Cosmetic Surgery And Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

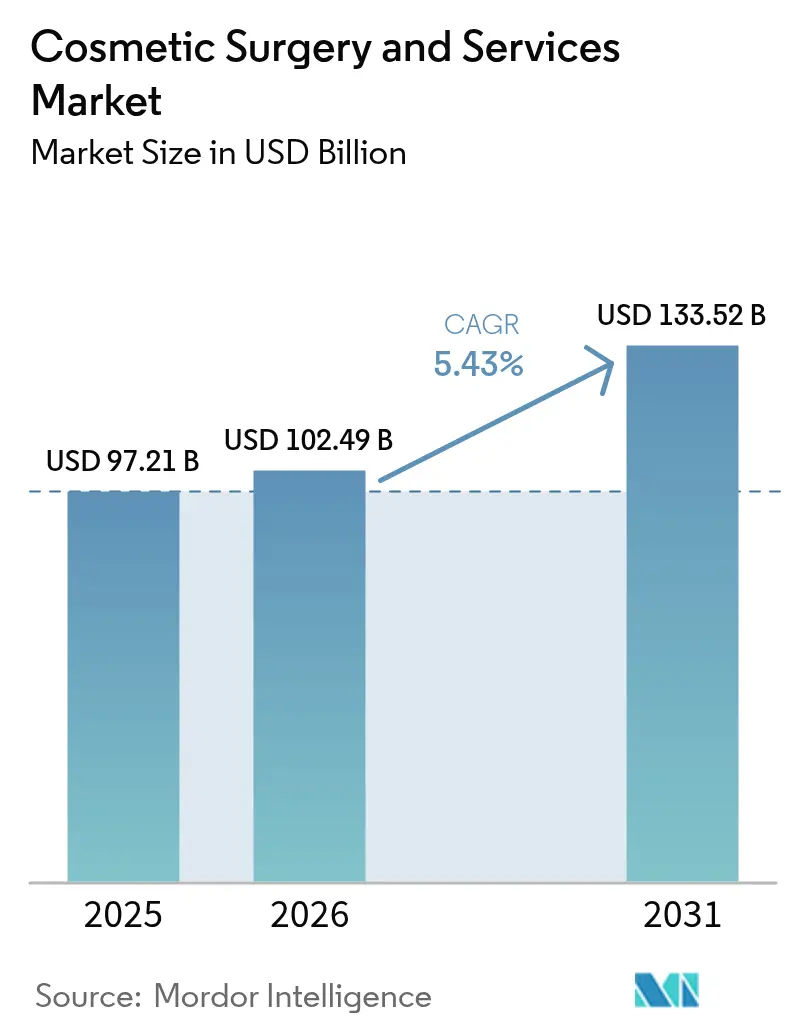

| Market Size (2026) | USD 102.49 Billion |

| Market Size (2031) | USD 133.52 Billion |

| Growth Rate (2026 - 2031) | 5.43% CAGR |

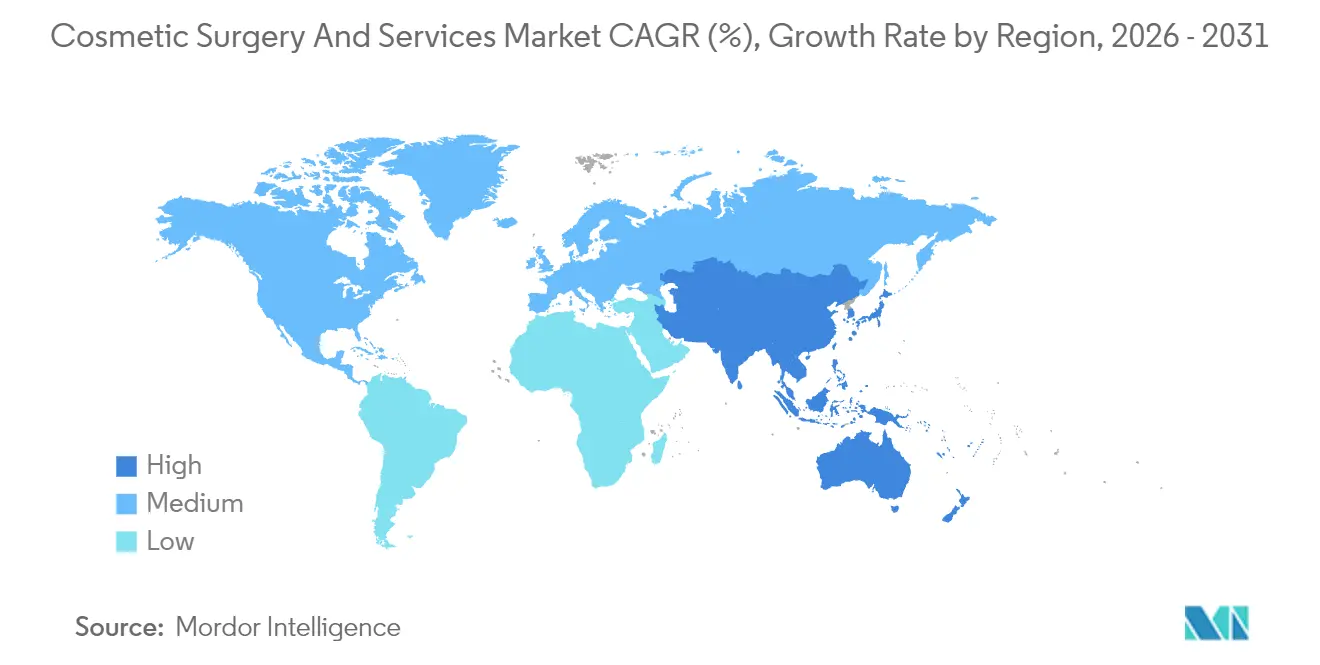

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

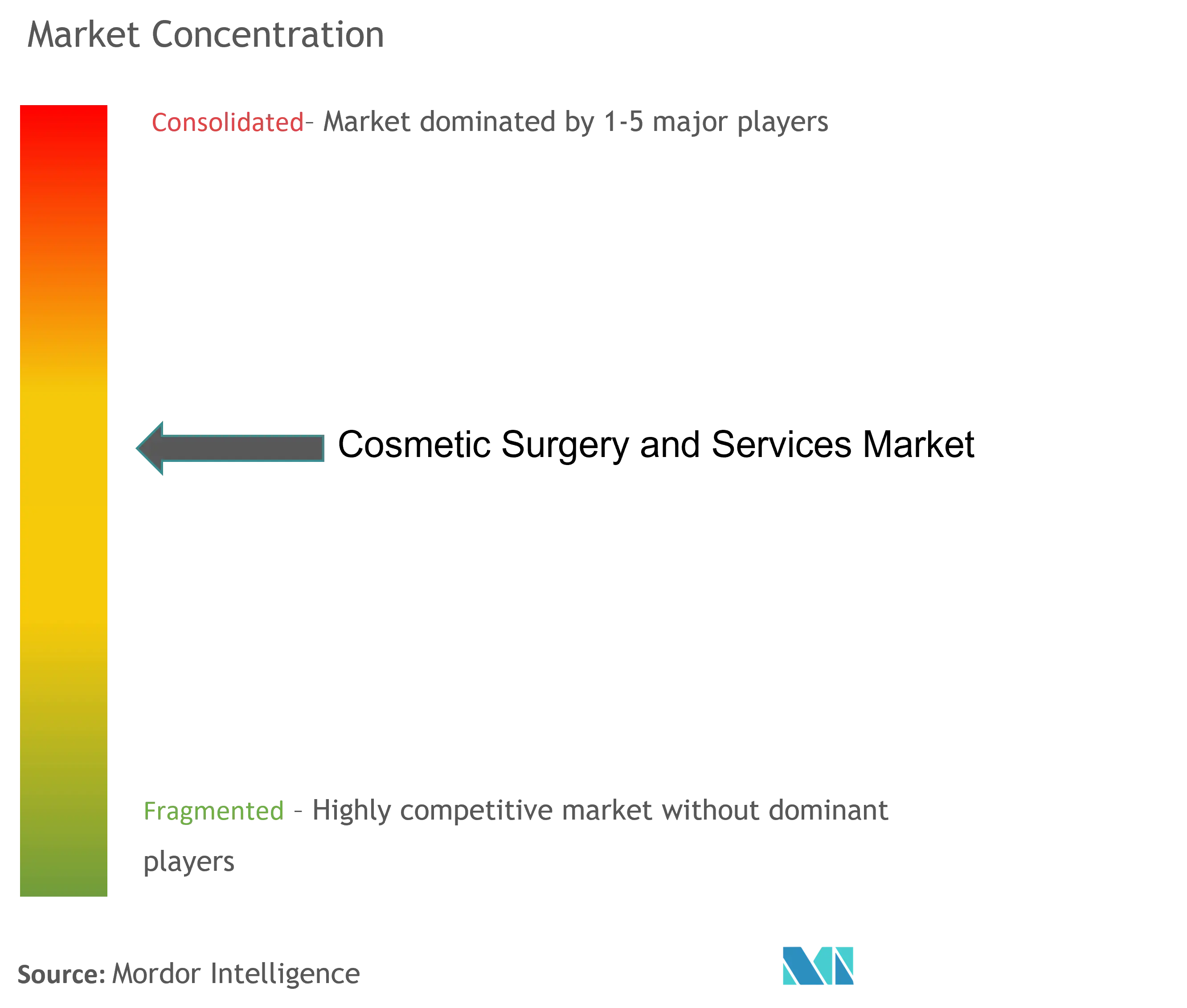

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cosmetic Surgery And Services Market Analysis by Mordor Intelligence

The cosmetic surgery & services market size was valued at USD 97.21 billion in 2025 and estimated to grow from USD 102.49 billion in 2026 to reach USD 133.52 billion by 2031, at a CAGR of 5.43% during the forecast period (2026-2031). Accelerated adoption of minimally invasive technologies, demographic shifts toward aesthetic self-optimization, and widening clinical indications for injectables are anchoring demand across both developed and emerging economies. Volume growth is reinforced by the 300% surge in GLP-1 weight-loss prescriptions that is generating incremental procedure needs, while social-media-mediated beauty standards continue to raise awareness and lower the psychological barrier to first-time treatment uptake. Consolidation among multi-specialty clinic chains is unlocking scale benefits in marketing, procurement, and digital engagement, thereby raising competitive thresholds for smaller providers. Although regulatory tightening around licensing, advertising, and product authentication is elevating compliance costs, the cosmetic surgery & services market remains structurally positioned for sustainable expansion through the decade.

Key Report Takeaways

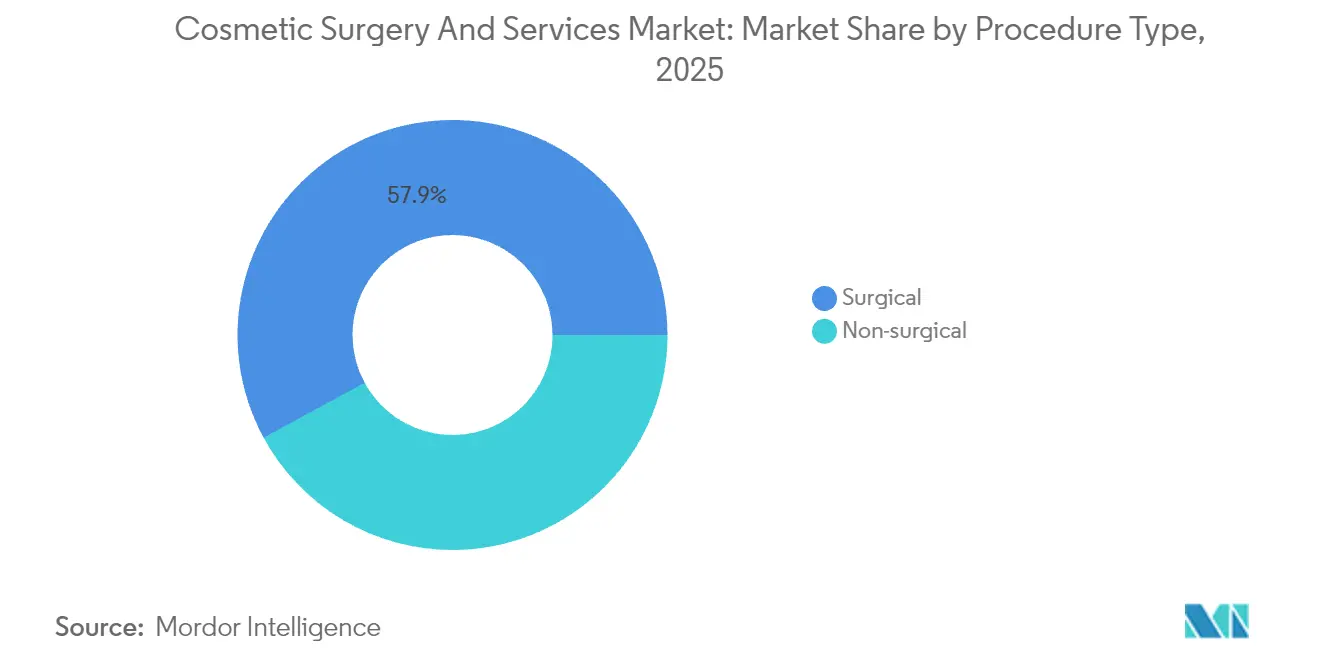

- By procedure type, surgical interventions led with 57.92% revenue share in 2025, whereas non-surgical modalities are projected to record the fastest 7.28% CAGR through 2031.

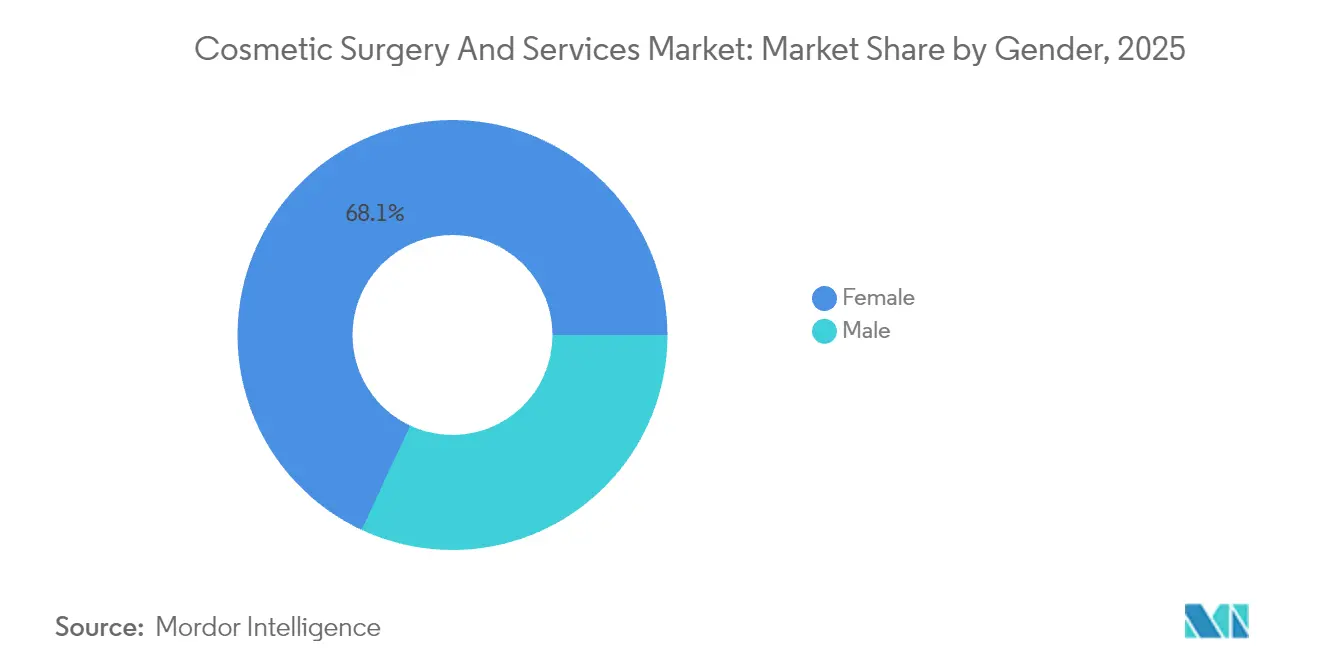

- By gender, female patients accounted for 68.05% of the cosmetic surgery & services market size in 2025; male clientele is advancing at a 6.88% CAGR to 2031.

- By age group, the 35-50 cohort captured 48.01% of cosmetic surgery & services market share in 2025, while the 18-34 segment is forecast to expand at 7.19% CAGR.

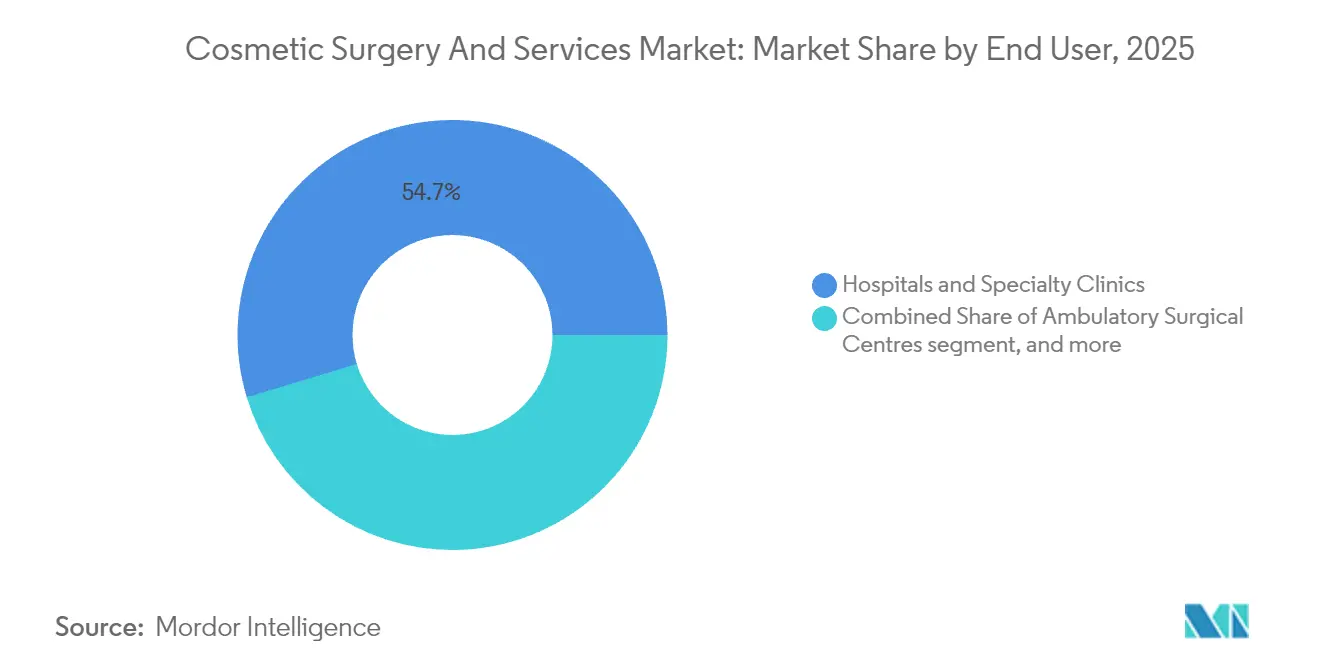

- By end user, hospitals & specialty clinics held 54.68% share of the cosmetic surgery & services market in 2025; medical spas are expected to post the highest 7.86% CAGR through 2031.

- By body area, face & head treatments contributed 61.72% of cosmetic surgery & services market size in 2025, whereas body & extremities procedures are growing at an 7.71% CAGR.

- By geography, North America dominated with 42.13% share in 2025, yet Asia-Pacific is projected to grow the fastest at 6.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cosmetic Surgery And Services Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for minimally & non-invasive procedures | 2.1% | Global, with early gains in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Technological advances in energy-based & injectable devices | 1.8% | Global, spill-over from developed to emerging markets | Long term (≥ 4 years) |

| Rising social-media-led beauty consciousness | 1.2% | Global, particularly strong in APAC and North America | Short term (≤ 2 years) |

| GLP-1 weight–loss drugs boosting post-loss contouring demand | 0.9% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Private-equity roll-ups creating clinic capacity & marketing muscle | 0.7% | North America core, spill-over to Europe | Long term (≥ 4 years) |

| AI-driven outcome simulation increasing first-time conversions | 0.5% | Developed markets initially, global expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Minimally & Non-Invasive Procedures Reshapes Treatment Paradigms

Non-surgical modalities now constitute 80% of all facial plastic procedures, with neurotoxins and dermal fillers favored across every age group[1]American Academy of Facial Plastic and Reconstructive Surgery, “2024 Annual Member Survey,” aafprs.org. Superior efficacy of fractional lasers, radiofrequency microneedling, and high-intensity focused ultrasound is shortening recovery windows, thereby elevating patient throughput and revenue per clinic hour. Younger consumers regard injectables as preventive care rather than corrective medicine, which is lengthening patient lifecycles and stabilizing recurring revenue streams. The cosmetic surgery & services market is benefiting from regulatory frameworks such as updated FDA guidance that raise quality thresholds and legitimize new treatment indications. Integration of combination protocols—for example toxin–filler pairings followed by light energy resurfacing—is further pushing the non-surgical CAGR beyond its surgical counterpart, reinforcing a structural shift in the procedure mix.

Technological Advances in Energy-Based Devices Create New Revenue Streams

AI-enabled skin analyzers, robotic injectors, and precision energy platforms are delivering outcomes historically limited to operating rooms. Treatment customization driven by software algorithms translates into higher satisfaction scores and word-of-mouth referrals, thus compressing patient acquisition costs. Radiofrequency microneedling and fractional CO₂ systems are capturing premium price points due to visible collagen remodeling within abbreviated downtime windows. Device manufacturers are co-developing exosome-enhanced protocols that merge regenerative medicine with energy delivery, producing hybrid treatments that support price differentiation. Asia-Pacific innovation hubs are accelerating iterative product updates, shortening global launch cycles and broadening the cosmetic surgery & services market addressable base.

Social Media Influence Drives Unprecedented Procedure Consideration Rates

Consumers exposed to more than four hours of aesthetic content daily exhibit an 87.9% likelihood of contemplating a cosmetic procedure. Platform filters that idealize skin texture and facial symmetry normalize aesthetic modification, while “dupe culture” encourages real-world replication of digital enhancements. The phenomenon has evolved into communal behavior as users collectively pursue “beauty fandom” ideals. Clinics report that prospective patients now arrive with curated reference images that dictate precise treatment objectives, compressing consultation time yet raising the bar for delivering individualized results. The cosmetic surgery & services market is consequently allocating larger budgets to social-media-native education campaigns aimed at shaping expectations and mitigating misinformation.

GLP-1 Weight-Loss Medications Generate Unexpected Aesthetic Demand

Prescription volumes for GLP-1 analogs have climbed 300%, and clinicians are documenting a 50% uptick in fat-grafting requests to counteract “Ozempic face” volume depletion. Body-contouring inquiries also escalate as rapid weight loss yields skin laxity and contour irregularities. Providers are developing integrated care pathways that stage skin tightening and volumization around predictable pharmacologic milestones. Cross-referral models between bariatric specialists and aesthetic surgeons are monetizing contiguous patient needs, broadening cosmetic surgery & services market penetration among health-motivated populations.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory approvals & practitioner-licensing gaps | -1% | Global | Long term (≥ 4 years) |

| Post-procedure side-effects & safety worries | -0.8% | Global | Medium term (2-4 years) |

| Tariff-driven cost spikes for imported injectables/fillers | -0.6% | Import-dependent markets in Asia-Pacific & Latin America | Short term (≤ 2 years) |

| Rising counterfeit product infiltration via e-commerce | -0.4% | Emerging economies with high online retail penetration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Approval Complexity Creates Market Access Barriers

The United Kingdom’s pending licensing overhaul illustrates a global push for stricter credentialing, facility standards, and advertising controls that will raise entry barriers and operational costs. In the United States, extended FDA review periods for new dermal fillers add time-to-market risk for manufacturers and delay revenue realization. Europe’s Medical Device Regulation imposes rigorous clinical evidence obligations that smaller firms find onerous, tipping competitive advantage toward well-capitalized incumbents. Collectively, these measures temper the growth trajectory of the cosmetic surgery & services market by slowing product roll-outs and limiting provider expansion.

Safety Concerns and Counterfeit Product Infiltration Threaten Market Confidence

Counterfeit botulinum toxin discovered in e-commerce channels has amplified consumer anxiety and prompted stepped-up enforcement sweeps. Highly publicized complications tied to inadequately supervised medical spas have led regulators to restrict scope-of-practice allowances for non-physician injectors. Recalls such as La Roche-Posay’s benzene-contaminated products demonstrate how quality lapses can erode brand equity across the wider aesthetic ecosystem. Heightened vigilance raises overhead for authenticity programs and insurance premiums, potentially dampening first-time adoption levels within the cosmetic surgery & services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Procedure Type: Surgical Dominance Faces Non-Surgical Disruption

Surgical interventions retained a 57.92% cosmetic surgery & services market share in 2025, buoyed by reimbursement support for reconstructive indications and relatively durable outcomes. Yet non-surgical categories are accelerating at 7.28% CAGR, propelled by injectables and energy devices that deliver quasi-surgical results without general anesthesia or extended downtime.

Eyelid surgery and liposuction remain top surgical procedures, but slowing breast augmentation volumes hint at a patient shift toward less invasive enhancement. Conversely, botulinum toxin surpassed 7.9 million sessions and hyaluronic acid fillers reached 6.3 million injections, underlining the momentum that is re-shaping the cosmetic surgery & services market size calculus in favor of quick-turn treatments with subscription-style repeat rates.

By Gender: Male Demographic Emerges as High-Growth Opportunity

Female patients continued to anchor demand at 68.05% of the cosmetic surgery & services market size in 2025. Male participation, however, is climbing with a projected 6.88% CAGR to 2031 as evolving workplace culture normalizes appearance investment among men.

Hair transplantation commands the largest male volume, yet uptake of neurotoxins, fillers, and jawline contouring solutions is expanding as product messaging pivots toward discreet, masculine outcomes. Clinics are retraining staff on male facial anatomy and marketing through professional networking channels to seize this incremental share of the cosmetic surgery & services market.

By Age Group: Younger Demographics Drive Preventive Treatment Adoption

Consumers aged 35-50 accounted for 48.01% of procedures, supported by peak disposable income and established aesthetic routines. The 18-34 segment shows higher velocity, growing at 7.19% CAGR as “prejuvenation” mindsets spur earlier entry into treatment cycles.

Millennial and Gen Z patients prioritize subtle, cumulative improvements aligned with social-media-visible recovery timelines, reinforcing demand for injectables and low-energy resurfacing. This shift is lengthening lifetime revenue per patient and expanding the prospective funnel for providers across the cosmetic surgery & services market.

By End User: Medical Spas Capture Market Share Through Accessibility

Hospitals & specialty clinics held 54.68% cosmetic surgery & services market share in 2025, fueled by broad procedure portfolios and robust safety infrastructure. Medical spas, though, are pacing at an 7.86% CAGR, leveraging relaxed atmospheres, consumer-friendly branding, and digital booking convenience.

Private equity investors are aggregating regional spa chains to create standardized experiences and scale marketing spend, a model expected to accelerate penetration in suburban and tier-two urban centers. These developments diversify service channels and reinforce volume growth within the cosmetic surgery & services market.

By Body Area: Facial Treatments Lead While Body Procedures Show Strong Growth

Face & head procedures captured 61.72% of revenue, reflecting high visibility and continuous product innovation that keeps patients engaged in maintenance regimens. Body & extremities treatments, benefiting from GLP-1-induced weight-loss aftercare, are rising at an 7.71% CAGR.

Technology cross-pollination from facial to body platforms—such as radiofrequency microneedling for abdominal skin tightening—is expanding total addressable sessions. Providers now bundle facial and body services, increasing average transaction values and deepening the cosmetic surgery & services market size potential per patient.

Geography Analysis

North America retained 42.13% share of the cosmetic surgery & services market in 2025 on the back of 6.2 million total procedures and payer support for select reconstructive cases. Clinical research density and a sophisticated regulatory environment stimulate early adoption of advanced devices and injectables, sustaining premium pricing.

Europe presents a fragmented yet significant opportunity set, with Western markets like Germany and France combining stable procedure volumes and growing medical tourism. Upcoming U.K. licensing reforms are poised to elevate operator quality while pressuring under-capitalized clinics. Eastern Europe offers above-average growth as disposable incomes rise and cross-border procedure packages become more accessible.

Asia-Pacific posts the fastest 6.18% CAGR, driven by China’s double-digit expansion, Japan’s high acceptance of non-surgical treatments, and South Korea’s status as a global hub for aesthetic innovation. Domestic device manufacturing advantages reduce input costs, facilitating aggressive price competition and broadening access. Australia’s new safety standards are projected to heighten consumer confidence and fortify the cosmetic surgery & services market in Oceania.

South America and the Middle East & Africa are emerging growth engines. Brazil’s 2.4 million surgical procedures affirm deep cultural affinity for aesthetic enhancement, while stricter cosmetics registration protocols are improving supply-chain transparency. Gulf economies leverage medical tourism corridors and high per-capita income, although geopolitical uncertainty tempers near-term investment appetites.

Competitive Landscape

Market concentration is moderate. AbbVie’s Allergan Aesthetics, Galderma, and Merz collectively anchor broad portfolios that span neurotoxins, fillers, and energy devices, enabling cross-category bundling strategies[3]The Aesthetic Society News Bureau, “Quarterly Market Insights 2025,” theaestheticsociety.org. Private equity-backed roll-ups are forming multi-location platforms that negotiate favorable supplier contracts and deploy unified electronic health record systems to standardize outcomes.

Technology investment is a central differentiator. Leading groups are piloting AI-driven outcome simulators that elevate consult-to-conversion ratios, while robotic injectors aim to reduce practitioner variability and malpractice exposure. Male-focused product lines, regenerative adjuncts, and combination therapy packages represent white-space segments receiving heightened R&D attention.

Emerging disruptors include tele-esthetic platforms offering remote consultations and at-home energy devices. However, regulatory hurdles around FDA clearance and practitioner licensing create a moat that favors entities with established compliance infrastructures. The cosmetic surgery & services market therefore balances innovation velocity against safety-driven governance, shaping a competitive field where capital depth and technology acumen dictate share gains.

Cosmetic Surgery And Services Industry Leaders

Bausch Health Companies Inc.

Johnson and Johnson

AbbVie Inc.

Galderma SA

Merz Pharma GmbH & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: FDA clears Evolysse hyaluronic acid fillers for nasolabial fold treatment, enriching practitioner choice and intensifying price competition in the mid-face segment

- March 2025: XWELL commits USD 4 million to acquire U.S. medical spas, underscoring investor conviction in scalable, wellness-oriented delivery models

- December 2024: Lorena Investments acquires sk:n clinics and The Harley Medical Group, intensifying U.K. clinic consolidation

Global Cosmetic Surgery And Services Market Report Scope

Cosmetic plastic surgery includes surgical and non-surgical procedures that enhance and reshape structures of the body to improve appearance and confidence. Since it is elective, cosmetic surgery is usually not covered by health insurance. The cosmetic surgery and services market is segmented by treatment type (surgical (Breast Augmentation, Liposuction, Tummy Tuck, Eyelid Surgery, Breast Lift), and non-surgical (Botulinum toxin, Dermal Fillers, Laser Hair Removal, Photo-rejuvenation, Microdermabrasion)) and geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The Market Report Also Covers the Estimated Market Sizes and Trends for 17 Countries Across Major Regions Globally. The report offers the value in USD million for the above segments.

| Surgical |

| Non-surgical |

| Female |

| Male |

| 18-34 years |

| 35-50 years |

| 51 years and above |

| Hospitals & Specialty Clinics |

| Ambulatory Surgical Centres |

| Medical Spas / Aesthetic Clinics |

| Face & Head |

| Breast |

| Body & Extremities |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Procedure Type | Surgical | |

| Non-surgical | ||

| By Gender | Female | |

| Male | ||

| By Age Group | 18-34 years | |

| 35-50 years | ||

| 51 years and above | ||

| By End User | Hospitals & Specialty Clinics | |

| Ambulatory Surgical Centres | ||

| Medical Spas / Aesthetic Clinics | ||

| By Body Area | Face & Head | |

| Breast | ||

| Body & Extremities | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the cosmetic surgery & services market in 2026?

It is valued at USD 102.49 billion and is projected to grow at a 5.43% CAGR to reach USD 133.52 billion by 2031.

Which procedure category is expanding the fastest?

Non-surgical treatments, including injectables and energy-based devices, are rising at a 7.28% CAGR.

Which region shows the highest growth momentum?

Asia-Pacific leads growth with a projected 6.18% CAGR, fueled by rising incomes and evolving cultural norms.

What demographic group is driving new demand?

The 18-34 age segment is growing at 7.19% CAGR as preventive ÒprejuvenationÓ gains popularity.

How are GLP-1 weight-loss drugs influencing demand?

Rapid weight-loss side effects are spurring a 50% increase in fat-grafting and related contouring procedures.

What is the main regulatory challenge providers face?

Stricter licensing and product approval requirements, particularly in the U.K. and EU, are raising compliance costs and delaying market entry.

Page last updated on: