as UN Comtrade for detergent and surfactant trade patterns, World Bank and IMF macro series for income and inflation context, and national statistics agencies for household spend and population baselines. We also checked regulatory and ingredient direction through sources such as the US EPA and the European Chemicals Agency, since formulation shifts can change average pricing and product mix.

To avoid building a model off one angle, the desk step also pulled from company filings and investor presentations for category revenue cues, alongside association websites and reputed press for capacity additions and raw material discussion. Where needed, we used a paid subscription for company financials and news screening, plus an import-export shipment-level view to sanity-check trade-linked supply signals in key corridors. The sources listed here are illustrative only, and many other public materials were used for cross-checks and clarification during the study.

Primary Interviews and Surveys

Primary work was used to pressure-test the desk assumptions on category mix, pricing progression, and where volume is shifting between liquids, powders, and newer formats. We spoke with a mix of detergent value chain participants and downstream buyers across major regions, then used follow-up questions to reconcile differences between trade signals, capacity commentary, and retail price movement.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 17% | APAC: 45% |

| Mid tier: 47% | Functional/Unit leaders: 37% | EMEA: 37% |

| Smaller Players: 22% | Managers: 46% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach, where macro demand pools are constructed first and then checked with supplier and channel reality. The top-down side reconstructs value by linking detergent consumption signals to population, household formation, washing machine penetration, and cleaning frequency, which are then translated into spend using observed price bands and mix shifts. To keep the estimate grounded, results were corroborated with selective bottom-up approximations, including sampled average selling price (ASP) times volume by form factor, plus channel checks on promo intensity and pack-size movement.

Inputs were chosen because they leave a clear trail for review, even when datasets are imperfect. In practice, we leaned on indicators such as surfactant and key feedstock price direction, import and export volumes for relevant product groups, and regional consumption patterns for laundry versus dishwashing. Where bottom-up gaps existed, missing pieces were filled using conservative penetration ranges and then adjusted only after primary feedback confirmed the ranges were realistic.

For forecasting, scenario analysis was used so the model could separate steady demand growth from step changes like premiumization, concentrated formats, and regulatory-driven reformulation. Assumptions on ASP progression and mix were only pushed forward after they matched what respondents described for contract timing, retail price resets, and expected input-cost pass-through behavior.

Data Validation & Update Cycle

Validation happens in layers so single-source errors do not flow into the final totals. We compare the model output against independent signals such as trade movement, macro spend constraints, and the direction of category pricing, and then investigate outliers region by region before sign-off. When a variance is large, the model is reopened, and follow-up calls are triggered to confirm whether the issue is scope, timing, or a real market shift.

Reports are refreshed annually, and interim checks are made when material events occur, such as major input-cost shocks or regulation changes that alter product mix. Before delivery, an analyst performs a fresh pass on key assumptions so clients receive the most current view aligned to the latest available data.

Mordor Intelligence's Detergents Market Sizing Compared With Other Published Estimates

Published values for detergents often do not line up, even when the topic name looks the same, because the counted product boundaries and the timing of price conversion can be different. It also matters whether the estimate treats industrial applications as a meaningful add-on, or stays focused mainly on household use.

The main gap drivers in this market are refresh cadence, currency timing, and how average selling prices are carried forward when raw material costs and promotions move quickly. When annual updates incorporate newer exchange rates and a more recent price mix (including liquids, powders, and newer formats), the result can shift even if underlying volumes change only modestly, which is the refresh-led effect applied in Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 145.82 B (2026) | |

| Global Consultancy A | USD 186.42 B (2025) | Uses a broader home care style scope and includes additional formats and adjacent categories in practice (such as fabric softeners and wider institutional coverage), which can lift the value total versus a tighter detergents-only boundary. The base year differs, so currency conversion and price levels are not aligned to the same timing. |

| Industry Publisher B | USD 124.41 B (2024) | Focuses on laundry and dishwashing detergents only, which can exclude detergent applications like general household cleaning and other listed end uses. Earlier-year pricing and mix assumptions (including pack sizes and premium share) can also keep the reported value lower than a later refresh. |

Taken together, the spread is explained more by scope and timing than by disagreement on the direction of demand. By keeping variables traceable to clear demand signals, and then checking price and mix assumptions through field feedback, the final number stays reproducible and easy to reconcile when clients map it to their own category definitions.

Key Questions Answered in the Report

What is the current value of the synthetic detergents market?

The synthetic detergents market size stands at USD 145.82 billion in 2026.

How fast will demand for synthetic detergents grow through 2031?

Global revenue is forecast to rise at a 4.07% CAGR, reaching USD 178.06 billion by 2031.

Which surfactant type is expanding the quickest?

Non-ionic surfactants, led by alcohol ethoxylates and alkyl polyglucosides, are projected to post a 4.95% CAGR.

Which region offers the highest growth runway?

The Middle East & Africa is expected to deliver the fastest regional CAGR at 4.78% through 2031.

How are enzymes changing laundry habits?

Cold-active enzymes allow effective cleaning below 20°C, cutting household energy use up to 60% and boosting adoption of cold-water cycles.

Page last updated on: