Cheek Augmentation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

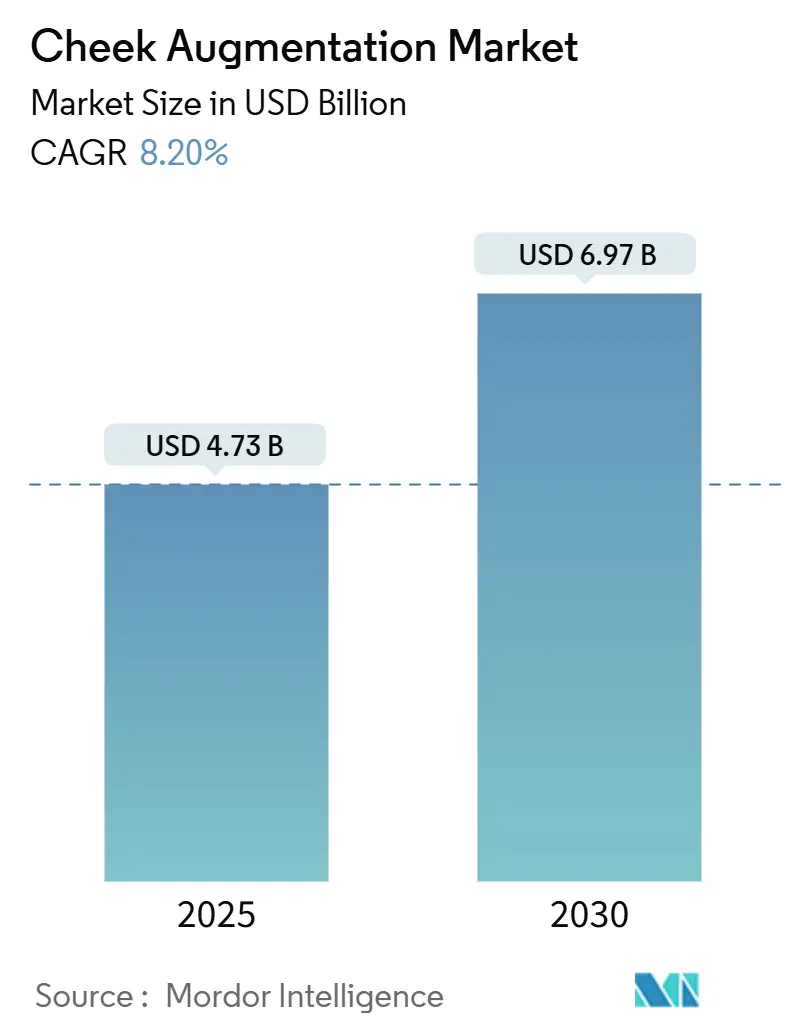

| Market Size (2025) | USD 4.73 Billion |

| Market Size (2030) | USD 6.97 Billion |

| Growth Rate (2025 - 2030) | 8.20% CAGR |

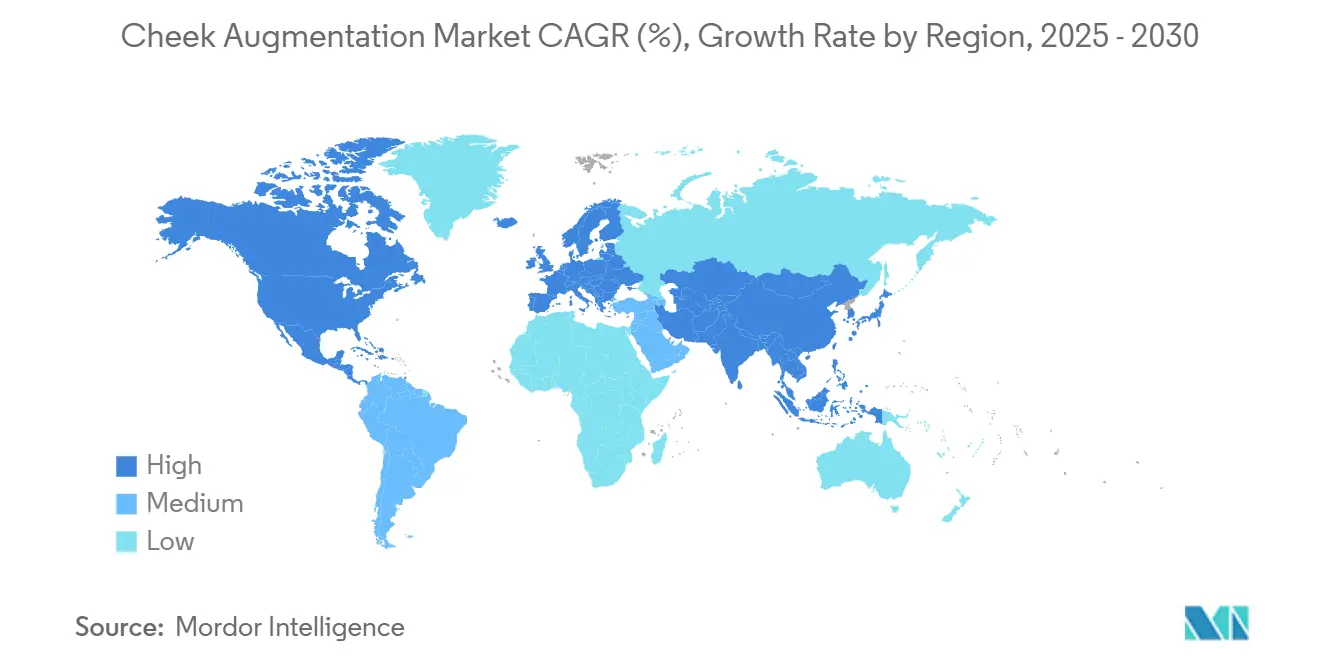

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cheek Augmentation Market Analysis by Mordor Intelligence

The cheek augmentation market size stood at USD 4.73 billion in 2025 and is projected to reach USD 6.97 billion by 2030, translating into an 8.2% CAGR over the forecast period. Rising acceptance of minimally invasive fillers, widening access through medspas, and the influx of post-GLP-1 weight-loss patients are reinforcing durable demand. Providers are capitalizing on advanced cross-linking technologies that extend hyaluronic-acid (HA) filler longevity while improving safety profiles, thereby encouraging repeat treatments at predictable intervals. Meanwhile, customized 3-D-printed implants manufactured from polyether ether ketone (PEEK) are enlarging the procedural toolkit for patients seeking permanent mid-face projection without donor-site morbidity. Regulatory attention is intensifying—most visibly through the U.S. FDA’s August 2025 advisory committee meeting on dermal fillers, which is expected to heighten post-market surveillance but also to enhance consumer confidence in approved products.

Key Report Takeaways

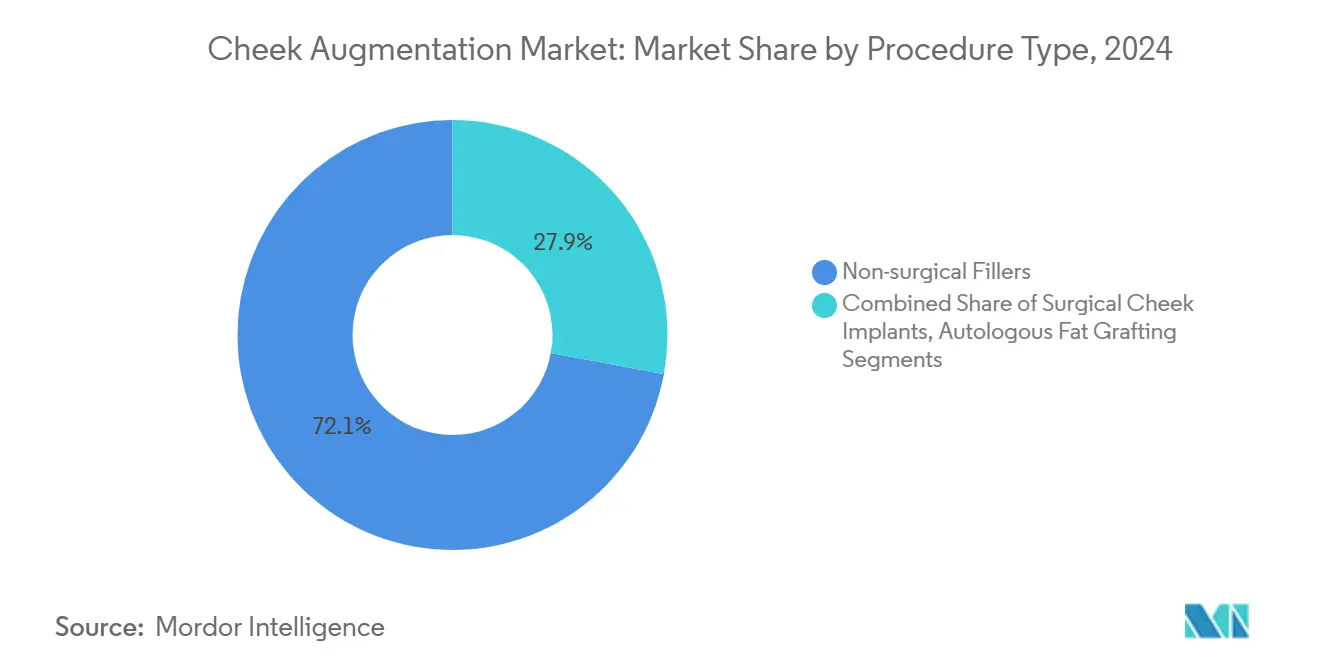

- By procedure type, non-surgical dermal fillers led with 72.1% revenue share in 2024; autologous fat grafting is advancing at a 13.2% CAGR through 2030.

- By material, silicone implants held 56.4% of the cheek augmentation market share in 2024, while PEEK implants are forecast to expand at an 11.5% CAGR to 2030.

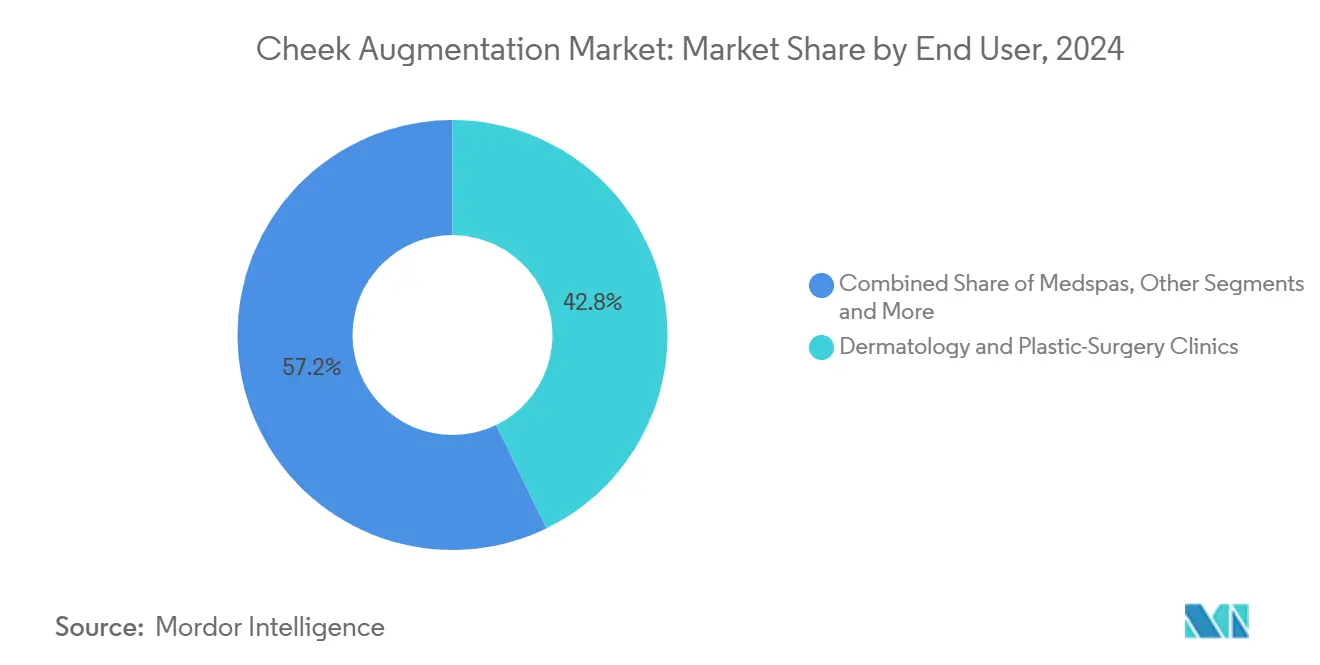

- By end-user, dermatology and plastic-surgery clinics accounted for 42.8% of the cheek augmentation market size in 2024; medspas are growing fastest at a 12.4% CAGR.

- By geography, North America commanded 38.2% share of the cheek augmentation market in 2024, whereas Asia Pacific is on track for an 11.2% CAGR during the outlook period.

Global Cheek Augmentation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for minimally invasive aesthetic procedures | +2.10% | Global; strongest in North America and Europe | Medium term (2-4 years) |

| Rapidly aging population seeking facial volume restoration | +1.80% | Global; most pronounced in developed markets | Long term (≥ 4 years) |

| Advancements in HA-based filler rheology and longevity | +1.40% | Global; early adoption in North America and Asia Pacific | Short term (≤ 2 years) |

| Social-media-driven beauty ideals and selfie culture | +1.20% | Global; urban markets across regions | Medium term (2-4 years) |

| Post-GLP-1 weight-loss patients requiring mid-face re-volumization | +0.90% | North America and Europe, expanding into Asia Pacific | Short term (≤ 2 years) |

| Rising gender-affirming facial surgeries boosting cheek work | +0.60% | North America and Europe; acceptance widening in select Asia Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Minimally Invasive Aesthetic Procedures

Global procedure statistics show a double-digit jump in injectable visits between 2019 and 2024, underscoring the structural pivot toward lunchtime treatments that fit modern work-life rhythms. HA-based fillers now arrive premixed and in finer-gauge syringes that enable micro-bolus placement, minimizing bruising and shortening downtime.[1]Plastic and Reconstructive Surgery – Global Open Editorial Team, “Hyaluronic Acid Filler Longevity in the Mid-Face: A Review,” journals.lww.com Combination therapy—such as layering HA with calcium-hydroxylapatite microspheres—delivers immediate lift and subsequent neocollagenesis, amplifying value per session. E-commerce-style booking engines used by medspas have lowered friction for first-time patients, while subscription packages bundle quarterly top-ups at predictable costs. Together, these factors propel the cheek augmentation market toward a service-oriented, consumer-convenience model.

Rapidly Aging Population Seeking Facial Volume Restoration

Facial fat-pad atrophy accelerates after age 35, reducing malar prominence and creating mid-face flattening that patients interpret as premature aging. Biostimulatory injectables such as poly-L-lactic acid activate fibroblasts, producing endogenous collagen over 24-plus months and lessening the need for frequent refills. Visual-simulation software that overlays future volume-loss trajectories helps physicians illustrate the preventive benefits of early intervention, driving uptake among high-earning millennials. In Japan, generational wealth transfer and a cultural appetite for subtle rejuvenation are simultaneously fueling demand, illustrating the global reach of this demographic driver.

Advancements in HA-Based Filler Rheology & Longevity

Cross-linker chemistry has evolved from simple BDDE bridges to proprietary dual-functional modifications that resist enzymatic degradation yet retain malleability; MRI scans have tracked HA residues up to 15 years post-injection. Galderma’s liquid neuromodulator platform employs PEARL Technology to achieve homogeneous particle dispersion, permitting smoother delivery in high-compression zones such as the zygoma. Vitamin B3-functionalized HA matrices further enhance oxidative resilience while encouraging dermal remodeling.[2]Bianca Esmonde-White et al., “Dual Functionalization of Hyaluronan Dermal Fillers with Vitamin B3,” mdpi.com These breakthroughs lower retreatment frequency, enlarge average invoice value, and support premium price points across the cheek augmentation market.

Social-Media-Driven Beauty Ideals & Selfie Culture

Academic research links heavy social-media engagement with heightened interest in cosmetic intervention, often anchored by aspirational filters that accentuate cheek contour and skin smoothness. Remote-work video calls have multiplied daily face time, exposing users to fixed-lens distortion that broadens mid-face proportions and spotlights asymmetry. Practitioners report that younger clients arrive armed with curated reference boards, accelerating decision cycles and skewing demand toward subtle, photogenic enhancements. Clinics that livestream live procedural demos gain rapid follower traction, reinforcing social proof and funneling inquiries toward cheek augmentation market providers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High out-of-pocket procedure costs | -1.70% | Global; strongest in price-sensitive emerging markets | Medium term (2-4 years) |

| Adverse-event risks and tightening regulatory scrutiny | -1.30% | Global; variable across jurisdictions | Short term (≤ 2 years) |

| Competition from energy-based skin-tightening devices | -0.90% | North America and Europe; affluent Asia Pacific segments | Medium term (2-4 years) |

| Emerging ESG pushback on polymeric implant waste | -0.60% | Europe and North America; increasing institutional influence | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Procedure Costs

Price remains the chief brake on broader adoption, with single-session injectable packages averaging USD 3,000–8,000. In Latin America and Southeast Asia, purchasing-power gaps divert patients toward off-label or uncertified fillers, elevating complication risk and depressing brand-name unit sales. U.S. installment-payment platforms seek to smooth spending spikes, yet interest charges can add 15–25% to total treatment costs. Parallel outlays for chronic GLP-1 therapy—often USD 1,000 monthly—further squeeze disposable income, forcing patients to delay elective facial work.

Adverse-Event Risks & Tightening Regulatory Scrutiny

Vascular occlusion, though infrequent, garners disproportionate media coverage, prompting cautious patients to favor reversible HA over permanent implants. The FDA’s 2025 advisory committee is expected to recommend expanded labeling requirements and mandatory ultrasound-guided training modules.[3]U.S. Food and Drug Administration, “General and Plastic Surgery Devices Panel Meeting Notice,” federalregister.gov Europe’s MDR 2017/745 already obliges filler makers to maintain continuous clinical-performance evaluation files, ratcheting compliance costs and elongating product-refresh cycles. While these measures raise barriers to entry, they may eventually consolidate confidence within the cheek augmentation market by weeding out substandard suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Procedure Type: Non-Surgical Modalities, Anchor Growth

Non-surgical dermal fillers contributed 72.1% of 2024 revenue, underscoring their role as the anchor modality inside the cheek augmentation market. Ultrafine cannulas reduce intravascular injection risk, while on-label lidocaine formulations improve patient comfort and throughput. Providers bundle fillers with botulinum toxin to soften dynamic wrinkles that can obscure newly created malar highlights, yielding synergistic outcomes. The segment’s 8.9% CAGR aligns with shifting consumer sentiment favoring outpatient fixes over full-OR sessions. Autologous fat grafting, although accounting for a smaller share, is projected to deliver the fastest 13.2% expansion; micro-fragmentation techniques allow for high-cell-viability transfer, lowering resorption rates and broadening appeal among fitness-oriented patients pursuing holistic body-and-face sculpting.

Surgical implants still retain a niche for patients requiring pronounced skeletal augmentation or long-term stability. Patient-specific PEEK devices fabricated via selective-laser-sintering shorten operating times by eliminating intra-operative carving and have lowered revision rates by up to 40% in early cohort studies. Nevertheless, recovery demands and anesthesia risks temper widespread use, keeping the surgical subset at mid-single-digit penetration within the cheek augmentation market.

By Material: Silicone Dominance Meets Polymer Innovation

Silicone held 56.4% of implant revenue in 2024, buoyed by decades of safety data, ready availability, and surgeon familiarity. Still, PEEK’s 11.5% forecast CAGR signals a steady pivot toward high-performance polymers with modulus properties closer to cortical bone. Surface-texturing and hydroxyapatite coatings promote osteointegration, reducing seroma formation and migration fears. For injectables, HA remains the workhorse, but CaHA and poly-L-lactic acid are securing double-digit traction by offering biostimulatory uplift vs mere volumization. Hybrid fillers that embed CaHA microspheres within HA gels achieve immediate lift plus ongoing collagenesis, extending retreatment intervals past 18 months—a compelling economic proposition for both patients and practices.

Manufacturers are also exploring cross-linked autologous plasma gels, banking on an all-natural positioning to placate ESG-minded consumers. Still, regulatory pathways for biologic derivatives remain opaque, likely delaying large-scale commercialization through the forecast window.

By End User: Medspas Democratize Access

Dermatology and plastic-surgery clinics encompassed 42.8% of 2024 procedures, leveraging cross-specialty talent and the ability to escalate to OR-level interventions when needed. They routinely capture complex revision cases, ensuring sustained share within the cheek augmentation industry. Medspas, however, are expanding 12.4% annually, fueled by retail-style storefronts, loyalty programs, and social-media micro-influencer partnerships that destigmatize aesthetic upkeep. Cloud-based electronic medical record (EMR) platforms help these establishments maintain physician oversight remotely, satisfying emerging state-level supervision mandates.

Hospitals and ambulatory surgical centers primarily manage reconstructive and trauma-driven cheek augmentation, comprising a smaller yet steady slice of the cheek augmentation market. Collaborations with burn units and oncology teams are common, as mid-face augmentation restores contour following ablative cancer surgeries.

By Material Technology: 3-D Printing and Smart Surfaces Differentiate Offerings

Porous polyethylene (Medpor) maintains relevance due to its tissue-ingrowth lattice, which anchors implants without bulky fixation hardware. PEEK, however, is gaining favor among surgeons seeking CT-matched geometries, improving symmetry outcomes. Researchers are piloting resorbable scaffolds fashioned from poly-L-lactide-co-ɛ-caprolactone that support tissue regeneration before gradually degrading, potentially eliminating foreign-body permanence concerns.

Simultaneously, smart surfaces that release anti-inflammatory cytokines aim to reduce capsular contracture incidence. The cheek augmentation market is also witnessing prototypes of sensor-embedded implants capable of detecting localized temperature rises that precede infection, alerting clinicians via Bluetooth to intervene early. Regulatory clarity on such cyber-physical devices is nascent, yet the competitive advantage could be sizeable once standards solidify.

Geography Analysis

North America generated 38.2% of global revenue in 2024, a reflection of mature consumer acceptance, robust insurer financing for complication management, and dense provider networks. In the United States, franchises operating under an MD-supervision model deliver fillers at suburban retail plazas, broadening reach beyond affluent coastal cities. Cross-border flow from Canada into U.S. border states hinges on favorable exchange rates, while Mexico continues to attract U.S. residents pursuing lower-cost surgical implants packaged with medical-tourism hospitality. The cheek augmentation market in North America remains innovation-centric; early-adopter clinicians are piloting AI-guided ultrasound visualization for real-time vascular mapping, a tool expected to compress procedure-time variability.

Europe’s share reflects heterogeneous adoption curves, but unified MDR compliance is leveling standards and fostering cross-border product harmonization. Germany and the United Kingdom lead procedural volumes; specialized filler referral networks in London’s Harley Street district and Munich’s Maximilianstrasse command premium pricing tiers. France and Italy exhibit momentum among millennial patients aligning facial aesthetics with luxury-fashion consumption. Southern European clinics promote winter-season recovery packages, capitalizing on mild climates to shorten postoperative swelling windows. Pan-European consumer preference skews toward understated results, nudging physicians to favor biostimulatory injectables and micro-bolus HA techniques that integrate seamlessly with regional beauty ideals.

Asia Pacific is the fastest-growing zone, expected to log an 11.2% CAGR through 2030. China’s rising middle class now considers mid-face volume optimization part of regular dermatologic maintenance, particularly among live-streaming influencers seeking flawless camera profiles. Regulatory complexities necessitate domestic clinical trials even for internationally approved fillers, delaying launches but spawning joint ventures that localize manufacturing. South Korea’s “small-face” aesthetic places strong emphasis on malar projection to create a V-line taper, pushing both filler artistry and micro-implant adoption. Japan’s preference for minimally invasive solutions aligns with its super-aging society, where subtlety and low downtime are prized. India and Southeast Asia remain price-elastic but represent long-term volume pools as urbanization and disposable income climb.

Competitive Landscape

Global market power rests with diversified pharmaceutical-cosmetic hybrids such as AbbVie (Allergan Aesthetics) and Galderma, each wielding vertically integrated pipelines spanning neurotoxins, fillers, regenerative cosmeceuticals, and digital-consultation platforms. AbbVie’s Juvederm family maintains its flagship status, yet revenue tempering in legacy SKUs is prompting investment in dual-phase products that merge HA with bioresorbable microspheres. Galderma’s record USD 1.129 billion Q1 2025 aesthetic sales underscore pricing power secured through first-in-class liquid neuromodulators.

Mid-tier innovators focus on device-material convergence; companies are pairing monopolar radio-frequency systems with immediate filler top-ups, offering bundled pricing that lifts overall ticket size while mitigating downtime. PEEK specialists leverage proprietary CAD software and surgeon co-design portals to lock in repeat orders. Meanwhile, private-equity-backed clinic chains expand their footprint via roll-ups, using centralized marketing and shared-services economics to capture local patient funnels.

Barriers to entry pivot on clinical-evidence requirements and distribution compliance. The FDA’s evolving Unique Device Identification (UDI) mandates necessitate real-time batch traceability, favoring incumbents with digital supply-chain infrastructure. Across Europe, MDR-required person-responsible-for-regulatory-compliance roles increase fixed costs, hampering smaller filler importers. Nonetheless, white-space remains in personalized implants and ESG-certified materials, areas where agile entrants could carve defensible niches.

Cheek Augmentation Industry Leaders

AbbVie (Allergan Aesthetics)

Galderma SA

Merz Aesthetics

Implantech Associates

Stryker Corp. (CMF)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: AbbVie’s Allergan Aesthetics debuted the AA Signature Program, codifying comprehensive cheek-augmentation protocols for global practitioner rollout.

- August 2024: Crown Laboratories announced a USD 924 million acquisition of Revance Therapeutics, integrating Daxxify neurotoxin with RHA fillers to widen product coverage across the cheek augmentation market.

- July 2024: FDA scheduled an August 2025 public meeting on dermal fillers, foreshadowing labeling and training updates relevant to all cheek-augmentation providers.

Global Cheek Augmentation Market Report Scope

| Non-surgical Dermal Fillers |

| Surgical Cheek Implants |

| Autologous Fat Grafting |

| Implant | Silicone |

| Porous Polyethylene (Medpor) | |

| Poly-Ether-Ether-Ketone (PEEK) | |

| Others (Hydroxyapatite, PMMA) | |

| Filler Composition | Hyaluronic Acid (HA) |

| Calcium Hydroxylapatite (CaHA) | |

| Poly-L-Lactic Acid (PLLA) | |

| Autologous Fat Micro-lipoinjection | |

| PMMA Microspheres |

| Hospitals & Surgical Centers |

| Dermatology & Plastic-Surgery Clinics |

| Medspas |

| Others (Ambulatory / Specialty Centers) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Procedure Type | Non-surgical Dermal Fillers | |

| Surgical Cheek Implants | ||

| Autologous Fat Grafting | ||

| By Material | Implant | Silicone |

| Porous Polyethylene (Medpor) | ||

| Poly-Ether-Ether-Ketone (PEEK) | ||

| Others (Hydroxyapatite, PMMA) | ||

| Filler Composition | Hyaluronic Acid (HA) | |

| Calcium Hydroxylapatite (CaHA) | ||

| Poly-L-Lactic Acid (PLLA) | ||

| Autologous Fat Micro-lipoinjection | ||

| PMMA Microspheres | ||

| By End User | Hospitals & Surgical Centers | |

| Dermatology & Plastic-Surgery Clinics | ||

| Medspas | ||

| Others (Ambulatory / Specialty Centers) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the global cheek augmentation market in 2025?

It is valued at USD 4.73 billion in 2025 and is set to reach USD 6.97 billion by 2030, reflecting an 8.2% CAGR.

Which procedure type currently dominates cheek enhancement demand?

Non-surgical dermal fillers account for 72.1% of global revenue, thanks to quick recovery times and continuous product innovation.

Which region is growing fastest for cheek enhancement treatments?

Asia Pacific is forecast to expand at an 11.2% CAGR through 2030, led by China, South Korea, and Japan.

What material is gaining popularity over traditional silicone implants?

PEEK implants are projecting an 11.5% CAGR because of bone-like mechanics and customizable 3-D-printed designs.

Why are medspas important to market expansion?

Medspas deliver convenient, retail-style services and are expanding 12.4% annually, making cheek augmentation more accessible to new demographics.

What regulatory trend should providers monitor?

The FDAs August 2025 advisory panel on dermal fillers may introduce stricter labeling and training prerequisites, affecting practice workflows.

Page last updated on: