Skin Tightening Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

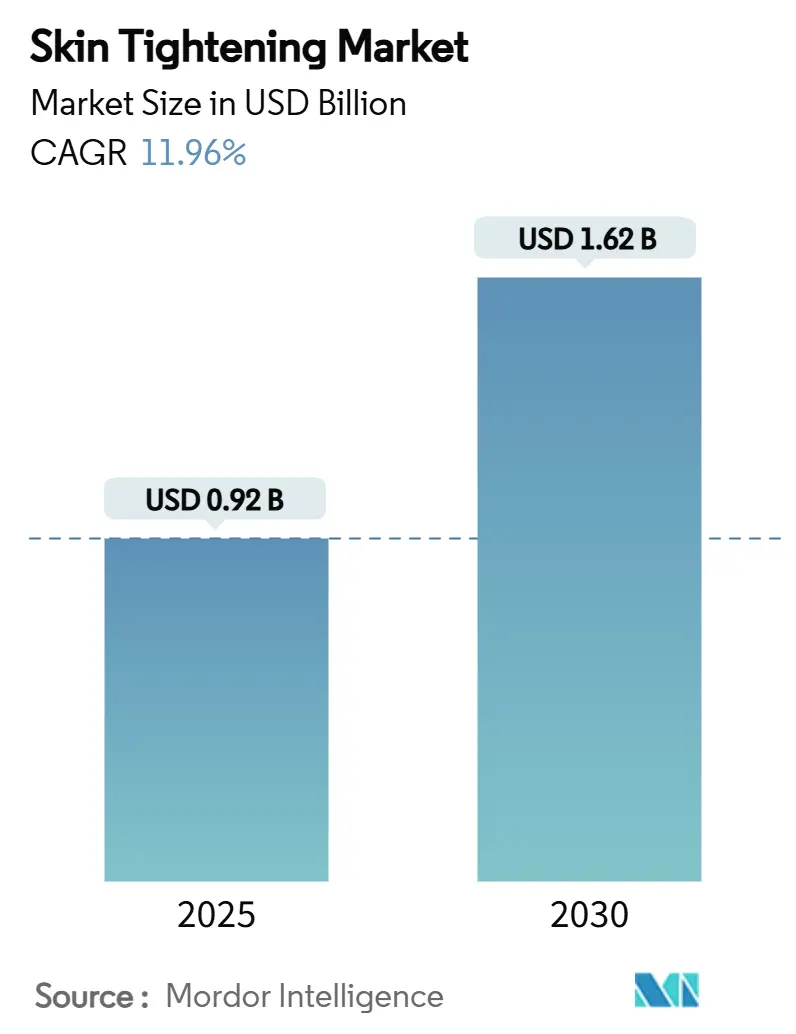

| Market Size (2025) | USD 0.92 Billion |

| Market Size (2030) | USD 1.62 Billion |

| Growth Rate (2025 - 2030) | 11.96% CAGR |

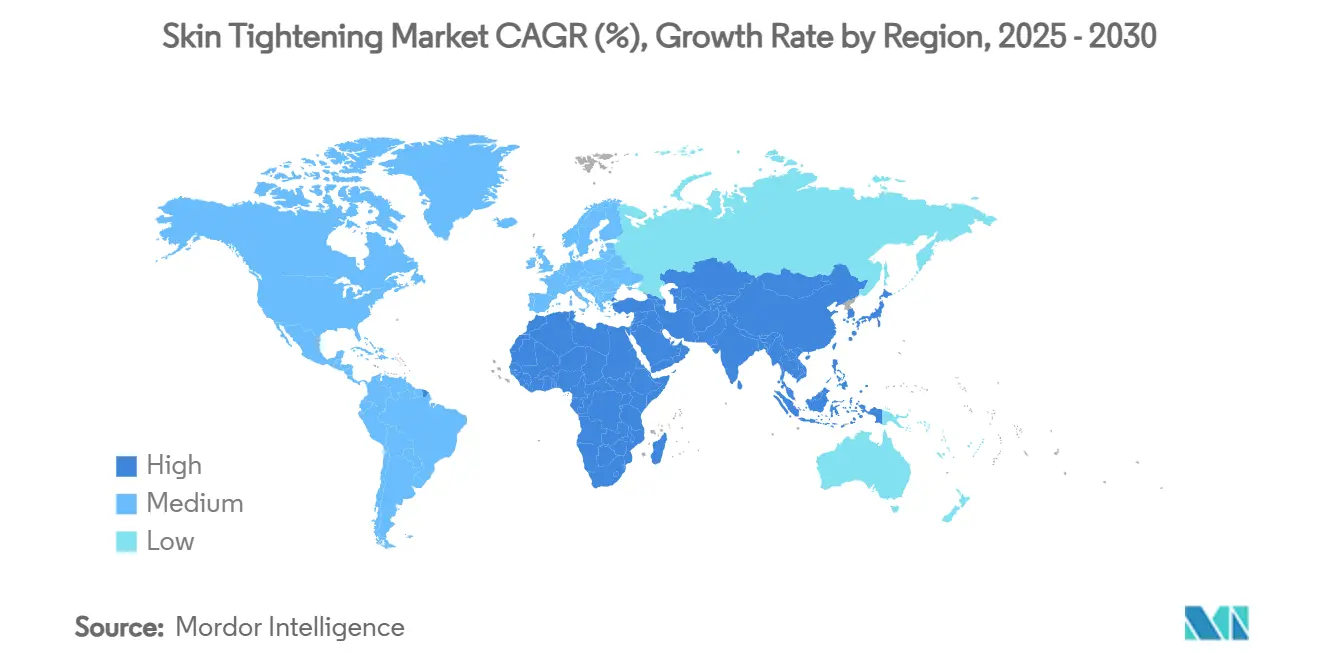

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Skin Tightening Market Analysis by Mordor Intelligence

The global skin tightening market size reached USD 0.922 billion in 2025 and is projected to climb to USD 1.62 billion by 2030, translating into an 11.96% CAGR over the forecast window. Rapid uptake of GLP-1 weight-loss medicines is producing an influx of patients with post-reduction skin laxity, and 62.4% of this cohort now cites sagging skin as its principal concern. Combination radiofrequency–ultrasound platforms have re-energized provider economics, while at-home systems broaden access for value-oriented consumers. North America maintains leadership through strong disposable income and well-established clinic networks; Asia-Pacific shows the fastest trajectory as middle-class populations expand and beauty culture intensifies. Regulatory clarity on over-the-counter radiofrequency devices is shrinking the gulf between clinical and consumer channels, and insurance pilots for medically necessary dermatologic care could further enlarge the candidate pool.

Key Report Takeaways

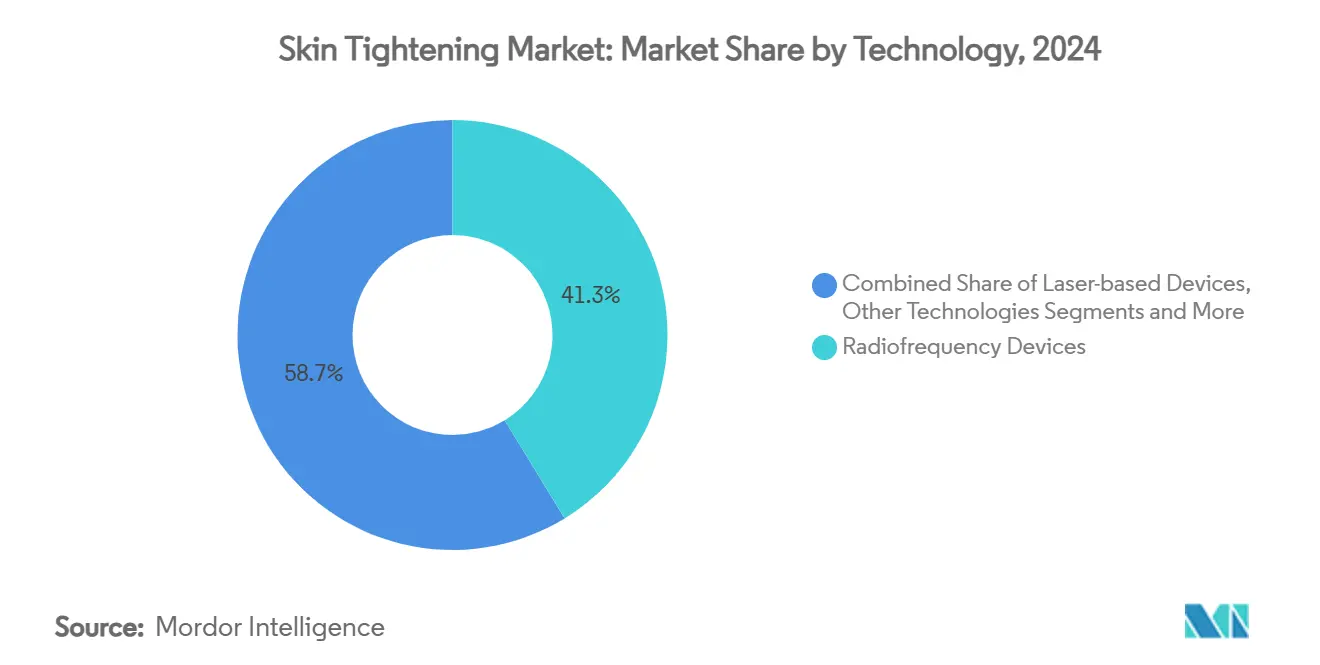

- By technology, radiofrequency commanded 41.26% of skin tightening market share in 2024, whereas combination/hybrid systems are set to pace a 14.78% CAGR through 2030.

- By product type, stand-alone systems contributed 46.32% revenue in 2024; portable and hand-held devices are forecast to advance at 13.34% CAGR to 2030.

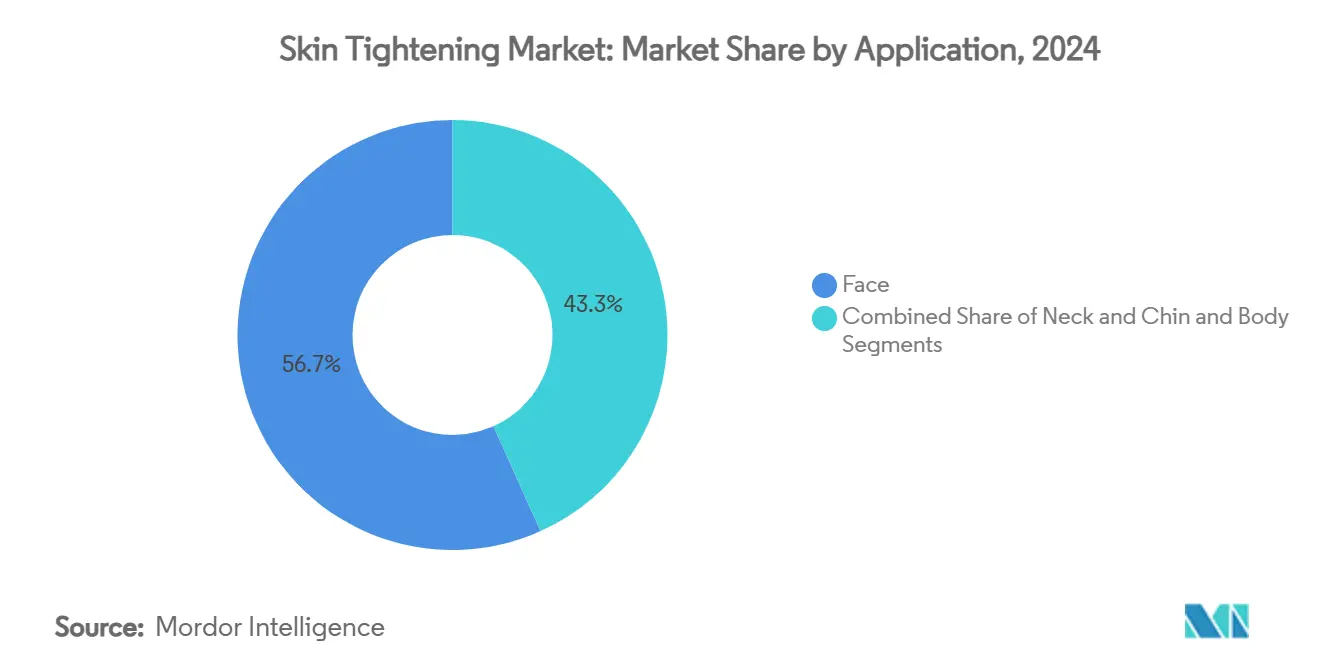

- By application, the face segment held 56.72% of the skin tightening market size in 2024; body treatments are tracking a 13.09% CAGR over 2025–2030.

- By end-user, aesthetic clinics retained 51.33% share in 2024, while the home-use channel is rising at a 15.02% CAGR through 2030.

- By geography, North America captured 36.77% revenue in 2024; Asia-Pacific is projected to grow at 13.76% CAGR, the fastest regional pace.

Global Skin Tightening Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for non-invasive procedures | +2.1% | Global – strongest in North America & APAC | Medium term (2-4 years) |

| Aging population with higher disposable income | +1.8% | North America & Europe core, extending to APAC | Long term (≥ 4 years) |

| Rising influence of social media & beauty | +1.5% | Global – peak in APAC & Latin America | Short term (≤ 2 years) |

| Technological advances in energy-based devices | +2.3% | Global – led by North America & Europe innovation hubs | Medium term (2-4 years) |

| Shift toward at-home skin-tightening tools | +1.9% | North America & Europe early, APAC following | Medium term (2-4 years) |

| Insurance coverage expansion | +0.8% | North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Non-Invasive Procedures

Non-surgical interventions now dominate the therapeutic mix, reflecting consumer preference for minimal downtime and the safety profile of energy-based technologies. Tele-working culture heightened awareness of appearance on digital platforms, stimulating incremental clinic visits for subtle refinement. Monopolar radiofrequency continues to show statistically significant improvements in laxity at both 12- and 24-week checkpoints without adverse events.[1]Young-Min Lee, “Efficacy and Safety of Monopolar Radiofrequency for Facial Laxity,” Cosmetics, mdpi.com The skin tightening market is therefore positioned as a first-line option for patients unwilling to contemplate surgical lifts, and its alignment with weight-management drug trends drives further scale.

Aging Population with Higher Disposable Income

Baby-boom consumers sustain demand as they move into retirement with record household wealth and heightened longevity expectations. Clinical observations link natural collagen depletion to visible sagging, a change that motivates elective intervention. Eight-week supplementation studies have reported 17.1% gains in elasticity, underscoring the appetite for multimodal regimens that pair nutrition and in-office treatment. Providers are thus bundling collagen stimulators with device sessions to lift perceived value and capture larger share-of-wallet in the skin tightening market.

Rising Influence of Social Media & Beauty Culture

Daily exposure to filtered imagery elevates aesthetic expectations and compresses adoption cycles. Influencer testimonials on TikTok and Instagram routinely highlight procedure journeys, normalizing the decision for young cohorts. The “selfie effect” keeps facial lines and jaw definition under constant scrutiny, motivating early engagement with non-ablative tightening solutions. Demand is also geographically elastic; Latin America and Southeast Asia show rapid uptake as localized content creators promote attainable beauty ideals.

Technological Advances in Energy-Based Devices

Platform innovation is moving from single-modality consoles toward AI-directed, multi-source systems. Integration of impedance monitoring and real-time cooling cuts discomfort while maintaining uniform thermal profiles. A compact metamaterial waveguide antenna raised intradermal temperature by 11.6 °C using only 20 W, signalling fresh efficiency benchmarks.[2]Hyo-Sang Kim, “Metamaterial Waveguide Antenna for RF Tightening,” Frontiers in Bioengineering and Biotechnology, frontiersin.org Emerging micro-coring tools have secured approvals in Canada and Saudi Arabia, broadening the clinical armamentarium. These advances collectively reinforce practitioner confidence and fuel the next expansion phase of the skin tightening market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure costs in emerging economies | -1.4% | APAC emerging markets, Latin America, MEA | Medium term (2-4 years) |

| Stringent device approval & regulatory hurdles | -0.9% | Global – strongest in North America & Europe | Long term (≥ 4 years) |

| Limited clinical evidence for long-term results | -1.1% | Global – premium segment | Medium term (2-4 years) |

| Shortage of trained aesthetic professionals | -1.6% | Global – most acute in emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Procedure Costs in Emerging Economies

A single radiofrequency session in Pune averages INR 5,500 (USD 66) versus USD 500-2,000 in the United States, creating stark affordability gaps. Import tariffs and volatile exchange rates elevate capital costs for devices, forcing clinics to charge premiums that cap patient volumes. Without local manufacturing scale, the skin tightening market in lower-income areas remains dependent on a thin affluent clientele.

Shortage of Trained Aesthetic Professionals

Certification pathways differ markedly across regions, and hands-on fellowships struggle to keep pace with device complexity. Insufficient anatomical training can increase adverse events, prompting tighter oversight and longer approval windows.[3]Alex Thiersch, “Training Requirements for Safe Med-Spa Practice,” American Med Spa Association, americanmedspa.org The resulting scarcity of skilled operators lengthens appointment wait times and slows geographic expansion of the skin tightening market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Radiofrequency Holds the Lead as Hybrid Systems Accelerate

Radiofrequency platforms accounted for 41.26% of the skin tightening market share in 2024, underscoring their long-standing role as the industry’s reference technology. Their non-invasive thermal profile stimulates fibroblast activity without downtime, which secures steady repeat-use revenues for clinics. Ultrasound and laser devices add depth-specific options, yet they trail radiofrequency on versatility and consumable cost efficiency. The segment’s innovation spotlight is now on hybrid consoles that merge radiofrequency with ultrasound, microneedling or electromagnetic pulses to address multiple concerns in a single session. These integrated systems are forecast to post a 14.78% CAGR through 2030, a pace that will gradually rebalance category economics toward multifunction workstations.

Combination technology also lowers capital risk for new entrants because one chassis covers several indications. Providers report higher utilization rates when hybrid tips are available, which improves payback periods and shields against rapid obsolescence. Electrical-stimulation research that targets Kv1.3 ion channels hints at the next modality likely to join the platform mix. Manufacturers are therefore embedding software upgradability so clinics can unlock new modes without buying fresh hardware. This design philosophy supports long-run stickiness and will keep technology at the center of skin tightening market size expansion over the forecast horizon.

By Product Type: Portables Challenge the Reign of Stand-Alone Towers

Stand-alone systems generated 46.32% of 2024 revenue, reflecting their superior power output and robust cooling that suits high-volume practices. Their large footprints often include advanced imaging and AI-guided protocols that refine dosage in real time. Even so, portable and hand-held devices are advancing at a 13.34% CAGR to 2030 as chains value equipment that can shuttle between rooms or clinics. Portables also feed the at-home channel, where prosumer buyers demand professional-grade outputs packed into countertop form factors. Venus Versa Pro is a case in point, delivering multiple modes through a suitcase-sized base that plugs into standard outlets.

Consumables and applicator tips remain vital but now lean toward reusable designs that reduce per-treatment costs. Face-conforming LED masks with 3,770 micro-LEDs have bridged the gap further by posting 340% gains in dermal elasticity during trials, proving that miniaturization can still match clinical benchmarks. Clinics hedge against revenue erosion by bundling device-based therapies with injectables or topical biologics, services not easily replicated at home. This dual-channel dynamic will keep both towers and portables relevant and together they will underpin future skin tightening market size growth.

By Application: Body Zones Move to the Forefront After Facial Dominance

Facial procedures held 56.72% of the 2024 skin tightening market share, a position earned through decades of consumer focus on visible features. Providers rely on predictable anatomy and well-studied energy parameters to deliver consistent outcomes around cheeks, periorbital folds and jawlines. Yet the rise of GLP-1 weight-loss drugs has pushed arms, abdomen and thighs into the spotlight, creating a 13.09% CAGR runway for body applications through 2030. Post-weight-loss patients often schedule bundled protocols that blend RF tightening with cryolipolysis or ultrasound contouring to smooth residual laxity.

Neck and submental areas also gain attention, driven by constant video-call exposure that highlights under-chin sagging. Combined radiofrequency and ultrasound sessions can lift skin firmness in as little as 12 weeks, improving cervical angle definition without incisions. Clinics respond by marketing full-body packages that sequence upper-face, lower-face and torso treatments over several months. This holistic approach deepens patient engagement and anchors recurring maintenance visits, fortifying the broader skin tightening market size across diverse anatomical targets.

By End-User: Home-Use Devices Reshape the Care Continuum

Aesthetic clinics retained 51.33% revenue leadership in 2024 thanks to physician oversight, anesthesia options and adjunct modalities that raise perceived safety. Hospital outpatient suites contribute reconstructive cases, but their share stays modest because insurers still classify most tightening work as elective. Meanwhile, the home-use segment is sprinting at a 15.02% CAGR as regulatory shifts allow over-the-counter radiofrequency tools once limited to professionals. One-time device purchases appeal to cost-sensitive users who balk at repeat clinical fees.

Adverse-event reports of burns and pigmentation changes highlight the need for rigorous instructions and smart sensors that shut down on overheating. Manufacturers increasingly preload treatment algorithms to lock unsafe settings, a feature that reassures first-time buyers. Clinics adapt by offering hybrid pathways: an initial in-office session establishes baseline results, then take-home gadgets manage maintenance until the next annual review. This blended model widens the funnel for novices while preserving long-term physician oversight, keeping every channel integral to overall skin tightening market share dynamics.

Geography Analysis

North America commanded 36.77% of the skin tightening market share in 2024, reflecting a mature clinic ecosystem, high discretionary spending and favorable reimbursement pilots. The United States drives most procedures through dense provider networks, while Canada’s 2025 clearance of the XERF radiofrequency system underscores the region’s openness to device upgrades. Mexico leverages competitive pricing and medical-tourism inflows to broaden access, though home-use devices are beginning to siphon lower-acuity cases. Regulatory approval of over-the-counter radiofrequency tools in May 2025 further blurs the line between clinical and consumer channels, a shift that could temper clinic growth but expand overall skin tightening market size through higher total user penetration.

Asia-Pacific is projected to pace a 13.76% CAGR to 2030, the fastest regional climb in the global skin tightening market. Korea anchors innovation; the 2024 merger of Cynosure and Lutronic created a cross-border platform that amplifies R&D scale and distribution reach. China and India contribute large pools of price-sensitive consumers who favor portable devices, prompting manufacturers to localize assembly and trim import duties. Japan’s aging population sustains high per-capita procedure counts, while Southeast Asian hubs such as Thailand and Malaysia ride inbound medical-tourism flows. Collectively, these vectors position the region to challenge North America’s revenue lead before decade-end.

Europe records steady mid-single-digit expansion, underpinned by Germany, France and the United Kingdom, though stringent CE-mark timelines can slow new modality rollout. Eastern European markets edge upward as disposable income rises and cross-border clinic chains expand. Latin America’s large patient volumes center on Brazil and Mexico, where aesthetic culture is entrenched and procedure bundles attract international travelers. In the Middle East and Africa, premium demand clusters in the Gulf Cooperation Council; Saudi Arabia’s 2025 approval of micro-coring technology signals regulatory maturation and growing appetite for advanced solutions. These emerging territories collectively add depth to the skin tightening market size by drawing new consumer strata into the aesthetic continuum.

Competitive Landscape

The industry remains moderately fragmented. Market leaders defend share by broadening portfolios into hybrid consoles and AI-guided treatment software, strategies that lengthen product lifecycles and lock in upgrade pathways. Consolidation momentum resurfaced in April 2024 when Hahn & Company combined Cynosure and Lutronic, creating a diversified powerhouse that straddles premium clinic towers and portable lines.

Strategic moves in 2025 highlight the race to refresh pipelines. Apyx Medical secured FDA clearance for a next-generation body-contouring platform, reinforcing its foothold in energy-based devices. Cutera announced divestitures aimed at boosting liquidity and concentrating on core radiofrequency franchises. Candela expanded indications for its Matrix RF system after an FDA green light for facial-wrinkle treatment, a move that widens consumable pull-through. Such approvals keep established brands front-of-mind with practitioners who prize regulatory pedigree.

Investor appetite for disruptive entrants remains robust. Acclaro Medical closed a USD 23 million Series B round in May 2025 to commercialize novel skin-laser architectures that promise shorter sessions and lower consumable costs. Start-ups targeting AI-driven parameter optimization and consumer-grade micro-energy wearables signal a future where software and hardware co-evolve. Competitive intensity therefore centers on versatility and data-guided personalization rather than raw energy output alone, a pivot that should preserve pricing power even as at-home devices gain ground in the global skin tightening market.

Skin Tightening Industry Leaders

Hologic Inc.

BTL Industries

InMode Ltd.

Cutera Inc.

Venus Concept Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Apyx Medical won FDA clearance for a new body-contouring radiofrequency device, broadening its energy-based suite.

- April 2025: Health Canada cleared the Cynosure Lutronic XERF platform for skin-tightening use, enhancing regional device options.

- April 2024: Hahn & Company initiated the merger between Cynosure and Lutronic, consolidating complementary portfolios.

Global Skin Tightening Market Report Scope

| Radiofrequency-based Devices |

| Ultrasound-based Devices |

| Laser-based Devices |

| Cryolipolysis Devices |

| Combination / Hybrid Platforms |

| Other Technologies |

| Stand-alone Skin-Tightening Systems |

| Portable / Hand-held Devices |

| Consumables & Accessories |

| Face |

| Neck & Chin |

| Body |

| Aesthetic Clinics |

| Hospitals |

| Beauty Centers & Spas |

| Home-use |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Radiofrequency-based Devices | |

| Ultrasound-based Devices | ||

| Laser-based Devices | ||

| Cryolipolysis Devices | ||

| Combination / Hybrid Platforms | ||

| Other Technologies | ||

| By Product Type | Stand-alone Skin-Tightening Systems | |

| Portable / Hand-held Devices | ||

| Consumables & Accessories | ||

| By Application | Face | |

| Neck & Chin | ||

| Body | ||

| By End-user | Aesthetic Clinics | |

| Hospitals | ||

| Beauty Centers & Spas | ||

| Home-use | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the skin tightening market by 2030?

It is expected to reach USD 1.62 billion by 2030, growing at an 11.96% CAGR.

Which technology currently leads the skin tightening market?

Radiofrequency systems supply 41.26% of global revenue, reflecting their mature safety and efficacy profile.

Why is Asia-Pacific the fastest-growing region?

Expanding middle-class populations, heightened social-media influence and increased clinic investment are propelling a 13.76% CAGR in the region.

How fast is the home-use segment growing?

Home-use devices are forecast to expand at a 15.02% CAGR as consumers prioritize convenience and cost savings.

Page last updated on: